Sample Category Title

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.14; (P) 146.80; (R1) 147.50; More...

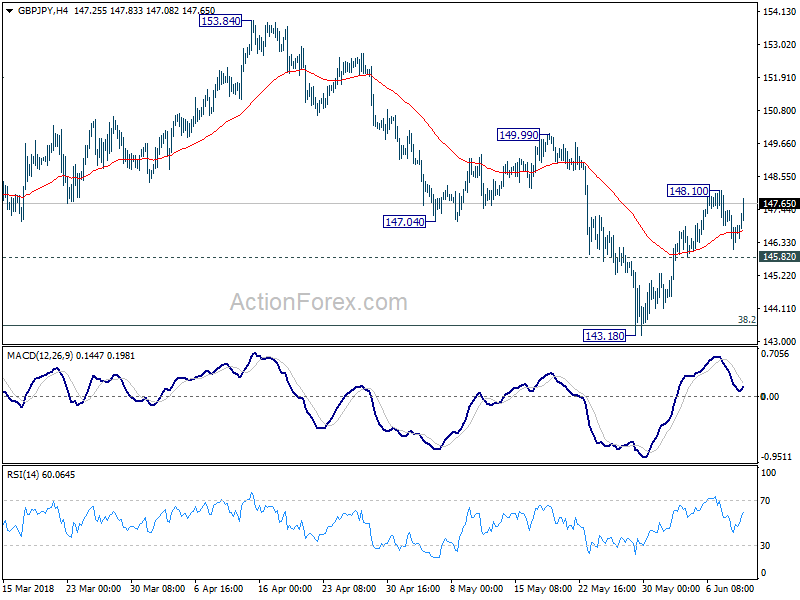

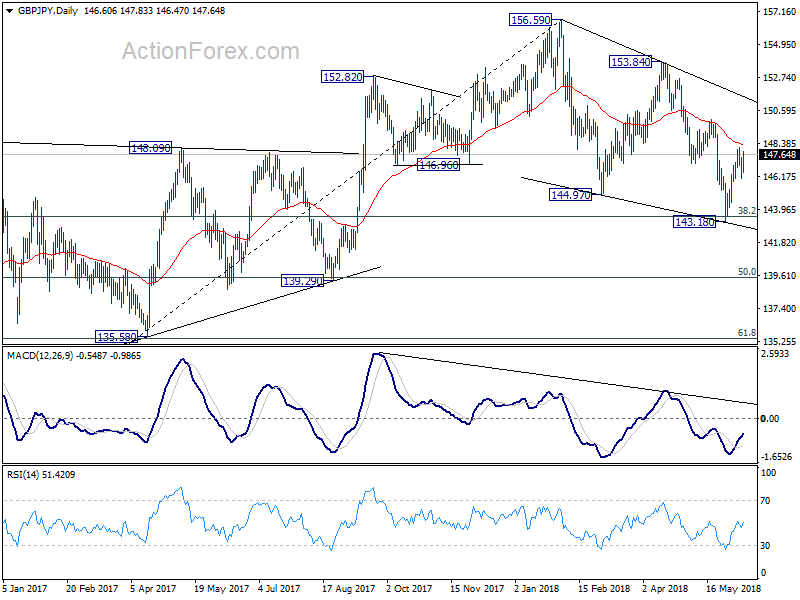

GBP/JPY rebounds strongly today but stays below 148.10 minor resistance. Intraday bias remains neutral first. On the upside, above 148.10 will resume the rebound from 143.18 and target 149.99, and then 153.84 resistance. However, break of 145.82 minor support will argue that the rebound from 143.18 is completed and bring retest of this low.

In the bigger picture, no change in the view that decline from 156.59 is a corrective move. In case of another fall, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. Meanwhile, break of 153.84 should confirm that the correction is completed and target 156.59 and above to resume the medium term up trend.

EURUSD Still Bullish Above 1.1750 Level

The euro has recovered upside momentum against US dollar, with buyers pushing the pair back towards the 1.1800 resistance level in early Monday trading. On Friday, the EURUSD pair fell towards the 1.1726 level, as risk-off sentiment spread through broader financial markets after poor German economic data. Traders are likely to remain increasingly cautious ahead of Tuesday’s meeting between US President Trump and North Korean leader, Kim Jong-Un on Tuesday.

The EURUSD pair is intraday bullish while trading above the 1.1750 level. Key resistance is located at the 1.1800 and 1.1839 levels.

If the EURUSD pair moves below the 1.1750 level, sellers will likely push price towards the 1.1726 and 1.1700 support level.

