Sample Category Title

Dollar ignores strong PPI as focus turns to FOMC

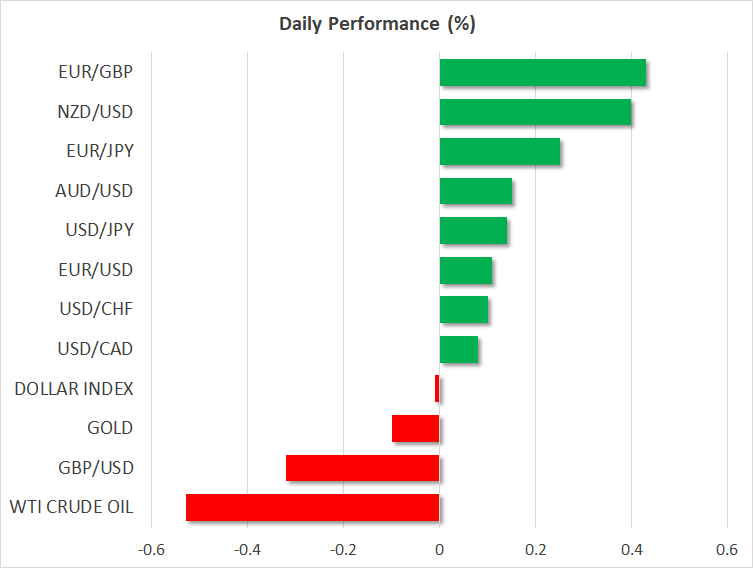

Dollar ignores stronger than expected PPI reading and is trading down against all but Sterling and Yen for the day.

Headline PPI rose 0.5% mom, 3.1% yoy in May, versus expectaiton of 0.2% mom, 2.8% yoy. Core PPI rose 0.3% mom, 2.4% yoy, versus expectation of 0.2% mom, 2.3% yoy.

Focus will now turn to FOMC rate decision today. Fed is widely expected to raise federal funds rate by 25bps to 1.75-2.00%. Voting will be the first thing to watch even though it will very likely be unanimous. Fed will also release updated economic projections.

