Sample Category Title

FOMC Raises Funds Rate Target, Alters Forward Guidance

The Fed raised the funds rate in June and added a fourth rate hike this year while upgrading its outlook for GDP and inflation. The Fed dropped guidance that the funds rate will stay below the long term rate for a while.

Policy Driver: Lower Unemployment Rates

For the FOMC, the decline in the unemployment rate below 4 percent (top graph) signals future upward pressure on inflation, therefore supporting continued fed funds rate increases. But how many?

In the current economic expansion, the decline in the unemployment rate has not been matched by an anticipated increase in measured inflation. The simple unemployment-inflation link has been broken by changes in demographics (declining labor force participation rates) and the globalization of the labor market. In addition, inflation, and thereby inflation expectations, have lowered the incentive of workers to seek higher wages to offset inflation, while having limited the ability of firms to offset higher wages by passing them on via higher consumer prices.

For decision makers, the decline in the unemployment rate has not been an effective tool for forecasting inflation. Moreover, the FOMC itself has regularly lowered its measure of the natural unemployment rate, effectively following the labor market decline in the unemployment rate while waiting for inflation to accelerate.

Inflation Overshoot: Tolerable – Yet Risky

As illustrated in the middle graph, the FOMC's benchmark inflation rate is expected to exceed its 2 percent long-term inflation target by 2019. Our estimate is that the PCE deflator will be above target starting in the second half of this year.

For the FOMC, they are comfortable with the overshoot and argue that their inflation target is symmetric around 2 percent. But will the economy and markets tolerate that? The persistence of above 2 percent inflation will have to be priced into short-term debt instruments even if the market and FOMC believe that the long-run target for inflation remains at 2 percent. For now, the spread between the benchmark 30-year and 10-year Treasury yields reinforce the belief that markets are okay with FOMC actions. However, there is a risk that the longer the FOMC tolerates above-target inflation, the more likely that markets will believe that the FOMC will have the courage to rein in inflation sometime in the future.

Dot-Plot: Realistic Given the Economy?

For the FOMC, the way ahead for the funds rate is clear, with steady rate increases in 2018, 2019 and 2020. We are skeptical. Our outlook is that the FOMC has given us a very linear projection in the fed funds rate through 2020, while also pursuing shrinkage in its balance sheet. Given the recent increases in auto and credit card delinquency rates, there is evidence of growing financial strains on mid-to-lower-credit households that may weaken overall economic growth into 2020. Linear projections in a cyclical economy do not raise our level of confidence. Source: FRB, U.S. Department of Labor, U.

FOMC Raises the Fed Funds Rate to Range of 1¾ to 2 Percent

As was widely expected, the Federal Open Market Committee (FOMC) raised its federal funds target rate range by 25 basis points to between 1¾ and 2 percent.

The statement noted solid economic growth, declining unemployment and a pickup in household spending. The relatively upbeat assessment was reflected in upgraded near-term economic forecasts and lower expectations for the unemployment rate:

- The median projection for real GDP growth in 2018 rose to 2.8% (from 2.7%) and was unchanged thereafter.

- The median unemployment rate forecast fell to 3.6% in 2018 (from 3.8% previously) and to 3.5% in 2019 and 2020 respectively (from 3.6% previously). Nonetheless, there were no changes to the long-term rate, believed to be around 4.5% (though the overall range fell a tenth of a percentage point on both the low and high end to 4.1% to 4.7%).

- On inflation, the median estimate for core PCE inflation rose to 2.1% in 2018 and 2019 up from 1.9% and 2.0%, respectively.

- The median expectation for the federal funds rate target rose to 2.4% (from 2.1%) and to 3.1% (from 2.9%) in 2019, suggesting that the median expectation is for two more rate hikes this year (one higher than indicated in the previous statement). Expectations for the federal funds rate target were unchanged for 2020 and the longer run.

Key Implications

The Fed raised interest rates by 25 basis points but lowered the word count on its policy statement by 100 words (about a quarter). Most of the cut was related to forward guidance, with the statement no longer including the note that "the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run." On balance, this suggests a somewhat more hawkish tone from the Committee.

