Sample Category Title

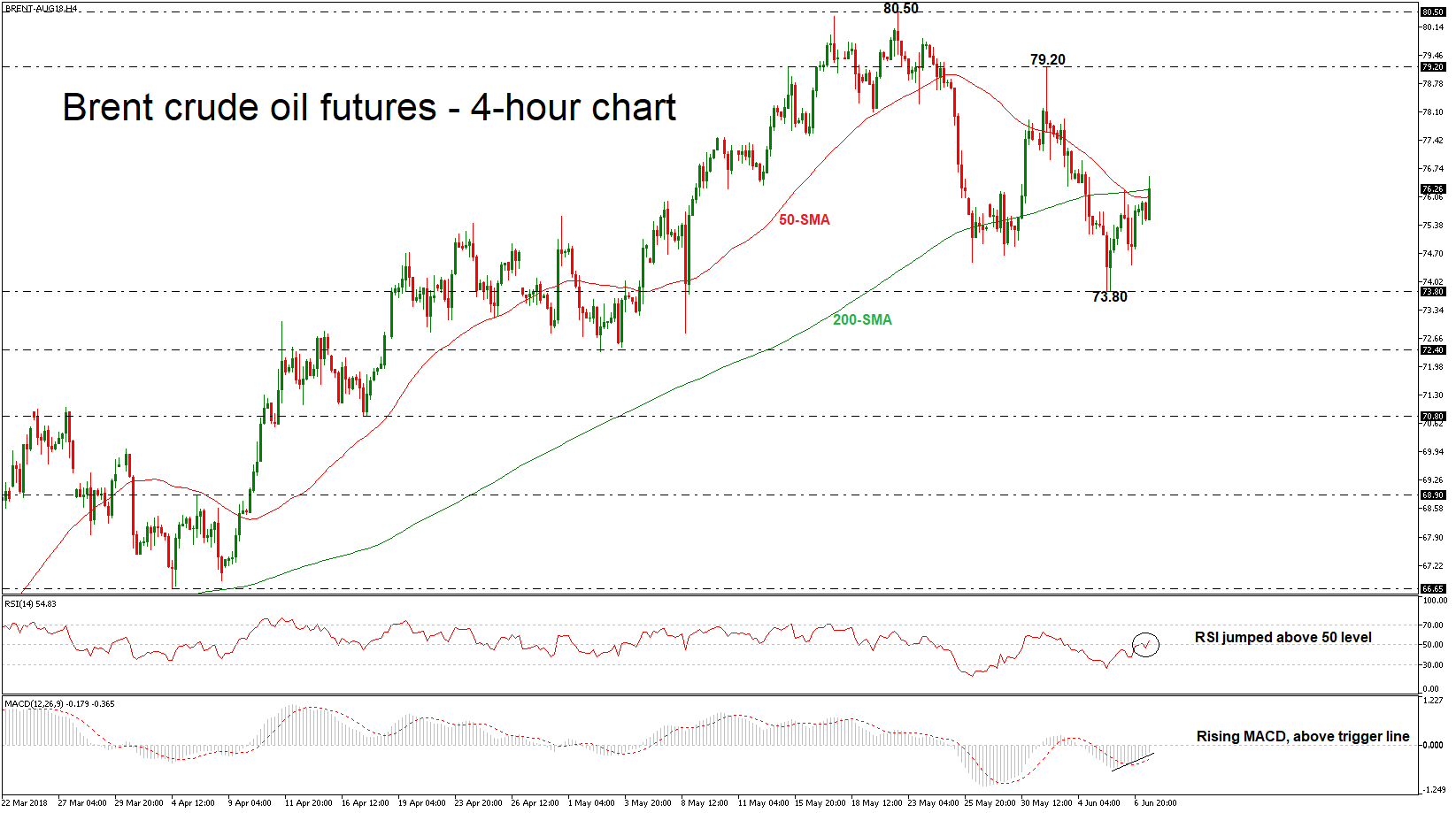

Brent Crude Oil Futures Turns Bullish in Short Term after Aggressive Sell-off

Brent futures have advanced considerably over the last couple of hours, surpassing the 50- and 200-simple moving averages (SMAs). The bullish picture in the short term looks to last for a while longer after the moving averages turned to the upside.

Support was met at around the 73.80 region after prices hit a one-month low, forcing the commodity to reverse higher. The positive bias in the near term is supported by the improvement in the momentum indicators. The MACD oscillator has risen sharply above its trigger line, while the RSI indicator is sloping upwards above the 50-neutral level, suggesting an upside correction.

If prices continue to head higher, resistance should come from the 79.20 mark, taken from the high on May 31. A climb above this region would reinforce the short-term bullish view and open the way towards the 80.80 barrier, which has been a major resistance area in the past.

However, should a downside reversal take form, immediate support will likely come from 73.80. A break of this level could shift the bias back to a bearish one, with the next support coming from the 72.40 level.

In the medium-term, the outlook remains positive since prices hold above all the moving averages and during the next few sessions, there is a possibility of a bullish cross between them.