Here are some previews

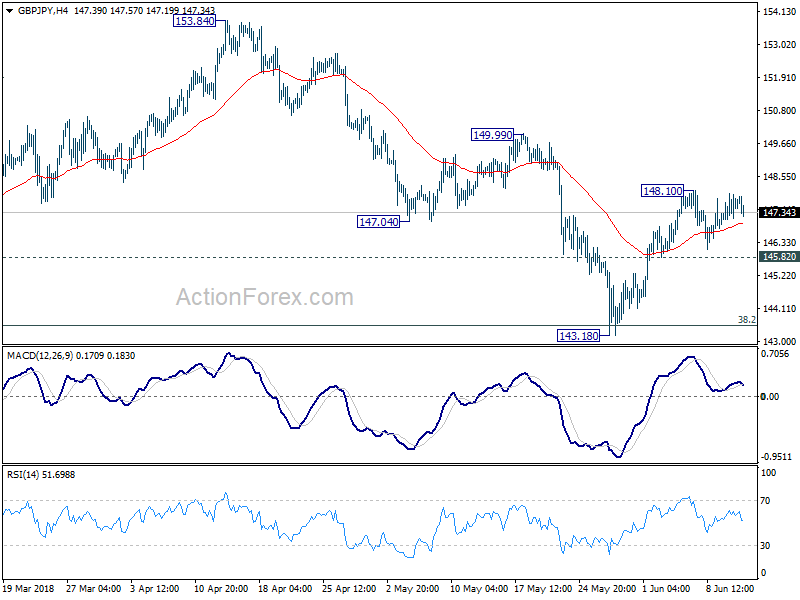

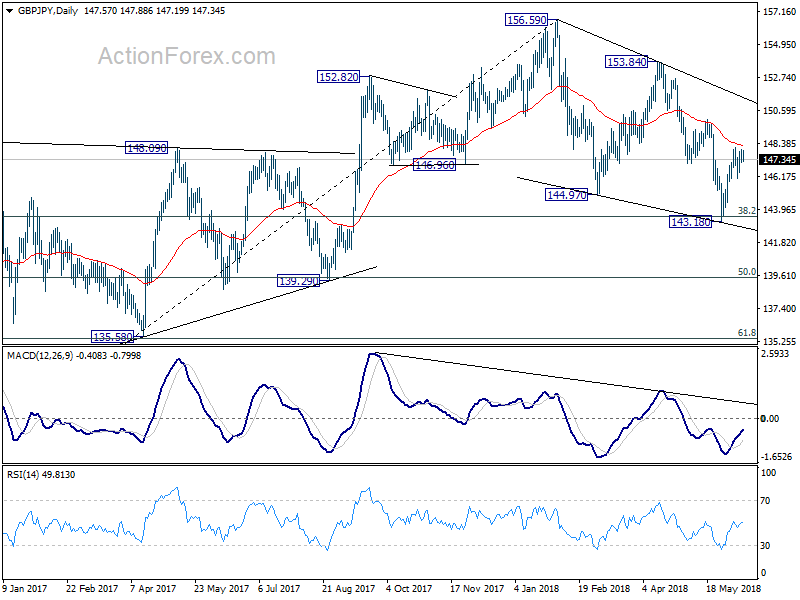

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.15; (P) 147.57; (R1) 148.03; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the upside, above 148.10 will resume the rebound from 143.18 and target 149.99, and then 153.84 resistance. However, break of 145.82 minor support will argue that the rebound from 143.18 is completed and bring retest of this low.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

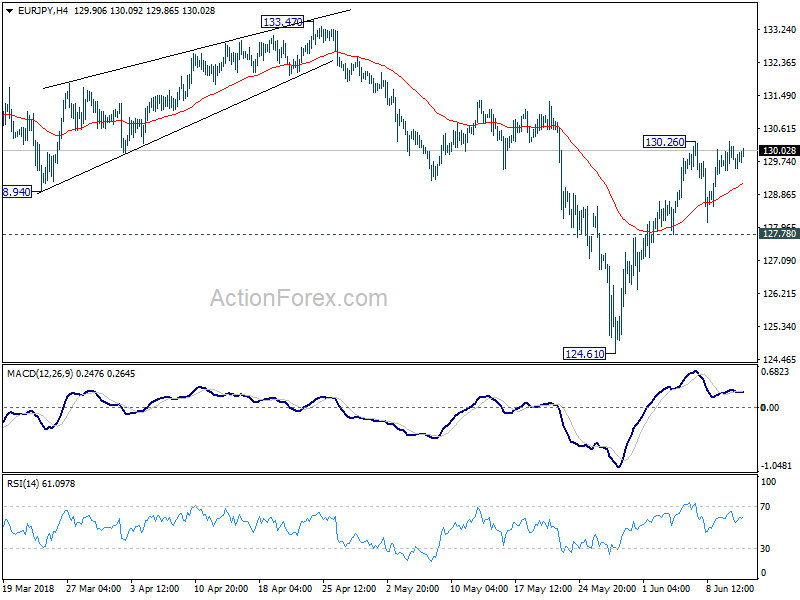

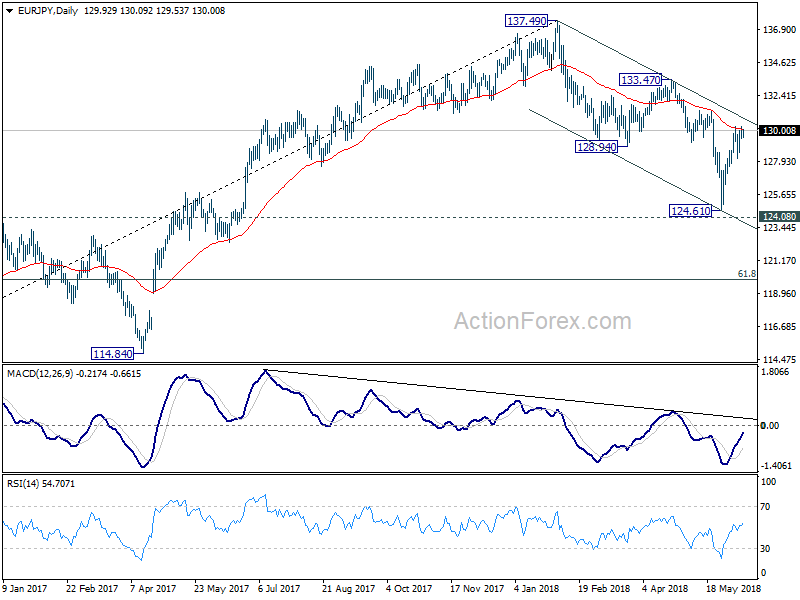

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.33; (P) 129.80; (R1) 130.11; More....

