Sample Category Title

ECB Preview: End Of QE Approaching But No Formal Announcement Just Yet

QE Coming To An End –Not Officially Announced Yet

Overall/forward guidance. At the governing council (GC) meeting next week, we do not expect explicit new forward guidance, but may see some hawkish bits, in particular in wage growth discussions along the lines of ECB's chief economist Peter Praet's comments on Wednesday, which were surprisingly hawkish.

Tasked committees. Draghi will face numerous questions on an (upcoming) change in forward guidance. Just as Draghi referred to tasked committees when lowering the APP purchase rate from EUR80bn to EUR60bn and EUR60bn to EUR30bn, we could envisage him using a similar reference while waiting for the July meeting .

Timing . While we expect forward guidance to be changed in July , we cannot rule out the possibility of it coming already next week given the recent comments from Praet. In our view, we have not received any data that should warrant the ECB moving already now. The ECB's actions, which were confirmed in March, have been reactive when removing stimuli and not proactive . In our view, a change to the forward guidance next week would also question the mantra of ECB being reactive . Should APP guidance change next week, we expect the ECB to step up its rhetoric on rates, reinforcing the depo rate guidance.

New staff projections. We expect growth to be revised down by 0.2pp and inflation to be revised up by 0.2pp in 2018 . We do not look for big changes in the core inflation forecast.

Italy. Focus on Italy during the Q&A. We do not expect the ECB's QE tapering discussions to be changed due to the Italian turmoil. Should the turmoil lead to a sustained deterioration in confidence (in turn leading to a slowdown in the fragile Italian economy) we expect the ECB to get more worried. Further, we expect Draghi to acknowledge the new government and to say that he expects all EU (EA) countries to live up to the rules and that any ECB response is laid out in the rule book (ESM).

Buzzword bingo. You will find our updated buzzword bingo at the end of this preview.

Fixed income. We expect little impact on the EGB term-premium from the June meeting and the impact on the long end should be small. If - contrary to our expectations - we see a more hawkish signal from the ECB, the 5Y point on the EUR curve could be especially exposed. We continue to be positioned for a tightening of periphery (excluding Italy) spreads versus Germany/swaps.

FX . EUR/USD in lower range for longer. Hawkish hints at the press conference should still keep up the sense of the ECB slowly but surely continuing policy 'normalisation' . While the USD is set to stay supported from a rates point of view, the ECB keeping up its exit process should ensure that EUR/USD is kept afloat further out. We look for broadly the 1.15-1.21 range to be sustained on a 6M horizon.

