Sample Category Title

Gold Steady as Federal Reserve in Focus

Gold has posted small gains in the Wednesday session. In North American trade, the spot price for one ounce of gold is $1297.73, up 0.13% on the day. On the release front, the Federal Reserve is expected to raise interest rates to a range between 1.75% and 2.00%. On the inflation front, there was positive news. The Producer Price Index jumped to 0.5%, well above the estimate of 0.1%. This marked the highest gain since April 2017. Core PPI edged up to 0.3%, above the forecast of 0.2% percent. On Thursday, the U.S releases retail sales reports and unemployment claims.

All eyes are on the Federal Reserve, which winds up its 2-day policy meeting on Wednesday. The Fed is widely expected to raise rates to a range between 1.75% and 2.0%. The odds of a quarter-point move stand at 96% percent, according to the CME Group. Although a rate hike has been priced in by the markets, such a significant move could boost the U.S dollar against its rivals. Investors will be paying close attention to the language of the rate statement as well as the “dot-plot” forecasts, looking for any clues regarding rate hikes in the second half of 2018. The Fed is currently projecting a total of three hikes this year, but a strong economy and rising inflation have raised speculation that the Fed could raise rates four times in 2018.

The Trump-Kim summit continues to dominate the headlines, but it appears to be a case of symbolism over substance. The joint statement put out by Presidents Trump and Kim was short on details, which could explain a lack of movement in gold prices this week. The joint statement reaffirmed North Korea’s full commitment to complete denuclearization, but there was no mention of a timetable or any verification mechanisms. Even if the summit was largely symbolic, there’s no denying that tensions have significantly eased and that the summit could mark a first step in bringing peace to the Korean peninsula. If investors sense that progress is being made over the longstanding conflict in Korea, risk appetite could climb and send gold prices downwards.

British pound steady as CPI matches forecast

The British pound continues to have an uneventful week. In Wednesday’s North American trade, GBP/USD is trading at 1.3378, up 0.04% on the day. On the release front, British CPI remained pegged at 2.4% for a second straight month and matched the forecast. Another key inflation indicator, PPI Input, jumped 2.8%, crushing the estimate of 1.7%. In the US, inflation reports were positive. The Producer Price Index jumped to 0.5%, well above the estimate of 0.1%. This marked the highest gain since April 2017. Core PPI edged up to 0.3%, above the forecast of 0.2% percent. Later in the day, the Federal Reserve is expected to raise rates by a quarter-point and will release a rate statement. On Thursday, we’ll get a look at retail sales in the U.K and the U.S. As well, the U.S releases unemployment claims.

All eyes are on the Federal Reserve, which winds up its 2-day policy meeting on Wednesday. The Fed is widely expected to raise rates to a range between 1.75% and 2.0%. The odds of a quarter-point move stand at 96% percent, according to the CME Group. Although a rate hike has been priced in by the markets, such a significant move could boost the US dollar against its rivals. Investors will be paying close attention to the language of the rate statement as well as the “dot-plot” forecasts, looking for any clues regarding rate hikes in the second half of 2018. The Fed is currently projecting a total of three hikes this year, but a strong economy and rising inflation have raised speculation that the Fed could raise rates four times in 2018.

Wage growth in the U.K continues to lag behind inflation, which is hampering consumer spending. The labor market remains tight, but surprisingly, this has not translated into stronger wages for British workers. Where does this leave the Bank of England? Policymakers will remain hesitant to raise interest rates, unless inflation reverses its downward trend and key economic indicators move higher. The BoE will convene on June 21 for a policy meeting, and the bank is expected to hold the benchmark rate at 0.50 percent.

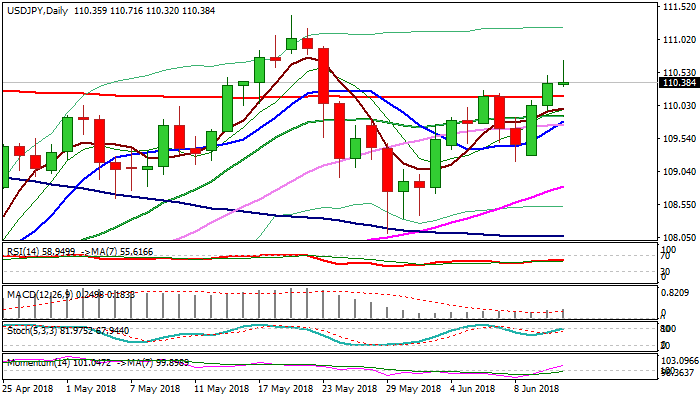

USDJPY – Pre-Fed Dips Seen as Positioning for Fresh Advance; 200SMA Marks Key Support

The pair pulled back from daily high at 110.71, posted during European trading and hit US session low at 110.32, exposing key supports at 110.22/16 (hourly cloud top / 200SMA).

The move is seen as positioning ahead of Fed, as traders expect hawkist tone from Fed chief Powell and looking for better buying levels, with dips expected to hold above 200SMA and keep bullish bias.

Firmly bullish daily techs and strong momentum are pointing higher. Current wave C eyes its FE 76.4% and 100% levels at 110.82 and 111.32 respectively, with break above former high of 21 May at 111.39, to signal extension of lager recovery rally from 104.63 (2018 low, posted on 26 Mar).

Dovish tone from Fed, on the other side, would risk extension through 200SMA, which would weaken near-term structure.

Res: 110.82; 111.00; 111.32; 111.88

Sup: 110.32; 110.16, 109.86; 109.75

Japanese Yen Steady ahead of Fed, BoJ Rate Statements

The Japanese yen is unchanged in the Wednesday session. In the North American session, USD/JPY is trading at 110.42, up 0.05% on the day. On the release front, there are no Japanese events on the schedule. In the US, inflation reports were positive. The Producer Price Index jumped to 0.5%, well above the estimate of 0.1%. This marked the highest gain since April 2017. Core PPI edged up to 0.3%, above the forecast of 0.2% percent. Later in the day, the Federal Reserve is expected to raise rates by a quarter-point and will release a rate statement.

