Sample Category Title

Sunset Market Commentary

Markets:

Global core bond trading was subdued today ahead of tonight’s FOMC meeting. Both the German and US yield curves flattened, anticipating the next steps in the normalization/tightening cycle of the ECB and the Fed. Changes on the US yield curve ranged between +0.8 bps (2-yr) and -0.6 bps (30-yr). German yield changes vary between +0.2 bps (2-yr) and -1.7 bps (30-yr). Intraday trading was erratic. Disappointing EMU industrial production data were expected following weak national prints earlier this/last week. US Treasuries made another shy attempt to move lower on higher than expected PPI data. The headline reading rose by 3.1% Y/Y in May, the fastest pace since the end of the 2011. The core measure accelerated to 2.4% Y/Y. Most investors remain side-lined though ahead of the Fed. Many uncertainties remain even if a 25 bps rate hike to1.75%-2% is discounted. Changes to the Fed’s communication strategy are possible. Will the Fed still label current policy as accommodative or do we enter “neutral” conditions? If so, will “neutral” be interpreted as dovish (time to slow tightening cycle) or hawkish (time to get from neutral to restrictive)? The Fed also ponders the possibility to do a press conference after every meeting. New growth, CPI and unemployment forecasts will be monitored as well. The list of variables to monitor is long which could make any market impact less outspoken with several items cancelling each other out. We hold our long term negative view on US Treasuries. Any gains of the US Note future in case of a dovish interpreted message might prove to be short-lived.

USD. As could have been expected, FX investors were mostly side-lined ahead of this evening’s Fed policy decision. The dollar was rather well bid overnight in Asia, but couldn’t maintain its positive momentum. EUR/USD settled in a rather tight range in the mid 1.17 area. The US currency even lost a few ticks early in US dealings. USD/JPY showed a similar picture. The pair set an intraday top near 110.70 but is also losing a few ticks. We expect a rather hawkish assessment (dots indicating two additional rate hikes in 2018). This might be USD supportive short-term. Especially USD/JPY might profit. The picture for EUR/USD is more diffuse as the ECB is also expected to signal a less easy policy tomorrow. We expect any EUR/USD decline to remain modest. In a MT perspective, we maintain the view that a further decline of EUR/USD below the 1.1510 support won’t be easy.

GBP. Today, sterling still showed a weak momentum. Yesterday, UK PM May avoided a defeat in a vote on amendments to the ‘Brexit withdrawal bill’. However, any positive impact on sterling was short-lived as the division within PM May’s Conservative Party isn’t solved at all. Tensions will probably resurface in coming weeks, maybe even in coming days. Today, UK May CPI data were close to expectations (2.4% Y/Y headline; 2.1% Y/Y core) but remained soft. The BoE shouldn’t feel pressured to raise rates anytime soon. The UK currency was already captured in a gradual intraday down-move ahead of the inflation data and lost a few more ticks afterwards. EUR/GBP is changing hands in the 0.8820 area. The ST range top of 0.8843 is again within reach. Early softness in cable was modestly reversed this afternoon as the USD lost slightly ground across the board (currently 1.3345 area).

News Headlines:

PM Theresa May has confirmed it was forced yesterday into promising a major concession to pro-EU lawmakers which could give parliament a greater say over the exit deal Britain negotiates with the EU. Today, Ian Blackford (leader of the Scottish National Party) was thrown out of the chamber by the Commons speaker. He refused to sit down while demanding a new debate on Scotland’s input for brexit negotiations.

Italy’s new finance minister, Giovanni Tria, has cancelled a trip to Paris to meet his French counterpart, Bruno Le Maire, as the diplomatic dispute concerning immigration policy escalated.

Factory output decreased by 0.9% in the euro zone in April from March, which was more than the expected decrease of 0.7%. These weak output numbers confirm other indicators that the economy in the euro zone is slowing. It also shows the difficult decision that has to be taken by ECB this Thursday on how to exit the APP.