Intraday bias in EUR/JPY remains neutral for the moment. On the upside, above 130.26 will resume the rebound form 124.61 and target 133.47 key near term resistance next. On the downside, however, break of 127.78 minor support will indicate completion of the rebound from 124.61. Intraday bias will be turned back to the downside for 124.61 first.

In the bigger picture, despite rebounding strongly ahead of 124.08 resistance turned support, there was no clear follow through buying. Note again that there is bearish divergence in daily MACD. Firm break of 124.08 will confirm trend reversal. That is, whole rise from 109.03 (2016 low) has completed at 137.49 already. In that case, deeper fall should be seen back to 61.8% retracement of 109.03 to 137.49 at 119.90 and below. Nonetheless, decisive break of 133.47 key resistance will likely extend the rise from 109.03 through 137.49 high.

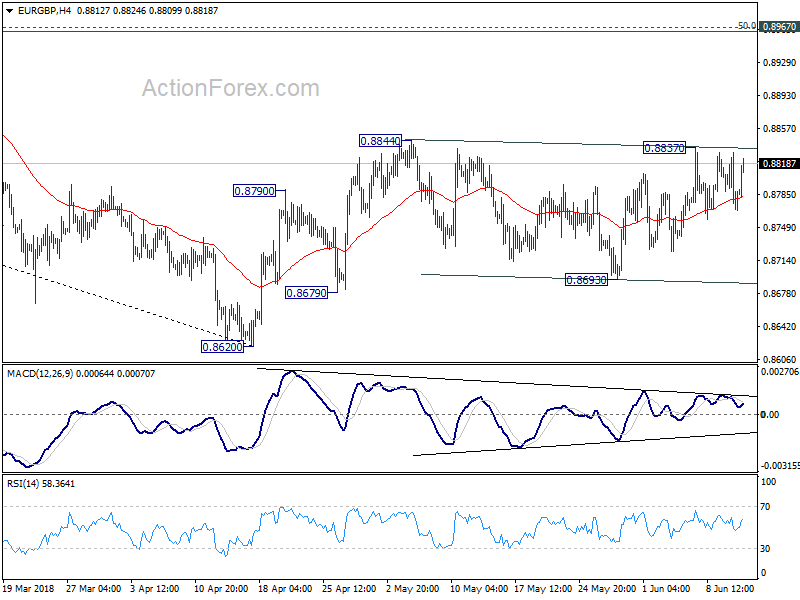

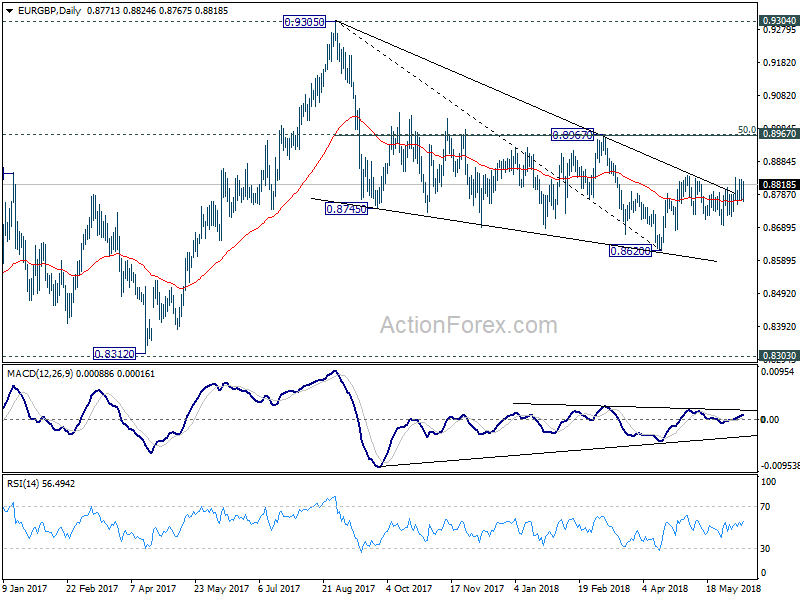

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8757; (P) 0.8796; (R1) 0.8821; More...