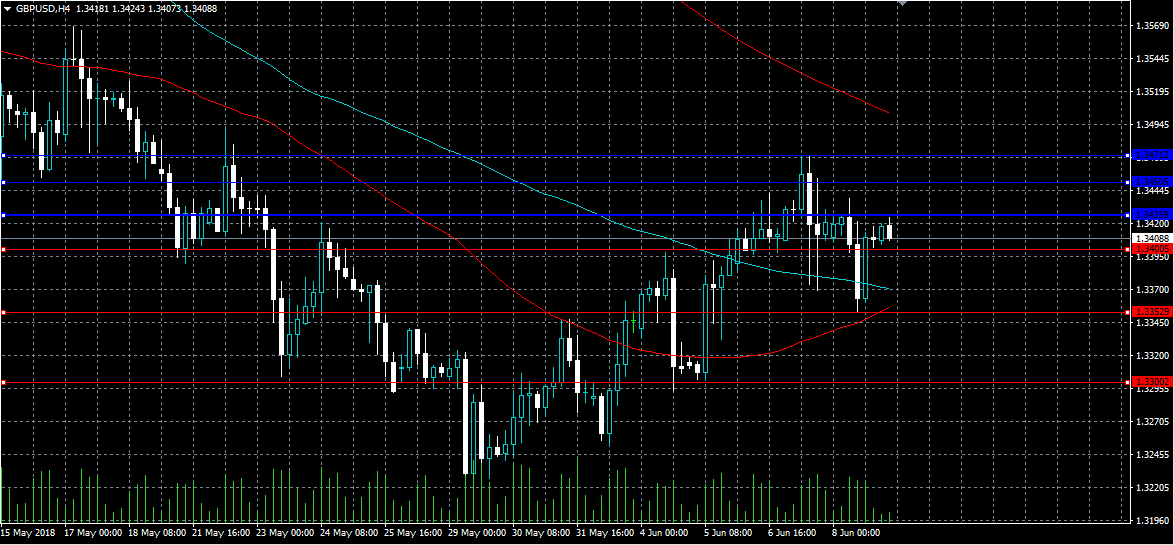

GBPUSD Only Bullish Above 1.3425 Level

The British pound has moved back towards the 1.3400 level against the US dollar, after finding strong dip-buying interest from the 1.3352 support level. The GBPUSD pair remains volatile, with high-impacting United Kingdom economic data and Brexit negotiations currently driving price-action. Traders now look towards the release of key Trade Balance, Industrial Production and Manufacturing data from the United Kingdom economy.

The GBPUSD pair is only bullish while trading above the 1.3425 level, key technical resistance is now located at the 1.3450 and 1.3471 levels.

If the GBPUSD pair moves below the 1.3400 level, key technical support is found at the 1.3352 and 1.3300 levels.

Markets Indecisive After The G7 Meeting Fails To Make Progress

Markets are indecisive this morning as the G7 meeting in many ways delivered on the expectations of traders with participants failing to find meaningful progress and the US marginalized in what has been dubbed the G6 +1 meeting. With the US rejecting the communiqué as predicted, the market is directionless and focusing now on the US/North Korean summit tomorrow.

Today’s economic calendar is light and unless the market finds direction traders may wait until the outcome of the Singapore Summit is understood and the results of the FOMC and ECB meetings, on Wednesday and Thursday respectively, are revealed. Bitcoin fell after the Coinrail exchange was hacked over the weekend. The Cryptocurrency is trading around 6800.00 after the South Korean exchange fell victim to the theft of NPXS, NPER and ATX coins.

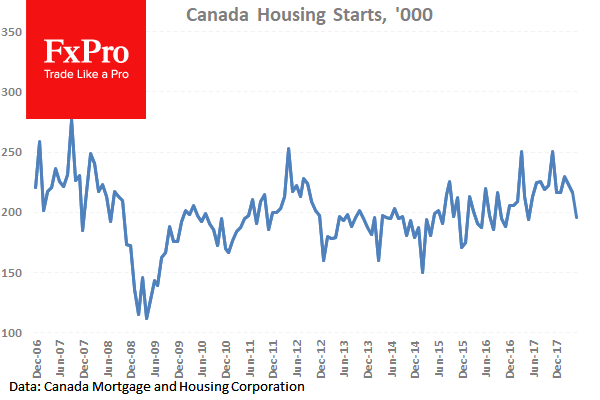

Canadian Housing Starts s.a (YoY) (May) was released coming in at 196K with an expected number of 218K from a previous 214K last month which was revised up to 217K. This data failed to beat expectations this month and has now dropped below the 200K level. The previous data was revised up but this revision is wiped out by the miss. USDCAD rose from 1.29768 to 1.30385 after this data.

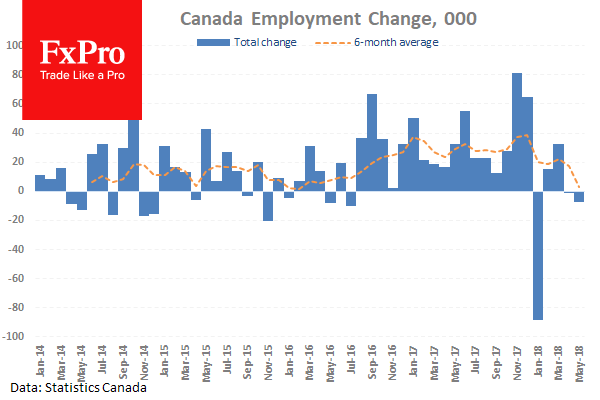

Canadian Unemployment Rate (May) came in as expected at 5.8% against a previous 5.8%. This data is remaining static at the current level which is close to the lowest levels seen since 2008. Participation Rate (May) came in at 65.3% against an expected 65.4% from 65.4% prior. The participation rate is now at a new low showing that there are fewer participants in work or looking for work. Net Change in Employment (May) was -7.5% against an expected 17.5K from a prior -1.1K. The Net Change in Employment data has dropped under zero as employment contracts which is negative for the economy. USDCAD fell from 1.30385 to 1.29720 following this data release.

