Sample Category Title

Forex Analysis: EURUSD

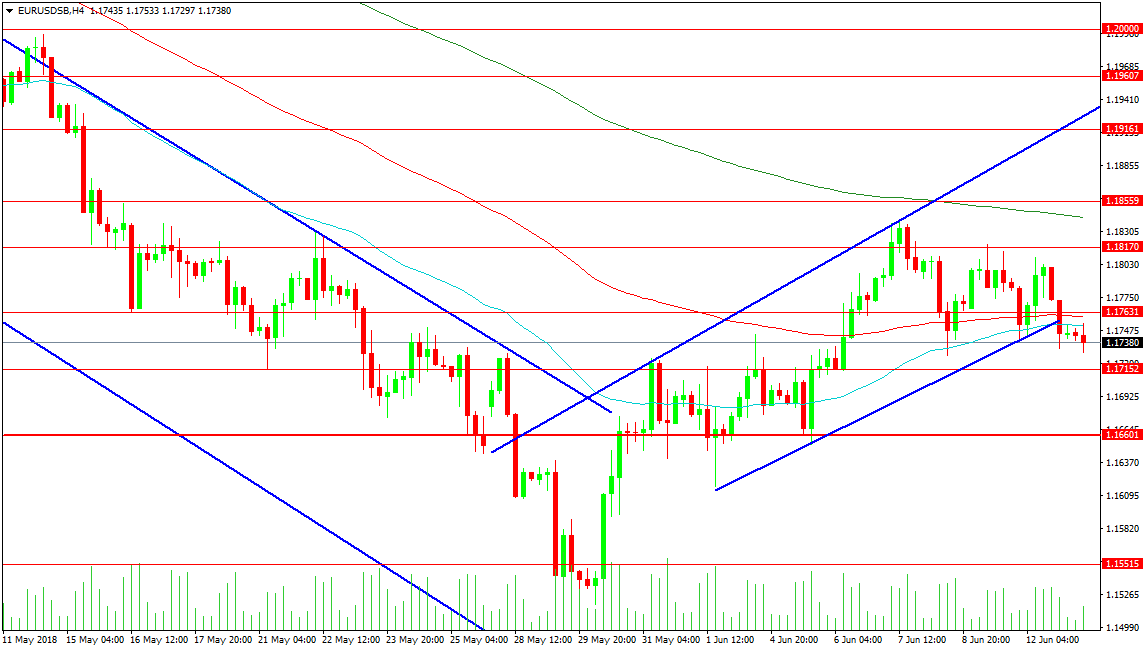

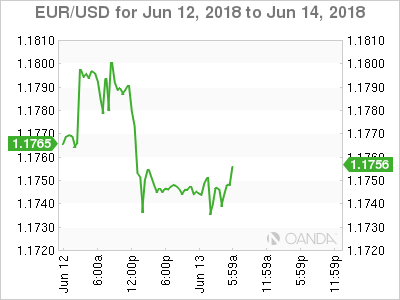

The EURUSD pair is trading in a range at the moment between 1.18350 and 1.17200 as we head into the FOMC meeting today and the ECB meeting tomorrow. Technically price has broken down in four hour from the 3 touch trend line shown on the chart but this move will need to be confirmed soon with a drop under support at 1.17200 or the volatility associated with the FOMC meeting can set the pair on a different path. For today and tomorrow we need to push out our view to take in the wider levels of support and resistance that may be needed as a result of central bank action. Support is strong below 1.16600 with a drop to 1.15515 possible and a revisit of last month’s low at 1.15096 followed by support at 1.14579.

The resistance at the high of last week may well be tested over the next 36 hours at 1.18395 with the 200 period MA at 1.18419. A level of interest close by is 1.18559 with these levels all combining to provide a relatively strong area of resistance. However as mentioned, reaction to the central banks can see price push through this zone. Above 1.19000 the 1.19161 level comes into play with the 1.19607 level guarding the way to 1.20000.

Forex Analysis: USDJPY Wave Analysis

USDJPY broke key resistance level 110.30

Likely to rise further

USDJPY recently rose sharply – breaking through the resistance area lying between key resistance level 110.30 (top of the previous correction (a)) and the 61.8% Fibonacci correction of the previous downward impulse 1 from the middle of May.

