Sample Category Title

US: Retail Sales Surge in May

Retail sales surged 0.8 percent in May after an upwardly revised 0.4 percent in April. Control group sales were up 0.5 percent after an upwardly revised 0.6 percent in April.

Strength Not Only Due To Higher Gasoline Prices

Retail sales surged 0.8 percent in May after an upwardly revised 0.4 percent increase in April. Excluding gasoline stations' sales, retail sales also increased a strong 0.7 percent. Furthermore, if we exclude motor vehicle & parts and gasoline stations' sales, retail sales were up 0.8 percent. The only negative readings in May were furniture & home furnishing stores' sales, down 2.4 percent during the month and sales at sporting goods, hobby, musical instrument, & book stores, which declined 1.1 percent sequentially.

The strongest sectors in May were miscellaneous store retailers' sales, up 2.7 percent, and building material & garden equipment & supplies dealers' sales, up 2.4 percent. Gasoline station sales were up 2.0 percent, mostly due to the increase in the price of gasoline. Meanwhile, sales at general merchandise stores were up 1.2 percent, while department store sales were surprisingly up a strong 1.5 percent after increasing 0.7 percent in April. Another strong sector in May was sales at clothing & clothing accessories stores, which were up 1.3 percent after a strong 1.2 percent reading in April. Non-store retailers' sales were relatively muted, increasing 0.1 percent after a strong 1.5 percent increase in April. Motor vehicle & parts dealers' sales as well as health & personal care stores' sales were up 0.5 percent during the month. Meanwhile, food & beverage stores' sales were flat in May.

However, on the service side of the retail report, food services & drinking places' sales were strong, up 1.3 percent in May after dropping 0.3 percent the previous month. This means that there are also signs that the service side of personal consumption expenditures (PCE) may also be relatively stronger during the second quarter of the year.

Sustaining This Pace Needs Higher Income Growth

Overall, the May retail sales report was very positive for the performance of the U.S. consumer in the second quarter of the year after a disappointing performance during the first quarter. This is clear by looking at the result for control group sales, whose index increased a stronger-than-expected 0.5 percent, while April's increase was revised up from a 0.4 percent increase to a 0.6 percent increase. The recovery in PCE during the second quarter of the year has been front and center for the past several months in the news and this retail sales report is just a confirmation of a very strong recovery by the U.S. consumer expected during the second quarter of the year. The relatively strong print by automobile sales is, perhaps, the realization by the American consumer that higher interest rates are here to stay and they should move ahead of even higher interest rates in the future. However, not all is good news for the U.S. consumer and for the U.S. economy, as we have also seen a slowdown in credit card borrowing, a further decline in the saving rate and much higher gasoline prices. Thus, Americans will need an improvement in income growth in order to continue down this path of growth in retail sales and PCE.

Sunset Market Commentary

Markets:

The ECB changed its forward guidance on the asset purchase program and on interest rates today. The former was widely anticipated, the latter came as a surprise. The monthly pace of asset purchases will drop from €30bn/month to €15bn/month in Q4 2018 after which net asset purchases will end. Progress on inflation has been substantial and the ECB grew confident that inflation convergence towards the 2% aim will be sustained, warranting the tapering of QE. However, an ample degree of monetary policy needs to remain in place to support a further build-up of domestic price pressure. The ECB’s reinvestment policy of maturing bonds from its asset portfolio therefore remains in place for the foreseeable future. The communication on interest rates changed from “remain at current levels for an extended period of time after ending net asset purchases” to “remain at present levels at least through the summer of 2019”. The ECB basically mapped out monetary policy for the next 15 months, suggesting a first rate hike in September 2019. That’s 3 months later than our previous June forecast. We think that this cautious approach is inspired by the growth moderation in Q1, coming from high levels and as the ECB doesn’t want to underplay existing risks to the outlook (trade, protectionism, higher volatility, supply constraints…). Officially, risks to the eco outlook remain broadly balanced. Growth forecasts remained unchanged for 2019 (1.9%) and 2020 (1.7%) for now, but this year’s projection decreased from 2.4% to 2.1%. Inflation forecasts faced an upward revision from 1.4% to 1.7%, both in 2018 and 2019, while the 2020 projection was unchanged at 1.7. Uncertainty over the inflation outlook is receding.

