Sample Category Title

British Pound Shrugs Off Strong Housing Inflation Data

The British pound has posted slight gains in the Thursday session. In North American trade, GBP/USD is trading at 1.3432, up 0.15% on the day. On the release front, British Halifax HPI recorded a strong gain of 1.5%, beating the estimate of 1.1%. In the U.S, unemployment claims ticked up to 222 thousand, just below the estimate of 223 thousand. On Friday, the U.K releases Consumer Inflation Expectations.

Talks between Britain and the European Union are largely stalled, even though time is of the essence, as Brexit is only nine months away. Prime Minister May continues to be hampered by serious divisions in her government concerning Brexit, making negotiations with the Europeans all the more difficult. One of the thorniest issues is the Irish border. Currently, there is no hard border between Northern Ireland and Ireland, but some mechanism will have to be put into place once Britain leaves the European Union. Many ideas have been floated about, and on Thursday, the May government proposed a ‘backstop’ (last resort) plan. This means that Britain would be part of the EU customs union up to December 2021, unless the parties reached an alternative arrangement prior to this date. May is calling this proposal a “temporary customs union”, and it remains to be seen if the EU will accept the backstop solution.

The annual G-7 summit is often a chance for leaders are often a chance to catch up with friends and hold a photo-op, but this year’s summit could be explosive, with plenty of bad will between six of the members and President Trump. The reason? The renewal of the tariff spat, courtesy of the U.S slapping aluminum and steel tariffs on the European Union and Canada. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. Will we see a higher profile, repeat performance at this meeting? Canada and Mexico have already announced retaliatory duties on U.S products. The escalating trade battle is sure to dominate the summit, and if the leaders fail to resolve matters, a trade war could hurt the British economy.

Loonie Looks Next at Employment Data for Direction

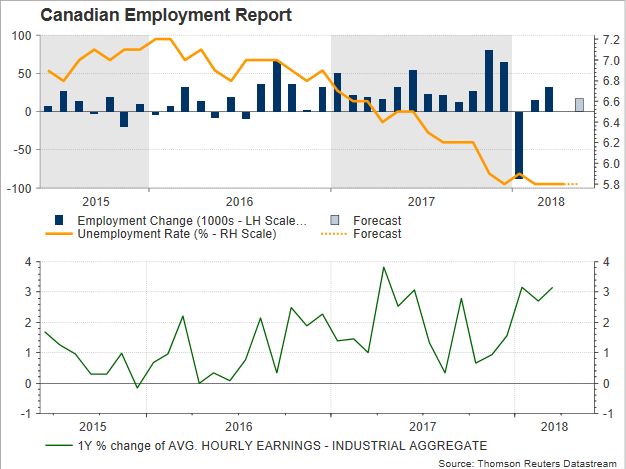

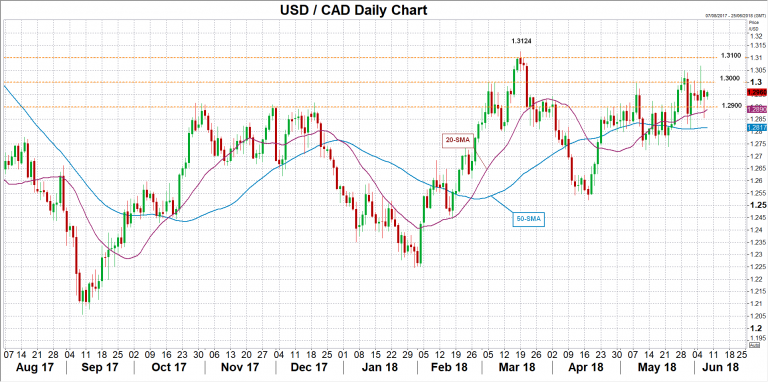

The weekend after Trump decided to impose tariffs on steel and aluminum imports from Canada, Mexico, and the EU, the Bank of Canada’s Governor, Stephen Poloz, returned to his more cautious style, saying that the central bank will use its data-dependent approach to adjust monetary policy. The statement also came a couple of days after the central bank’s rate statement laid the ground for further monetary tightening this year, with investors now turning focus to upcoming employment data to verify whether July’s rate hike could ever take place.

