Sample Category Title

UK May had constructive talks with Davis over backstop plan

UK Prime Minister Theresa May and her ministers will meet today to try to conclude on a "backstop" plan for Irish border after Brexit. The current proposal is believed to tie UK to EU customs union after a transition period.

But it's widely reported that Brexit minister David Davis is at odds with May over the the proposal because of the lack of end date. Davis also threatened to quit over the disagreement. May's spokeswoman said today that May and Davis had "constructive talks". And it's rumored that nobody will resign from the UK government today over Brexit.

Looking ahead, June 28-29 EU summit is an important deadline by which UK has to give an agreeable answer to EU regarding the Irish border. For now, it's highly unlikely for this to be met. Instead, the decision could be delayed to October 17-18 EU summit. But at the same time, October is the deadline for agreement the divorce bill and terms. So, tough time ahead for May for sure.

Dollar Softer Ahead Of G7 Summit

Thursday June 7: Five things the markets are talking about

G6 + 1

Despite global equities extending gains overnight on growing investor confidence in global growth, the markets attentions is turning towards the G7 conference that begins tomorrow in Quebec, Canada.

Expect this summit to be an intensive affair amidst heightened trade tensions between the U.S and some of its closest allies now that they indicated that they would retaliate against President’s Trump’s decision to impose duties on steel and aluminum imports from the E.U, Canada, and Mexico.

Nevertheless, risk continues to dominate proceedings for now. The EUR remains well supported, advancing for a fourth consecutive session amid talk of an end to the ECB quantitative easing program.

U.S Treasury yields are holding below the psychological barrier of +3%, and U.S. technology shares, drivers of previous rallies, notch up further records.

Elsewhere, crude oil has pared some of yesterday’s losses after U.S inventory reports reported a surprise increase in domestic crude stockpiles.

1. Global equities see the light

In Japan, the Nikkei share average rose to a two-week high overnight to stay above a key technical level as it tracked yesterday’s Wall Street gains. The Nikkei gained +0.8%, while the broader Topix advanced +0.6%.

Down-under, Aussie shares also edged higher overnight, led by material stocks and banks. But the gains were capped by Australia’s biggest wealth manager AMP closing at its worst level in more than nine years on the back of a fourth class action lawsuit. The S&P/ASX 200 index advanced +0.5%. In S. Korea, the Kospi edged +0.6% higher.

In Hong Kong, stocks have rallied on Thursday encouraged by signs of progress in the Sino-U.S. trade talks, easing fears of a trade war. The Hang Seng index rose +0.8%, while the China Enterprises Index gained +1.0%.

In China, stocks slipped as investors booked profits on consumer and healthcare firms after recent gains. The blue-chip CSI300 index closed -0.2% down, while the Shanghai Composite Index also lost -0.2%.

In Europe, regional bourses trade higher, following on from Wall Street’s lead yesterday. The FTSE has faded a tad after an earlier technical glitch meant a delayed opening.

U.S stocks are set to open in the ‘black’ (+0.1%).

Indices: Stoxx600 +0.3% at 388.0, FTSE flat at 7710, DAX +0.2% at 12860, CAC-40 +0.4% at 5481, IBEX-35 +0.9% at 9879, FTSE MIB +0.4% at 21890, SMI +0.5% at 8595, S&P 500 Futures +0.1%

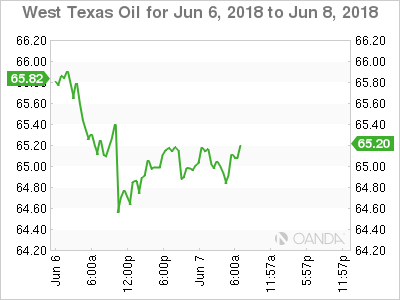

2. Oil prices rise on Venezuelan supply troubles, gold higher

Oil prices are a tad firmer on the back of plunging exports by OPEC-member Venezuela, although another surge in U.S production still caps advances.

Brent crude futures are up +51c, or +0.7%, to +$75.87 a barrel. U.S West Texas Intermediate (WTI) crude is up +30c, or +0.5%, at +$65.03 a barrel. It ended yesterday’s session -1.2% lower at +$64.73 a barrel.