The breakout of this resistance area accelerated the active short-term impulse wave (c) – which belongs to the ABC correction 2 from the end of May.

USDJPY is likely to rise further and retest the next resistance level 111.35 (top of the previous corrective wave (2) from May and the target price for the completion of the active wave 2).

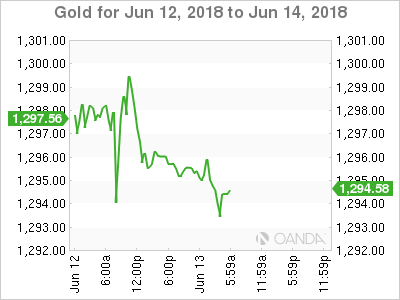

Forex Analysis: Gold

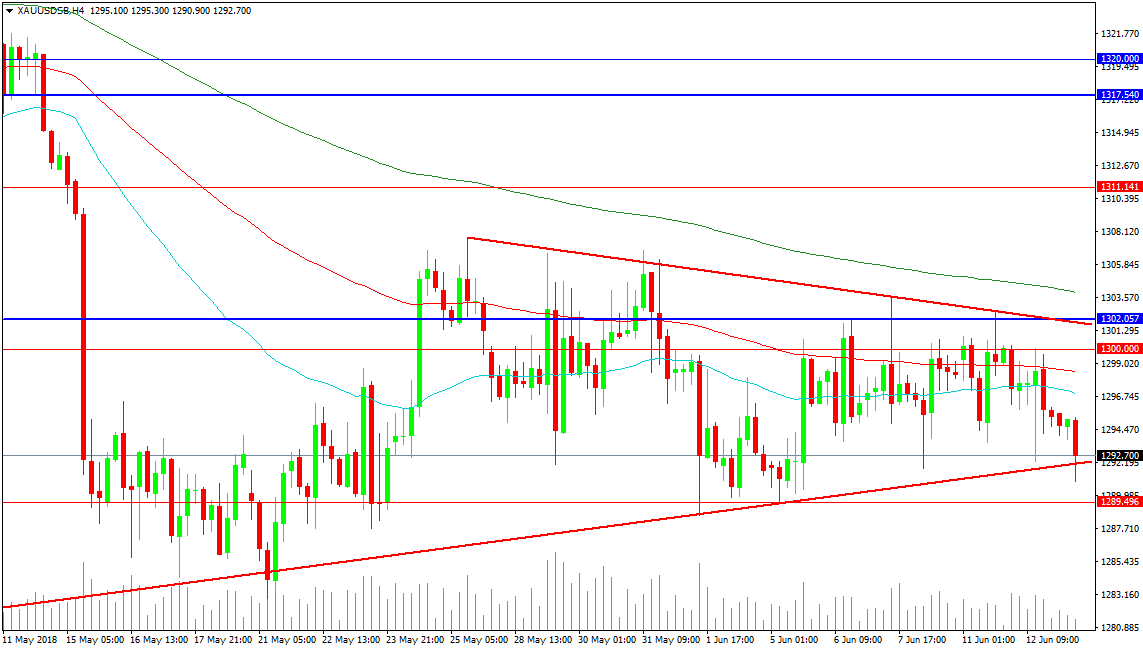

The precious metal has been in a consolidation pattern around 1300.00 for some time now, with today and tomorrow having the potential to jolt the market back to life. The price action has set up what appears to be a bearish wedge continuation pattern. As can be seen the price entered the pattern from above suggesting it will exit the pattern with a move lower. The target of the double top pattern from 1365.30, remains in the 1240.00 area. A move under 1289.50 followed by 1280.00 is needed to confirm the move lower. Supports come in at 1276.95, 1265.25 and 1250.00.

Resistance can be found at 1302.00 followed by the 200 period at 1304.00. A move above this area would need to be followed by a push above 1311.14 to continue the advance to 1317.55 and 1320.00. This would open the way to 1340.00 and a retest of the 1350.00 level.

