Sample Category Title

Euro Recovery Refueled By ECB Speculation, Trade Developments Continue To Dominate Attention

Here are the latest developments in global markets:

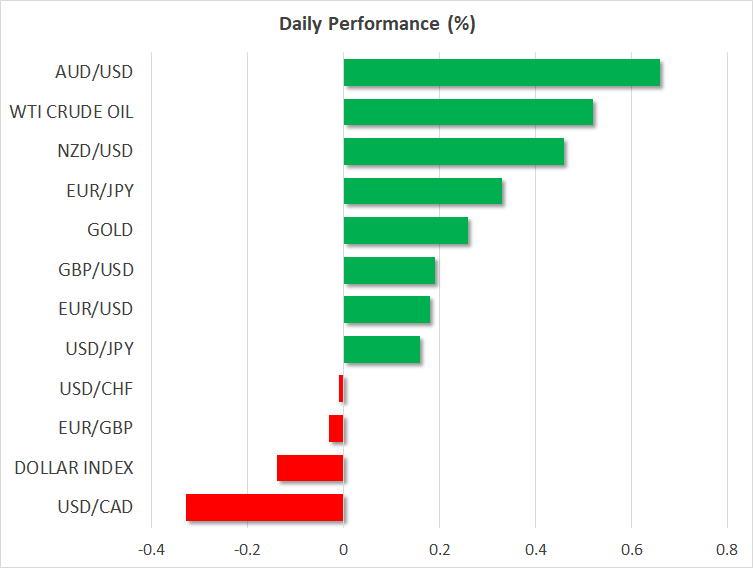

FOREX: The US dollar index is trading 0.1% lower on Wednesday, looking set to post its third consecutive day of declines. The euro continued to recover amid speculation around an ECB QE announcement coming sooner rather than later, while the Canadian dollar went for a ride following mixed signals on NAFTA.

STOCKS: Major US indices closed mixed yesterday, with the tech-heavy Nasdaq Composite and the S&P 500 climbing by 0.41% and 0.07% respectively, but the Dow Jones edging lower by 0.06%. Risk sentiment looks to have improved notably though, with futures tracking the Dow, S&P, and Nasdaq 100 all currently flashing green, pointing to a higher open today. In Asia, Japan’s Nikkei 225 and the Topix rose by 0.38% and 0.15% correspondingly, while in Hong Kong, the Hang Seng was up by 0.66%. In Europe, futures tracking all the major indices were a sea of green, suggesting these benchmarks may open with gaps to the upside today.

COMMODITIES: Oil prices rose on Wednesday, building on some gains from yesterday. WTI is up by 0.5% while Brent is trading 0.8% higher, buoyed by fresh Reuters reports suggesting that Venezuela’s main oil producing company may soon be unable to service prior contracts it had with buyers. The report seemed to overshadow other news that the US may formally ask Saudi Arabia and other major producers to raise their output to offset supply outages from Iran and elsewhere. In precious metals, gold is up by almost 0.3% today, currently trading a couple of dollars below the $1,300/ounce level. The yellow metal continues to trade in a very narrow range after having been rejected from its 200-day moving average multiple times recently, which keeps the technical picture cautiously negative.

Major movers: ECB speculation lifts the euro; loonie & peso hit by NAFTA uncertainties

The common European currency got a helpful hand yesterday from a Bloomberg report which suggested the ECB could announce an end-date to its QE program as soon as at next week’s policy meeting, citing sources familiar with the matter. This probably came as a surprise for most investors, considering that the streak of soft economic data and the Eurozone’s recent political woes were widely expected to keep the ECB sidelined at least until July before making a decision on QE. Euro/dollar surged to break back above 1.1700 on the news, and is also trading 0.2% higher today.

While the euro could perhaps continue to recover in the coming days as markets digest these signals and price in a potential QE-announcement by next week, one must sound a note of caution, as an actual decision still seems unlikely to be taken so early. At its latest gathering, the Bank signaled it will maintain a cautious approach while it monitors whether the recent bout of economic weakness was transitory or more persistent. If anything, data since then have continued to paint a picture of a slowing economy, so the ECB has little motivation to take the next step towards the QE-exit door, for the moment.

