Sample Category Title

China Data Lower Than Expected

General Trend:

- Overall markets are trading lower, tracking late US session, absorbing Fed rate hike and increased expectations for future policy moves

- USD lower in the session, after several days of strength; bond yields also tracking slightly lower

- Trade tensions remain front and center as talk circulates that Trump will meet with advisers tomorrow in order to decided on China tariffs

- Australia employment changed registered lower than expected; though unemployment rate fell 0.1%; A$ weakened 0.2% on the data

- China data came in softer than expected, though NBS affirmed 2018 GDP of 6.5%. Also noted Cannot rule out possibility that China's firms rush to export in anticipation of trade war with US

- KRW opened for trade much lower against the dollar

- BOJ reduced purchases of 3-5 year JGBs

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.5%

- Subaru, 7270.JP May delay release report on improper testing - Nikkei

- (JP) Japan Investors Net Buying of Foreign Bonds: -¥488.5B v -¥1.66T prior week; Foreign Net Buying of Japan Stocks: -¥108.5B v -¥527.8B prior week

- (JP) Japan PM Abe considering summit with N. Korea Kim Aug/Sept - Japan press

- (JP) BoJ announcement related to daily bond buying operation: cuts 3-5-yr buying by ¥30B

Korea

- Kospi opened -0.7%

- (KR) South Korea analysts trade between the Koreas could be profitable but will require large amounts of investment - Korean press

- (KR) President Trump: Would love to have troops out of South Korea but its not an option right now; will talk to South Korea about them paying the US for troop presence

- (KR) North Korea Kim said to have promised to destroy Tongchang-Ri ICBM site - Korean press

- (KR) South Korea Vice Fin Min Ko: Do not expect large capital outflows due to rate gap with Fed; expects limited short term market impact from Fed

- (KR) Bank of Korea (BOK) Gov Lee: Today's Fed move will have limited impact on markets

- (KR) Sec of State Pompeo: suspending war games with South Korea requires productive talks with the North; wants to see major disarmament from North Korea in two years

- (KR) US Sec State Pompeo: South Korea President Moon said that South Korea will cooperate to implement agreement; Moon helped set foundation for Trump/Kim meeting

China/Hong Kong

- Hang Seng opened -0.1%, Shanghai Composite -0.4%

- (CN) Reportedly Pres Trump to meet with trade advisors tomorrow to decide whether to go ahead with China tariffs – press

- (CN) China PBOC Adviser: Cut to RRR is still necessary; Expect 2018 M2 growth to be higher y/y - China press

- (HK) Hong Kong Monetary Authority (HKMA) raises base rate 25bps to 2.25% (in line with Fed)

- (HK) HKMA Chief Chan: HK$ rates will follow US rate normalization; HK banks will eventually raise prime rates

- (CN) China PBoC Open Market Operation (OMO): Injects combined CNY150B in 7-day, 14-day and 28-day reverse repos v CNY130B prior: Net injects CNY70B v injects CNY70B prior;Leaves rates unchanged

- (CN) China PBoC sets yuan reference rate at 6.3962 v 6.4156 prior

- (CN) China PBOC Gov Yi Gang: China's economy is shifting to high quality development era; to use RRR and relending tools to support SMEs - speaking at forum

- (CN) CHINA MAY SURVEYED JOBLESS RATE: 4.8% V 4.9% PRIOR

- (CN) CHINA MAY INDUSTRIAL PRODUCTION Y/Y: 6.8% V 7.0%E; YTD Y/Y: % V 6.9%E

- (CN) China May Foreign Direct Investment (FDI) YTD y/y: 1.3% v 0.1% prior

- (CN) CHINA MAY RETAIL SALES Y/Y: 8.5% V 9.6%E; YTD Y/Y: 9.5% V 9.7%E

- (CN) China NBS Spokesperson: Confident of reaching 6.5% GDP in 2018. economy has continued with steady growth in H2

- (CN) China Banking and Insurance Regulatory Commission (CBIRC) Chairman Shuqing: Overall default ratio is very low compared to other countries; to appropriately deal with bond defaults

- (CN) China MOFCOM: China will push for a change in its exports pursuing size and speed to quality and efficiency