UK CPI Data In-Line And Remains At Lowest Level In A Year

Notes/Observations

- Packed week for big events but so far it’s hard to argue that anything has gone against the grain (US-NK Summit, US CPI data, UK Parliamentary Vote on Brexit process)

- UK May CPI data in-line; on track to cool faster than BOE forecast

- FOMC meets today, expected to hike by 25bps; focus on Fed Chair Powell press conference

Asia:

- RBA Gov Lowe reiterated no strong case for near term adjustment in monetary policy; next move likely to be up if economic growth was sustained

Europe:

- UK Parliament rejected plan to remove a fixed Brexit date of March 29, 2019 (as expected, in support of govt stance)

- UK's lower house (Commons) rejected an amendment put forward by the upper house (House of Lords) that would require the government to accept the direction of Parliament in the event that no deal was reached with the EU27 (Note: Under government plan, if parliament rejected the negotiated Brexit deal, government must report back with new strategy within 28 days)

- Italy EU Affairs Min Savona stated that he never asked for Italy to leave the euro; there was no 'Plan B'

Energy:

- Russia said to have asked for oil cuts rollback for most OPEC+ nations; to propose 1.8M bpd shared quota increase. Planned to leave 1M bpd of involuntary oil reductions intact - Weekly API Oil Inventories: Crude: -0.7M v -2M prior

Economic Data:

- (FI) Finland Apr Final Retail Sales Volume Y/Y: 1.9% v 0.1% prelim

- (ES) Spain May Final CPI M/M: 0.9% v 0.9%e; Y/Y: 2.1% v 2.0%e

- (ES) Spain May Final CPI EU Harmonized M/M: 0.9% v 0.9%e; Y/Y: 2.1% v 2.1%e

- (ES) Spain May CPI Core M/M: 0.4% v 0.8% prior; Y/Y: 1.1% v 1.1%e

- (TR) Turkey Apr Industrial Production M/M: 0.9% v 0.7%e; Y/Y: 6.2% v 6.2%e

- (CH) Swiss May Producer & Import Prices M/M: 0.2% v 0.4% prior; Y/Y: 3.2% v 2.7% prior

- (CH) Swiss Q1 Industrial Output WDA Y/Y: 9.0% v 9.9% prior

- (CZ) Czech Apr Current Account (CZK): 29.3B v 7.5Be

- (UK) May CPI M/M: 0.4%e v 0.4%e; Y/Y: 2.4% v 2.4%e ((matched the lowest annual pace in a year); CPI Core Y/Y: 2.1% v 2.1%e; CPIH Y/Y: 2.3% v 2.3%e

- (UK) May RPI M/M: 0.4% v 0.4%e; Y/Y: 3.3% v 3.4%e, RPI-X (ex-mortgage interest payment) Y/Y: 3.4% v 3.4%e, Retail Price Index: 280.7 v 280.9e

- (UK) May PPI Input M/M: 2.8% v 1.8%e; Y/Y: 9.2% v 7.6%e

- (UK) May PPI Output M/M: 0.4% v 0.3%e; Y/Y: 2.9% v 2.9%e

- (UK) May PPI Output Core M/M: 0.2% v 0.2%e v 0.1% prior; Y/Y: 2.1% v 2.5%e - (UK) Apr ONS House Price Index Y/Y: 3.9% v 4.2% prior

- (IS) Iceland Central Bank (Sedlabanki) left its 7-Day Term Deposit Rate unchanged at 4.25%

- (EU) Euro Zone Apr Industrial Production M/M: -0.9% v -0.7%e; Y/Y: 1.7% v 2.7%e

- (EU) Euro Zone Q1 Employment Q/Q: 0.4% v 0.3% prior; Y/Y: 1.4% v 1.6% prior

Fixed Income Issuance:

- (DK) Denmark sold total DKK400M in 3-month and 6-month Bills

- (IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

- (NO) Norway sold NOK2.0B vs. NOK2.0B indicated in 2% May 2023 Bonds; Avg Yield: 1.41% v 1.19% prior; Bid-to-cover: 2.44x v 1.88x prior

- (SE) Sweden sold SEK1.5B vs. SEK1.5B indicated in 1% 2026 Bond; Avg Yield: 0.4226% v 0.6878% prior; Bid-to-cover: 4.17x v 4.48x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.2 at 388.4, FTSE +0.1% at 7713, DAX +0.1% at 12850, CAC-40 +0.3% at 5468, IBEX-35 -0.4% at 9870, FTSE MIB +0.4% at 22194, SMI flat at 8642, S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European Indices trade mixed following a mixed US and Asian session overnight. The Spanish Ibex underpeforms being weighed by shares of retail giant Inditex which trades lower after results. Elsewhere retailers Dixons Carphone trades lower after a data breach, Mulberry, Biff and Charles Stanley among other names trading lower following earnings. Connect Group is a notable faller after seeing pretax materially lower than estimates, with Neste and Meyer Burger also trading lower. Looking ahead earnings include BitAuto and Korn/Ferry.