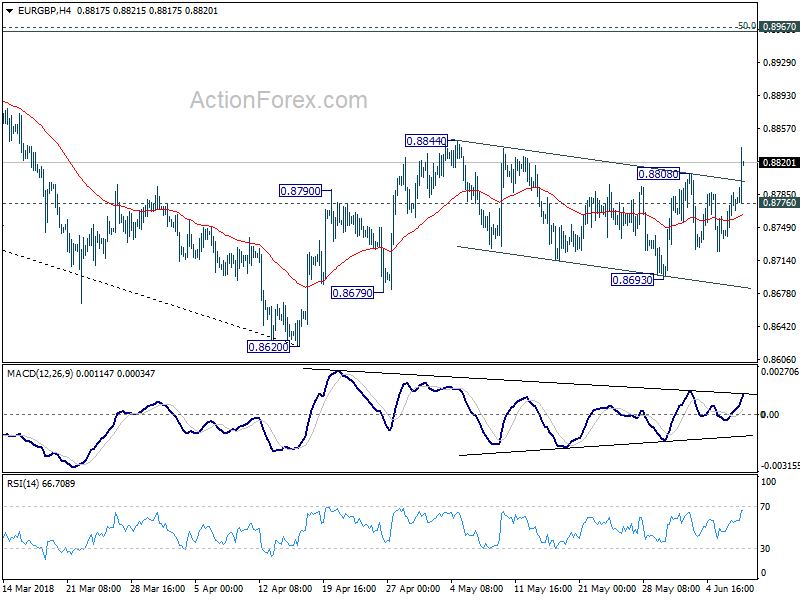

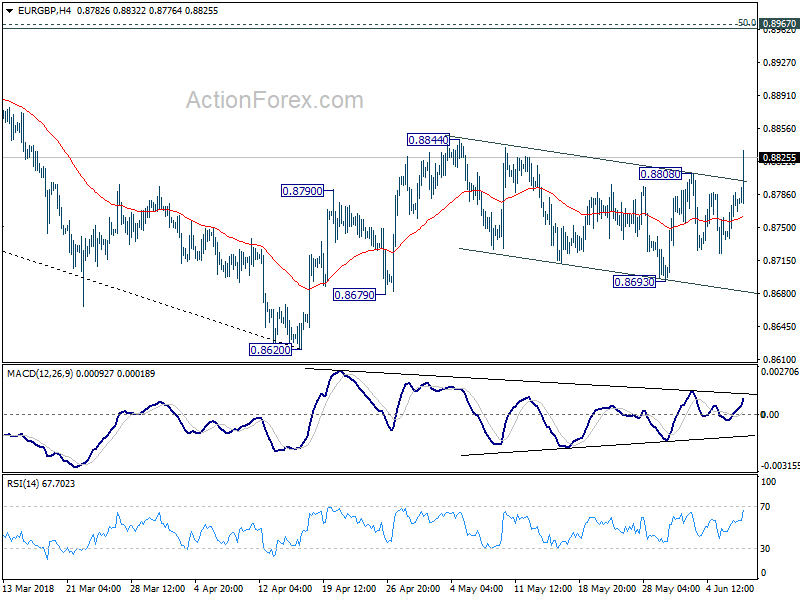

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8748; (P) 0.8769; (R1) 0.8798; More...

EUR/GBP surges to as high as 0.8837 so far today and the strong break of 0.8808 resistance argues that rise fro 0.8620 is ready to resume. Intraday bias back on the upside for 0.8844 resistance Decisive break there will confirm our bullish view and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). On the downside, below 0.8776 minor support will dampen the bullish case again and turn bias neutral.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

EURGBP Jumps as Fortunes of Euro and Sterling Diverge

Swiss Franc and Euro remain the strongest ones together. They're riding on the expectation that ECB will finally announce to quit the asset purchase program next week. Meanwhile, Sterling starts to lag behind and suffers some heavy selling today. Brexit uncertainty is back in spotlight, in particular the stick issue of Irish border. Australian and Canadian Dollar also turned weak while US Dollar is getting no love ahead of the G6+1 summit in Canada.

Technically, EUR/GBP's break of 0.8808 resistance is a key development today. This could finally make the end of a month long consolidation. But break of 0.8844 resistance is needed to confirm. Otherwise, it's just another false breakout. 0.8844 will be a focus for the rest of the day.

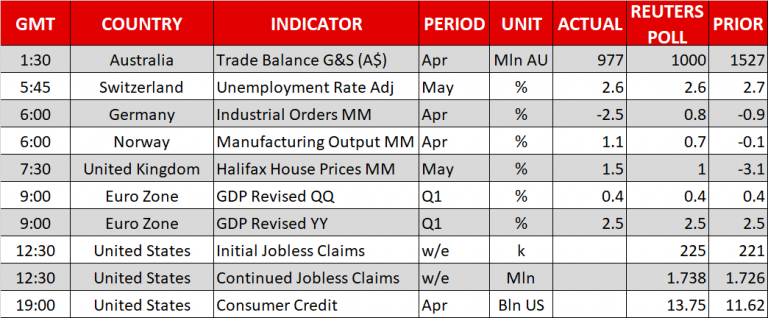

US initial jobless claims dropped 1k to 222k in the week ended June 2, below expectation of 225k. The four week moving average rose 2.75k to 225.5k. Continuing claims dropped -6k to 1.72m in the week ended May 26. Four week moving average of continuing claims dropped -13.25k to 1.72875m, lowest since December 8, 1973.

Released earlier, Eurozone GDP was finalized at 0.4% qoq in Q1, unrevised. German factory orders dropped -2.5% mom in April. Swiss unemployment rate dropped 0.1% to 2.6% in May. Swiss foreign currency reserves dropped to CHF 741b in May. Australia trade surplus narrowed to AUD 0.98B in April versus expectation of AUD 1.03B. Japan leading indicator rose to 105.6 in April.