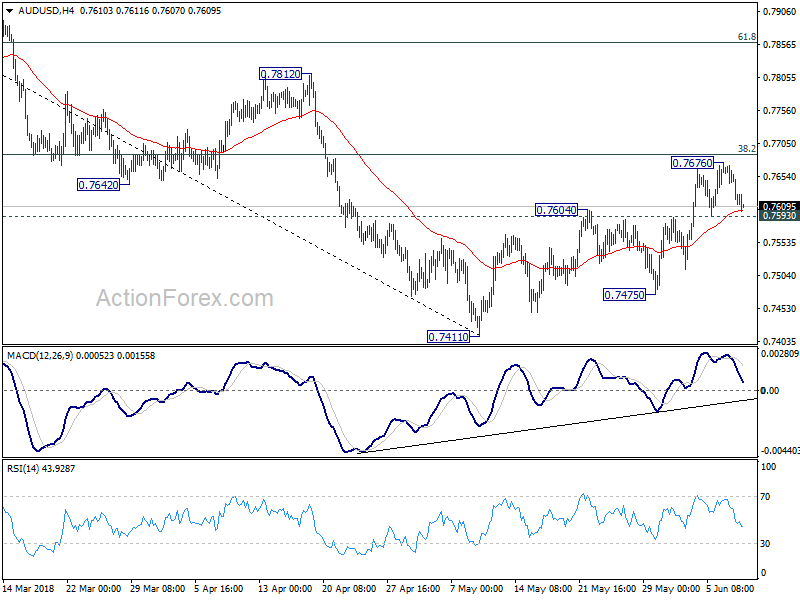

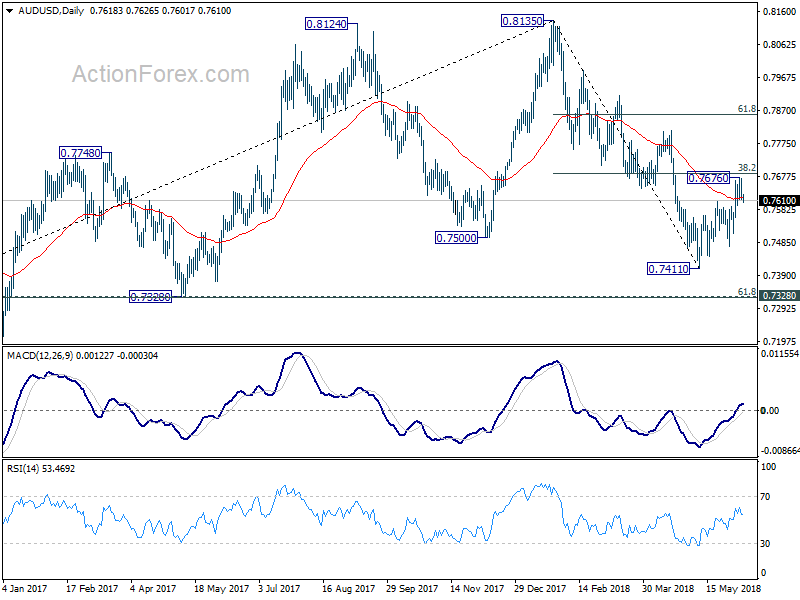

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7600; (P) 0.7637; (R1) 0.7661; More...

Intraday bias in AUD/USD stays neutral at this point and outlook is unchanged. Rebound from 0.7411 is seen as a correction. Hence, upside should be limited by 38.2% retracement of 0.8135 to 0.7144 at 0.7688. On the downside, below 0.7593 minor support will turn bias to the downside for 0.7475 first. Break there will likely resume larger fall through 0.7411 to 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326). However, sustained break of 0.7688 will dampen our bearish view and target 61.8% retracement at 0.7585 instead.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

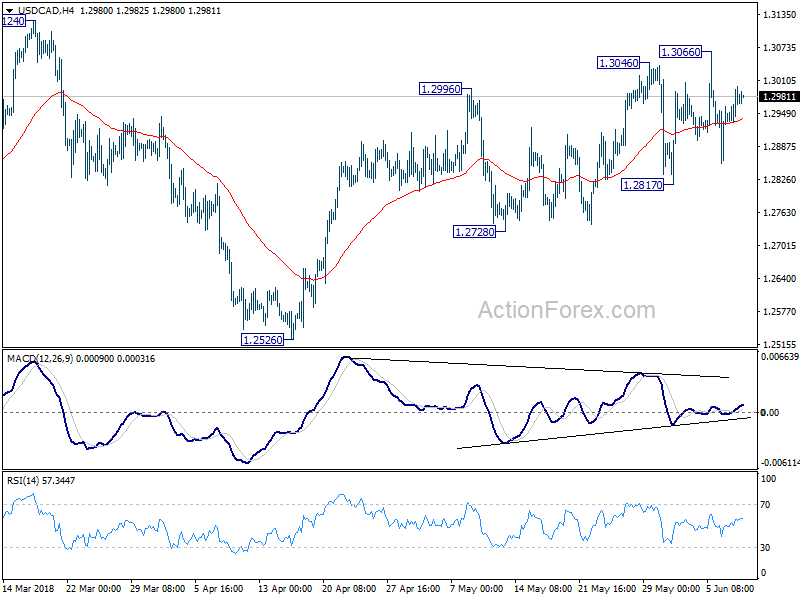

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2933; (P) 1.2967; (R1) 1.3007; More.....

USD/CAD is still bounded in tight range below 1.3066 and intraday bias remains neutral. Near term outlook will stay cautiously bullish as long as 1.2817 support holds. Above 1.3066 will extend the rise from 1.2526 to 1.3124 key resistance. Decisive break there will carry larger bullish implication. However, break of 1.2817 will indicate near term reversal and turn bias to the downside for 1.2728 support and below.