Both European/German interest rates and the euro trended higher ahead of the ECB decision. Investors positioned for the ECB announcing a reduction in policy stimulus. The ECB effectively announced a two-step phasing out of APP, but also committed to keep rates unchanged at least till September 2019. In a first reaction, yields were inclined to rise. EUR/USD briefly jumped to the mid 1.18 area. However, markets soon realized that the new guidance on interest rates ‘guaranteed’ extremely low (official) EMU interest rates at least for the next 15 months. The monetary policy horizon in EMU is more or less cleared for ‘an extended period of time’. German bond yields turned back south. Yields decline between -2.5 bps (30-y) and -3.5 bps (5 y). Intra-EMU-spreads widened substantially in the run-up to the ECB decision, but narrowed sharply after the announcement. The 10-yr yield spread between Italy and Germany is little changed (+3 bps). The euro also made an impressive U-turn. EUR/USD reversed the initial spike higher and the euro decline accelerated throughout the press conference. Draghi indicating that the ECB didn’t underestimate risks (both on the economy and with respect to global uncertainty) probably added to the euro decline. EUR/USD trades currently in the 1.1680 area. US retail sales also printed very strong (0.9% M/M) during the press conference. The report reinforced the slight underperformance of US Treasuries versus Bunds. US yields decline by 0.8 bps (2-y) to 2.0 bps (10-y). Strong US data were also slightly supportive for the dollar. USD/JPY rebounded off the intraday low just below 110 and trades currently again in the 110.35 area. In a more global perspective, yesterday’s Fed decision/trajectory and today’s ECB communication might reduce market volatility again as uncertainty on monetary policy has been reduced sharply.

Brexit moved a bit to the background today as a driver for sterling trading. Attention turned to the May UK retail sales. After a rebound in April, May sales were again strong. Temporary factors (sales related to the Royal wedding, better weather) were at least partially in play. Even so, the report suggests that Q2 growth might be less weak than feared. On the other hand, it is far from sure that this improvement will be enough for the BoE to already fully play the card of an August rate hike. The market implied probability for an August hike hovers around 50%. The gain of sterling after the retail sales report was modest. EUR/GBP dropped temporary below 0.88, but sterling momentum remained sluggish. The post-ECB setback of the euro also weighed on EUR/GBP later in the session. The pair trades currently again in the 0.8775 area. USD strength pushed cable back to the 1.3325 area.

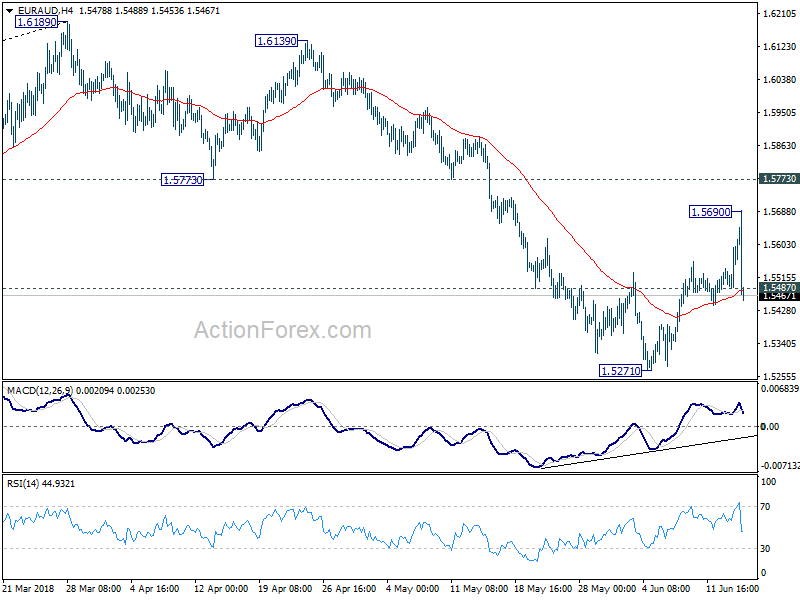

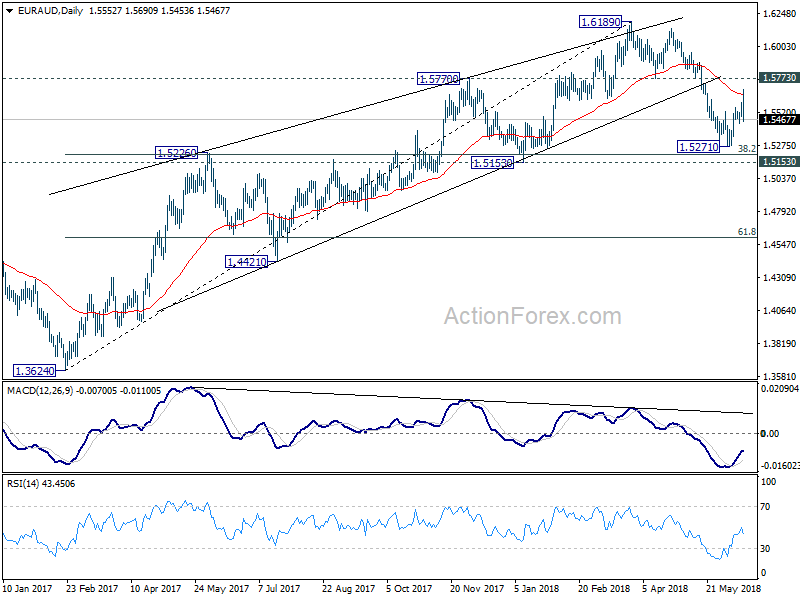

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.5500; (P) 1.5547; (R1) 1.5606; More....