Elsewhere, pound/dollar is 0.2% higher today, extending its gains from yesterday after the UK services PMI for May rose by more than expected, reigniting hopes that the economy’s recent soft patch may have indeed been transitory, as the BoE believes. That said, markets remain hesitant to price in a greater likelihood for a rate hike as soon as August, with the probability for such action remaining stuck around 45% according to the UK OIS.

On the trade front, the Canadian dollar and the Mexican peso stumbled on Tuesday, after White House economic advisor Larry Kudlow suggested the US is considering holding separate negotiations with Canada and Mexico. Dollar/loonie touched a fresh two-month high of 1.3065, before it retreated to erase all its gains a few hours later as the US dollar lost some ground, and following a report that Treasury Secretary Mnuchin urged Trump to exempt Canada from the recent metal tariffs.

In the antipodeans, aussie/dollar rose by 0.65% today, briefly touching a six-week high of 0.7610 after Australia’s GDP data for Q1 beat expectations. Kiwi/dollar is nearly 0.5% higher as well.

Day ahead: Trade data and related developments closely watched

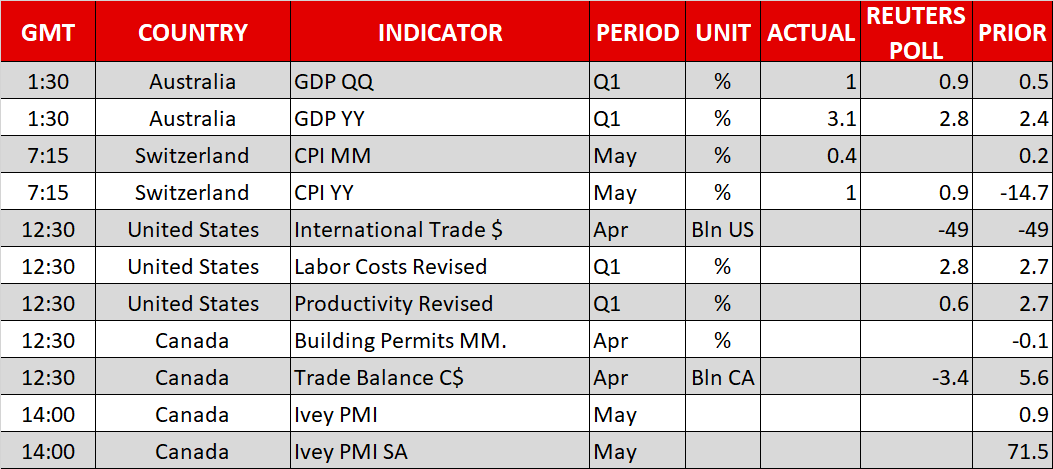

Wednesday is going to be a relatively quiet day in terms of data releases, though some trade data out of the US and Canada are likely to attract attention, especially in light of trade frictions and a G7 summit commencing on Friday in Quebec, where trade is likely to rank high on the agenda.

At 1230 GMT, trade figures will be made public out of the US, with the trade deficit expected to have remained at $49 billion in April, after a sharp decrease in March attributed to record high exports. The politically-sensitive bilateral deficit with China will also be attracting attention. In the big picture, these numbers do not constitute a typical market mover in FX markets, though the latest developments on the trade front are rendering them of more interest. First-quarter data on labor costs and productivity will also be released out of the world’s largest economy at the same time.

Again at 1230 GMT, Canada will be on the receiving end of trade numbers for April as well; the nation’s trade deficit is projected to shrink to C$3.4bn from March’s deficit of around C$4.1bn. Canadian building permits are slated for release at the same time, while later in the day (1400 GMT), May’s Ivey PMI is also due out of the country.

The Canadian dollar and Mexican peso took a hit yesterday on the back of worries that the US will pull out of NAFTA. In this respect, White House economic adviser Larry Kudlow said that President Trump is considering bilateral talks/deals with the two countries, a move away from the trilateral NAFTA deal. Developments will be closely watched. Meanwhile, also of interest are reports earlier on Wednesday that US Treasury Secretary Steven Mnuchin has been urging President Trump to exempt Canada from tariffs – this has offered some relief to the loonie.

