Sample Category Title

USD/JPY Remains In Uptrend Above 109.40

Key Highlights

- The US Dollar traded higher and moved above the 109.00 resistance against the Japanese Yen.

- There is a short-term ascending channel forming with support at 109.60 on the 4-hours chart of USD/JPY.

- Recently in the US, the Initial Jobless Claims for the week ending June 2, 2018 declined from the last revised from 223K to 222K.

- Today, Canada's net employment change for May 2018 will be released, which is forecasted to post 17.5K.

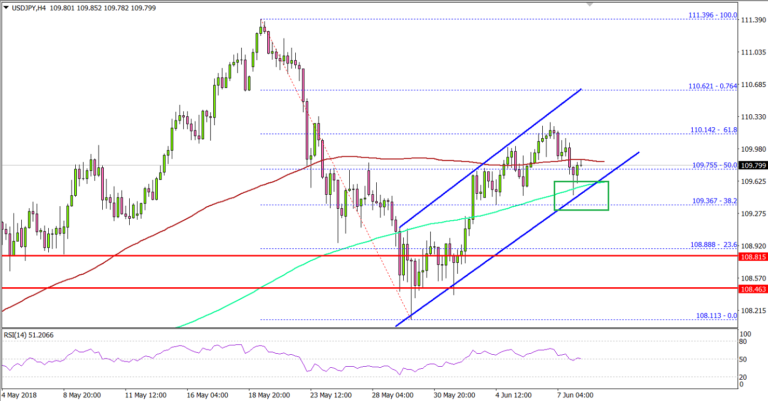

USDJPY Technical Analysis

The US Dollar started a decent upside move from the 108.50 level against the Japanese Yen. The USD/JPY pair is now placed nicely above the 109.00 level with bullish signs.

During the recent upside move, the pair broke the 108.80 resistance zone to start an upside move. It cleared the 109.20 barrier and the 200 simple moving average (green, 4-hours) to move into a bullish zone.

There was also a break above the 50% fib retracement level of the last decline from the 111.39 high to 108.11 low. The pair traded close to the 110.40 resistance and is currently following a short-term ascending channel with support at 109.80 on the 4-hours chart.

As long as the pair is above the 109.40 and 109.20 support levels, it may continue to rise in the near term. On the upside, an immediate resistance is at 110.40, followed by 110.80 and 111.00.

Recently in the US, the Initial Jobless Claims for the week ending June 2, 2018 was released by the US Department of Labor. The market was looking for a rise from the last reading of 221K to 225K.

However, the actual result was a bit positive as there was a decline from the last revised reading of 223K to 222K. The US Dollar is currently correcting lower, but upsides in EUR/USD and GBP/USD could be limited in the near term.

Economic Releases to Watch Today

- Germany's Industrial Production for April 2018 (MoM) – Forecast +0.3%, versus +1.0% previous.

- Germany's Trade Balance for April 2018 – Forecast €21B, versus €22B previous.

- Canada's net employment change May 2018 – Forecast 17.5K, versus -1.1K previous.

- Canada's Unemployment Rate May 2018 – Forecast 5.8%, versus 5.8% previous.

Let The Games Begin

Maximus Pressure or Circus Maximus

Both the S & P and Nasdaq fell overnight snapping the 5-day winning streak as the tech sector sags. But entering weeks end investors are taking another peek at the calendar and thinking that perhaps booking some profit is prudent in case politics gets messy over the next week or so.

There's a high level of circumspection associated with this weekend's G7 meeting as President Trump prepares to enter the G-7 lion's den. Usually, a non-event for markets but with all the focus on escalating trade tensions amongst long-standing G-7 allies, there's a good reason for investors to be chary as this meeting is unlikely to follow an orderly arrangement of discussion. Even more so as Canada and Mexico have retaliated against a range of U.S. exports and the EU has promised to do so as well.

Ultimatums and revelation around the upcoming Trump-Kim summit are spooking investors. The President reinforced his denuclearisation ultimatum to North Korea and is prepared to walk if 100 % compliance with his rigid demands is not agreed. My quants are busy entering the phrase ” maximum pressure” into the news reader algorithm as Trump promises to use these words if the meeting goes bad. Maximus Pressure or Circus Maximus, strap up as this could get bumpy.

Then there's that small matter of the European Central Bank and Federal Reserve Board meeting's which could be very crucial for the markets next tack.

The Fed is widely expected to announce an interest rate hike on Wednesday, but investors will be keying on forward guidance for clues if the U.S. central bank could raise rates a fourth time this year.

