Sample Category Title

GBP/JPY Retracement Trend Line Breakouts For Uptrend Continuation

The GBP/JPY, so popular "Dragon" has been making obvious trend line breaks above the ascending trend line. This signifies both retracement-continuation pattern in uptrend (a for of zig-zag pattern). 147.05-40 is the POC zone and we could see another rejection should the price retrace again. A strong 1h momentum candle or 4h close above 148.11 should target 149.15. Have in mind that 149.15 is a weekly target and the final weekly resistance. If the price gets there before the end of the week, we might see even stronger uptrend.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

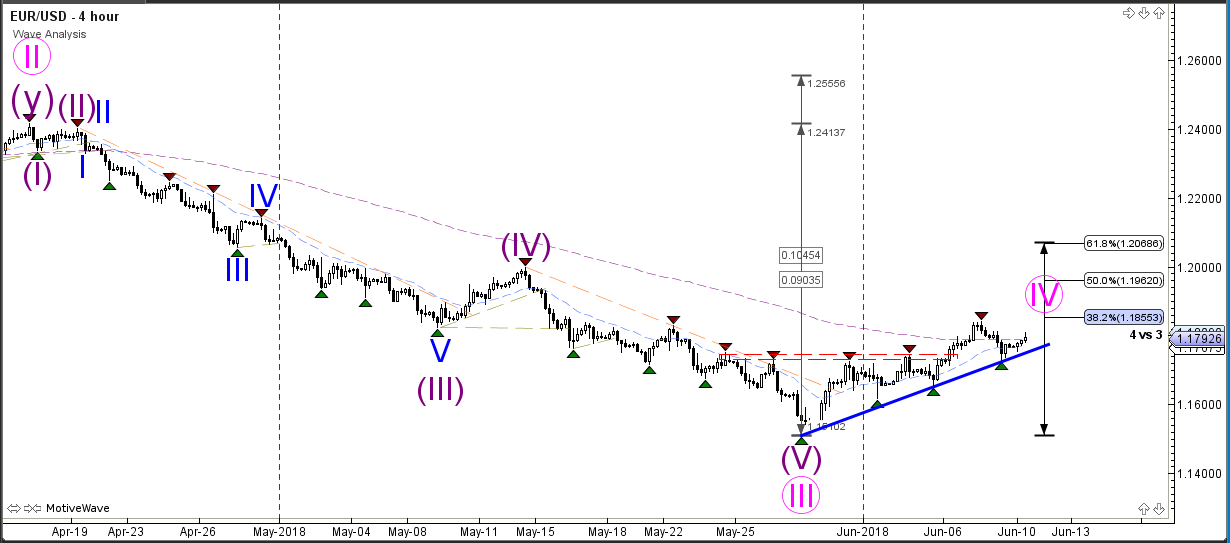

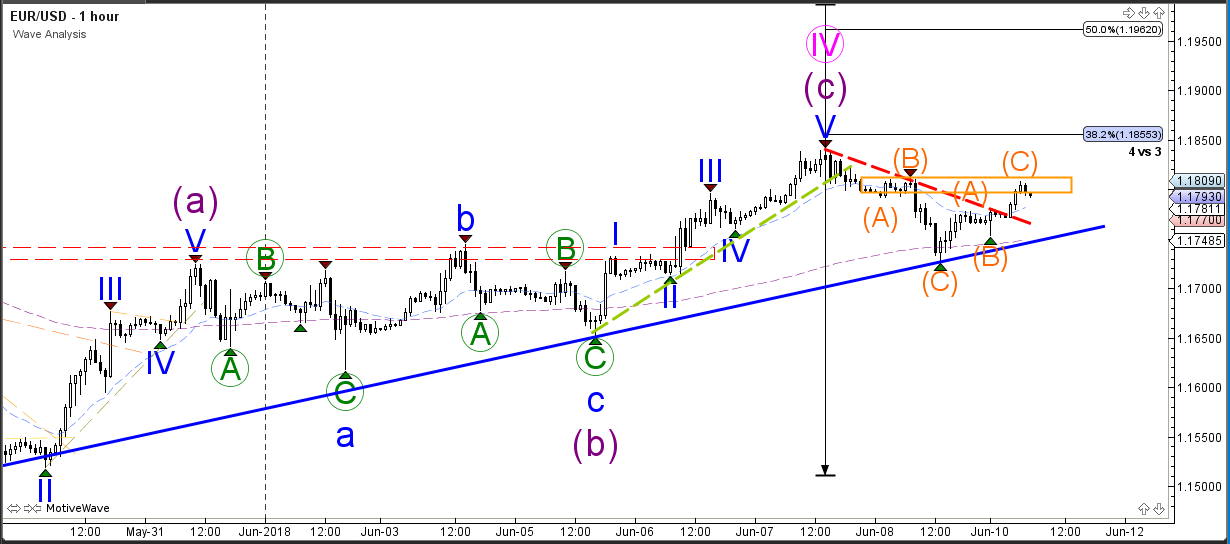

EUR/USD Testing Support Trend Line and Fibonacci Resistance

The EUR/USD reached the 38.2% Fibonacci retracement level of wave 4 (pink) and made a bearish bounce. This could indicate the restart the downtrend if price manages to break below the support trend line (blue). In that case the EUR/USD would have completed a wave 4 pattern and potential started bearish wave 5.

A bullish bounce could indicate a larger retracement towards the 50% Fib of wave 4. A break above the 50% indicates that another wave count is more likely whereas a bounce at the 38.2% Fib and later on bearish breakout below the support trend line (blue) indicates the end of wave 4. Price seems to be building ABC zigzags at the moment and is awaiting a breakout.

Potential Winners And Losers From Unprecedented US-North Korea Summit

Singapore will be considered as the capital of the world for at least the early part of this week. The unprecedented summit between US President Trump and North Korean leader Kim Jong-un in Singapore is considered a major event in the financial markets and we can expect that it will be closely monitored by investors around the globe. The summit might have had an on-again off-again feel to it for months, but now both leaders have arrived in Singapore, the 12 June meeting is set to demand the attention of the globe.

Although meetings between world leaders are typically not considered market events and would usually encourage a muted market reaction, this summit risks being viewed differently. Such a historic meeting between a very unpredictable United States President and the leader of a nation with nuclear capabilities that has been in complete isolation for decades represents an event that investors will not be able to ignore. Assuming that the meeting goes as planned, there are a number of potential winners and losers from alternative scenarios of the summit ending positively or negatively. Before diving into these, it is important to provide an overview of what is likely to be on the meeting agenda.