Remaining within trade, sources are suggesting that China is offering to boost its purchases of US goods by $25bn, with the US’ “goodwill” being reflected by its actions to help China’s ZTE Corp. effectively get back to business. These are positive news in the sense that they deviate from the confrontational stance from previous days.

In European politics, while uncertainty has eased considerably in Italy, anxiety over the new government remains and this is also reflected in bond markets. Will the anti-establishment forces ruling the country play by the “rules of the game”, something which is anticipated to be perceived as euro-friendly by markets, or will they attempt to shake things up?

In energy markets, the EIA weekly report on crude oil inventories due at 1430 GMT might offer some short-term direction to oil prices. Crude stocks are projected to have declined by 1.8 million barrels during the week ending June 1, after falling by around 3.6m in the previously tracked week.

In equities, Netflix may attract additional interest ahead of today’s shareholders’ meeting.

ECB members of the Supervisory Board Pentti Hakkarainen and Ignazio Angeloni are scheduled to be making appearances today at 1330 GMT and 1710 GMT respectively; the topic of discussion in the case of the former though is such that it is unlikely to yield any market sensitive comments. Meanwhile, Bank of England MPC member Ian McCafferty will be taking part in a Q&A session with listeners of LBC radio.

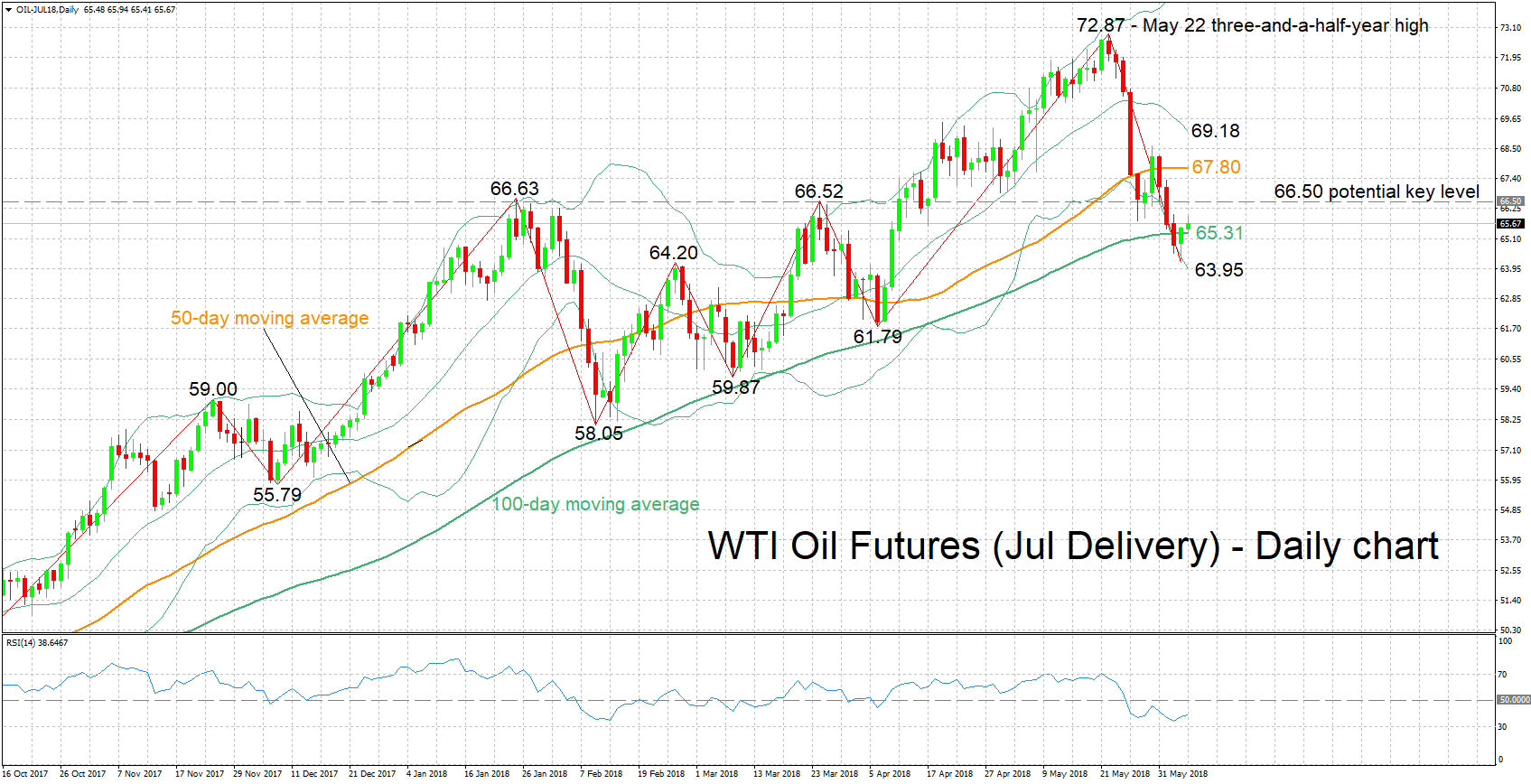

Technical Analysis: WTI oil futures bearish momentum weakens after 2-month low

WTI oil futures for July delivery have declined considerably after posting a three-and-a-half-year high of 72.87 on May 22. On Tuesday, they recorded a two-month low of 64.20. The RSI remains in bearish territory below 50, though it has halted its decline; a change in momentum might take place.