While Draghi's lieutenants rolled out a well-orchestrated PR campaign leaving the market convinced the ECB would discuss the removal of QE at next week's meeting. This news is hardly a watershed moment, but being so deprived of any hawkish ECB inference the markets will run take off running at any hawkish glean.

Oil Market

From a supply and demand perspective, oil markets are so finely tuned that any perceived supply disruption will send Oil prices surging higher.

Oil prices surged as concerns over declining Venezuelan production and exports escalated after a report was released that shipments were running a month behind. Also, suspicions regarding the disposition of OPEC-led producers to ease production limits at their upcoming June 22 summit also supported the rally. Iraq's oil minister Jabbar al-Luaibi told Reuters that an output increase isn't on the table at June's gathering in Vienna

Oil traders realise that price at the time of the Vienna meeting will have as much to do with OPEC supply rebalancing act as global supplies themselves. So, oil traders continue to respect this $ 64-65 per barrel support level.

While oil prices may have seen their near-term peaks, it's highly unlikely prices will collapse but rather OPEC, through gradual supply increases, will guide prices low enough so US consumers will not feel the pinch, yet remain high enough to benefit the industry going forward.

Gold Market

Gold prices have been very steady despite the lack of safe-haven demand. But the market is struggling to find a direction amidst a plethora of conflicting signals. While haven flows are tepid around 1,300 gold continues to remain bid on the dip as traders know we are little more than a spark away from igniting another risk aversion free for all. Also, the USD remains persona non- gratis as in the absence of the US tier one economic data, the USD is struggling to find a grip.

However, there are some significant events on the horizon none more so than the Trump-Kim summit which suggests trader's angst will be running high as we approach June 12 and should attract some attention from gold hedgers.

But in general, as with most cross-asset classes, we remain in a wait and see mode ahead of the US Federal Reserve Board(Fed) and European Central Bank policy announcements next week. But since no one is expecting a hawkish shift from the Fed, this too could prove to be a blessing for Gold bulls.

Currency Market

EUR: The markets have shifted ECB expectations and have pared back of EUR shorts, almost as if Italy never happened. But be cautious of Draghi's propensity to downplay QE reduction at the follow-up presser, which could prove to be a bitter pill to swallow going all in on the EUR at this stage of the game.

JPY: A bit of risk aversion playing into the equation as US 10-year yields collapsed to 2.88 % as some sizable bock order trades went through. The pair should continue to watch Bond yields and will likely be quite sensitive to next week's FOMC and ECB outcomes.

AUD: Jittery risk assets are leading to some underperformance on FX high beta like the Aussie dollar. But continue to like the Aud higher via the NZD near-term.

Asia Market

With so much focus on Brazil overnight, it's hard to know what to expect for EM Asia.

But Asia FX should be relatively isolated from these events

However, there's a ton market chatter this morning around @TheTerminal headlines suggesting that China Trade surplus my narrow about 10% in 2018 and the PBOC may respond by cutting the RRR despite expected Fed hikes

Malaysia

There are a lot of competing narratives, and we saw the Asian currencies trade with a weaker bias despite the higher EUR (weaker USD). That tells me that local currencies including the MYR are debating how more hawkish ECB comments could feed through to Asia FX. But the stronger EUR will not hurt sentiment in the same fashion as a stronger USD. But this hawkish shift from the ECB was a sudden shift, so you see EUR MYR risk adjustment and hedging vs the likely change in ECB policy

MYR: The problem for the Ringgit, despite the obvious fiscal uncertainties, continues to be the lack of action on the bond markets.

Gold Yawns As US Jobless Claims Within Expectations

Gold has inched higher in the Thursday session. In the North American session, the spot price for one ounce of gold is $1297.31, up 0.05% on the day. On the release front, U.S, unemployment claims ticked higher to 222 thousand, just below the estimate of 223 thousand. On Friday, G-7 leaders will gather in Quebec for their annual summit.

The upcoming G-7 meeting in Quebec is being closely monitored, as the summit comes at a time of escalating trade tensions between the U.S and some of its major trading partners. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. The trouble started last week, when the Trump administration slapped stiff tariffs on Canada, Mexico and the European Union. This resulted in promises of retaliation, and Canada and Mexico have already announced duties on U.S products. The trade spat is sure to dominate the summit, but will the leaders resolve matters? If not, investors could head for the hills and dump their riskier assets in favor of safe-haven gold.