- (CN) China Securities Regulatory Commission (CSRC): Overseas investors have an obvious tendency to hold yuan assets, explains yuan strength against backdrop of weakness in some other currencies

- ZTE, 763.HK White House said to be working to prevent Congress from re-imposing penalties - US press

Australia/New Zealand

- ASX 200 opened 0.0%

- (AU) AUSTRALIA MAY EMPLOYMENT CHANGE: +12.0K V 19.0KE; UNEMPLOYMENT RATE: 5.4% V 5.5%E

- FCG.NZ NZ Commerce Commission believes method for calculating estimate of risk in the cost of financing milk processing operations is too low; creating a higher calculated milk price than competitors - NZ press

- Atlas Iron, [-19%], AGO.AU Gives update on North West Infrastructure: Got notice from WA Govt saying NWI does not have priority right to develop Stanley Point berths 3 &4 in Port Hedland

- (AU) Australia Jun Consumer Inflation Expectation: 4.2% v 3.7% prior

- (NZ) New Zealand sells NZ$200M v NZ$200M indicated in 2025 bonds; avg yield 2.6042%; bid to cover 2.13x

North America

- (US) FOMC RAISES TARGET RATE RANGE BY 25BPS TO 1.75-2.00% (AS EXPECTED)

- (US) FOMC UPDATED ECONOMIC FORECAST FOR JUNE MEETING (V. MAR): now forecasts 4 rate hikes in 2018; Raises Median forecast for end-2018 rate 2.375% (prior 2.125%)

- FOXA Comcast makes all-cash $35/shr proposal to acquire Twenty-First Century Fox after spinoff of "New Fox", values 21CF at $65B

- (US) FCC Chairman Pai said to be planning to vote on limits of TV station ownership at July 12th meeting; not clear on how he will propose changing it

Europe

- (UK) May RICS House Price Balance: -3% v -5%e

Levels as of 01:30ET

- Hang Seng -0.9%; Shanghai Composite -0.3%; Kospi -1.3%; Nikkei225 -0.7%; ASX 200 -0.2%

- Equity Futures: S&P500 +0.0%; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 -0.2%

- EUR 1.1788-1.1810; JPY 110.09-110.38; AUD 0.7553-0.7582;NZD 0.7016-0.7036

- Aug Gold +0.2% at $1,303/oz; Jul Crude Oil -0.0% at $66.62/brl; Jul Copper -0.5% at $3.24/lb

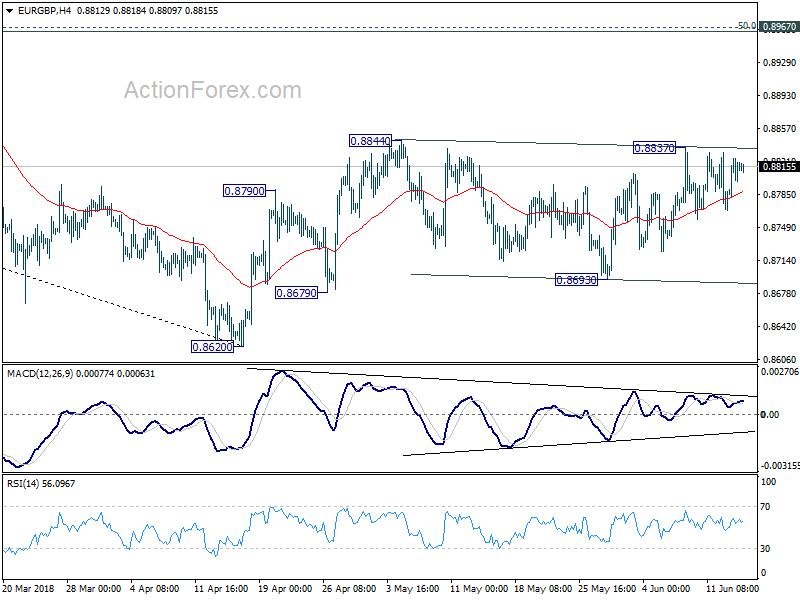

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8786; (P) 0.8807; (R1) 0.8835; More...

