Sample Category Title

Weekly Focus: Mother of All Weeks

Market movers ahead

- Next week is swamped with key events to follow. On Monday, the outcome of the G7 meeting will be digested ahead of the highly expected meeting between US President Donald Trump and North Korean peer Kim-Jong Un in Singapore on Tuesday.

- From Wednesday to Friday, the focus turns to very important central bank meetings. On Wednesday, the FOMC will meet and we expect it to hike the policy rates again and take another step closer to a neutral rate. On Thursday, the ECB meets to decide whether it take another step in forward guidance. We think this would be premature and await an announcement only in July but we do expect hawkish bits for next week. Finally, on Friday, the Bank of Japan is due to meet, although we have no expectations for new policy signals.

- The US-China trade war will be on full display on Friday, when we expect the US President to decide whether he will impose a tax on Chinese exports worth USD50bn.

- In Scandinavia, Danish and Swedish inflation are set to be in focus on Monday.

Global macro and market themes

- Global growth has slowed but is set to stay above the potential growth rate.

- Volatility has increased but fundamentals are still solid.

- We expect gradual monetary policy tightening amid muted inflation pressures.

Week Ahed – Policy Shift Looms As Fed And ECB Meet, UK And US Inflation Also In Focus

All eyes will be on the US Federal Reserve and the European Central Bank next week as the two central banks are expected to take further steps towards policy normalization. In contrast, the policy meeting by the Bank of Japan is anticipated to be a non-event. Economic data will also be making the headlines as inflation figures are released in the UK and the US, employment numbers are due in Australia and the UK, and retail sales data will be watched in China, the UK and the US.

Aussie to look to domestic and Chinese data to extend gains

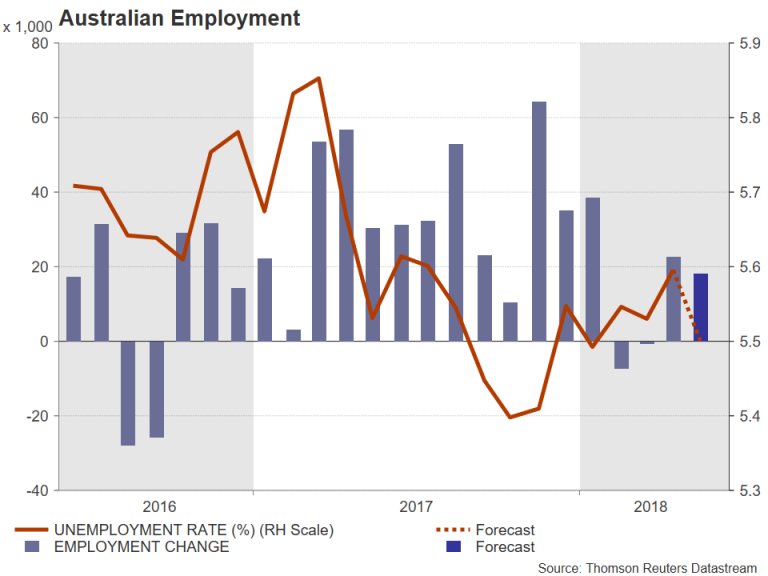

The Australian dollar was boosted this week from upbeat indicators out of Australia but hit a wall at the six-week high of $0.7676. Data due in the coming seven days could decide whether the current upside correction has more room to run. First on the calendar is the NAB business confidence index for May on Tuesday along with April housing finance figures. On Wednesday, Westpac’s consumer sentiment gauge is due, but Thursday will be the most important day for aussie traders as the latest employment report is published and a batch of Chinese data are released too.

Australia’s economy is forecast to have added 18k jobs in May and the jobless rate is expected to tick down to 5.5% from 5.6%. Strong jobs gains on the back of the past week’s robust first quarter GDP print could push the aussie to break past its resistance barrier, especially if there is additional support from Chinese indicators. China’s annual growth in retail sales, industrial output and investment in urban areas are all forecast to hold steady in May near April’s levels.

