Sample Category Title

EUR Better Bid Ahead Of ECB Meeting

Cautious Fed sends USD lower

As broadly expected the Federal Reserve increased rates by another 25bps and adopted a cautious approach during its June meeting. After spending most of Wednesday grinding lower, the greenback appreciated sharply in the minutes before the announcement but erased those gains immediately as investors realised nothing has changed. It is true that the statement underwent significant change as the FOMC removed the 'forward guidance' part, which was a remainder of the financial crisis.

Regarding the dots plot, it didn't change much as well. Fed members continue to signal two more rate hikes for 2018, most likely in September and December. Nevertheless, he said that interest rate decisions are not on autopilot and can adapt to unexpected development of the economy, which gives the Fed flexibility to stay sidelined should the economy need a breather.

Powell carefully avoided mentioning the trade war initiated by Donald Trump, even though it could have significant consequences for the US economy and recalled that trade policy is not part of the Fed mandate.

In the FX market, the buck is losing ground against all its G10 peers, with the exception of the Australian dollar that is suffering from trade war uncertainties and weak Chinese data. With the Fed is already in the rear view mirror, investors are impatiently awaiting this afternoon ECB meeting.

ECB focuses on 'normalization'

Today's European Central Bank meeting is critical. ECB board members have been quiet on normalization, so it should provide insight into the minds of Draghi & Co for any quantitative-easing tapering or interest hikes. Last quarter's decelerating European growth will hurt the GDP outlook. Weak prices are sending core inflation back towards cycle lows. ECB's corporate line is that risks are transitional and balanced. But given the soft-patch, no one would be confused by an ECB pause in hawkishness. With economic worries haunting, the risk is increasing that an anticipated June or July decision of tapering might be delayed.

Meanwhile, political risk and hype is building in Italy, Spain and Greece, which might change the ECB's mind. The recent, sharp rise in interest rates on the periphery suggests tighter finances for the region's weaker nations. However, the threat of a shock will only strengthen the ECB's desire to get policy off the bottom, because it has few options to manage a crisis. Rates are already negative and bond buying is running into supply shortages. As with the US Federal Reserve in 2013, the need to remove extreme policy, to regain policy firepower, outweighs temporary economic weakness. Given the weakness in EUR/USD, the market is underpricing ECB's commitment to 'normalization.'

Euro Could Crumble If ECB Disappoints, Gold Shines

The Euro has extended gains against the Dollar today, ahead of what could be considered as one of the European Central Bank’s most significant policy meetings this year.

Although the ECB is widely expected to keep monetary policy unchanged in June, investors are likely to be more concerned with the latesteconomic growth and inflation forecasts. Expectations remain somewhat elevated over the ECB potentially signalling an end to QE at the meeting. While hawkish comments from ECB officials and accelerating inflation have fueled speculation over QE coming to an end, this could be a classic case where markets may be setting themselves up for disappointment. With economic growth in the Eurozone slowing in recent months and lingering political risk in Italy weighing on sentiment, Mario Draghi may be hesitant to reveal a QE end-date. This possible reluctance may leave investors empty-handed and ultimately expose the Euro to heavy losses.

Withregards to the technical picture, the EURUSD is starting to look bullish on the daily charts. Prices are trading above the daily 20 Simple Moving Average while the MACD is in the process of crossing to the upside. A solid daily close above the 1.1820 level could encourage an incline higher towards 1.1890. Alternatively, if the 1.1820 proves a stubborn resistance, then prices may descend back towards 1.1750.

Commodity spotlight – Gold

Gold prices have staged a solid rebound despite the Federal Reserve raising US interest rates by 25 basis points yesterday evening.

There is a suspicion that the yellow metal’s appreciation could be offthe back of Dollar weakness. With investors simply engaging in a bout of profit-taking on the Greenback following the US interest rate increase, Gold could appreciate further in the short term. However, Gold’s gains are likely to remain limited by heightened expectations over two more US interest rate increases this year.

Taking a look at the technical picture, the decisive breakout above the $1300 psychological level could invite an incline higher towards $1324.

Focus On ECB And QE Exit Guidance, UK Retail Sales Surge In May Aided By Decent Weather And Royal...