OPEC member Venezuela continues to struggle to meet its supply obligations, with dozens of tankers waiting to take on its oil. The backlog is so severe that state-owned PDVSA has told some customers it may declare force majeure, allowing it to temporarily halt contracts, if they do not accept new delivery terms.

Note: OPEC and Russia are due to meet in Vienna on June 22 to discuss production policy. Iraq said on Wednesday that a production increase was not on the table as the market was stable and prices good.

Capping global prices is U.S production. EIA data this week showed that U.S production hit another record last week at +10.8m bpd. That’s a +28% gain in two years.

Note: Surging U.S production has helped widen WTI’s discount to Brent to more than +$10 per barrel.

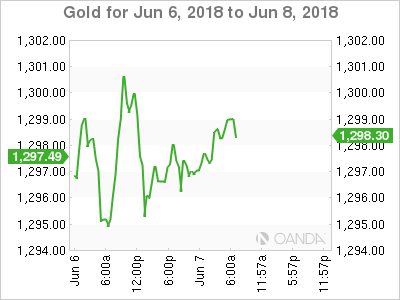

Ahead of the U.S open, gold prices have rallied a tad higher on the back of a weaker U.S dollar as the market seeks directional cues from this week-ends G7 summit and next weeks key central banks and the U.S/North Korea summit. Spot gold is up +0.1% at +$1,297.46 per ounce, while U.S gold futures for August delivery is unchanged at +$1,301.50 per ounce.

3. U.S Treasury prices follow Euro debt lower

U.S government bonds prices continue to weaken, but still trade below the psychological +3% handle, as a fresh wave of selling has hit European debt.

The yield on the U.S 10-year note is at +2.982%, compared with +2.917% earlier in the week.

This week, Euro yields have drifted higher, under pressure after comments from an ECB official on Wednesday, which the market has interpreted as being ‘hawkish.’

Investors should expect bond movement to pick up more next week as the U.S Treasury Department will be holding a series of auctions, including sales of 10- and 30-year debt, and the Fed will conclude its next monetary policy meeting.

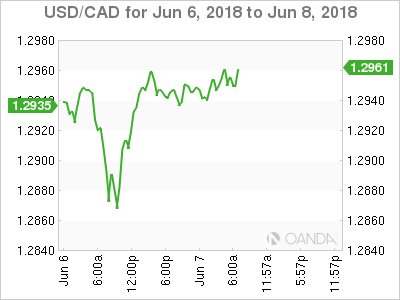

In Canada, yesterday’s strong April trade report is consistent with expectations that the BoC could move its key interest rate higher at its next policy announcement in July. Yesterday’s data showed that Canada’s exports rose to their highest level on record and imports fell, resulting in a smaller overall trade deficit than expected.

Note: The positive numbers come during a time of heightened trade uncertainty, after the U.S imposed tariffs on steel and aluminum from Canada and amid signs that Nafta talks have stalled.

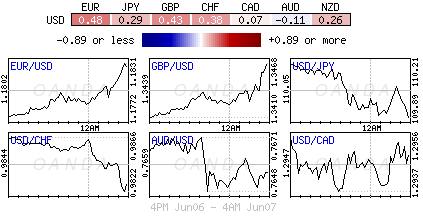

4. Dollar softer ahead of G7

The USD is a tad softer against the major pairs, with heightened trade tension ahead of tomorrow’s two-day G7 summit in Canada. Market consensus seems to believe that there is no chance that the U.S and other G7 members could reach common ground. Expect it to be an intensive affair.

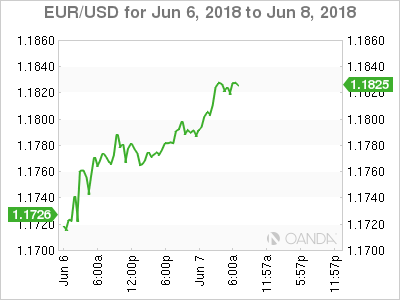

EUR/USD (€1.1821) continues to find traction to move higher as the market unwinds a number of ‘bearish’ ECB bets. The consensus believes that the ECB will likely discuss QE quantitative easing at next week’s meeting (June 14) and could hint when investors should expect its end.