The Trump-Kim summit continues to dominate the headlines, as it marked the first time that leaders of the United States and North Korea met face-to-face. However, the joint statement put out by Presidents Trump and Kim was short on details, which could explain a lack of movement in the currency markets following the summit. The joint statement reaffirmed North Korea’s full commitment to complete denuclearization, but there was no mention of a timetable or any verification mechanisms. Even if the summit was largely symbolic, there’s no denying that tensions have significantly eased and that the summit could mark a first step in bringing peace to the Korean peninsula. Japan is carefully watching developments as they unfold, and is clearly worried after Trump abruptly announced an end to war exercises between the U.S and South Korea, in a significant gesture of goodwill towards North Korea.

Central banks will be in the spotlight this week, with rate statements from the Federal Reserve and the Bank of Japan. The Fed is widely expected to raise the benchmark rate to a range between 1.75% and 2.0%. The Fed is widely expected to raise rates to a range between 1.75% and 2.0%. The odds of a quarter-point move stand at 96% percent, according to the CME Group. Although a rate hike has been priced in by the markets, such a significant move could boost the US dollar against its rivals. Investors are still uncertain whether the Fed will raise rates three or four times in 2018. Investors will be paying close attention to the rate statement and the “dot-plot” forecasts, looking for any clues regarding rate hikes in the second half of 2018. The Fed is currently projecting a total of three hikes this year, but a strong economy and rising inflation have raised speculation that the Fed could raise rates four times in 2018. The Bank of Japan is expected to maintain rates at -0.10%, and BoJ Governor Haruhiko Kuroda will hold a press conference. The markets are not expecting anything dramatic, as Kuroda will likely reiterate that the bank is committed to its massive easing policy until inflation levels move closer to the BoJ target of just under 2 percent.

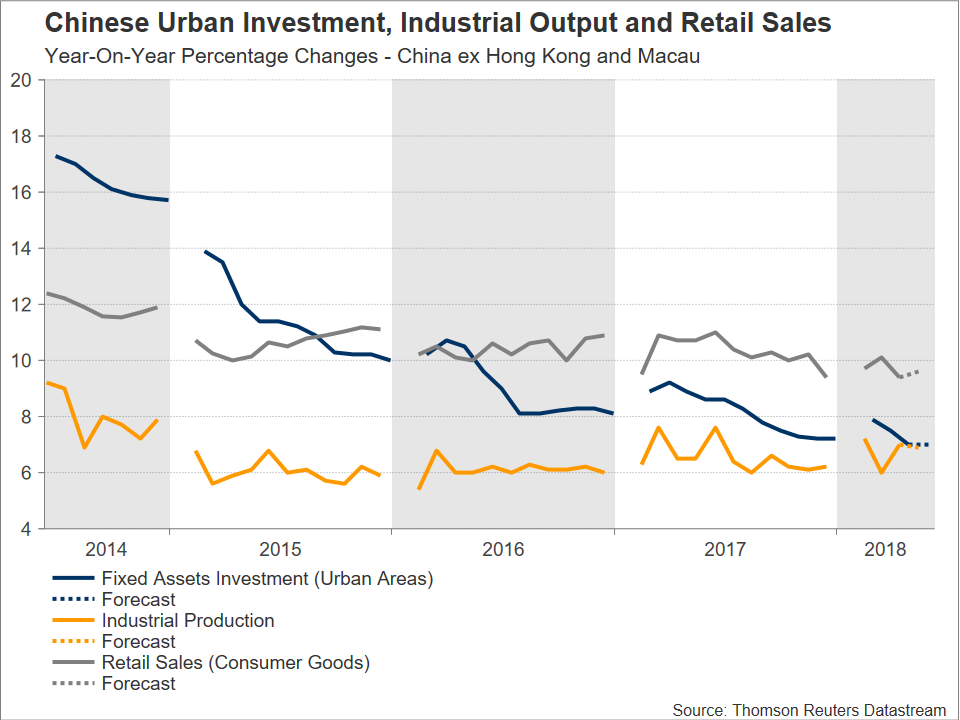

China Sees Release of Important Data amid Trade Developments; Aussie Gathers Attention

Chinese figures on fixed asset investment, industrial production and retail sales for May will be released on Thursday at 0200 GMT. Positioning might take place on the aussie as the numbers hit the markets, due to it being perceived as a liquid proxy for China’s economy by the investor community.

Fixed asset investments in urban areas are anticipated to have grown by 7.0% y/y in the year to May, the same pace as in April. Meanwhile, industrial output is projected to have marginally eased in May after a surprisingly solid reading in April, expanding by 6.9% y/y (vs 7.0% in April), while retail sales are expected to accelerate to 9.6% y/y (vs 9.4% in April).

Overall, if the prints come in line with forecasts, they would point to robust growth, especially in light of government efforts to curb pollution and limit financial risks stemming from excessive credit by the so-called “shadow” banking sector.