On Friday at 1230 GMT, Canada’s employment report for the month of May is expected to show a respectful rise of 17.5k in job positions after April’s numbers indicated an unexpected a fall of 1.1k. The big miss, however, did not raise worries as the job losses were recorded in part-time positions, while full-employment continued to grow. Regarding the unemployment rate, this is projected to remain unchanged at 5.8% – the lowest level reached since 1974 – for the third consecutive time.

Given that average hourly earnings printed the strongest growth since the start of the year in March, inflation has been trending around the Bank of Canada’s midpoint price target (1-3.0%) and GDP growth picked up steam in May, an upbeat employment report would more likely increase optimism of higher interest rates in July. But with trade risks heating up on the horizon, policymakers, who meet next on July 11, will find it hard to decide whether it is time to reduce stimulus. There are fears that higher borrowing costs could harm consumption and business sentiment if US trade frictions hurt jobs in heavily indebted Canada. Last Friday, Canada, who is the top source of US steel imports, punched back with countermeasures after the US chose to activate its metal tariffs on Canadian, Mexican and EU products instead of postponing the exemption deadline beyond June 1. While this has already put NAFTA negotiations on life support, the US administration added a further challenge this week, proposing bilateral agreements to with Canada and Mexico, in a warning that a NAFTA deal is likely not going to happen ahead of the Mexican presidential elections on July 1 as well as the US mid-term elections on November 6.

Still, the loonie did not lose ground in the wake of the above news as sources stated at the same time that US Treasury Secretary, Steven Mnuchin, backed the option of exempting their Canadian counterparts from import tariffs while when communicating with the US president. The loonie hit higher instead, gaining additional speed after Wednesday’s Canadian trade stats showed a narrower trade deficit with the US, evidence that could deteriorate Trudeau’s position in Quebec, Canada, where the G7 meeting will take place on Friday. Despite the trade retaliatory game, the odds for a 25 bps rate hike by BoC in July (as indicated by overnight index swaps) also jumped on Wednesday, from around 61% to 70.37%, hinting that BoC policymakers will likely return to their hiking path next month as the last rate statement signaled. Recall that at May’s policy meeting, BoC, which has already raised rates three times since July, held rates unchanged at 1.25% but dropped the cautious wording for future potential rate rises.

Turning to Friday’s employment report, an upward surprise could add conviction that BoC will probably deliver higher borrowing costs in July, pushing dollar/loonie down to the 1.2900 round level, a previous resistance target. Below that, the 20-day simple moving average (SMA) standing currently at 1.2880 could provide support as well, while steeper declines could shift focus to the 50-day SMA at 1.2817.

On the other hand, disappointing prints could lift the pair up to the 1.3000 psychological level before the market touches Wednesday’s high of 1.3066. Then even higher, resistance could run towards the 1.3100 handle, with scope to retest the nine-month peak of 1.3124.

Euro Outlook Clouded by Politics, Easing Economic Momentum; Recent Rally a ‘Convenient’ Time to Sell?

Eurozone’s common currency finished 2017 on a strong note versus the US dollar, advancing by 14.1% to render itself the best performing major currency. Largely euro-friendly election outcomes and economic data pointing to an ever-improving growth outlook were instrumental for the euro’s strong performance. The current year, though, is presenting a shift in direction, with the euro possibly coming under pressure in the coming months.