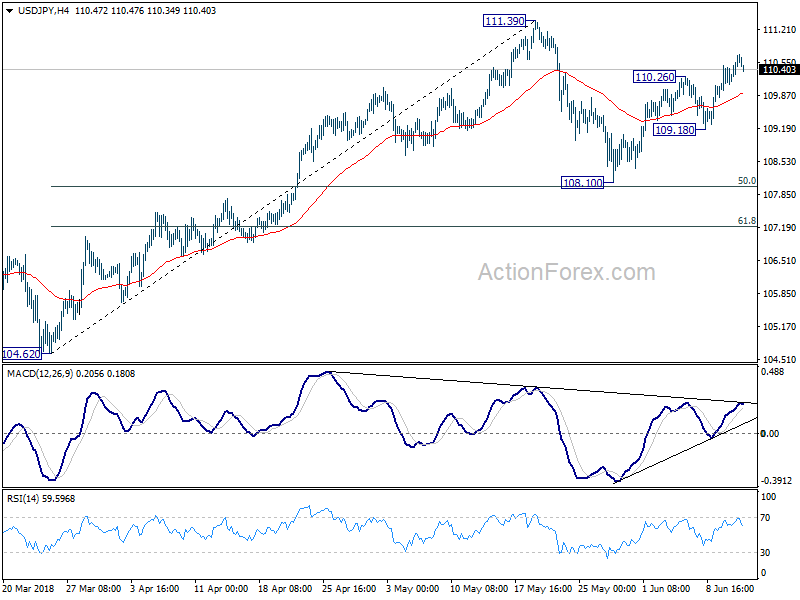

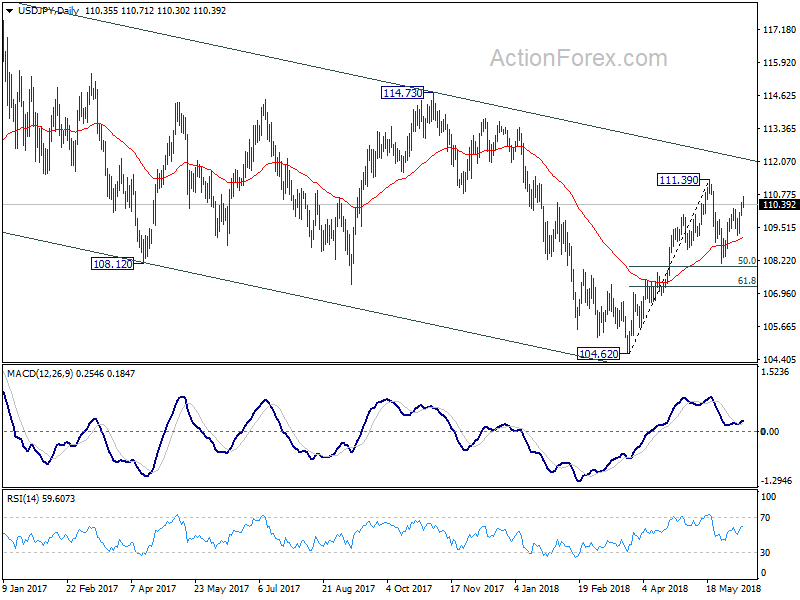

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.06; (P) 110.28; (R1) 110.58; More...

USD/JPY retreats mildly after hitting 110.71. But intraday bias stays on the upside for 111.39 resistance. Break there will resume the whole rebound from 104.62. On the downside, break of 109.18 will extend the consolidation from 111.39 with another decline towards 108.10 support.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