Gold prices have been steady in June, as the base metal continues to hover close to the $1300 level. Recent geopolitical hotspots include Italy and North Korea, but both of these are calmer this week, boosting risk appetite. Italy has formed a government after months of political drama, and the on-again-off-again summit between Donald Trump and Kim Jong-un will indeed take place in Singapore next week. Although no agreements are expected to be signed at the summit, both leaders are unconventional and could surprise the world with a dramatic breakthrough in the longstanding Korean conflict. If this occurs, risk appetite could sore and send gold prices downwards.

USDJPY rebound completed as US yield reverses

US treasury yields had a wild session overnight. 10 year yield hit as high as 2.992 but closed sharply lower at 2.933, down -0.042.

There was no apparent major reason for the ride. Reasons cited include slump in emerging market currencies, fat finger trade as well as technical resistance at 3% handle.

Net effect in the forex market is also no too clear, except that USD/JPY is dragged down. Judging from 6H action bias chart, the rebound from 108.10 is likely over.

CBI expects BoE hikes in Q3 2018, Q1 2019 and Q4 2019

The Confederation of British Industry projects UK growth to lag well behind peers in 2018 and 2019. UK real GDP growth is forecast to be at 1.4% in 2018 and 1.3% in 2019 only. Eurozone growth is forecast to be at 2.2% in 2019 and 1.7% in 2019. US growth is forecast to be at 2.% in 2018 and 2.3% in 2019.

Though, UK would still be better than Japan at 1.1% growth in both 2018 and 2019. India is projected to stay strong with 7.3% growth in 2018 and 7.1% in 2019. China's growth is expected to slow notably to 6.3% in 2018 and 5.8% in 2019.

On monetary policy, CBI expects 25bps BoE hike in Q3 2018, Q1 2019 and Q4 2019. Inflation is projected to slow to 2.1% at the end of 2019.

CBI Chief Economist Rain Newton-Smith said that there is no disguising that UK is in "slow lane" for growth. And, "productivity weakness is a structural challenge for the UK economy and a drag on living standards." She also urged firms to work with the Government to "nurture a pro-enterprise environment to drive growth and create wealth." Also, "business and government must work together to drive competitiveness at home so firms can make the most of opportunities overseas" after Brexit.

Full release here.

French Macron: We don’t mind being six, if needs be

French President Emmanuel Macron urged to remain polite and productive in the G6+1 summit in Canada. But he also warned that "no leader is forever".

Macron added that "maybe the American president doesn't care about being isolated today, but we don't mind being six, if needs be."

And, "because these six represent values, represent an economic market, and more than anything, represent a real force at the international level today."

Trump blasts allies again, to escape from G6+1 summit early

The White House announced yesterday that Trump will leave the G6+1 summit in Canada earlier than anticipated, right after Saturday's morning session, on June 9. Then he will fly straight to Singapore for the highly anticipated Kim-Trump summit on June 12. G7 Sherpa and Deputy Assistant to the President for International Economic Affairs Everett Eissenstat will stay for the remaining session.

Ahead of the expected confrontation with other G7 members, Trump continued to blast Canada and EU with his tweets.

https://twitter.com/realDonaldTrump/status/1004909785547001856

https://twitter.com/realDonaldTrump/status/1004871827406061573

https://twitter.com/realDonaldTrump/status/1004846478253273088

Latest Bank of Canada FSR Paints Picture of Improving Vulnerabilities

The Bank of Canada released its latest Financial System Review (FSR) this morning – its biannual assessment of the risks facing Canada's financial system. The core message is that vulnerabilities remain, but have begun to ease as policy measures have improved the resilience of the financial system. The key vulnerabilities identified are high household indebtedness and housing market imbalances. Cyber risks also remain a concern.

On household indebtedness, healthy income gains, a marked slowing of credit growth, and improvements in credit quality have helped reduce this vulnerability. Also helping are higher interest rates and policy measures (notably the B-20 underwriting change). On the latter point, it remains too early to fully assess the extent of impacts, notably potential shifts to credit unions and private lenders. At the same time, credit growth may have slowed, but debt levels remain high. These high levels make existing debtholders more sensitive to rate increases.

There are also pockets of undiminished risk. In auto lending, the Bank notes that loans terms have become increasingly longer, and that one in three new car buyers owe more on their existing vehicle than it is worth at the time of trade-in, thus ballooning the size of the new loan. Similarly, although the mortgage underwriting standards seem to have reduced the growth of loans to highly-indebted borrowers, it remains too early to draw any firm conclusions. Moreover, although private lenders haven't meaningfully increased the pace of originations so far this year, the slowing in overall credit growth has pushed these lenders up to a roughly 8% market share in the GTA.