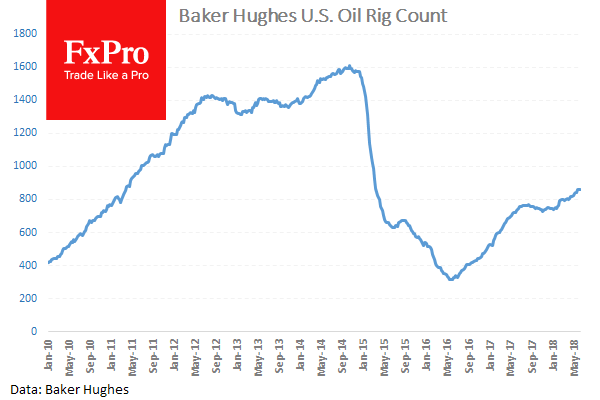

Baker Hughes US Oil Rig Counts was released with a headline number of 862 up 1 from last week’s number of 861. As this number creeps higher more and more rigs are coming into operation increasing the supply of oil onto the market and adding downward pressure on prices. WTI Oil was flat on the week as the rise in rig counts increased signalling additional supply in the US market but price is at the lowest levels in two months.

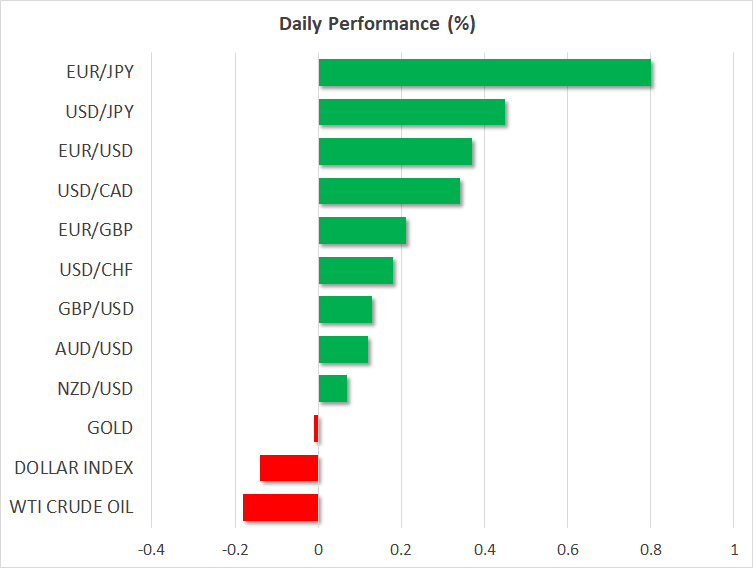

EURUSD is up 0.23% overnight, trading around 1.17941.

USDJPY is up 0.24% in the early session, trading at around 109.762.

GBPUSD is down -0.06% this morning trading around 1.34010.

Gold is up 0.03% in early morning trading at around $1,298.08.

WTI is down -0.11% this morning, trading around $65.48

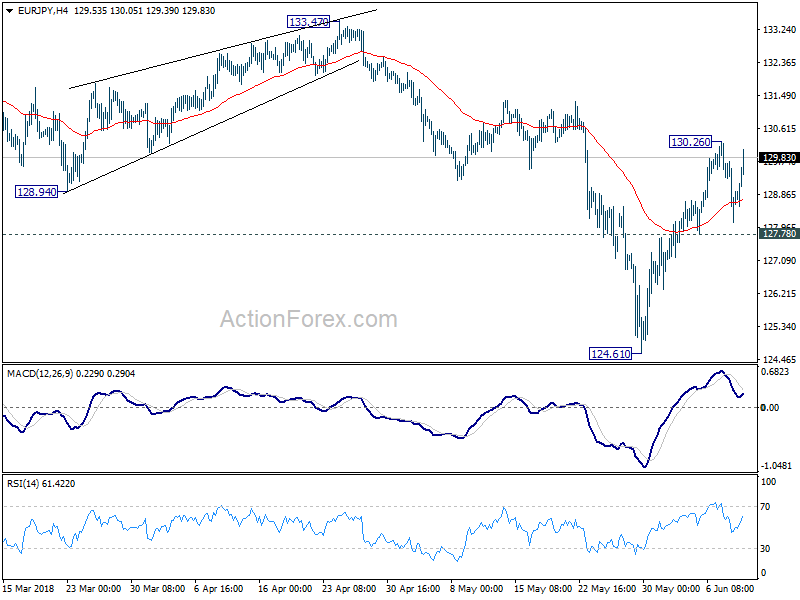

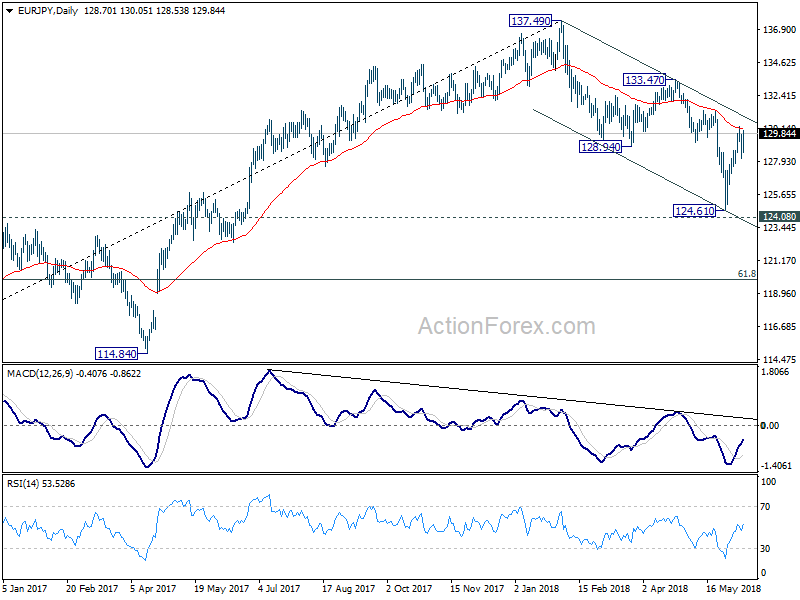

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.10; (P) 128.92; (R1) 129.72; More....

