Sample Category Title

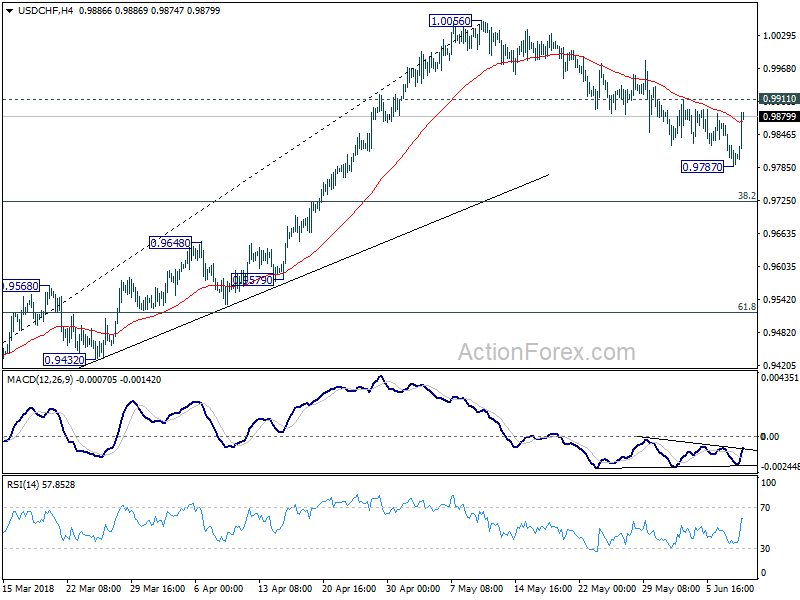

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9772; (P) 0.9821; (R1) 0.9853; More...

Intraday bias in USD/CHF is turned neutral with today's rebound. But outlook is unchanged. Choppy decline is seen as a correction. Below 0.9787 will extend to 0.9724 fibonacci level. We'd expect strong support from there to bring rebound. On the upside, break of 0.9911 minor resistance should indicate completion of the fall, on bullish convergence condition in 4 hour MACD. In such, case, intraday bias will be turned back to the upside for retesting 1.0056 high.

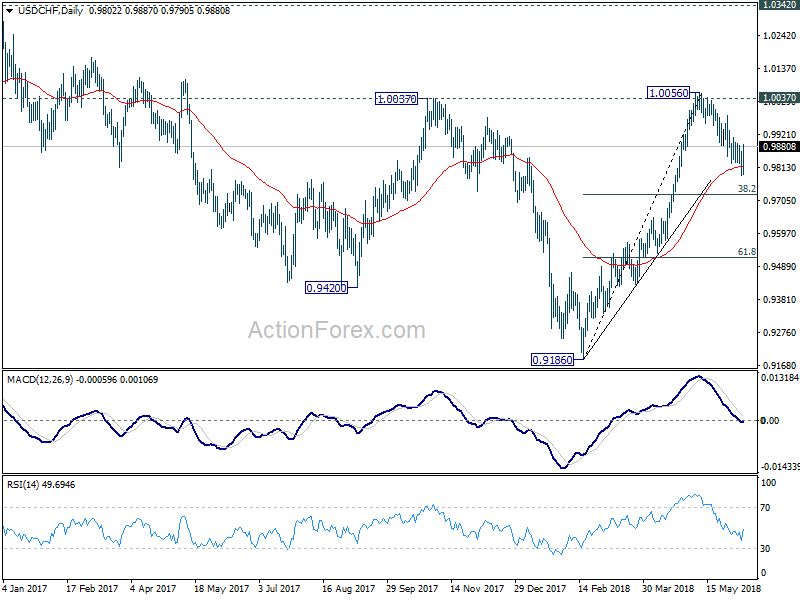

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

Caution Prevails ahead of G7 Showdown, Gold Steady

There seems to be a huge sense of anticipation mounting across financial markets ahead of the G7 summit which officially kicks off in Quebec today.

Global stocks weakened this afternoon as investors rushed to the sidelines in what could be a market-shaking “G6 plus one” showdown. With US President Donald Trump already sparking uncertainty by lashing out at Canada and France ahead of the meeting, optimism has diminished over any agreement being reached on trade during the two-day summit. Risk sentiment could take a hit if the talks between G7 leaders descend into disagreements and arguments. With escalating trade tensions seen as a major threat to global stability, the outcome of the summit could leave a mark on global sentiment.

Gold firms ahead of G7 meeting

Gold prices edged slightly higher as investors turned cautious ahead of today’s G7 summit. Price action suggests that the yellow metal needs a fresh catalyst for its next major move. If the G7 summit concludes in a deadlock with trade tensions heightened, the yellow metal could benefit as investors rush to safety. While risk aversion created from heightened trade concerns is positive for Gold, expectations over higher US interest rates are likely to threaten upside gains. With the Fed expected to announce another interest rate increase next week, zero-yielding Gold may face some headwinds down the road.