Movers

- Consumer Discretionary Inditex [ITX.UK] -1.1% (Earnings), Connect Group [CNCT.UK] -46% (Profit warning), Mulberry [MUL.UK] -1.9% (Earnings), Dixons Carphone [DC.UK] -3.2% (Data breach), Biffa [BIFF.UK] -3.2% (Earnings)

- Financials Charles Stanley [CAY.UK] -2.6% (Earnings, Management change)

- Technology Meyer Burger Tech [MBTN.CH] -6% (Alleged accounting irregularities)

- Energy Neste [NESTE.FI] -3.6% (Finnish Gov sells shares)

- Utilities Acea [ACE.IT] -1.4% (Chairman arrested)

Speakers

- Italy Fin Min Tria said to seek avoiding a VAT hike

- Italy Interior Min Salvini (also Dep PM): Govt will begin flat tax changes in 2018 and dismantle pension reform piece by piece

- Sweden Central Bank (Riksbank) Business Survey: Economic upswing was continuing with plenty of demand all over. Demand was strong in all sectors but some unease over housing market developments

- German Institute for Economic Research (DIW) cut its German 2018 GDP growth forecast from 2.2% to 1.9%

- Russia Energy Min Novak: Domestic market to stabilize if oil price declined to $70/barrel (**Reminder: On Jun 12th reports circulated that Russia would ask for oil cuts rollback for most OPEC+ nations)

- IEA Monthly Oil Report noted that economic environment for 2018 and 2019 remained supportive for oil demand but risks were increasing. World economy was feeling some pain with higher oil prices. Iran and Venezuela oil production could slump by 30% but OPEC members could raise output in short order by 1.1M bpd to cover losses elsewhere

Currencies

- Dealers noted that the FOMC meeting was the main risk event in the session. With a rate hike almost fully priced by the markets, price action would most likely be driven by potential changes in rate guidance. USD could rally further if the FOMC signaled that real yields were likely to rise materially from here

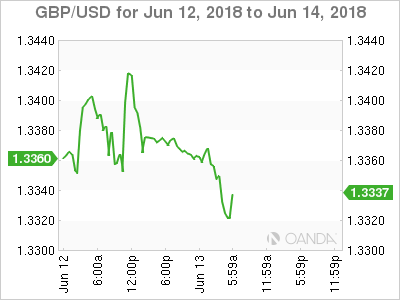

- GBP/USD was softer ahead of key inflation data with political uncertainties remaining for PM May’s Brexit strategy as she continues to ward off a revolt from pro-European lawmakers on her legislation. UK May CPI data was in-line at 1-year lows with analysts noting that it was on track to cool faster than BOE expected

- USD/JPY was higher for the 3rd straight session to approach the 110.70 area as a 25bps rate increase by the Fed was almost a given.

Fixed Income

- Bund Futures trade 42 ticks lower at 159.43 as Eurozone bond markets await the ECB's meeting on Thursday, with potentially some hints at the exit strategy from asset purchases and at the timing and path of interest rate increases. Upside targets 161.75 followed by 162.50, while a return lower targets the 158.75 level.

- Gilt futures trade at 122.14 higher by 40 ticks as UK inflation is on track to cool faster than BOE expects. Support continues stands at 120.75 then 119.25, with upside resistance at 122.85 then 123.35.

- Wednesday’s liquidity report showed Tuesday’s excess liquidity fell from €1.910T to €1.905T. Use of the marginal lending facility decreased from €231M to €43M.

- Corporate issuance continues to see companies rush sell bonds to try to outrun potential market turmoil that could come when central banks tighten policies. Corporations have already issued $34B of high-grade debt this month.