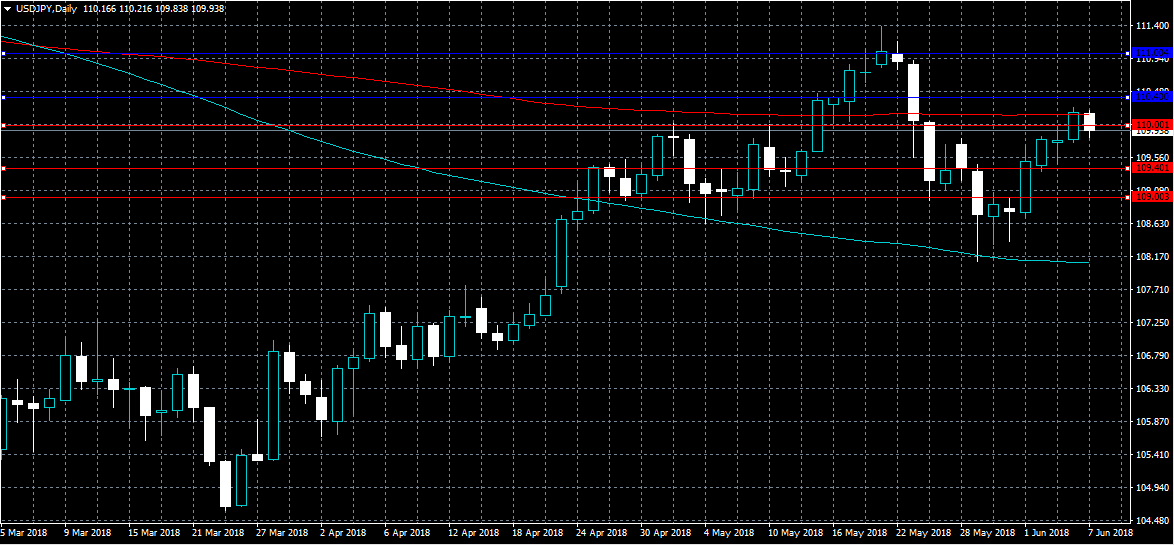

The USD/JPY (¥109.91) has moved back below the psychological ¥110 level with dealers citing some uncertainty on trade issues ahead of the G7 leader summit.

Note: Techies believe that the pair has failed to overcome its 200 DMA and the 61.8% retracement level of its previous decline and could pave the way for a test lower towards ¥108.

5. German industrial orders slump

Data this morning from Europe showed that German manufacturing orders dropped sharply in April, which suggests that their economic slowdown is stretching into Q2.

Demand for manufacturing goods fell for the fourth consecutive month, with total orders down -2.5% compared with March. The market was expecting a +0.6% gain.

Dipping data would suggest that rising trade tensions could be discouraging companies’ for new investments.

Note: Germany’s economy has started to cool, with the country’s annualized growth rate slowing to +1.2% in Q1 from +2.5% in the Q4, 2017.

Digging deeper, Germany’s Economic ministry noted that demand for aircraft, railway vehicles and vessels was particularly weak, as orders in this volatile category slumped -35.9% from the month before. Domestic orders for German manufacturing goods fell -4.8% m/m, while orders from the rest of the eurozone dropped almost -10%.

Demand from customers outside the eurozone remained strong, however, as orders increased +5.4% and that the order backlog was still “very high” in April y/y.

DAX Steady As Eurozone GDP Matches Expectations

The DAX has ticked higher in the Thursday session. Currently, the DAX is at 12,847, up 0.13% on the day. In economic news, German Factory Orders plunged 2.5%, missing the estimate of 0.7%. In the eurozone, Revised GDP dipped to 0.4%, matching the estimate.

