Sample Category Title

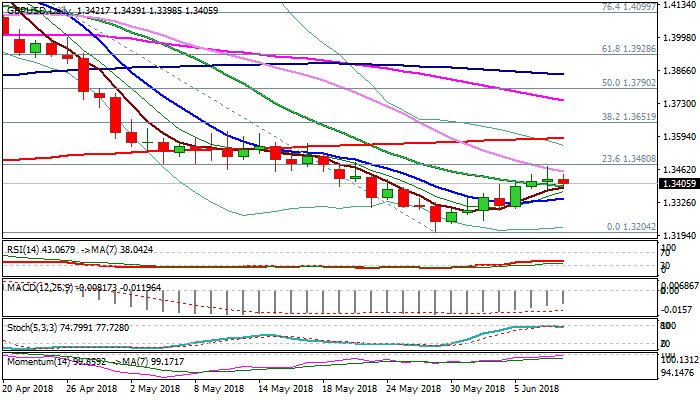

GBPUSD Outlook– Recovery Rally Shows Signs Of Indecision After Being Capped By Falling 30SMA

Cable holds within tight range in the mid-European trading on Friday, signaling further indecision after Thursday’s action ended in long-legged Doji.

The pound was initially supported by upbeat comments from BoE deputy governor Ramsden, but came under pressure after leaked comments from foreign minister Johnson about Brexit collapse.

Recovery leg from 1.3204 low was capped by falling 30SMA on Thursday and Friday’s trading remains below, generating initial signs of recovery stall.

Reversal of slow stochastic from overbought zone and flat RSI support scenario which requires close below 20SMA (1.3390) and today’s close in red to generate reversal signal.

Meanwhile, the pair may hold in extended consolidation between 20 and 30SMA’s, before establishing in fresh direction.

Bullish scenario needs weekly close above 30SMA (1.3454) to signal continuation and expose 200SMA (1.3590).

Res: 1.3454, 1.3480, 1.3520, 1.3590

Sup: 1.3390, 1.3362, 1.3343, 1.3301

European Markets Lower With Focus On G-7, Apple Warns Of 20% Drop On New iPhone Parts

- Risk aversion sentiment seeped back into the markets (concerns on trade, emerging markets and European periphery)

- Awkward G7 leader summit seen as allies poise for showdown with Trump; trade row could deepen

- Fed, ECB and BOJ decisions next week

Asia:

- China May Trade Balance: $24.9B v $33.8Be; Imports Y/Y: 26.0% v 18.8%e

- China Securities Journal reiterated PBoC had room to cut the RRR despite of US Fed rate hike (Note: recent speculation suggested that PBoC might cut the RRR, but raise yields on the MLF facility and reverse repos)

- Japan Q1 Final GDP revised lower and confirmed its 1st contraction in 9 quarters (QoQ: -0.2% v -0.1%e; Annualized : -0.6% v -0.4%e)

- BoJ said to consider cutting inflation forecasts at its upcoming policy meeting on Jun 14-15th (Reminder: In the BoJ’s Quarterly Outlook for Economic Activity (released on April 27th), the central bank then removed the wording on reaching the 2% inflation target around FY19/20)

Europe:

- BOE Dep Gov Ramsden (dove): period of unusually subdued growth in wages appears to be coming to an end. MPC view that the slowdown in early 2018 was temporary has been borne out by data

Americas:

- White House: US President Trump to leave the G-7 in Canada earlier than scheduled. To leave on Saturday to travel to Singapore ahead of meeting with North Korea's Kim

Economic Data:

- (NL) Netherland Apr Manufacturing Production M/M: +0.6 v -0.1% prior; Y/Y: 5.0 v 3.3% prior; Industrial Sales Y/Y: 10.2 v 2.2% prior

- (DE) Germany Apr Current Account: €22.7B v €20.0Be; Trade Balance: €20.4B v €20.2Be; Exports M/M: -0.3% v -0.3%e; Imports M/M: 2.2% v 0.6%e

- (DE) Germany Apr Industrial Production M/M: -1.0% v +0.3%e; Y/Y: 2.0% v 2.8%e

- (DE) Germany Q1 Labor Costs Q/Q: 1.0% v 0.4% prior; Y/Y: 2.3% v 1.5% prior

- (FI) Finland Apr Industrial Production M/M: -1.7% v +2.2% prior; Y/Y: 3.9 v 7.2% prior

