Sample Category Title

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1547; (P) 1.1583; (R1) 1.1630; More....

EUR/CHF's rebound from 1.1366 resumed by taking out 1.1639 minor resistance. Intraday bias is back on the upside for 61.8% retracement of 1.2004 to 1.1366 at 1.1760. But after all, the corrective pattern from 1.2004 is expected to extend with at least one more falling leg. Hence, we'll look for reversal signal again above 1.1760. On the downside, break of 1.1505 will suggest that the rebound is completed. And intraday bias will be turned back to the downside for retesting 1.1366.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

Currencies: Euro To Be Better Bid Going Into ECB And Fed Policy Meetings?

Rates: Key central bank meetings looming

Core bonds eventually ended near opening levels on Friday as EM assets managed a late rebound. This week’s event calendar is loaded with the US/North-Korean Summit, Fed and ECB meeting. The Fed might hint at stepping up the tightening cycle, while we expect the ECB to announce an end to QE by end 2018.

Currencies: euro to be better bid going into ECB and Fed policy meetings?

FX traders are looking forward to the Fed and ECB policy meetings this week. Both central banks might sound relatively hawkish. However, the ECB potentially preparing markets for a the end of APP bond buying might be the more important factor for FX markets. Sterling trading faces a series of important eco data and a key vote on Brexit in Parliament

The Sunrise Headlines

- All US markets closed in green before the weekend with no real outliers. This morning, Asian stock markets are opening mixed. Only in Japan we see all markets reaping gains.

- The relations between the US and its allies plunged after the G7 summit this weekend. With a strong German-French critique on Trump’s imposed tariffs and a US backlash at Canadian PM Trudeau. No unanimous G7 communiqué was signed.

- In a referendum on Sunday, Swiss voters have strongly rejected the ‘Vollgeld’ proposal, which would disarm Swiss banks’ ability to create money when giving loans to customers and businesses.

- North-Korean leader Kim Jong Un and US President Donald Trump have landed in Singapore for their historic summit of tomorrow. The pair will discuss whether a possible denuclearisation deal is achievable in the near future.

- Giovanni Tria, Italy’s new finance minister, has assured EU officials that a scenario where Italy will exit the euro is not on the agenda. He said “the new government is clear and unanimous to keep the country inside the euro”.

- In China, the inflation numbers were released on Saturday with a CPI (YoY) of 1.8% (1.8% expected) and a PPI (YoY) of 4.1% (3.9% expected). These numbers are not expected to move policy directions.

- On the economic calendar today we only see the UK with the release of Industrial Production MoM/YoY and Manufacturing Production MoM/YoY for April.

Currencies: Euro To Be Better Bid Going Into ECB And Fed Policy Meetings?

EUR/USD better bid going into policy meeting

On Friday, trading started in a cautious risk-off modus as EM currencies remained under pressure. The unwinding of EM carry trades favoured the dollar. EUR/USD tested the 1.1830/40 resistance area on Thursday, but the test was rejected and USD strength pushed EUR/USD back south in the 1.1510/1.1830 range. However, risk off and the dollar rally eased in US dealings. EUR/USD closed the session at 1.1769 (from 1.1800). The initial save haven bid slightly supported the yen, but the swings in USD/JPY were modest. The pair closed the session at 109.55. Overnight, sentiment in Asia turned cautiously positive. Pressure on most EM currencies is easing slightly, at least for now. There is only little fall-out from the G7 meeting, which shows quite some political division between US and the rest of the group. USD/JPY gains modest ground. (109.80 area). At the same time the euro outperforms. EUR/USD is trading near 1.18. The Italian Fin Min reiterated that an Italian euro exit is not on the agenda.