The eurozone economy has been performing well and inflation continues to move higher, raising the question of what’s next for the ECB stimulus program. The ECB currently buys EUR 30 billion each month, and the scheme is scheduled to end in September. The bank has extended the program in the past, but stronger economic conditions have strengthened the case to finally end stimulus. The ECB has not formally discussed the issue, leaving the markets to hunt for any clues about the bank’s plans. On Wednesday, ECB chief economist Peter Praet said that the ECB would commence discussing the issue next week, when the Governing Council meets in Riga, Latvia. Many policymakers favor a gradual reduction in stimulus over several months, rather than completely turning off the tap in September. If the ECB makes any announcements regarding further tapering, we could see some volatility from European the stock markets.

Canada will host the leaders of the Group of 7, starting on Friday. These meetings usually do not make the headlines, but this meeting could be explosive, with plenty of bad will between six of the members and President Trump. The reason? The renewal of the tariff spat, courtesy of the U.S slapping aluminum and steel tariffs on the European Union and Canada. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. Will we see a higher profile, repeat performance at this meeting? Canada and Mexico have already announced retaliatory duties on U.S products. The escalating trade battle is sure to dominate the summit, and if the leaders fail to resolve matters, the result could be a nasty trade war between the U.S and its major trading partners.

Euro Rises To 3-Week High On Talk Of Stimulus Wind-Up

EUR/USD has posted gains in the Thursday session. Currently, the pair is trading at 1.1822, up 0.40% on the day. On the release front, German Factory Orders plunged 2.5%, missing the estimate of 0.7%. In the eurozone, Revised GDP dipped to 0.4%, matching the estimate. In the U.S, unemployment claims is expected to edge higher to 223 thousand.

After years of stimulus to boost the eurozone economy, ECB policymakers are focused on the question of whether it is time to wind up the bank’s bond purchase program. The ECB currently buys EUR 30 billion each month, and the scheme is scheduled to end in September. The bank has extended the program in the past, but stronger economic conditions have strengthened the case to finally end stimulus. The ECB has not formally discussed the issue, leaving the markets to hunt for any clues about the bank’s plans. On Wednesday, ECB chief economist Peter Praet said that the ECB would commence discussing the issue next week, when the Governing Council meets in Riga, Latvia. Many policymakers favor a gradual reduction in stimulus over several months, rather than completely turning off the tap in September. If the ECB makes any announcements regarding further tapering, we could see some strong movement from EUR/USD.

Meetings between G-7 leaders are often a chance to catch up with friends and hold a photo-op, but this year’s summit could be explosive, with plenty of bad will between six of the members and President Trump. The reason? The renewal of the tariff spat, courtesy of the U.S slapping aluminum and steel tariffs on the European Union and Canada. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. Will we see a higher profile, repeat performance at this meeting? Canada and Mexico have already announced retaliatory duties on U.S products. The escalating trade battle is sure to dominate the summit, and if the leaders fail to resolve matters, the result could be a nasty trade war between the U.S and its major trading partners.

Forex Analysis: EURCAD Wave Analysis

EURCAD broke resistance zone

Further gains are likely

EURCAD recently broke the resistance zone lying between the key resistance level 1.5200 (which has been reversing the price from the middle of May) and resistance trendline of the daily down channel from March.

The breakout this resistance accelerated the active medium-term impulse wave (1) – which is the part of the recently started upward impulse sequence ③ from the end of May.

EURCAD is expected to continue to rise and re-test the next strong resistance level 1.5450 (former support from April, which stopped the previous short-term correction (b)).