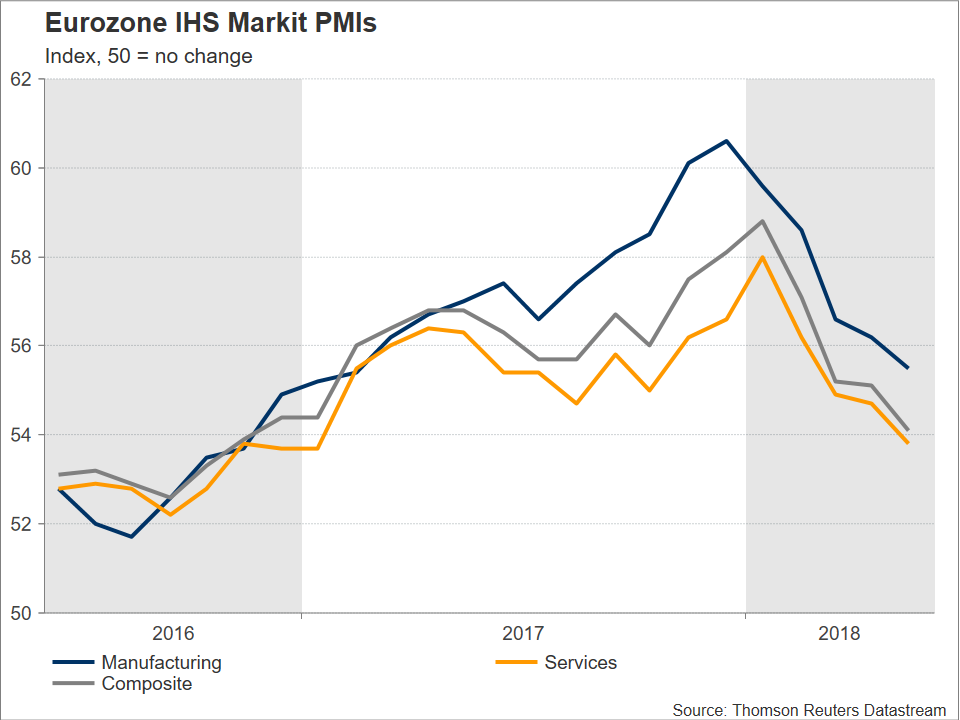

IHS Markit’s manufacturing PMI for the eurozone hit the highest on record in December last year, with the prints for the services sector, as well as the composite measure than blends manufacturing and services, coming in at more than decade highs in January. The eurozone economy seemed to be firing on all cylinders and the common currency was looking set for another year of outperformance against the greenback, having reached a zenith last experienced in late 2014 of 1.2555 around mid-February.

Fast forward to today: the eurozone’s PMI reading on manufacturing activity has recorded its fifth straight monthly decline in May, with the corresponding figures pertaining to services and the composite print both falling for the fourth consecutive month. Specifically, the composite PMI, which is viewed as a good overall growth indicator for eurozone economies, touched its lowest since November 2016 in May when it came in at 54.1. Not only that, but Markit also made reference to a eurozone outlook that has “darkened dramatically.”

Currency movements, however, are not determined in isolation but in relative terms. Still, despite weakening economic momentum, should the eurozone economy expand at a higher pace in 2018 compared to the US one, then this would be a factor contributing to a higher euro/dollar pair. This does not appear to be the case though, or at least data releases from recent months have not been supportive of a positive growth differential between the eurozone and the US. In particular, and in contrast to the euro area, the investor community seems to agree that the US economy has accelerated in the second quarter of the year, something which was also evidenced by May’s mostly upbeat employment report out of the US released in early June.

Politics are also clouding the euro area’s outlook. While the “Quitaly” story has tempered, allowing the euro to recover from a 10-month low of 1.1506 hit on May 29, uncertainties continue to persist, tilting the risk for euro/dollar to the downside. Italian public debt-to-GDP is second only to Greece’s in the currency union, and the new Italian government has very ambitious public spending plans. What if the anti-establishment parties ruling the country clash with the European Commission – which can reject Italy’s budget plans if it deems they deviate from EU-mandated fiscal targets – over those fiscal expansion plans? Such an outcome can bring back to the fore existential threats to the eurozone and more widely the EU, consequently hurting the common currency.

What is also interesting is that markets seem to not be pricing in such threats for the most part. Perhaps they’re extrapolating from Greece’s case, expecting that Italian politicians will eventually capitulate on their demands as their Greek counterparts have done in the past. Such extrapolation may be overly simplistic though: Italy is a much larger economy compared to Greece, specifically the eurozone’s third biggest economy, and thus carries much more leverage. To put it differently, unlike Greece, Italy is simply “too big to (be allowed to) fail”.

Also, what if the “trade war” narrative picks up steam in the aftermath of the Trump administration’s announcement it would not renew an exemption from tariffs on imports of aluminum and steel for the EU? Such a scenario, though reasonably expected to weigh on both the US and European economies, would prove much more detrimental for the latter given that the trade imbalance heavily favors the EU. Moreover, the US has opened the door for tariffs on imported European cars – an investigation is under way to determine whether the levy should be imposed – with the stock prices of German carmakers already feeling the burn from such a threat. Meanwhile, it should be kept in mind that the automotive industry is of far more importance than the steel or aluminum sectors for the eurozone economy.