Today, mostly contains second tier data. Markets will mainly look forward/adapt positions ahead of the Fed policy decision (Wednesday) and the ECB meeting (Thursday). The meeting of president Trump with North Korean leader Kim Yong Un and headlines on the trade conflict between the US and its allies are wildcards for trading. Last week, EUR/USD bottomed and gradually regained some ground. Tensions on Italy moved to the background and the ECB indicated that it is coming closer to a new step in policy normalisation. Both the Fed and the ECB might sound relatively hawkish. Recent US eco data might support the case for two additional rate hikes after a hike this week. However, the ECB preparing markets for the end of APP bond buying in September might be more important for FX markets than the Fed holding course. In this context we assume that markets won’t be keen to be euro short going into the ECB meeting. EUR/USD breaking beyond the 1.1830/40 resistance might support the some further euro gains going into the ECB & Fed meetings.

On Friday, euro strenght and uncerainty on the Brexit proces supported the EUR/GBP cross rate. The pair returned to the high 0.87 area. This week, the UK eco calendar contains key eco data and the house of Commons will vote on key Brexit issues. For now, there is no indication that UK PM May will be able to put a consistent Brexit strategy in place. We assume sterling to stay weak as long as this uncertainty persists.

EUR/USD: euro downside might be well protected as markets look forward to change in ECB guidance

Trade Tensions Return After G7 Ends Without The Support Of US

General Trend:

- Regional equity markets opened mixed tracking Friday US session; trade tensions also returned to front and center after a difficult G7

- S&P futures opened lower by 0.25%

- After leaving, Trump tweets he will not endorse official G7 communique due to due to "false" statements made by Canada PM Trudeau; later followed by another tweet against trade with Canada

- G7 Official Communique (with support from all but the US): We acknowledge free, fair and mutually beneficial trade is key engine for growth and jobs; We strive to reduce tariff barriers, non-tariff barriers and subsidies

- German Chancellor Merkel expresses her disappointment in Trump’s response and says EU is ready with counter tariffs to US if needed

- President Trump and North Korea Kim arrive in Singapore ahead of Summit on June 12th

Headlines/Economic Data

Japan

- Nikkei 225 opened slightly lower

- (JP) JAPAN APR CORE MACHINE ORDERS M/M:10.1% V 2.4%E; Y/Y: 9.6% V 3.8%E

- (JP) Japan May Money Supply M2 y/y: 3.2% v 3.3%e; M3 y/y: 2.7% v 2.8%e

- (JP) LDP-backed candidate Hideyo Hanazumi wins governor race in Niigata seen as a boost for nuclear power and a key ally to PM Abe - Japan press

- Looking ahead: Japan PPI data expected tomorrow

Korea

- Kospi opened +0.1%

- (KR) North Korea agenda for talks with Trump: Expects that the historic summit talks would offer an important occasion in achieving peace and stability of the Korean peninsula; to focus on peace and denuclearization in talks - KCNA

- (KR) North Korea said to have asked US to establish a liaison office - KBS

- (KR) South Korea Fin Min Kim: There are various signs of change between North and South Korea; Asian countries must be wise, the wise build bridges, the foolish build walls

- (KR) South Korea sells KRW1.8T v KRW1.8T indicated in 10-yr bonds at 2.74%; bid to cover 2.88x

- (KR) South Korea cryptocurrency exchange CoinRail was hacked, sending Bitcoin lower - press

- Looking ahead: North Korea Kim and US President Trump hold summit in Singapore

China/Hong Kong

- Hang Seng opened +0.2%, Shanghai Composite -0.3%

- (CN) China and Russia sign deal on nuclear; Russia affirms cooperation with China is at an unprecedented level – press

- (CN) China cuts subsidy for solar power – press

- Hong Kong Aircraft Engineering, 44.HK Swire Pacific makes HK$72/shr offer to privatize in a HK$3B deal

- Luye Pharma, 2186.HK Starts phase 3 clinical trial for LY03005

- (CN) China PBoC Open Market Operation (OMO): Skips OMO for the second consecutive session; Net drain CNY20B v CNY40B drain prior

- (CN) China PBoC sets yuan reference rate at 6.4064 v 6.4003 prior

- (HK) Hong Kong 1-month HIBOR rises to 1.49679%; 3-month rises to 1.96983% (both highest level since 2008)