Notes/Observations

- UK May retail sales handily beat expectations (aided by good weather and royal wedding)

- Markets seemed poised for a hawkish ECB, Discussion on QE with final decision seen at the July Council meeting. ECB should provide some clarity on the ‘technicals’ of exiting from QE

- Central bank measures to reduce liquidity might present a summer of de-correlation among asset classes

Asia:

- Australia May Employment Change: +12.0K v +19.0Ke; Unemployment Rate: 5.4% v 5.5%e

- China May Retail Sales registers its slowest pace since Jun 2003 (YoY: 8.5% v 9.6%e). Attributed to seasonal factors and delayed consumption

- China May Industrial Production YoY: 6.8% v 7.0%e

- China Stats Bureau: China’s economy maintained a steady and improving trend in May, to maintain relatively sound momentum in H2 and confident that China’s economy to grow around 6.5% target this year

- Japan PM Abe considering summit with N. Korea Kim Aug/Sept

Europe:

- UK Parliament voted 327-126 to reject House of Lords plan to make staying in European Economic Area (EEA) a negotiating objective ( backs Govt)

Americas:

- President Trump to meet with trade advisers on Thursday (Jun 14th) to decide whether to go ahead with China tariffs

- White House, Commerce and Treasury officials said to have met with Trump before recent G7 and agreed that US should move ahead with tariffs on China. Measures could be levied as soon as Friday, Jun 15th

- FOMC updated Economic Forecasts now saw now forecasts 4 rate hikes in 2018; Raised Median forecast for end-2018 rate 2.375% (prior 2.125%). Dropped its reference it expected rates to be below neutral rate for “some time”. Fed Chair stated that intended to hold press conferences following each meeting from Jan 2019

Economic Data:

- (NL) Netherlands Apr Trade Balance: €3.8B v €5.7B prior

- (DE) Germany May Final CPI M/M: 0.5% v 0.5%e; Y/Y: 2.2% v 2.2%e

- (DE) Germany May Final CPI EU Harmonized M/M: 0.6% v 0.6%e; Y/Y: 2.2% v 2.2%e

- (SE) Sweden May PES Unemployment Rate: 3.5% v 3.6% prior

- (FI) Finland May CPI M/M: 0.1% v 0.2% prior; Y/Y: 1.0% v 0.8% prior - (IN) India May Wholesale Prices (WPI) Y/Y: 4.4% v 4.0%e

- (FR) France May Final CPI M/M: 0.4% v 0.4%e; Y/Y: 2.0% v 2.0%e; CPI Ex-Tobacco Index: 103.06 v 103.00e

- (FR) France May Final CPI EU Harmonized M/M: 0.5% v 0.4%e; Y/Y: 2.3% v 2.3%e

- (SE) Sweden May CPI M/M: 0.2% v 0.2%e; Y/Y: 1.9% v 1.9%e; CPI Level: # v 327.91e

- (SE) Sweden May CPIF M/M: 0.3% v 0.2%e; Y/Y: 2.1% v 2.1%e

- (PL) Poland May Final CPI M/M: 0.2% v 0.1% prelim; Y/Y: 1.7% v 1.7% prelim

- (UK) May Retail Sales Ex Auto Fuel M/M: 1.3% v 0.3%e; Y/Y: 4.4% v 2.5%e

- (UK) May Retail Sales (Includes Auto Fuel) M/M: 1.3% v 0.5%e; Y/Y: 3.9% v 2.4%e

- 04:30 (HK) Hong Kong Q1 Industrial Production Y/Y: 1.1% v 0.8% prior

- (HK) Hong Kong Q1 PPI Y/Y: 3.8% v 3.5% prior

- (GR) Greece Q1 Unemployment Rate: 21.2% v 21.2% prior

Fixed Income Issuance:

- (IE) Ireland Debt Agency (NTMA) sold €500M vs. €500M indicated in 12-month bills; Avg yield -0.46% v -0.53% prior; Bid-to-cover: 2.28x v 2.88x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 % at 3,466, FTSE -0.7% at 7,652, DAX -0.3% at 12,845, CAC-40 -0.4% at 5,432; IBEX-35 -0.2% at 9,878, FTSE MIB -0.6% at 22,052, SMI -0.7% at 8,571 , S&P 500 Futures flat]