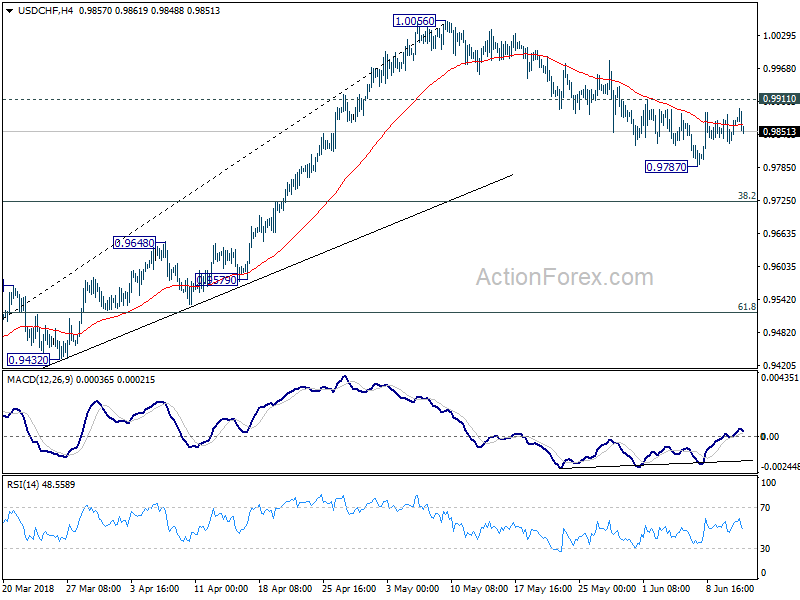

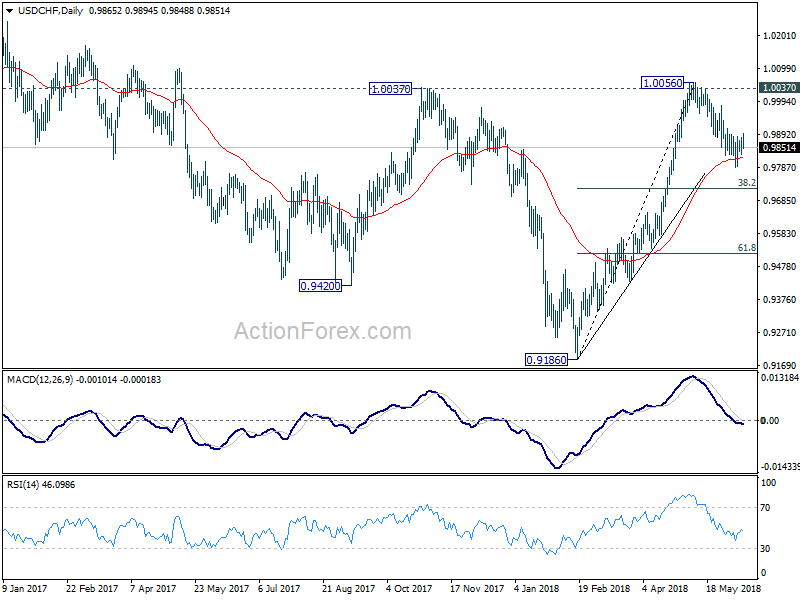

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9837; (P) 0.9861; (R1) 0.9891; More...

USD/CHF is still staying in tight range of 0.9787/9911 and intraday bias stays neutral at this point. On the upside, break of 0.9911 minor resistance will suggest that the corrective pull back from 1.0056 is already completed. Intraday bias would then be turned back to the upside for retesting 1.0056 first. On the downside, below 0.9787 will extend the correction. But we'd expect strong support from 0.9724 fibonacci level to contain downside and bring rebound.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

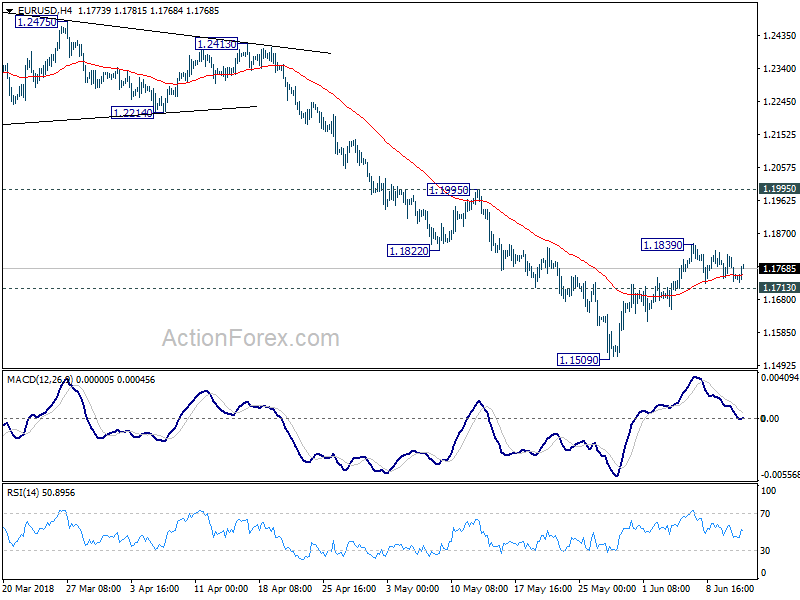

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1716; (P) 1.1762 (R1) 1.1792; More.....