Fed to raise rates; will it signal steeper path?

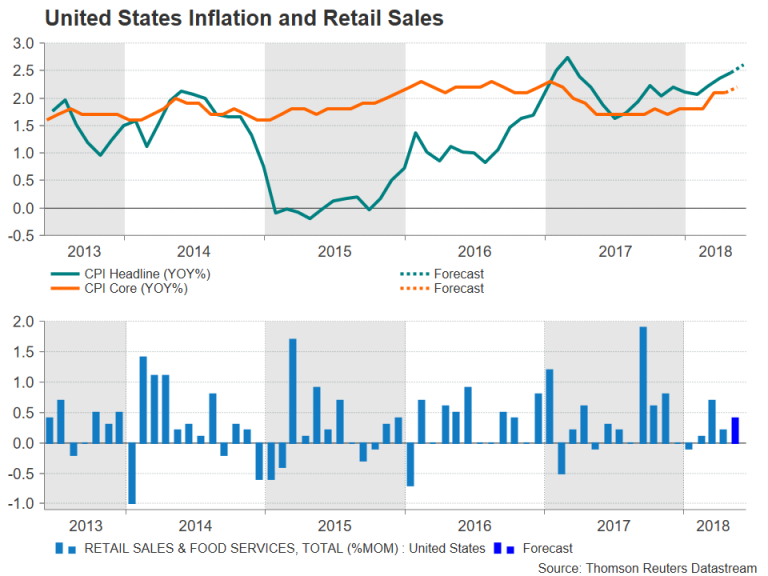

The Fed will be the first of three central banks to announce its latest monetary policy decision next week, but US data also look set to keep traders busy. US inflation numbers are due on Tuesday with the consumer price index expected to edge up to 2.6% year-on-year in May, which would make it a 15-month high. Core CPI is also forecast to inch higher by 0.1 percentage points, to 2.2% y/y. Producer prices will follow on Wednesday, and on Thursday, retail sales will be in focus. The headline measure of retail sales is forecast to rise by 0.4% month-on-month in May, doubling from the prior 0.2%. On Friday, there will be more important indicators to round up the week. Industrial output is expected to post a third straight month of positive growth, rising by 0.3% m/m. Other data to watch are the University of Michigan’s preliminary consumer sentiment index and the Empire State Manufacturing index, both for June.

If the data sticks to the recent positive trend, it could invite enough bulls to return to the market and drive the US dollar back towards the May top of 111.39 yen. However, the dollar’s direction will more likely be directed by the Fed’s latest quarterly economic projections on Wednesday. The Federal Open Market Committee (FOMC) is widely expected to raise the fed funds rate by 25 basis points to a target range of 1.75-2.00%. The FOMC will also publish its updated dot plot chart, which plots the Fed’s projected rate path. If the chart shows the median number of rate hikes for 2018 increasing from three to four, which is possible after the recent run of solid US data, that would signal a hawkish shift, while if the expected rate increases remain at three, it would be perceived as somewhat dovish.