EUR/JPY rebound strongly today but stays below 130.26. Intraday bias remains neutral for the moment. ON the upside, above 130.26 will resume the rebound form 124.61 and target 133.47 key near term resistance next. On the downside, however, break of 127.78 minor support will indicate completion of the rebound from 124.61. Intraday bias will be turned back to the downside for 124.61 first.

In the bigger picture, despite rebounding strongly ahead of 124.08 resistance turned support, there was no clear follow through buying. Note again that there is bearish divergence in daily MACD. Firm break of 124.08 will confirm trend reversal. That is, whole rise from 109.03 (2016 low) has completed at 137.49 already. In that case, deeper fall should be seen back to 61.8% retracement of 109.03 to 137.49 at 119.90 and below. Nonetheless, decisive break of 133.47 key resistance will likely extend the rise from 109.03 through 137.49 high.

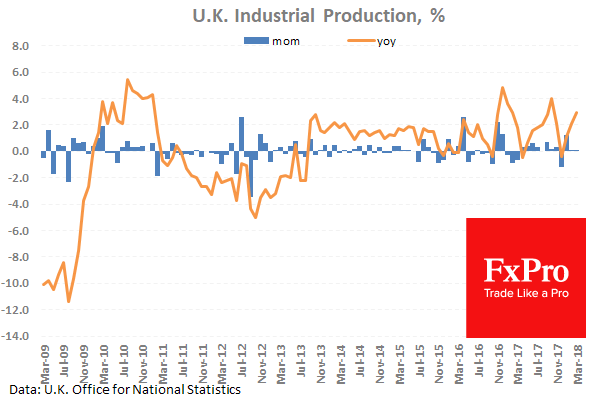

UK Production Data In Focus On A Light Calendar

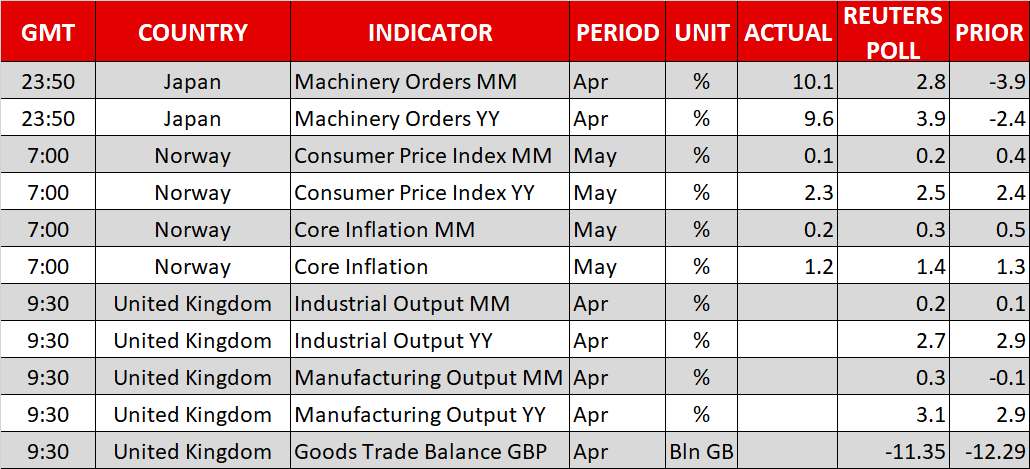

At 08:30 GMT, UK Industrial Production (YoY) (Apr) is expected to be 2.7% against a previous 2.9%. Industrial Production (MoM) (Apr) is expected to be 0.2% against 0.1% previously. Last month this data was flat but is expected to marginally beat today. Manufacturing Production (YoY) (Apr) is expected to be 3.1% against 2.9% previously. Manufacturing Production (MoM) (Apr) is expected to be 0.3% against -0.1% previously. This figure has fallen under the zero mark showing a contraction on the monthly number. The negative impact from Brexit is continuing to plague the economy as orders are delayed and production postponed. GBP pairs can move because of this data release.

Major data releases and events for the week ahead:

On Tuesday at 01:00 GMT, US President Trump will meet with North Korean Leader Kim Jong – Un in Singapore.

At 08:30 GMT, UK Average Earnings data will be announced.

At 17:00 GMT, US Consumer Price Index data will be released.

On Wednesday at 08:30 GMT, UK Consumer Price Index data will be published.

At 18:00 GMT, US FOMC Interest Rate Decision and Monetary Policy Statement will be announced. Press Conference will follow at 18:30 GMT.

On Thursday at 11:45 GMT, ECB Rate Decision will be announced with a Press Conference at 12:30 GMT.

At 12:30 GMT, US Retail Sales and Jobless data will be released.

On Friday at 09:00 GMT, Eurozone Consumer Price Index data will be published.

Yen Retreats Ahead Of Key Events, UK Manufacturing Output Coming Up

Here are the latest developments in global markets:

FOREX: The US dollar index – which measures the greenback's performance against a basket of six major currencies – is lower on Monday, though by less than 0.2%. The euro is higher across the board, as some encouraging remarks from Italy's new finance minister helped to calm markets. Meanwhile, the yen is on the back foot amid subsiding European political risks, and as investors position for the several events this week will bring.