Regarding the technical picture, prices remain in limbo on the weekly charts with $1300 acting as a psychological level. A technical breakout above $1300 may inspire bulls to challenge $1324. Alternatively, if the $1300 level proves to be a stubborn resistance, prices could sink back towards $1280.

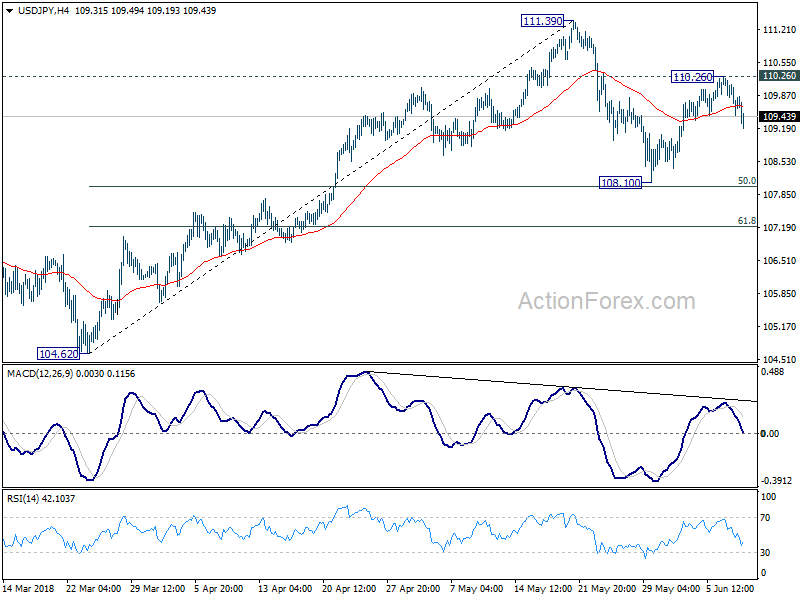

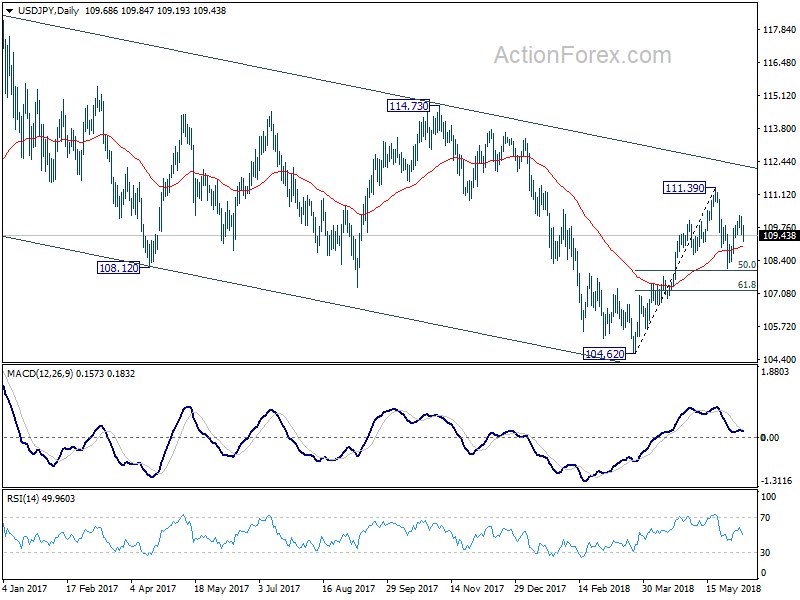

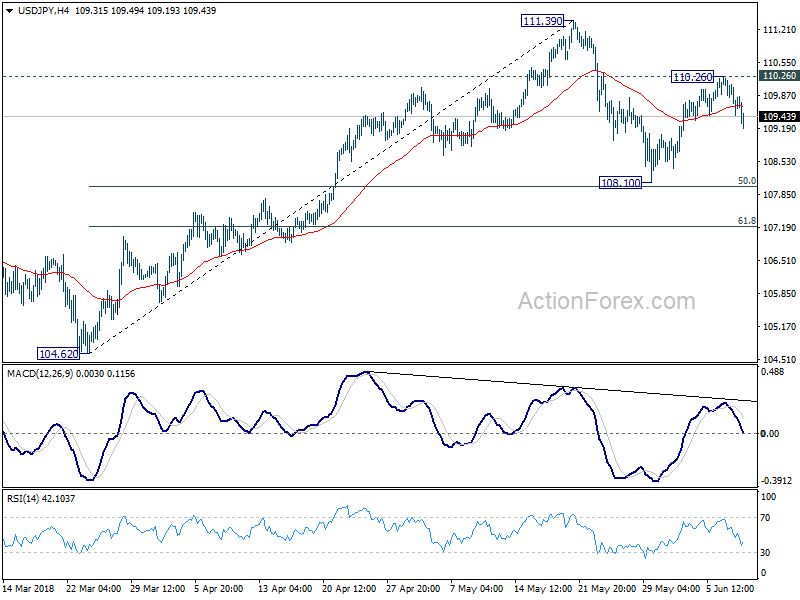

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.39; (P) 109.79; (R1) 110.10; More...

Break of 109.46 minor support suggests that USD/JPY's rebound from 108.10 has completed at 110.26 already. Intraday bias is turned back to the downside for 108.10 support or below. For now, price actions from 111.39 are seen as a corrective pattern. We'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. Meanwhile, break of 110.26 resistance will resume the rebound to 111.39 resistance next.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Canadian Dollar Shrugs Off Weak Employment Data, Yen Higher head of G7 Showdown

Safe haven flow is the main theme today as markets await G6+1 showdown in Canada. Yen is the biggest winner today, followed by Dollar. But these two remain the weakest ones for the week next to Canadian Dollar. Despite weaker than expected job data, CAD is indeed rather steady in early US session. The main moves in the forex markets are likely driven by treasury yields. German 10 year bund yield is dropping -0.036 at the time of writing, trading below 0.45 handle. Italian 10 year yield rises 0.068 to 3.061. That is, German-Italian spread is back above 250. Adding to that, European indices open the day generally lower. Despite paring much losses, DAX is still down -0.4%. US futures are also pointing to slightly lower open.