In the bigger picture, we're favoring the case that that rebound from 1.2061 has not completed yet. But there is no follow through upside momentum so far. Focus remains on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

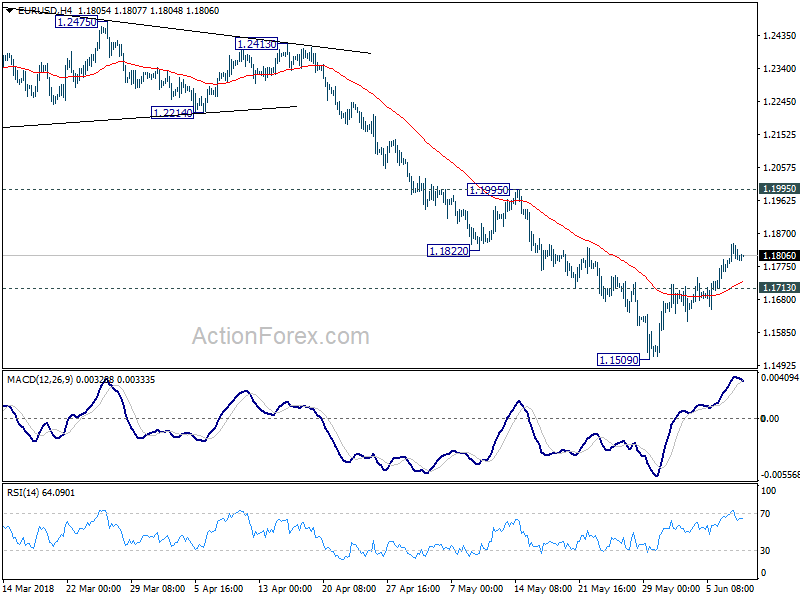

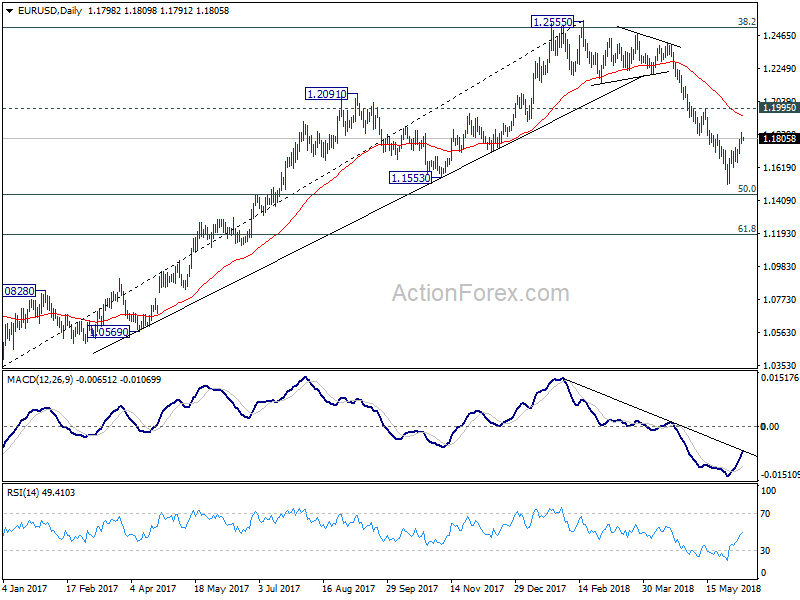

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1768; (P) 1.1804 (R1) 1.1837; More.....

EUR/USD is losing upside momentum as seen in 4 hour MACD. But near term outlook is unchanged. Corrective rise from 1.1509 could extend higher. But upside should be limited by 1.1995 resistance to bring fall resumption eventually. On the downside, break of 1.1713 minor support will likely resume larger fall from 1.2555 through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