Despite jumping to 1.5690, subsequent sharp fall and break of 1.5487 minor support argues that rebound from 1.5271 has completed already, ahead of 1.5773 support turned resistance as expected. EUR/AUD was limited limited by 55 day EMA. Intraday bias is turned back to the downside for 1.5271 low first. Break there will resume whole fall from 1.6189 to 1.5153 key support next.

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further decline is expected in medium term, even in case of strong rebound.

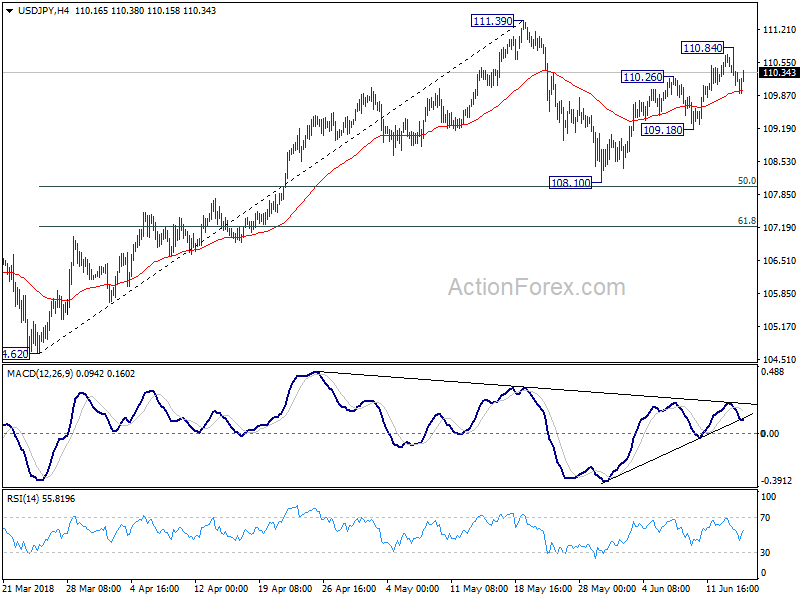

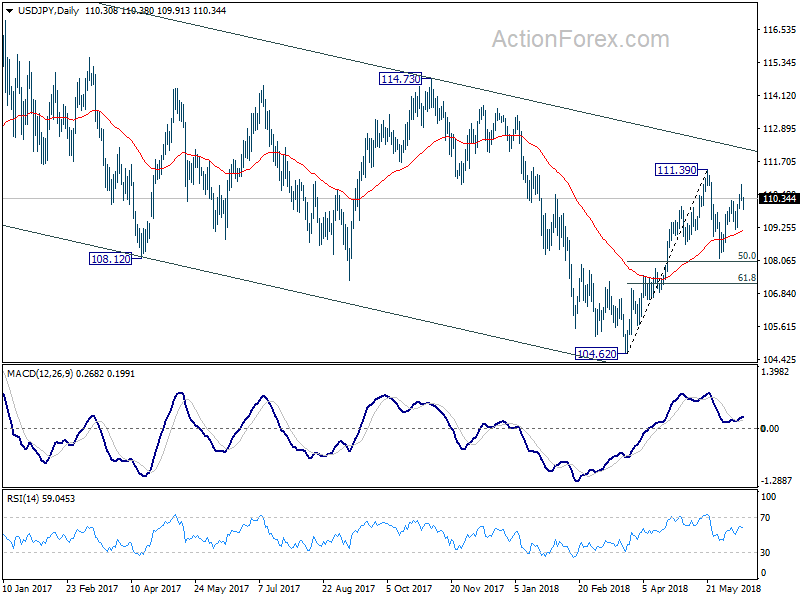

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.12; (P) 110.49; (R1) 110.70; More...

USD/JPY is drawing support from 4 hour 55 EMA but it's bounded in range below 110.84 so far. Intraday bias remains neutral. Overall outlook is unchanged that price actions from 111.39 are developing into a corrective pattern. Below 109.18 will start the third leg to 108.10 and possibly below to complete the pattern. Above 110.84 will bring retest of 111.39 first. Break will resume the whole rebound from 104.62.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