- Market Focal Points/Key Themes: European markets open lower across the board; yesterday's rate decision by the Fed weighing on market optimism; materials stocks biggest losers at open; energy stocks supported; Turkey closed for holiday; Mediaset impacted while Sky bolstered after latter wins Serie A transmission rights; upcoming earnings expected in the US session include Micheals companies, Destination Maternity and Fred's

Equities

- Consumer discretionary: PZ Cussons PZC.UK -6.4% (Trading update), Gerry Webber GWI1.DE -5.0% (Earnings, outlook), Revolution Bars RBG.UK -11.2% (Earnings)

- Energy: NWF Group NWF.UK +5.8% (Outlook)

- Industrials: Rolls Royce RR.UK +2.9% (Restructuring plan), Volkswagen VOW3.DE -0.4% (EU fine)

- Materials: Aperam APAM.NL -3.7% (analyst action)

- Technology: Soitec SOI.FR -5.3% (results

Speaker

- EU's Dombrovskis noted the ongoing efforts for an agreement on Greece at the next Eurogroup meeting

- ESM chief Regling: Greece access to markets remained fragile (**Reminder: On Jun 6th reports circulated that Greece delayed a planned bond sale due to concerns about instability in Italy)

- Greece Alternate Fin Min Chouliarakis stated that the govt would meet all prior actions in time. Refuted press speculation that it had postpone a planned bond issuance

- UK Brexit Secretary Davis stated that he had productive and positive talks with EU's Barnier

- UK Brexit Min Baker: Increasingly confident that a good Brexit agreement could be achieved

- Moody's affirms Australia sovereign rating at Aaa, outlook stable

- China PBoC Vice Gov Pan Gongsheng: To increase market role in CNY currency (Yuan) rate mechanism. To increase transparency of Yuan fixing

- China PBoC Research Dir Xu Zhong: Room to use monetary policy was very limited

- China Foreign Ministry spokesperson Geng Shuang: Trade talk progress would be lost if US went ahead and implemented tariffs

- Russia Energy Min Novak: Saudi and Russia shared the view that OPEC/Non-Opec oil production should gradually recover; timing and volumes of any increase were still under discussion

Currencies

- USD was softer in the post FOMC decision environment despite hawkish tone from the Fed. Some analysts believe the were increasing signs that the USD had peaked for now.

- Markets seemed poised for a hawkish ECB with a discussion on QE expected at today meeting with final decision seen at the July Council meeting. EUR/USD by holding above the 1.18 level as markets prepared for the signal of ECB policy normalization. EUR/USD higher by 0.2% at 1.1820 area just ahead of the NY morning.

- GBP/USD jumped 0.5% to test 1.3440 after better-than-expected retail sales data for May. Several parliamentary victories for PM May and her Brexit strategy putting some of the political headwinds aside for now.

- USD/JPY softer by 0.3% and back below the 110 handle.

Fixed Income

- Bund Futures trade at 159.76, down 31 ticks ahead of today's ECB rate decision. Continued downside sees 159.55 followed by potential support at 159.37, with a firm break of 160 targeting 160.22 then 160.44.

- Gilt futures trade at 121.94 down 22 ticks on the back of a stronger retail sales number. Continued downside targets 121.73 then 121.33, while a move above 122.25 targets 122.50.

- Thursday’s liquidity report showed Wednesday’s excess liquidity fell from €1.905T to €1.903T. Use of the marginal lending facility increased from €43M to €99M.

- Corporate issuance saw a quiet day with no new primary issues.