Should today’s EIA report show a larger-than-anticipated drawdown in crude inventories, then prices could move higher. Resistance to advances may come from the area around 66.50, which encapsulates a couple of peaks from previous months. An upside break might meet an additional barrier around the current level of the 50-day moving average line at 67.80.

On the downside, immediate support could be taking place around d the 100-day MA at 65.31. In case of a smaller-than-expected drawdown in crude stocks (or a buildup) that pushes prices further down, additional support might be provided around the lower Bollinger band at 63.95; the region around this includes the 64 round figure, as well as yesterday’s two-month low of 64.20.

Of course, any updates on OPEC/non-OPEC supply issues also have the capacity to move prices.

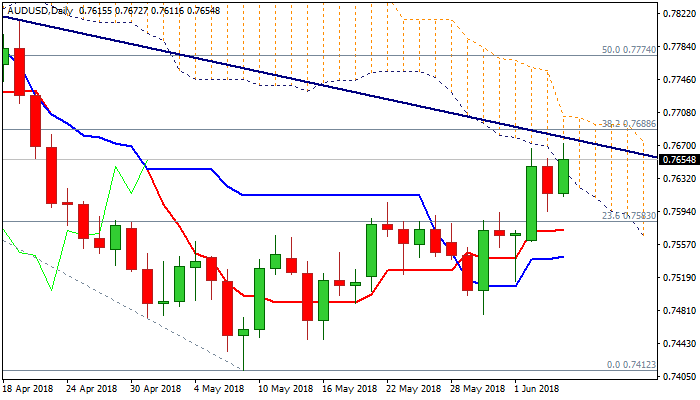

AUDUSD Outlook: Rose After Upbeat GDP Data And Pressures Key Barriers At 0.7675/88

The Aussie dollar accelerated higher in early Wednesday’s trading and hit 1 ½ month high at 0.7672, boosted by better than expected Australian GDP, which rose 1% in Q1, beating the forecast at 0.8%.

Annualized figure came at 3.1% vs expected 2.8%.

Fresh strength fully retraced Tuesday’s dip and generated bullish signal on penetration of falling daily cloud (cloud base lays at 0.7642) and probe above 0.7660 (Fibo 61.8% of 0.7812/0.7412 descend). Bulls pressure next pivotal barriers at 0.7675 (bear-trendline drawn off 0.7988, 6 Feb high) and 0.7688 (Fibo 38.2% of 2018 0.8135 / 0.7412 fall), break of which confirm strong bullish signal for continuation of recovery leg from 0.7412 low.

Bullish setup of daily MA’s which created bull-crosses (5/10, 20/30SMA’s) and north-heading momentum support scenario. Broken 55 SMA (0.7612) holds today’s action and marks solid support (reinforced by rising 5SMA in attempt to form bull-cross) which should keep the downside protected.

