Sample Category Title

The Euro Is Circling The Drain

The Euro is circling the drain

Instead of a major roadblock, the ECB was a significant catalyst for the US dollar. And it is tough to argue against the intensity of the EUR downside move as the ECB didn't just disappoint to the dovish side they were overtly dovish pushing back rate hike expectation well into 2019 while revising down their growth outlook. Draghi not only laid it on thick but he applied several layers of heavy-handed coats to his dovish guidance.

The signals from the FOMC and ECB couldn't be more different. The Fed, barring any unexpected financial market calamity, is primed to raise interest rate every quarter while the ECB will continue to sit on their hands well into 2019. These opposing views should see interest rates diverging more between the two most powerful central banks in the US's favour which should continue to lend support to the USD. And should keep the Euro circling the drain well into the summer.

It was a big day for the greenback as the robust US retail sales all but confirmed the Fed hawkish stance from Wednesday. And after back to back the loud retail sales prints, suggesting the trickle-down effect from Trump tax cuts are putting more money in households' pockets, vindicating the Fed for their hawkish view. There is no denying it; the US economy is on a roll.

US equity market

Equity investors took cues from the stronger-than-expected US retail sales and the overtly dovish ECB which saw US stocks closed mostly higher on Thursday. But investors remain very cautious as President Trump is preparing to announce tariffs on Chinese products later tonight, a move that could trigger retaliatory action by China. As it stands right now, the President is unlikely to wrap himself in political correctness as he moves forward with directed tariffs at China.

Oil market

Traders continue to express their bullish and bearish views on Oil which has seen prices test both the upper and lower ends of the near-term ranges as headline risk remain the primary driver of volatility.

But given the signals from Saudi Arabia and Russia that view easing of production limits as inevitable, the market is still is still left wondering how much and when. But suggesting this will be a gradual process has some traders position for the lower end of the 500 K-1.5 m barrel per day increase.

With extremist clashing in Lybia forcing the closure of Es Sider oil export terminal, oil has been testing the upper end of the recent ranges overnight, but again OPEC supply uncertainty is capping gains, particularly against Brent.

Gold market

On a positive signal for gold investors, the precious metal is trading above the critical $ 1300 despite the USD dollar running on overdrive suggesting we may have seen a near-term bottom in prices.

But indeed, with as US-China trade deadline looms ominously, investors continue to view gold as an excellent hedge against a possible equity market tumult if trader wars do escalate beyond the status quo. An escalation of trade war could prove extremely disruptive for financial markets so Gold should hold it bid as we enter another phase of geopolitical uncertainty. Like a nagging backache, there appears to be little relief from protracted trade unease between the US and the rest of the world.

Currency market

While we didn't get the expected reaction from the hawkish Fed, but fortunately history reminded me that is would be folly to dismiss the USD before the ECB.

EUR: While few currency trends move in a straight line, given the apparent widening policy divergence between the ECB and FOMC, the Euro should continue to circle the drain for the foreseeable future as traders are in full out bear mode

JPY: Risk aversion is keeping the top side in check, so G-10 trader are viewing the short EUR and AUD as the quickest road to the bank.

AUD: With the RBA all but hanging their policy hat on the illusive wage inflation, there is little sign that will materialise. And since I've been doing a lot of handicapping this week, I would think an RBA rate hike anytime soon is about as unlikely as McLaren P1 showing up in my garage.

CNH: Yesterday's weaker China economic data dump suggest the Pubco will be in little rush to match the Fed hike, so expect more CNH weakness to ensue. The question is will this interest rate divergence be a threat to capital outflow?

Local EM: Still waiting for the dust to settle on US-China trade before taking a strong view on local currencies. But with the Dollar ratcheting higher vs most of G-10 it would suggest there is Asia FX pain in the making.

Eco Data 6/15/18

[php_everywhere instance="1"]

ECB: Making Plans to Dial Back Policy Accommodation

The ECB will end its quantitative easing program at the end of the year, and the Governing Council anticipates that it will keep rates on hold through the summer of 2019.