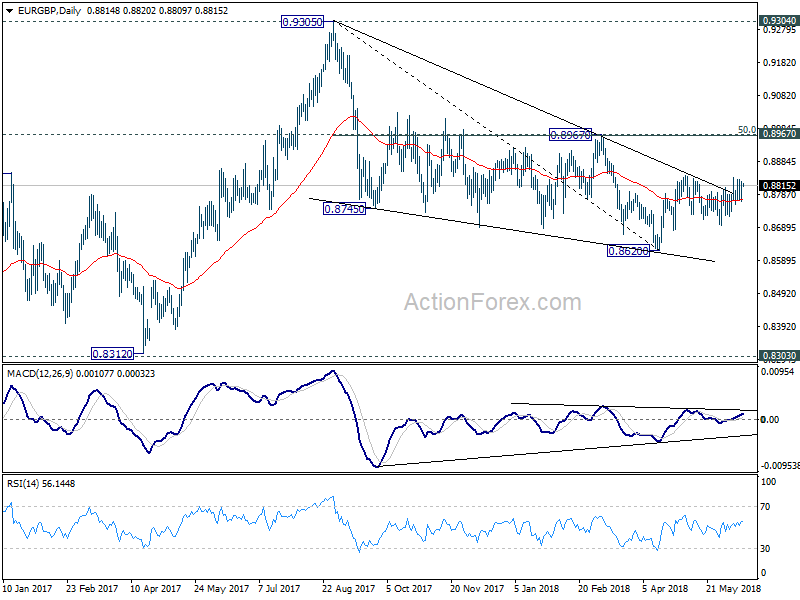

No change in EUR/GBP's outlook as it's bounded in range of 0.8693/8844. Intraday bias remains neutral at this point. Another rise is expected as long as 0.8693 support holds. Break of 0.8844 will resume the rebound from 0.8620 for 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8693 will bring deeper fall back to retest 0.8620 low.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Currencies: Dollar Doesn’t Profit From ‘Hawkish’ Fed. ECB To Propel The Euro?

- Rates: US Treasuries limit losses despite the Fed's message

The Fed hiked its policy rate to 1.75%-2% while median rate forecasts for 2018 and 2019 increased, suggesting a quarterly rate hike pace at least until mid-next year. Strong growth and a positive outlook support this scenario, while inflation is allowed to temporary move above the symmetric 2% target. US Treasuries took the news quiet well, limiting losses. - Currencies: Dollar doesn't profit from 'hawkish' Fed. ECB to propel the euro?

The dollar couldn't maintain modest gains yesterday as the Fed raised its policy rate. Powell also suggested that more is to come. The focus turns to the ECB today. The ECB will probably prepare markets for the end of APP at the end of this year. This symbolic move to policy normalization might support further euro gains.

The Sunrise Headlines

- The US equity markets reacted negatively to the Fed news, with the DOW JONES leading the pack lower (-0.47%). Asian markets follow the US example and open with losses of around -0.50%.

- The Federal Reserve has without surprise lifted rates by a quarter point to 1.75%-2% and signalled that two more interest rate hikes are expected in 2018. FED chairman Powell supported it with a bullish assessment of the US economy.

- China's new economic numbers indicate a slight setback in economic momentum. Retail Sales YoY (8.5%), Industrial Prodution YoY (6.8%) and Investment (6.1%) were below the expected the 9,6%, 7% and 7% in May.

- The US has released the list of products that it imports from China that will be targeted for tariffs, for a total value of $50bn. The move came despite China's pledge to buy $70bn in US farm and energy exports.

- Greece has accelerated it's reform debate to pass measures for receiving a final tranche of international bailout funds. It said to be preparing the country's exit of the stability support programme.

- Australia created 12k jobs in May (19k expected), mostly by increases in part time jobs (+32k). The RBA remains concerned with the only marginal increase in average wages and a high household debt to impose risks on its economy.

- The US will release its weekly update on Jobless Claims today together with its Retail Sales for May. In the UK the Retail Sales Ex Auto Fuel MoM/YoY (May) are given. In the EU, it is looking forward to ECB's announcements.