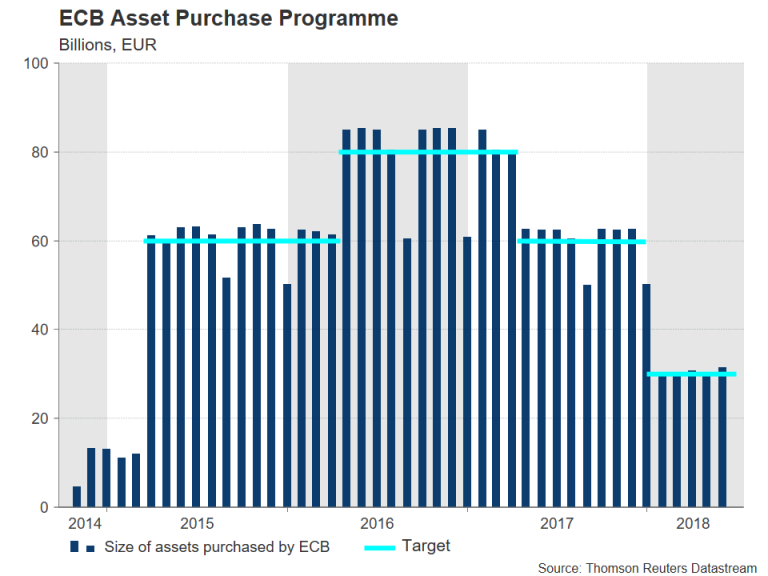

ECB to discuss ending QE

The European Central Bank’s policy meeting on Thursday is building up to be to next week’s most anticipated event following strong hints by senior bank policymakers that the Governing Council will discuss putting an end date to the asset purchase program (APP) when they meet in Latvia on June 13-14. If the ECB announces that the APP will end by December 2018, as expected, that would pave the way for the first rate increase since the Eurozone debt crisis in 2011 to arrive sometime in the middle of 2019. The euro has been gaining on those expectations, charging above the $1.18 level. However, euro bulls run the risk of being disappointed if the ECB surprises by deciding a longer taper period of six months instead of three (current program expires in September), or the forward guidance is more cautious than expected (e.g. keeps the option open for a further extension to the APP if needed).

Ahead of the ECB decision, Germany’s ZEW economic sentiment gauge will be released on Tuesday. The index is forecast to tumble to a 5½-year low of -12.4 in June as export-dependent German businesses fret about escalating trade tensions. On Wednesday, industrial production figures will be out for the euro area, and on Friday, the final reading of the Eurozone CPI for May will be published. No revision is expected to the flash CPI figure of 1.9% – a 13-month high.

BoJ to hold rates as inflation progress stalls

The last central bank decision will come from the Bank of Japan on Friday. With Japanese inflation appearing to have peaked in recent months, few are expecting any changes to BoJ monetary policy next week. Growth in Japan has also been weaker since the start of the year, further clouding the timing for a stimulus exit by the BoJ. Although the Japanese central bank has already been slowly reducing the amount of government bonds it purchases since introducing its yield curve control in September 2016, its policy of ultra-loose monetary stimulus is expected to last well into 2019, if not into 2020.

In the meantime, investors will likely hear little new from BoJ Governor, Haruhiko Kuroda, at his press conference next week. The yen is also not expected to see much reaction to Japanese data, consisting of Monday’s machinery orders and Tuesday’s corporate goods prices.

UK inflation and jobs reports eyed

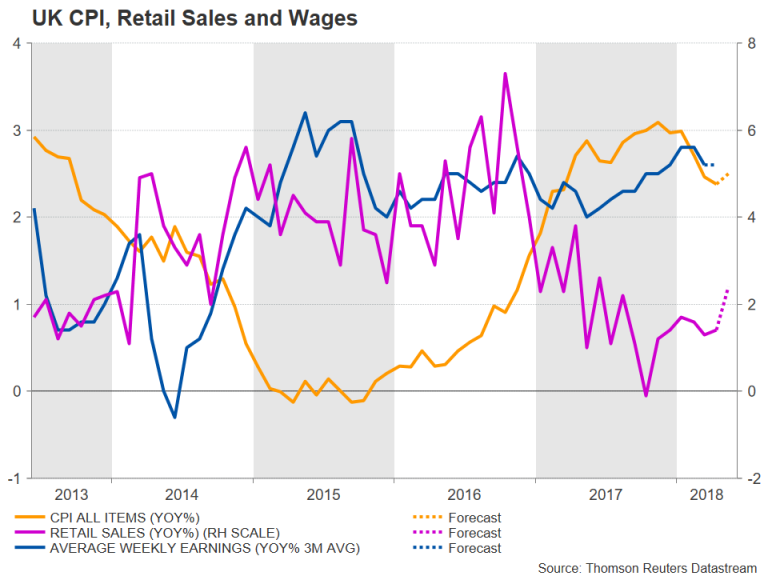

The UK will have one of the busiest calendars next week, comprising of several key data releases. Industrial and manufacturing figures will start the week on Monday. Industrial output is expected to have risen by 0.2% m/m in April, while manufacturing production is forecast to grow by 0.3%. Also due on Monday are trade numbers for April. On Tuesday, the latest employment report will be watched closely for possible signs of accelerating wage growth. Britain’s unemployment rate is forecast to remain at 4.2% in the three months to April. But there’s unlikely to be a pick-up in wage growth as average weekly earnings are anticipated to see an annual increase of 2.6% in the three months to April, unchanged from the prior period.