On the monetary policy front, which is of course interlinked with the aforementioned, the outlook is also supportive of a weakening EURUSD. Surely, the latest developments with the European Central Bank finally putting on the table a discussion – during the meeting concluding on June 14 –on bringing its asset purchase programme to an end by the end of 2018 was a euro-positive, but the policy normalization path is at a much more advanced stage and appears much clearer in the case of the Federal Reserve; in other words, peak policy divergence in the favor of the US has probably yet to materialize. For the record, the US central bank, will be completing its own monetary policy meeting one day before the ECB’s respective gathering next week, and it is widely expected to deliver another 25bps interest rate increase. This would constitute the seventh such hike since the Fed started normalizing rates back in 2015.

Taking everything into account, if a projection were to be made for the next two-to-three months, then it would be one for a lower euro/dollar. That said, FX markets are volatile and unpredictable. Early in 2017, many analysts were forecasting a dollar that would flex its muscles throughout the year, even making reference to EURUSD at or near-parity levels by the end of the year. Not only did such views shy away from reality, but the greenback experienced its worst year since 2003 during the year that preceded. Year-to-date in 2018, euro/dollar is down by 1.4%.

Lastly, based on the abovementioned and taking into account the recent rally in EURUSD on the back of ECB-taper speculation, then opportunities may be present to short the pair aiming to take advantage of downside potential in the coming months. Having said that, the latest appreciation in the pair may first have some more room to run over the next couple of weeks though, especially if the ECB makes an announcement on an end-of-year halt of its QE programme as soon as next week.

Sunset Market Commentary

Markets:

Yesterday’s trends simply continued today amid a very thin eco calendar. Core bonds remain under pressure with Bunds underperforming US Treasuries as investors reposition into next week’s ECB meeting. Rumours and comments pulled forward bets on a first ECB rate hike from Q1 2020 to Q4 2019. We think that this positioning is still to dovish. German yields increased by 0.2 bps (2-yr) to 3.1 bps (10-yr). The German 10-yr regained the 0.46%/0.47% mark, entering a new range topped by 0.65%. The US yield curve marginally bear flattened with yields 1.1 bp (2-yr) to 0.8 bps (30-yr) higher. Peripheral yield spreads narrowed by up to 8 bps for Greece, Spain and Italy.

The single currency remains upwardly oriented, but the ECB-induced short squeeze in EUR/USD lost traction. The pair is currently testing the 1.1830 resistance area. Eco data included the details from Q1 EMU GDP and US weekly jobless claims. The former showed stronger than expected consumption (+0.5% Q/Q) while investments slightly disappointed (+0.5% Q/Q). Weekly jobless claims continue to hover near cyclical low levels (222k), confirming tightness on the US labour market. Neither influenced intraday dynamics.

EUR/GBP rose from the 0.8780 area towards 0.8840. After a week of bickering, the UK government published a long awaited note on the Irish backstop (proposal to avoid a hard border with temporary customs arrangement) in the Brexit negotiations. Any agreement should be “time limited” and new, final, arrangements should be in place by the end of 2021. The latter is a concession from May to hard brexiteers and probably why sterling is under some minor selling pressure. The note remains rather vague overall and merely suggests that the government is kicking the can down the road.

News Headlines:

“Czech interest rate should already be above 1% as the economy is feeling the effects of overheating”, central bank vice-governor Hampl said in an interview. Governor Rusnok earlier this week said that a weaker than expected CZK and building inflation pressure warrant sooner-than-forecast and additional rate hikes this year. The June 27 meeting is a likely candidate to hike the policy rate from 0.75% to 1%. CZK and EUR strength currently cancel each other out with EUR/CZK trading around 25.65.

Turkey joined a string of emerging-market central banks whose interest-rate decisions have surprised investors, tightening policy - for the third time in less than two months. They raised the one-week repo rate from 16.50% to 17.75%. The lira surged with EUR/TRY declining from 5.43 to 5.30.

Brazil’s central bank again increased its intervention in the currency markets as the real slumped towards the psychological 4.00 per dollar level. The central bank announced it would offer up to an additional 40,000 foreign exchange swap contracts Thursday. It normally auctions 15,000 contracts a day.

German industrial orders unexpectedly plunged due to weak demand from domestic and euro zone clients in April (-2.5% M/M vs 0.8% M/M consensus), posting their fourth straight drop on the month, as growing uncertainty about a global trade war led companies to scale back investment plans.