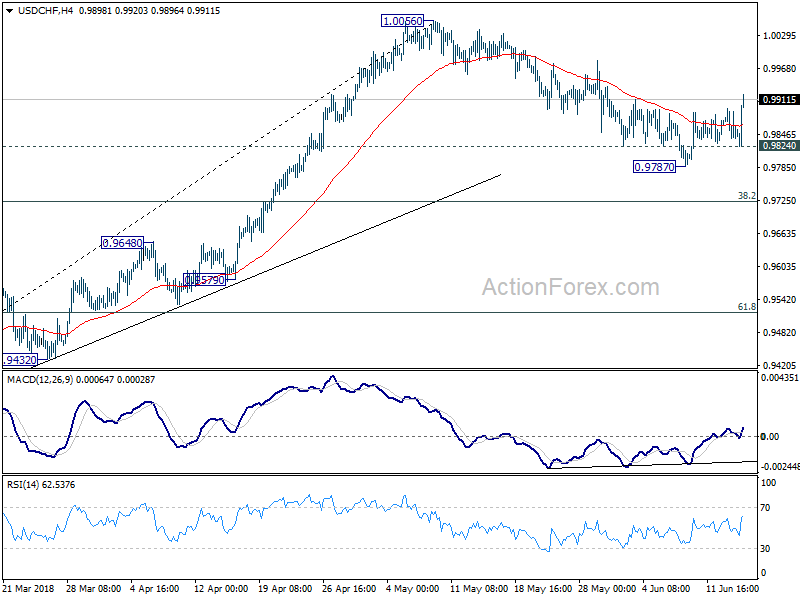

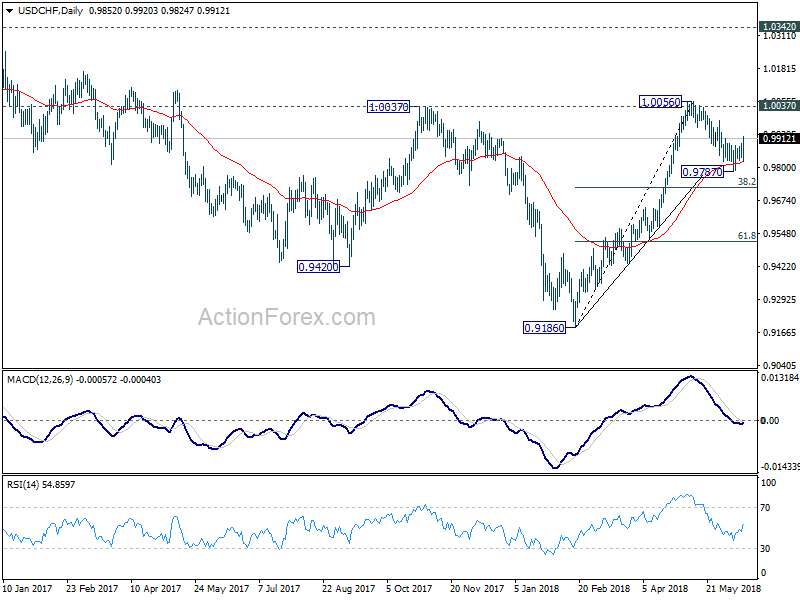

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9832; (P) 0.9863; (R1) 0.9887; More...

USD/CHF's rally and break of 0.9911 minor resistance argues that the correction from 1.0056 has completed at 0.9787 already. Intraday bias is now on the upside for 1.0056 first. Decisive break there will resume the whole rise from 0.9186 and target 1.0342 key resistance next. On the downside, below 0.9824 will extend the correction from 1.0056. But we'd expect strong support from 0.9724 fibonacci level to contain downside and bring rebound.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

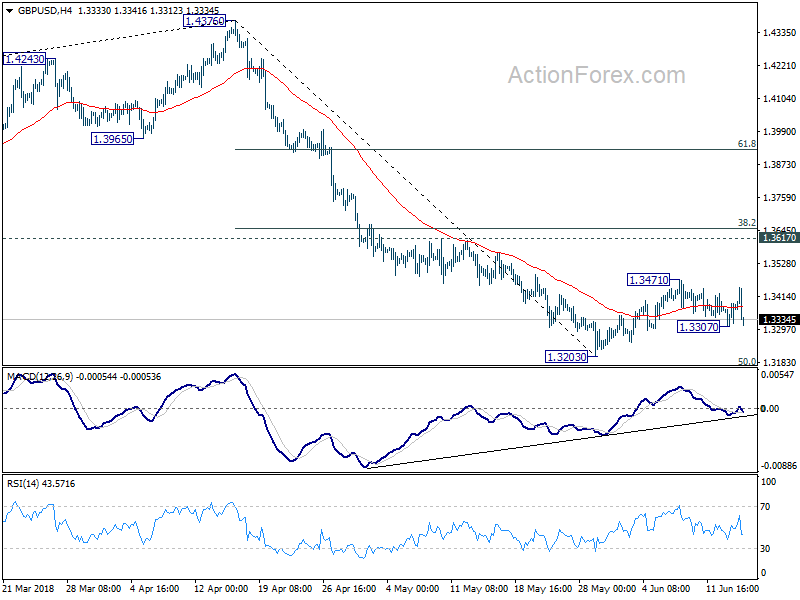

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3323; (P) 1.3362; (R1) 1.3416; More...