Inflation figures are up next on Wednesday. The 12-month CPI rate has been falling short of expectations in the past three months, confounding the Bank of England’s forecasts that inflation will take longer to move towards the 2% target. The headline rate is expected to nudge up to 2.5% y/y in May, which could potentially boost the odds of a rate hike in August. The core rate is forecast to stay unchanged at 2.1% y/y. The final piece of data is Thursday’s retail sales numbers. After a surprise big bounce in April, retail sales are forecast to recover further in May, rising by 0.6% on a monthly basis and by 2.4% on a yearly basis.

US CPI Preview: Inflation Approaching 3 Percent

After softer-than-expected readings in April, CPI is poised for a pickup in May. We expect headline CPI to rise 0.3 percent due to higher gas costs and a stronger core reading. CPI should be up 2.8 percent from a year-ago.

Ready for a Rebound

CPI inflation looks set to quickly close in on 3 percent as the FOMC kicks off its June meeting on Tuesday. We look for an above-consensus gain of 0.3 percent for May, pushing the year-over-year change up to 2.8 percent. Our model predicts the non-seasonally adjusted index rising to 251.47.

After a miss in April, core inflation should rise 0.2 percent. May will likely get a modest lift from April's below-trend reading (0.10 percent vs. a 12-month average of 0.18 percent). Over the past five years, however, May has been a below-average month in terms of monthly gains. Therefore, we see the risks to our 0.2 percent call as fairly balanced. Year-over-year, core CPI should edge up to 2.2 percent.

What We'll Be Watching…

Gasoline in the Driver's Seat: Energy will be in the spotlight once again in May given the continued upward march in gasoline prices. According to AAA, gasoline prices rose 6.4 percent nationally in May. While gasoline prices typically rise this time of year as the summer driving season kicks off, last month's increase was roughly twice as large as the average May gain over the past five years. We estimate gasoline will lift headline CPI about 5 bps in May and, with prices up more than 20 percent over the past year, contribute nearly a percentage point to the year-over-year increase in CPI.

Flying High: Airline fares fell 2.7 percent in April, which was the largest monthly drop in more than four years and pushed prices further into negative territory on a year-ago basis. We expect to see fares bounce-back in in May. Beyond the usual volatility of this line item, which makes back-toback declines of April's magnitude look unlikely, airlines are starting to contend with higher fuel costs. Around one-third of the airline industry's direct costs stem from fuel. Although there may be some willingness for the industry to accept lower margins, rising energy costs (alongside growing wage pressures) suggest the days are numbered for declining airline fares.

A Bumpy Ride for Vehicles: Prices for new and used autos hit a big speed bump in April. Used vehicles prices posted the largest single-month decline since the depth of the Great Recession and, when combined with a drop in new vehicles, autos shaved 6 bps off of April's smaller-than-expected rise in headline CPI. Used auto prices are likely to remain under pressure given the high number of vehicles coming off lease, but with the Manheim Index for used vehicle pricing recovering some ground in the past two months, we doubt the extent of April's decline as measured by the CPI will be repeated.

Turning the Dining Tables: After prices for food at home declined 1.3 percent and 0.2 percent in 2016 and 2017, the U.S. Department of Agriculture expects growth of 0.5-1.5 percent in 2018, setting up food for a greater contribution to headline CPI. Significantly above-trend price growth for food at home in April (0.3 percent gain) makes a repeat unlikely in May, but we will be watching for strength from this component in coming months.