President Trump has made no secret of his dislike for nuclear weapons and is expected to push hard for the ultimate goal, that North Korea proceeds with denuclearization. In return for giving up its nuclear weapons, it is expected that international sanctions on North Korea would gradually be relaxed, and the United States could potentially offer to invest and help build the nation's economy.

This could be enticing to Kim Jong-un, as the future of a more prosperous North Korea would likely portray him as a hero back home and create a legacy of his being a leader who took his homeland away from global isolation. Kim Jong-un would perhaps seek additional assurances that he would not be portrayed as a 'yes man' for giving up nuclear weapons. References to the United States applying the

so-called 'Libyan Model' for disarmament have apparently caused upset to the North Korean leader back home.

Let's now take a look at the potential winners if the meeting goes positively:

North Korea: we are talking about a nation that has lived in isolation for decades. Those who live in North Korea are reported to do so in unimaginable living conditions, but that could all change if the country is pulled out of isolation. The eventual denuclearization would likely open North Korea to international investment and access into the market.

Korean Won: the Korean Won has been lively in the days before the summit. This is potentially as significant for South Korea as it is for North Korea. It is expected that the Korean Won would rally as a result of a positive meeting between Trump and Kim Jong-un, mainly because it increases the likelihood of further improved relations between North and South Korea.

Donald Trump: for all of the unpredictable moments that have occurred since Trump became President of the United States, the news that he would have a summit with Kim Jong-un is perhaps the most significant. If Trump is able to persuade North Korea to disarm its nuclear weapons, he would achieve a remarkable feat just months before the mid-term elections. The USD could even catch a bid and move higher on optimism that Trump's foreign policy tactics could encourage world peace.

Currencies pegged to the Dollar: the uncertain nature of US foreign policy and the unpredictable tactics of President Trump were seen as the main catalyst behind the Dollar dropping so sharply from its peak shortly after his inauguration in January 2017. If the USD does receive a bid following the conclusion of the summit, those currencies that are pegged to the Dollar should be able to jump on the wave. The UAE Dirham, Saudi and Qatari Riyal and Lebanese Pound are just a few of the pegged currencies that would benefit from a stronger Dollar

Stock markets: improved risk appetite would be seen as encouragement for global stocks. Uncertainty over the past year or so around Trump - Kim Jong-un relations was seen as one of the major risks for the financial markets. A reduction of this uncertainty should encourage investors to carry on investing in global stocks.