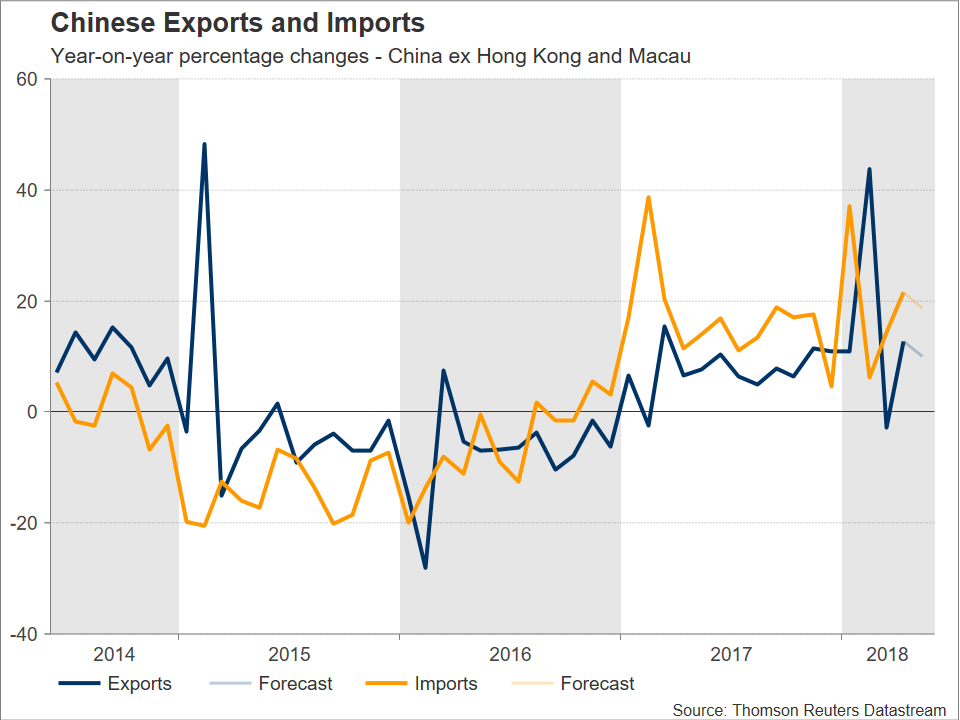

Chinese Trade Data Due Amid Trade Frictions, Inflation Data Also On The Horizon

Chinese trade numbers for the month of May are scheduled for release on Friday, with the figures perhaps attracting more interest in light of trade discussions between the US and China. Also of importance out of the world’s second largest economy, will be producer and consumer price inflation data due on Saturday.

Friday’s figures are anticipated to show both exports and imports growing solidly on an annual basis, albeit at a slower pace relative to the previously recorded month. Specifically, exports and imports are projected to rise by 10.0% and 18.7% y/y respectively in May, down from April’s corresponding readings of 12.7% and 21.5%. Meanwhile, the trade surplus (measured in USD) is forecast to expand to $31.90 billion, up from April’s $28.38bn. It should be kept in mind that the figures lack a specific time of release.

Despite economic momentum appearing to ease in certain economies – such as the euro area –, still global growth is anticipated to record a relatively robust year in 2018 according to analysts. Chinese exports are expected to benefit in such an environment; China is the world’s largest exporter. Posing risks to the outlook for Chinese exports, however, is the prospect of protectionist policies by the Trump administration, including the levy of tariffs on goods imported by China. In this respect, talks between China and the US have failed to provide a constructive outcome so far, with risks to global trade remaining in the background.

Regarding the outlook for imports, strong consumer spending, in conjunction with last week’s announcement that China plans to cut tariffs on approximately 1.5k consumer products, are supportive of higher prints moving forward. A factor that might negatively affect imports are government efforts to limit debt availability on the back of worries of a potential credit crisis; this though is expected to benefit the Chinese economy in the longer term.

For the record, US data released on Wednesday showed China’s bilateral trade surplus with the US standing at $28.0bn in April, having risen by 8.1% relative to March. However, the country’s (US) overall trade deficit fell to a seven-month low of $46.2bn, as exports touched a record high.