GBP/USD rebounded strongly to 1.3446 today but dropped sharply since then. After all, it's bounded in range of 1.3307/3471 and intraday bias remains neutral. On the downside, break of 1.3307 will reaffirm the case that corrective rise from 1.3203 has completed. Retest of 1.3203 should then be seen. Break will resume the fall from 1.4376 to 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next. On the upside, break of 1.3471 will extend the corrective rise. But upside should be limited by 1.3617 resistance to bring fall resumption eventually.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3617 resistance holds, even in case of strong rebound.

US Retail Sales Blow Past Expectations, as Americans Go Back to the Mall

Retail sales surged by 0.8% in May according to the advance Census Bureau report – double the increase expected by Wall Street. Better yet, April's data was revised up a touch – from 0.3% to 0.4%.

Sales at gasoline stations rose 2.0% with auto & parts dealers registering a 0.5% rise. Excluding autos and gas, retail sales were also up 0.8% on the month – again, double expectations.

After two months of declines, spending on building materials surged (+2.4%). Spending at restaurants and bars was also up, but a bit more modest 1.3%, after a slight pullback in April.

Excluding gas, autos, building materials, and food services, the so-called 'control group' used in calculating GDP was up 0.5% on the month – a sliver above the 0.4% gain expected. Gains in the control group were led by miscellaneous stores (+2.7%), but department (+1.5%) and clothing (+1.3%) stores also posted good gains. In fact, only two categories, namely furniture (-2.4%) and sporting goods (-1.1%) exhibited declines in dollar terms – with the former coming off a solid stretch of gains.

Key Implications

This was hands-down one of the best retail sales reports in recent years. After a weak start to the year, with no gains during the first two months of 2018, consumers have been on a three month tear, rising by about 2% since – or over 8% in annualized terms. The persistence of the gains suggests that American consumers are, in fact, utilizing both the wage and income gains that have materialized as a result of the tighter labor market, the rise in wealth stemming from higher stock and home prices, as well as the windfall from the tax breaks implemented at the start of the year.

All in all, this reports suggests that growth in consumption will be north of 3% in Q2, helping lift GDP up by more than 4% (both figures in annualized terms). Moreover, while some of the momentum in retail spending may fade from the current, arguably unsustainable pace, consumers should remain in the driver's seat during the medium term as the American economy benefits from a fiscal boost, lower taxes, and a reduced regulatory burden.

Today's report will surely give the Fed hawks ammunition for pushing their case for faster rate hikes going forward. In fact, the figures corroborate the upbeat view of the economy, highlighted in yesterday's Fed statement and strengthen the case for the upgraded 'dots' in the Summary of Economic Projections. The FOMC projections suggest that two more hikes are in the cards for the rest of the year, and the case is certainly stronger after this morning's report.