UK May had constructive talks with Davis over backstop plan

UK Prime Minister Theresa May and her ministers will meet today to try to conclude on a "backstop" plan for Irish border after Brexit. The current proposal is believed to tie UK to EU customs union after a transition period. Based on current information, May could have conceded to an end date for the backstop plan. And the "harder" Brexit is not too welcomed by the market.

It's widely reported that Brexit minister David Davis is at odds with May over the the proposal because of the lack of end date. Davis also threatened to quit over the disagreement. May's spokeswoman said today that May and Davis had "constructive talks". And it's rumored that nobody will resign from the UK government today over Brexit.

Looking ahead, June 28-29 EU summit is an important deadline by which UK has to give an agreeable answer to EU regarding the Irish border. For now, it's highly unlikely for this to be met. Instead, the decision could be delayed to October 17-18 EU summit. But at the same time, October is the deadline for agreement the divorce bill and terms. So, tough time ahead for May for sure.

Euro extends rally on ECB expectations

On the other hand, Euro continues to shine on expectation that ECB could finally announce the end of the asset purchase program next week. It's generally believed that expectations are well in place that the EUR 30b per month asset purchase will end this year. And more importantly, ECB policymakers wouldn't want to upset such expectation. The question is whether the program will end after September or December. Recent stronger than expected inflation data is pushing the chance towards September. This is also helped by receding political risks in Italy. The expectation was also affirmed by ECB chief economist Peter Praet that policy makers will have a judgement call next week.

German 10 year bund yield's rally this week is a clear reflection of the situation. It reached as low as 0.186 at the height of Italian political turmoil last week. But today, it breaks 0.5 handle to as high as 0.520. It's back at the pre-Italian crisis support level and we'll see if it can push through 0.5 with conviction.

Trump to fight for the US at G6+1 against its allies

G7 summit will be the key focus towards the weekend. It's turning out to be a G6+1 with Trump against all the supposed US allies. French President Emmanuel Macron and Canadian Prime Minister Justin Trudeau expressed their unified stance on the push for "strong multilateralism" after meeting in Ottawa yesterday. The G7 meeting is set to be a confrontation between G6 versus the US on a range of issues, in particular, the US steel and aluminum tariffs on its closest allies. Trudeau said there will be " frank and sometimes difficult discussions around the G7 table, particularly with the US president on tariffs." Trump appears not backing down on his protectionism as he tweeted that he's "Getting ready to go to the G-7 in Canada to fight for our country on Trade (we have the worst trade deals ever made)".

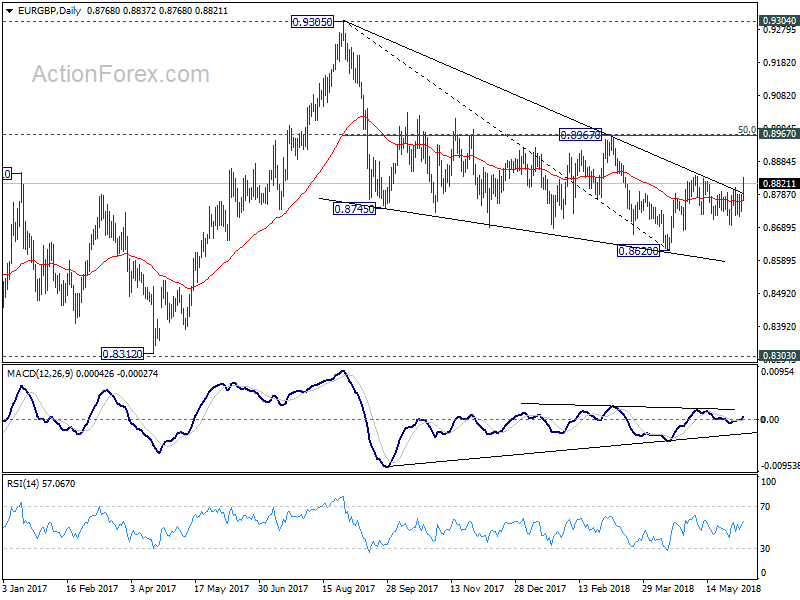

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8748; (P) 0.8769; (R1) 0.8798; More...

EUR/GBP surges to as high as 0.8837 so far today and the strong break of 0.8808 resistance argues that rise fro 0.8620 is ready to resume. Intraday bias back on the upside for 0.8844 resistance Decisive break there will confirm our bullish view and target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963). On the downside, below 0.8776 minor support will dampen the bullish case again and turn bias neutral.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Apr | 0.98B | 1.03B | 1.53B | 1.73B |

| 05:00 | JPY | Leading Index CI Apr P | 105.6 | 105.6 | 104.4 | |

| 05:45 | CHF | Unemployment Rate May | 2.60% | 2.60% | 2.70% | |

| 06:00 | EUR | German Factory Orders M/M Apr | -2.50% | 0.70% | -0.90% | -1.10% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) May | 741B | 757B | ||

| 07:30 | GBP | Halifax House Prices M/M May | 1.50% | 1.10% | -3.10% | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 F | 0.40% | 0.40% | 0.40% | |

| 12:30 | USD | Initial Jobless Claims (2 JUN) | 222K | 225K | 221K | 223K |

| 14:30 | USD | Natural Gas Storage | 87B | 96B |

US initial jobless claims dropped -1k to 222k in the week ended June 2

US initial jobless claims dropped -1k to 222k in the week ended June 2, below expectation of 225k. The four week moving average rose 2.75k to 225.5k.