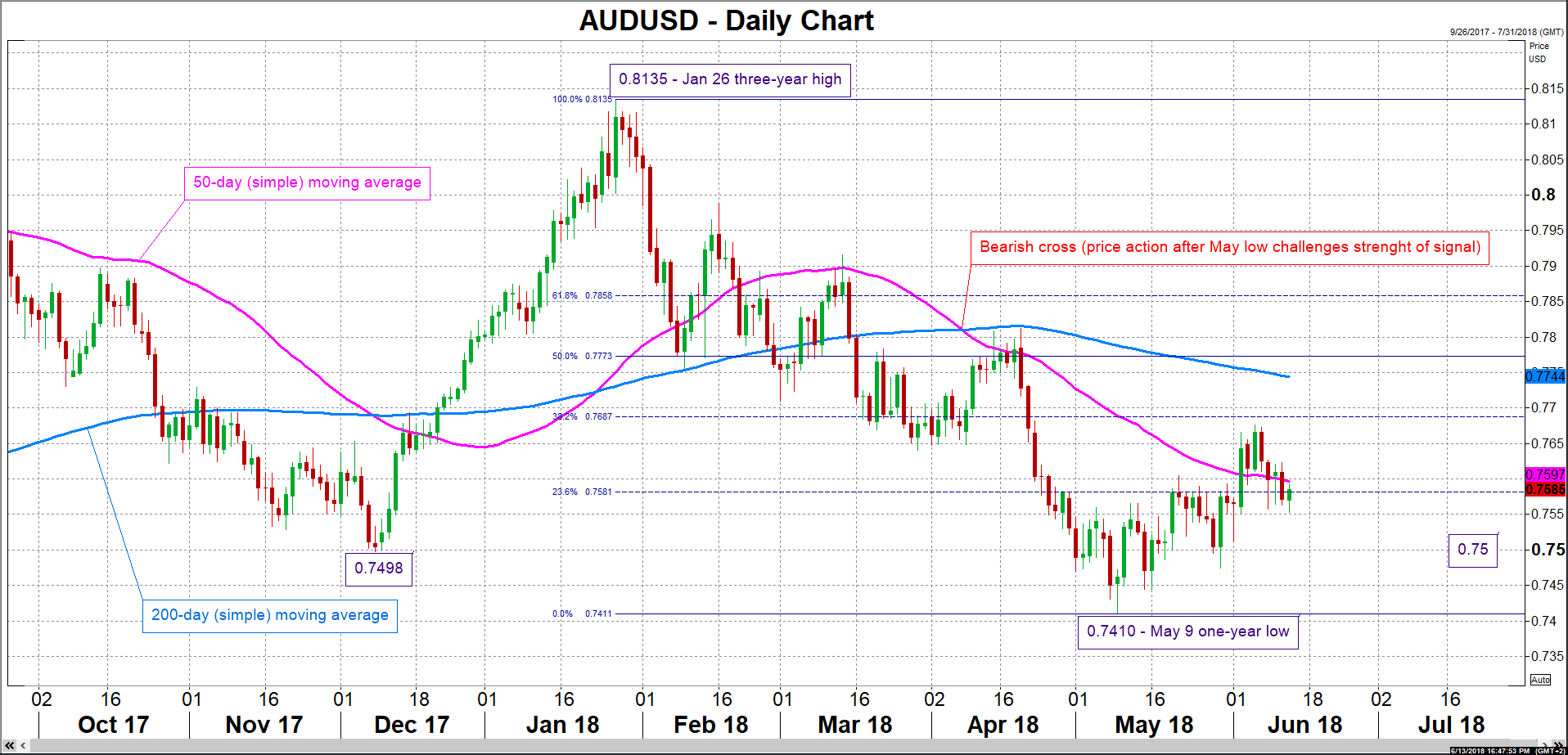

In terms of market reaction, Australia’s close economic ties with China have rendered the Australian currency a liquid proxy for China’s economy. In this respect, besides the yuan, the Australian dollar will also be closely watched as the data are made public; a strong Chinese economy is seen as aussie-positive.