Currencies: Dollar Doesn't Profit From 'Hawkish' Fed. ECB To Propel The Euro?

Dollar doesn't profit from 'hawkish' Fed rate hike

The dollar traded with a cautious negative bias yesterday going into the Fed decision, with EUR/USD nearing 1.18. USD/JPY eased to the mid 110 area. The Fed as expected raised the Fed fund target range by 0.25%. The dots suggest two additional rate hikes this year and Fed's Powell remained positive on the economy. On the other hand, Powell reiterated that the inflation target is symmetric and that policy shouldn't react to short-term deviations from target. Yields and the dollar spiked temporary higher upon the Fed decision, but the gains couldn't be sustained. EUR/USD closed the session at 1.1791 (from 1.1745). USD/JPY finished the session little changed at 110.34 after a temporary post-Fed trip towards the 110.85 area.

Asian stocks mostly show moderate losses overnight. Disappointing Chinese data and a moderately hawkish Fed yesterday are weighing on regional markets. The dollar also fails to capitalize on yesterday's hawkish Fed message. EUR/USD returned to the 1.18 area. USD/JPY eases back to the low 110 area. The Aussie dollar continues trading soft (AUD/USD 0.7560 area) after mediocre Australian labour market data.

US retail sales and import prices will be published today. Retail sales are expected solid (0.4% M/M) and import prices will probably maintain an upward trajectory. However, a big surprise is probably needed to trigger a USD reaction with the Fed rate hike path more or less cemented. The dollar might be more sensitive to weaker rather than to strong data. Still, the focus will be on the ECB.. We expect the ECB to prepare markets to stop APP end of this year. This might cause a further repositioning in favour of the euro. Over the previous days, we held the working hypothesis that the downside of EUR/USD had become better protected even with a more hawkish Fed. We maintain that view. A return of EUR/USD below 1.1510 has probably become difficult. First resistance in EUR/USD stands at 1.1830/40. A break would open the way to the 1.20 area.

Sterling traded with a slightly negative bias (against the euro) yesterday as UK CPI remained soft an as Brexit noise persisted. May retail sales are expected to rise modestly (0.3% M/M core). We maintain the view that a substantial positive surprise is needed to support a sustained rebound of sterling. Brexit uncertainty persists. We expect EUR/GBP to hold in the upper part of the 0.8700/0.8850 consolidation pattern.

EUR/USD: will ECB propel euro beyond 1.1830/40 resistance

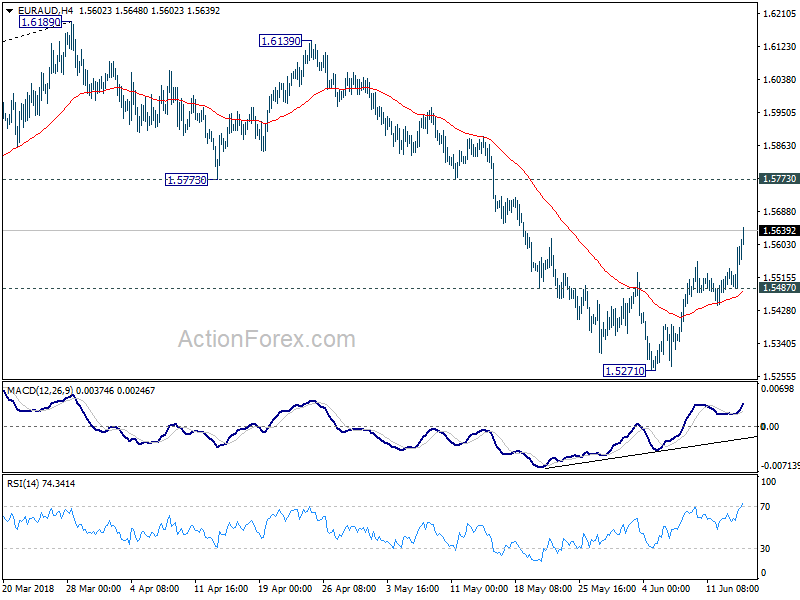

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5500; (P) 1.5547; (R1) 1.5606; More....