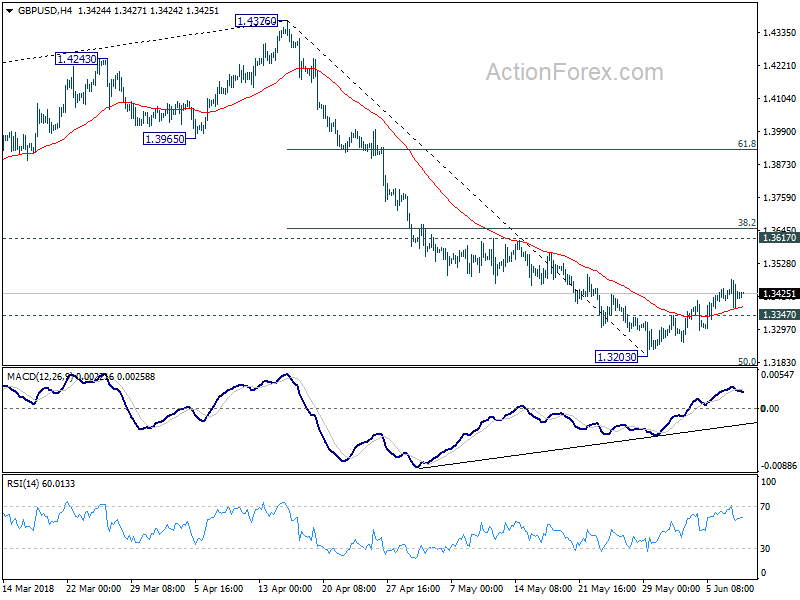

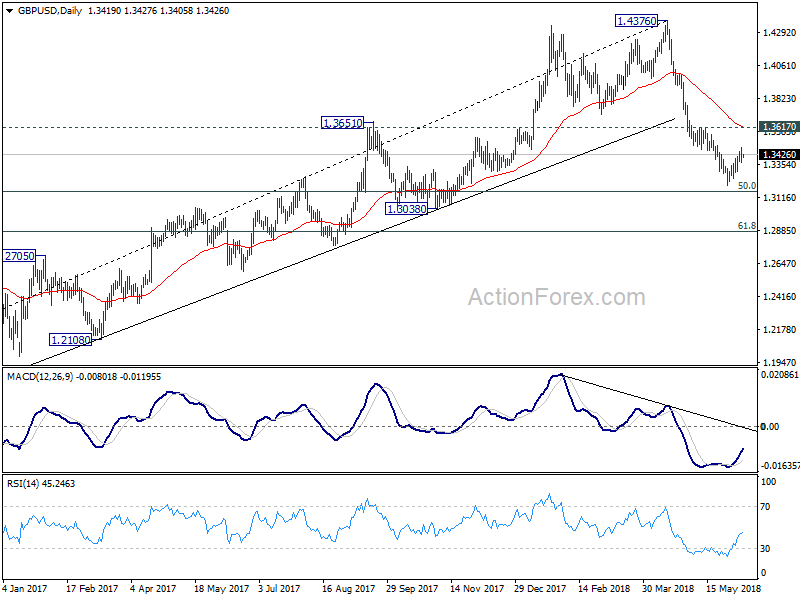

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3371; (P) 1.3422; (R1) 1.3470; More...

GBP/USD is losing upside momentum as seen in 4 hour MACD. But overall outlook is unchanged. Corrective rise from 1.3203 could still extend higher. But upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3347 minor support will likely resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3648) holds, even in case of strong rebound.