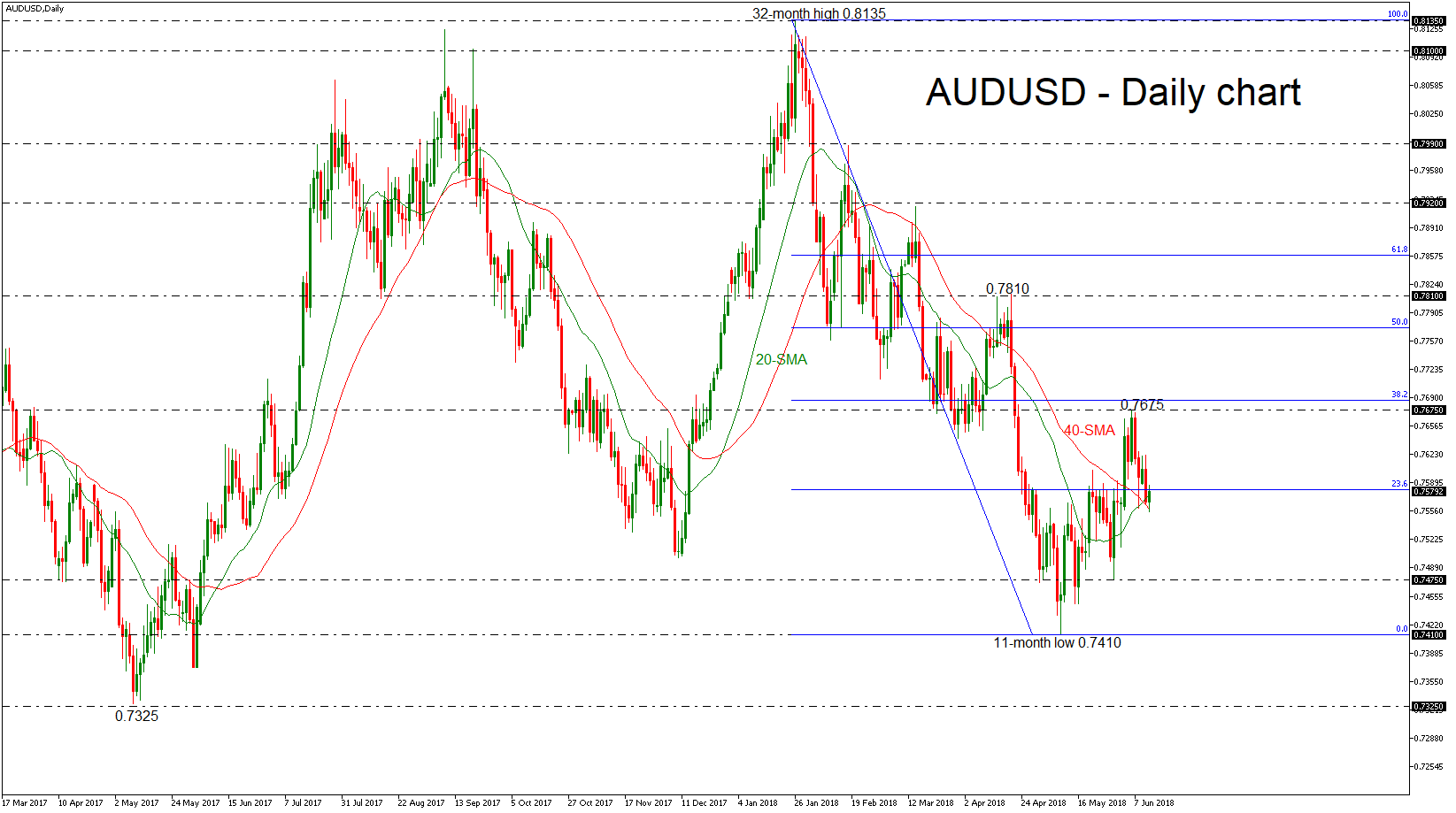

Focusing on aussie/dollar, better-than-expected releases out of China are likely to spur buying interest for the pair. AUDUSD is at the moment attempting a more conclusive break above the 23.6% Fibonacci retracement level of the January 26 to May 9 downleg at 0.7581, with the current level of the 50-day moving average at 0.7597, as well as the 0.76 round figure seemingly acting as a resistance zone to gains. A move above would turn the attention to the region around the 38.2% Fibonacci mark at 0.7687, which also encapsulates the June 6 seven-week high of 0.7676 and the 0.77 handle. Conversely, weaker data releases may exert downside pressure in AUDUSD. The area around the 0.75 handle, which was relatively congested in previous weeks, may provide support to declines, with shaper losses increasingly turning the focus to May 9’s one-year low of 0.7410.

Of more importance than Thursday’s numbers though, are trade deliberations between the US and China. In this respect, the White House said it plans on making an announcement by Friday that may see the US imposing a 25% tariff on a list of Chinese products – amounting to $50 billion – imported to the country. China warned that such an action would result in it taking off the table past trade-related commitments it made to the US. The aussie is also likely to be negatively affected in case of escalating tensions. In the meantime, following this week’s US-North Korea summit, US Secretary of State Mike Pompeo will tomorrow be in Beijing to discuss bilateral as well as broader international issues.

Lastly and related to movements in the aussie/dollar pair, it should be kept in mind that the US central bank will be completing its meeting on monetary policy later on Wednesday (1800 GMT), with the Fed chief attending a news conference half an hour later. Moreover, Australia’s employment report for May is slated for release on Thursday (0130 GMT), before the abovementioned Chinese data.

ECB: More Upbeat, But June May be Too Early for QE Commitment

When the European Central Bank (ECB) announces its rate decision on Thursday at 1145 GMT and President Draghi holds his press conference at 1230 GMT, policymakers will have a delicate job on their hands of signaling that the end of QE is drawing closer. Markets are speculating the Bank may announce a firm end-date to its asset purchases, implying that if officials choose to postpone that decision until July instead, then the euro could come under renewed selling interest on the decision.

Preparing markets for the end of ultra-easy money at a period of slowing momentum in Eurozone’s economy is no easy feat, but if anyone can succeed, it is the “maestro” himself – ECB President Mario Draghi. The Bank has long signaled its asset purchase program (QE) was heading to an end towards the end of this year, with a potential announcement coming in the summer. Recent developments, though, have likely made policymakers more hesitant to move towards the stimulus-exit door.