The Committee's confidence in its normalization path was further confirmed in the edging up of its expectations for rate hikes this year coupled with the firming in its expectations for economic growth, inflation, and lower unemployment.

Notably, the Fed has kept its expectations for the longer run unemployment rate at 4.5%, currently a full percentage point above its projection for 2020. The fact that the FOMC sees very little overshoot in inflation (just one tenth above its 2.0% target) suggests that it is confident that its policy path, which will bring the federal funds rate 50 basis points above its longer-run expectation, will be sufficient to keep inflation close to target.

Fed Raises Rates, Drops Forward Guidance in Pared Down Statement

Highlights:

- The target range for the fed funds rate was raised by 25 basis points to 1.75-2.00% in a unanimous decision.

- Growth and inflation projections for 2018 were revised slightly higher while the unemployment rate is expected to be even lower than previously forecast.

- The ‘dot plot’ was little changed, though consensus edged up to four total rate hikes this year from three previously.

- The committee took note of accelerating Q2 growth (activity now rising at a “solid” rate vs. “modest” previously), stronger household spending, and a recent decline in the unemployment rate.

- They also dropped an earlier comment that market-based measures of inflation compensation remain low—a change we thought could have been made in May. Instead, the statement focuses on stability in longer-term inflation expectations.

- Chairman Powell announced he’ll be conducting press conferences after all eight FOMC meetings starting in January.

Our Take:

Today’s rate hike was fully expected but changes to the accompanying policy statement and economic projections gave Fed watchers plenty to analyze. Those changes leaned hawkish and sent both the US dollar and interest rates higher. Most significantly the Fed dropped their forward guidance that rates will remain below neutral “for some time.” The committee consensus also shifted to seeing four total rate hikes as appropriate this year, up from three previously. But Chairman Powell downplayed these changes in his press conference, noting that the Fed’s policy outlook hasn’t changed. Dropping forward guidance is simply a reflection that rates are now closer to neutral, and changes to the dot plot were admittedly minor. Powell’s comments trimmed back some of the initial market moves.

So what to make of the changes? For now we think the Fed’s tightening cycle will remain in cruise control. Aside from a pause in Q3/17 to announce a change in their balance sheet policy, the central bank has now raised rates once per quarter since the end of 2016. And for good reason—decades-low unemployment, above-trend hiring and GDP growth, and inflation around 2% all indicate the time for highly-accommodative monetary policy has passed. With the fed funds rate remaining around 100 basis points below neutral, it’s hard to see the pace of tightening slowing in the near term. But as today’s statement showed, we are nearing the time for a discussion on how much further rates will need to rise to keep inflation in check. With plenty of fiscal stimulus being thrust upon an at-capacity economy, monetary policy arguably needs to become somewhat restrictive over the medium term. Our forecast assumes quarterly rate hikes will continue next year, pushing the fed funds rate above most estimates of the neutral rate.

Back to the Drawing Board

Despite a hawkish Fed hike last night the USD failed to rally. Without reading too much into the usual FOMC exercise in verbal gymnastics. The USD dollar couldn’t find a grip above near-term resistance after US 10 year Treasuries could not break above 3 % when Chair Powell reminded markets the economy is far from overheating which suggests the Fed will remain very much data dependent with inflation metrics top of the list reinforcing an all too familiar Fed narrative. But with the ECB looming this afternoon, traders were happy to book profit knowing all too well that they are probably in for the usual topsy-turvy session when Draghi and Company take centre stage. The ECB is more challenging to handicap, and there is the chance, however remote, for a hawkish surprise.

Equity markets

The US benchmarks closed near session lows. Equity markets don’t like rate hikes especially when the FOMC guidance comes in a bit more aggressive than expected. But with the US-China trade deadline looming June 15, that too is contributing to a bit of risk off momentum in early APAC trade as traders are nimbly shifting into some haven hedges, JPY -Gold and US bonds.

Oil markets

WTI has surged over 60 cents on the back of the DoE weekly inventory data. After the API data on Tuesday, the market was pricing in a minimal build but was slapped with a massive draw that was conclusively more bullish than the API print. According to the tale of the tape higher crude runs, increased exports and lower imports that were more than enough to offset a further 0.1 million barrels per day increase in estimated crude oil production to a record 10.9million barrels per day.