STOCKS: US markets closed higher on Friday, with the S&P 500 and Dow Jones climbing by 0.31% and 0.30% respectively, while the tech-heavy Nasdaq Composite lagged, rising by 0.14%. Meanwhile, it appears the worrisome signals on global trade from the G7 summit over the weekend were not enough to worry equity investors, as futures tracking the S&P, Dow, and Nasdaq 100 are all currently in positive territory, albeit marginally so. In Asia, most markets were in the green on Monday. Japan's Nikkei 225 and Topix gained 0.48% and 0.30% correspondingly, as a softer yen brightened the outlook for exporting firms. In Hong Kong, the Hang Seng rose 0.37%. Meanwhile in Europe, futures tracking the major benchmarks were pointing to a much higher open for all these indices, possibly due to some encouraging signals from Italy over the weekend.

COMMODITIES: In energy markets, oil prices are lower on Monday, extending losses from Friday. WTI and Brent crude are down by 0.2% and 0.3% respectively, with the losses being attributed to signs that US and Russian productions continue to surge. Active US oil rigs ticked up again during the past week, while Russian news agency Interfax said the nation's production touched 11.1 million barrels per day in early June, above its OPEC-deal target of under 11.0 million. In precious metals, gold prices are practically flat on Monday, after experiencing a similarly lackluster session on Friday. The metal continues to trade in a very narrow range, and this week's risk events could finally be the trigger for a break in either direction (US-North Korea summit, Fed & ECB meetings, US tariff announcement on Chinese goods).

Major movers: Euro looks to extend recovery; yen on the defensive ahead of key events

The US President backed out of signing a joint statement with the G7 over the weekend, presumably due to some remarks by Canadian Prime Minister Trudeau, who said that Canada would impose retaliatory tariffs on the US commencing July 1. Leaving the meeting, Trump reiterated on Twitter the US is looking at introducing tariffs on imported vehicles, something that would single out major car-manufacturing nations and classic US allies, such as Germany and Japan.

Yet, the market response was muted, with haven currencies like the Japanese yen trading 0.4% lower against the US dollar and 0.8% down against the euro on Monday. The lack of reaction may be owed to some market-friendly comments by the new Italian economy minister, and investors positioning for this week's numerous risk events – for instance by reducing their exposure to the yen. Both the Fed and ECB are expected to take one more tiny step towards reducing monetary accommodation when they meet again this week, and since the BoJ is not expected to alter its ultra-loose policy anytime soon, that helps to reduce the yen's appeal. Moreover, expectations around a positive outcome in the Trump-Kim Jong Un summit tomorrow may be reducing geopolitical risk premium and hence, diverting flows out of haven currencies like the yen and Swiss franc.

Over the weekend, Italy's new finance minister Giovanni Tria said “there is no question of leaving the euro”, a move that is likely to put to rest any surviving speculation for an imminent ‘Italexit', at least for now. He also emphasized the nation has to reduce its debt/GDP ratio and prioritize structural reforms over more deficit spending. The message was well-received, as Italian government bond yields are lower across the board today while the euro is higher against its major counterparts.

Day ahead: UK industrial and manufacturing output on the horizon; trade, Trump-Kim meeting, central bank decisions in investors' minds

Barring some data releases out of the UK, Monday's calendar is empty of other data points out of major economies. In the absence of releases, investors may focus on the global trade outlook, tomorrow's Trump-Kim meeting, as well as on speculating on the actions of major central banks which will be completing their meetings on monetary policy as the week unfolds.

At 0830 GMT, the UK will be on the receiving end of industrial & manufacturing production data for April. Month-on-month, manufacturing output is anticipated to have risen by 0.3%, after contracting by 0.1% in March. The yearly pace of growth is expected at 3.1%, up from March's 2.9%. Industrial output is also forecast to have expanded at a faster pace on a monthly and annual basis in April compared to the previously tracked month. Stronger-than-projected prints can stoke market expectations for a Bank of England rate hike sooner rather than later. For the record, market participants currently see a mere 11% chance for the delivery of a 25bps rate increase when the Bank meets next week according to UK overnight index swaps.

UK data on April's goods trade balance will also be made public at 0830 GMT; the deficit is expected to narrow to 11.35 billion pounds from 12.29bn in March.

Ahead of tomorrow's meeting with North Korea's Kim Jong Un, Trump maintained a confrontational stance with traditional US allies, such as Canada (with NAFTA negotiations ongoing), after last week's G7 meeting. In this respect, trade developments, as well as Tuesday's US-North Korea summit in Singapore will be on investors' minds. Meanwhile, the Fed (Wednesday), ECB (Thursday) and the Bank of Japan (Friday) will be completing their respective meetings on monetary policy later in the week; the euro continues to enjoy positive momentum after a slew of hawkish comments by ECB policymakers last week, with euro/dollar currently trading above the 1.18 handle.

Potentially of interest is a news conference that will follow after a meeting between German Chancellor Angela Merkel and the heads of the IMF, WTO, the World Bank, the ILO and the OECD in Berlin at 1500 GMT.