Confrontations are expected to continue between the US and others on trade issue, at the G6+1 summit in Canada, today and tomorrow. Ahead of the meeting, Trump pledged, with his tweets to, straightening out unfair trade deals with G7 countries. Facing pressure from Germany, France and Canada, Trump will continue with his confrontational approach. Yet, Trump will leave earlier than anticipated, right after Saturday's morning session, on June 9. Then he will fly straight to Singapore for the highly anticipated Kim-Trump summit on June 12.

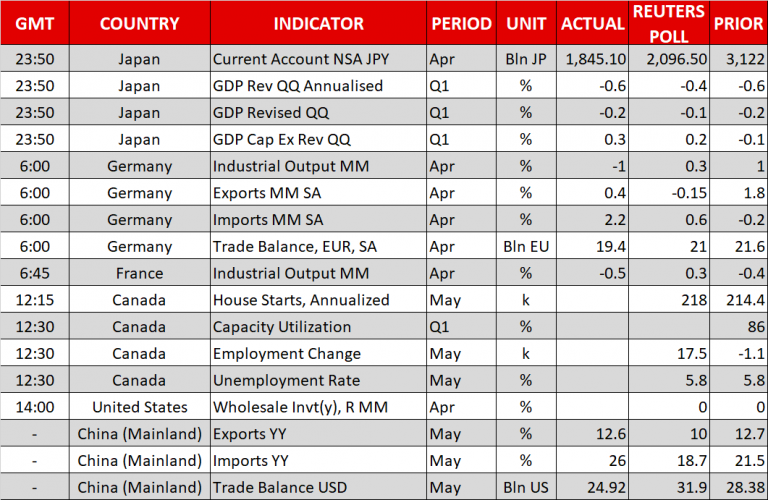

On the data front, Canada employment dropped -7.5k in May, below expectation of 19.1k growth. Unemployment rate was unchanged at 5.8%. Housing starts dropped to 196k in May, below expectation of 217k. German trade surplus narrowed to EUR 19.4b in April, industrial production dropped -1.0% mom. China trade deficit narrowed to USD 24.9B in May, below expectation of USD 32.5B. Japan Q1 GDP was finalized at -0.2% qoq, unrevised. GDP deflator was finalized at 0.5% yoy. Current account surplus widened to JPY 1.89T in April.

UK Hammond: Collaborative approach is generally more productive than a confrontational approach

UK Chancellor of Exchequer Philip Hammond said today that a "collaborative approach... is generally more productive than a confrontational approach, in dealing with Germans French and Italians. And, for a better Brexit deal, Hammond said it's important to engage the partners. He added that "finding a mutually beneficial outcome is the only way forward. That is the firm intention of my government. Theresa May, the prime minister, has said so very clearly."

That was in response to a recording of Foreign Minister Boris Johnson on Brexit approach, published by Buzzfeed. Johnson said "imagine Trump doing Brexit," "there'd be all sorts of breakdowns, all sorts of chaos. Everyone would think he'd gone mad. But actually you might get somewhere. It's a very, very good thought."