Looking Ahead

- (IT) Italy Debt Agency (Tesoro) to sell 2021, 2025 and 2046 and 2048 BTP Bonds

- 05:30 (DE) Germany to sell €2.0B in 0.5% Feb 2028 Bunds

- 05:30 (PT) Portugal Debt Agency (IGCP) to sell €0.75-1.0B in 2023 and 2028 OT bonds

- 06:00 (IE) Ireland Apr Property Prices M/M: No est v 0.7% prior; Y/Y: No est v 12.7% prior

- 06:00 (IL) Israel May Trade Balance: No est v -$2.3B prior

- 06:00 (ZA) South Africa Q2 BER Business Confidence: No est v 45 prior

- 06:00 (CZ) Czech Republic to sell 2022 and 2030 bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (RU) Russia to sell in OFZ bonds (2 tranches)

- 07:00 (US) MBA Mortgage Applications w/e Jun 8th: No est v 4.1% prior

- 07:00 (ZA) South Africa Apr Retail Sales M/M: 0.6%e v 0.0% prior; Y/Y: 4.4%e v 4.8% prior

- 08:00 (PL) Poland Apr Current Account: -€0.4Be v -€1.0B prior; Trade Balance: -€0.1Be v -€0.3B prior; Exports: €17.3Be v €18.1B prior; Imports: €17.3Be v €18.4B prior

- 08:00 (IS) Iceland May Unemployment Rate: No est v 2.3% prior

- 08:00 (BR) Brazil Apr Retail Sales M/M: 0.6%e v 0.3% prior; Y/Y: -0.5%e v +6.5% prior

- 08:00 (BR) Brazil Apr Broad Retail Sales M/M: 1.4%e v 1.1% prior; Y/Y: 8.3%e v 7.8% prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (CA) Canada May Teranet/National Bank HPI M/M: No est v 0.2% prior; Y/Y: No est v 5.6% prior; HPI Index: No est v 219.49 prior

- 08:30 (US) May PPI Final Demand M/M: 0.3%e v 0.1% prior; Y/Y: 2.8%e v 2.6% prior

- 08:30 (US) May PPI Ex Food and Energy M/M: 0.2%e v 0.2% prior; Y/Y: 2.3%e v 2.3% prior

- 08:30 (US) May PPI Ex Food, Energy, Trade M/M: 0.2%e v 0.1% prior; Y/Y: No est v 2.5% prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 12:00 (DE) German Foreign Min Altmaier on global economy

- 14:00 (US) FOMC Rate Decision: Expected to raise target range by 25bps to 1.75-2.00%

- 14:30 (US) Fed Chair Powell post rate decision press conference

- 15:00 (AR) Argentina Q1 Unemployment Rate: 8.5%e v 7.2% prior

- 18:00 (CL) Chile Central Bank (BCCH) Interest Rate Decision: Expected to keep Overnight Rate Target unchanged at 2.50%

Euro Ticks Higher Ahead of Expected Fed Rate Hike

EUR/USD is steady in the Wednesday session. Currently, the pair is trading at 1.1760, up 0.13% on the day. In the eurozone, Employment Change edged up to 0.4%, above the estimate of 0.3%. Industrial Production declined 0.9%, weaker than the forecast of -0.6%. In the U.S, PPI is expected to rise to 0.3% and Core PPI is forecast to remain pegged at 0.2%. The Federal Reserve is expected to raise the benchmark rate by a quarter-point. On Thursday, German releases CPI and the ECB is expected to maintain rates at a flat 0.0%. The U.S will release retail sales reports and unemployment claims.

The Singapore Summit was a milestone, as it marked the first time that leaders of the United States and North Korea met face-to-face. However, the joint statement put out by Presidents Trump and Kim was short on details, which could explain a lack of movement in the currency markets following the summit. The joint statement reaffirmed North Korea’s full commitment to complete denuclearization, but there was no mention of a timetable or any verification mechanisms. Even if the summit was largely symbolic, there’s no denying that tensions have significantly eased and that the summit could mark a first step in bringing peace to the Korean peninsula.