Res: 0.7660, 0.7672, 0.7688, 0.7703

Sup: 0.7639, 0.7612, 0.7594, 0.7579

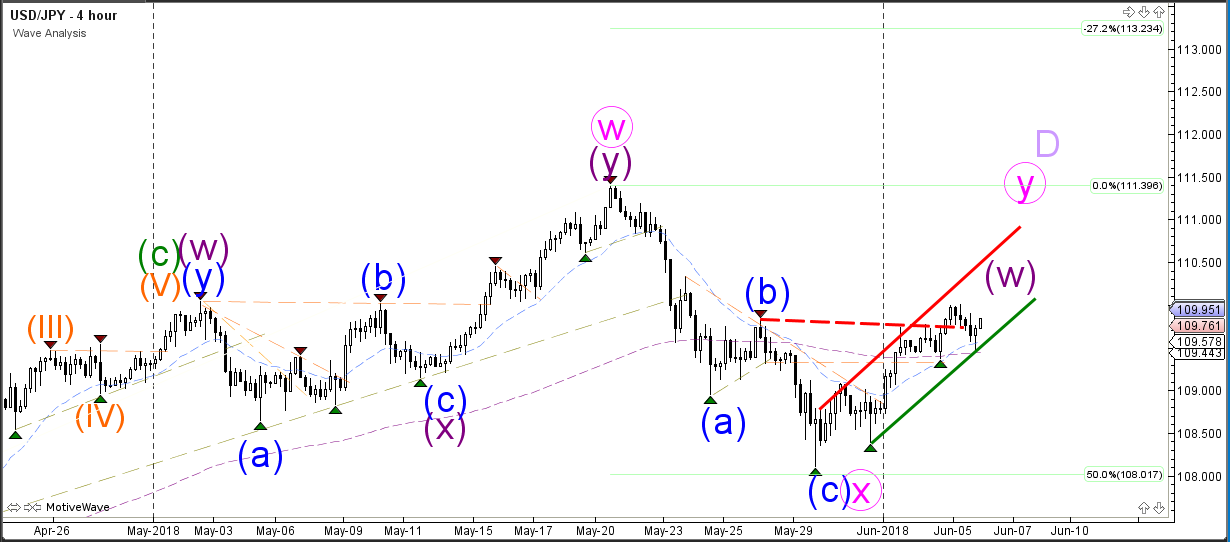

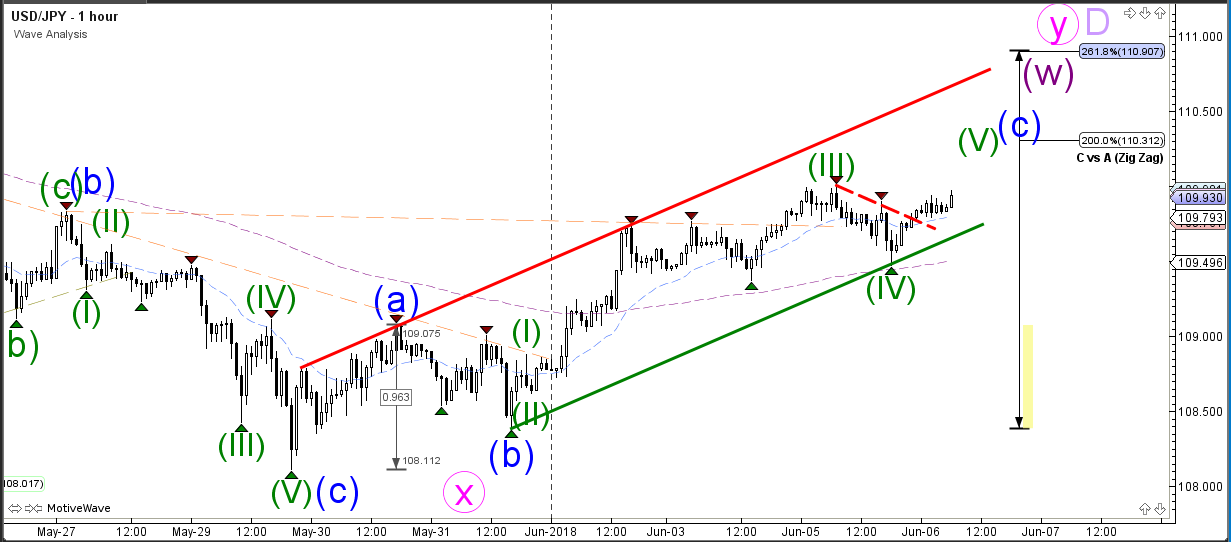

USD/JPY Breaks Bull Flag Pattern And Challenges 110 Again

The USD/JPY failed to break above the 110 round resistance level but price is now approaching the key zone again. The bullish bounce in the channel keeps the uptrend channel intact. The bullish price action is probably part of a larger WXY (purple) correction within wave Y (pink).