Intraday bias in EUR/GBP remains neutral as it's stuck in rage of 0.8693/8844. Another rise is expected as long as 0.8693 support holds. Break of 0.8844 will resume the rebound from 0.8620 for 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8693 will bring deeper fall back to retest 0.8620 low.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

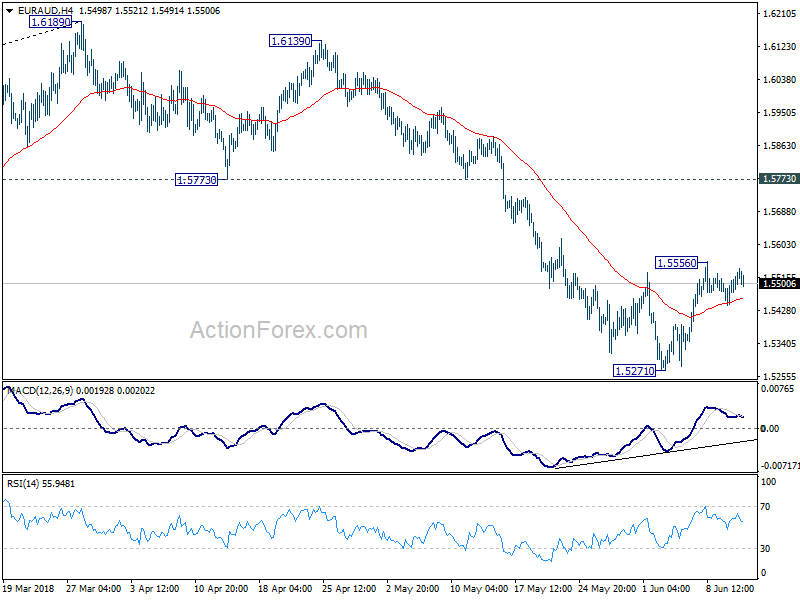

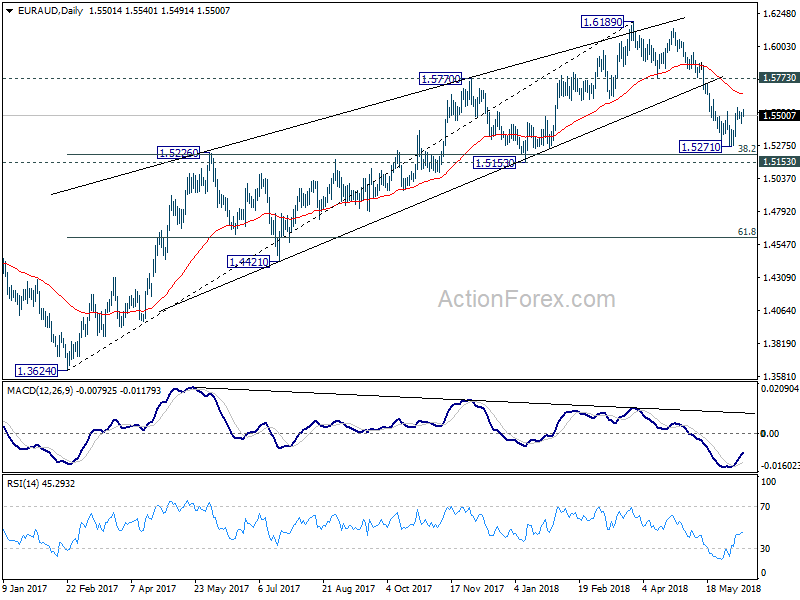

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5458; (P) 1.5489; (R1) 1.5537; More....

Intraday bias in EUR/AUD remains neutral for the moment. Corrective rise from 1.5271 could still extend. But upside should be limited below 1.5773 support turned resistance and bring fall resumption. On the downside, break of 1.5271 will extend the fall from 1.6189 to 1.5153 next.

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further decline is expected in medium term, even in case of strong rebound.