Central banks will be in the spotlight this week, with rate statements from the Federal Reserve on Wednesday and the ECB on Thursday. The Fed is widely expected to raise rates, with odds of a quarter-rate hike at 94%. Although the rate increase has been priced in, the U.S dollar could still make some gains against its major rivals. In Europe, the ECB will be looking for any clues with regard to the ECB’s asset-purchase program. Currently, the bank is purchasing EUR 30 billion/mth, and the scheme is scheduled to wind up in September. However, some ECB policymakers want to phase out the program slowly, rather than turn off the tap completely in September. ECB chief economist Peter Praet recently said that the ECB board members would conduct a detailed discussion about the fate of the stimulus package at the June meeting. Mario Draghi will likely make mention of the program at his press conference, so traders should be prepared for some volatility from EUR/USD on Thursday.

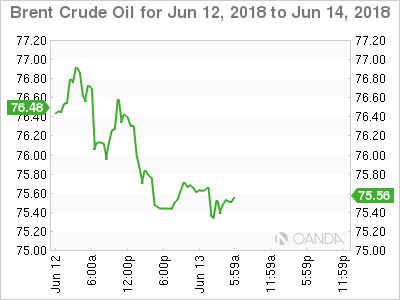

WTI Oil Outlook: Recovery Hold Within Daily Cloud But The Downside Remains Vulnerable

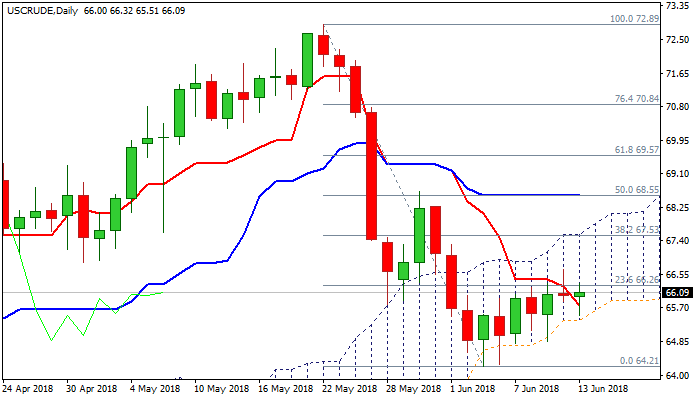

WTI oil price bounced after testing daily cloud base ($65.38) on Wednesday, keeping strong rising support which underpins recovery rally from $64.21 (05 June low). Series of higher lows and higher highs define near-term uptrend, but recovery was so far mild and keeping well below pivotal barrier at $67.53 (daily cloud top / Fibo 38.2% of $72.89/$64.21 fall). Release of US API crude stocks data on Tuesday impacted oil price negatively, as data showed crude inventories rose 0.83 million barrels vs expected draw of 2.7 million barrels. Focus turns towards release of US EIA weekly crude stocks report, due later today, to gauge the strength of demand in the US. Weekly crude stocks are forecasted for 1.44 million barrels draw, compared to 2 million barrels build previous week, which would boost oil price if release comes at/below expectations. Conversely, oil price may drop on negative outcome today (build of crude inventories). Daily cloud base marks key support and close below it would weaken near-term structure and risk return to $64.21 low. Daily studies are bearishly aligned and support negative scenario for now.

Res: 66.68, 67.63, 67.85, 68.55

Sup: 65.38, 64.84, 64.21, 63.81

EUR/USD Breaks Support But Remains Indecisive Before USD Rate

The EUR/USD downtrend channel after bouncing at the 38.2% Fibonacci retracement level of wave 4 (purple) is mild and choppy. This could indicate that the wave 4 could expand into a larger sideways consolidation or triangle. A bearish breakout could indicate the restart the downtrend but could also lead to larger wave X (orange) correction. Keep in mind that later today there is USD interest rate decision.

EUR/USD broke multiple support trend lines (dotted green) but price action is now building a new sideways zone. A new bearish breakout could see price test the next support zones around 1.1650, 1.16, and 1.1550. A bullish breakout could indicate a larger bullish correction towards the 50% Fib on the 4 hour chart.

GBP/USD Respects Downtrend Channel And Now Challenges 1.33

The GBP/USD is breaking another support trend line which could spark a downtrend continuation but traders need to be aware of the big USD rate decision later today. A bearish breakout could aim at 1.30.

The GBP/USD needs to break below 1.33 and the mild angled downtrend channel before a larger bearish breakout could be expected.

The GBP/USD broke the support trend lines (dotted blue) yesterday, which caused lots of volatility. Eventually the resistance trend lines and broken support levels held and price moved lower. The next bearish breakout is seeing price test the bearish channel. A breakout is needed before price could be in a potential wave 3.