Japanese Yen Edges Higher, Final GDP Next

The Japanese yen has posted modest gains in the Thursday session. In the North American session, USD/JPY is trading at 109.99, down 0.17% on the day. On the release front, Japanese Leading Indicators improved to 105.6%, matching the forecast. In the U.S, unemployment claims ticked up to 222 thousand, just below the estimate of 223 thousand. Later in the day Japan releases Final GDP and Current Account. The markets are braced for Final GDP to decline 0.1 percent. This would mark the first decline in over two years and if GDP does point to contraction, traders should expect the yen to lose ground. Japan’s current account surplus is expected to widen to JPY 2.10 trillion. On Friday, Japan publishes Economy Watchers Sentiment and the G7 leaders will meet in Quebec.

Japan finds itself in the enviable position of being on the sidelines in a simmering trade dispute, after the US slapped tariffs on steel imports from between the European Union, Canada and other countries. However, Japan has plenty to lose if the tit-for-tat tariff battle escalates, which could snowball into a full-blown global trade war. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. The leaders of the G-7 are meeting on Friday in Quebec, and President Trump is likely to receive an earful about the tariffs from the six other members. The escalating trade battle is sure to dominate the summit, and if the leaders fail to resolve matters, it could spell bad news for the export-reliant Japanese economy, which has greatly benefited from a stronger global economy.

Japanese officials are keeping a close eye on the upcoming summit between US President Trump and North Korean President Kim Jong-un next week in Singapore. The meeting will mark the first ever face-to-face meeting between leaders of the U.S and North Korea. Trump has tried to lower expectations, saying the sides are unlikely to reach an agreement on North Korea relinquishing its nuclear weapons. Still, the fact that the two leaders are meeting is a sign that significant progress is being made in the long-standing dispute in the Korean peninsula. North Korean missiles represent a significant threat to Japan’s security, and Japanese Prime Minister Abe is expected to press Japan’s concerns when he meets with Trump ahead of the summit.

UK published document on temporary Brexit customs arrangements

The UK government released a document titled Technical note: temporary customs arrangement on Brexit today. That's is the so-called backstop plan to avoid a hard Irish border if the UK cannot come to an agreement with EU on the issue. Here is a summary for the key points.

It's in the document that "the UK expects the future arrangement to be in place by the end of December 2021 at the latest". In other words, the transition arrangement could last a year longer than previously planned. The current agreed 21-month transition period will start from March 29, 2019 and end on December 31, 2020.

During the period, UK will be outside the Common Commercial Policy. That is, "the UK able to negotiate, sign and ratify free trade agreements (FTAs) with rest of world partners and implement those elements that do not affect the functioning of the temporary customs arrangement."

The backstop solution will cover the whole of UK, not just North Ireland. And, there would be an ongoing role for European Court of Justice during the period. The document added that "if as part of the future partnership, parliament passes an identical law to an EU law, it may make sense for UK courts to look at the appropriate ECJ judgments."

Here is the full document.