Prime Minister Theresa May's spokesman said that May "of course" still have confidence in John. And, "the PM believes that her cabinet and her government are working hard to deliver on the will of the people and working hard to take back control of our money, laws and our borders."

Japan automakers slam Trump's tariffs as Abe kept silence

Japan Prime Minister Shinzo Abe has been so far very quiet regarding trade tensions with the US. Abe and his cabinet members have repeatedly said that they do not want bilateral trade agreements. But Trump is insisting to force Japan into it. And that's not to mention that Japan was the only close ally that was not even given a temporary exemption on the steel and aluminum tariffs. It's even unsure what retaliation they'll take. The meeting between Abe and Trump ahead of G6+1 submit also produced no progress on trade.

But back in his homeland, Abe is facing increasing pressure on him to take a stance. The Japan Automobile Manufacturers Association issued a statement today slamming the US probe of automobile imports using national security as excuse again. In the statement, JAMA expressed "gravely concerned" of the investigation. It emphasized that "automobiles are sold to consumers on the basis of their own choices, and it is consumers themselves who would be penalized, through increased vehicle prices and reduced model options". Additionally, "business plans of automobile and auto parts manufacturers as well as imported vehicle dealers could be seriously disrupted, with potentially adverse impacts on the U.S. economy and jobs."

JAMA also pointed to "facts" that their member companies operate "24 manufacturing plants and 44 R&D/design centers in 19 U.S. states and in 2017, nearly 3.8 million vehicles were produced by American workers at those facilities." "Of that total, over 420,000 units were exported to countries around the world, further underscoring our contributions to employment and economic growth in the United States."

JAMA concluded that "free and fair trade and a competitive climate in line with global rules benefit consumers in the United States and strengthen the sustainable growth of the U.S. auto industry and its economy. We will continue to monitor this situation closely and to uphold the vital importance of free trade worldwide."

China YTD trade surplus with EU narrowed to USD 45.2B, with US widened to USD 104.9B

China's trade surplus narrowed to USD 24.9B in May, below expectation of USD 32.5B. Exports rose 12.6% yoy to USD 212.8B while imports rose 26.0% yoy to USD 187.9B. in CNY terms, Exports rose 3.2% to CNY 1341B while imports rose 15.6% to CNY 1185B. Trade surplus narrowed to CNY 157B, below expectation of CNY 192B.

From January to May, exports to US rose 13.6% yoy to USD 175.17B while imports from the US grew 11.9% yoy to USD 70.32B. Trade surplus to the US was at USD 104.85B, widened from 2017 same period of USD 92.9B. Total trade with the US grew 13.1% to USD 245.50B.

For the same period, exports to EU rose 12.0% yoy to USD 155.39B while imports from EU rose 19.9% yoy to USD 110.21B. Trade surplus to EU was at USD 45.18B, narrowed from 2017 same period of USD 47.9B. Total trade with EU rose 15.1% yoy to USD 265.60B.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.39; (P) 109.79; (R1) 110.10; More...

Break of 109.46 minor support suggests that USD/JPY's rebound from 108.10 has completed at 110.26 already. Intraday bias is turned back to the downside for 108.10 support or below. For now, price actions from 111.39 are seen as a corrective pattern. We'd expect strong support from 61.8% retracement of 104.62 to 111.39 at 107.20 to contain downside and bring rebound. Meanwhile, break of 110.26 resistance will resume the rebound to 111.39 resistance next.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Current Account (JPY) Apr | 1.89T | 2.09T | 1.77T | |

| 23:50 | JPY | GDP Q/Q Q1 F | -0.20% | -0.20% | -0.20% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 F | 0.50% | 0.50% | 0.50% | |

| 03:15 | CNY | Trade Balance (CNY) May | 157B | 192B | 183B | |

| 03:23 | CNY | Trade Balance (USD) May | 24.9B | 32.5B | 28.8B | |

| 06:00 | EUR | German Trade Balance (EUR) Apr | 19.4B | 20.3B | 22.0B | 21.6B |

| 06:00 | EUR | German Industrial Production M/M Apr | -1.00% | 0.40% | 1.00% | |

| 12:15 | CAD | Housing Starts May | 196K | 217K | 215K | |

| 12:30 | CAD | Net Change in Employment May | -7.5K | 19.1K | -1.1K | |

| 12:30 | CAD | Unemployment Rate May | 5.80% | 5.80% | 5.80% | |

| 14:00 | USD | Wholesale Inventories M/M Apr F | 0.00% | 0.00% |

USD/CAD – Ontario Vote Fails To Boost Canadian Dollar, Job Data Next

It continues to be an uneventful week for the Canadian dollar, and the trend has continued on Friday. Currently, USD/CAD is trading at 1.3007, up 0.17% on the day. In economic news, Canada will release key employment data. Employment Change is expected to rebound with a gain of 19.1 thousand and the unemployment rate is forecast to remain pegged at 5.8%. There are no major U.S events on the schedule.