Looking Ahead

- (PE) Peru Apr Economic Activity Index (monthly GDP) Y/Y: 6.2%e v 3.9% prior

- (PE) Peru May Unemployment Rate: 7.1%e v 7.3% prior

- 05:30 (ZA) South Africa Apr Total Mining Production M/M: -0.4%e v -3.4% prior; Y/Y: -3.6%e v -8.4% prior, Gold Production Y/Y: No est v -18.0% prior, Platinum Production Y/Y: No est v -6.1% prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 12-month Bills

- 06:00 (IL) Israel Q1 Current Account: No est v $2.6B prior

- 06:00 (RO) Romania to sell Bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Jun FGV Inflation IGP-10 M/M: 1.8%e v 1.1% prior

- 07:45 (EU) European Central Bank (ECB) Interest Rate Decision: Expected to leave Main Refinancing Rate unchanged at 0.00%

- 08:00 (BR) Brazil Apr IBGE Services Sector Volume Y/Y: +1.3%e v -0.8% prior

- 08:00 (SE) Sweden PM Lofven Q&A in Parliament

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) May Advance Retail Sales M/M: 0.4%e v 0.2% prior (revised from 0.3%); Retail Sales Ex Auto M/M: 0.5%e v 0.3% prior, Retail Sales Ex Auto and Gas: 0.4%e v 0.3% prior, Retail Sales Control Group: 0.4%e v 0.4% prior

- 08:30 (US) Initial Jobless Claims: 222Ke v 222K prior; Continuing Claims: 1.73Me v 1.741M prior

- 08:30 (US) May Import Price Index M/M: 0.5%e v 0.3% prior; Y/Y: 3.9%e v 3.3% prior; Import Price Index ex Petroleum M/M: 0.2%e v 0.1% prior

- 08:30 (US) May Export Price Index M/M: 0.3%e v 0.6% prior; Y/Y: No est v 3.8% prior

- 08:30 (CA) Canada Apr New Housing Price Index M/M: 0.0%e v 0.0% prior; Y/Y: 1.7%e v 2.4% prior

- 08:30 (US) Weekly USDA Net Export Sales

- 08:30 Draghi post rate decision press conference

- 08:30 (EU) ECB updates staff forecasts

- 09:00 (RU) Russia Gold and Forex Reserve w/e Jun 8th: No est v $458.5B prior

- 10:00 (US) Apr Business Inventories: 0.3%e v 0.0% prior

- 10:00 (NO) Norway Central Bank (Norges) Dep Gov Matsen

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (US) Treasury announcement on upcoming 30-year TIPS auction

- 12:00 (CA) Canada to sell 30-year Inflation-linked bonds

- 15:00 (AR) Argentina May National CPI M/M: 2.5%e v 2.7% prior; Y/Y: No est v 25.5% prior

- (JP) Bank of Japan (BOJ) Interest Rate Decision: Expected to leave Interest Rate on Excess Reserves (IOER) Unchanged at -0.10%

ECB Eyed After Fed Raises Rates

European markets are trading slightly in the red on Thursday, while US futures are relatively flat ahead of the open, as we await the ECB monetary policy decision.

The ECB announcement follows the Federal Reserve’s decision on Wednesday to raise interest rates and signal that two more will follow this year in a slightly hawkish shift from the last meeting. While four rate hikes this year won’t come as a major surprise to anyone, it was an interesting shift from the central bank given its hesitance to do so previously and the global concerns over a trade war.

While the Fed has shown a willingness to tolerate above target inflation, the uptick we have continued to see has clearly been a key influence in its decision to signal a fourth hike this year. There will naturally be some concern among investors about the potential negative impacts that tightening too fast will have which may have contributed to the slight decline we’ve seen in equities but generally, they do appear comfortable with them.

The ECB on the other hand is likely to be far more cautious in its approach to tightening monetary policy. This has been evident by its insistence that the winding down of quantitative easing is not tapering, clearly an attempt to disassociate itself with the taper tantrum the Fed experienced when it was going through the same process.

Today we should get some insight into the ECBs plans for when the current purchases expire in September. While I don’t expect the central bank to commit to anything yet – be it an short extension and reduction or anything else – they may hint at discussions that have been had and the options that are on the table. Naturally, there’ll be plenty of questions in the press conference after on its plans beyond QE but I expect President Mario Draghi to keep his cards relatively close to his chest.

Given the political situation in Europe right now, most notably Italy, and the prospect of a trade war with the US, the ECB will want to be extremely careful with exiting QE and laying the groundwork for a potential rate hike next year. Especially as growth remains modest and inflation well below target.