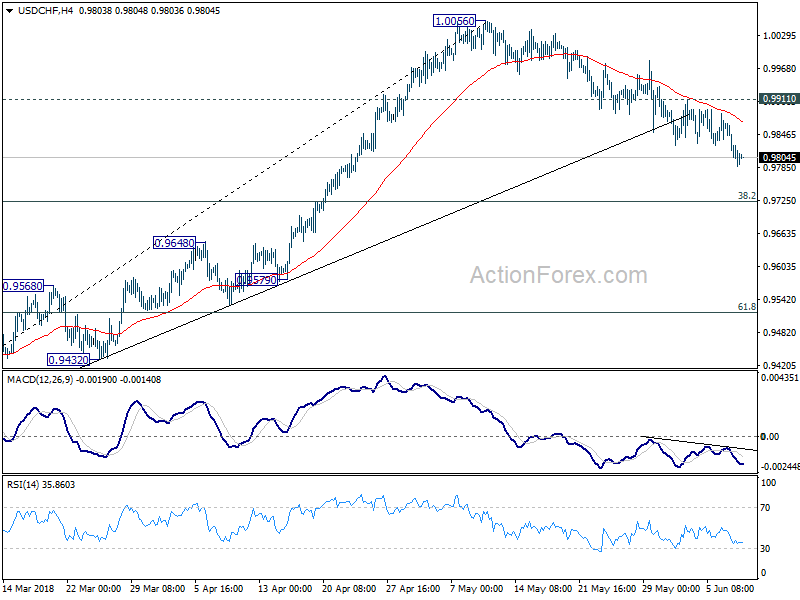

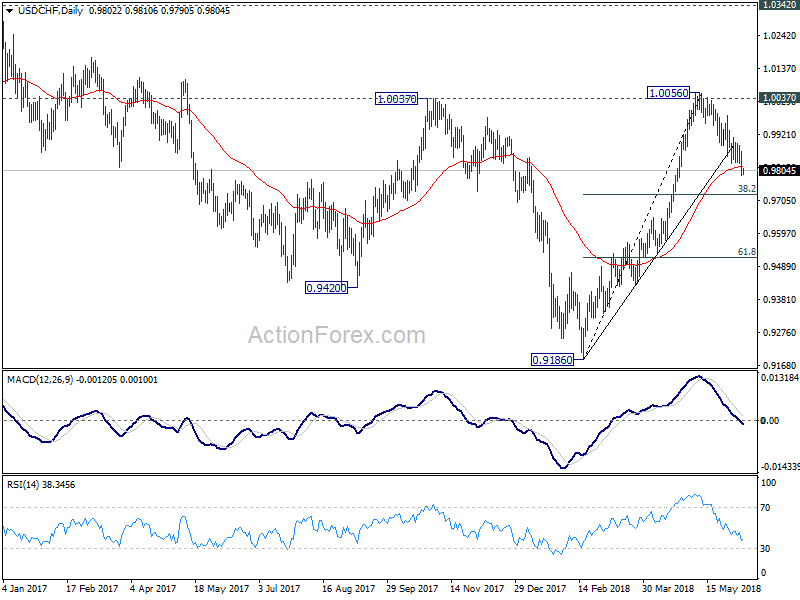

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9772; (P) 0.9821; (R1) 0.9853; More...

USD/CHF's corrective fall from 1.0056 is still in progress. Intraday bias stays on the downside for 0.9724 fibonacci level. We'd expect strong support from there to bring rebound. Though, on the upside, break of 0.9911 minor resistance is needed to indicate completion of the fall. Otherwise, near term outlook will remain mildly bearish in case of recovery.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