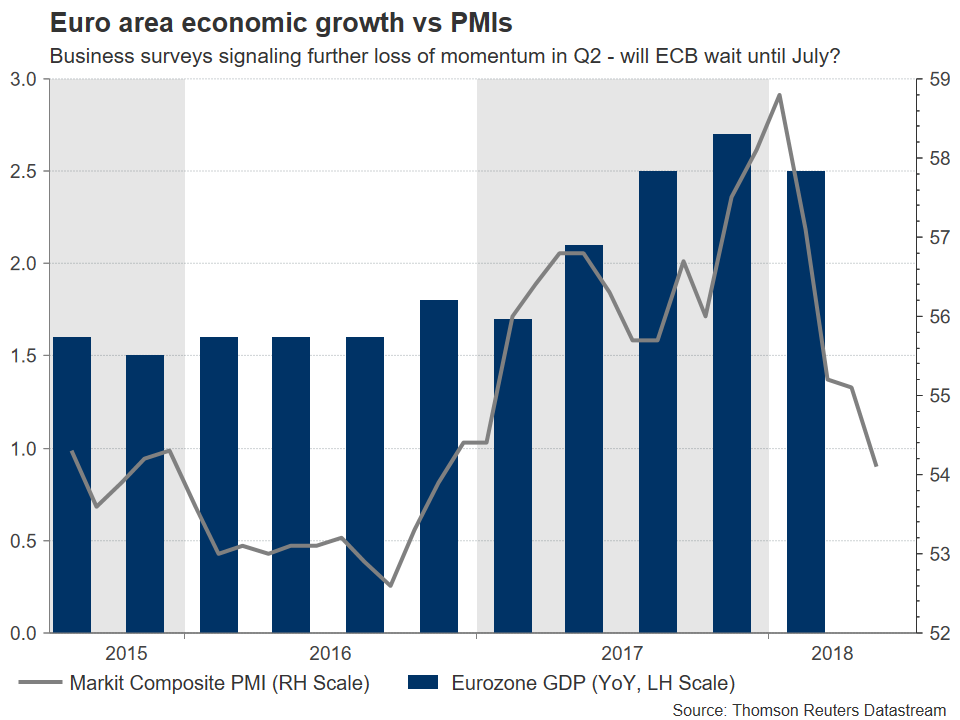

While the bloc’s economy is still expanding at a decent pace, it has lost considerable speed since the start of the year, and forward-looking surveys like the Markit PMIs suggest the slowdown has continued in Q2. While this is discouraging, the Bank still has some reasons to be optimistic. As ECB chief economist Peter Praet recently pointed out, there are signs wages are finally picking up, something considered a prelude to higher inflation. Speaking of Praet, in a rather uncharacteristic move last week, he spearheaded an effort by ECB officials to signal that they will be debating whether and when to end QE when they meet this week. Coming on top of media reports suggesting the Bank could announce a timeline on ending QE completely in June, these helped the euro recover in recent days.

Investors appear to be split on whether a concrete QE end-date will come now, or at the July gathering. Short-term price action in the euro is likely to be dictated by whether the Bank will indeed commit to a timeline, or not. If it does, that would signal policymakers are resolute about normalizing even despite short-term woes, propelling the euro higher. On the contrary, since the currency has been bid up on expectations for such an announcement, a postponement could come as a disappointment and hence push the euro lower.

What is more likely? A middle-of-the-road solution appears the most realistic outcome. Policymakers may express confidence around improving wages and signal that a discussion on a QE-exit did occur, but that nothing has been set in stone yet, keeping some flexibility in case the outlook deteriorates. Essentially, officials could use this meeting as a stepping stone, laying the groundwork for a formal announcement in July, and buying themselves extra time to monitor the economy’s performance. After all, neither Draghi nor the ECB as a whole are keen on pre-committing. A failure to follow through on a policy commitment, for any reason, could cause unwarranted market volatility and damage the Bank’s credibility in the process.

Another area markets will focus on are any signals on how the tapering will occur, meaning at what pace the Bank may reduce its purchases and over what timeframe. The ECB is currently committed to buying assets worth €30 billion/month “until the end of September 2018, or beyond, if necessary” – a much slower pace compared to the €60 billion/month it was buying up until December last year. There are multiple approaches the Bank could employ to end purchases completely, with market chatter suggesting the most likely one is halving them again to €15 billion/month from October to December, and then reducing them to zero.

While the lack of a June action could spell trouble for the common currency on the decision, it may have only limited implications for its broader direction – especially if Draghi and Co set the stage for a July move. In other words, it may not matter much if the announcement comes in June or July – so long as it does come. In the big picture, the coming months are likely to bring a lot of volatility, not least due to trade frictions and potential tensions between Brussels and Rome over EU fiscal rules. That said, the fact that the ECB is set to phase out unconventional measures suggests the longer-term outlook for the euro remains positive on the back of relative interest rates, particularly against the currencies of nations whose central banks aren’t likely to normalize anytime soon, like the yen and Swiss franc.