EUR/AUD's rebound from 1.5271 resumed by breaking 1.5556 and reaches as high as 1.5648 so far. Intraday bias is back on the upside for further rally. At this point, we're still viewing the rebound as a correction and expected upside to be limited below 1.5773 support turned resistance. On the downside, below 1.5487 will indicate completion of the rebound and bring retest of 1.5271 low. However, decisive break of 1.5773 will invalidate our view and bring retest of 1.6189 high instead.

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further decline is expected in medium term, even in case of strong rebound.

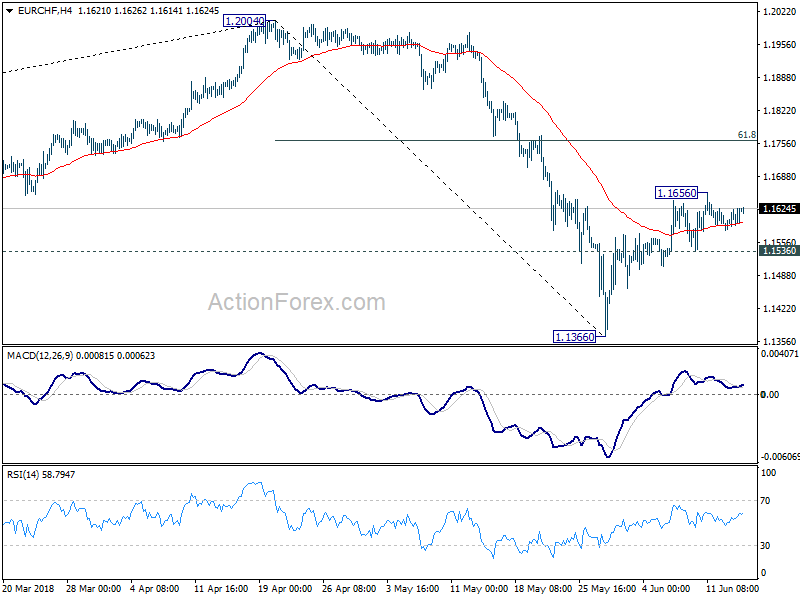

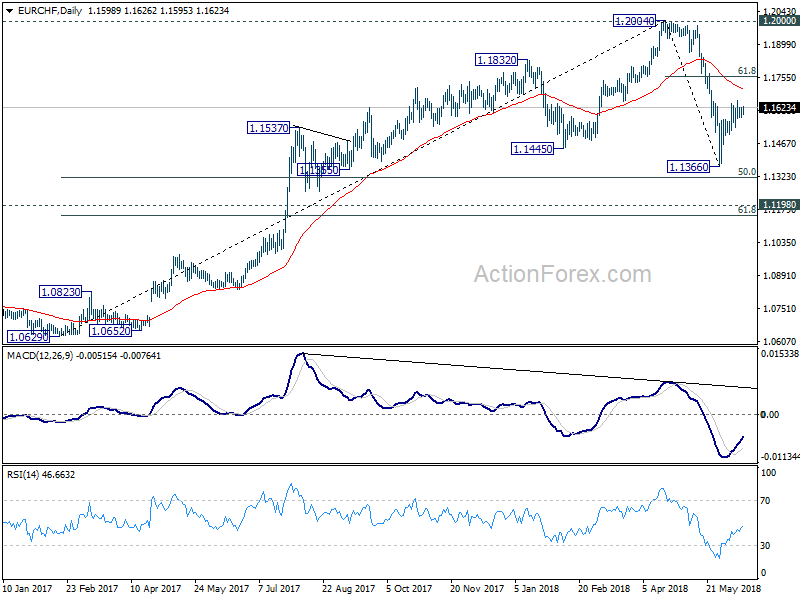

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1596; (P) 1.1611; (R1) 1.1637; More....