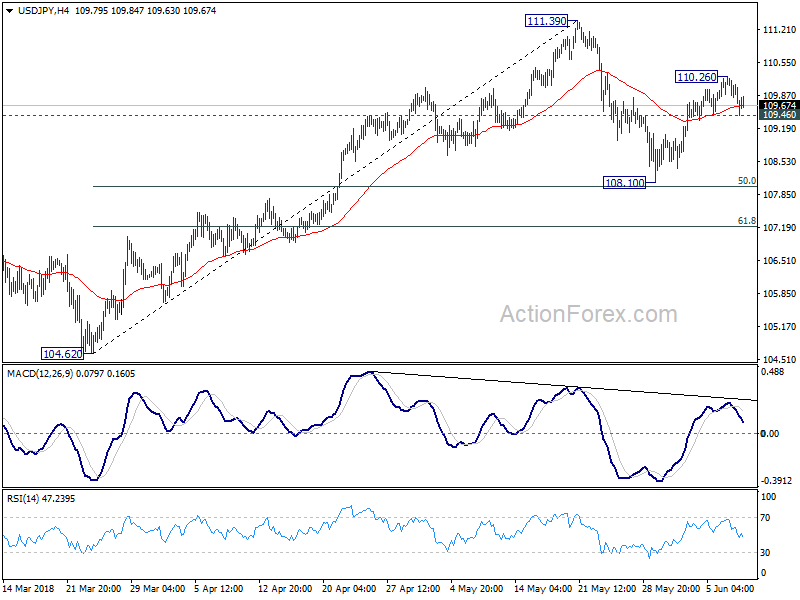

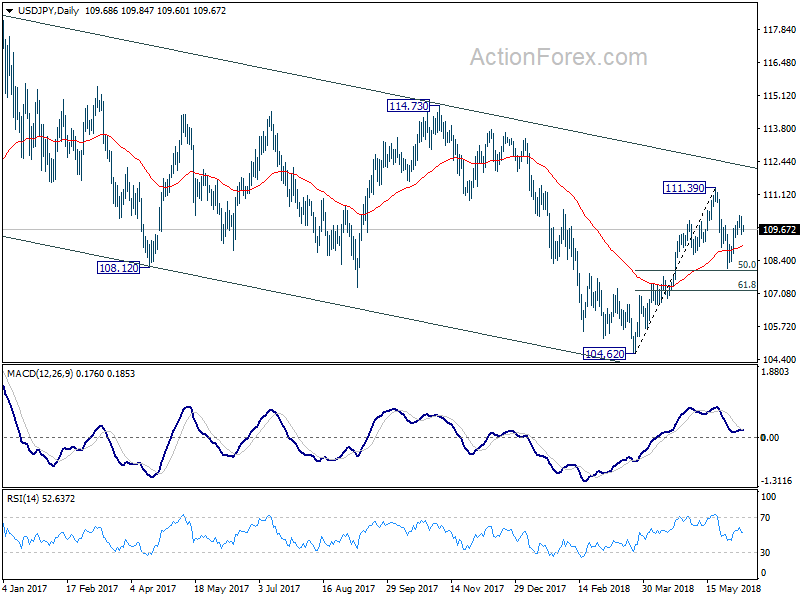

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.39; (P) 109.79; (R1) 110.10; More...

Intraday bias in USD/JPY is neutral for the moment with focus on 109.46 minor support. Break there will suggest that rebound from 108.10 has completed at 110.26 already. And intraday bias will be turned back to the downside for 108.10, or further to 61.8% retracement of 104.62 to 111.39 at 107.20. Though, break of 110.26 will resume the rebound to 111.39 resistance next.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

USDJPY Rebound at Risk as US Yields Reversed, G6+1 in Focus

Yen is picking up some strength in Asian session today while commodity currencies are generally lower. Pull back in US treasury yield is a factor that's support the Yen. 10 year yield hit as high as 2.992 over night but reversed to close at 2.933, down -0.042. That development dragged down USD/JPY, which is now back pressing 109.46 minor support. There isn't much new developments in the markets as eyes are on the G6+1 summit in Canada today and tomorrow. Confrontations are expected to continue between the US and others on trade issue. But traders could find themselves disappointed as US President Donald Trump has decided to leave the summit earlier to prepare for the meeting with North Korean Kim Jong-un three days after.

French Macron: We don't mind being six, if needs be

French President Emmanuel Macron urged to remain polite and productive in the G6+1 summit in Canada. But he also warned that "no leader is forever". Macron added that "maybe the American president doesn't care about being isolated today, but we don't mind being six, if needs be." And, "because these six represent values, represent an economic market, and more than anything, represent a real force at the international level today."

Combative Trump to leave the G6+1 ring early

The White House announced yesterday that Trump will leave the G6+1 summit in Canada earlier than anticipated, right after Saturday's morning session, on June 9. Then he will fly straight to Singapore for the highly anticipated Kim-Trump summit on June 12. G7 Sherpa and Deputy Assistant to the President for International Economic Affairs Everett Eissenstat will stay for the remaining session.

CBI expects BoE hikes in Q3 2018, Q1 2019 and Q4 2019

The Confederation of British Industry projects UK growth to lag well behind peers in 2018 and 2019. UK real GDP growth is forecast to be at 1.4% in 2018 and 1.3% in 2019 only. Eurozone growth is forecast to be at 2.2% in 2019 and 1.7% in 2019. US growth is forecast to be at 2.% in 2018 and 2.3% in 2019.

Though, UK would still be better than Japan at 1.1% growth in both 2018 and 2019. India is projected to stay strong with 7.3% growth in 2018 and 7.1% in 2019. China's growth is expected to slow notably to 6.3% in 2018 and 5.8% in 2019.

On monetary policy, CBI expects 25bps BoE hike in Q3 2018, Q1 2019 and Q4 2019. Inflation is projected to slow to 2.1% at the end of 2019.

CBI Chief Economist Rain Newton-Smith said that there is no disguising that UK is in "slow lane" for growth. And, "productivity weakness is a structural challenge for the UK economy and a drag on living standards." She also urged firms to work with the Government to "nurture a pro-enterprise environment to drive growth and create wealth." Also, "business and government must work together to drive competitiveness at home so firms can make the most of opportunities overseas" after Brexit.