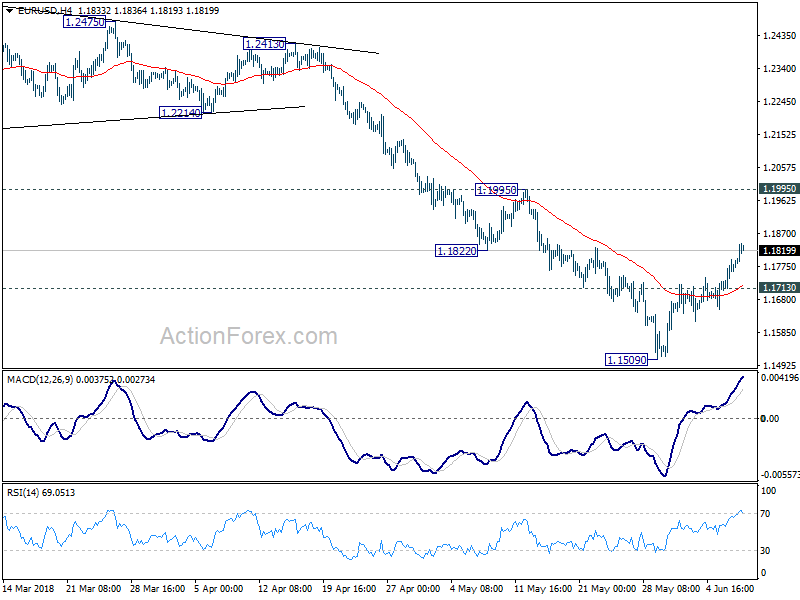

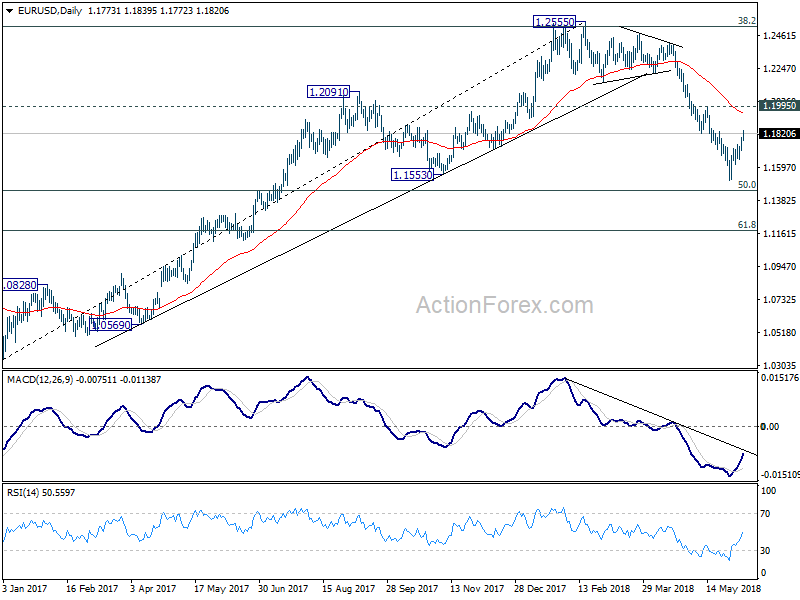

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1727; (P) 1.1761 (R1) 1.1811; More.....

EUR/USD's rebound from 1.1509 is still in progress and intraday bias remains mildly on the upside. Such rise is seen as a corrective move. And we'd expect upside to be limited by 1.1995 resistance to bring fall resumption eventually. On the downside, break of 1.1713 minor support will likely resume larger fall from 1.2555 through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