Australia/New Zealand

- ASX 200 closed for holiday

- (NZ) New Zealand Q1 Manufacturing Activity q/q: 0.6% v 2.8% prior; Activity Volume q/q: 1.4% v 1.0% prior

- (AU) Australia May Port Hedland Iron Ore Exports: 45.0Mt v 42.6Mt prior

Other Asia

- (MY) Malaysia PM Mahathir: US is no longer a good example of free trade; growing countries need some protection on trade

North America

- (US) President Trump: US will not endorse the G7 communique due to "false" statements made by Canada PM Trudeau - financial press citing tweets

- RCII Completes strategic review; updates guidance based on materially improved performance; Did not get any sales offers meeting objectives

Europe

- (CH) SWITZERLAND VOLLGELD REFERENDUM RESULTS: VOTERS REJECT MOTION TO ABOLISH TRADITIONAL BANK LENDING AND ALLOW ONLY MONEY CREATED BY THE SNB (AS EXPECTED)

- (DE) German Chancellor Merkel: EU has prepared counter measures against the US tariffs on steel and aluminum; We wont allow us being ripped off over and over again, we will also act then

- Rolls Royce, RR.UK Expected to announce job cuts totaling 4,000 this week, mostly middle managers and back office staff - UK press

- (DE) Germany Foreign Min Altmaier: Europe will defend its interests against US tariffs; ready to talk about imbalances in trade

Levels as of 01:30ET

- Hang Seng +0.4%; Shanghai Composite -0.4%; Kospi +0.6%; Nikkei 225 +0.5%; ASX200 closed

- Equity Futures: S&P500 +0.1%; Nasdaq100 -0.1%, Dax -0.1%; FTSE100 +0.2%

- EUR 1.1771-1.1808; JPY 109.31-109.84; AUD 0.7561-0.7673;NZD 0.7022-0.7047

- Aug Gold -0.0% at $1,302/oz; Jul Crude Oil -0.2% at $65.58/brl; Jul Copper -0.4% at $3.29/lb

Mexican Guajardo to engage strongly in July on NAFTA

Mexican Economy Minister Ildefonso Guajardo said Mexico, Canada and the US will be "engaging strongly" later in July to work on a NAFTA agreement that 's "feasible, workable and benefits the three nations involved."

He added that "the only way we will find that solution is if countries involved have sufficient flexibility to be able to find that narrow strip where we have to land."

And he warned that "an agreement that does not give us certainty, does not give us rules that have to be obeyed and mechanisms to settle disputes will not be of help for the business community."

New Zealand Parker: None of us can beat globalization

New Zealand Trade Minister David Parker urged the world to stand up to defend rules-based trade system. And he added that "none of us can beat globalization"

He noted that "what's happening in the world worries me. But the world is already developing alternatives like CPTPP".

The Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), also known as TPP-11, was an advanced version of the Trans-Pacific Partnership (TPP) that was signed in March. The US was originally in the TPP but Trump pulled out of it immediately after taking office.

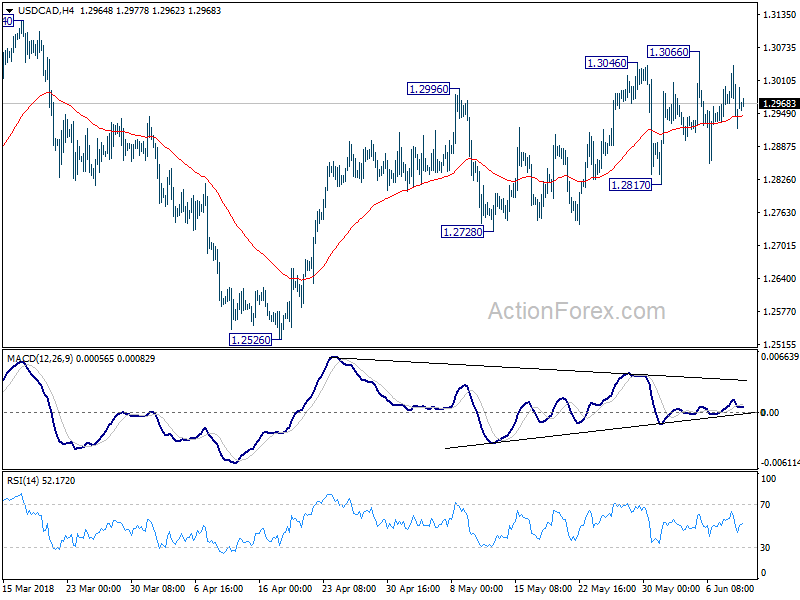

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2892; (P) 1.2960; (R1) 1.3000; More.....