QE to End in December, Rates on Hold Through Next Summer

The European Central Bank made some important announcements at its highly anticipated policy meeting today. First, the Governing Council reaffirmed its commitment to purchase €30 billion worth of bonds per month through September. But, as we have been forecasting, the ECB will dial back its asset purchase program to €15 billion worth of bonds per month in October. It also said that it will cease buying bonds altogether after December, assuming that the pace of economic activity and the inflation outlook evolve as the Governing Council generally anticipates.

Second, the Governing Council decided to keep its three main policy rates unchanged at the levels that have been maintained since March 2016 (top chart). Furthermore, the Governing Council said that it anticipates that it will keep its three policy rates at these levels "at least through the summer of 2019." Previously, we had looked for the ECB to hike its deposit rate, which currently stands at -0.40 percent, sometime in the early summer of 2019 while keeping its main refinancing rate (0.00 percent at present) and its marginal lending facility rate (0.25 percent) unchanged. We then looked for the ECB to hike all three rates in late summer 2019.

We take the Governing Council at its word regarding its commitment to keep rates unchanged through the summer of 2019. Consequently, we need to make some tweaks to our forecast for ECB policy rates. We have pushed back our forecast for the first move in the deposit rate from Q2-2019 to Q3-2019. Specifically, we look for the Governing Council to lift its deposit rate from -0.40 percent to -0.20 late in Q3-2019 while keeping its main refinancing rate and its and its marginal lending facility rate unchanged at 0.00 percent and 0.25 percent, respectively. We then look for it to hike its deposit rate to 0.00 percent, its main refinancing rate to 0.25 percent, and its marginal lending facility rate to 0.50 percent sometime late in Q4-2019.

What could alter our forecast of ECB policy? Simply, changes to our macroeconomic forecasts. After strengthening throughout 2017, real GDP growth in the Eurozone slowed in Q1-2018 (middle chart). In our view, the slowdown in the first quarter was just a temporary soft patch, and we look for the expansion to remain intact for the foreseeable future. But if growth were to remain sluggish, then we would need to rethink our outlook for eventual ECB rate hikes.

Furthermore, there are few inflationary pressures in the euro area at present. Although the overall CPI inflation rate jumped up to 1.9 percent in May, the core rate of inflation remains depressed at roughly 1 percent (bottom chart). If the core rate of inflation remains well below the ECB's target of "below, but close to, 2 percent over the medium term" then the Governing Council may keep the policy rate unchanged for even longer than we now anticipate.

British Pound Dips Despite Sharp Retail Sales

The British pound has posted losses in the Thursday session. In North American trade, GBP/USD is trading at 1.3328, down 0.36% on the day. On the release front, retail sales sparkled on both sides of the pond. British retail sales jumped 1.3%, crushing the estimate of 0.5%. In the U.S, core retail sales climbed 0.9%, its strongest gain since November. This easily beat the forecast of 0.5%. It was a similar story for retail sales, which improved 0.8%, above the forecast of 0.4%. There was more good news from the U.S employment front, as unemployment claims dropped to 218 thousand, below the estimate of 223 thousand.

Consumer spending has looked strong in the second quarter. Retail Sales in May posted a strong gain of 1.3%, after an even stronger gain of 1.6% in April. Both readings easily beat their estimates. An unusually warm May and the Royal Wedding contributed to stronger consumer spending, a key driver of economic growth. Another factor that may have coaxed consumers to spend more is lower inflation, which remained at 2.4% in May.

The markets had priced in a rate hike from the Federal Reserve on Wednesday, and the Fed didn’t disappoint. The central bank raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