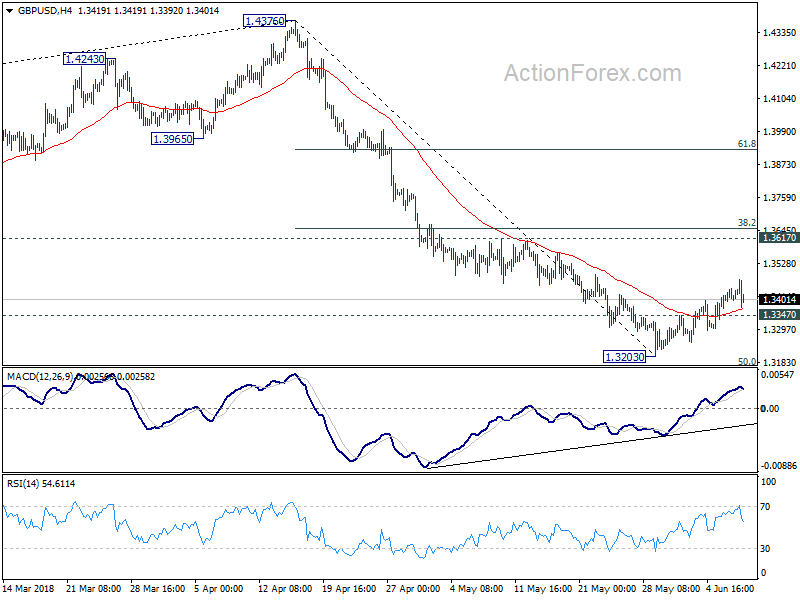

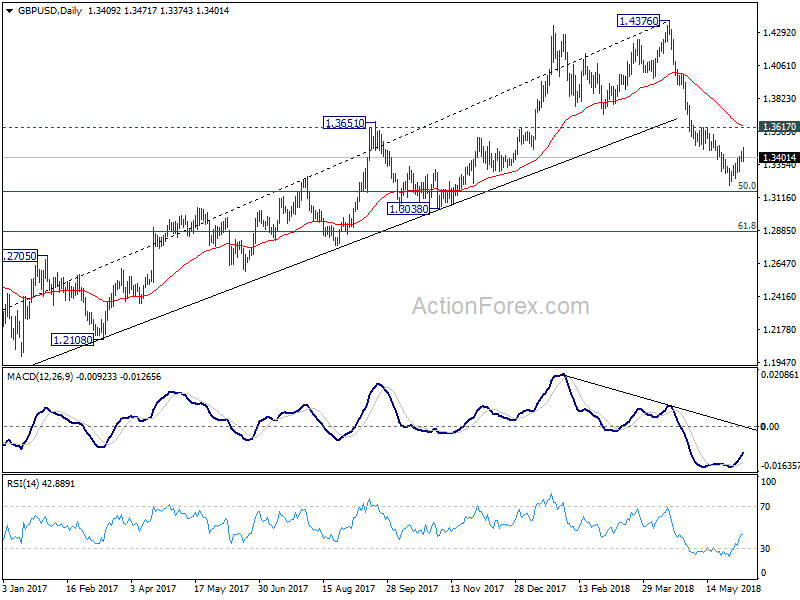

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3380; (P) 1.3412; (R1) 1.3446; More...

No change in GBP/USD's outlook. With 1.3347 minor support intact, rebound from 1.3203 could extend higher. But as it's a correction, upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3347 minor support will likely resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3648) holds, even in case of strong rebound.

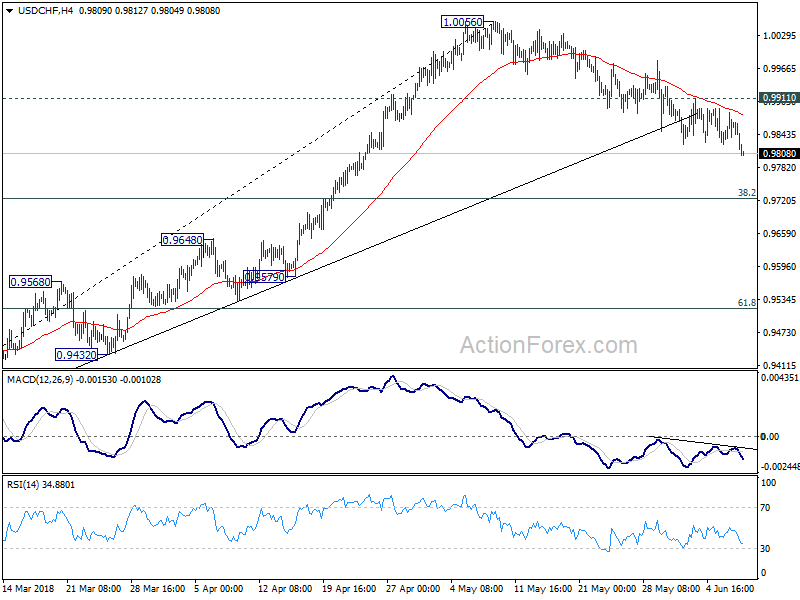

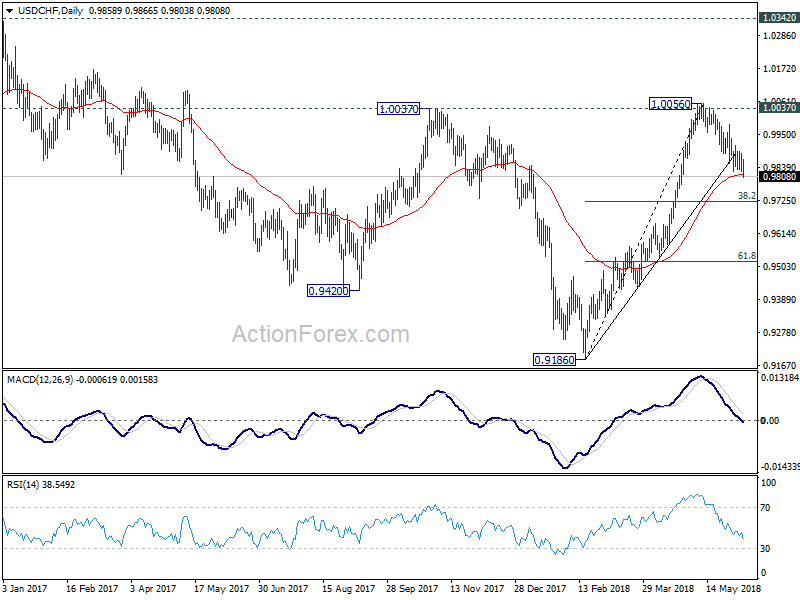

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9838; (P) 0.9863; (R1) 0.9890; More...