- (FR) France Apr Industrial Production M/M: -0.5% v +0.3%e; Y/Y: 2.1% v 2.9%e

- (FR) France Apr Manufacturing Production M/M: 0.4% v 1.3%e; Y/Y: 3.0% v 3.7%e

- (HU) Hungary May CPI M/M: 0.6% v 0.5%e; Y/Y: 2.8% v 2.7%e (3rd straight month back within target range and fastest pace in 15 months)

- (CZ) Czech May Unemployment Rate 3.0% v 3.0%e

- (HU) Hungary Apr Preliminary Trade Balance: €0.5B v €0.8Be

- (SE) Sweden May Average House Prices (SEK): 3.031M v 3.069M prior

- (SE) Sweden May Budget Balance (SEK): 50.6B v 2.8B prior

- (SE) Sweden Apr (SE) Sweden Apr Household Consumption M/M: 0.5% v 0.9% prior; Y/Y: 3.1% v 2.8% prior

- (TW) Taiwan May Trade Balance: $4.4B v $4.3Be; Exports Y/Y: 14.2% v 12.0%e; Imports Y/Y: 12.0% v 9.0%e

- (UK) BOE/TNS May Inflation Survey next 12-months: 2.9% v 2.9% prior

- (GR) Greece May CPI Y/Y: 0.6% v 0.0% prior; CPI EU Harmonized Y/Y: 0.8% v 0.5% prior

- (GR) Greece Apr Industrial Production Y/Y: 1.9% v 1.2% prior

- (IS) Iceland Q1 GDP Q/Q: -2.6% v +0.6% prior; Y/Y: 5.4% v 1.5% prior

Fixed Income Issuance:

- (IN) India sold total INR120B vs. INR120B indicated in 2022, 2028, 2035 and 2045 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.6% at 383.7, FTSE -0.7% at 7649, DAX -1.2% at 12656, CAC-40 -0.3% at 5432, IBEX-35 -0.9% at 9740, FTSE MIB -1.5% at 21433, SMI -0.8% at 8484, S&P 500 Futures -0.6%]

- Market Focal Points/Key Themes: European Indices trade lower across the board in risk off trade, tracking US Index futures lower. The Nasdaq futures trade lower after reports Apple were warning suppliers of 20% drop in component orders for upcoming models, with Apple shares dropping 2% in the premarket on those reports. Tech names in Europe are also under pressure following these reports with Dialog Semi and Infineon trading over 2% lower. Elsewhere Clas Ohlson drops on a miss in earnings, with Air France, Commerzbank and Aberdeen Asset Management other notable fallers this morning. Bucking the trend, BT trades higher after the stepping down of its CEO.

Movers

- Consumer Discretionary Air France [AF.FR] -2.4% (May metrics), Clas Ohlson [CLASB.DK] -11% (Earnings), Fastjet [FJET.UK] -3.2% (Delays earnings)

- Materials Kaz Minerals [KAZ.UK] -6.5% (Investment by NFC into Koksay project)

- Technology Dialog Semi [DLG.DE] -3.2%, Infineon [IFX.DE] -2.1% (Tech sector pressure)

- Financials Standard Life Aberdeen [SLA.UK] -3.5% (Lloyds places shares), Deutsche Bank [DBK.DE] -1.6%, Commerzbank [CBK.DE] -2.3% (Reportedly resurfacing of potential merger talks)

Speakers

- ECB’s Mersch (Luxembourg): Should maintain the flexibility of collateral framework (**Note: ECB now in blackout period ahead of next week’s rate decision)

- German Fin Min Scholz: Look to avoid a hard Brexit. Wanted to maintain a close cooperation with UK in the future. Optimistic on an agreement for the ESM in coming weeks (**Note: look to have it turned into an IMF-like facility)

- Ireland Dep PM Coveney (also foreign Min): Welcomed UK proposal on backstop; regulatory issues still needed to be addressed

- Italy Industry and Labor Min Di Maio (also Dep PM): Will ask for more funds from EU 7-year budget plan

- Italy European Affairs Min Savona: Need to strengthened the EU single market and Euro

- Bank of Italy (BOI) Director Rossi: Wider BTP-Bund spread due to concerns over Euro exit risk

- ESM said to have postponed a €1.0B decision regarding a bailout payment on Greece. Looking for confirmation for some payment of arrears reduction by the Greek govt

- Russia Central Bank (CBR) Gov Nabiullina stated that she saw a real discussion on interest rates at the upcoming meeting (Fri, Jun 15th). Inflation expectations remained unanchored and volatile