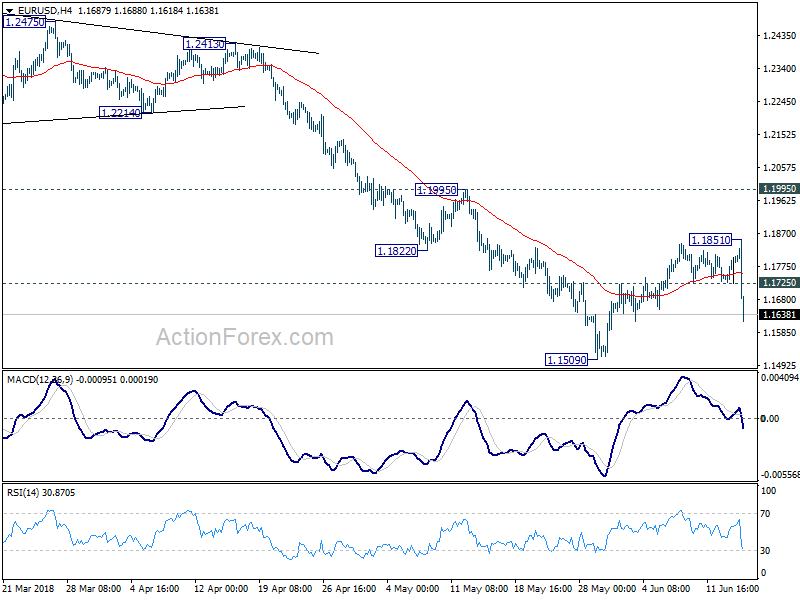

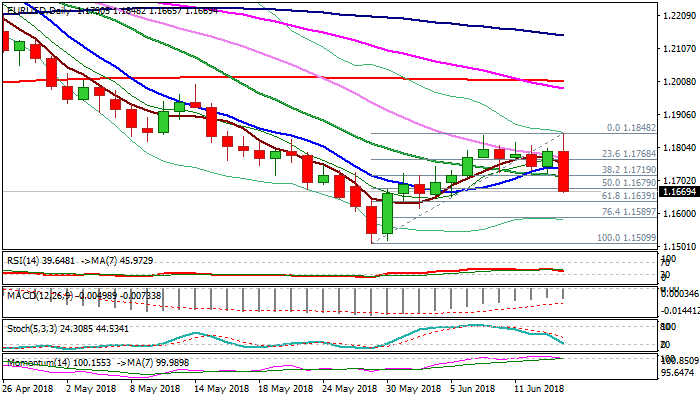

EUR/USD short opportunity for position trading

Let's have a look at EUR/USD follow today's post ECB selloff.

First of all, EUR/USD is clearly in a medium term down trend as seen in W action bias chart. Despite near term rebound from 1.1509, W action bias stayed downside red throughout.

D action bias chart turned neutral after a string of downside red bars. This is consistent with the view that price actions from 1.1509 are corrective in nature. And such corrective rise was indeed relatively weak, without any upside blue bar.

The sharp fall today turned 6H action bias downside red too, with a few persistent red bars in H action bias too.

The development suggests that EUR/USD's down trend is possibly resuming. The main hesitation for us is that D action bias bar hasn't turned red yet. Hence, we'd opt for a safer strategy and sell of recovery to 1.1725 minor resistance, with stop above 1.1851. We're looking at 61.8% retracement of 1.0339 to 1.2555 at 1.1186 as target for position trading.

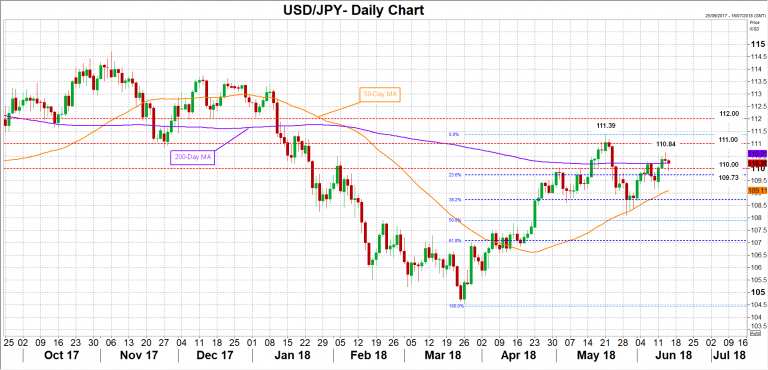

Yen Unchanged ahead of BoJ Rate Announcement

The Japanese yen is unchanged in the Thursday session. In the North American session, USD/JPY is trading at 110.39, up 0.04% on the day. On the release front, Japanese Revised Industrial Production fell to 0.5% but managed to beat the estimate of 0.3%. In the U.S, consumer spending reports were unexpectedly strong. Core Retail Sales climbed 0.9%, its strongest gain since November. This easily beat the forecast of 0.5%. It was a similar story for Retail Sales, which improved 0.8%, above the forecast of 0.4%. There was more good news on the employment front, as unemployment claims dropped to 218 thousand, below the estimate of 223 thousand. Later in the day, the Bank of Japan releases a rate statement, followed by a press conference with BoJ Governor Haruhiko Kuroda.