EUR/CHF remains bounded in range of 1.1536/1656 and intraday bias remains neutral. With 1.1536 minor support intact, further rise is mildly in favor to 61.8% retracement of 1.2004 to 1.1366 at 1.1760. But after all, the corrective pattern from 1.2004 is expected to extend with at least one more falling leg. Hence, we'll look for reversal signal again above 1.1760. On the downside, break of 1.1505 will suggest that the rebound is completed. And intraday bias will be turned back to the downside for retesting 1.1366.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

Emerging Markets Unexpectedly Benefit From Upbeat Federal Reserve

Despite the Federal Reserve coming across much more upbeat than expected after raising US interest rates for the second time in 2018, some softness in the Dollar following the decision has provided a short-term boost to many different emerging market currencies.

In a surprising move, traders appear to be taking profit on the Dollar after the latest US interest rate decision. This is benefiting many different emerging market currencies in early Thursday trade. With exception of the Indonesian Rupiah, Thai Baht and the New Taiwan Dollar, most emerging market currencies across Asia are trading higher against the USD at time of writing. This includes the Malaysian Ringgit, Chinese Yuan, Indian Rupee, Philippine Peso and Korean Won.

Although this would be seen as negative news for holders of emerging market currencies, I am unsure how long this rebound in sentiment will last. It could be a temporary move, largely encouraged by investors taking profit on a persistent resurgence in the Dollar over the second quarter of 2018. After all, the Federal Reserve appeared significantly more upbeat than most expected yesterday with markets even receiving a surprise by seeing two more US interest rate increases before the end of the year in the dot plot forecast. Federal Reserve Chair Jerome Powell also appeared very optimistic about the current health of the US economy in his comments.

The combination of an improved fundamental outlook for the United States andan adjustment higher in US interest rate expectations will probably encourage investors to purchase the Dollar at lower levels.

Lira unable to find buyers

As an exception to the theme that there seems to be an improved appetite towards most emerging market currencies in early Thursday trade, theTurkish Lira is still suffering from a lack of buying appetite and is already down by another 0.5% for the day. There are a number of different factors that are persistently weighing on sentiment for the Lira, including worrying inflation and ongoing concerns about the direction of the country in the lead up to the Turkish general election on 24 June.

The motivator behind the latest woes for the Lira is more likely than not traders pricing in the broad concerns that President Recep Erdogan will undermine the central bank if he is declared victorious in less than two weeks from now.

ECB next on investor radar

While this has already been a historic week and what many are proclaiming to be the busiest week of the year for the financial markets it is not over yet, with the latest meeting with the European Central Bank (ECB) set to conclude today.

It is already considered a foregone conclusion that the ECB will be leaving monetary policy unchanged today, although many investors are hoping for guidance on its plan to exit quantitative easing.

With the financial markets now appearing much calmer around the recent political uncertainty in Italy, I find the Euro attractive at its current levels and it could receive a bid today if the ECB offers any insight about exiting QE.

Elliott Wave View: EURJPY Starting The Next Leg Higher

EURJPY short-term Elliott wave view suggests that the rally from 5/29 low (124.59) to 6/07 high (130.276) ended intermediate wave (1). The internals of that rally higher unfolded as Impulse Elliott Wave structure where subdivision of Minor 1, 3 and 5 unfolded also as an impulse in lesser degree. Down from there, the pair made a 3 waves pullback in Intermediate wave (2) as a Zigzag correction.

The internal of Intermediate wave (2) unfolded as zigzag structure where Minor A ended at 129.25, Minor wave B ended at 129.73 and Minor wave C of (2) ended at 128.056 low. Up from there, the rally is taking place as another impulse structure in Intermediate wave (3) higher. The pair has already made a marginal new high above 130.26 peak, confirming the next leg higher. This marginal high has created a bullish sequence from 5/29 low. Near-term, while dips remain above 128.05 low, expect pair to see more upside towards 131.55 – 132.37, 0.618-0.764% Fibonacci extension area of Intermediate wave (1)-(2) at first. Afterwards, it should pullback and extend higher again towards 133.73 – 135.03, 100%-123.6% Fibonacci extension area of (1)-(2) at later stage. We don’t like selling the pair and expect intraday traders to appear in 3, 7 or 11 swings against 128.05 low.