Intraday bias in USD/CAD remains neutral at this point. As long as 1.2817 minor support holds, near term outlook remains cautiously bullish and further rise is in favor. Above 1.3066 will resume the rise from 1.2526 and target 1.3124 key resistance next. However, break of 1.2817 will indicate near term reversal and turn bias to the downside for 1.2728 support and below.

In the bigger picture, we're favoring the case that that rebound from 1.2061 has not completed yet. But there is no follow through upside momentum so far. Focus remains on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

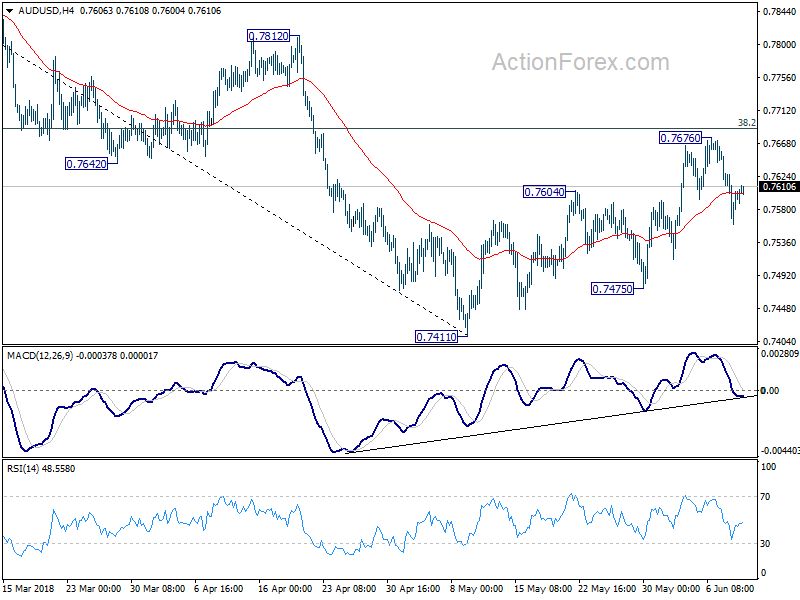

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7563; (P) 0.7595; (R1) 0.7631; More...

No change in AUD/USD's outlook. Corrective rise from 0.7411 should have completed at 0.7676 already, ahead of 38.2% retracement of 0.8135 to 0.7144 at 0.7688. Deeper fall should be seen to 0.7475 support first. Break there should resume larger fall from 0.8135 and target 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326).