All eyes were on the Ontario election on Thursday, and although there was a dramatic shift in the political landscape, the Canadian dollar yawned and continued to hug the symbolic 1.30 level. The Conservatives won a decisive majority of seats, as the business sector sighed in relief. With the Conservatives and the left-wing NDP running neck-and-neck in the polls, there had been concerns that the NDP could win the election, or at least deny the Conservatives a majority. The new premier, Doug Ford, is a former businessman and investors can expect the new government to have a pro-business platform. This should translate into gains for Canadian stock markets as well as the Canadian dollar.

Prime Minister Justin Trudeau will play host to the G-7 meeting in Quebec City, which begins on Friday. However, the embraces and smiles could be a formality ahead of some heated discussions, as the summit comes at a time of escalating trade tensions between the U.S and some of its major trading partners. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. The trouble started last week, when the Trump administration slapped stiff tariffs on Canada, Mexico and the European Union. This resulted in promises of retaliation, and Canada and Mexico have already announced duties on U.S products. Will we see a higher profile, repeat performance at this meeting? The escalating trade battle is sure to dominate the summit, where Trump can expect to hear strong complaints from other leaders over the tariffs, which Trump justified on the grounds of ‘national security’. If the leaders fail to resolve matters, the result could be a nasty trade war between the U.S and its major trading partners.

Investors Look For Safe Havens Ahead Of G7 Summit

Here are the latest developments in global markets:

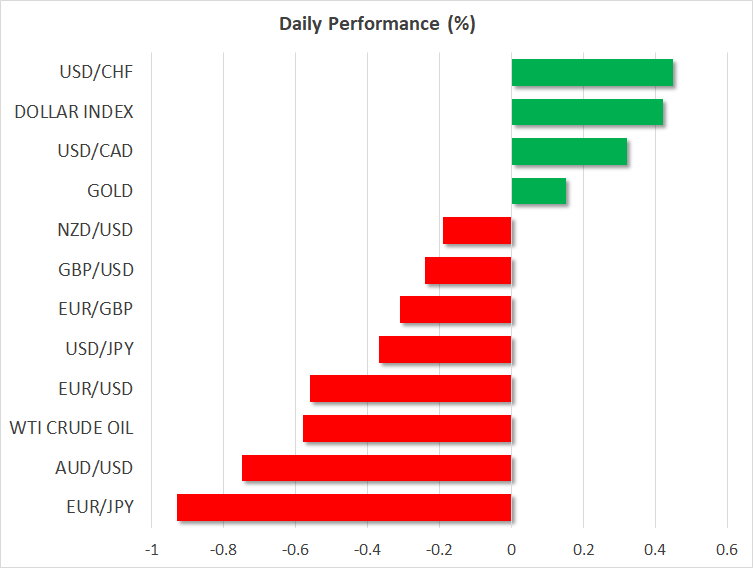

FOREX: Despite optimism that the ECB will end its QE program by the end of this year, the euro went downhill on Friday against its US counterpart as appetite for riskier assets eased on fears trade tensions could heighten if the US and its G6 partners fail to reach agreement on a joint statement at today’s meeting in Quebec, Canada. The pair also lost ground after German trade numbers indicated a narrower trade surplus in the biggest EU economy, with euro/dollar crawling down to 1.1748 (-0.41%) after hitting a two-week high of 1.1839 yesterday. Pound/dollar was slightly weaker today at 1.3391 (-0.22%) with Brexit uncertainties adding to trade pressures. Yesterday, rumors said that UK Brexit Secretary, David Davis, was up to resign if he did not get a guarantee by the UK Prime Minister, Theresa May, that the backstop proposal – a hard border with Northern Ireland – would not extend beyond December 2021. While today’s headlines stated that Davis would stay in the role, the threat exposed once again divisions over Brexit in May’s cabinet ahead of a withdrawal bill vote in the UK’s lower house on June 12. Euro/pound slipped to 0.8771 (-0.17%). Dollar/yen remained in the red, extending losses for the second day towards 109.45(-0.23%) as the yen was gaining ground in the face of risk-off sentiment. The safe-haven Swiss franc, though, was unable to advance on risk aversion as a key banking vote in Switzerland on Sunday (on whether the SNB central bank would be the only issuer of Swiss francs) could alter the country’s monetary system. Dollar/swiss franc was up at 0.9841 (+0.40%). The dollar index benefitted from euro and pound weakness, climbing to 93.72 (+0.35%). Aussie pairs, which are vulnerable to US-China trade relations, were among the worst performers despite upbeat Chinese trade figures early today, with aussie/dollar retreating to 0.7588 (-0.51%) and aussie/yen tumbling to 83.05 (-0.68%). Kiwi/dollar stood lower at 0.7021 (-0.07%). Dollar/loonie changed hands at 1.3015, higher by 0.12% before the release of the Canadian employment report later today.