- China govt said to be scraping the rules on foreign ownership in domestic banks and asset management companies

Currencies

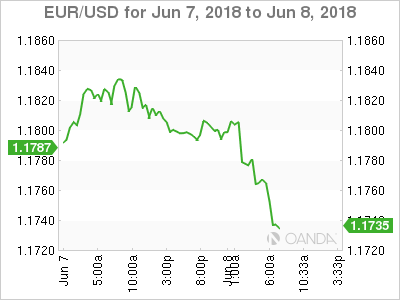

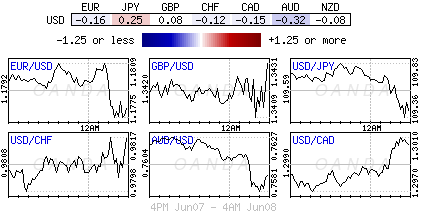

- Risk aversion sentiment seeped back into the markets on Friday with concerns that the US trade row could deepen amongst its own allies and continued concerns over emerging markets. Market participants anticipated an awkward G7 leader summit as allies seemed poise for showdown with Trump. Also reports circulating that Apple warned on a 20% decline in new iPhone parts orders weighed on the tech sector. USD, CHF and JPY were the main beneficiaries of the safe-haven flows

- EUR/USD moved back below the 1.18 level as Italian yields continued to edge higher with the 10-year BTP yield above 3.07%.

- GBP/USD saw its initial gains ebbed away and was retesting the 1.34 just ahead of the NY morning. . Market did like the recent proposal on the backstop from the UK. In summary the UK would not leave the customs union until permanent arrangements could be put in place, possibly involving new technologies that avoid the emergence of a visible border between Northern Ireland and the Republic of Ireland

- USD/JPY testing below the 109.30 level for 1-week lows due to safe-haven flows

- Emerging market currencies were weaker with South African Rand off 2% to test above 13.25 and the Turkish Lira giving back over half of Thursday’s gains despite the aggressive rate hike by the CBRT.

Fixed Income

- Bund Futures trade 39 ticks higher at 160.58 following the move in Treasuries as the FX risk-off move hits emerging markets. Upside targets 161.75 followed by 162.50, while a return lower targets the 159.25 level.

- Gilt futures trade at 123.07 higher by 29 ticks and off the lows of the week. Support continues stands at 122.75 then 122.25, with upside resistance at 124.85 then 126.35.

- Friday’s liquidity report showed Thursday’s excess liquidity rose from €1.922T to €1.924T. Use of the marginal lending facility decreased from €146M to €92M.

- Corporate issuance saw 4 issuers raise $3.7 in the primary market

Looking Ahead

- (G7) Leader Summit

- (UR) Ukraine May CPI M/M: 0.5%e v 0.8% prior; Y/Y: 12.3%e v 13.1% prior

- 05:30 (ZA) South Africa to sell ZAR600M in I/L 2022, 2033 and 2046 bonds

- 06:00 (PT) Portugal Apr Trade Balance: No est v -€1.2B prior

- 06:00 (IE) Ireland May Live Register Monthly Change: No est v -3.1K prior; Live Registry Level: No est v 229.6K prior

- 06:00 (UK) DMO to sell combined £4.0B in 1-month, 6-month and 12-month Bills (£1.5B, £1.0B and £1.5B respectively)

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (BR) Brazil May IBGE Inflation IPCA M/M: 0.3%e v 0.2% prior; Y/Y: 2.7%e v 2.8% prior

- 08:00 (CL) Chile May CPI M/M: 0.3%e v 0.3% prior; Y/Y: 2.0%e v 1.9% prior

- 08:00 (CL) Chile May CPI Ex Food and Energy M/M: 0.2%e v 0.3% prior; Y/Y: No est v 1.6% prior

- 08:00 (UK) EU Chief Brexit Negotiator Barnier:

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:15 (UK) Baltic Dry Bulk Index - 08:15 (CA) Canada May Annualized Housing Starts: 220.0Ke v 215.3K prior (revised from 214.4K)

- 08:30 (CA) Canada May Net Change in Employment: +23.5Ke v -1.1K prior; Unemployment Rate: 5.8%e v 5.8% prior

- 08:30 (CA) Canada Q1 Capacity Utilization Rate: 86.4%e v 86.0% prior

- 08:30 (CL) Chile Central Bank Traders Survey

- 10:00 (US) Apr Final Wholesale Inventories M/M: 0.0%e v 0.0% prelim, Wholesale Trade Sales M/M: No est v 0.3% prior