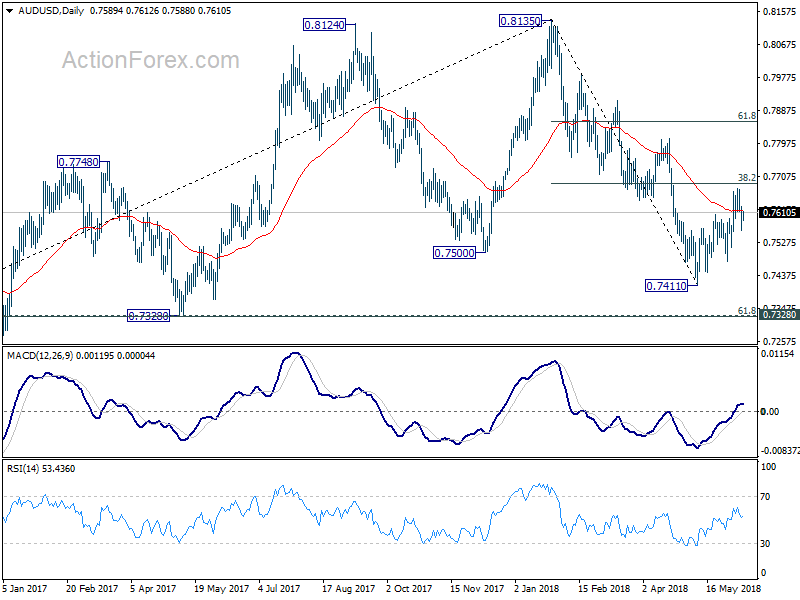

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

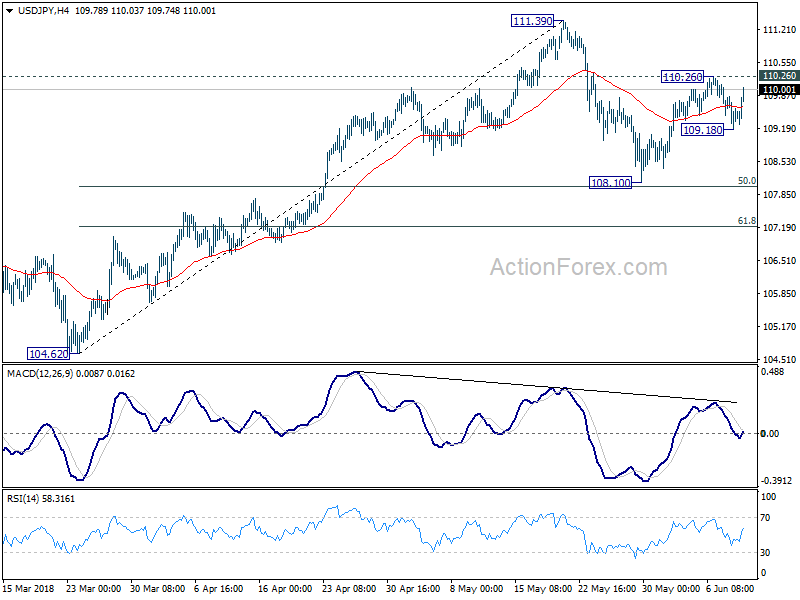

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.20; (P) 109.53; (R1) 109.87; More...

With the current strong rebound, intraday bias in USD/JPY is turned neutral, with focus back on 110.26 resistance. Break there will resume the rebound from 108.10 for a test on 111.39 high. On the downside, below 109.18 will bring another fall to 108.10 or below. Overall, price actions from 111.39 are viewed as a corrective pattern which might extend. But in case of deeper fall, we'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