DAX Dips As Investors Eye ECB Rate Annoucement

The DAX index has posted losses in the Thursday session. Currently, the DAX is at 12,849, down 0.32% since the close on Wednesday. On the release front, German Final CPI climbed 0.5%, a 3-month high. This reading matched the forecast. Later in the day, the ECB winds up its policy meeting and will release a rate statement. On Friday, the eurozone releases Final CPI.

Investors were keeping a close eye on the Federal Reserve on Wednesday. As widely expected, the Federal Reserve raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

Fresh from the Fed’s rate hike, the markets will shift their focus to Frankfurt, where the ECB is holding its policy meeting. Will we see any clues with regard to the ECB’s asset-purchase program? Currently, the bank is purchasing EUR 30 billion/mth, and the scheme is scheduled to wind up in September. The eurozone economy hit some headwinds in the first quarter and the new populist government in Italy could pose a major headache for Brussels. This could mean that the ECB will phase out the stimulus program over several months, rather than turn off the tap completely in September. What is clear is that the ECB board members will conduct a detailed discussion about the fate of the stimulus package at this meeting. If ECB President Mario Draghi discusses any new developments regarding stimulus at his press conference, we could see some volatility from EUR/USD on Thursday.

Euro Edges Higher Ahead Of ECB Meeting

EUR/USD has posted slight gains in the Thursday session. Currently, the pair is trading at 1.1827, up 0.29% on the day. On the release front, German Final CPI climbed 0.5%, a 3-month high. This reading matched the forecast. Later in the day, the ECB winds up its policy meeting and will release a rate statement. In the U.S, consumer spending is expected to improve in May, with Retail Sales expected to rise to 0.4% and Core Retail Sales predicted to rise to 0.5%. Unemployment Claims is expected to tick up to 223 thousand. On Friday, the eurozone releases Final CPI and the US publishes manufacturing and consumer confidence reports.

As widely expected, the Federal Reserve raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

Fresh from the Fed’s rate hike, the markets will shift their focus to Frankfurt, where the ECB is holding its policy meeting. Investors will be looking for any clues with regard to the ECB’s asset-purchase program. Currently, the bank is purchasing EUR 30 billion/mth, and the scheme is scheduled to wind up in September. However, some ECB policymakers want to phase out the program slowly, rather than turn off the tap completely in September. What is clear is that the ECB board members will conduct a detailed discussion about the fate of the stimulus package at this meeting. If ECB President Mario Draghi discusses any new developments regarding stimulus at his press conference, we could see some volatility from EUR/USD on Thursday.