Canadian May Employment Drops Though the Unemployment Rate Stays Low

Highlights:

- May employment unexpectedly fell 7.5K following a 1.1k drop in April. To date this year employment has declined an average of 10k per month but is still up 20k per month over the last 12 months.

- Despite declining employment, the unemployment rate has remained low averaging 5.8% to date this year and thus below assumed full employment within a range of 6% to 6 1/2%.

- The annual increase in wages rose to 3.9% from 3.3% in April reflecting in part a minimum wage increase in Quebec though tight labour markets was also likely a key factor.

Our Take:

Canadian May employment came in weaker than expected dropping 7.5k following a 1.1k drop in April. To date this year employment has declined on average around 10k per month but is still up 20k per month over the last 12 months. That is still almost double what we view as trend employment growth. As well, despite the recent weakness in employment growth the unemployment rate has remained low averaging 5.8% to date this year and thus below estimates of full employment of 6% to 6 1/2%. An economy operating beyond capacity was reinforced by the year-over-year increase in average hourly earnings steadily rising this year to the 3.9% recorded in May relative to the 2.9% that prevailed the end of last year. Some of this pressure likely reflected minimum wage increases introduced this year in both Ontario and Quebec though these legislated wage increases do not explain all of the upward pressure. Evidence of labour markets operating slightly beyond capacity with a low unemployment rate and attendant upward pressure on wage growth argue for the Bank of Canada to continue tightening.

Canadian Housing Starts Dropped in May

Highlights:

- Housing starts fell to a 12-month low of 196k annualized units in May — well-below the 223k average in Q1

- The May drop was accounted for largely by big declines in the (often-volatile) multiple-unit component in Ontario and Quebec.

- The drop in May starts was probably overstated — permit issuance has remained very strong in recent months and weakness was concentrated in the often-volatile multiple-unit component. Nonetheless, we continue to expect slower home resale activity year-to-date will eventually spill over into slower homebuilding activity as well.

Our Take:

Housing starts dropped to 196k in May, down almost 10% from 217k in April and the first sub-200k reading in a year. The often-volatile multiple-unit component dropped 16% while single-unit starts rose 2%. Regionally, there were big declines in Ontario and Quebec — both driven by big declines in multiple-unit starts — but increases in the Prairies and British Columbia. Clearly there has been a slowing in home resale activity year-to-date in Canada following the implementation of new mortgage stress tests — and we expect that will eventually be followed by slower homebuilding as well. The drop in May starts, though, probably reflects ’normal’ monthly volatility more than a deterioration in underlying trends. Permit issuance has remained very strong, with 232k residential permits issued in April, arguing for at least some near-term bounce-back. On a six-month moving average starts were still an elevated 216k in May, still well-above most estimates of the underlying rate of household formation.

Sunset Market Commentary

Markets:

Trading started in risk-off mode today as boiling tensions on emerging markets got a grip on global trading. The sell-off in EM currencies like the Brazilian real, Indian rupee or Turkish Lire accelerated of late with central banks deploying their ammunition (rate hikes, interventions) to stop the rod. Most efforts remained in vain until now. Asian currencies and stock markets set the tone for significantly weaker opening of European stocks. Core bonds extended gains of the end of yesterday’s session, profiting from safe haven flows. Disappointing German and French April production data supported a Bund outperformance. Risk sentiment started improving around European noon as the pressure on EM currencies eased. Stocks and bonds made an intraday turnaround. The German yield curve bear flattens at the time of writing with yields 2.9 bps (2-yr) to 4.2 bps (30-yr) lower. An overnight effect exaggerates changes. US yields trade about 1.2 bps higher across the curve. 10-yr yield spreads changes vs Germany widen 2 bps with Belgium (+5 bps) and Greece (+16 bps) underperforming.