- 11:00 (EU) Potential sovereign ratings after the European close (Iceland and Poland Sovereign Debt to be rated by Fitch; Iceland Sovereign Debt to be rated by S&P)

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 21:30 (CN) China May CPI M/M: No est v -0.2% prior; Y/Y: 1.8%e v 1.8% prior; PPI Y/Y: 3.9%e v 3.4% prior

Trump said to straighten out unfair trade at G6+1

Trump continues to "sound" agressive ahead of the G6+1 meeting in Canada. But hold on for a minute, didn't he plan to leave early? So did he expect to accomplish what he said so quickly? Or he expects to fail before doing it, and yells some empty protest slogan?

https://twitter.com/realDonaldTrump/status/1005033088202756097

Btw, he blasts Canada again with isolated information.

https://twitter.com/realDonaldTrump/status/1005030839019802625

Risk Aversion Seen Ahead Of Hostile G6+1 Summit

- Trade a Touchy Subject as Trump Isolates US Ahead of Quebec Meeting;

- May Heads to Canada After Tough Week as Brexit Continues to Divide;

- Canadian Jobs Data Eyed Ahead of Possible Rate Hike in July.

Trade a Touchy Subject as Trump Isolates US Ahead of Quebec Meeting

Financial markets are in risk aversion mode ahead of the G7 summit in Quebec on Friday, with investors potentially concerned as leaders clash over trade and other issues.

While Trump has at times appeared friendly with certain other heads of state in the past, the relationships have at least appeared to have become more hostile since tariffs were imposed on the European Union, Canada and Mexico by the US last week. The G7 meeting has become more like a G6+1, with Trump choosing to isolate the US on a number of issues from trade to Iran and climate change.

Macron himself made reference to this in a tweet on Thursday which Trump quickly followed with one of his own attacking the EU and Canada over trade tariffs and non-monetary trade barriers. None of this makes investors particularly hopeful that the two “allies” will reach an agreement and avoid an escalation of the trade spat that has caused so much worry for investors.

They may have taken last week’s tariffs in their stride, largely because it had been lined up for months and priced in, but further escalations will weigh on confidence in the markets and could trigger further corrections. We still haven’t fully recovered fully from the correction after the turn of the year – Dow just under 5% off its highs, S&P 500 more than 3% - and that is partly due to the ongoing spat between the US and its major trading partners.

May Heads to Canada After Tough Week as Brexit Continues to Divide

Theresa May is going to the G7 summit after a difficult week at home, as internal Brexit discussions continue to run into difficulty on how to resolve the Irish border dispute. May appeared to have come very close to losing her Brexit Secretary this week at a critical time in negotiations but managed to persuade him to stick around after putting a backstop date in place.

Talks won’t get any easier from here though which may limit any upside in the pound that has benefited over the last couple of weeks from broad dollar weakness. Brexiteers on her team have been very vocal in their disagreement over her backstop strategy and are clearly concerned that May is embarking down a path towards a soft Brexit or worse, delaying Brexit for a long enough time that it could be reversed altogether. The split is not helping negotiations at all and could make the next few months very uncomfortable for investors.

Canadian Jobs Data Eyed Ahead of Possible Rate Hike in July

It’s looking a little quiet on the economic calendar, with Canadian jobs data and the Baker Hughes oil rig count the only notable releases. The Bank of Canada is widely expected to raise interest rates at least once this year, with the next meeting in July almost 70% priced in, so the data will be followed very closely for signs that this could be pushed back.

Dollar In Demand Ahead Of G6+1

Friday June 8: Five things the markets are talking about

Global equities saw red overnight, as tech stocks continued their retreat in the Asian session, while in Europe, stocks has been hampered by disappointing industrial production data from Germany.

All market negativity is supporting investors’ risk-off mood ahead of today’s G7 summit beginning in Quebec, Canada.

The G6+1 meeting is expected to be an intense affair amidst heightened trade tensions between the U.S and some of its closest allies.

Naturally, the market is looking for further clues on trade after the Trump administration’s decision last week to impose tariffs on steel and aluminum imports from fellow G-7 countries. With President Trump already announcing that he is leaving early on Saturday don’t expect much to be achieved.

U.S Treasuries are steady after 10-year yields tumbled as much as -9 bps yesterday, and the dollar has edged higher.

On Tap: Canadian employment numbers are expected at 08:30 am EDT.