USD Grinds Higher On Pending Rate Hike

USD better bid ahead of Fed decision

The demand for US dollar rose on Wednesday as investors await the outcome of the June FOMC meeting. Despite the fact that there is no question the Federal Reserve will increase short-term interest rates by another 25bps, which would bring the target band to 1.75% - 2%, investors remain cautious amid uncertainties regarding a potential shift in expectations for future policy. Indeed, FOMC members are due to provide updated economic and financial forecasts.

According to official data, the US economy is on a solid footing with inflation rising towards the Fed’s 2% goal and accelerating GDP growth rate. However, we believe that Fed officials won’t get ahead of themselves and will adopt a precautionary approach as many uncertainties remain. Primarily, the Fed started to unwind its giant $4.5tn balance sheet just a few months ago and it will take a few more months to see the effects of this reduction of dollar liquidity on the market. Secondly, the impressive improvement in the job market have not translated into an increase in real wage yet. Despite improvement in nominal wages, the increase in inflation pressure hurt has eroded wage gains. On an inflation-adjusted basis, US wage growth eased for a second straight month in May as it rose only 0.3%y/y, compared to 0.4%y/y in April.

We anticipate the FOMC members will signal one more rate hike this year, most likely in September, as well as a moderate upward adjustment in their growth forecast. Modification of inflation expectations should be more cosmetic. Overall, we think that Fed members will start considering a slower path of tightening as the effect of balance sheet unwinding will start to kick in.

Short the yen

USD/JPY and EUR/JPY should be reloaded now This week’s Bank of Japan policy decision will be to hold rates. USD/JPY continued to strengthen ahead of critical US Federal Reserve and BoJ meetings. The BoJ has made it clear: no change should be expected. In addition, the trade dispute with the US has caused some distortion in the market pricing of the Euro. Monetary policy divergence remains the primary drive in USD/JPY positioning.

Inflation is far off target, and the BoJ has said that changes would materialize only when inflation reaches the bank’s target. Growth has also disappointed, led by weakening private demand, indicating a target-hit is also unlikely next year. Investment and consumptions could easily correct lower should, weighing on wages and prices, should the market feel that the stimulus is now causing stocks to fall. Therefore, further easing could be on the table to prop-up asset prices and confidence. Finally, the political threat to Prime Minister Abe and ‘Abenomics’ has faded. With a firm grip on power, Abenomics could fire up again.

Fed To Hike, But What Next?

Yesterday's data showed that U.S consumer prices climbed in May, a further sign price pressures stateside are solidifying. The Fed, which began its two-day policy meeting yesterday, is watching price data closely as it weighs the path of short-term interest rates.

This afternoon, Fed officials are widely expected to announce an increase in their benchmark short-term interest rate (2:00 pm EDT), when they also are expected to signal their plans for H2, 2018.

Note: The Fed's preferred inflation measure, the personal consumption expenditures index, rose +2% in April from a year earlier, matching the Fed's annual inflation target for a second consecutive month. Prices ex-food and energy rose +1.8% y/y.

ECB may wait until July

Most of the focus at tomorrow's ECB meeting will be on potential signals for what happens after September. While the market looks for the asset purchases – currently at €30B a month – to be tapered in Q4, the ECB might wait until next month to reveal details.

The ECB will publish staff forecasts on growth and inflation – staff are likely to boost inflation forecasts on the back of a weaker currency and higher oil prices than three-months ago.

On tap: U.K inflation, FOMC statement & AUD employment (June 13), U.K retail sales, ECB rate announcement, U.S retail sales & Bank of Japan (BoJ) rate announcement (June 14).

1. Stocks mixed results

Global equities have mostly traded sideways overnight ahead of the Fed's statement later, when officials are widely expected to hike interest rates and provide further clues on their future path.

In Japan, stocks edged higher overnight, but gains were limited as many investors await the Fed's policy decision. The Nikkei share average ended +0.4% higher, while the broader Topix also gained +0.4%.

Down-under, mining stocks led Aussie shares lower on Wednesday. The benchmark S&P/ASX 200 index was down -0.5%. It added +0.2% on Tuesday.