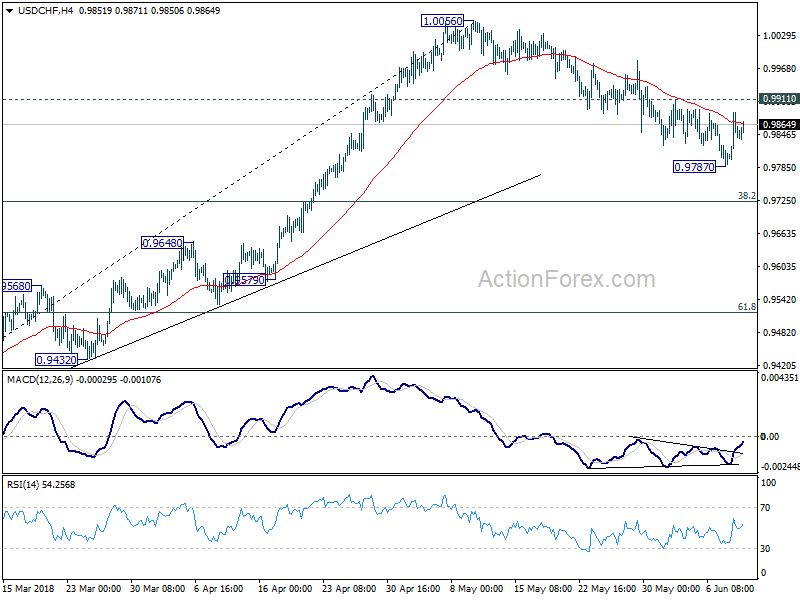

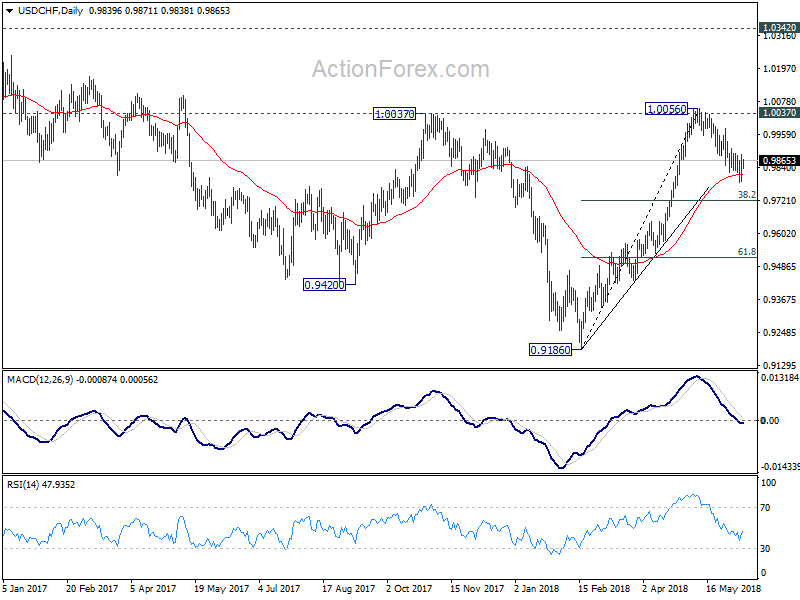

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9798; (P) 0.9843; (R1) 0.9895; More...

Intraday bias in USD/CHF remains neutral at this point. Corrective decline from 1.0056 could still extend lower. But in that case, we'd expect strong support from 0.9724 fibonacci level to contain downside and bring rebound. On the upside, break of 0.9911 will argue that the pull back from 1.0056 has completed. In such case, intraday bias will be turned back to the upside for retesting 1.0056.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

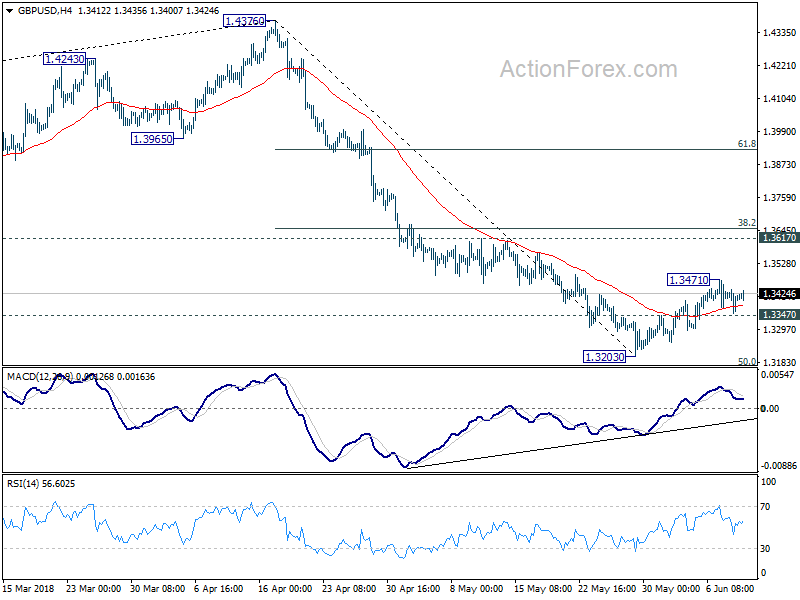

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3364; (P) 1.3402; (R1) 1.3448; More...

Intraday bias in GBP/USD remains neutral at this point. The corrective rebound from 1.3203 could extend higher. But upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3347 minor support should resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 1.3617 resistance holds, even in case of strong rebound.