The unexpectedly large draw has caught the markets by surprise causing yet another positioning whipsaw. But, as we have seen all week given the uncertainty over likely production increases and record US shale output, top side remains in check.

Lots of discussions centred on the review provisions on the OPEC agreement and whether Russia and Saudi will use this mechanism to phases out production cuts. Even more so after OPEC June report said inventories had fallen by 26 million barrels below the 5-year average. The original OPEC/Russia production cuts were supposed to get inventories back to the 5-year average. AS they say, the devil is in the details.

Interesting timing as we could find out more on this issue after tonight’s Saudi Arabia vs Russia World Cup match as the Saudi Crown Prince and Russian President meet in Moscow to watch the game

Gold Markets

The weaker US dollar and falling equity markets are providing a boost to gold prices. While the FOMC added another dot to the policy equation, but with the committee remaining ever so data dependent suggesting a 4th rate hike in 2018 is far from a lock, the USD dollar gave up all its overnight gains and some. Equity market hates higher interest rates and so should gold markets, but see some decent bids this morning as investors are nimbly entering some haven hedges as tomorrow US-China trade deadline looms ominously. Indeed, the stakes are running high.

Currency markets

Well, it’s back to the drawing board courtesy of the elusive US inflation narrative.

EUR: Too difficult to handicap and with the EUR anchoring at 1.1730 overnight after a ” hawkish ” fed hike. And to guard against the possible hawkish shift from the ECB, traders are unwinding EUR shorts.

JPY: NO joy on the upside after US rates yielded when Powell highlighted the lack of inflation as worrisome. And with risk aversion factoring in ahead of tomorrow important US-China trade deadline, the slate is clean waiting for a better read on Trade and Tariff and US interest rates.

MYR: While USDMYR came close to testing 4.0 after a hawkish FOMC USD dollar profit taking eased the pressure but currency traders now face an uncertain ECB.

Expect another lazy day on the local bond markets as investor remain side-line ahead of the ECB as investors remain glued to macro moves in the Global interest rate environment. But volumes remain tepid ahead of this week festive holiday which could see an added flurry of risk reduction ahead of tomorrow testy US-China trade deadline.

Hawkish Fed Boosts US Dollar But Tariffs Bring Currency Down to Earth

The US dollar is lower against major pairs after the U.S. Federal Reserve raised the benchmark Fed funds rate by 25 basis points on Wednesday. The move was heavily anticipated by the market, but the strong pace of the US economy could mean more rate hikes. The latest projections from the US central bank now have 8 Fed official forecasting four rate hikes in 2018. The USD gained as soon as the projections and the rate announcement were public, but there was a sudden retraction when the news of the Trump administration moving forward with tariffs on Chinese goods that could come as early as Friday. Fed Chair Jerome Powell was asked about his view on trade during the press conference following the FOMC statement but he choose to sidestep by mentioning that the Fed does not seek to play a role in trade policy.

- ECB could announce plans after end of QE

- List of Chinese goods under tariffs to be ready Friday

- Canadian Foreign Minister to visit Washington, DC on Thursday

**Dollar Vulnerable to Trade War **

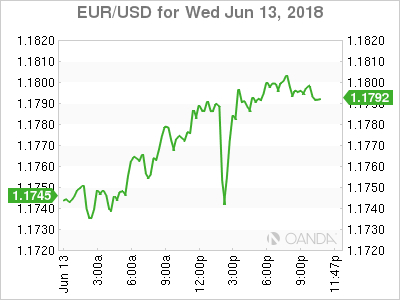

The EUR/USD gained 0.39 percent on Wednesday. The single currency is trading at 1.1777 after the U.S. Federal Reserve lifted rates to the 175–200 basis points range as expected. While the market had anticipated the move the surprise came in the more hawkish projections and language used by the members of the FOMC. While awaiting for Fed Chair to deliver his prepared remarks and to field questions from the financial press a report that the Trump administration is finalizing a list of Chinese goods to be subject to additional tariffs hit the US dollar like a ton of bricks. The upward momentum from higher rates was lost as once again the US is ready to fire another shot in what seems an impending trade war.