The USD/JPY broke above the resistance trend line (dotted red) of the bull flag continuation chart pattern after bouncing at the support trend line which was probably a wave 4 (green) correction. The current bullish momentum could be a wave 5 (green) of wave C (blue) and aiming at the Fibonacci targets of wave C (blue). The wave C could also be a wave 3 if the bullish momentum is strong.

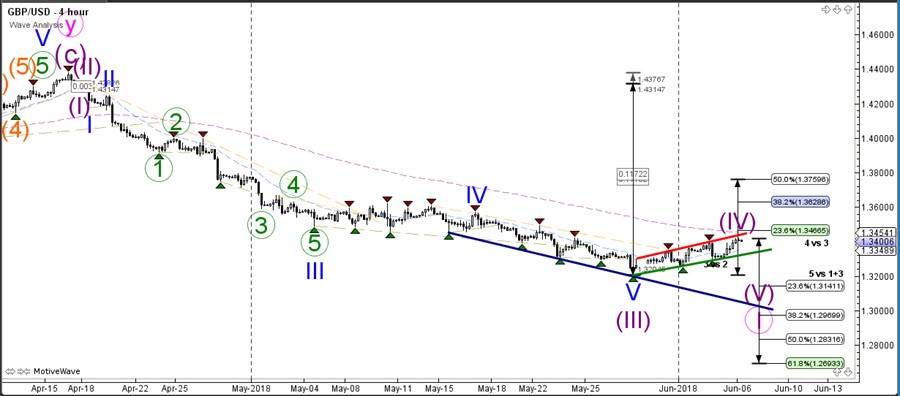

GBP/USD Bullish Bounce Approaches 23.6% Fib At 1.3465

The GBP/USD bounced at the support trend line (green) and is expanding the bear flag chart pattern. Price could challenge the 23.6% Fibonacci level of wave 4 around 1.3450-1.35.

The GBP/USD seems ready to test the Fibonacci levels of wave 4 vs 3 which could act as resistance spots. A bearish break below the bear flag chart pattern could indicate the start of wave 5 (purple).

The GBP/USD broke above yesterday’s 50% Fib at 1.3340 which indeed created bullish price action. Price is now in a wave C (green) but needs to break above the trend line to make the last push towards the Fib levels. A bearish turn could still find support at around 1.3350.

EUR/USD Bullish ABC Pattern Aims At 1.1850 And 38.2% Fib

The EUR/USD bounced at support and expanded the wave 4 pattern. Price is now testing the resistance zone (red) again and a bullish break could see EUR/USD move towards the 38.2% Fibonacci resistance level at 1.1850.

The EUR/USD is moving sideways at the moment but eventually price is expected to complete wave 4 at the Fibonacci resistance levels (50% Fib or lower) and break below the correction for one more bearish wave 5.

The EUR/USD is probably building a bullish ABC (blue) pattern within wave Y (purple). The EUR/USD could bounce at resistance (red) and support (blue) before making a breakout

Eurozone Inflation Rises Raising Prospects Of ECB Exit From QE In September 2018

Consumer prices in the Eurozone showed a sharp increase in the month of May led by higher energy costs and helped to soothe nerves as ECB officials battle the recent slump in inflation and the market turbulence from the geo-politics in the region.

The data comes as the European Central bank prepares to exit from its quantitative easing program which is all set to end on September 2018.

According to data from the statistics agency, Eurostat, inflation in the 19 country block sharing the euro currency increased 1.9% in May. This marks a strong gain in consumer prices from 1.2% that was registered in April. The data was also above expectations which called for a 1.6% increase.