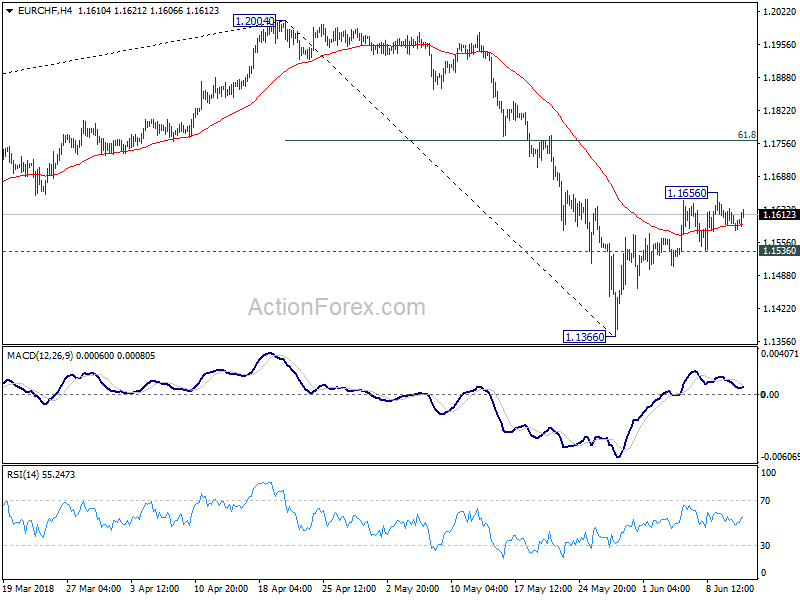

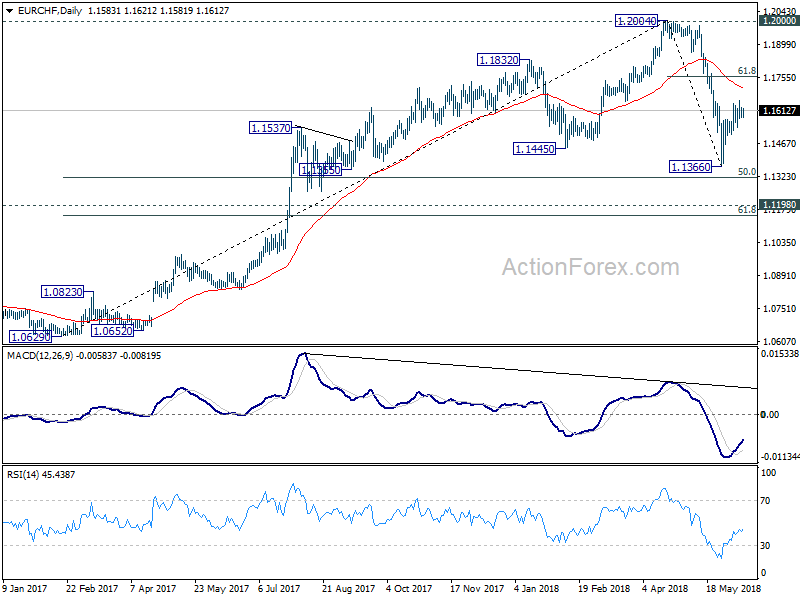

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1570; (P) 1.1599; (R1) 1.1618; More....

Intraday bias in EUR/CHF stays neutral for the moment. And, with 1.1536 minor support intact, further rise is mildly in favor to 61.8% retracement of 1.2004 to 1.1366 at 1.1760. But after all, the corrective pattern from 1.2004 is expected to extend with at least one more falling leg. Hence, we'll look for reversal signal again above 1.1760. On the downside, break of 1.1505 will suggest that the rebound is completed. And intraday bias will be turned back to the downside for retesting 1.1366.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

DAX Moves Higher Ahead Of Fed Rate Announcement

The DAX index has posted gains in the Wednesday session. Currently, the DAX is at 12,898, up 0.44% on the day. On the release front, Eurozone employment change edged up to 0.4%, above the estimate of 0.3%. Eurozone industrial production declined 0.9%, weaker than the forecast of -0.6%. In the U.S, the Federal Reserve is expected to raise the benchmark rate by a quarter-point. On Thursday, Germany releases CPI and the ECB is expected to maintain rates at a flat 0.0%.

All eyes are on the Federal Reserve, which is expected to raise rates by a quarter-point at its policy meeting on Wednesday. The odds of a quarter-point move stand at 96% percent, according to the CME Group. Although a rate hike has been priced in by the markets, such a significant move could still boost the stock markets. Investors are still uncertain whether the Fed will raise rates three or four times in 2018. Fed policymakers seemed divided on this question, and the rate statement could provide clues about future monetary policy.