China YTD trade surplus with EU narrowed to USD 45.2B, with US widened to USD 104.9B

China's trade surplus narrowed to USD 24.9B in May, below expectation of USD 32.5B. Exports rose 12.6% yoy to USD 212.8B while imports rose 26.0% yoy to USD 187.9B. in CNY terms, Exports rose 3.2% to CNY 1341B while imports rose 15.6% to CNY 1185B. Trade surplus narrowed to CNY 157B, below expectation of CNY 192B.

From January to May, exports to US rose 13.6% yoy to USD 175.17B while imports from the US grew 11.9% yoy to USD 70.32B. Trade surplus to the US was at USD 104.85B, widened from 2017 same period of USD 92.9B. Total trade with the US grew 13.1% to USD 245.50B.

For the same period, exports to EU rose 12.0% yoy to USD 155.39B while imports from EU rose 19.9% yoy to USD 110.21B. Trade surplus to EU was at USD 45.18B, narrowed from 2017 same period of USD 47.9B. Total trade with EU rose 15.1% yoy to USD 265.60B.

Canada job data to watch

On the data front, Japan Q1 GDP was finalized at -0.2% qoq, unrevised. GDP deflator was finalized at 0.5% yoy. Current account surplus widened to JPY 1.89T in April. German trade balance and industrial production will be featured in European session. But the main focus will be on Canada job data. The employment market is expected to grow 19.1k in May while unemployment would be unchanged at 5.8%. Canada will also release housing starts.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.39; (P) 109.79; (R1) 110.10; More...

Intraday bias in USD/JPY is neutral for the moment with focus on 109.46 minor support. Break there will suggest that rebound from 108.10 has completed at 110.26 already. And intraday bias will be turned back to the downside for 108.10, or further to 61.8% retracement of 104.62 to 111.39 at 107.20. Though, break of 110.26 will resume the rebound to 111.39 resistance next.

In the bigger picture, at this point, we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Current Account (JPY) Apr | 1.89T | 2.09T | 1.77T | |

| 23:50 | JPY | GDP Q/Q Q1 F | -0.20% | -0.20% | -0.20% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 F | 0.50% | 0.50% | 0.50% | |

| 03:15 | CNY | Trade Balance (CNY) May | 157B | 192B | 183B | |

| 03:23 | CNY | Trade Balance (USD) May | 24.9B | 32.5B | 28.8B | |

| 06:00 | EUR | German Trade Balance (EUR) Apr | 20.3B | 22.0B | ||

| 06:00 | EUR | German Industrial Production M/M Apr | 0.40% | 1.00% | ||

| 12:15 | CAD | Housing Starts May | 217K | 215K | ||

| 12:30 | CAD | Net Change in Employment May | 19.1K | -1.1K | ||

| 12:30 | CAD | Unemployment Rate May | 5.80% | 5.80% | ||

| 14:00 | USD | Wholesale Inventories M/M Apr F | 0.00% | 0.00% |

China YTD trade surplus with EU narrowed to USD 45.2B, with US widened to USD 104.9B

China's trade surplus narrowed to USD 24.9B in May, below expectation of USD 32.5B. Exports rose 12.6% yoy to USD 212.8B while imports rose 26.0% yoy to USD 187.9B. in CNY terms, Exports rose 3.2% to CNY 1341B while imports rose 15.6% to CNY 1185B. Trade surplus narrowed to CNY 157B, below expectation of CNY 192B.

From January to May, exports to US rose 13.6% yoy to USD 175.17B while imports from the US grew 11.9% yoy to USD 70.32B. Trade surplus to the US was at USD 104.85B, widened from 2017 same period of USD 92.9B. Total trade with the US grew 13.1% to USD 245.50B.

For the same period, exports to EU rose 12.0% yoy to USD 155.39B while imports from EU rose 19.9% yoy to USD 110.21B. Trade surplus to EU was at USD 45.18B, narrowed from 2017 same period of USD 47.9B. Total trade with EU rose 15.1% yoy to USD 265.60B.

2018 May trade data here

Market Morning Briefing: Dollar Index Tested A Low Near 93.21

STOCKS

Overall the global stock indices are mixed. While Nikkei and Shanghai may move down after facing stiff resistance levels, Dow looks bullish on a successful attempt to break above current levels. Dax and Nifty may remain stable in the near term.