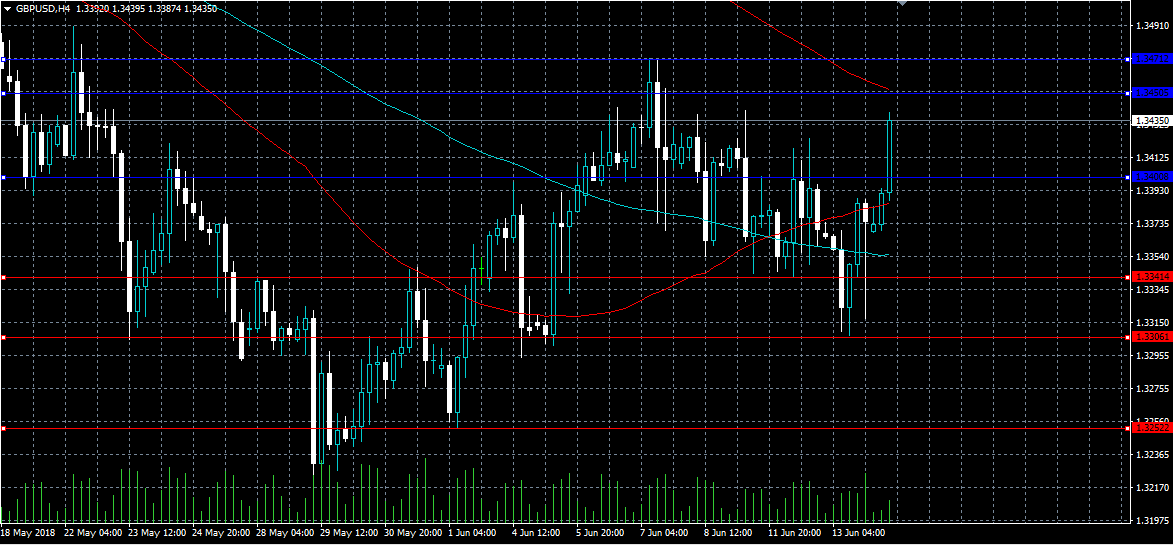

GBPUSD Now Bullish Above 1.3420 Level

The British pound has surged to a fresh weekly trading-high against the US dollar, following the release of much stronger than expected UK Retail Sales Data. The GBP/USD pair currently trades around the 1.3435 level and remains technically bullish while trading above the 1.3420 level. Sterling traders now look towards the release of key US Retail Sales data and the UK Inflation Report Hearing.

The GBPUSD pair is bullish while trading above the 1.3420 level, key technical resistance is located at the 1.3450 and 1.3471 levels.

If the GBPUSD pair fails to move above 1.3420 level, sellers may test back towards the 1.3400 and 1.3341 support regions.

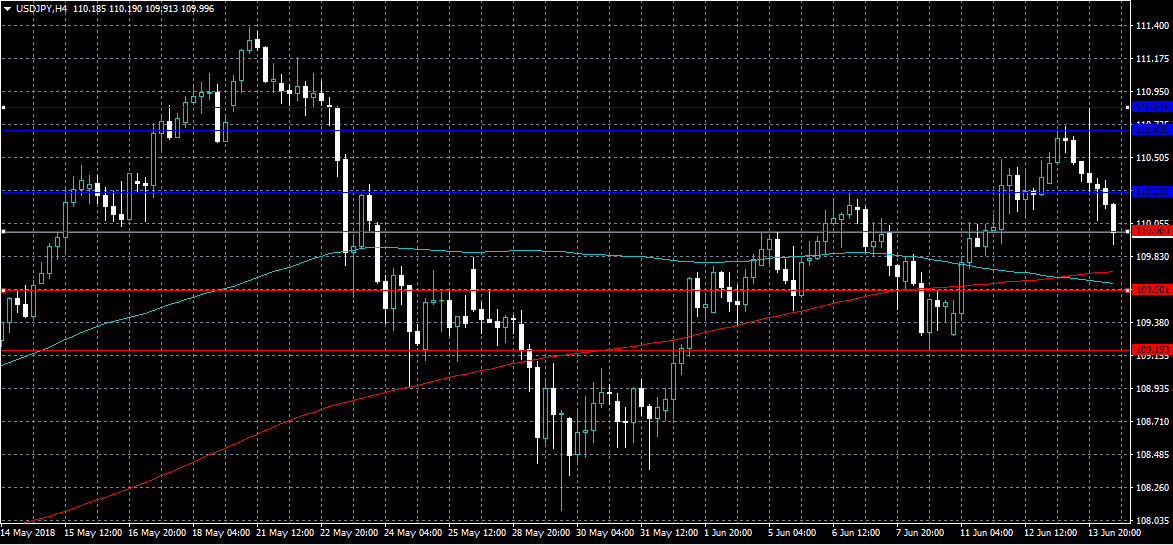

USDJPY Bearish Below 110.26 Level

The US dollar has fallen back towards the 110.00 level against the Japanese yen currency, as the greenback comes under heavy selling pressure. The USDJPY pair is currently testing demand around the 110.00 level, after finding weekly technical resistance from the 110.84 level. Traders now look towards key Retail Sales data from the American economy, and the upcoming Bank of Japan Monetary Policy Decision.

The USDJPY pair is intraday bearish while trading below the 110.26 level, key technical support is now found at the 109.60 and 109.19 levels.

If the USDJPY pair moves above the 110.26 level, buyers may test toward the 110.68 and 110.81 levels.