Central banks will be in the spotlight this week, with rate statements from the Federal Reserve on Wednesday and the ECB on Thursday. The Fed is widely expected to raise rates, with odds of a quarter-rate hike at 94%. Although the rate increase has been priced in, the U.S dollar could still make some gains against its major rivals. In Europe, the ECB will be looking for any clues with regard to the ECB’s asset-purchase program. Currently, the bank is purchasing EUR 30 billion/mth, and the scheme is scheduled to wind up in September. However, some ECB policymakers want to phase out the program slowly, rather than turn off the tap completely in September. ECB chief economist Peter Praet recently said that the ECB board members would conduct a detailed discussion about the fate of the stimulus package at the June meeting. Mario Draghi will likely make mention of the program at his press conference, so we could see some movement in the stock markets on Thursday.

Dollar Hits Fresh 3-Week Highs Ahead Of FOMC Rate Decision

Here are the latest developments in global markets:

FOREX: Sterling dipped towards a 1-week low of 1.3310 against the US dollar on Wednesday (-0.20%) after CPI figures out of the UK missed slightly expectations on a yearly basis, coming at 2.4% instead of 2.5% analysts forecasted. Dollar/yen reached a 3-week high of 110.71 (0.15%) before the two-day FOMC policy meeting concludes later today, which will give hints on how many more rate hikes are in the Fed's radar. The dollar index, which measures the dollar's strength against a basket of six major currencies, edged up by 0.04% to 93.89. Euro/dollar rose by 0.18% despite industrial production in the Eurozone easing more than expected. Thursday's ECB policy meeting remains the main event for the euro as investors are eagerly waiting for policymakers to give direction on the quantitative easing program which expires in December. No rate hikes, though are anticipated at this meeting. The antipodean currencies are moving higher with aussie/dollar adding 0.17% to its performance to 0.7582, while kiwi/dollar advancing by 0.34% to trade at 0.7037. Dollar/loonie climbed by 0.06% to 1.3020. Also, dollar/lira returned to gains over the last couple of days, surging by 1.30% today to 4.6530.

STOCKS: Most of the European stocks opened in positive territory on Wednesday ahead of the Federal Reserve rate decision. The pan-European STOXX 600 jumped by 0.22% as miners and tech companies led a broad advance and the blue-chip Euro STOXX 50 was up by 0.17%. The German DAX 30 climbed by 0.16%, while, the French CAC 40 gained 0.28%. Moreover, the Italian FTSE MIB rose by 0.23% while the UK's FTSE 100 advanced by 0.22%. However, the Spanish IBEX 225 retreated by 0.05%. The US stock future indices were pointing to a positive open.

COMMODITIES: Oil prices dived after an industry report showed US stockpiles expanded. Moreover, sources stated today that Saudi Arabia was considering several plans for higher OPEC output, raising speculation that a supply hike could be possible at the OPEC's policy meeting next week. West Texas Intermediate (WTI) crude oil decreased by 0.15% to $66.26 per barrel and Brent declined by 0.25% to $75.69 per barrel, the lowest in a week. In precious metal developments, gold prices fell by 0.11% to $1,294.76.

Day ahead: FOMC rate decision takes center stage; Australian employment figures to move aussie