1. Stocks see red

In Japan, the Nikkei share average snapped a four-day winning streak overnight as investors stayed on the sidelines ahead of major economic events, while large-cap stocks weighed on the index. The Nikkei ended -0.6% lower, but is still up +2.4% for the week, its biggest gain in nearly three-months. The broader Topix fell -0.4%.

Down-under, Aussie shares ended lower in light trading as investors kept to the sidelines ahead of key central bank meetings next week with losses in industrial and material stocks outweighing gains in consumer and energy stocks. The S&P/ASX 200 index was down -0.2%. It advanced nearly +1% this week, in its first weekly gain in four. In S. Korea, the Kospi was down -0.7%.

In China and Hong Kong stocks fell overnight, as investors were worried about the impact from the listings of big-caps, and amid uncertainty over trade relations. The CSI300 index was down -1.3%, while the Shanghai Composite Index also lost -1.3%. In Hong Kong, the Hang Seng index dropped -1.2%, while the Hong Kong China Enterprises Index lost -1.3%.

In Europe, regional bourses trade lower as the risk-off trade intensifies, and is tracking U.S index futures lower. The tech sector in particular has been one of the hardest hit on rumours that Apple has warned on a -20% decline in new iPhone parts orders.

U.S stocks are set to open deep in the ‘red’ (-0.6%).

Indices: Stoxx600 -0.6% at 383.7, FTSE -0.7% at 7649, DAX -1.2% at 12656, CAC-40 -0.3% at 5432, IBEX-35 -0.9% at 9740, FTSE MIB -1.5% at 21433, SMI -0.8% at 8484, S&P 500 Futures -0.6%

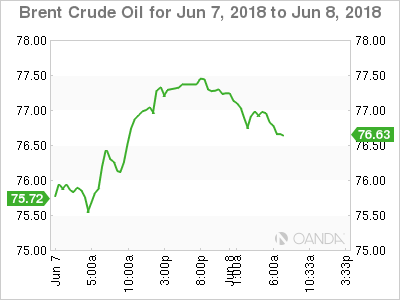

2. Oil prices fall on dip in China demand, surging U.S output, and gold higher

Oil prices are under pressure as signs of weakening demand in China and surging U.S output weighs on markets despite support from supply woes in Venezuela and OPEC’s production cuts.

Brent crude futures are at +$76.79 per barrel, down -53c, or -0.7%, from yesterday’s close. U.S West Texas Intermediate (WTI) crude futures are down -38c, or -0.6% at +$65.57 a barrel.

Customs data this morning showed that China’s May crude oil imports eased away from a record high hit the previous month, with state-run refineries entering planned maintenance.

May shipments were +39.05m tonnes, or +9.2m bpd vs. the +9.6m bpd in April.

Further weighing on prices has been surging U.S output. According to this week’s EIA report, it hit another record last week at +10.8m bpd.

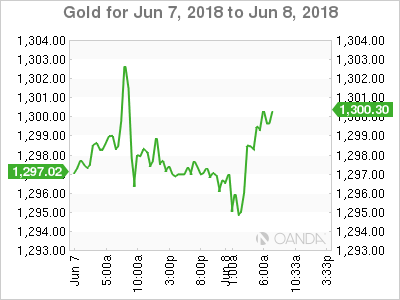

Ahead of the U.S open, gold prices have eased as the dollar has inched up, while investors’ remain cautious ahead of today’s G7 meeting and other key events next week such as a U.S Federal Reserve policy meeting and a U.S-North Korea summit (June 12).

3. Investor demand push sovereign yields lower

In Europe, the cost of insuring exposure to Italy’s sovereign debt has jumped this morning due to broad-based global risk aversion and unease about Rome’s spending plans, prompting a sell off in Italy’s government bonds.

Italian two-year BTP yields have rallied +20 bps to +1.775% percent, while a rise in 10-year BTP yields pushed the gap over benchmark German Bund yields to around +265 bps – the widest in around two-weeks. Under risk aversion, Germany’s 10-year Bund yield has fallen -5 bps to +0.43%.

Elsewhere, the yield on 10-year Treasuries fell -1 bps to +2.91%, the lowest in a week, while in the U.K the 10-year Gilt yield sank -4 bps to +1.4%, the largest tumble in more than a week.

4. Dollar in demand ahead of G6+1

There are no surprises that risk-aversion dominates proceedings ahead of today’s G6+1 summit on concerns that the U.S trade row could deepen.

EUR/USD (€1.1770) is again trading below the psychological €1.18 level as Italian yields continued to edge higher and widen the spread to Bunds.