The European Central Bank (ECB) will follow the lead from the U.S. Federal Reserve and is expected to tighten monetary policy. The central bank could start laying out their exit strategy after its massive QE program comes to an end. The market forecasts a tapering from the 30 billion euros a month down to zero in early 2019. The ECB has not validated that estimate, and could potentially wait until its July meeting to outline its monetary policy plans.

Eurozone growth is slowing down and rising political uncertainty as evidenced by the formation of the Italian government will give the ECB food for thought. The central bank has already acted too fast with monetary policy only to be forced to undo those decisions. The hardest trick for ECB President Mario Draghi will be to end the QE program and avoid a resulting taper tantrum.

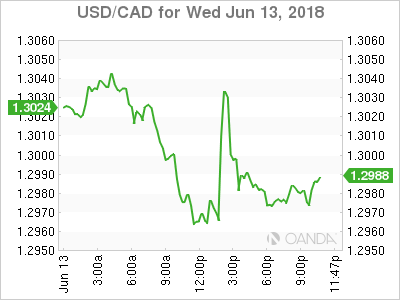

Canadian Dollar Rebounds After Fed Hike

The USD/CAD fell 0.20 percent in the last 24 hours. The currency pair is trading at 1.3003 after the U.S. Federal Reserve raised borrowing costs by 25 basis points. The pressure will now be on the Bank of Canada (BoC) to try to keep the rate gap from expanding further. The Canadian interest rate stands at 1.25 percent. The BoC will meet in July with a growing probably of a rate hike announcement.

The main headwind against the loonie has been the uncertainty about NAFTA. The trade agreement has been under constant threat as the Trump administrations has not show willingness to sit down and negotiate. The Foreign Affairs Minister Chrystia Freelander will meet with her counterpart Trade Representative Robert Lighthizer on Thursday. She has already met with the US Senate foreign relations committee. Trade is the obvious topic of discussion after the G7 meeting ended in a tense exchange as US President Donald Trump made its way to Singapore.

Oil prices surged with West Texas Intermediate trading at $66.63. US crude inventories came in way under expectations with a drawdown of 4.1 million barrels when a shortage of 1.4 million was forecasted. Crude reached a two week high despite the Energy Information Administration (EIA) publishing a report that shows US oil production is on the rise. Organization of the Petroleum Exporting Countries (OPEC) and Russian production has increased ahead of their talks in Vienna to review the supply cut agreement.

Market events to watch this week:

Wednesday, June 13

- 9:30pm AUD Employment Change

Thursday, June 14

- 4:30am GBP Retail Sales m/m

- 7:45am EUR Main Refinancing Rate

- 8:30am EUR ECB Press Conference

- 8:30am USD Core Retail Sales m/m

- 8:30am USD Retail Sales m/m

- Midnight JPY BOJ Policy Rate

- Midnight JPY Monetary Policy Statement

Friday, June 15

- Tentative JPY

- BOJ Press Conference

*All times EDT

Fed Raised Policy Rate in June. Two More to Come amidst Upbeat Economic Developments

Decided unanimously, FOMC raised the Fed funds rate by +25 bps to a range of 1.75-2.00%. In a technical adjustment, it also lifted the interest rate paid on required and excess reserve balances, by +20 bps, to 1.95% so as to maintain the trading in the fed funds market at rates well within the FOMC's target range. Certainly, the focuses are on the indication on the future rate hike path and economic projections. The members are more upbeat on the economic developments since the last meeting, noting “solid” growth, compared with “moderate” growth in the prior meeting. The staff upgraded the GDP growth forecast for this year and inflation outlook for this year and 2019. The median dot plot suggests 2 more rate hikes, one more than projected in the prior meeting.