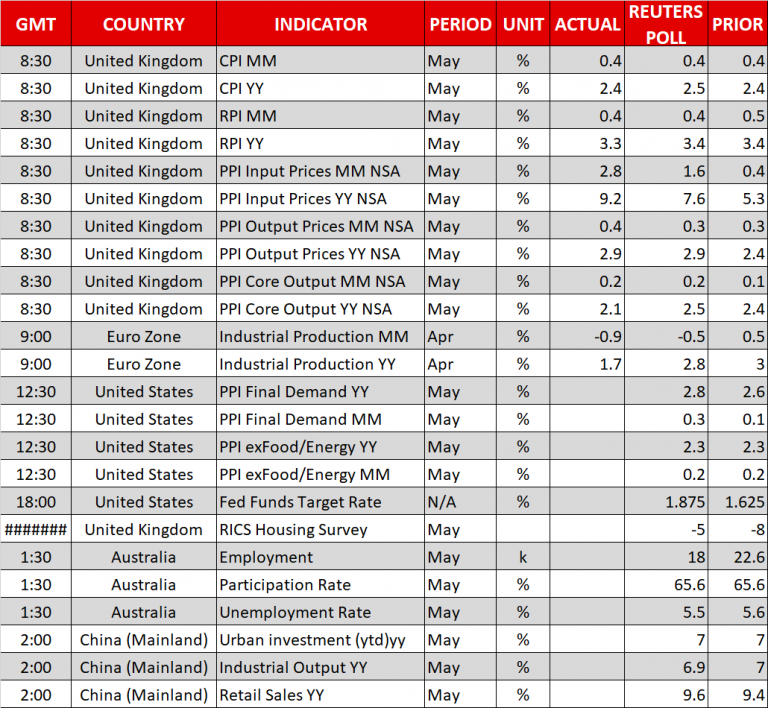

Wednesday's economic calendar will feature PPI figures out of the US later in the day, though the conclusion of the two-day FOMC policy meeting will be the main headline.

At 1800 GMT in the US, the Federal Open Market Committee will announce its decision on interest rates, providing the reasoning behind it through its policy statement. Analysts are widely expecting the central bank to lift interest rates by 25bps to 2.0%, completing the second rate hike this year, and at the same time remaining globally at the forefront of the move to reduce monetary stimulus. Since the rate rise has been already fully priced in the markets, the focus will switch to the rate statement and the central bank's fresh economic projections, while at 1830 GMT, all eyes will turn to the Fed chairman, Jerome Powell's press conference. Should policymakers back a positive outlook – probably citing recent upbeat economic numbers – hinting the Fed could feel more comfortable to become more aggressive in the future, dollar bulls could push even further towards the 111 round level versus the yen. On the other hand, concerns over US's trade relations with its closest allies are not unlikely to keep policymakers cautious over future economic trends. The famous dot plot, which displays where interest rates will head in the next few years according to projections made by Fed policymakers, will also gather a great amount of attention.

Before the FOMC meeting comes to an end, however, US PPI figures for the month of May will have the potential to move the dollar. Expectations are for the measure to rise from 2.6% y/y to 2.8%, while in the absence of volatile components such as food and energy, producer price growth is anticipated to stand flat at 2.3%.

In energy markets, the Energy Information Administration will deliver its weekly report on US oil inventories at 1430 GMT. Analysts believe that crude oil stocks have declined by 2.74 million barrels in the week ending June 8 after rising by 2.07mn in the preceding week. Gasoline and distillate stocks are projected to continue to rise but at a slower pace relative to the previous week.

In other data in focus, UK's RICS house price index will come under review at 2300 GMT, while on Thursday at 0130 GMT, Australia will see the release of employment stats. Particularly, it would be interesting to see whether the unemployment rate has slipped back to 5.5% in May after inching up to 5.6% in April. The numbers are also forecast to show a slowdown in job creation, with analysts expecting the number of jobs to have risen by 18k compared to 22.6k seen previously. In case the data prove encouraging, aussie/dollar could extend today's rebound from an almost two-week low of 0.7555 before the Chinese industrial production and retail sales due at 0200 GMT bring fresh volatility to the pair.