Excluding the volatile energy and food prices, consumer prices also gained 1.3%. Core CPI was registered at 1.1% in April and managed to rise sharply. Other measure of core inflation which excludes alcohol and tobacco showed a 1.1% jump in May, up from 0.7% previously.

The ECB had been targeting a 2.0% inflation rate. Consumer prices had earlier firmed but soon started to ease back. However, the flash estimates show that the higher oil prices were feeding in to reflect the jump in consumer prices.

The latest inflation data showed that headline CPI was ever closer to the ECB's inflation target rate. Still, with the ECB noting on various occasions that it would be focusing on the core CPI, there is still a lot more for the ECB to mull over.

Other components of the harmonized index of consumer prices also logged strong gains. The cost of food, alcohol and tobacco rose 2.6% extending the gains from 2.4% previously.

Energy prices posted a strong jump, rising from 2.6% in April to 6.1% in May. Elsewhere, other regional inflation reports showed that Germany's consumer prices rose 2.2% in May while French inflation increased 2.3%, up from 1.8% in April.

Consumer prices in Spain also increased, rising 2.1% compared to 1.1% that was registered in April. It was only Italy, where consumer prices remained below the 2% target. Italy's consumer prices increased 1.1% in May, up from 0.6% in April.

Other news over the week included the Eurozone unemployment rate. Data showed that unemployment rate in the Eurozone fell to 8.5% from 8.6% in April. This was the lowest unemployment rate since December 2008.

The positive data did not yield much results in the currency markets as the euro continued to remain subdued. This came amid the ongoing political drama from Italy. The markets opened to a nervous week after Italian President dismissed the coalition government formed by the 5-Star Party and the League.

However, nerves were calmed after a compromise was reached and thus fresh elections were avoided.

Still, other political concerns remain. Several high ranking officials in Spain are being investigated on charges of corruption which is expected to embolden the anti-establishment parties in Spain as well.

The above factors, alongside a stronger U.S. dollar put the euro currency on the back foot. Last week, data from the United States showed that the core PCE price index, which is the Fed’s preferred gauge of inflation was at 2.0% for the second consecutive month.

The Fed had previously signaled its willingness to tolerate an overshoot of inflation for a short while. Following the recent FOMC meeting minutes, investors have priced in another 25 basis point rate hike from Fed officials in June.

The ECB will also be meeting in June where it is likely to give its forward guidance on interest rates and also to confirm whether its 30 billion euro bond purchase program will end in September as initially indicated.

Investors forecast that the interest rates in the Eurozone could rise approximately within nine months after the QE program is closed

XAUUSD Intraday Analysis

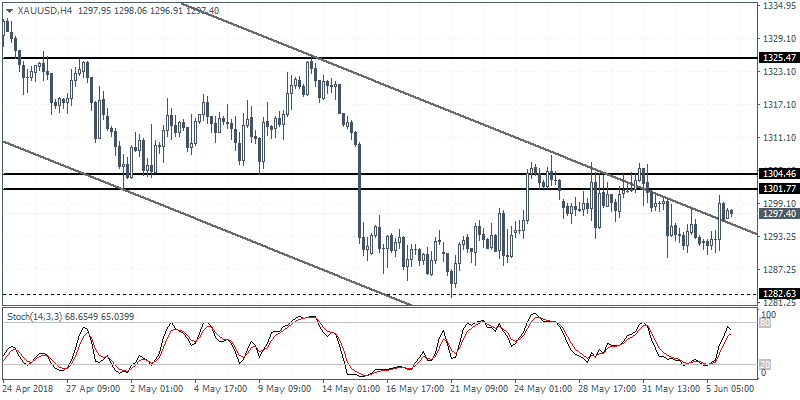

XAUUSD (1297.40): Gold prices eased on the day as price action was seen drifting lower. However, the higher low that was formed is likely to signal a possible breakout above 1304 - 1301 level of resistance. Currently, gold prices are seen testing the dynamic resistance off the falling price channel. The downside is expected to be limited but another retest of support at 1282 cannot be ruled out. Overall, gold prices are looking to form a bottom around the 1282 level ahead of an upside breakout that is in store.