The dollar was in the driver seat on FX market, profiting from the unwinding of carry trades. The rally also slowed after European noon. USD/JPY was the notable exception to the rule, the yen being a typical outperformer in such market circumstances. EUR/USD moved lower in the 1.1830-1.1510 trading range following yesterday’s extensive test of the upside. The pair currently trades just north of 1.1760. Sterling initially took the upper hand over the euro, but fortunes for the queen’s money made a turn for the worse after EU Barnier shot down yesterday’s backstop plan by the UK. The border offer is short on answers to the EU’s questions. He stressed the importance of the June Summit to convince markets of an orderly exit. EUR/GBP is heading back to the 0.88 area at the time of writing.

The event calendar heats up next week. US President Trump and North Korean leader Kim Jung-un meet on Tuesday to discuss a denuclearization. The Fed is expected to raise its policy rate by 25 bps to 1.75%-2% on Wednesday. The new dot plot could show a hawkish shift in this year’s forecast and with regard to the neutral rate. The ECB flagged a debate on ending its asset purchase programme on Thursday, but will Draghi already inform markets or postpone communication to July? The Bank of Japan is expected to keep policy unchanged on Friday, but could be the biggest wildcard for trading if they hint on policy normalization.

News Headlines:

After German reports showed yesterday that manufacturing orders fell in April for the fourth consecutive month, Industrial Production (MoM) also disappointed with a decline of 1% in April from March (+0.3% expected). French factory data were also below expectations with a decline of 0.5% (+0.3% expected). Both results add to the evidence that the EMU economy is unlikely to rebound strongly after Q1’s slowdown.

US President Trump has responded to Canadian PM Trudeau and French President Macron’s criticism on US tariffs on steel and aluminium by saying Canada and France are too charging the US with large tariffs. He said “to be looking forward to straightening out unfair Trade Deals with the G-7 countries”. Macron responded that they are not afraid to sign a 6 country agreement.

UK Prime Minister May’s blueprint for avoiding a hard border between Ireland and Northern Ireland that she presented yesterday has been rejected by Chief EU negotiator Michel Barnier. stating that the proposal cannot apply to the whole UK, an element that is crucial to being acceptable to the UK.

EU Barnier: Backstop cannot be extended to whole UK

EU Brexit negotiator Michel Barnier criticized UK's backstop proposal regarding Irish border. He said that "our backstop cannot be extended to the whole UK. Why? Because it has been designed for the specific situation of Northern Ireland." And he emphasized that "what is feasible for a territory the size of Northern Ireland is not necessarily feasible for the whole UK."

On the other hand, UK spokesman for PM May said that UK will never accept a customs border between Northern Ireland and the rest of the UK. And he countered-criticized that European Commission's proposals do not achieve maintaining the integrity of UK. And that's the reason why May put forward its own backstop solutions for customs in Brexit talks.

UK published document on temporary Brexit customs arrangements earlier this week.

Another Tick Down for Canadian Employment in May

Canadian employment fell by 7.5k net positions in May. The unemployment rate remained unchanged at 5.8%, as slightly fewer Canadians looked for work.

The soft headline print was matched with soft details. Full-time employment pulled back by 31k net positions, while 23.6k part-time positions were added. In terms of employment types, the public sector added 12.9k jobs, while private employment dropped 4.8k. Self-employment also dropped 15.6k, bringing the overall tally into negative territory.

Goods-producing industries again led the way lower, shedding 29k positions on the back of weakness in manufacturing (-18.3k) and construction (-13k). Conversely, the service-sector continued to add jobs (+21.5k), with notable gains in accommodation and food services (+17.6k), and professional services (+17.0k).

Looking across the provinces, much of the decline can be chalked up to B.C., where employment fell 12.4k in May. Mixed performances were observed elsewhere.

Aggregate hours worked were effectively unchanged in May, leaving the year-on-year gain at 2.0%. Wages were up quite a bit, rising 3.9% (year-on-year) for permanent employees – the strongest advance since April 2009.

Key Implications

Disappointment is today's theme. Often a weak headline print will mask encouraging details, but whether it is the FT/PT employment split, the drop in the number of people looking for work, or other details, there was little positive that can be taken away from today's report (with the notable exception of wages).