Asian emerging market currencies: the emerging markets are generally classified as one of the riskier investment assets out there. They would likely benefit from the improved sentiment in the stock markets enticing investors towards emerging market currencies. Those closest to North Korea geographically would be the contenders to rally. This includes the Korean Won, Chinese Yuan, Thai Baht, Indonesian Rupiah, and Malaysian Ringgit. The Singapore Dollar could also benefit.

High-yielding emerging market currencies: higher yielding currencies such as the South African Rand, Mexican Peso and Russian Ruble are strongly reliant on investor appetite towards taking on risk. It would be expected that currencies like the Rand would follow the lead from the global stock markets, if they do rally on indications of a positive summit.

Losers from a positive summit

Gold: the yellow metal has struggled greatly over the second quarter of 2018 from the unexpected resurgence in the USD. Buying sentiment for Gold is highly reliant on market uncertainty and the potential rally in the stock markets, in addition to lower attraction towards safe haven assets would be seen as negative momentum for Gold.

Japanese Yen: similar to Gold, the Japanese Yen relies heavily on its safe-haven status for buying momentum. The potential rally in the stock markets following a positive summit and added risk appetite would consequently be seen as a minus for holding Japanese Yen.

In the event that the summit does not go well, there are also some potential losers in the financial markets:

Chinese Yuan: a leading contender for major loser to a negative outcome in Singapore could unexpectedly be the Chinese Yuan. It would not surprise if President Trump threatens to introduce further trade tariffs on China in an attempt to encourage the country to do more when it comes to influencing North Korea to destroy its nuclear weapons. China is seen as one of the only allies North Korea has.

Korean Won: in the aftermath of the breaking development months ago that Donald Trump and Kim Jong-un would meet, relations between North and South Korea have improved to an extent that some might have thought unimaginable. If the summit takes a negative turn, it can't be ruled out that the Korean Won would sell off on market uncertainty that North Korea could return to testing nuclear capabilities.

Stock markets / emerging market currencies / South African Rand: depending on the extent to which the summit might go down an undesirable path, there is the likelihood of investors entering a 'risk-off' mode if negative headlines overshadow the meeting. Market uncertainty would be seen as a negative for global stocks in the event that risk appetite diminishes and would consequently have a knock-on effect on emerging market currencies. A period of risk aversion would encourage investors to steer close of high-yielding currencies like the South African Rand.

When considering the complexities of Trump and Kim Jong-un getting together, there are a multitude of ways that the summit could potentially impact the financial markets. Although President Trump has said himself that he is meeting the North Korean leader on a 'mission of peace' and by that account the summit should conclude on a positive note, this is still considered as a major risk event for the financial markets and one investors will need to closely monitor.

Awkward G-7 Event| Fed And ECB Meeting Under Focus | Bitcoin Down 52% This Year

The takeaway for investors is that there are more rifts

Fed would be increasing the interest rate.

ECB is determined to tighten the grip on its monetary policy.

The G-7 meeting has been fractious, simply put it was nothing more than a blame game and Mr Trump made the best use of his favourite weapon- Twitter. The takeaway for investors is that there are more rifts and divide between the US, Europe and Canada.

Moving away from the G-7, investor are focused on the upcoming central bank’s meeting this week which would drive most of the trading action for the forex markets (as long as Trump keep things calm on his Twitter account). First, we have the Fed over in the US, who would be increasing the interest rate. This would be the second interest rate hike for this year and the only question which investors would be asking is: how many more interest rate hikes are in the pipeline? Increase in the interest rate would surely spur the rally for the dollar index but what matters most is that how the Fed view the economic health of the country given that there is some serious rift between the US and its important allies.

On Thursday, the ECB would be holding its meeting and one thing which is confirmed is that the ECB is determined to tighten the grip on its monetary policy. The Euro has seen some serious strength against a basket of currencies on the back of this. Inflation has been creeping higher and the economic health of the Eurozone does look stable. Hence, the officials would have to explain about their formal chat about ending the QE.

Bitcoin has touched its two months low and lost half of its value this year. A headline worth paying attention. The crypto king-Bitcoin suffered another blow today and its price tumbled as much as 13%. Exchanges are not utilising the top-notch technology to protect consumers and hackers are taking full advantage of this issue. The South Korean crypto exchange, Coinrail suffered another cyber attack. The question is; is there any limit to these hacks? After every few months, we are seeing the same pattern emerging. This is the result of loose regulatory control and regulators must step in to protect the consumers. Anyone who wants to do with anything with exchanges should be forced to adopt high-grade security and regular security upgrades.