STOCKS: Investors were in a cautious mood in European stock markets, driving equities lower ahead of the widely expected G7 meeting later in the day. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.16% and 0.06% respectively at 1130 GMT despite speculation of tighter monetary conditions, with all sectors being in the red. The German DAX 30 dropped by 0.62%, with industrials leading the losses, the French CAC 40 declined by 0.13%, UK’s FTSE 100 moved down by 0.16% and the Spanish IBEX 35 declined by 0.94%. The Italian FTSE MIB was the worst performer, losing 1.54%. Futures tracking US stock indices were all in the red, pointing to a negative open.

COMMODITIES: Oil prices were falling on Friday after finishing the day higher on Thursday as data showed on Friday that crude oil imports out of China in May, the world’s second largest oil consumer, pulled back from record highs reached last month. Investors were also pricing in that OPEC could announce an output hike at its two-day policy meeting on June 22-23 amid rising US production. WTI crude and Brent were trading lower at $65.65/barrel (-0.55%) and $76.48/barrel (-1.09%) respectively. In precious metals, the risk-off sentiment attributed mainly to escalating trade disputes between the US and the rest of the world shifted some demand towards safe-havens, helping gold to pick up to $1,298.30/ounce (+0.08%).

Day Ahead: Trade developments take the front seat; Canadian jobs figures on the agenda

With the only major release on the economic agenda being Canada’s employment report on Friday, investors’ focus would turn also on comments or statements coming from the G7 gathering.

The G7 summit in Quebec, Canada will take place today and will conclude tomorrow. Investors have started to price in the uncertainty surrounding the summit, as the US has already decided to levy tariffs on steel and aluminium imports from countries that were previously exempt. Germany and France have stated that they will not sign any agreement before progress is made on the Paris Climate Accord, the Iranian deal, and tariffs. Meanwhile, US President Donald Trump has decided to leave the two-day summit earlier than anticipated right after Saturday’s morning session on June 9, to head to Singapore where he will hold a meeting with the North Korean leader Kim Jong-un three days after. Before the summit kicks off though, the US President already engaged in a war of words, expressing his willingness to clean up any “unfair trade deals” at the meeting.

Out of Canada, housing starts for the month of May will become public at 1215 GMT, but the main release of the day is the employment report scheduled at 1330 GMT. The unemployment rate is forecast to have held steady at its four-decade low of 5.8% for the fourth consecutive month, while the net change in employment is anticipated to have rebounded, following a sharp decline previously. The net change in employment is expected to show that the economy added 17.5k jobs during the month of May after losing 1.1k in April. Upside surprises would likely be encouraging news for the Bank of Canada,which is looking to hike rates in July.

The day continues with the US wholesale sales for the month of April at 1400 GMT, while in energy markets, investors will keep a close eye on the US oil rigs count issued by the Baker Hughes company at 1700 GMT.

Overnight, China will announce CPI and PPI data for May. Predictions are for the CPI figure to remain on hold to 1.8% y/y, while the PPI rate is forecasted to have ticked up to 3.8% y/y versus 3.4% in the preceding month.

Hong Kong 50 Index Slides Back Inside Symmetrical Triangle, Bearish Bias In Place

The Hong Kong 50 Index is having a rough ride today, extending the negative momentum below the 20-day simple moving average (SMA). While the index jumped above the symmetrical triangle in the previous two days it failed to extend gains towards the 32,000 resistance level and reversed back down. Technical indicators point to further downside movements in the short-term.

The RSI indicator continues to fluctuate near the 50 level and is currently moving downwards, meaning that the risk is tilted to the downside. The fast stochastics are also negatively sloped, while it they recorded a bearish cross in the overbought zone, suggesting further losses.

Should the market stretch lower, support could come first at around 30,000 near the ascending trend line before the focus shifts to 29,740 a frequently congested area during May. A drop below this area, could raise bearish sentiment and drive the index further down to the 29,100 barrier, taken from the low on April 4.

On the other side, if the market rebounds, resistance could be found around the 31,620 hurdle. A close above the symmetrical triangle, could decisively fuel bullish sentiment. In this case, the door could open to the 32,000 key-mark.