EUR/USD continues to be bounded in tight range below 1.1839. Intraday bias remains neutral for the moment. On the downside, break of 1.1713 minor support suggest completion of the correction fro 1.1509. Intraday would be turned back to the downside to resume larger fall from 1.2555, through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447. In case of another rise, upside should be limited by 1.1995 resistance to bring reversal.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

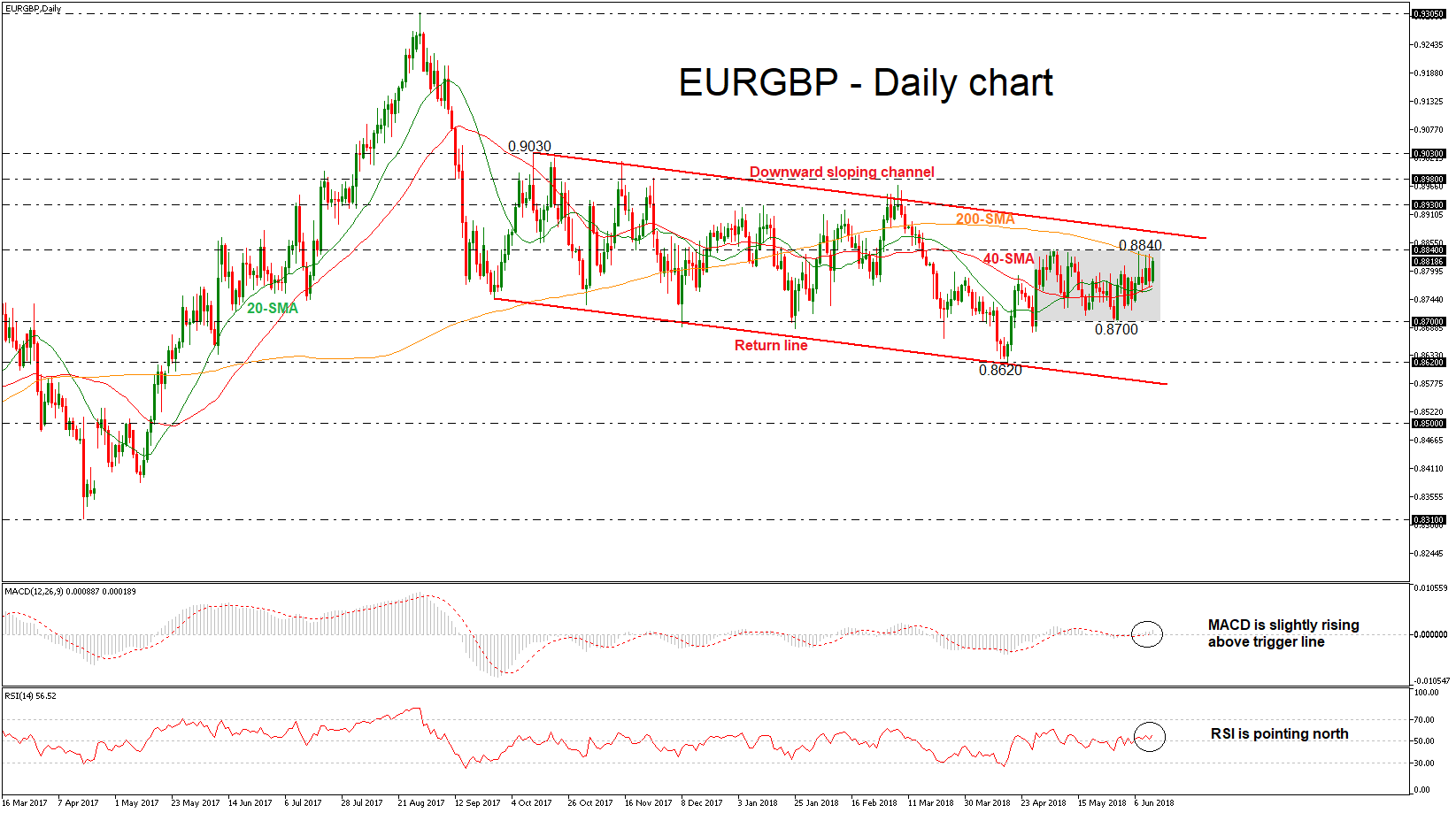

EURGBP Finds Strong Resistance at 200-SMA; Holds in Trading Range in Short Term

EURGBP has remained in a trading range in the short-term over the last one-and-a-half month with upper boundary the 0.8840 resistance level and lower boundary the 0.8700 handle. The price has found strong obstacle at the 200-simple moving average (SMA) in the medium-term as it has been developing below it since the beginning of March.

From the technical point of view, in the daily timeframe, the price is moving well above the 20- and 40-day SMAs, while the technical indicators hold above their neutral levels. The RSI indicator is pointing up and it has managed to cross into positive territory above the 50 level. Also, the MACD oscillator is slightly strengthening its momentum in the bullish area.

Strong gains could drive the price towards the next immediate resistance level of 0.8840, which stands above the 200-SMA. In case of a run above the aforementioned level, the price could touch the upper boundary of the downward sloping channel, near 0.8880. In case of further upside pressure, the pair could penetrate the channel to the upside and drive EURGBP towards the 0.8930 barrier.