Continuing claims dropped -6k to 1.72m in the week ended May 26. Four week moving average of continuing claims dropped -13.25k to 1.72875m, lowest since December 8, 1973.

Will Ontario Election Shake Up Canadian Dollar?

It has been an uneventful week for the Canadian dollar, and the trend has continued on Thursday. Currently, USD/CAD is trading at 1.2958, up 0.11% on the day. On the release front, the U.S unemployment claims is expected to edge up to 223 thousand. The Bank of Canada will release its semi-annual Financial System Review, followed by a press conference with BoC Governor Stephen Poloz. Ontario is holding a provincial election, with the Conservatives expected to form a majority government. On Friday, Canada releases employment change and the unemployment rate. As well, G-7 leaders are meeting in Quebec for their annual summit.

All eyes are on the Ontario provincial election on Thursday. Just hours before poll stations opening, the election remains too close to call. Polls are showing the Conservatives with a slender majority in the popular vote over the left-wing NDP, with the governing Liberals trailing far behind. However, the Conservatives are expected to win most of the electoral districts (ridings), and the latest polls are showing a whopping 87% likelihood that they will form a majority government. The actual results will largely depend on voter turnout and regional dynamics. A Conservative majority will likely boost the Canadian dollar, but a minority government or an NDP win would likely send the loonie sharply lower.

Meetings between G-7 leaders are often a chance to catch up with friends and hold a photo-op, but this year’s summit could be explosive, with plenty of bad will between six of the members and President Trump. The reason? The renewal of the tariff spat, courtesy of the U.S slapping aluminum and steel tariffs on the European Union and Canada. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. Will we see a higher profile, repeat performance at this meeting? Canada and Mexico have already announced retaliatory duties on U.S products. The escalating trade battle is sure to dominate the summit, and if the leaders fail to resolve matters, the result could be a nasty trade war between the U.S and its major trading partners.

Bristish Pound dives as Brexit comes back to spotlight, EURGBP upside breakout

Entering into US session, Swiss Franc and Euro remain the strongest one for today. However, Sterling is starting to lag behind.

Indeed, the Pound is suffering some heavy selling on Brexit under certainties. UK Prime Minster Theresa May is yet to unify his cabinet on the backstop plan over Irish border. Ahead of their meeting today, it's widely reported that May is at odds with Brexit secretary David Davis, who threatened to quit.

EUR/GBP is showing some strength by breaking 0.8808 resistance. H and 6H action bias have both turned upside blue. But they can be force signal in ranging consolidation markets.

Hence, we'd wait for a firm break of 0.8844 resistance to confirm resumption of rise from 0.8620 to go long. Target is 0.8967 key resistance level.

Dollar Takes The Back Seat As Euro, Pound Move Forward

Here are the latest developments in global markets:

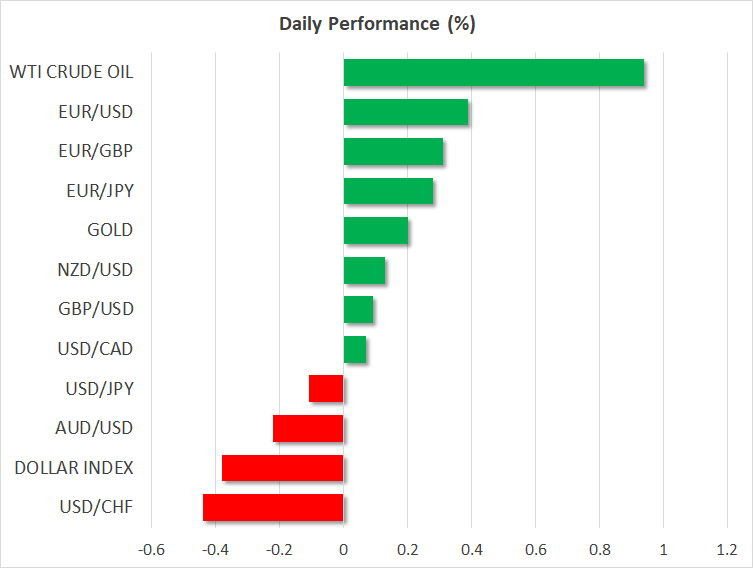

FOREX: The euro kept shining during the early European afternoon as yesterday’s comments by ECB officials raised speculation that the central bank was preparing to exit its quantitative program by the end of this year, with the announcement probably coming as soon as next week. Euro/dollar managed to peak at a fresh three-week high of 1.1837 before it fell to 1.1815 (+0.39%), being the best performer among its major peers. Against the yen, the euro posted moderate gains, edging up to 129.91 .(+0.15%), while versus the swiss franc it was down today at 1.1592 (-0.16%). Meanwhile in Italy, April’s retail sales recorded the sharpest decline since February, with the statistical office noting that economic growth could lose steam in coming months. Pound/dollar was the second-best performer of the day, winning 0.32%. Upbeat Halifax House prices helped the pair to reach a new two-week peak at 1.3471, though it soon returned to 1.3448. Euro/pound changed hands higher at 0.8788 (+0.13%). The dollar was on the back foot today at 109.92 (-0.22%), while the dollar index also stood lower at 93.32 (-0.36%) as investors turned more confident on the euro and pound amid tense trade relations between the US and the rest of the world. Dollar/loonie was steady at 1.2947. Aussie/dollar remained near today’s lows, fluctuating at 0.7655 (-0.20%) after trade stats out of Australia disappointed early today, showing a narrower trade surplus. Kiwi/dollar rose to 0.7047 (+0.23%). Dollar/Turkish lira moved up to 4.58 (+0.54%) ahead of a rate decision by the Turkish central bank. Recall that the Turkish President’s interest to monitor monetary policy after the June 24 presidential elections drove the pair to record highs recently.