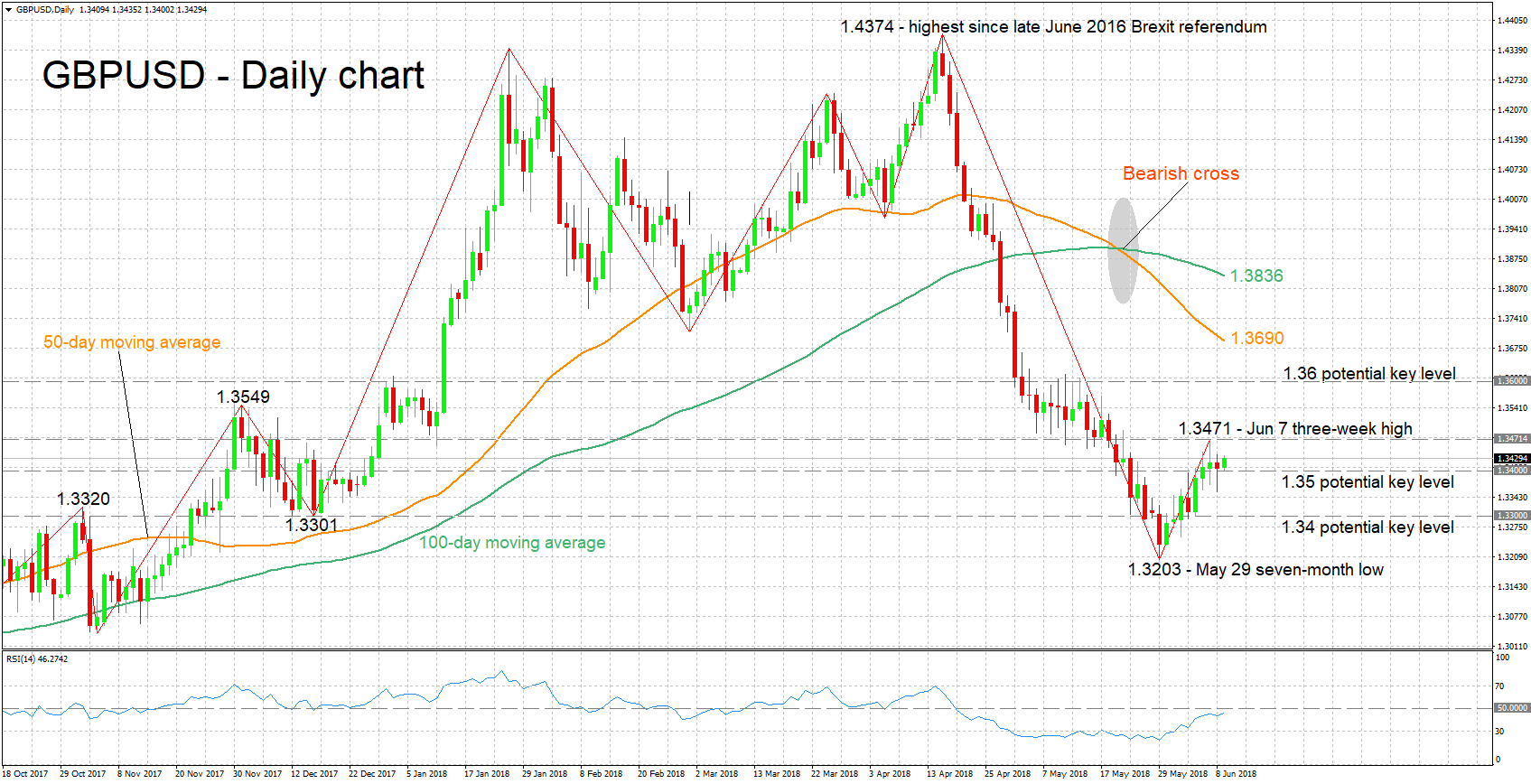

Technical Analysis: GBPUSD looking bullish in the short-term

GBPUSD has gained more than 200 pips after touching a seven-month low of 1.3203 on May 29. The RSI is rising in support of a positive picture in the short-term.

Upbeat UK data later in the day can support the pair. Resistance to advances may come around last week's three-week high of 1.3471, including the 1.35 round figure. Further above, the attention would increasingly turn to the 1.36 handle.

Weaker-than-anticipated figures on the other hand, are likely to exert selling pressure in GBPUSD. Immediate support could be met around 1.35, and further below at the 1.34 handle.

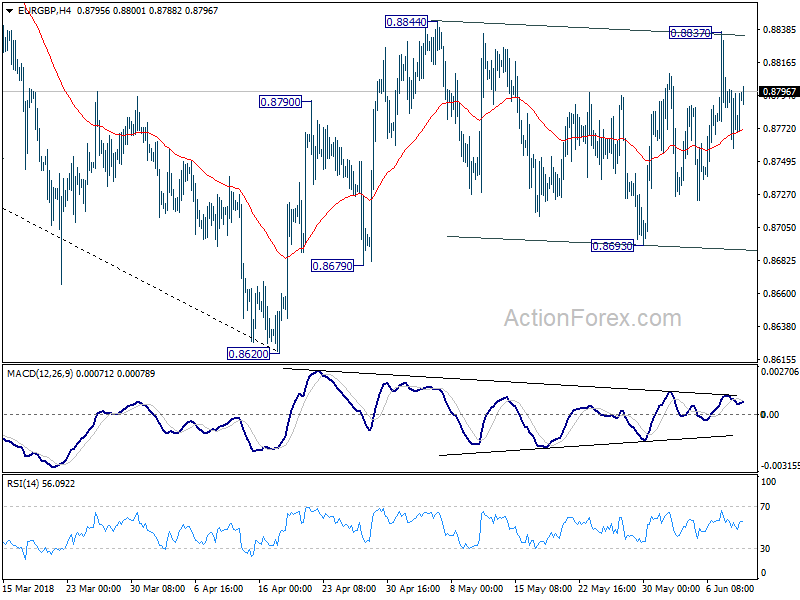

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8756; (P) 0.8779; (R1) 0.8799; More...