Turning to the medium-term picture, the index has been holding within a symmetrical pattern since December 2017. However, the neutral picture could be about to change as the price has been making several attempts in recent weeks and come close to breaking outside of the triangle.

Apple Stock Hits Fresh All-Time High, Bullish Bias Back In Force

Apple's stock reached a fresh all-time high of 193.90 on Thursday, having staged a spectacular rally after touching a ten-week low of 160.50 on April 27. Price action remains comfortably above both the 100-day and 200-day moving averages, reinforcing the bullish medium-term outlook.

Looking at momentum oscillators, the RSI has just turned down after meeting resistance near its overbought 70 line, signaling that positive momentum may be losing some steam. The MACD – already in positive territory – has just crossed above its trigger line, this being a bullish short-term signal. Combined, these suggest that although there may be a minor pullback in prices in the immediate term, the stock's broader bias remains to the upside.

Further advances could encounter immediate resistance at the all-time high of 193.90; price action is currently taking place just below this hurdle. An upside break would bring prices into uncharted waters, setting the stage for a test of 197.50, which is the 161.8% Fibonacci extension level of the March 13 – April 27 pullback, from 183.40 to 160.50. Even higher, sell orders may be found near the round figure of 200.00 initially, and 210.00 thereafter.

On the downside, preliminary support may come near the 190.30 zone, defined by the peaks of May 10. A downside break could open the way for 186.00, an area that successfully halted several declines in mid-May. Lower still, the March 13 top of 183.40 would increasingly come into focus.

Overall, both the short- and medium-term outlooks are currently looking bullish, though there are some signs of easing momentum in the near-term.

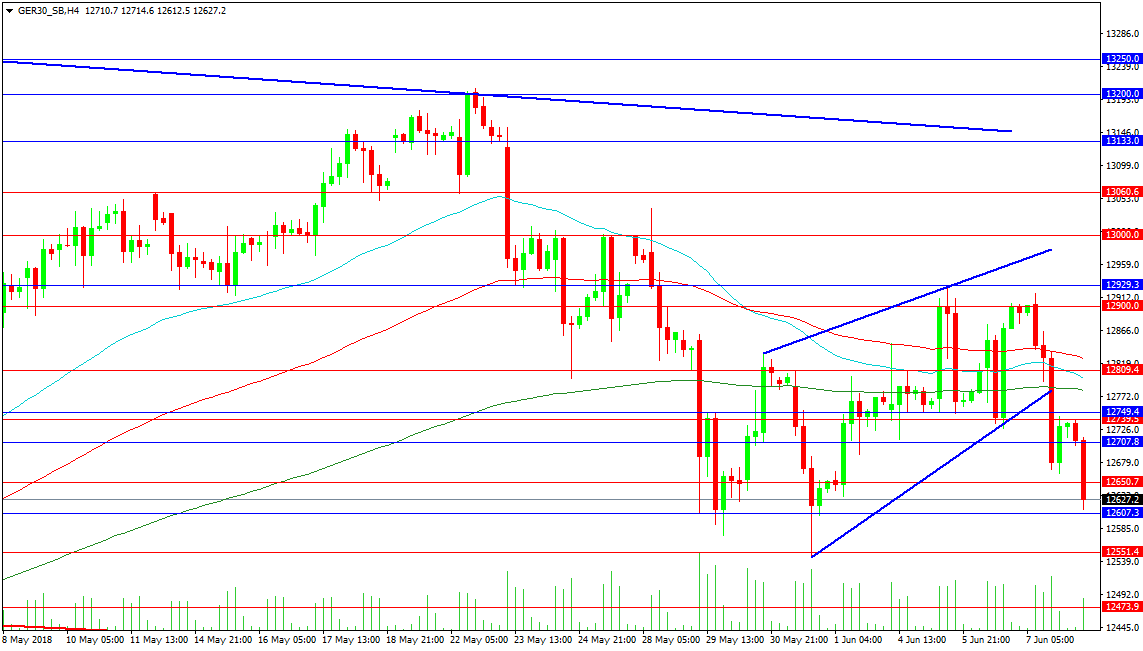

Forex Analysis: GER 30 And US 500 Indexes

German 30

The German 30 Index has been under the cosh this week and has lagged the rally in equities as the Euro has prohibited it from making headway. The economic data has also dragged on the index and paints a less than positive picture for Europe. Finally the ECB has made comments concerning the end of Asset Purchases creating a further headwind. Price found resistance in the pocket above 129000.00 this week at the previously supportive level of 12930.00. An attempt to rally yesterday ended in failure and we are now trading 300 pips down from yesterdays high. A rally above 13000.00 is needed to restore equilibrium to the market with 13200.00 the point of control for bulls to retarget the high of 13600.00.