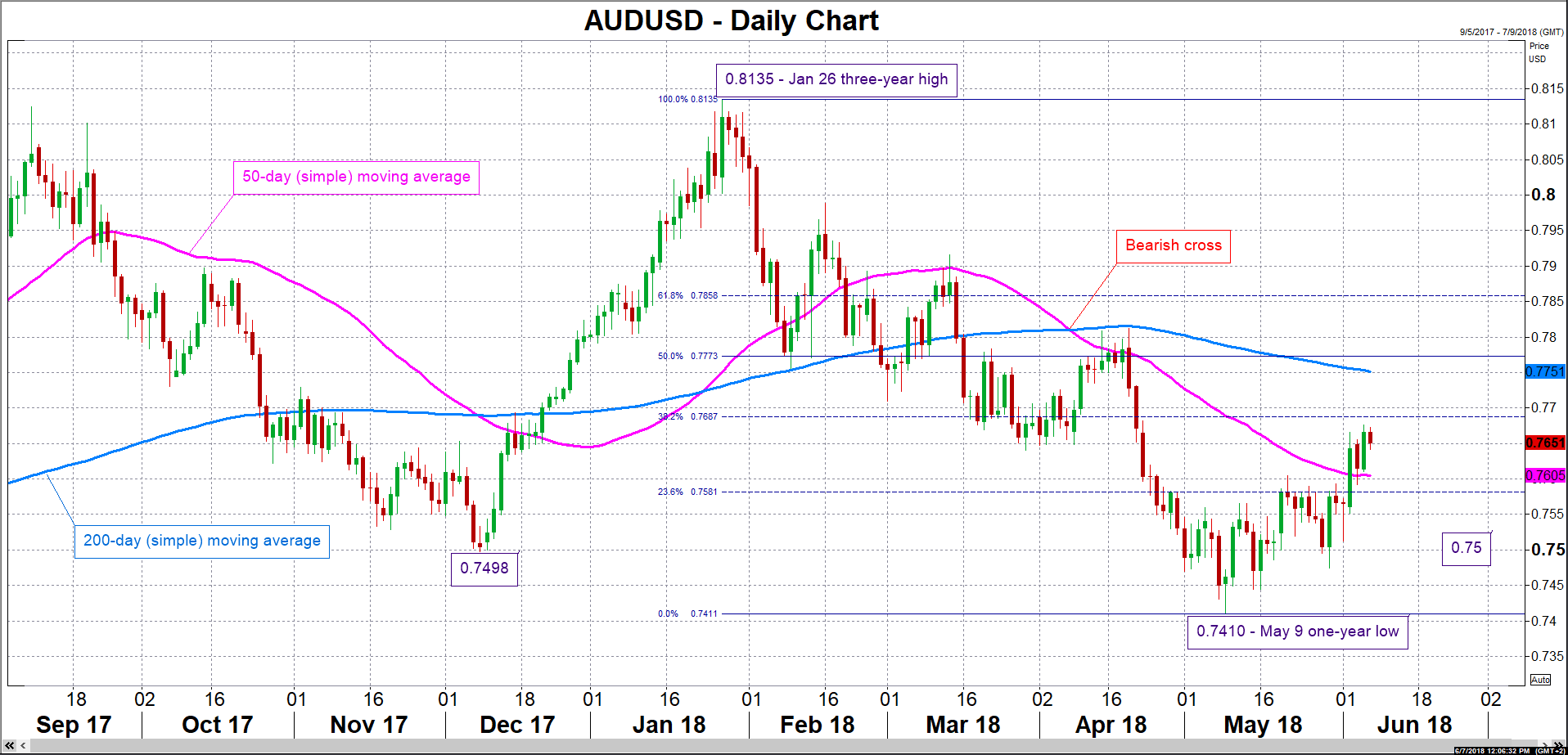

In the currency markets, Australia’s close economic ties with China have rendered the aussie dollar a liquid proxy for China’s economy. In this respect, besides the yuan, the Australian currency will also be closely watched as the trade data go public; a strong Chinese economy is seen as aussie-positive.

However, it could be argued that developments relating to trade negotiations between Beijing and Washington can much more profoundly affect the aussie, rather than Friday’s release. The rationale behind the aforementioned is that such developments can affect Australia’s economic outlook; barriers to trade are expected to act to the detriment of global growth, with the hit on the Australian economy being amplified given that it heavily relies on commodity exports. That said, the recent exchange of “tough talk” between the US and China did not weigh much on the aussie, with market participants seemingly getting used to the rhetoric. Conclusive punitive actions between the world’s two largest economies though, are most likely to result to positioning in the markets.