GBP/USD (£1.3412) is again being dominated by Brexit proceedings. The market does not seem to like the recent proposal on the ‘backstop’ from the U.K.

Note: The U.K would not leave the customs union until permanent arrangements could be put in place, possibly involving new technologies that avoid the emergence of a visible border between Northern Ireland and the Republic.

USD/JPY (¥109.38) testing lower, trading atop of its one-week lows due to safe-haven flows.

5. German industrial output, exports fell in April

Early morning data showed that German industrial production and exports declined in April compared with March. Again, this would suggest that Europe’s largest economy is struggling to gain momentum following a weak Q1.

According to the Federal Stats office, German industrial output dropped -1.0% from March while exports slipped -0.3%. Market consensus had expected a small increase in industrial production.

Data published Thursday showed that German manufacturing orders dropped for the fourth consecutive month in April, which suggest that the slowdown has indeed entered Q2.

Note: Germany’s annualized growth rate slowed to +1.2% in Q1 from +2.5% in Q4, 2017.

DAX Slides Ahead Of Possible Showdown At G-7

The DAX index has recorded sharp losses in the Friday session. Currently, the DAX is at 12,707, down 0.82% on the day. Earlier in the day, the DAX had declined more than 1.0 percent. On the release front, German numbers missed expectations. German Industrial Production declined 1.0%, well off the estimate of 0.4%. Germany's trade surplus narrowed to EUR 19.4 billion, short of the estimate of EUR 20.3 billion. Later in the day, leaders of the Group of 7 will gather for a two-day meeting in Quebec City.

It was a disappointing week for Germany manufacturing indicators, which pointed to a contraction in the key manufacturing sector in April. Factory orders declined 2.5%, its worst showing in three months. On Friday, Industrial Production fell 1.0%, marking the fourth decline in five months. Germany is considered the locomotive of the eurozone – if German numbers continue to miss expectations, investor sentiment over the eurozone economy could sour and weigh on European stock markets.

The markets are bracing for a rough-and-tumble meeting of heads of state at the G-7 meeting in Quebec City, on Friday and Saturday. The gathering comes at a time of escalating trade tensions between the U.S and some of its major trading partners. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. The trouble started last week, when the Trump administration slapped stiff tariffs on Canada, Mexico and the European Union. This resulted in threats of retaliation, and Canada and Mexico have already announced duties on a range of U.S products. Will we see a higher profile, repeat performance at this meeting? The tariff spat is sure to dominate the summit, where Trump can expect to hear strong complaints from other leaders over the recent tariffs, which Trump justified on the grounds of ‘national security'. If the leaders fail to resolve matters, the result could be a nasty trade war between the U.S and its major trading partners, which would be bad news for global stock markets.

Euro Dips On Soft German Data

EUR/USD has posted gains in the Friday session. Currently, the pair is trading at 1.1766, down 0.28% on the day. On the release front, German numbers were a disappointment. German Industrial Production declined 1.0%, well off the estimate of 0.4%. Germany’s trade surplus narrowed to EUR 19.4 billion, short of the estimate of EUR 20.3 billion. French Industrial Production also declined, with a reading of -0.5%. This missed the estimate of 0.4%. There are no major U.S events on the schedule. Later in the day, leaders of the Group of 7 will gather for a two-day meeting in Quebec City.

Is the German manufacturing sector in trouble? After a sluggish first quarter, analysts were hoping for a rebound in manufacturing data in the second quarter. However, this week’s manufacturing indicators are pointing to a downturn in April. Factory orders declined 2.5%, its worst showing in three months. On Friday, Industrial Production fell 1.0%, marking the fourth decline in five months. As the locomotive of the eurozone, German indicators can have a strong impact on the euro exchange rate – if German numbers continue to miss expectations, investors could give the euro a thumbs down and send it lower.

The upcoming G-7 meeting in Quebec is being closely monitored, as the summit comes at a time of escalating trade tensions between the U.S and some of its major trading partners. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. The trouble started last week, when the Trump administration slapped stiff tariffs on Canada, Mexico and the European Union. This resulted in promises of retaliation, and Canada and Mexico have already announced duties on U.S products. Will we see a higher profile, repeat performance at this meeting? The escalating trade battle is sure to dominate the summit, where Trump can expect to hear strong complaints from other leaders over the tariffs, which Trump justified on the grounds of ‘national security’. If the leaders fail to resolve matters, the result could be a nasty trade war between the U.S and its major trading partners.