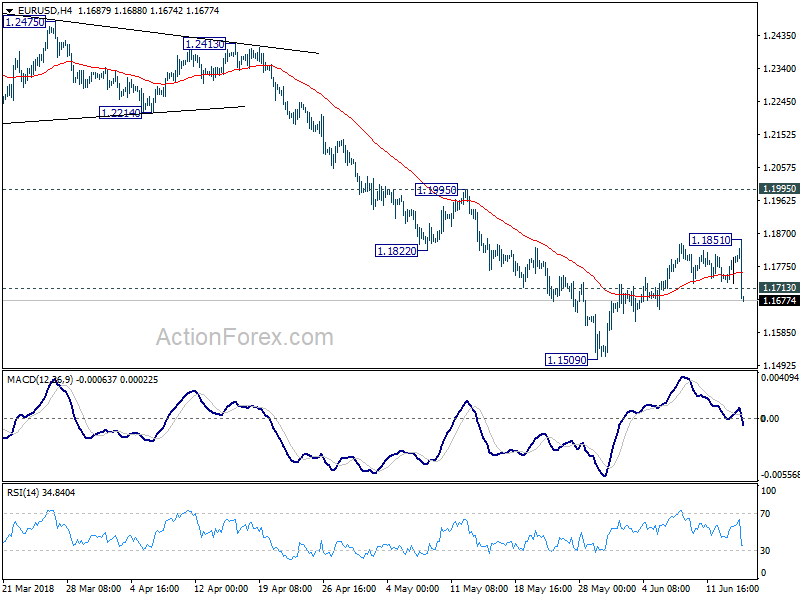

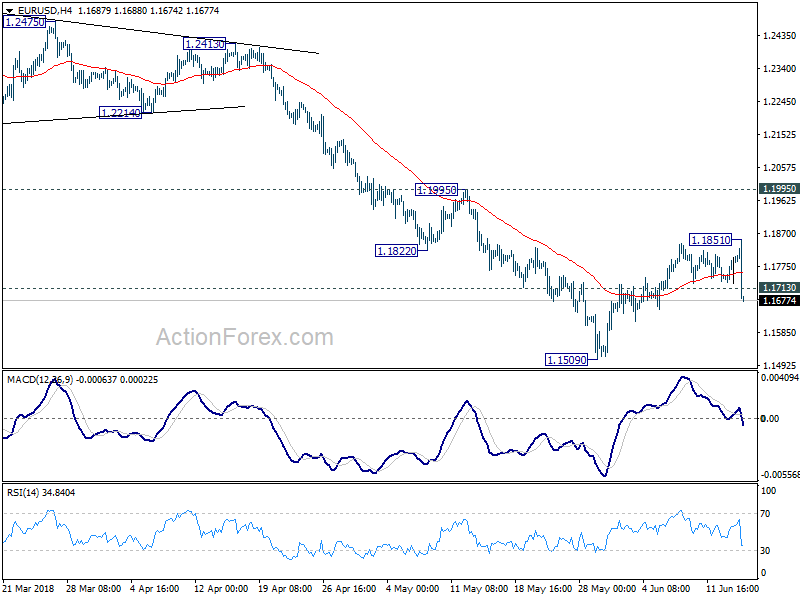

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1745; (P) 1.1773 (R1) 1.1822; More.....

EUR/USD's sharp fall and firm break of 1.1713 minor support suggests that corrective rise form 1.1509 has completed at 1.1851 already. Intraday bias is turned back to the downside for 1.1509 low first. Break will resume larger down trend from 1.2555 to 50% retracement of 1.0339 to 1.2555 at 1.1447. On the upside, above 1.1851 will extends the corrective rise from 1.1509. But as noted before, upside should be limited by 1.1995 resistance to bring down trend resumption eventually.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Euro Dives after ECB Announces to End QE this Year, But Interest Rates Will Stay Unchanged At least Through...

Euro drops sharply today as markets are not quite happy with ECB announcement. In particular, while deciding to end the asset purchase program this year, ECB said interest rate will remain at current level at least through 2019 summer. President Mario Draghi also sounds cautious as usual in the post-meeting press conference. Adding to that, 2018 GDP growth forecast was revised notably lower. Though, a positive point is that inflation projections are revised notably higher too. On the other hand, Dollar is lifted by stellar retail sales report and solid as usual jobless claims report. Sterling was lifted briefly earlier today by strong retail sales data. But the Pound was dragged down by Euro in early US session.

Technically, EUR/USD's break of 1.1713 should now indicate completion of recent rebound from 1.1509. Retest of this low would be seen shortly. USD/CHF's rebound also put 0.9911 resistance into focus. Firm break of which will confirm completion of corrective pull back from 1.0056.

ECB to taper APP to EUR 15B/M after September, end it after December

ECB left monetary policies unchanged as widely expected today. And it announced to taper the asset purchase program after September, then end it after December this year. The main refinancing rate is held at 0.00%. Correspondingly, the marginal lending facility rate is held at 0.25%. Deposit facility rate is held at -0.40%. Also, ECB said the key interest rates will "remain at their present levels at least through the summer of 2019".

The current EUR 30B per month asset purchase program will continue to run as planned till the end of September. Then, the monthly size will be tapered to EUR 15B, subject to incoming data. The program will then run till the end of December 2018 and end there. ECB said the decisions "maintain the current ample degree of monetary accommodation that will ensure the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term."

Euro drops sharply as markets are not too happy with ECB's "judgement". The decision to taper, instead of ending it right after September could be a factor. The more important one could be this part of the statement. "The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with the current expectations of a sustained adjustment path."

ECB President Mario Draghi's cautious tone is not helping Euro neither. One important point to note in the introductory statement is the revision in economic projections. ECB now projects annual GDP growth to be at 2.1% in 2018, that's notable downward revision from March projection of 2.4%. For 2019 and 2020, GDP projections were kept unchanged at 1.9% and 1.7% respectively. On the other hand, HICP inflation is projected to be 1.7% in 2018, 2019 and 2020. That's notably revised up from March projection of 1.4% in 2018, 1.4% in 2019 and 1.7% in 2020.

Also from Eurozone, German CPI was finalized at 0.50% mom, 2.2% yoy in May.

US retail sales and jobless claims beat expectations

Initial jobless claims dropped -4k to 28k in the week ended June 9, slightly better than expectation of 223k. Four-week moving average of initial claims dropped -1.25k to 224.25k. Continuing claims dropped -49k to 1.697m in the week ended June 2, lowest since December 1, 1973. Four-week moving average of continuing claims dropped -3.75k to 1.726m, lowest since December 8, 1973.

Headline retail sales rose 0.8% in May versus expectation of 0.4% mom. Ex-auto sales rose 0.9% versus expectation of 0.3%. Import price rose 0.6% mom in May versus expectation of 0.5% mom.

Also released, new housing price index rose 0.0% mom in April versus expectation of 0.2% mom.

Trump's decision on Chinese tariffs watched

Main focus in the US session will now be on Trump's decision regarding tariffs on USD 50B of 1300 lines of Chinese imports. that's the action under section 301 investigation in response to forced transfer of U.S. technology and intellectual property. It's different from the section 232 steel and aluminum tariffs against the world. The section 301 tariffs solely targeted at China. Trump will meet with his trade advisors to make a decision. The final list of tariffed products could be unveiled as soon as tomorrow.