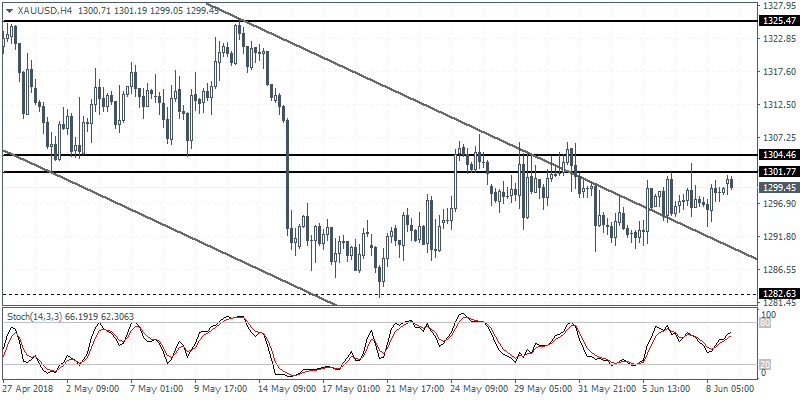

XAUUSD Intraday Analysis

XAUUSD (1299.43): The consolidation in gold prices continues as price action remains subdued below the 1300 level. Still, there is scope for gold prices to extend the declines down to 1282 level in the short term. To the upside, gold prices will need to convincingly breakout above the support level at 1300 in order to confirm the upside toward 1325 level of resistance that is pending a retest. The consolidation could break closer to the FOMC and the ECB meetings that are due this week.

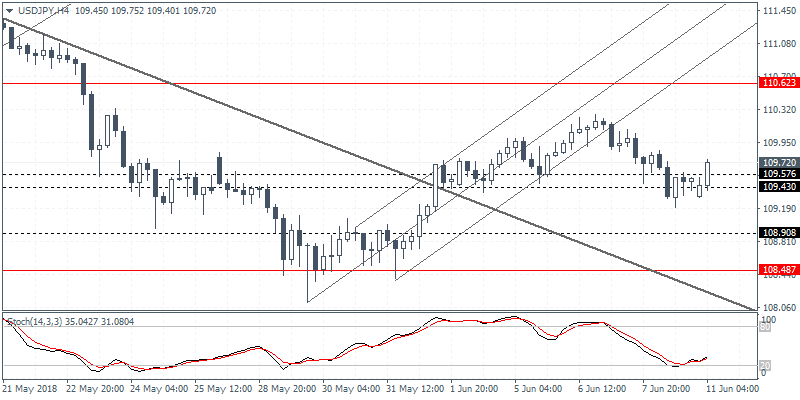

USDJPY Intraday Analysis

USDJPY (109.72): The USDJPY currency pair was seen trading at the support level of 109.57 - 109.43 level. With the support level holding up, we expect to see the currency pair pushing higher in the near term. However, failure to break out above the previous highs could signal weakness in the currency pair. To the upside, the resistance level at 110.62 remains the target, while to the downside, the support level at 108.90 is likely to be tested in the short term.

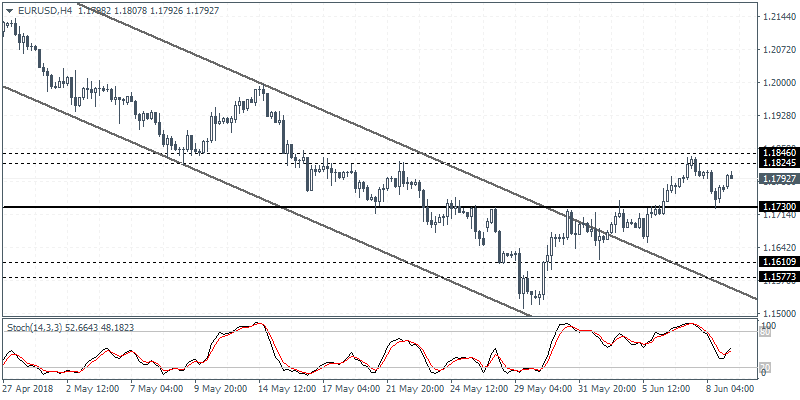

EURUSD Intraday Analysis

EURUSD (1.1792): The EURUSD currency pair managed to hold steady above the 1.1730 support level with Friday's price action seen briefly testing this level. A firm retest of this support could potentially signal a near term correction to the upside as the currency pair targets the resistance level at 1.1960 1.1920 region. On the 4-hour chart with price action making a hidden bullish divergence at the mentioned support, we expect to see the upside being confirmed. However, the EURUSD could remain range bound within the levels of 1.1846 - 1.1730 in the near term, with a breakout off this level confirming the next direction in the trend.