Even on a trend basis – the better way of looking at this volatile series, the six month moving average stands at just 2.7k. An unemployment rate below its longer-term 'neutral' level should bring a moderation of job gains with it, but 2.7k is somewhat below what would be expected.

Still, this report can be seen as confirming the tightness of Canadian labour markets. Wage gains hit a nine-year high, undoubtedly helped by Quebec's minimum wage increase, but the broader story of price pressures remains – 12 of 16 major industries saw wage growth above the 3% mark in May, which also marked the 12th straight month of real wage gains.

The Bank of Canada may not be encouraged by all the details of today's report, but wage growth nearing 4% y/y will be certain to garner discussion. All told, there is little in today's report to alter our view that the Bank remains likely to hike its policy rate in July, switching into 'hold and assess' mode thereafter.

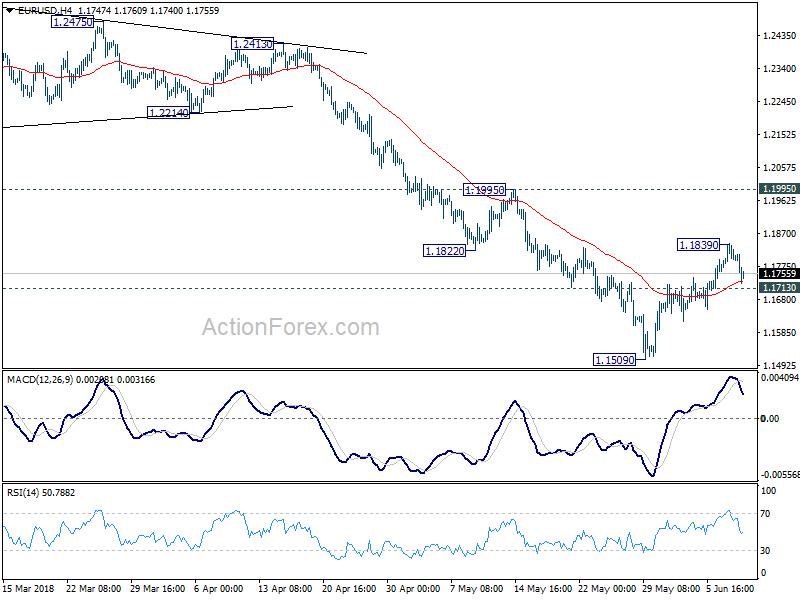

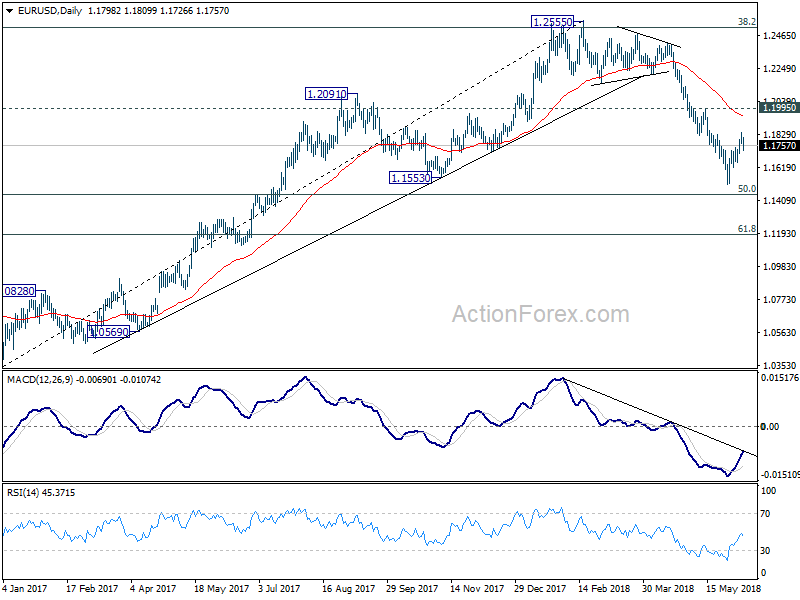

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1768; (P) 1.1804 (R1) 1.1837; More.....