Intraday bias in EUR/GBP remains neutral as sideway trading continues. Another rise is expected as long as 0.8693 support holds. Break of 0.8844 will resume the rebound from 0.8620 for 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). However, break of 0.8693 will bring deeper fall back to retest 0.8620 low.

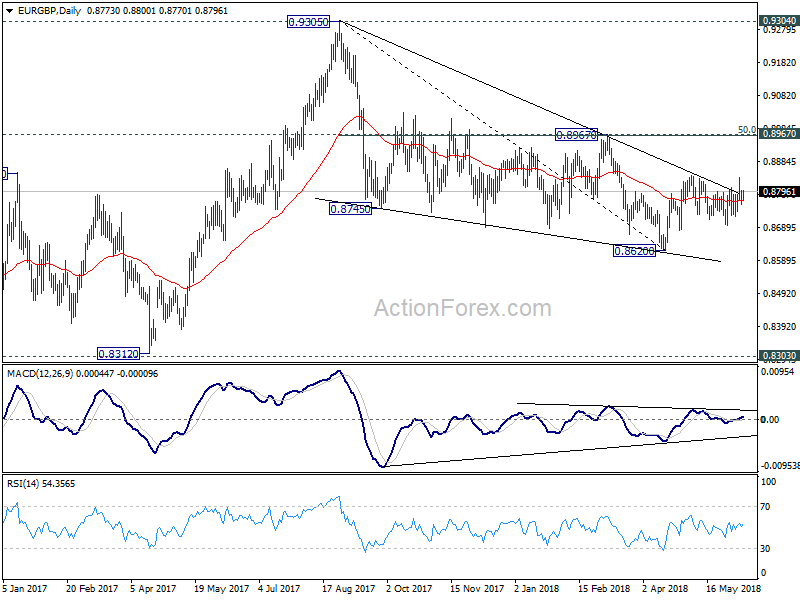

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

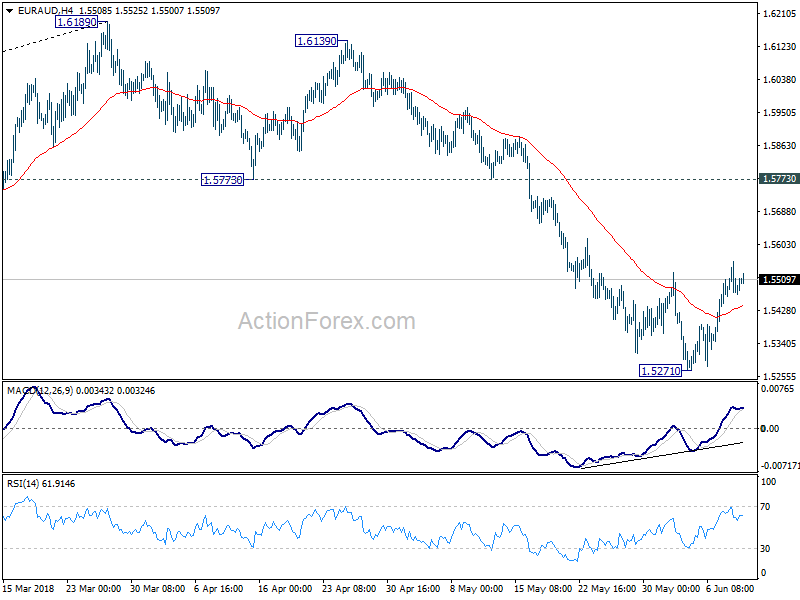

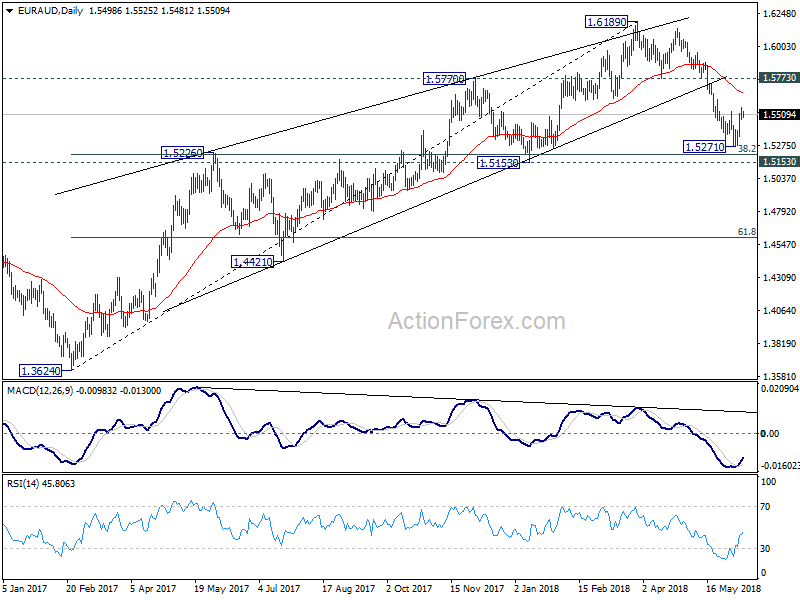

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5380; (P) 1.5447; (R1) 1.5542; More....