Intraday bias in USD/CHF remains on the downside at this point. Correction from 1.0056 is in progress and should target 0.9724 fibonacci level. On the upside, break of 0.9911 minor resistance is needed to indicate completion of the fall. Otherwise, near term outlook will remain mildly bearish in case of recovery.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

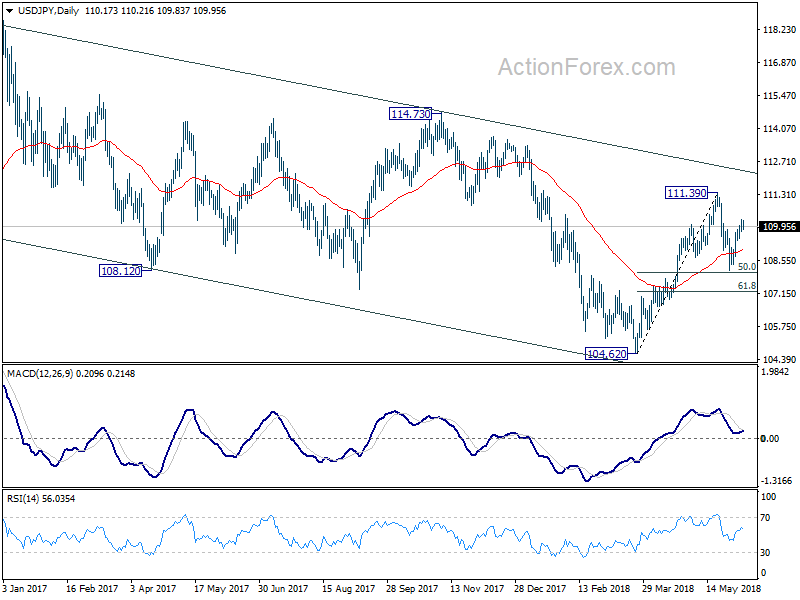

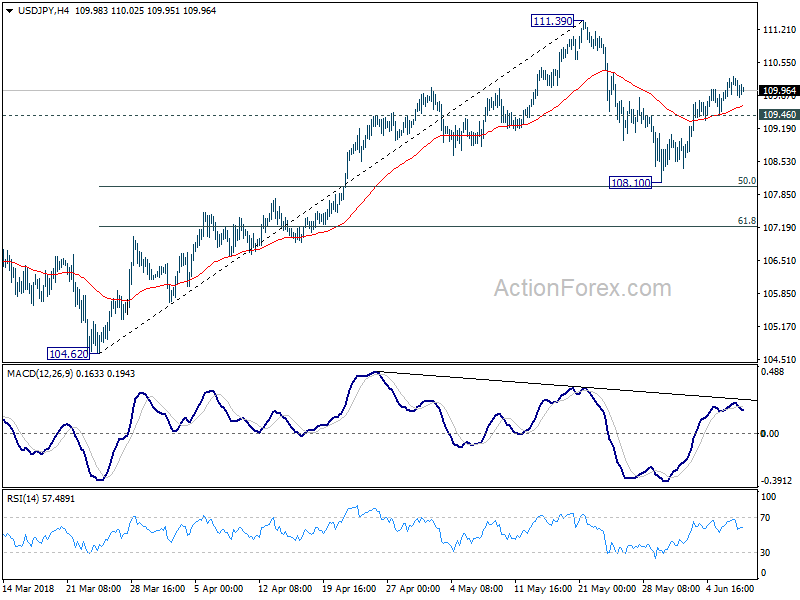

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.88; (P) 110.08; (R1) 110.38; More...

Upside momentum in USD/JPY remains unconvincing. But with 109.46 minor support intact, further rise is in favor. Rebound from 108.10 should extend to retest 111.39 resistance. Break will resume the rebound from 104.62 and target a test on 114.73 key resistance level. However, on the downside, below 109.36 minor support will delay the bullish case and turn bias to the downside for 108.10 support again.

In the bigger picture, at this point , we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.