On the flip side, an immediate support level is likely to come from the 20- and 40-SMAs, both near 0.8770 which has proved a strong resistance area in the past. A break below that could lead prices near the 0.8700 handle. Further losses could push the pair until the 0.8620 support.

In the bigger picture, the pair remains in a slightly downward-tilting channel, which has been in place since September 2017.

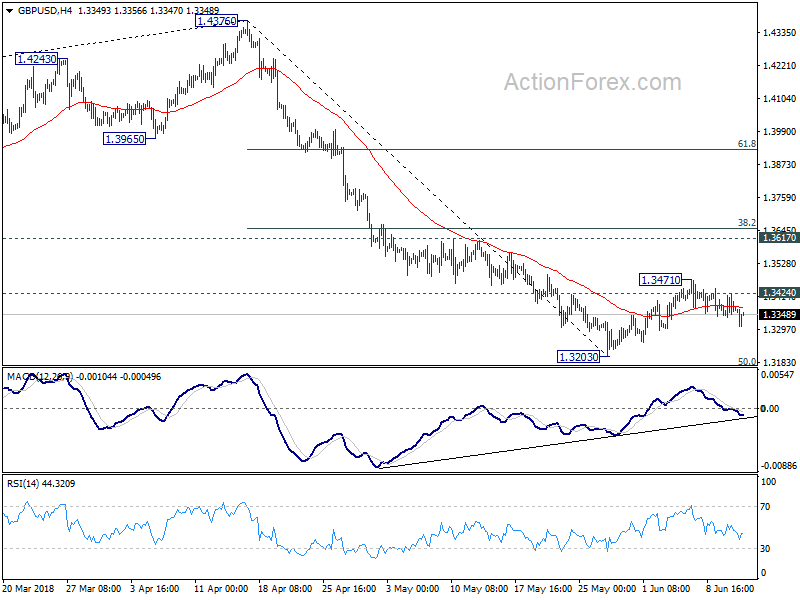

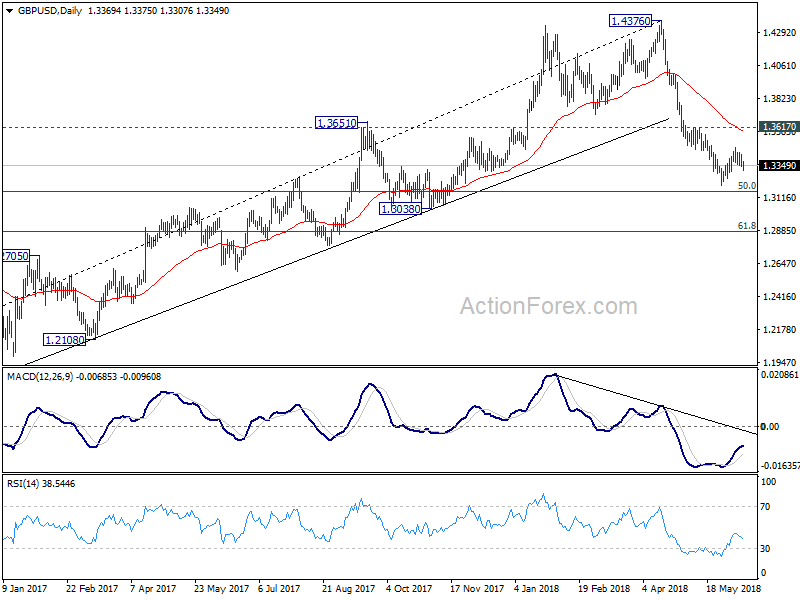

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3333; (P) 1.3379; (R1) 1.3416; More...

GBP/USD drops to as low as 1.3307 so far today. Break of 1.3341 minor support indicate completion of corrective rise from 1.3203. Intraday bias is now on the downside for 1.3203. Break will resume the fall from 1.4376 to 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next. Nonetheless, above 1.3424 minor resistance will extend the corrective rise through 1.3471 before completion.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3617 resistance holds, even in case of strong rebound.

Dollar Soft as Markets Look Through Strong PPI to FOMC, Pound Lower on CPI Miss

Dollar is trading in soft tone in range against most major currencies except versus Yen and Sterling. The greenback shrugs off stronger than expected PPI as markets are awaiting FOMC rate hike, economic projections and press conference. Sterling is trading as the weakest one today as headline UK CPI missed market expectations. But loss is limited so far. Yen is following as the second weakest. Meanwhile, New Zealand Dollar and Euro are the strongest one for today.