Taking a look at the median dot plot, policymakers project the federal funds rate target to increase to 2.4% (from 2.1%) this year and to 3.1% (from 2.9%) in 2019, suggesting that the median expectation is for two more rate hikes this year. This marks one more hike than previously indicated. Expectations for the policy rate target were unchanged for 2020 and the longer run. Fed’s confidence at the current path of interest rate normalization is also exemplified in the accompanying statement, in which, as we had expected, the forward guidance is amended. In May, the Fed noted that “the economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data”. The reference is shortened a lot, only to emphasize that “further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee's symmetric 2% objective over the medium term”.

The more hawkish tone is supported up the buoyant developments since the last meeting. Intermeeting dataflow shows that economic activity has been rising at a “solid rate”, compared with a “moderate rate” in May. On employment, “the unemployment rate has declined”, compared with staying “low” in May. Meanwhile, the growth of household spending “has picked up”, compared with “moderated” in May. Indicators of longer-term inflation expectations are little changed, on balance. In the latest staff economic projections, GDP growth is expected to accelerate to +2.8% this year, up from +2.7% estimated previously. Growth forecasts remain unchanged thereafter. On inflation, the median estimate for core PCE inflation was upgraded to +2.1% in 2018 and 2019, up from +1.9% and +2%, respectively. Moreover, the median unemployment rate forecast was revised lower to 3.6% in 2018 (from 3.8% previously) and to 3.5% in 2019 and 2020, respectively (from 3.6% previously). The long-term rate stays unchanged at 4.5%.

The Fed has turned more hawkish. Yet, the degree of hawkishness appeared to have priced in before the meeting. As a result, the USD index initially climbed higher before retreating. The greenback was mixed against major currencies. The price action was also driven by Chair Jerome Powell’s comment at the press conference that “most participants did not revise their projections”. Probably he wanted to downplayed the more upbeat “dot plot".

Eco Data 6/14/18

[php_everywhere instance="1"]

Dollar jumps on hawkish Fed projections, four hikes in total this year

The new economic projections are rather hawkish.

Fed projects GDP to grow 2.8% in 2018, revised up from 2.7% in March projection. 2019 and 2020 GDP projections were unchanged at 2.4% and 2.0% respectively.

Unemployment rate is projected to be at 3.6% by the end of 2018, 3.5% In 2019 and 2020. There were clear downward revision from March projection of 3.8% in 208, 3.6% in 2019 and 2020.

Headline PCE projection was raised to 2.1% from 2018 to 2020. That compares to March projection of 1.9% in 2018, 2.0% in 2019 and 2.1% in 2020.

Core PCE projection was raised to 2.0% in 2018 and kept unchanged at 2.1% in 2019 and 2020. March projections predicted 1.9% in 2018, 2.1% in 2019 and 2020.

Most importantly, federal funds rate is projected to be at 2.4% by the end of 2018, revised up from 2.1%. That is, Fed is now leaning towards total of four rate hikes this year. Federal funds rate is projection to be at 3.1% at 2019, that is, around three hikes in 2019. 2020 projection was left unchanged at 3.4%, arguing that it could be close to the neutral rate of policy makers.

Dollar is lifted after the release but traders are probably awaiting press conference before jumping in.

Fed hikes federal funds rate to 1.75-2.00%, full statement

FOMC raised federal funds rate to 1.75-2.00% as widely expected. Statement below.

Federal Reserve Issues FOMC Statement

Information received since the Federal Open Market Committee met in May indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Job gains have been strong, on average, in recent months, and the unemployment rate has declined. Recent data suggest that growth of household spending has picked up, while business fixed investment has continued to grow strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy have moved close to 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee's symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-3/4 to 2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the FOMC monetary policy action were Jerome H. Powell, Chairman; William C. Dudley, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Loretta J. Mester; Randal K. Quarles; and John C. Williams.

(FED) Federal Reserve Issues FOMC Statement

Information received since the Federal Open Market Committee met in May indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Job gains have been strong, on average, in recent months, and the unemployment rate has declined. Recent data suggest that growth of household spending has picked up, while business fixed investment has continued to grow strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy have moved close to 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee's symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-3/4 to 2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the FOMC monetary policy action were Jerome H. Powell, Chairman; William C. Dudley, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Loretta J. Mester; Randal K. Quarles; and John C. Williams.