Intraday bias in EUR/USD remains neutral for the moment. Corrective rise from 1.1509 could still extend beyond 1.1839. But upside should be limited by 1.1995 resistance to bring fall resumption eventually. On the downside, break of 1.1713 minor support will likely resume larger fall from 1.2555 through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

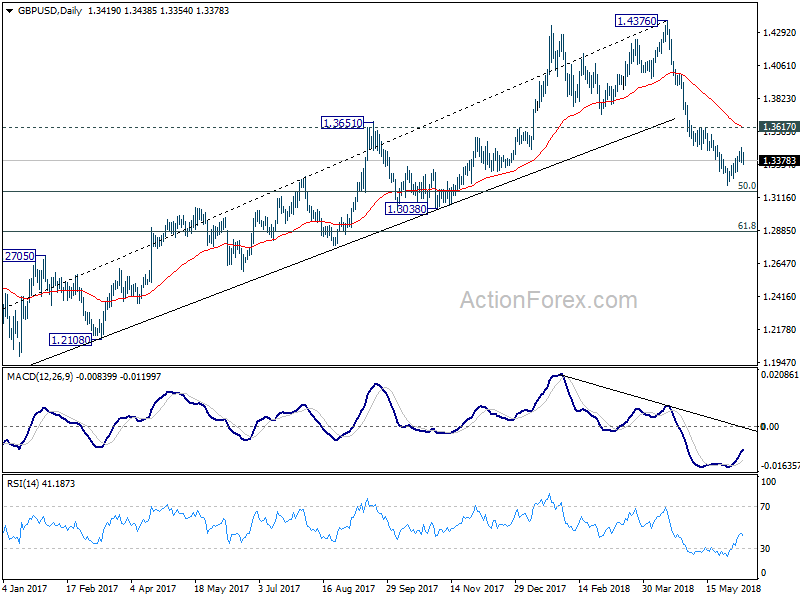

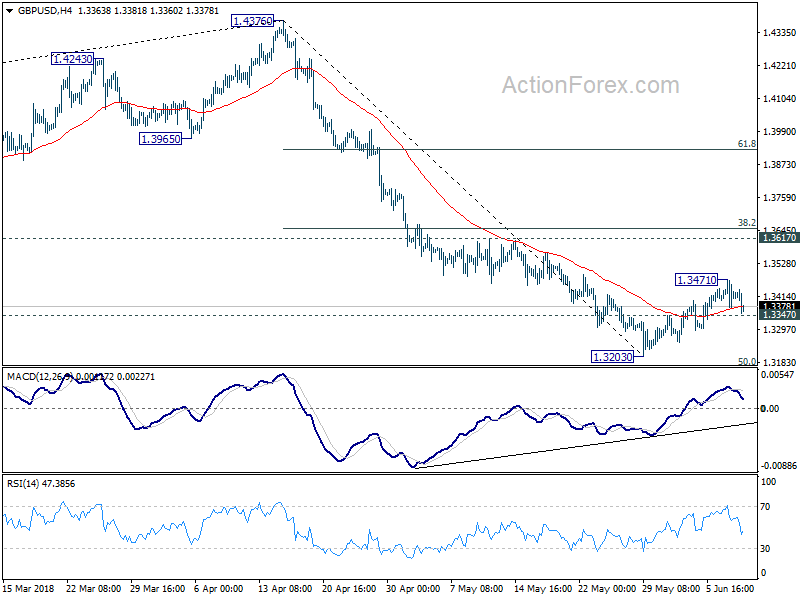

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3371; (P) 1.3422; (R1) 1.3470; More...

Intraday bias in GBP/USD remains neutral at this point. Corrective rise from 1.3203 could still extend beyond 1.3471. But we'd expect strong resistance from 1.3617 resistance to bring reversal. On the downside, break of 1.3347 minor support will likely resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3648) holds, even in case of strong rebound.