STOCKS: After a respectful rally in Wall Street, European equities opened higher, with financials joining the biggest gains after ECB officials signaled that the central bank’s bond-buying program could come to an end by December this year. At 1100 GMT, the pan-European STOXX 600 was up by 0.15%, while the blue-chip Euro STOXX 50 was rising by 0.11%. The German DAX 30 gained 0.15%, the French CAC 40 climbed by 0.27% and the Italian FTSE MIB jumped by 0.31%. UK’s FTSE 100 inched up by 0.02% after a delayed open in the London Stock Exchange market due to technical issues, while the Spanish IBEX 35 was the best performer, surging by 0.79% towards two-week highs. In the US, futures tracking major stock indices were marginally higher, pointing to a slightly positive open.

COMMODITIES: Crude oil prices were rising on Thursday, supported by supply troubles in Venezuela. Particularly, the OPEC member is said now to be one month behind from serving customers from its export terminals as Trump’s sanctions imposed on the state-owned oil company PDVSA were said to disrupt the flow of activities. Increasing production in the US and worries that OPEC could raise its output at its two-day policy meeting on June 22-23 capped gains in the market. WTI crude and Brent were last seen at $65.35/barrel (+0.96%) and $76.34/barrel (+1.30%) respectively. In precious metals, gold was trading moderately higher around $1,298.70/ounce (+0.19%) on the back of a weaker dollar.'

Day Ahead: US jobless claims and Japan’s final GDP growth figures on today’s calendar

Looking at the calendar, out of the US, weekly jobless claims – initial and continued – due at 1230 GMT will be gathering attention. The Department of Labor forecasts 223,000 individuals to have applied for unemployment benefits in the week ending June 1, little changed from the preceding week’s 221,000. The world’s largest economy will also see the release of October consumer credit data at 1900 GMT.

Still, investors are turning their focus to the Group of Seven meeting later this week that may give clues on global trade tensions, as well as policy meetings from the European Central Bank and Federal Reserve next week. Today, sources stated that Germany and France joined voices to warn the US President of an inconclusive G7 meeting if progress in tariffs and the Iranian nuclear deal fails to be made.

Overnight, at 2350 GMT, the focus will also turn to Japan with the release of final GDP growth data. GDP growth is expected to fall by 0.4% on an annualized basis, less than the 0.6% decline estimated initially. On a quarterly basis, GDP growth is predicted to decline by 0.1% compared to a fall of 0.2% in the previous quarter.

The Bank of England’s Deputy Governor of Markets and Banking, Dave Ramsden is scheduled to speak in public today at 1600 GMT, while earlier at 1515 GMT, the Bank of Canada Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins will be holding a press conference to discuss the contents of the Financial System Review

Meanwhile, the U.S. President Donald Trump will meet with Japanese Prime Minister Shinzo Abe at the White House ahead of next week’s US-North Korea summit in Singapore.

In Turkey, the central bank will decide on interest rates at 1100 GMT, while in the UK, British Ministers will meet in an effort to find common ground on the Irish border, an issue that continues to be a thorn in Brexit negotiations

Peripheral Yields Move Lower In Session Aided By Strong Spainish Auction Results

Notes/Observations

Asia:

- Germany Apr Factory Orders miss expectations

- Trade tension seen ahead of G7 leader summit; speculation that there was no chance that the US and other G7 members could reach common ground

- China May FX Reserves registers its 3rd straight monthly decline

- Spain auction results deemed strong

Asia:

- China Commerce Min (MOFCOM): Some 'specific' progress made on just completed trade talks, details in trade talks will US 'are to be confirmed'; to implement consensus reached in Washington. Reiterated view that did not want trade tensions to escalate. Confirmed talks included in depth discussions on energy and agriculture

- Australia Apr Trade Balance registers its 4th straight surplus (A$1.0B v A$1.0Be)

Europe:

- Italy's PM Conte government won a 2nd confidence vote, in lower House (as expected)

- Greece said to have delayed a planned bond sale due to concerns about instability in Italy

- UK PM May said to be keeping Brexit supporters in the dark about her backstop plans

- PM May reportedly has compromised with Tory rebels on timing of withdrawal bill hearing; ministers believe Tory rebels will be won over on Customs Union amendment to EU withdraw bill next week. To meet senior ministers in an attempt to resolve tensions over the government's Brexit "backstop" plan. In the proposal the UK would match EU tariffs temporarily in order to avoid a hard Irish border post-Brexit. It would also outline what would happen should no permanent solution be agreed with the EU before the UK's 2019 exit

Americas:

- Senate Banking Committee to vote on June 12 on nominations of Richard Clarida for Fed Vice Chair and Michelle Bowman for Fed Governor

Economic Data:

- (NL) Netherlands May CPI M/M: 0.3% v 0.4% prior; Y/Y: 1.7% v 0.9% prior

- (NL) Netherlands May CPI EU Harmonized M/M: 0.4% v 0.6% prior; Y/Y: 1.9% v 1.3%e

- (CH) Swiss May Unemployment Rate: 2.4% v 2.5%e; Unemployment Rate (Seasonally Adj): 2.6% v 2.6%e

- (DE) Germany Apr Factory Orders M/M: -2.5% v +0.8%e; Y/Y: -0.1% v +3.6%e

- (RO) Romania Q1 Preliminary GDP (2nd reading) Q/Q: 0.0% v 0.0% advance; Y/Y: 4.0% v 4.0%e

- (NO) Norway Apr Industrial Production M/M: -1.4% v -0.7% prior; Y/Y: -1.9% v +0.2% prior

- (NO) Norway Apr Manufacturing Production M/M: 1.1% v 0.7%e; Y/Y: 1.3% v 0.9% prior

- (DK) Denmark Apr Industrial Production M/M: +1.2% v -0.4% prior

- (ZA) South Africa May Gross Reserves: $51.2B v $49.4Be; Net Reserves: $42.9B v $43.0Be

- (FI) Finland Apr Preliminary Trade Balance: +€0.1B v -€0.2B prior

- (AU) Australia May Foreign Reserves (AUD): 82.5B v 72.8B prior

- (FR) France Apr Trade Balance: -€5.0B v -€5.1Be

- (FR) France Apr Current Account: -€1.1B v -€0.6B prior

- (ES) Spain Q1 INE House Price Index Q/Q: 1.4 % v 0.9% prior; Y/Y: 6.2% v 7.2% prior

- (CH) Swiss May Foreign Currency Reserves (CHF): 740.9B v 757.2B prior

- (AT) Austria May Wholesale Price Index M/M: 1.4% v 1.3% prior; Y/Y: 5.2% v 2.9% prior

- (MY) Malaysia End-May Foreign Reserves: $108.5B v $109.4B prior

- (UK) May Halifax House Prices M/M: 1.5% v 1.0%e ; 3M/Y: 1.9% v 1.9%e

- (IT) Italy Apr Retail Sales M/M: -0.7% v +0.1%e; Y/Y: -4.6% v +2.9% prior

- (CZ) Czech May International Reserves: $144.9B v $147.5B prior

- UN FAO World Price Index: 176.2 v 173.5 prior

- (CN) China May Foreign Reserves: $3.1106T v $3.107Te (3rd straight monthly decline)

- (IT) Bank of Italy (BOI) May Balance sheet aggregates: Target-2 liabilities €464.7B (record level) v €426.1B prior

- (EU) Euro Zone Q1 Final GDP Q/Q: 0.4% v 0.4%e; Y/Y: 2.5% v 2.5%e

- (EU) Euro Zone Q1 Household Consumption Q/Q: 0.5% v 0.2%e; Govt Expenditure Q/Q: 0.0% v 0.2%e, Gross Fixed Capital Q/Q: 0.5% v 0.7%e

- (GR) Greece Mar Unemployment Rate: 20.1% v 20.6% prior

- (HU) Hungary May YTD Budget Balance (HUF): -1.188T v -1.081T prior

- (SG) Singapore May Foreign Reserves: $287.9 v $287.7B prior

Fixed Income Issuance:

- (ES) Spain Debt Agency (Tesoro)sold total €2.35B vs.€2.0-3.0B indicated range in 2021, 2023 and 2028 SPGB Bonds

- Sold €718M in 0.05% Jan 2021 SPGB; Avg yield: -0.037% v -0.145% prior, Bid-to-cover: 3.30x v 2.66x prior

- Sold €558M in 0.35% July 2023 SPGB; Avg yield: 0.440% v 0.443%prior; Bid-to-cover: 2.88x v 1.83x prior

- Sold €1.07B in 1.40% Apr 2028 SPGB; Avg yield: 1.406% v 1.370% prior, Bid-to-cover: 2.19x v 2.25x prior

- (ES) Spain Debt Agency (Tesoro) sold €2.17B vs. €1.25-2.25B indicated range in I/L 2023 bonds (SPGBei;Bonoei); Real Yield: -0.792% v -1.578% prior; Bid-to-cover: 1.69x v 2.67x prior

- (FR) France Debt Agency (AFT) sold total €8.997B vs. €8.0-9.0B indicated range in 2028, 2029, 2031 and 2036 Oats

- Sold €3.387B in 0.75% Nov 2028 Oat; Avg Yield: 0.90% v 0.81% prior; Bid-to-cover: 1.92x v 1.88x prior (May 3rd 2018)

- Sold €1.999B in 5.5% Apr 2029 Oat; Avg Yield: 0.86% v 0.60% prior; Bid-to-cover: 2.05x v 1.79x prior (Dec 7th 2017)

- Sold €2.164B in 1.50% May 2031 Oat; Avg Yield 1.08% v 1.01% prior; Bid-to-cover: 1.84x v 1.62x prior (Nov 2nd 2017)

- Sold €1.447B in 1.25% May 2036 Oat; Avg Yield 1.37% v 1.35% prior; Bid-to-cover: 2.14x v 1.90x prior