As widely expected, the Federal Reserve raised interest rates by a quarter-point, to a range between 1.75 percent and 2.00 percent. Fed Chair Jerome Powell sounded hawkish in his press conference, saying that the economy was performing well and that “overall outlook for growth remains favorable”. This message echoed the rate statement, in which policymakers said that “economic activity has been rising at a solid rate”, pointing to stronger consumer spending and business investment. What was may have been the most notable development was that the Fed rate projections were revised upwards, predicting two additional rate hikes in 2018, for a total of four hikes. Until now, the Fed had projected three rate hikes this year. This represents a nod to the strength of the U.S economy and could boost the dollar against its rivals.

The markets aren’t expecting any moves from the BoJ as it winds up its policy meeting on Thursday, as the bank is expected to hold the course with regard to fiscal and interest rate policies. Still, with the economy continuing to expand, the bank is expected to wind up its massive stimulus program. The magic question is when will the BoJ start to taper the program. Economists remain divided – some are forecasting that reductions in stimulus will begin in 2119, with others saying that won’t happen until 2020 or even later. Given the size of the stimulus program, any hints from the bank that it is considering a taper is sure to shake up the yen’s exchange rate. With inflation expected to remain below the BoJ target of around 2 percent for the near future, there isn’t much pressure on the BoJ to alter its current

All agreed inflation will linger well below the central bank’s elusive 2 percent target for some time.

ECB Review: End of APP But Stronger on Rate Guidance

- The ECB announced its formal end to QE in June and not in July as we expected. This said, the announcement was as we expected, with the APP Q4 purchase rate of EUR15bn per month; hence, the bond being bought by the end of the year.

- At the same time, the ECB stepped up its forward guidance on rates and said 'interest rates to remain at their present levels at least through the summer of 2019'. This means that we expect the first 'live' meeting to be in September 2019.

- This does not warrant us changing our call on the first ECB rate hike being by 20bp in December 2019.

The ECB ended its APP as it is more confident on the path of inflation towards the aim. It emphasised that the strength of the economy (growth projection of 2.1% this year, still significantly above potential), well-anchored long-term inflation expectations and 'continued ample degree of monetary accommodation' are grounds to be confident on the path of inflation towards the 2% target, even after winding down QE purchases.

Mario Draghi struck a dovish tone throughout the press conference, in both the introductory statement and the Q&A. Furthermore, there remain a lot of 'ifs' in the statement (i.e. 'state dependency'), making the further reduction of QE in Q4 and first hike timing still dependent on incoming data on economic/inflation developments.

The stronger guidance on rates followed the speech by Benoît Coeuré back in February, when he said that a 'shorter purchase horizon could be combined with stronger rate forward guidance so as to mitigate the risk of investors unduly bringing forward their rate expectations'. With the wording 'the Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019', we pay close attention to 'at least through the summer of 2019'. This suggests the first 'live' meeting will be in September 2019, which makes us confident on our call for December 2019 to be the first rate hike. Draghi further said that the ECB did not discuss raising rates.

On inflation, a very interesting comment on the back of Peter Praet's comments last week was the introductory statement on 'tightening labour markets and rising wages'. The ECB does indeed seem more confident on wage dynamics – and we take note of the increased usage and focus on 'wage' compared with the past five to six years. 'Wage' has been mentioned three times now. Draghi even referred to this data as 'overlooked'.

The ECB also continued to stress the importance of the reinvestment policy as its language on the reinvestment policy was unchanged from last time, i.e. that it will reinvest 'as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation'. Overall, the ECB has become more confident on inflation, albeit there are risks to the growth outlook.

We still think the ECB will continue to be dovish, at least in the near term. Overall, markets took the introductory statement and Q&A as dovish (see intraday chart overleaf).

ECB staff projections

The ECB also released new economic forecasts at the meeting.