Related to high debt levels are imbalances in the Canadian housing market. Here, the Bank sees somewhat less positive developments, noting evidence of speculation in condo markets. Interesting analysis suggests that neighborhoods with a significant investor presence tended to see larger declines in home prices from 2016 to April 2018. This is consistent with the Bank's concern that price-gain-expectation fueled price increases are more sensitive to adverse shocks. With carrying costs reported to increasingly exceed rental revenue, the risk of a negative adjustment appears elevated.

Cyber threats remain a constant, with the interconnectedness of the financial system allowing such an event to potentially propagate beyond its source. The Bank continues to improve its defensive capabilities, and work with the major banks on recovery plans should a serious incident occur. Other risks discussed include the funding profiles of smaller banks (monolines), which rely on brokered deposits – the experience of Home Capital last year underscored the potential speed with which this funding can be withdrawn. For larger banks, the reliance of foreign funding (about 7% of assets) and risk of its withdrawal is a concern.

Risks need a trigger to metastasize into real economy impacts. Three are on offer: a severe recession, seen as 'Elevated but decreasing' in light of a strong labour market and a healthy economy more generally; A house price correction in overheated markets, a 'Moderate' risk given slowing home prices; and a sharp increase in long-term rates, seen as 'Moderate but increasing', given the global trend of monetary policy normalization.

Key Implications

This is by definition a report meant to raise eyebrows, and raise eyebrows it does. Things may be moving in the right direction, but the legacy of past developments will hang over the economy for some time to come. For instance, underwriting standards have undoubtedly improved in the wake of B-20 changes, but the few months of lending under this new regime have to be stacked up against the stock of debt already outstanding. Similarly, risks around auto loans and condo markets bear careful monitoring.

These risks must be considered against their economic backdrop. As it stands, the economy remains healthy, with the unemployment rate at a more than 40 year low and wage growth trending above the 3% mark. What's more, while housing continues its adjustment process, it is likely almost over, with underlying demand expected to stabilize activity around mid-year, albeit at diminished levels.

If there is a key trigger, it may somewhat counterintuitively be of too strong an out-turn, particularly in the United States. As noted in the FSR, longer-term Canadian rates are influenced by international factors. With the U.S. economy likely to deliver a robust performance this year and next, yields will rise and will impact borrowing costs here. We expect the Bank of Canada to monitor these developments closely, and this remains a key factor constraining the path of Canadian monetary tightening going forward. In many ways, the Federal Reserve will help do the Bank of Canada's job for it, and so the challenge for the Bank of Canada may thus be ensuring financial conditions here remain appropriate given the risks discussed – notably the elevated sensitivity of households to interest rates.

BoC Seeing Financial System Vulnerability Start to Ease, But Long Road Ahead

Highlights:

- On household indebtedness, the bank noted growing incomes, slower credit accumulation and improving credit quality have “begun to ease” the vulnerability associated with high household debt.

- On housing, the bank noted the vulnerability associated with housing market imbalances has “shown some signs of lessening” but continues to be elevated.

- Going forward, the FSR will be published once a year in June. Quarterly MPRs will feature more discussion of financial stability risks, and a new “financial system hub” on the BoC’s website will also provide more up-to-date information throughout the year.

Our Take:

Today’s Financial System Review showed a further evolution in the Bank of Canada’s concerns about the health of the financial system. Recall that last November’s FSR was the first in some time that didn’t note an increase in key vulnerabilities related to household debt and housing market imbalances. This time around, the bank noted signs of easing in those vulnerabilities. To be clear, they remain elevated and issues like high household debt will be with us for some time. But the BoC seems to see a turning point over the last year, where new regulations and rising interest rates are starting to improve the risk profile of borrowers and take some heat out of the housing market. As usual the bank is concerned with how these vulnerabilities might amplify the impact of an economic shock. The bank judges that key risks to the economy—from a severe recession, house price correction or sharp increase in interest rates—are little changed, on balance, since last November.

It’s always difficult to draw monetary policy implications from the FSR. We would go back to comments Governor Poloz has made in the past—that with the economy running at full capacity, higher interest rates will help meet the bank’s inflation target while at the same time addressing financial system vulnerabilities. High household debt means they will have to be gradual in raising rates, but the tradeoff between macroeconomic and financial stability risks points to less accommodation being needed. We continue to expect the BoC will raise rates again at their next meeting in July.

Eco Data 6/8/18

[php_everywhere instance="1"]