Chinese Foreign Ministry spokesman Geng Shuang said today that there were progress in the trade talks with the US. But he warned that those agreements reached will be voided if Trump decides to go on with the tariffs. He also emphasized that that "The essence of China-U.S. trade and business ties is cooperation and win-win. We have consistently upheld that both sides should appropriately resolve relevant trade and business problems ... via dialogue and consultations,"

Sterling enjoyed brief rally on stellar May retail sales

Sterling surges after much stronger than expected retail sales data in May. But it was then dragged down by Euro after ECB rate decision. Retail sales include fuel rose 1.3% mom versus expectation of 0.5% mom and prior 1.8% mom. Retail sales include fuel rose 3.9% yoy versus expectation of 2.4% yoy and prior 1.4% yoy. Retail sales ex-fuel rose 1.3% mom versus expectation of 0.3% mom and prior 1.4% mom. Retail sales ex-fuel rose 4.4% yoy versus expectation of 2.5% yoy and prior 1.4% yoy.

In the release, ONS noted that "feedback from retailers suggested that a sustained period of good weather and Royal Wedding celebrations encouraged spending in food and household goods stores in May." And, the sharp 3.9% yoy rise in headline years was "possibly due to a combination of warm weather and slow year-on-year growth in May 2017 at 0.8%."

Also from UK, RICS house price balance improved to -3 in May.

Australian Dollar lower on job and China data

Australian Dollar is pressured by its own data miss as well as weaker than expected China data today. Australia employment rose 12k seasonally adjusted in May, below consensus of 19.2k. Unemployment rate dropped to 5.4%, as participation rate also dropped to 65.5%.

From China, retail sales rose 8.5% yoy in May, slowed from 9.4% yoy and missed expectation of 9.6% yoy. Industrial production slowed to 5.8% yoy, down from 7.0% yoy and missed expectation of 7.0% yoy. Fixed asset investment slowed to 6.1% yoy, down from 7.0% yoy and missed expectation of 7.0% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1745; (P) 1.1773 (R1) 1.1822; More.....

EUR/USD's sharp fall and firm break of 1.1713 minor support suggests that corrective rise form 1.1509 has completed at 1.1851 already. Intraday bias is turned back to the downside for 1.1509 low first. Break will resume larger down trend from 1.2555 to 50% retracement of 1.0339 to 1.2555 at 1.1447. On the upside, above 1.1851 will extends the corrective rise from 1.1509. But as noted before, upside should be limited by 1.1995 resistance to bring down trend resumption eventually.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance May | -3% | -5% | -8.00% | -7% |

| 01:00 | AUD | Consumer Inflation Expectation Jun | 4.20% | 3.70% | ||

| 01:30 | AUD | Employment Change May | 12.0K | 19.2K | 22.6k | 18.3K |

| 01:30 | AUD | Unemployment Rate May | 5.40% | 5.60% | 5.60% | |

| 02:00 | CNY | Retail Sales Y/Y May | 8.50% | 9.60% | 9.40% | |

| 02:00 | CNY | Industrial Production Y/Y May | 6.80% | 7.00% | 7.00% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y May | 6.10% | 7.00% | 7.00% | |

| 04:30 | JPY | Industrial Production M/M Apr F | 0.50% | 0.30% | 0.30% | |

| 06:00 | EUR | German CPI M/M May F | 0.50% | 0.50% | 0.50% | |

| 06:00 | EUR | German CPI Y/Y May F | 2.20% | 2.20% | 2.20% | |

| 08:30 | GBP | Retail Sales Inc Auto Fuel M/M May | 1.30% | 0.50% | 1.60% | 1.80% |

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | CAD | New Housing Price Index M/M Apr | 0.00% | 0.20% | 0.00% | |

| 12:30 | USD | Retail Sales Advance M/M May | 0.80% | 0.40% | 0.30% | |

| 12:30 | USD | Retail Sales Ex Auto M/M May | 0.90% | 0.30% | 0.30% | |

| 12:30 | USD | Import Price Index M/M May | 0.60% | 0.50% | 0.30% | 0.60% |

| 12:30 | USD | Initial Jobless Claims (Jun 09) | 218K | 223K | 222K | |

| 14:00 | USD | Business Inventories Apr | 0.30% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 87B | 92B |

(ECB) Introductory Statement to the Press Conference

Mario Draghi, President of the ECB,

Luis de Guindos, Vice-President of the ECB,

Riga, 14 June 2018

INTRODUCTORY STATEMENT

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. I would like to thank Deputy Governor Razmusa for her kind hospitality and express our special gratitude to her staff for the excellent organisation of today's meeting of the Governing Council. We will now report on the outcome of our meeting.