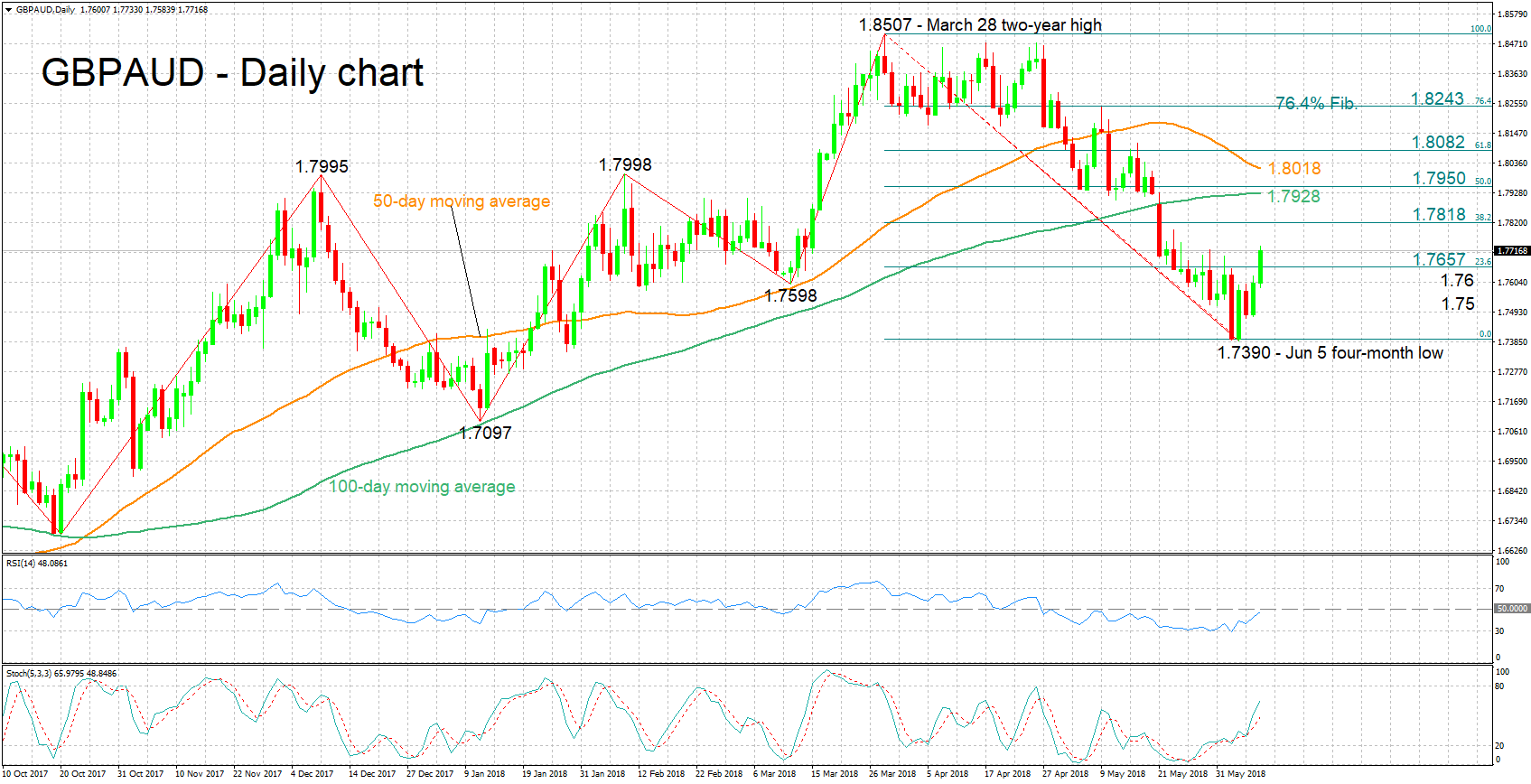

GBPAUD Posts Two-Week High, Medium-Term Outlook Looks Mostly Bearish

GBPAUD is experiencing notable gains for the second straight day, having risen by around 120 pips so far on Friday. Earlier in the day, it also recorded a two-week high of 1.7733.

The RSI is rising in support of a positive short-term picture, while the stochastics are also projecting a bullish picture in the very short-term. Specifically in the case of the latter, the %K line has moved above the slow %D one and both lines are heading higher.