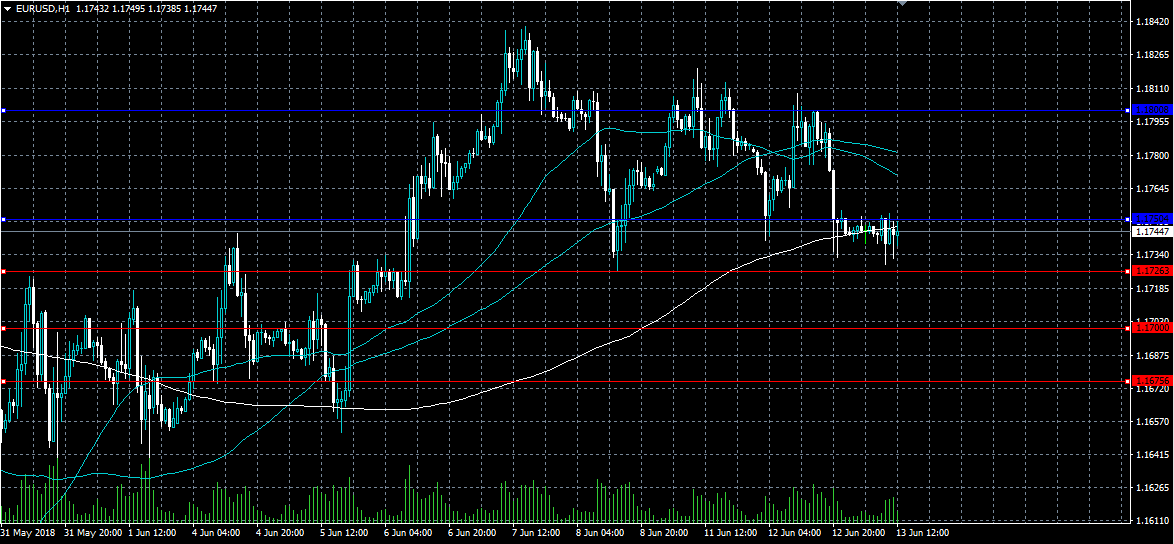

EURO Still Bearish Below 1.1750 Level

The euro currency has fallen towards the weekly price-low against the US dollar, as the greenback strengthens ahead of the FOMC rate decision later today. The EURUSD pair currently trades around the 1.1745 level, as dip-buyers push price back towards the 1.1750 level. Euro traders now await key monetary policy decisions from the FED and the ECB over the coming trading session.

The EURUSD pair remains intraday bearish while trading below the 1.1750 level. Key support is located at the 1.1700 and 1.1675 levels.

If the EURUSD pair moves above the 1.1750 level, buyers are likely to test towards the 1.1800 and 1.1839 resistance levels.

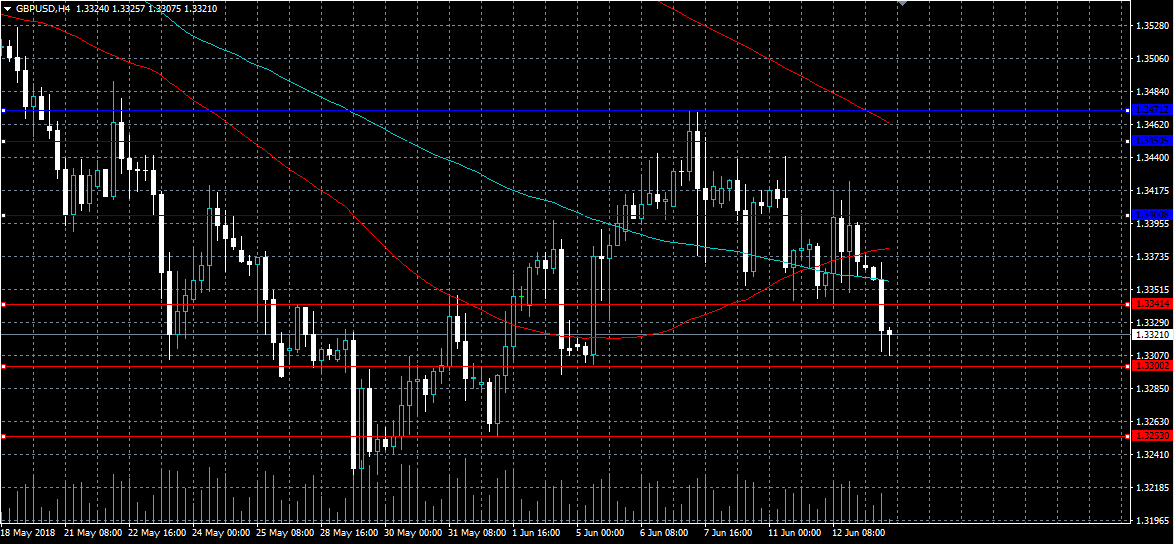

GBPUSD Strongly Bearish Below 1.3300

The British pound has fallen to a fresh weekly trading-low against the US dollar, following the release of key United Kingdom CPI Inflation data. The GBPUSD pair currently trades around the 1.3320 level and remains under technical selling pressure while price trades below the 1.3341 level. Sterling traders will look for further weakness below the 1.3300 support level as the key FOMC rate decision approaches.

The GBPUSD pair is strongly bearish while trading below the 1.3300 level, key technical support is now located at the 1.3253 and 1.3200 levels.

If the GBPUSD pair holds above the 1.3300 level, buyers may test towards the 1.3341 and 1.3400 resistance levels.