Sterling dips as trade balance and production missed

Sterling dips notably lower after a batch of weaker than expected data.

Visible trade deficit widened to GBP -14.0B in April, from GBP -12.0B, missed expectation of -11.5B.

Industrial production at -0.8% mom 1.8% yoy in April , versus expectation of 0.1% mom 2.7yoy and prior 0.1% mom 2.9% yoy

Manufacturing production at -1.4% mom 1.4% yoy, versus expectation of 0.3% mom 2.9% yoy, and prior -0.1% mom 2.9% yoy.

Construction output rose 0.5% mom in April versus expectation of 2.4% mom and prior -2.3% mom.

The pound will face more tests in CPI, employment and retail sales later in the week.

Markets Open To A Busy Week Of Central Bank Decisions

The U.S. dollar was seen trading mixed on Friday. Investors are looking to a busy trading week that will see the Fed's meeting and the ECB and the BoJ central bank decisions.

On Friday, Japan's GDP showed that the quarterly expansion declined to a revised 0.2%. This was more than the forecasts which suggested that the GDP would be revised to show a decline of 0.1% instead.

Data from the Eurozone continued to remain weak with German industrial production falling 1.0% on a month over month basis. The data comes ahead of the ECB's meeting this week where policy makers are likely to debate on the QE exit plans.

Canada's jobs report showed that wage growth advanced strongly as the unemployment rate held steady at 5.8%. However, the economy posted net decline in jobs. The monthly employment change fell 7.5k on the month extending from 1.1k declines just the month before.

Looking ahead, the economic calendar today will see the release of the UK's manufacturing and industrial production figures. Estimates show that manufacturing production increased 0.3% on the month while industrial production advanced 0.1% on the month.

UK Data In The Spotlight

The United Kingdom's Office for National Statistics will dominate the headlines on Monday with reports on factory output and trade. Currency traders will also be on high alert for geopolitics after US President Donald Trump and North Korea's Kim Jong-un arrived in Singapore over the weekend.

In terms of economic data, the Italian government will kick off the European session with a report on industrial production at 08:00 GMT. Thirty minutes later, the UK government will release the entirety of its data flows for the session.

Industrial production, manufacturing production and the trade balance will all be released at 08:30 GMT. The UK's industrial production index is forecast to grow 0.2% in April, which translates into an annualized growth rate of 2.7%. Manufacturing output is projected to rise 0.3% month-on-month and 2.9% annually.

On the trade front, London's goods deficit likely narrowed to £-11.25 billion in April from £-12.3 billion in March.

The National Institute of Economic and Social Research (NIESR) is also scheduled to release its latest estimate of UK GDP. The report, which is released monthly, measures GDP output on a three-month basis.

Earlier in the day, China reported a sharp acceleration in producer inflation for the month of May. The producer price index (PPI) jumped 4.1% annually, compared with 3.4% in April. Analysts had forecast a reading of 3.8%.

China's consumer price index (CPI) held steady at 1.8% in May.

Monetary policy will dominate the headlines on Tuesday as the Federal Open Market Committee (FOMC) begins its two-day meeting in Washington. On Wednesday, Federal Reserve officials are widely expected to raise interest rates by 25 basis points to 2%.

EUR/USD

Europe's common currency is fresh off its best week since February, as the dollar bulls continued to retreat. EUR/USD peaked around 1.1840 last Thursday before a 100-pip correction dragged prices back down to the low 1.7730 range. At the time of writing, EUR/USD was trading at 1.1782, having gained 0.1% from the previous close. The pair faces strong resistance at last Thursday's high. Meanwhile, immediate support is located at 1.1725.

GBP/USD

Cable's recovery stalled on Friday as investors turned their attention to the G7 Summit in Quebec. Prices have rallied back above 1.3400 but momentum has slowed significantly. GBP/USD is likely to run into resistance near 1.3469, the high from 7 June. On the opposite side of the ledger, immediate support is located at 1.3395.

AUD/USD

The Australian dollar was little changed on Monday as traders continued to assess Chinese inflation figures. AUD/USD continues to hover around 0.7600. Prices swung as high as 0.7678 last week before reversing all the way back down to 0.7664. The short-term outlook remains guided by monetary policy.