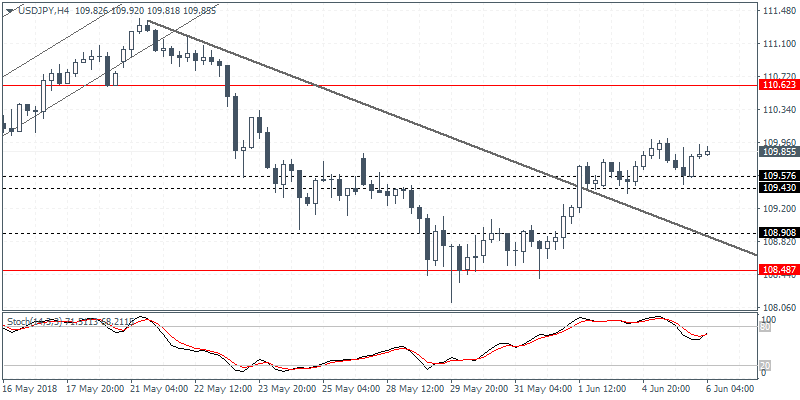

USDJPY Intraday Analysis

USDJPY (109.88): The USDJPY currency pair was seen falling back to the support level of 109.57 - 109.43 region. The retest of this support level could potentially see further gains in store. To the upside, the test of resistance at 110.62 is very likely. Alternately, a breakdown below 109.57 - 109.43 level could signal a deeper decline with the next lower support at 108.90 being the likely target.

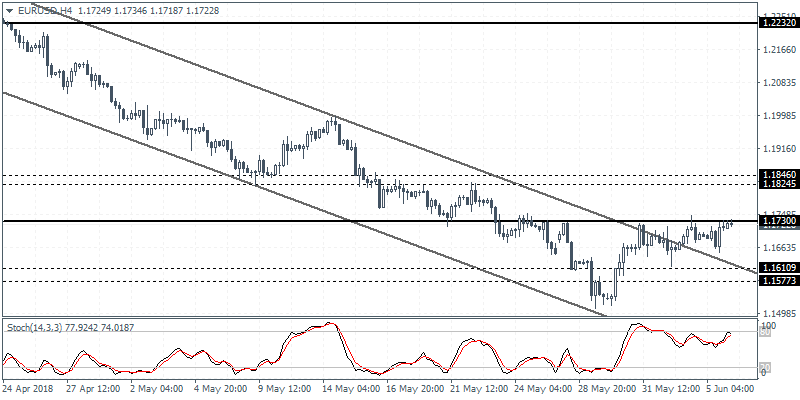

EURUSD Intraday Analysis

EURUSD (1.1722): The EURUSD currency pair was trading subdued on Tuesday with price action confined to the resistance level of 1.1730. As the EURUSD trades within the resistance level of 1.1730 and 1.1610 we expect to see this range breaking in the near term. An upside breakout could potentially signal a correction to the sharp declines seen over the past few weeks. There is a possibility that the EURUSD could retest the main resistance level at 1.2232. To the downside, declines are likely to stall at 1.1610 - 1.1577 level of support.

Australia GDP Rises Sharply

The U.S. dollar was seen trading mixed on Tuesday. The declines came despite a strong non-manufacturing PMI report from ISM. The ECB President, Mario Draghi was scheduled to speak on Tuesday but the meeting was called off. Meanwhile, the new Italian Prime Minister Giuseppe Conte gave his speech where he touched upon the manifesto of the coalition government which included rejecting austerity measures. The Euro was little changed on his comments.

The RBA's monetary policy meeting did not see any major changes as the central bank held interest rates unchanged at 1.50% as widely expected. Markit's services PMI data from the Eurozone showed that services sector activity eased to 53.8, down from April's print of 53.9. In the UK, the services sector activity rebounded to 54.0 beating estimates of a modest increase to 52.9.

In the U.S. trading session, the ISM's non-manufacturing PMI data showed a strong increase to 58.6 which was above estimates of 57.9 and higher than April's 56.8.

Earlier in the day, Australia’s quarterly GDP data showed a 1.0% increase in the first quarter. This was higher than the estimates of a 0.9% increase and the GDP advanced from a revised 0.5% in the fourth quarter of 2017.

Looking ahead, the economic calendar for the day includes the trade balance figures from Canada which will later be followed by the U.S. non-farm productivity report.