In terms of reaction in the FX markets and focusing on aussie/dollar, abating trade risks are likely to spur buying interest for the pair. Resistance to advances might come around the 38.2% Fibonacci retracement level of the January 26 to May 9 downleg at 0.7687. Notice that the area around this mark was relatively congested between mid-March and early-April, while it also includes the 0.77 round figure that may hold psychological significance. More bullish movement would turn the attention to the region around the 200-day moving average line at 0.7751. On the other hand, a fallout in US-China discussions that considerably raises the chances for a trade war is expected to exert selling pressure in AUDUSD. A first-line of support could take place around the 50-day MA at 0.7605, including the 0.76 handle. The 23.6% Fibonacci level lies not far below at 0.7581, while steeper losses would increasingly bring into focus the 0.75 handle, which may also hold psychological importance, for additional support.

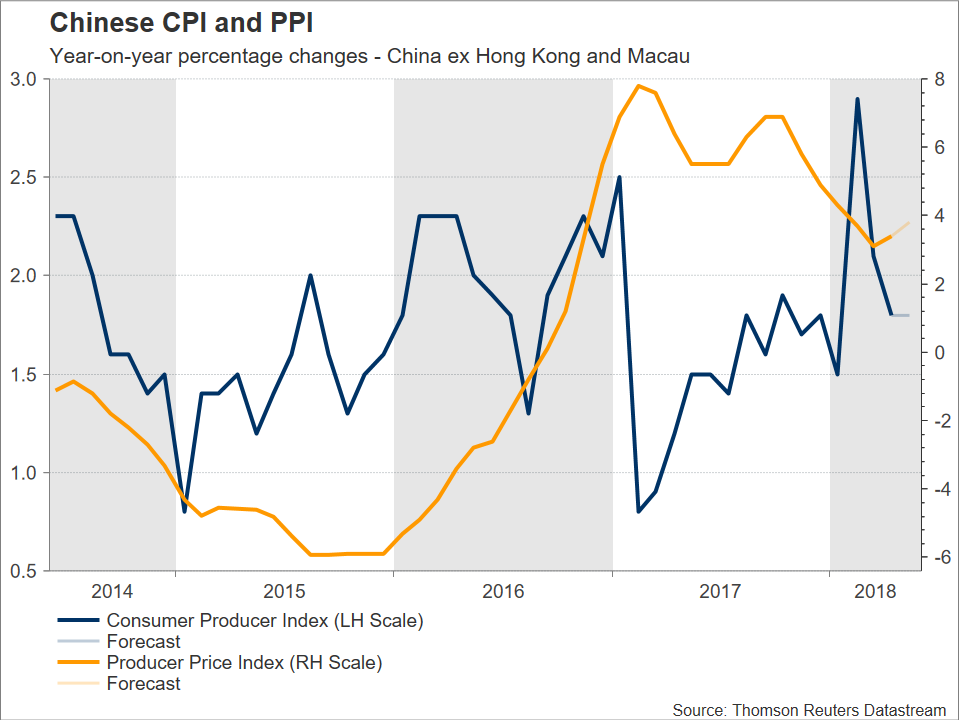

Other notable releases out of China during the current week are Saturday’s (0130 GMT) producer price index (PPI) and consumer price index (CPI), both for the month of May. Factory prices, as gauged by the PPI, are forecast to maintain positive momentum, expanding at a faster pace – 3.8% y/y – for the second straight month, after easing to 3.1% in March, the lowest reading since late 2016. This is encouraging news in an environment of increased efforts to curb pollution and limit lending by so-called “shadow” banking vehicles. In terms of CPI, it is anticipated to remain steady at 1.8% y/y in May.