Support comes in at last week’s low of 12540.00 with a loss of that level potentially resulting in a drop towards 12000.00. The 12473.90 level could find buyers but it is the 12375.00 level that bulls will most likely engage with as it has falling trend line support. A break under this level puts the index on a collision course with 12000.00. A fall under that level can find buyers but if 11600.00 is lost a deeper correction can in sue.

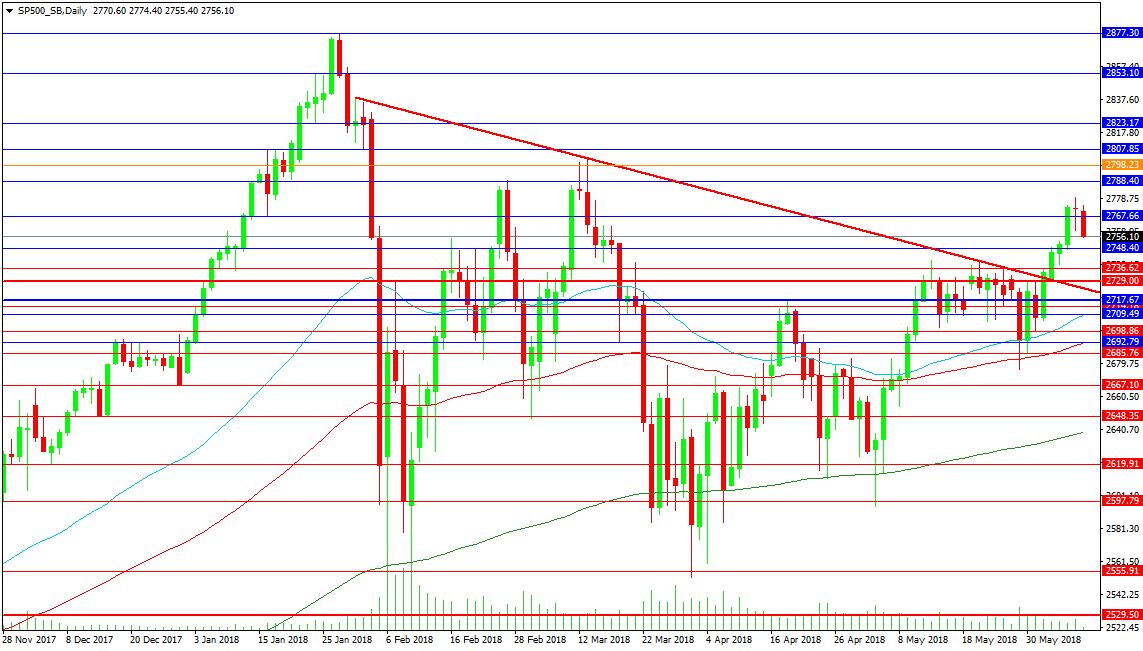

US 500

The US 500 Index has strung together a decent rally from the Non-Farm payrolls data on Friday but the looming G7 Meeting in Canada today and a sector rotation in US equities yesterday has ended the rally. Trades issues are set to dominate the meeting with President Trump scheduled to only pay a flying visit as he moves on to Singapore to for North Korean talks. The markets are duly concerned ahead of the G7 and are pairing risk. The 2800.00 level remains the first target for the Index with an advance to the high at 2877.00 to follow.

Support comes in at 2748.00 followed by the more robust area around 2740.00. A loss of this level puts price back into the previous range with light support at 2700.00 and the 2680.00 level providing bulls with a area to lean against. A loss can see sentiment swing to the bears who would target 2640.00 and the 200 DMA where buyers would attempt to engage with the market. This is likely to be the extent of any drop unless sentiment is hammered. In that event the lows around 2555.00 and 2530.00 may be revisited.

UK Hammond: Collaborative approach is generally more productive than a confrontational approach

UK Chancellor of Exchequer Philip Hammond said today that a "collaborative approach... is generally more productive than a confrontational approach, in dealing with Germans French and Italians. And, for a better Brexit deal, Hammond said it's important to engage the partners. He added that "finding a mutually beneficial outcome is the only way forward. That is the firm intention of my government. Theresa May, the prime minister, has said so very clearly."

That was in response to a recording of Foreign Minister Boris Johnson on Brexit approach, published by Buzzfeed. Johnson said "imagine Trump doing Brexit," "there'd be all sorts of breakdowns, all sorts of chaos. Everyone would think he'd gone mad. But actually you might get somewhere. It's a very, very good thought."

Prime Minister Theresa May's spokesman said that May "of course" still have confidence in John. And, "the PM believes that her cabinet and her government are working hard to deliver on the will of the people and working hard to take back control of our money, laws and our borders."