Since the start of our asset purchase programme (APP) in January 2015, the Governing Council has made net asset purchases under the APP conditional on the extent of progress towards a sustained adjustment in the path of inflation to levels below, but close to, 2% in the medium term. Today, the Governing Council undertook a careful review of the progress made, also taking into account the latest Eurosystem staff macroeconomic projections, measures of price and wage pressures, and uncertainties surrounding the inflation outlook.

As a result of this assessment, the Governing Council concluded that progress towards a sustained adjustment in inflation has been substantial so far. With longer-term inflation expectations well anchored, the underlying strength of the euro area economy and the continuing ample degree of monetary accommodation provide grounds to be confident that the sustained convergence of inflation towards our aim will continue in the period ahead, and will be maintained even after a gradual winding-down of our net asset purchases.

Accordingly, the Governing Council today made the following decisions:

First, as regards non-standard monetary policy measures, we will continue to make net purchases under the APP at the current monthly pace of €30 billion until the end of September 2018. We anticipate that, after September 2018, subject to incoming data confirming our medium-term inflation outlook, we will reduce the monthly pace of the net asset purchases to €15 billion until the end of December 2018 and then end net purchases.

Second, we intend to maintain our policy of reinvesting the principal payments from maturing securities purchased under the APP for an extended period of time after the end of our net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Third, we decided to keep the key ECB interest rates unchanged and we expect them to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with our current expectations of a sustained adjustment path.

Today's monetary policy decisions maintain the current ample degree of monetary accommodation that will ensure the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term. Significant monetary policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term. This support will continue to be provided by the net asset purchases until the end of the year, by the sizeable stock of acquired assets and the associated reinvestments, and by our enhanced forward guidance on the key ECB interest rates. In any event, the Governing Council stands ready to adjust all of its instruments as appropriate to ensure that inflation continues to move towards the Governing Council's inflation aim in a sustained manner.

Let me now explain our assessment in greater detail, starting with the economic analysis. Quarterly real GDP growth moderated to 0.4% in the first quarter of 2018, following growth of 0.7% in the previous quarters. This moderation reflects a pull-back from the very high levels of growth in 2017, compounded by an increase in uncertainty and some temporary and supply-side factors at both the domestic and the global level, as well as weaker impetus from external trade. The latest economic indicators and survey results are weaker, but remain consistent with ongoing solid and broad-based economic growth. Our monetary policy measures, which have facilitated the deleveraging process, continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by growing household wealth. Business investment is fostered by the favourable financing conditions, rising corporate profitability and solid demand. Housing investment remains robust. In addition, the broad-based expansion in global demand is expected to continue, thus providing impetus to euro area exports.

This assessment is broadly reflected in the June 2018 Eurosystem staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020. Compared with the March 2018 ECB staff macroeconomic projections, the outlook for real GDP growth has been revised down for 2018 and remains unchanged for 2019 and 2020.

The risks surrounding the euro area growth outlook remain broadly balanced. Nevertheless, uncertainties related to global factors, including the threat of increased protectionism, have become more prominent. Moreover, the risk of persistent heightened financial market volatility warrants monitoring.

According to Eurostat's flash estimate, euro area annual HICP inflation increased to 1.9% in May 2018, from 1.2% in April. This reflected higher contributions from energy, food and services price inflation. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around the current level for the remainder of the year. While measures of underlying inflation remain generally muted, they have been increasing from earlier lows. Domestic cost pressures are strengthening amid high levels of capacity utilisation, tightening labour markets and rising wages. Uncertainty around the inflation outlook is receding. Looking ahead, underlying inflation is expected to pick up towards the end of the year and thereafter to increase gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

This assessment is also broadly reflected in the June 2018 Eurosystem staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.7% in 2018, 2019 and 2020. Compared with the March 2018 ECB staff macroeconomic projections, the outlook for headline HICP inflation has been revised up notably for 2018 and 2019, mainly reflecting higher oil prices.

Turning to the monetary analysis, broad money (M3) growth stood at 3.9% in April 2018, after 3.7% in March and 4.3% in February. While the slower momentum in M3 dynamics over recent months mainly reflects the reduction in the monthly net asset purchases since the beginning of the year, M3 growth continues to be supported by the impact of the ECB's monetary policy measures and the low opportunity cost of holding the most liquid deposits. Accordingly, the narrow monetary aggregate M1 remained the main contributor to broad money growth, although its annual growth rate has receded in recent months from the high rates previously observed.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations stood at 3.3% in April 2018, unchanged from the previous month, and the annual growth rate of loans to households also remained stable, at 2.9%.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households and credit flows across the euro area. This is also reflected in the results of the latest Survey on the Access to Finance of Enterprises in the euro area, which indicates that small and medium-sized enterprises in particular benefited from improved access to financing.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed that today's monetary policy decisions will ensure the ample degree of monetary accommodation necessary for the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute more decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Regarding fiscal policies, the ongoing broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt remains high. All countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

We are now at your disposal for questions.