- Near-term growth outlook revised down but medium-term outlook still solid: Draghi acknowledged that growth has moderated as of late due to a combination of supply-side constraints and temporary factors but stressed that growth remains solid and broad based and he expects it to remain so over the medium term. Reflecting weaker Q1 growth, the ECB lowered the forecast for 2018 from 2.4% to 2.1%, while it left its projections for 2019 and 2020 unchanged at 1.9% and 1.7%, respectively. Risks to the growth outlook were judged to be broadly balanced but uncertainties related to global factors, including the threat of increased protectionism, have become more prominent, while heightened financial market volatility warrants monitoring.

- More optimistic inflation outlook due to energy prices: The ECB expects headline inflation to hover around the current level (1.9% in May) for the remainder of the year. Draghi stressed that underlying inflation pressures remain subdued but, at the same time, the tightening labour market and rising wages mean the uncertainty on the inflation outlook is receding. Hence, the ECB raised its 2018 and 2019 headline inflation forecast from 1.4% to 1.7%, due mainly to the recent increase in oil prices. The revision was partly also a reflection of higher core inflation projections in 2019 and 2020, also on the back of the ECB's expectations of higher wage growth.

Fixed income

The forward guidance on key interest rates dominated the market reaction in EUR fixed income space despite the announcement of the end of QE. In the press release, the sentence regarding the GC's expectations of unchanged ECB key interest rates 'at least through the summer of 2019' induced a rally in EUR rates. Consequently, marked-based expectations of an ECB hike before or during the summer of 2019 fell significantly.

In contrast to our expectations, the ECB announced an end-date for the APP programme. However, as expected, the outlined taper scheme included a reduced pace of net bond purchases, i.e. down to EUR15bn/month after September 2018 until December 2018, where after the net purchases ends.

Note, in addition to the net bond purchases, expected APP re-investments implied by the estimated redemptions from Oct-18 to Dec-18 also amounts to around EUR45bn. Hence, ECB bond purchases will remain significant also in Q4 18.

In terms of the ECB keeping the front end of the Eonia curve well anchored, the forward guidance on key interest rates will likely keep EUR rates volatilit low and prolong the 'search for yield environment' in EUR fixed income space. We continue to be positioned for a tightening of periphery markets (ex. Italy) spreads vs Germany/swaps. Moreover, even though the QE programme ends in 2018, significant reinvestments will be seen in 2019. The first 5 months PSPP reinvestments will be on average EUR 15.4bn a month.

FX: rate guidance keeps EUR/USD <1.20 for extended period

A short-lived knee-jerk move higher in EUR/USD on the QE end-date announcement but this quickly more than reversed as the rate guidance was crucially reinforced and the press briefing kept the dovish tone. Indeed, for the FX market, we stress that it is the new time-dependent rate guidance that is key for the euro: by keeping rate-hike expectations at bay, this effectively keeps the ECB from luring capital flows back to the eurozone near term – a factor we still believe holds EUR upside potential longer term. Despite some evidence of flows turning less EUR negative recently (see chart), with both the Fed (via hikes and balance-sheet reduction) and the Treasury (via issuance) continually adding to the 'carry appeal' of USD, this underlines that relative rates will weigh on EUR/USD for some time still and avert a move back to the mid-1.20s any time soon. We still look for the recent range (1.17 +/- a few big figures) to hold near term. It is likely we will need to get much closer to the first rate hike, which now cannot take place before September 2019 at the earliest, before seeing a sustained move above the 1.20 mark (our 12M target remains 1.25).

ECB to End QE in December, No Rate Hike At Least Until Summer 2019

ECB's decisions in June came in largely in line with our expectations, although it might have contained surprises for other market participants. The central bank decides to reduce the size of its QE program to 15B euro/ month, from the current 30B euro/ month, from October. The entire purchase would end in December, as we had forecast. The Council also affirmed that interest rates would stay at the current level at least until "summer of 2019". In response to the moderation in growth and uncertainty over US’ trade policy, the staff revised lower GDP growth estimate for this year. Euro tumbled on profit-taking as the market had priced in a QE tapering after Peter Praet speech last week. Another reason for the selloff was the change in the forward guidance of the interest rate path. Although it is a surprise to many market participants, we had suggested that the ECB would signal for how long it would keep the rates at the current levels.