Dow (25241.41, +0.38%) saw an intra-day high of 25326, breaking above the 25250 levels. This rise if sustains could turn bullish for the index towards 25750-26000 levels for the near term.

Dax (12811.05, -0.15%) is stable near current levels and does not look very bullish just now. As mentioned yesterday, there is some room on the upside towards 13000-13100 but while that holds, bearish possibilities of the index exist towards 12600-12500 or even lower.

Nikkei (22787.42, -0.16%) moved up to test daily trend resistance near 22800. If the resistance holds, we could see a rejection at current levels, pushing the index back towards 22000 levels. In case the index manages to break above 22800-23000 levels, it could turn bullish for the medium term thereby pulling up Dollar Yen also to higher levels.

Shanghai (3077.65, -1.02%) has started to dip from levels near 3150 and is again heading towards 3050. Near term is likely to be stable in the 3050-3150 region.

Nifty (10768.35, +0.78%) could remain in the broad trade range of 10850-10600 (both being immediate resistance and support levels) for the coming sessions. A break on either side would confirm the next course of movement. Till then we may expect some sideways consolidation to take place.

COMMODITIES

Commodities are all mixed. While precious metals remain stable, Copper is trading lower as part of the corrective dip after the recent sharp rally.Crude prices have moved up but need to break above immediate resistances to turn bullish for the longer run.

Copper (3.2588) is trading below 3.30 just now after moving up to 3.3130 on the upside. A corrective fall towards 3.20 looks likely before an attempt to move up further. Near term looks bearish.

WTI (66.07) has moved up a bit and could test 67 on the upside. Near term downside could be capped at 64 just now. Some movement in the broad 67-64 region is possible before a break on either direction. Brent (77.28) has also moved up sharply as expected. Downside could be limited to 76 in the next few sessions. WTI and Brent will have to break above 67 and 78 to turn bullish for the medium term and start moving up again; else there could be more dips in the coming sessions.

Gold (1296.55) continues to remain stable with no major movement. A small dip towards 1285 may be seen in the next couple of sessions.

FOREX

Dollar index (93.47) tested a low near 93.21 yesterday and is currently trading at higher levels. It could see an upmove till levels around 93.6-93.7 today and again move lower after that. As mentioned yesterday, 92.8 is a crucial level. A break below 92.8 would be the first indication of bearishness for Dollar Index in the medium term.

Euro (1.18): After seeing a high of 1.184 yesterday, the Euro has dipped. It could dip further to levels near 1.177-1.178 today, after which a rise back beyond 1.18 should take place. The 8 weeks MA near 1.19 is a crucial level and a breach of 1.19, if it happens, would be the first indication of a bullish Euro in the medium term.

Dollar Yen (109.77) again saw a high near 110.2 yesterday and has dipped from there. If it respects the upward channel on daily candles, then there could be a dip to 109.4 today followed by a rise towards 110-111 next week. There is crucial long term resistance on weekly line chart near 111 which should produce a dip.

Euro Yen (129.54): Euro Yen has dipped after seeing a high near 130.28 yesterday. Our expected upmove till 131.0-131.5 hasn’t come about yet. Given that we expect Euro and Dollar Yen to move towards 1.19 and 111 next week, Euro Yen could stay above 129 for most of the coming week.

Pound (1.3419): As per expectation, Pound has dipped after testing resistance on daily candles (near 1.347) yesterday. It should now move lower towards 1.33 in the coming sesions.

Dollar Rupee (67.125) : Near-term Resistances at 67.15-35 still holding on Dollar-Rupee. Whether the market closes above/ below 67.10 today may set the trend for next week.

INTEREST RATES

Current yields: US 10 Year (2.94%), 30 Year (3.08%), 5 Year (2.78%), 2 Year (2.50%)

The US 10 Year yield dropped from 2.97% to 2.92% yesterday on back of trade worries. It had earlier risen in the previous couple of days due to some hawkish comments by the ECB chief economist.

As we have been mentioning, the markets seem to be waiting for a trigger next week for the next significant move in US bond yields. The CPI data release on 12th June and the FOMC meet on 13th June could be the deciding factor for whether the 10 Year yield again rises past 3% or whether it drops to medium term support near 2.55%. A test of 2.55% by the 10 Year would open up the following levels for the other yields:

2.9% (30 Year) and 2.2% (5 Year)