In China and Hong Kong, stocks slid overnight, pressured by shares of telecommunications – (ZTE had about -$3B wiped off its market value after agreeing to pay up to +$1.4B in U.S penalties). The CSI300 index fell -0.7%, while the Shanghai Composite Index lost -0.8%. The Hang Seng index dropped -0.6%, while the Hong Kong China Enterprises Index lost -1.0%.

In Europe, regional bourses trade mixed. The Spanish Ibex is underperforming, weighed by retail shares, which trades lower after results.

U.S stocks are set to open in the ‘black' (+0.1%).

Indices [Stoxx600 +0.2 at 388.4, FTSE +0.1% at 7713, DAX +0.1% at 12850, CAC-40 +0.3% at 5468, IBEX-35 -0.4% at 9870, FTSE MIB +0.4% at 22194, SMI flat at 8642, S&P 500 Futures +0.1%.

2. Oil prices drop as supplies increase, gold unchanged

Oil prices are under pressure, hit by rising supplies in the U.S and expectations that producer group OPEC could relax voluntary output cuts.

Benchmark Brent crude is down -35c at +$75.53 a barrel, while U.S. light crude is -40c lower at +$65.96.

Note: OPEC and some non-OPEC producers started withholding output in 2017 to reduce a global supply overhang and prices have risen by around +60% over the last year.

However, OPEC said yesterday that the outlook for the oil market in H2 of this year was highly uncertain, and warned of downside risks to demand.

OPEC will meet on June 22 in Vienna, to discuss future production policy.

Note: In the U.S, API data yesterday showed that crude oil inventories rose by +830k barrels in the week to June 8, to +433.7m.

Ahead of the U.S open, gold prices are holding steady after falling to a one-week low Tuesday, as the market waits for clues on the pace of future interest rate hikes by the Fed. Spot gold is little changed at +$1,295.02 per ounce, after it touched a one-week low of +$1,292.60 yesterday.

3. Sovereign bond yields trade like commodities

Italy's borrowing costs have dropped sharply this morning ahead of a key bond auction after the country's new E.U Affairs Minister Paolo Savona said the EUR was “indispensable” and denied he had ever suggested leaving the single currency.

Note: Savona had previously expressed hostile views on the ‘single' unit, and his potential appointment as economy minister for the anti-establishment coalition last month had sparked a market selloff.

Italy's two-year government bond saw its yield drop well below +1% and is last down -14 bps at +0.90%. This is below where it started the week – at +1.13% – and a long ways from last week's peak of +2.73% when the market concerns were at their most intense.

Elsewhere, the yield on 10-year Treasuries gained +1 bps to +2.97%, the highest in a week. In Germany, the 10-year yield dipped less than -1 bps to +0.49%. In the U.K, the 10-year Gilt yield fell -1 bps to +1.401%.

4. Dollar looks for guidance

With a Fed rate hike almost fully priced by the markets, price action would most likely be driven by potential changes in rate guidance.

The ‘bulls' expect the USD to rally further if the FOMC signal that real yields were likely to rise materially from here.

GBP/USD (£1.3317) is a tad softer after today's inflation data (see below). It has also come under geo-political pressure – political uncertainties are remaining for PM May's Brexit strategy as she continues to ward off a revolt from pro-European lawmakers on her legislation.

USD/JPY (¥110.61) is higher for the third straight session to approach the 110.70 area as a +25 bps rate increase by the Fed was almost a given.

Bitcoin (BTC) has tumbled to its lowest level since February. BTC fell below +$6,500, bringing the slide for the year to more than -50%.

5. U.K inflation held steady in May

Data this morning showed that annual inflation in the U.K was steady in May, as rising crude oil prices pushed up companies' costs.

According to the ONS, consumer prices rose +2.4% on year in May, matching the rate seen in April. Digging deeper, higher prices for gas and airfares offset weakening pressure on inflation from housing services and food and drink.

The figures suggest that inflationary pressures persist in the U.K despite subdued wage growth. This should keep the BoE in play for the time being.

Note: Governor Carney has suggested that he expects to raise borrowing costs in the U.K two to three times within the next few years to bring inflation back to their +2% target.

Currently, consensus expects the next BoE rate increase could come as soon as August, but those expectations have taken a hit following a run of poor growth signals.