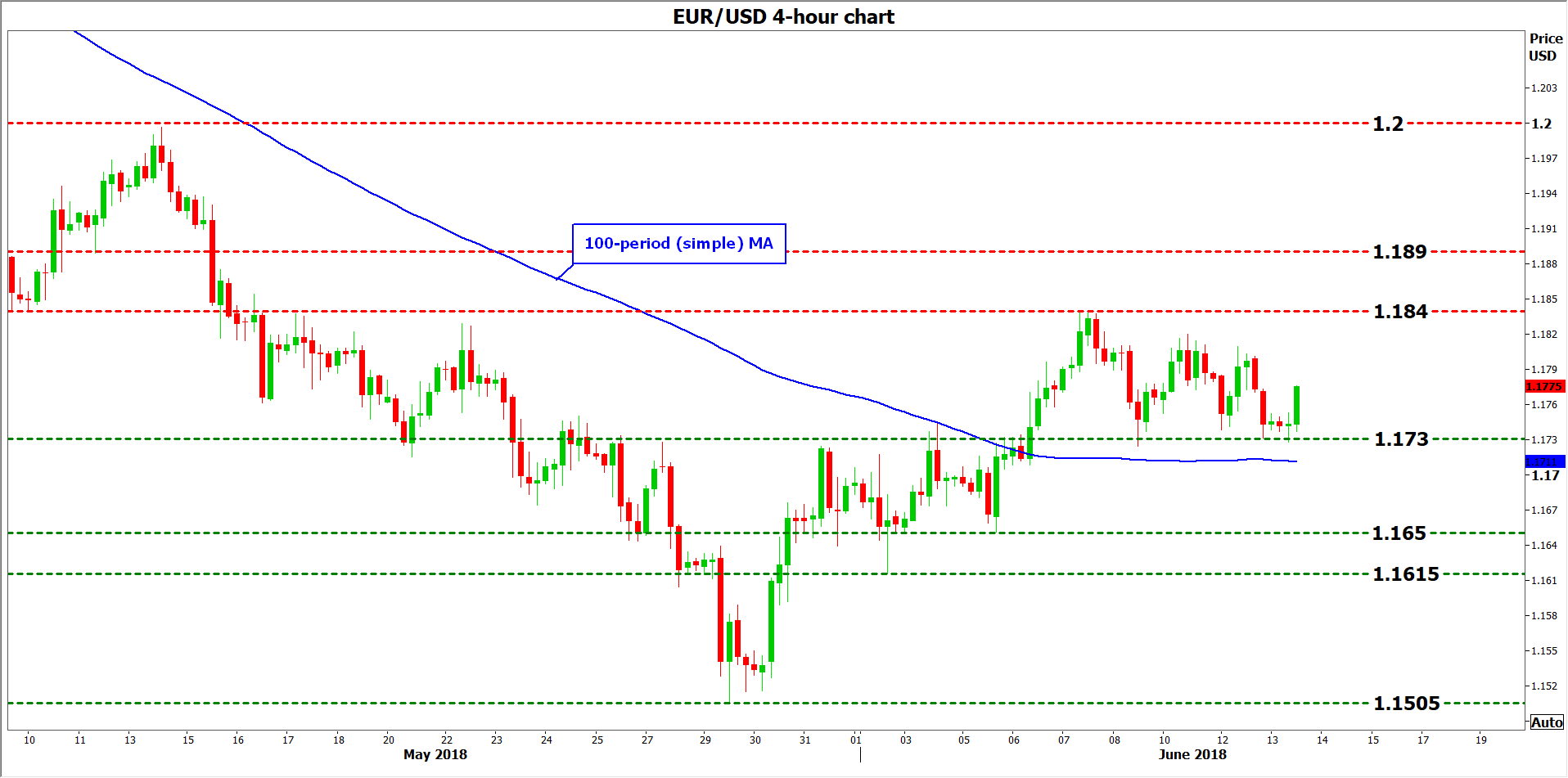

Technically, looking at euro/dollar, support to declines may come around the 1.1730 hurdle, identified by the low of June 12. A downside break would bring into view the 1.1650 level initially and the 1.1615 barrier thereafter, marked by the lows on June 5 and June 3 respectively.

On the other hand, and in case the Bank does provide a timeline for ending QE on Thursday, immediate resistance to advances could be found near the June 7 peak of 1.1840. If the bulls manage to power through it, that could open the way for 1.1890, the May 11 trough, before the attention shifts to the psychological territory of 1.2000.

Finally, it should be noted that the Fed policy decision on Wednesday could impact price action in euro/dollar ahead of the ECB’s own decision on Thursday.

UK Retail Sales Rebound Seen as Vital for August Rate Hike Expectations

After this week’s extremely poor manufacturing and trade gap figures out of the United Kingdom, hopes of a rebound in economic growth in the second quarter have been dashed. That’s put the focus even more on Thursday’s retail sales numbers, scheduled for release at 08:30 GMT. Sterling is headed for further volatility in a week jam-packed with major data releases and Brexit risk events.

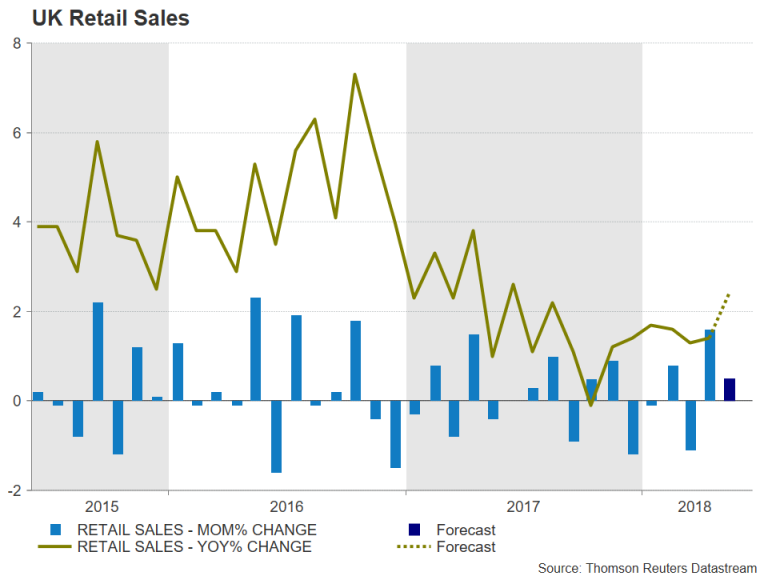

British retail sales jumped by 1.6% month-on-month in April, recovering sharply from a dire performance in the first three months of the year. Sales are forecast to grow further in May, rising by 0.5% m/m. The annual rate is expected to accelerate to 2.4% in May from the prior 1.4%.

With household consumption making up about two-thirds of the UK GDP, a weak set of figures on Thursday, would spell bad news for second quarter growth, especially when other sectors of the economy are not doing any better. Industrial production fell by 0.8% m/m in April and the manufacturing subset performed even worse, with output plunging by 1.4% over the month. The trade deficit also deteriorated in April as exports tumbled by 6.1% m/m.

This week’s employment numbers were more encouraging as a robust 146k jobs were created in the three months to April – although wage growth fell short of expectations, slowing to 2.5% year-on-year. Inflation data also disappointed, as the annual rate of CPI held steady at 2.4% in May instead of ticking higher to 2.5%. If the retail sales figures also miss the forecasts, it would cast further doubt about the chances of a rate hike by the Bank of England in August.