The central bank has announced important changes to its QE program. It would maintain the current monthly pace of 30B euro until the end of September 2018, and then reduce the purchases to 15B euro until the end of December 2018 and that net purchases will then end. After the program is ended, ECB would still maintain the size of the balance sheet by reinvesting the principal payments from maturing securities purchased.

On the policy rate, ECB in June left the main refi rate, the marginal lending rate and the deposit rate at 0%, 0.25% and -0.40% respectively. The Council also announced that it would keep interest rates at “present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path”. Previously, ECB had been reiterating to keep the interest rates “at their present levels for an extended period of time, and well past the horizon of the net asset purchases”. The amendment in the above forward guidance has not only affirmed the market that any potential rate hike would come well after the end of the QE program, but also has given a concrete idea of the appropriate timing of expecting the first rate hike.

On economic projections, the region’s GDP growth is expected to reach +2.1% in 2018, down from March projection of +2.4%, before easing to +1.9% in 2019 and then to +1.7% in 2020. Reflecting the increase in oil price, inflation is expected to reach +1.7% this year and through 2020, compared with March projection of +1.4% for this year and in 2019. Policymakers revised slightly higher the forecast for core inflation by both 2019 and 2020 to +1.6% and +1.9%, respectively.

ECB in Free Fall after ECB Ruled Out Any Rate Hike Till Late 2019 and Kept QE

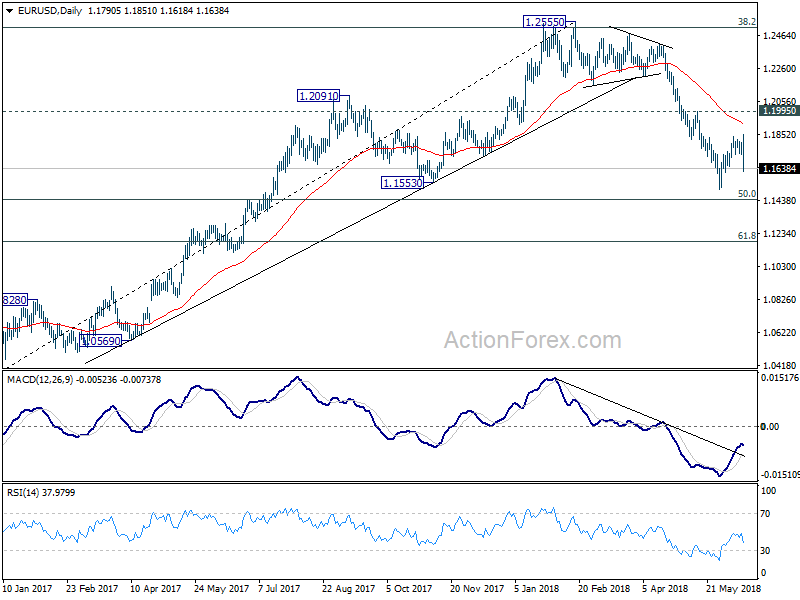

The Euro is in free fall after ECB and chief Draghi's remarks on post policy meeting press conference. The pair so far fell nearly 1.5% since ECB's rate announcement and showing scope for further weakness. Initial negative signal was comment for future rate hikes as the ECB ruled out any rate hike until the second half of 2019. Mario Draghi highlighted solid broad-based growth in the Eurozone and expressed his optimism about underlying inflation, but decision to keep the QE program as significant monetary stimulus is still needed, disappointed traders. My comments two days ago that Euro's rally is positioning for ‘buy the rumor – sell the fact' post ECB action proved to be true. Today's significant fall dented bullish near-term outlook and signals that recovery from 1.1509 low might be over. Double-top that was left at 1.1839/48 is bearish signal as acceleration through a cluster of MA supports, which now reverted to resistances, marked next bearish signal. Bearish acceleration surged through thick 4-hr cloud (spanned between 1.1772 and 1.1674) and currently probing through cloud base, which would generate further bearish signa. Bears need to break and close below 1.1639 (Fibo 61.8% of 1.1509/1.1848 recovery leg) to confirm reversal and expose key support at 1.1509 (29 May low – the lowest since July 2017).