- (SE) Sweden sold SEK500M in I/L 2027 Bond; Avg Yield: -1.3716% v -1.2300% prior; Bid-to-cover: 1.90x v 2.51x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.3% at 388.0, FTSE flat at 7710, DAX +0.2% at 12860, CAC-40 +0.4% at 5481, IBEX-35 +0.9% at 9879, FTSE MIB +0.4% at 21890, SMI +0.5% at 8595, S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European Indices trade higher across the board following on from a strong session in Wallstreet overnight, and lower peripheral yields. The FTSE fades earlier gains after an earlier technical glitch meant a delayed opening. Brokers CMC Markets and Plus 500 trade higher after upbeat results and outlook, with Autotrader, RWS and Mitie Group notable risers after earnings and updates. Meanwhile Remy Cointreau trades almost 5% lower after its full year results slightly missed expectations. Shares of Duerr in Germany also outperforms after the company lifted its full year Revenue outlook. Looking ahead notable earners include Conn's Inc, JM Smucker and Vail resorts.

Movers

- Consumer Discretionary Autotrader [AUTO.UK] +6% (Earnings), Remy Cointreau [RCO.FR] -4.9% (Earnings), Mitie Group [MTO.UK] +5% (Earnings), RWS [RWS.UK] +8.4% (Earnings)]

- Industrials Duerr [DUE.DE] +6% (Lifts outlook)

- Financials Plus 500 [PLUS.UK] +5.8% (Upbeat outlook), CMC Markets [CMCX.UK] +5% (Earnings)

Speakers

- Italy Stats Agency (ISTAT) Monthly Economic Outlook: leading indicators show a slowdown for next months

- Sweden Central Bank (Riksbank) Jochnick: Approaching the time for the 1st rate hike. Needed to see inflation stabilize around the 2% level and slightly higher underlying inflation. He added that need to wait a bit longer with Repo rate hikes

- Greece govt official stated that the gvot was committed to existing fiscal reforms targets under post-bailout surveillance. IMF prefered debt relief measures beyond what the Eurogroup wanted. France proposal to link debt repayments to GDP growth on the table; depended on length that loans are extended after 2022

- Norway Fin Min Jensen: Neutral fiscal stance is appropriate

- IMF on Norway: Higher economic growth in Norway warranted a neutral fiscal stance and central bank should gradually normalize monetary policy. Forecasted Norway’s Mainland 2018 and 2019 GDP growth at 2.5%

- Norway Stats Agency (SSB) Economic Outlook cuts 2018 Mainland GDP from 2.4% to 2.1%and Underlying CPI from 1.7% to 1.6% it

- Russia Central Bank (CBR) Gov Nabiullina: Easy policy was necessary to provide time to enact reforms. Move to neutral policy would mean the end of the rate cut cycle and could raise interest rates if there were risks. Goal was to keep inflation around the 4% target

- Philippines Central Bank (BSP) May Minutes: Rate hike was preemptive to temper CPI and help arrest 2nd round effects

- China FX Regulator SAFE reiterated view that FX reserves to remain stable overall

Currencies

- The USD was softer against the major pairs with trade tension ahead og G7 cited as a factor as there appeared to be no chance that the US and other G7 members could reach common ground

- EUR/USD continued its move higher as dealers continued the unwind of bearish ECB bets . Market participants believe that the ECB was likely to discuss quantitative easing at its June meeting and could hint when investors should expect its end.

- The USDJPY moved back below the 110 level in the session with dealers citing some uncertainty on trade issues ahead of the G7 leader summit that begins on Friday. On a technical note one analyst noted that the pair has failed to overcome its 200DMA and the 61.8% retracement level of its previous decline and could pave the way for a test lower towards 108 area.

Fixed Income

- Bund Futures trade 35 ticks lower at 159.60 as German 10-year Bund yield rises back to the 0.50 level. Upside targets 161.75 followed by 162.50, while a return lower targets the 159.25 level.

- Gilt futures trade at 123.31 lower by 48 with the September Gilt falling under pressure. Support continues stands at 122.75 then 122.25, with upside resistance at 124.85 then 126.35.

- Thursday’s liquidity report showed Wednesday’s excess liquidity fell from €1.923T to €1.922T. Use of the marginal lending facility increased from €99M to €146M.

- Corporate issuance saw 8 issuers raise $7.2B in the primary market

Looking Ahead

- (IL) Israel May Foreign Currency Balance: No est v $115.4B prior

- 06:00 (IE) Ireland May CPI M/M: No est v -0.2% prior; Y/Y: No est v -0.4% prior

- 06:00 (IE) Ireland May CPI EU Harmonized M/M: No est v -0.2% prior; Y/Y: No est v -0.1% prior

- 06:00 (RO) Romania to sell Bills

- 06:00 (RO) Romania to sell Bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (TR) Turkey Central Bank (CBRT) Interest Rate Decision: Expected to leave One-Week Repo Rate unchanged at 16.50%; Raise Overnight Lending Rate by 75bps to 18.75%; Raises the Overnight Borrowing Rate by 50bps to 15.50%; Leave the Late Liquidity Window (LLW) unchanged at 19.50%

- 07:00 (ZA) South Africa Apr Manufacturing Production M/M: 0.3%e v 1.3% prior; Y/Y: +1.7%e v -1.3% prior

- 07:00 (BR) Brazil May FGV Inflation IGP-DI M/M: 1.4%e v 0.9% prior; Y/Y: 4.9%e v 3.0% prior