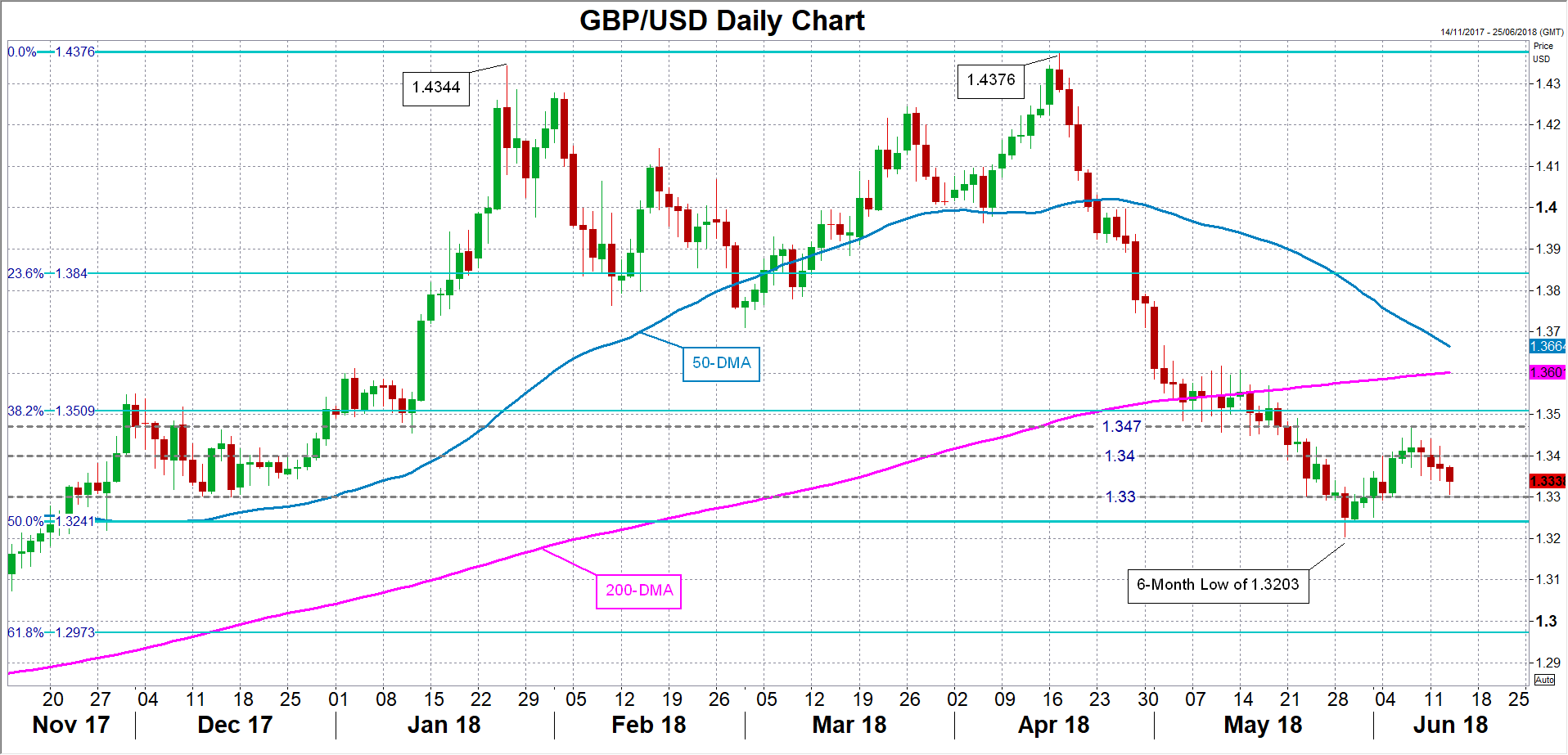

The pound would struggle to hold above immediate support at the psychological $1.33 level if sales fail to point to a further recovery in consumption. A drop below $1.33 would make a breach of the 50% Fibonacci level of the March 2017 to April 2018 uptrend more likely. Declines below the 50% Fibonacci of $1.3240 would signal a longer-term bearish shift for pound/dollar, especially if it crossed May’s 6-month low of $1.3203.

On the other hand, a stronger-than-expected rise in retail sales would keep the possibility of a BoE rate hike in the summer firmly on the table, boosting the pound. A fresh upside attempt would likely see the first resistance coming at the $1.34 handle before challenging the June top of $1.3471. A successful break above this hurdle would clear the way to the next key Fibonacci level at $1.3510.

Adding to the pound’s volatility this week are the votes in the UK Parliament as the House of Lords amendments to the government’s EU Withdrawal bill make their way back to the House of Commons. The retail sales data could get sidelined if MPs were to unexpectedly back an amendment for Britain to remain in the European single market after Brexit in a vote scheduled for later today.

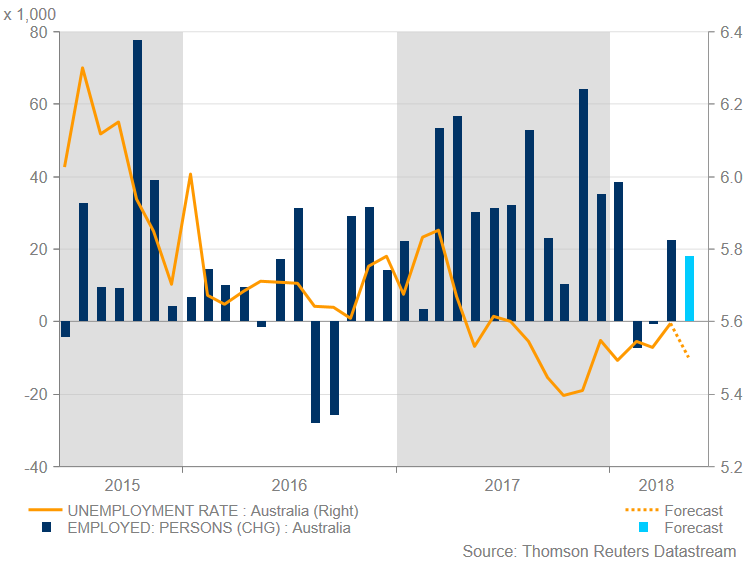

Aussie Eyes Employment Report before RBA Minutes Next Week

Australia’s employment report for May is likely to attract investors’ attention and is scheduled for release on Thursday at 0130 GMT. The unemployment rate is forecasted to tick lower to 5.5% for the month of May from 5.6% in the preceding month, while the employment change is expected to show that the economy added 18,000 jobs, 4,600 jobs less than the previous month. Meanwhile, the participation rate is predicted to remain unchanged at 65.6%.