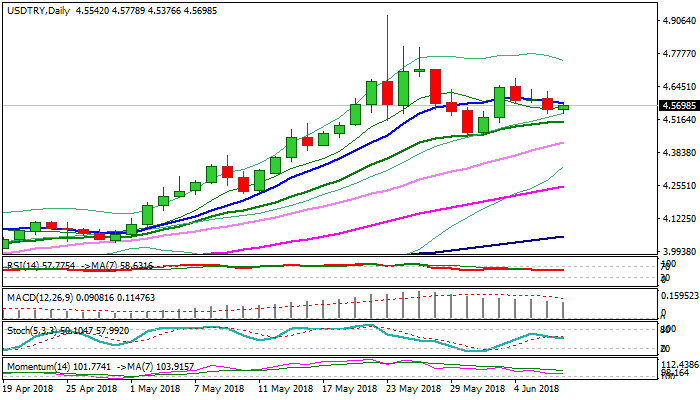

USDTRY Outlook: The CBRT Rate Decision Is The Key Event For Turkish Lira Today

The USDTRY holds in tight range on Thursday and awaiting key event today, the CBRT rate decision, due at 11:00 GMT.

The central bank is expected to hike rates in order to fight rising inflation, with expectations holding between 50 and 100bps increase, following 300bps hike in an unscheduled meeting last month.

From the economic point of view, further tightening is necessary, but the influence of politics cannot be ignored.

Turkish President Erdogan is looking to take more control over the central bank, in order to further support his low-rates policy, to boost the economy.

Should the CBRT stay on hold today this may raise a question overs its independence and send lira significantly lower.

Such scenario could bring in focus recent record high at 4.9273 and risk test of psychological 5.00 barrier, which was not until recently on forecast, with break higher to take lira again in the uncharted territory.

Fibonacci projections at 5.0406 (123.6%) and 5.1107 (138.2%) would be initial target, with stronger acceleration capable of travelling to Fibo 161.8% expansion at 5.2240.

If the central bank raises rates today, lira could strengthen further and extend above last month’s post rate hike high at 4.4473, towards 4.3724 (Fibo 61.8% of 4.0294/4.9273 upleg).

Res: 4.5782, 4.6280, 4.6782, 4.8020

Sup: 4.5087, 4.4783, 4.4473, 4.4240

USDJPY Intraday Bearish Below 110.00 Level

The US dollar has fallen below the key 110.00 level against the Japanese yen, as the greenback comes under heavy selling pressure. The USDJPY pair moved to a fresh monthly-high, hitting 110.26, before retreating below the pairs key 200-day moving average, at 110.16. Traders look towards the release of key US jobs data and the 93.00 support level on the US dollar index.

The USDJPY pair is intraday bearish below the 110.00 level, key support is found at the 109.40 and 109.00 levels.

Key intraday resistance for the USDJPY pair is currently located at the 110.26 and 110.40 levels.

EURUSD Buyers In Charge Above 1.1800 Level

The euro has moved above the key 1.1800 level against the US dollar, hitting 1.1836, during the European trading session as the greenback slumps lower across the board. The EURUSD pair currently trades close to session highs, as bullish momentum increases after yesterday’s break above the 1.1750 level. Traders now look towards the release of weekly jobs data from United States economy, and further EURUSD gains above the 1.1800 level.

The EURUSD pair is strongly bullish while trading above the 1.1800 level. Key resistance is now found at the 1.1836 and 1.1868 levels.

If the EURUSD pair falls below the 1.1800 level, sellers may test towards the 1.1750 and 1.1700 support levels.

ECB To Finally Unwind, Sparking Euro

Euro rallies as investors anticipate ECB to pull the trigger

The single currency extended gains on Thursday amid mounting expectations the ECB will start discuss quantitative tightening and broad weakness in the dollar. ECB governor Praet said they could start discuss QE unwinding at next week ECB meeting. The recovery in German yields accelerated yesterday with the 2-year and 10 year yields climbing 5bps to -0.6% and 10bps to 0.48%. Nevertheless, they are not back to their pre-Italian crisis levels yet, which suggests that investors have not dropped their guard.

After having broken the 1.1745 resistance yesterday, EUR/USD is currently testing the following resistance area that lies at 1.1835-1.19. A break out of this area would open the door towards 1.20. EUR/CHF consolidated at around 1.1615 as USD/CHF fell another 0.40% to 0.9825. Overall, we maintain our bearish USD view, especially against the single currency.