Res: 1.1719; 1.1741; 1.1771; 1.1800

Sup: 1.1639; 1.1616; 1.1589; 1.1509

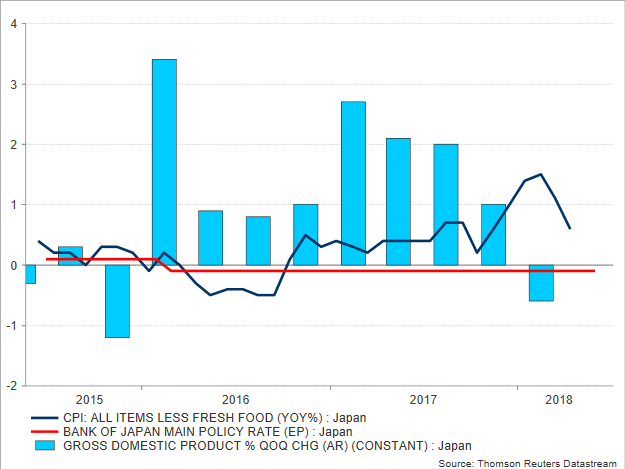

Bank of Japan: Rate Hikes Not Yet in the Cards

The second quarter of the year did not enjoy a good start in Japan, with inflation and business indicators slowing down to warn policymakers that a move from stimulative monetary policies is probably not a good idea this Friday.

Early on Friday at a tentative time, the Bank of Japan will make an announcement on interest rates and deliver its rate decision statement. Policymakers are widely expected to refrain from raising borrowing costs, maintaining short-term interest rates at minus 0.1% and keeping their ultra-easy monetary policy in place. This also includes continuing to buy government bonds in order to hold the yields on 10-year Japanese government bonds around zero percent.

It was late February when markets got optimistic that inflationary pressures in Japan had heated up as the core CPI edged closer towards the BoJ’s price target of 2.0% on an annual basis (though it was still far below that level, at 1% y/y). However, in the next month the measure stalled and in the following months, the gauge reversed to the downside to end up at 0.5% y/y in May, casting doubts on the effectiveness of the BoJ’s policy to drive inflation towards its target. In contrast, average earnings printed the fastest growth in almost four years in March, but April’s reversal proved that the pickup was temporary and not sustainable to boost consumer prices, despite the unemployment rate standing at its lowest since 1993. Moreover, household spending contracted in April for the third consecutive month, while updated GDP growth estimates for the first quarter confirmed a contraction of 0.6% y/y as analysts initially predicted, both flagging that inflation will take longer to reach its goal and therefore a rate hike could move further back in time.

Note that during April’s gathering, the BoJ abandoned its target date of achieving its inflation target by fiscal 2019. The move gives more flexibility to policymakers to avoid pressures for more stimulus in case this deadline, which has been postponed six times since 2013, fails to hold, while at the same time, in the absence of such expectations, the market reaction could be more subdued in the wake of any announcements on inflation. Nevertheless, BoJ Governor Kuroda did not abandon his hopes for inflation touching 2.0% by 2019 as expressed by his comments at the University of Zurich on Monday. Note that the central bank is not scheduled to renew its economic forecasts at this meeting, hence all eyes will turn to the press conference following the rate decision for any clarifications on how policymakers assess the country’s economic outlook.

Turning to forex markets, dollar/yen is heading for a weekly gain, as confidence in the US economy continues to grow. A dovish BoJ for example, which would probably focus on Japan’s recent poor economic releases, could bode well for the greenback, sending the pair up to yesterday’s high of 110.84 before the 111 round level comes into view. Any break above the latter could then retest the previous peak of 111.39, while steeper increases could also open the way towards the 112 psychological mark.

On the other hand, if policymakers use a more optimistic tone instead, expressing confidence in inflation resuming its uptrend, then dollar/yen could reverse to the downside to meet the 110 round level again. Slightly lower, the 23.6% Fibonacci of 109.20 of the upleg from 104.05 to 111.34 could also provide support ahead of the 50-day (simple) moving average at 109.11.