Forex Analysis: EURAUD

With the ECB meeting today markets are rightly focussed on the EUR crosses. We join EURAUD at an interesting junction with price breaking higher from its trend line resistance yesterday and reaching its 50 and 100 DMAs at 1.56483 resistance today. Depending on the market reaction to the ECB decision and press conference the price may move above resistance and make an attempt to reach the 1.57000 level or even the 1.57691 level which marks the boundary of a resistance band up to 1.58153. A break of this area in the coming days can see price advance further to 1.60000 and the highs around 1.61000.

It should be noted that price is channelling higher on the weekly time frame but the bottom of the channel has not been properly tested and remains around 1.50000. A reaction to the ECB where the price moves lower would focus on 1.55525 as light support with stronger support at the 1.54938 level where the 200 DMA is positioned along with the broken trend line. A loss of this area would see price re-enter the down channel with supports at 1.54147 and 1.53228 followed by 1.52595. A push lower would test the 1.51553 level and the channel bottom at 1.51183.

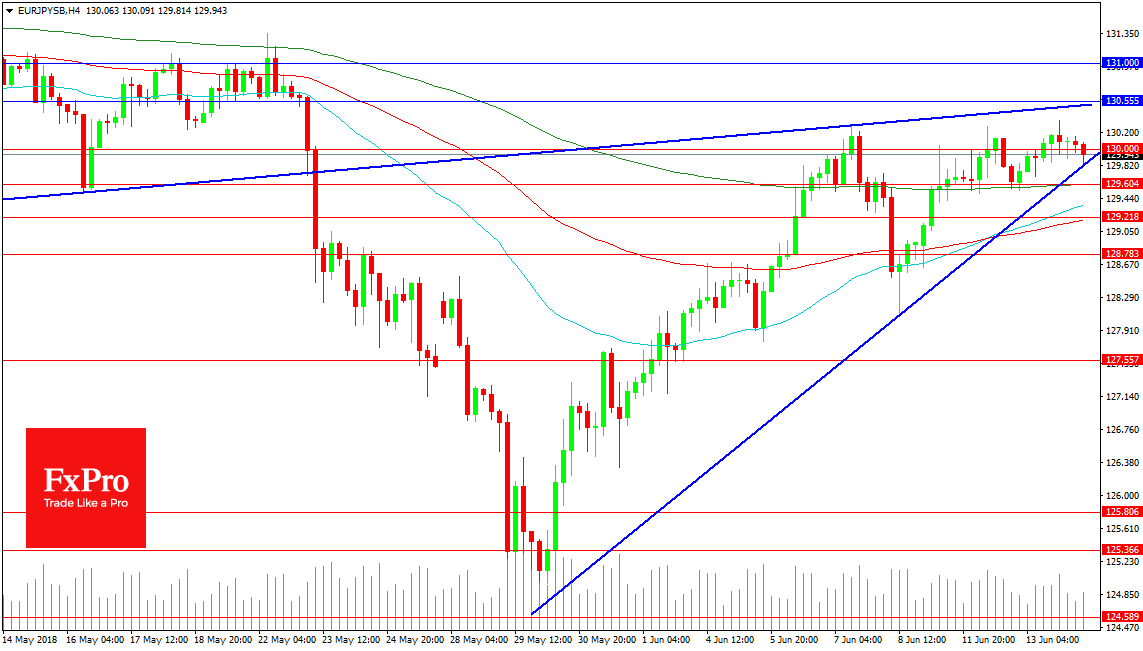

Forex Analysis: EURJPY

This pair has positioned itself between the two trend lines shown around the 130.000 level. It is likely that the ECB decision today will force a breach of the trend lines giving traders and opportunity to interact with the market. Resistance comes in at 130.520 for the trend line with the 131.000 level above. A break above this area is likely to test towards 131.800 where resistance is expected to firm around the 132.000.

Support for the pair has already been used today as the rising trend line at 1.29814 setting the low. A drop under this level could result in a test of the 200 period MA at 129.604 followed by the 50 period MA at 129.354 and the 100 period at 1.29200. Losing these levels opens the way for a bigger move to the higher low at 128.107 and the 127.557 level. A move below this point would result in a price discovery run to see where support lies ahead of 125.800.