The nation’s seasonally adjusted unemployment rate unexpectedly edged up to 5.6% in April from 5.5% in the prior month. It is the highest jobless rate since last July, even though the economy added 22,600 jobs. Despite that the number of unemployed increased by 10,600. Moreover, the labor force participation rate increased to 65.60% in April from 65.50% before, as more people entered the workforce. However, weaker releases in the coming months could push the RBA to be neutral for a longer period.

Turning to monetary policy, on June 19 the Reserve Bank of Australia (RBA) will publish the minutes of its last meeting that took place on June 5. The RBA left the cash rate unchanged at a record low of 1.5%, as widely expected. Policymakers referred that the Australian economy is predicted to advance a bit above 3% in 2018 and 2019, supported by positive business conditions and rising non-mining investment, while consumer prices are likely to remain low for some time. Inflation rose by 1.9% through the year to the March quarter, the same as in the previous quarter. Additionally, the economy grew an annual 3.1% in the first quarter of 2018, following a 2.4% expansion in the prior quarter and above expectations of a 2.8% growth. It is the fastest annual growth rate since Q2 of 2016.

In the previous week, on June 7, senior officials from Australia’s Department of Foreign Affairs and Trade met representatives from the foreign ministries of India, Japan and the US in Singapore. The officials continued discussions on promoting an open, inclusive and prosperous Indo-Pacific where all countries respect the sovereignty and international law, freedom of navigation and overflight, and sustainable development. The revival of the Quadrilateral Security Dialogue, aimed at curbing China’s influence in the region, risks further damaging already strained relations between Canberra and Beijing. China is Australia’s biggest export destination and worsening relations could harm Australia’s export-dependent miners.

Having a look at aussie/dollar, in the medium-term, the price completed three consecutive green weeks, with low volatility after the rebound on the 0.7410 support level on May 9.

A worse-than-expected figure could create a downward pressure for the pair and would retest the 0.7475 support level in the daily timeframe. In case of a penetration of this area, the bullish retracement could come to an end and hit the 11-month low of 0.7410. The next support is coming from the 0.7325 barrier, taken from the low on May 2017.

If the employment report surpasses the consensus, then the price could create a rally until the 0.7675 strong resistance level in case of a jump above the 23.6% Fibonacci retracement level of the downleg from 0.8135 to 0.7410, around the current market price of 0.7585. Slightly above this area, the price could meet the 38.2% Fibonacci near 0.7690. In addition, a break above the aforementioned obstacle could open the door towards the next immediate resistance of the 50.0% Fibonacci of 0.7770.

GOLD: Faces Price Hesitation

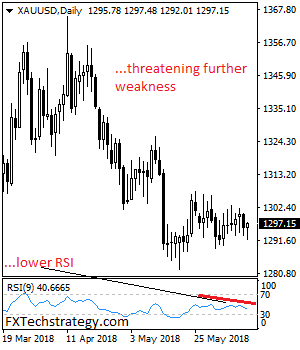

GOLD: The pair still faces price consolidation risk as it looks for directional moves. On the downside, support comes in at the 1,290.00 level where a break will turn attention to the 1,280.00 level. Further down, a cut through here will open the door for a move lower towards the 1,270.00 level. Below here if seen could trigger further downside pressure targeting the 1,260.00 level. Conversely, resistance resides at the 1,310.00 level where a break will aim at the 1,320.00 level. A turn above there will expose the 1,330.00 level. Further out, resistance stands at the 1,340.00 level. All in all, GOLD looks to break out of its consolidation range.

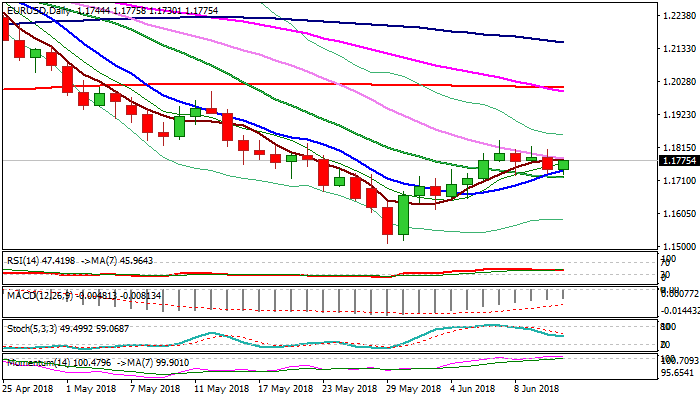

EURUSD Outlook: Stands at the Front Foot and Extends Recovery ahead of Fed

The Euro hits new session high in early US session trading on Wednesday, on extension of bounce from daily low at 1.1730, posted in late Asian session, where thick rising 4-hr cloud contained dips.

The single currency rallied despite weaker than expected EU IP data (Apr -0.9% vs -0.5% f/c and 0.6% in Mar) and returned above 10SMA (1.1740) which was cracked on short-lived dip to 1.1730.

Break and close above 30SMA (1.1781) which capped upside attempts in past four days, is needed to provide relief and shift near-term focus higher.

More likely scenario sees Euro lower on hawkish Fed, with upticks seen as positioning.

Bearish scenario requires close below 1.1721/13 pivots (20SMA/Fibo 38.2% of 1.1509/1.1839), to generate fresh bearish signal which could be boosted by dovish ECB tomorrow, for extension towards 1.16 zone.

Res: 1.1781; 1.1809; 1.1839; 1.1850

Sup: 1.1730; 1.1713; 1.1674; 1.1652