Intraday bias in EUR/AUD remains mildly on the upside as rebound from 1.5271 is in progress, for 55 day EMA (now at 1.5664). But upside should be limited below 1.5773 support turned resistance and bring fall resumption. On the downside, break of 1.5271 will extend the fall from 1.6189 to 1.5153 next.

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further decline is expected in medium term, even in case of strong rebound.

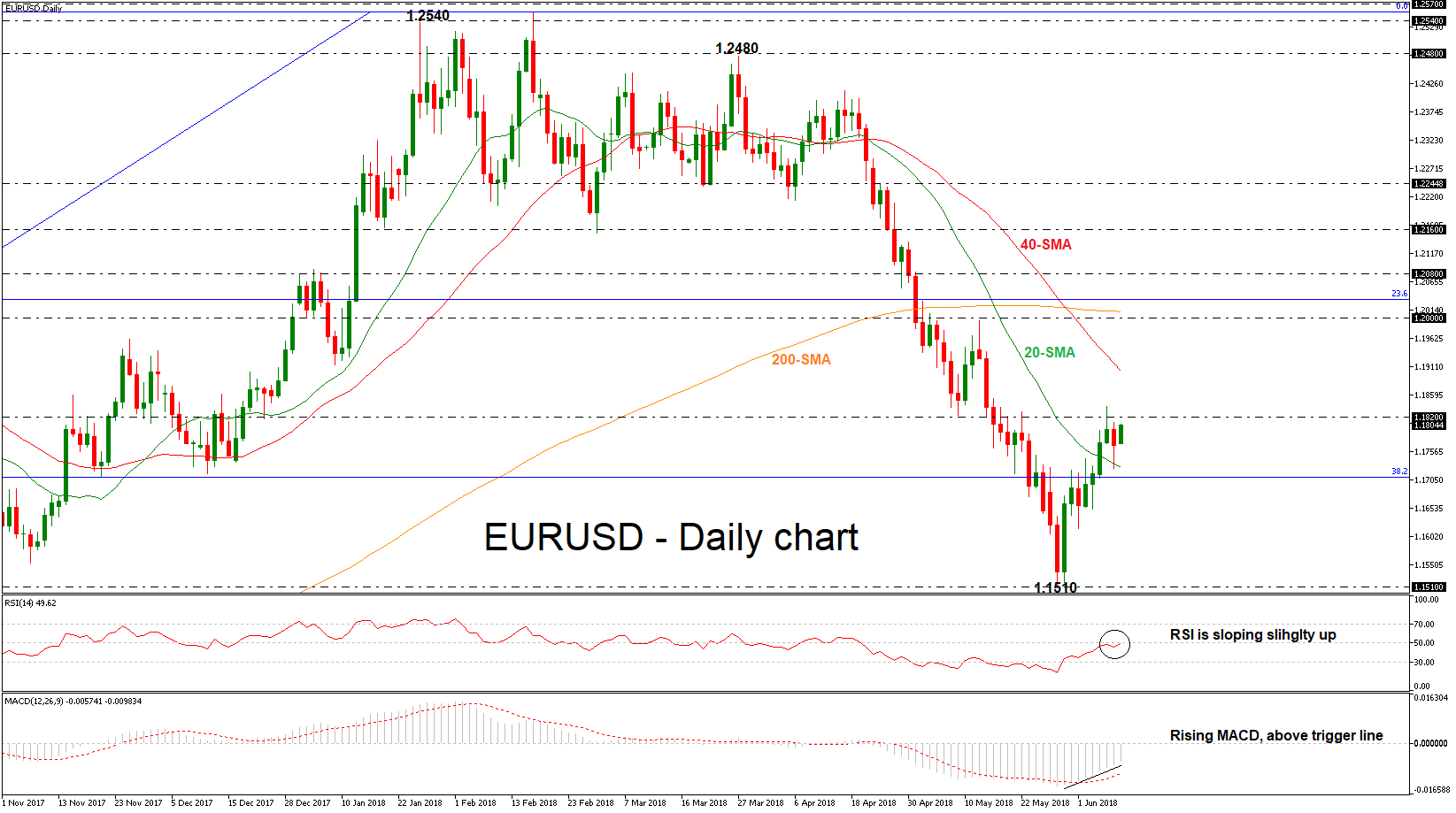

EURUSD On Course For Positive Correction, Looks To Jump Even Higher

EURUSD is in progress to create a bullish retracement following the pullback from the 10-month low of 1.1510 support level. The aggressive bearish movement, especially in the previous seven weekly sessions, has snapped during the past week, completing a bullish candle. Moreover, the momentum indicators in the near-term are supportive for the bullish correction.

From the technical point of view, in the daily timeframe, the RSI indicator is sloping slightly to the upside near the threshold of 50, while the MACD oscillator jumped above its trigger line and is rising in the bearish territory.

Immediate resistance is being provided by the 1.1820 level and the price successfully surpassed the 20-day simple moving average (SMA). Should prices jump higher, the next resistance would likely come from the 1.2000 psychological barrier but the pair first needs to climb above the 40-day SMA near 1.1900. As a side note, the 200-day SMA stands around 1.2010, near the aforementioned psychological level.

On the downside, EURUSD would likely meet support at the 38.2% Fibonacci retracement level of 1.1710 of the upleg from 1.0340 to 1.2540. A break below this significant level would endorse downside pressure and challenge the 10-month low near 1.1510. Steeper declines should drive the common currency until the 50.0% Fibonacci of 1.1450.

In the longer timeframe, the bullish view has turned to bearish, however, should price pare the previous weeks’ losses, this would risk shifting the long-term picture to a positive one again.