EURJPY 1 Hour Elliott Wave Chart

The Initial Losses In EUR/USD Were Also Quickly Erased

Market movers today

With the Fed meeting behind us, focus turns to the ECB meeting. We do not expect any changes in policy or forward guidance, but some hawkish comments could be envisaged. Instead, we expect the forward guidance to change in July. The ECB will also publish new growth and inflation projections, where we expect a lower growth forecast for 2018 and an increase in inflation project ions, especially for 2018. Furthermore, focus will also be on how President Draghi will address the recent weeks of political turmoil in Italy.

In Sweden, we expect CPIF and CPIF ex energy to both overshoot Riksbank's forecast (0.2pp and 0.04pp, respectively). This would bolster the Riksbank's current plans for a rate hike in Q4 this year to which we assign about a 20% probability. For more details, see page 2.

In the US and the UK, retail sales in May are due out.

The Bank of Japan meets today and is expected to announce its monetary policy early Friday morning European time. We expect both the policy balance rate and the 10Y yield target to be left unchanged, at 0.10% and 0.00%, respectively.

Selected market news

As expected, the Fed raised the target range by 25bp to 1.75%-2.00% last night . The median dot for this year was lifted from a total of three hikes to four, as one member became more upbeat , which was enough to move the median. More importantly, the Fed removed a lot of soft forward guidance in the statement, as Chairman Jerome Powell wants more flexibility now the Fed funds rate is close to neutral. This is slight ly more hawkish than we had expected an d we now think it is more likely than not that the Fed is going to hike in both September and December (previously only in December) although it is st ill a close call between three and four hikes, which is also what the dot plot signals. For more details see FOMC review: Four hikes more likely after removal of soft wordings, 13 June.

US yields initially gained across the government bond curve with the 10Y yield briefly rising above 3% on the FOMC announcement . However, increases quickly faded and the 2Y10Y US yield curve flattened to 40bp – the flat test since 2007. The initial losses in EUR/USD were also quickly erased as Powell st ressed that an inflation overshoot will be allowed (USD negative)

US equity markets ended the day lower and the negative close in the US is mirrored in Asia this morning, where weaker-than-expected Chinese retail sales and industrial production data also weigh on risk sentiment .

The Bank of Japan (BoJ) reduced its buying of bonds for the second time this month, by cut ting purchases in the 3-5Y segment by JPY30bn to JPY300bn at its regular operation. The reduction in the 3-5Y segment follows t he BoJ's unexpected cut in buying in the 5-10Y segment by JPY20bn on 1 June, and should would encourage flattening along the yield curve.

Euro Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the EUR rose 0.46% against the USD and closed at 1.1798.

On the economic front, the Euro-zone's seasonally adjusted industrial production retreated more-than-anticipated by 0.9% on a monthly basis in April, highlighting concerns over the strength of the economy and compared to market expectations for a fall of 0.7%. In the previous month, industrial production had advanced 0.5%.

The US Dollar declined against a basket of major currencies, after the US Federal Reserve (Fed) raised the key interest rate, for the second time this year and signalled four more rate hikes in 2018

The Fed, at its latest monetary policy meeting, voted unanimously to lift the benchmark interest rate by a quarter percentage point to a range of 1.75% to 2.00%, citing robust economic growth, strong labour market and inflation moving towards the central bank's 2.00% goal.

Further, Fed's Chairman, Jerome Powell, stated that the US economy has strengthened in recent months, but warned over the prospects of higher inflation.

Separately, the nation's producer price index (PPI) grew 3.1% on a yearly basis in May, more than market expectations for a rise of 2.80%. In the previous month, the PPI had risen 2.6%.