US Headline PPI rose 0.5% mom, 3.1% yoy in May, versus expectation of 0.2% mom, 2.8% yoy. Core PPI rose 0.3% mom, 2.4% yoy, versus expectation of 0.2% mom, 2.3% yoy. Focus will now turn to FOMC rate decision today. Fed is widely expected to raise federal funds rate by 25bps to 1.75-2.00%. Voting will be the first thing to watch even though it will very likely be unanimous. Fed will also release updated economic projections. The statement, as usual, will be scrutinized.

Awaiting FOMC, a look at Fed's March projections

Currently, Fed fund futures are pricing in 75% chance of a hike in September 2.00-2.25%, but less than 50% chance for December hike to 2.25-2.50%. But market pricing could change drastically based on revision to Fed's economic forecasts. To recap, back in March, Fed projected growth to be at 2.7% in 2018, to slow to 2.4% in 2019 then 2.0% in 2020. Unemployment rate is projected to be at 3.8% in 2018, dropped to 3.6% in 2019 and stay there in 2020. That is, Fed only expected the tax cut to have temporary boost to the economy. And based on recent economic data, Fed is not too likely to change these projections.

Headline CPI is projected to be at 1.9% in 2018, 2.0% in 2019 and 2.1% in 2020. Core CPI is projected to be at 1.9% in 2018, rise to 2.1% in 2019 and stay there in 2020. Headline PCE was already at 2.0% in April and core CPE at 1.8%. There is chance of an upgrade in inflation forecasts. And if Fed does, it would be Dollar positive.

Finally, and most importantly, Fed projects policy rate to be at 2.1% at the end of 2018, 2.9% in 2019 and 3.4% in 2020. That is, one more hike only this year, and three more next. Any chance to this set of figures could trigger strong reactions in the greenback.

Fed's March projections:

More on FOMC

- FOMC Preview – Fed's Rate Hike A Done Deal, Focus Turned to Forward Guidance

- FOMC Meeting: Rate Hike A 'Done Deal' But What About Inflation?

- Dollar Firm as Rate Hike Imminent; But Will Fed also Raise Rate Path Forecast?

Pound dips as UK CPI unchanged at 2.4% yoy, missed expectations

Sterling dips notably as UK consumer inflation data missed expectation. Headline CPI was unchanged at 2.4% yoy in May, below consensus of 2.5% yoy. Core CPI was also unchanged at 2.1% yoy, met expectations. RPI dropped to 3.3% yoy, down from 3.4% yoy and missed expectation of 3.4% yoy. But the pressure on the Pound is relatively mildly. While the set of inflation data doesn't give BoE any push to hike in August, it doesn't give a lot of reasons for BoE to wait. So, the MPC members and the markets would probably need another month of data before making up their mind.

PPI input was at 2.8% mom, 9.2% yoy, versus expectation f of 1.7% mom, 7.0% yoy, and prior 0.6% mom, 5.6% yoy. PPI output was at 0.4% mom, 2.9% yoy, versus expectation of 0.3% mom, 2.9% yoy, and prior 0.4% mom, 2.5% yoy. PPI output core was at 0.2% mom, 2.1% yoy, versus expectation of 0.1% mom, 2.2% yoy, and prior 0.2% mom, 2.0% yoy. UK House price index rose 3.9% yoy in April, below expectation of 4.4% yoy.

Also released in European session, Eurozone industrial production dropped -0.9% mom in April versus expectation of -0.5% mom. Eurozone employment rose 0.4% in Q1 versus expectation of 0.3% qoq. Swiss PPI rose 0.2% mom, 3.2% yoy in May versus expectation of 0.2% mom, 3.2% yoy.

RBA Lowe: Any increase in interest rates, they're some time away

RBA Governor Philip Lowe delivered a speech titled "Productivity, Wages and Prosperity" today. There he pointed out that "over the past couple of years, output growth has been subdued, but employment growth has been strong." And, it's productivity that's holding the economy back. Low pointed to strong employment growth in household services, but output per hour worked was only 4% higher than it was in 2010. In contrast, the output per hour worked was up 13% to 16% in other industry groups.

He urged "strong ongoing focus on training, education and the accumulation of human capital" to bring up the overall productivity. And he emphasized that "our national comparative advantage will increasingly be built on the quality of our ideas and our human capital."