Further advances might meet a barrier around the 38.2% Fibonacci retracement level of the March 28 to June 5 downleg at 1.7818; the area around this also encapsulates the 1.78 round figure. Stronger gains would turn the attention to the region around the current level of the 100-day moving average at 1.7928.

On the downside, the range around the 23.6% Fibonacci mark at 1.7657 failed to act as a barrier on the way up earlier on Friday and might instead provide support to declines. In case of shaper losses, the 1.76 (the area around this also includes a bottom from around mid-March at 1.7598) and 1.75 handles may also act as support.

Despite the considerable upside movement lately, the medium-term picture is looking predominantly negative at the moment with price action taking place below the 50- and 100-day moving average lines. Should the positive short-term momentum remain in place for a while longer though, pushing prices roughly up to the 50% Fibonacci level at 1.7950, then the view for a bearish outlook would no longer be valid.

Overall, the near-term bias is positive, and the medium-term outlook is currently looking mostly bearish.

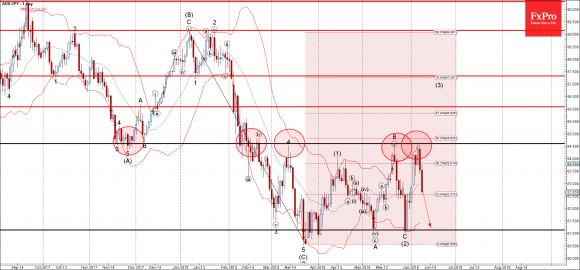

Forex Analysis: AUDJPY Wave Analysis

AUDJPY reversed from resistance zone

Further losses are likely

AUDJPY recently reversed down from the resistance zone lying between the strong resistance level 84.60 (which has been reversing the pair from February), upper daily Bollinger Band and the 50% Fibonacci retracement of the previous sharp downward impulse (C) from January.

The downward reversal from this resistance zone created the daily Japanese candlesticks reversal pattern Bearish Engulfing (the previous reversals from this resistance zone created the daily Evening Star).

AUDJPY is expected to fall further and re-test the next major support level 81.10 (which stopped the previous waves A and (2) in May).

Trump Sends Markets To Risk-Off

Markets switch to risk-off mode as G7 meeting kicks off

Global equities took a hit on the last trading day of the week as investors reallocates their portfolio toward less risky assets. The move was similar in the FX market with the US dollar extending gains against most of its peers, with the exception of the Japanese yen (up 0.25%) and the Swiss franc (range bound). The Eurostoxx 600 gave up 0.65%, the DAX slid 1.40%, while the SMI fell 0.85%. EUR/USD was unable to break the 1.1854 resistance to the upside and eased below 1.1770. After tumbling on its 200dam, USD/JPY fell to 109.35. The currency pair is heading towards its 50dma, which currently stands at 108.84. A break of the latter resistance would open the door towards 108.11 (low from May 29th).

Against such a backdrop, emerging market are bearing the brunt of the sell-off. The South African rand lost another 2% this morning and reached its weakest level against the greenback since December last year amid disappointing economic data. The Brazilian real gave up 1.44% yesterday as USD/BRL hit 3.9657 amid mounting concerns over upcoming elections. INR, KRW, PHP and IDR were no exception as they fell 0.70%, 0.65%, 0.58% and 0.45% against the greenback, respectively.

Trade tariffs discussions will be at centre stage at today G7 meeting in Canada. The US will find themselves isolated as Donald Trump managed to make enemy of most of its allies.

Strategic long EUR/USD

The European Central Bank meeting next Thursday will indicate the end of asset purchases. Council members say that if inflation remains stable, bond buying should be taper. We think that markets are focused on the pure economic data. However, the ECB decision is more practical than fundamental, because Quantitative Easing has expanded its balance sheet to destabilizing heights. ‘Moral hazard' has increased, as highlighted by the recent Italian political chaos. The ECB wants to avoid owning more than one-third of any nation's sovereign debt, which after years of buying is coming dangerously close. Stealth ‘debt mutualisation' in the Eurozone is really happening. Moreover, the ECB wants to reclaim its tools. With a bloated balance sheet and negative rates, the bank has few policy options, should Europe hit a shock. Just as the US Federal Reserve in 2013 saw normalization not just as a function of economic data, so now does the ECB.

Ending QE does not necessary mean higher interest rates, which are expected to come 6-8 months after ECB completely tapers. We remain constructive on EUR/USD as the US rate hike cycle is nearing the end while ECB is nearing the start. We see the current 1.1765 as a good position to reload strategic longs.