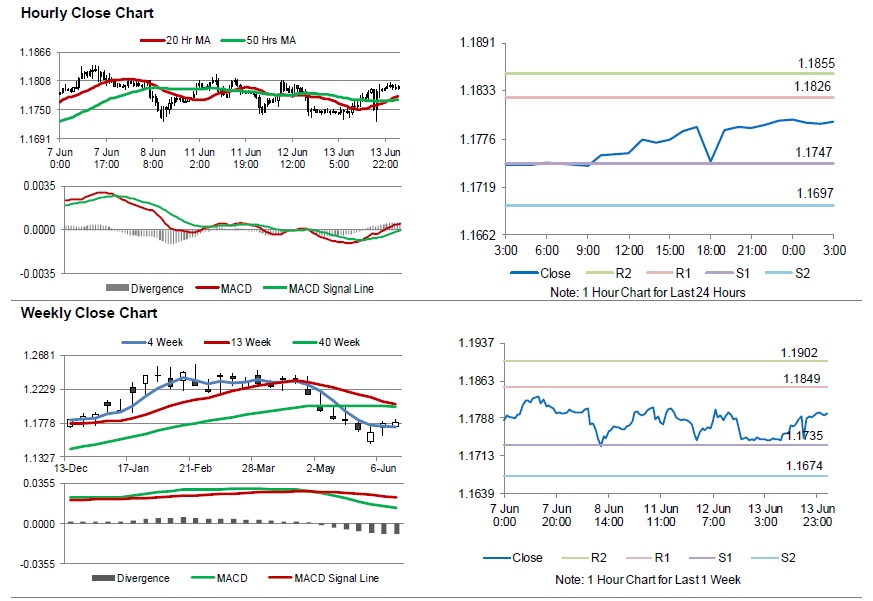

In the Asian session, at GMT0300, the pair is trading at 1.1797, with the EUR trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.1747, and a fall through could take it to the next support level of 1.1697. The pair is expected to find its first resistance at 1.1826, and a rise through could take it to the next resistance level of 1.1855.

Moving ahead, the European Central Bank's (ECB) monetary policy meeting, due later in the day, will be closely watched for further hints on monetary policy. Additionally, the release of Germany's final consumer price index for May, will be eyed by investors. Later in the day, the US advance retail sales for May, followed by the initial jobless claims data and business inventories for April, will pique significant amount of investor attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

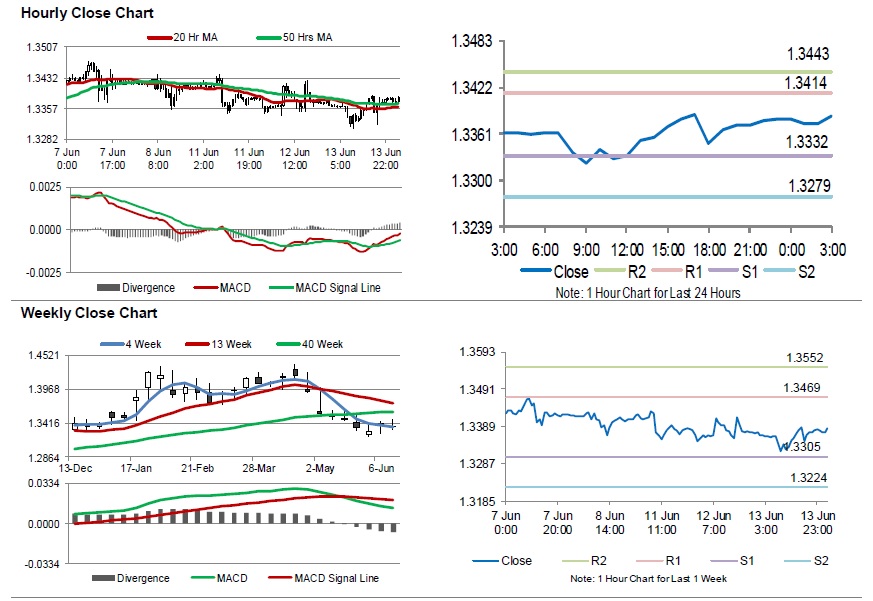

Britain’s Annual Inflation Growth Remains Unchanged In May

For the 24 hours to 23:00 GMT, the GBP rose 0.07% against the USD and closed at 1.3381.

Macroeconomic news released showed that UK's consumer price index (CPI) rose 2.4% on an annual basis in May, meeting market expectations and marking its lowest level since March 2017. In the prior month, the CPI had recorded a similar gain.

In the Asian session, at GMT0300, the pair is trading at 1.3385, with the GBP trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.3332, and a fall through could take it to the next support level of 1.3279. The pair is expected to find its first resistance at 1.3414, and a rise through could take it to the next resistance level of 1.3443.

Moving ahead, investors would closely monitor UK's retail sales data for May, scheduled to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.