Regarding monetary policy, Lowe said the economy is "moving in the right direction" and the next move in interest rate will be "up, not down". But, "the environment in which interest rates are increasing is also likely to be one in which people's incomes are growing more quickly than they are now."And, "any increase in interest rates, however, still looks to be some time away."

Also released, Australia Westpac consumer confidence rose 0.3% in June.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3333; (P) 1.3379; (R1) 1.3416; More...

GBP/USD drops to as low as 1.3307 so far today. Break of 1.3341 minor support indicate completion of corrective rise from 1.3203. Intraday bias is now on the downside for 1.3203. Break will resume the fall from 1.4376 to 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next. Nonetheless, above 1.3424 minor resistance will extend the corrective rise through 1.3471 before completion..

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3617 resistance holds, even in case of strong rebound..

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Jun | 0.30% | -0.60% | ||

| 07:15 | CHF | Producer & Import Prices M/M May | 0.20% | 0.10% | 0.40% | |

| 07:15 | CHF | Producer & Import Prices Y/Y May | 3.20% | 3.20% | 2.70% | |

| 08:30 | GBP | CPI M/M May | 0.40% | 0.40% | 0.40% | |

| 08:30 | GBP | CPI Y/Y May | 2.40% | 2.50% | 2.40% | |

| 08:30 | GBP | Core CPI Y/Y May | 2.10% | 2.10% | 2.10% | |

| 08:30 | GBP | RPI M/M May | 0.40% | 0.40% | 0.50% | |

| 08:30 | GBP | RPI Y/Y May | 3.30% | 3.40% | 3.40% | |

| 08:30 | GBP | PPI Input M/M May | 2.80% | 1.70% | 0.40% | 0.60% |

| 08:30 | GBP | PPI Input Y/Y May | 9.20% | 7.00% | 5.30% | 5.60% |

| 08:30 | GBP | PPI Output M/M May | 0.40% | 0.30% | 0.30% | 0.40% |

| 08:30 | GBP | PPI Output Y/Y May | 2.90% | 2.90% | 2.70% | 2.50% |

| 08:30 | GBP | PPI Output Core M/M May | 0.20% | 0.10% | 0.10% | 0.20% |

| 08:30 | GBP | PPI Output Core Y/Y May | 2.10% | 2.20% | 2.40% | 2.00% |

| 08:30 | GBP | House Price Index Y/Y Apr | 3.90% | 4.40% | 4.20% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | -0.90% | -0.50% | 0.50% | |

| 09:00 | EUR | Eurozone Employment Q/Q Q1 | 0.40% | 0.30% | 0.30% | |

| 12:30 | USD | PPI M/M May | 0.50% | 0.20% | 0.10% | |

| 12:30 | USD | PPI Y/Y May | 3.10% | 2.80% | 2.60% | |

| 12:30 | USD | PPI Core M/M May | 0.30% | 0.20% | 0.20% | |

| 12:30 | USD | PPI Core Y/Y May | 2.40% | 2.30% | 2.30% | |

| 14:30 | USD | Crude Oil Inventories | -1.4M | 2.1M | ||

| 18:00 | USD | FOMC Rate Decision (Upper Bound) | 2.00% | 1.75% | ||

| 18:00 | USD | FOMC Rate Decision (Lower Bound) | 1.75% | 1.50% | ||

| 18:30 | USD | FOMC Press Conference |

Canadian Dollar Steady as Markets Await Fed Rate Hike

The Canadian dollar is subdued in the Wednesday session. Currently, USD/CAD is trading at 1.3019, up 0.03% on the day. On the release front, there are no Canadian events. PPI is expected to rise to 0.3% and Core PPI is forecast to remain pegged at 0.2%. The Federal Reserve is expected to raise the benchmark rate by a quarter-point. On Thursday, the U.S will release retail sales reports and unemployment claims, and Canada publishes a housing inflation report.

It’s been a quiet day for the Canadian dollar, but that could change after the Federal Reserve meets on Wednesday. The Fed is widely expected to raise rates to a range between 1.75% and 2.0%. The odds of a quarter-point move stand at 96% percent, according to the CME Group. Although a rate hike has been priced in by the markets, such a significant move could boost the US dollar against its rivals. Investors are still uncertain whether the Fed will raise rates three or four times in 2018. Investors will be paying close attention to the rate statement and the “dot-plot” forecasts, looking for any clues regarding rate hikes in the second half of 2018. The Fed is currently projecting a total of three hikes this year, but a strong economy and rising inflation have raised speculation that the Fed could raise rates four times in 2018.