- 08:00 (PL) Poland May Official Reserves: No est v $113.2B prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Initial Jobless Claims: 221Ke v 221K prior; Continuing Claims: 1.74Me v 1.726M prior

- 08:30 (CL) Chile May Trade Balance: $0.9Be v $1.0B prior; Total Exports: $6.6Be v $6.4B prior; Total Imports: $5.8Be v $5.4B prior; Copper Exports: No est v $3.0B prior

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (MX) Mexico May CPI M/M: -0.2%e v -0.3% prior; Y/Y: 4.5%e v 4.6% prior, CPI Core M/M: 0.2%e v 0.2% prior

- 09:00 (CL) Chile Apr Nominal Wage M/M: 0.9%e v 0.6% prior; Y/Y: 3.8%e v 3.7% prior

- 09:00 (RU) Russia Gold and Forex Reserve w/e Jun 1st: No est v $457.2B prior

- 09:00 (RU) Russia May Official Reserve Assets: $458.0Bev $459.9B prior

- 10:30 (CA) Bank of Canada (BOC) Financial System Review (FSR)

- 10:30 (TR) Turkey May Cash Budget Balance (TRY): No est v -12.9B prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (UK) BOE’s Ramsden in London

- 12:00 (US) Fed Reports Q1 Financial Accounts: Household Change in Net Worth: No est v $2.076T prior

- 15:00 (US) Apr Consumer Credit: $14.0Be v $11.6B prior

- 19:00 (PE) Peru Central Bank (BCRP) Interest Rate Decision: Expected to leave Reference Rate unchanged at 2.75%

Markets Mixed As Focus Turns To Brexit Talks

- EUR Adds to Gains as ECB Mulls Over QE Exit;

- GBP Benefits From Weaker USD;

- Jobless Claims and Central Bankers Today's Notable Events.

EUR Adds to Gains as ECB Mulls Over QE Exit

It's been a relatively quiet start to trading on Thursday, with much of the focus falling on the UK as it prepares for more Brexit talks with the European Union. Stock markets are trading relatively mixed while US futures are pointing to a similar open on Wall Street.

The dollar is making further declines today even as yields on US bonds tick higher on a combination of safe haven unwinding and an expectation of higher interest rates. It's also worth noting that the greenback has made strong gains over the last couple of months and the recent weakness is actually only a small corrective move in that rise.

The decline in the dollar has been strongly aided by a sudden hawkish shift in some comments coming out of the ECB though, which has in turn lifted the euro since the start of the month. While the central bank was always likely to adopt a more hawkish tone if it was planning to exit QE this year, people were starting to question whether this would in fact happen due to slowdown in inflation, growth and PMI surveys at the start of the year. This contributed to the drop off in the euro against the dollar, the only question now is whether the pair has bottomed for now.

GBP Benefits From Weaker USD

The move in the greenback is also aiding other currencies, with the pound seeing decent gains on the day despite the lack of specific sterling positive news and as Brexit negotiations appear to have reached a very difficult point. Speculation has been growing that David Davis – Brexit Secretary – could resign in protest against Theresa May's backstop plans, which would be a major blow to the Prime Minister and could risk triggering more if other Brexiteers are of similar views.

Still, that doesn't appear to be weighing on the pound just yet and the gains in the currency is once again weighing on the FTSE 100 which is underperforming its peers in Europe. As negotiations progress, sterling traders may not be quite so forgiving to the constant splits on the Brexit “war cabinet” which is significantly hampering the process.

Jobless Claims and Central Bankers Today's Notable Events

It's going to be another relatively quiet session from an economic data standpoint, with the only notable release coming from the US in the form of weekly jobless claims, although it's been some time since that's been much of a market impacting release. We will also hear from Bank of Canada Governor Stephen Poloz and the Bank of England's David Ramsden which may provide some comments of note.

US Futures Setting A Strong Tone | How Low Can Oil Go?

US futures are roaring once again, investors are picking up the momentum where they left off yesterday. Dow Jones topped the 25K mark yesterday and the NASDAQ is equally flexing its muscles. This has stimulated confidence amidst investors.

European political woes have taken the back seat. Investors are finding comfort that things are back to normal after Italian Prime Minister won the second vote of confidence without any labour. There has been enormous upheaval in the European political landscape from all angles: a new government in Italy, a new Prime Minister in Spain.

Yes, on the outset, things are looking a lot more calmer today but investors should not forget that the new government in Italy is a populist one. Tensions could anchor in no time.

When it comes to the forex market, it is only one event which matters the most- the European Central Bank meeting. Although, the Euro is no longer as strong as it was a couple of months ago, but we do think that between now and until the day the ECB meets, it is likely that the path of the least resistance may be skewed to the upside. Why? Because it is about time that the ECB shows it’s strong side and a firm stance towards winding down the tents of its easing monetary policy.

Euro bulls have already started to react positively and the Euro/Dollar pair has gained a lot of its lost ground. The battle is on.

As for the energy market, we are seeing some recovery in the oil market and the fact that Venezuela is in trouble with respect to its export. The flashing red light on the trader’s dash board is still the possibility of the production increase by the cartel- OPEC. The cartel curved the supply to prop up the prices but given that the Iranian oil may see some roads closed to the global market, the cartel needs to cover this supply.

Realistically speaking, the price has been battered already from its highs: the price of WTI moved from its high of $72 to all the way to $64. But, I do think there is still more room left for this trade as speculators would aim for the round number of $60.