The Singapore Summit was a milestone, as it marked the first time that leaders of the United States and North Korea met face-to-face. However, the joint statement put out by Presidents Trump and Kim was short on details, which could explain a lack of movement in the currency markets following the summit. The joint statement reaffirmed North Korea’s full commitment to complete denuclearization, but there was no mention of a timetable or any verification mechanisms. Even if the summit was largely symbolic, there’s no denying that tensions have significantly eased and that the summit could mark a first step in bringing peace to the Korean peninsula.

Dollar Waits for Fed Rate Decision, Lira Crumbles

The major event risk across financial markets today will be the Federal Reserve policy meeting, which is widely expected to conclude with interest rates being hiked by 25 basis points.

With a rate hike in June considered a done deal, investors may be more concerned with the economic projections and press conference with Fed Chair, Jerome Powell. Markets are poised to closely scrutinize the Fed’s monetary policy statement for clues on how fast the Fed may raise interest rates during the second half of this year. With inflation jumping to a six-year high in May and the US economic outlook being encouraging, it will be interesting to see if there is an upgrade to the “dot-plot” forecasts. If the Federal Reserve expresses optimism over the health of the US economy and offers fresh insight into rate hike timings beyond June, this could be viewed as hawkish by market players.

Traders will also closely scrutinize Mr. Powell’s comments for any signs of inflation fears returning, or that trade tensions have impacted monetary policy. Expectations over the Fed raising rates more frequently could be heightened if Powell announces that he will be holding news conferences after every policy meeting.

In regards to the technical picture, the Dollar Index remains firmly bullish on the daily charts with 94.00 acting as a level of interest. A solid breakout above this level could trigger a jump towards 94.30.

Turkish Lira tumbles ahead of FOMC

A growing sense of anxiety over Turkey’s looming presidential and parliamentary elections next week has left the Lira vulnerable to downside risks.

Heightened expectations over the Federal Reserve tightening monetary policy simply added to the Lira’s woes, with the local currency tumbling across the board today. With high inflation fears and political instability in Turkey likely to continue haunting investor attraction towards the Lira, currency weakness could remain a recurrent market theme.

Focusing purely on the technical picture, the USDTRY is currently following a positive trajectory on the daily charts. Prices have scope to punch above 4.700 if the Lira continues to depreciate.

Commodity spotlight – Gold

Gold drifted slightly lower ahead of the Federal Reserve meeting this evening, which is expected to conclude with the announcement of an interest rate increase.

For an extended period, the yellow metal has bounced within a range, with $1300 acting as a psychological pivotal point. Price action continues to suggest that Gold needs a fresh directional catalyst to make its next significant move. A US interest rate increase in June, coupled with expectations of further rate hikes during the second half of the year could spell trouble for zero-yielding Gold.

Focusing on the technical picture, investors will continue closely observing how prices behave around the $1300 level. A breakout above $1300 could trigger an incline towards $1324. Alternatively, a failure for bulls to conquer $1300 is likely to result in a decline back to $1280.

Awaiting FOMC, a look at Fed’s March projections

Fed is widely expected to raise federal funds rate by 25bps to 1.75-2.00%. Fed fund futures are pricing in 96.3% chance of that and there is no way for Fed to disappoint.

The main question is on firstly, whether Fed in on course for another hike in September. And, would Fed hike the fourth time this year in December? Fed fund futures are pricing in 75% chance of a hike in September 2.00-2.25%, but less than 50% chance for December hike to 2.25-2.50%.

Market pricing could change drastically based on revision to Fed's economic forecasts. To recap, back in March, Fed projected growth to be at 2.7% in 2018, to slow to 2.4% in 2019 then 2.0% in 2020. Unemployment rate is projected to be at 3.8% in 2018, dropped to 3.6% in 2019 and stay there in 2020. That is, Fed only expected the tax cut to have temporary boost to the economy. And based on recent economic data, Fed is not too likely to change these projections.

Headline CPI is projected to be at 1.9% in 2018, 2.0% in 2019 and 2.1% in 2020. Core CPI is projected to be at 1.9% in 2018, rise to 2.1% in 2019 and stay there in 2020. Headline PCE was already at 2.0% in April and core CPE at 1.8%. There is chance of an upgrade in inflation forecasts. And if Fed does, it would be Dollar positive.

Finally, and most importantly, Fed projects policy rate to be at 2.1% at the end of 2018, 2.9% in 2019 and 3.4% in 2020. That is, one more hike only this year, and three more next. Any chance to this set of figures could trigger strong reactions in the greenback.

Fed's March projections: