Sample Category Title

Swiss CPI rose 0.4% mom, 1.0% yoy. Import prices led

Swiss CPI rose 0.4% mom, 1.0% yoy in May, above expectation of 0.0% mom, 0.8% yoy.

Core CPI rose 0.1% mom, 0.4% yoy. Domestic products CPI rose 0.2% mom, 0.4% yoy. Imported products CPI rose 0.8% mom, 2.7% yoy.

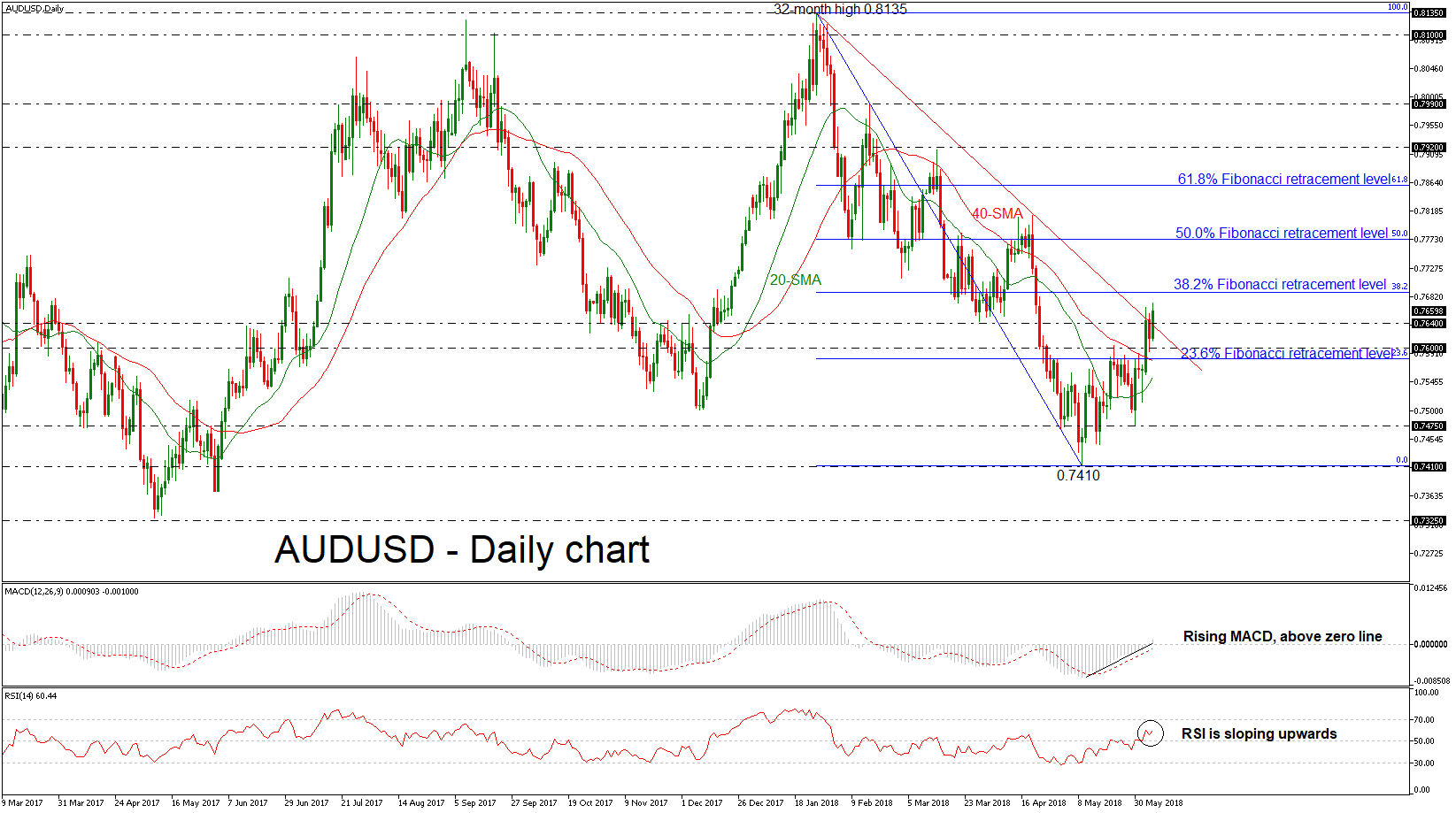

AUDUSD Posts Strong Gains Surpassing Medium-Term Descending Trend Line

AUDUSD is looking more bullish over the last few hours as the price aggressively surpasses the medium-term tentative descending trend line in the daily timeframe. The negative momentum appears to have run out of steam as prices have been attempting to close a day above the line.

Looking at momentum oscillators in the short-term timeframe though, they suggest further upside correction movement may be on the cards. The RSI indicator lies above its neutral 50 line, detecting positive momentum, and is also pointing upwards. The MACD oscillator, already positive, holds above its trigger and zero lines. In addition, the 20-simple moving average (SMA) is sloping up, approaching the 40-SMA and getting close to creating a bullish cross.

In case of a further bullish run in the pair, immediate resistance may be found near the 38.2% Fibonacci retracement level of the downleg from 0.8135 to 0.7410, around 0.7690. An upside break of that zone would open the way for the 50.0% Fibonacci of 0.7770. If buyers manage to push above that hurdle too, that would drive the price towards the 61.8% Fibonacci level near 0.7860.

On the flipside, if the bears retake control, price declines may stall initially near the latest lows of 0.7475. A potential downside violation of this region would send prices until the 0.7410 support barrier, raising the likelihood of more downside pressure. In such a case, the 0.7325 level could act as a barrier to the downside, identified by the May 9 low.

Broadly, in the medium-term, the outlook would shift to bullish if AUDUSD ends the day above the downtrend line.

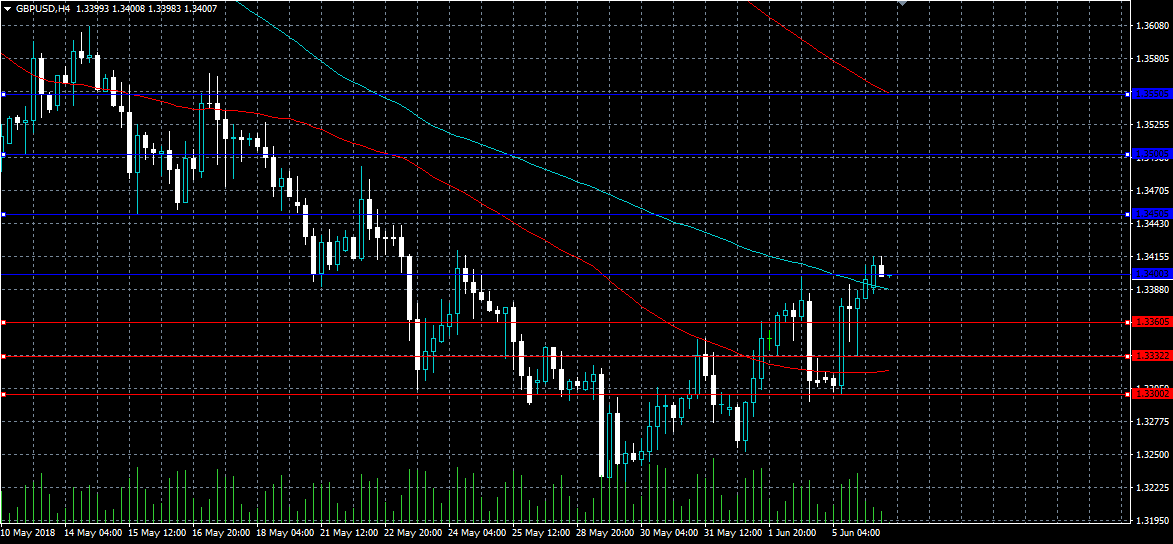

GBPUSD Strongly Bullish Above 1.3400 Level

The British pound has moved above the 1.3400 level against the US dollar, following reports that the ECB will debate an end to its current QE programme at its June 12th Policy Meeting. The GBPUSD pair currently trades around the 1.3400 handle, after finding interim technical resistance from the 1.3415 level earlier today. Traders now look towards ongoing Brexit negotiations between the EU and UK, and scheduled speeches from Bank of England members Tenreyro and McCafferty.

The GBPUSD pair is intraday bullish while trading above the 1.3400 level, key technical resistance is located at the 1.3450 and 1.3500 levels.

If the GBPUSD pair moves below the 1.3360 level, we may see sellers testing the 1.3332 and 1.3300 support levels.

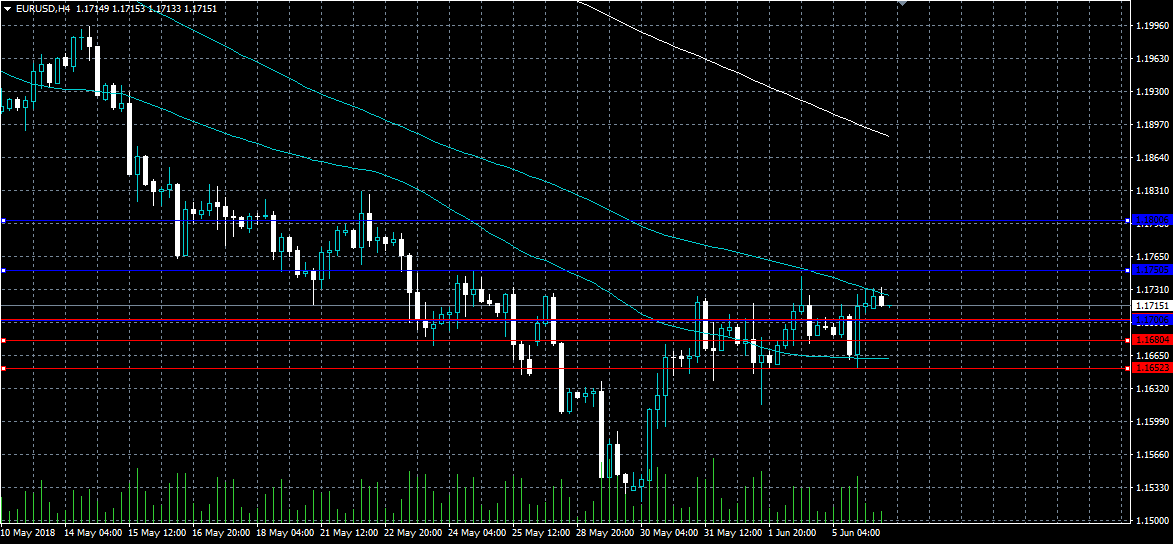

EURUSD Intrady Bullish Above 1.1680 Level

The euro currency has moved back above the 1.1700 level against the US dollar, after unconfirmed sources stated that the ECB will be discussing an exit to its QE programme at its next Policy Meeting. The EURUSD pair currently trades around the 1.1715 level, after finding strong weekly support from the 1.1652 level on Tuesday. EURUSD buyers will look for further gains above the key 1.1750 level, while sellers will look for further losses below the 1.1680 level.

The EURUSD pair is intraday bullish while trading above the 1.1680 level. Key resistance is located at the 1.1750 and 1.1800 levels.

If the EURUSD pair moves below the 1.1680 level, sellers may push price towards the 1.1652 and 1.1600 support levels.

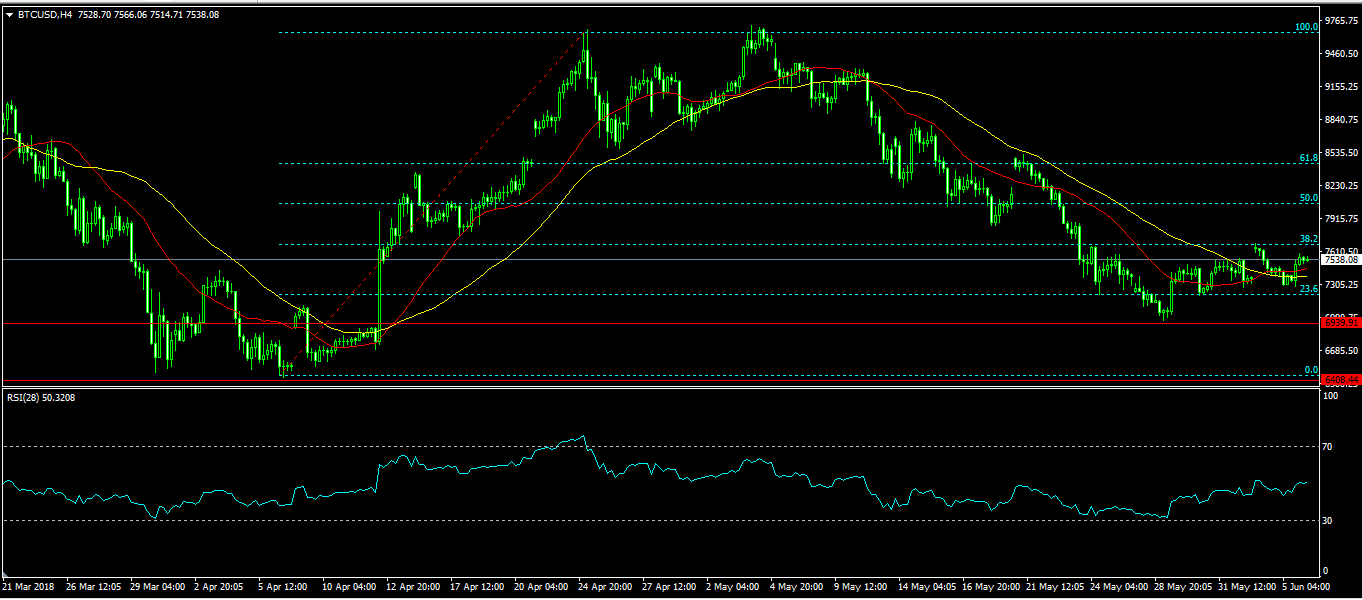

Bitcoins Falls As Jim Chanos Reiterates His Bearish Outlook

In early April, the price of bitcoin started to rally after the tax season in the United States ended. Traders believed that the demand for bitcoin and other cryptocurrencies would increase as Americans returned to the market. The price managed to rise from $6,400 and reached a high of $9,700 in late April. In May, the price fell from over $9,000 and reached a monthly low of $6940. This month, the BTC/USD pair has moved sideways in a narrow range.

Yesterday, the price of a bitcoin dropped after bearish statements by Jim Chanos. Jim is the founder of a hedge fund known as Kynikos Associates. He is one of the best-known short sellers in the market renowned for placing a bet that Enron would collapse. Enron was a Texas-based natural gas trading company, once valued at more than $70 billion. It collapsed in 2001.

Sharing his crypto-related thoughts with the Institute of New Economic Thinking, Chanos said that bitcoin and other cryptocurrencies would essentially be the last thing people relied on in the event of a crisis. He explained that “if the grid goes down,” bitcoin would not be a store of value in the event of a mass disaster. As a currency, he argued that bitcoin was unreliable in that it is more expensive than fiat currencies and is not widely accepted by physical and online retailers.

The BTC/USD pair is currently trading at $7,540. The price is slightly higher than the one-month and two-month simple moving average. Its RSI is currently at 50. The price is slightly below the 38.2% Fibonacci Retracement level. If the pair breaks out to the upside, it will likely test the 50% Fibonacci retracement level at $8070.

North American Trade In Focus On Wednesday

From a calendar perspective, US and Canadian trade data are the focal point of Wednesday's session. Both countries are scheduled to report on their international trade balance at the start of North American trade. Very few data headlines are expected before then.

The European session begins with a speech from a top central banker at 06:30 GMT. European Central Bank (ECB) official Peter Praet will deliver remarks that will be closely monitored by the financial markets.

About 30-minutes later, the Spanish government will report on industrial output for the month of April. Production is forecast to grow 0.3% month-on-month, which translates into an annualized rate of 5%>

At 07:15 GMT, Switzerland will release the latest edition of its consumer price index (CPI). The May reading is expected to come in at 0.3%, leading to a year-over-year growth rate of 0.9%.

Bank of England (BOE) policymaker Silvana Tenreyro is scheduled to deliver a speech at 10:40 GMT. Tenreyro has served as a tenured professor at the London School of Economics.

Shifting gears to North America, both the United States and Canada will unveil their trade numbers at 12:30 GMT. The US Commerce Department is forecast to show a deficit of $49 billion for April. Meanwhile, Statistics Canada will likely show a deficit of around $3.4 billion, smaller than the $4.14 billion shortfall during March.

Commodity traders will be keeping a close eye on weekly crude inventory data courtesy of the US Energy Information Administration (EIA). The EIA will likely show a drawdown of 2.5 million barrels for the week ended 1 June, compared with a 3.62 million-barrel drawdown the week before.

AUD/USD

Australia's currency dipped on Tuesday after the central bank voted to keep interest rates on hold. The Reserve Bank of Australia (RBA) has left the benchmark rate at a record low of 1.5% for 20 straight months. AUD/USD bottomed at 0.7601 but has since rebounded to trade in the 0.7625-0.7630 region. The pair faces interim support at the 50-day simple moving average, which is currently at 0.7605.

EUR/USD

Europe's common currency underwent a series of volatile moves on Tuesday, with prices bottoming in the low 1.1660 region. Prices then immediately bounced back toward the 1.1730 handle, where they are now trading. EUR/USD is currently testing the 1.1730 resistance level and a clean break is needed to drive prices back toward 1.1770 and eventually 1.1800.

GBP/USD

Cable is back on the offensive this week, with prices overtaking the 1.3400 handle for the first time in roughly two weeks. GBP/USD is currently trading around 1.3410, with the bulls taking aim at the 1.3460 handle. However, to cross that level, they need to put some distance behind the 20-day moving average, which is in the low 1.3400 region

AUD/USD Rises Above 0.7650

Markets

Global core bonds closed higher yesterday. German Bunds outperformed US Treasuries. German yields dropped by 2.2 bps (30-yr) to 4.9 bps (10-yr). The US curve bull steepened with yields 2.4 bps (2-yr) to 0.1 bp (30-yr) lower. Strong US eco data (non-manufacturing ISM, JOLTS) were unable to offset core bond gains stemming from new stress on the Italian BTP market and a volatile oil price. The Italian 10-yr yield spread vs Germany widened by 30 bps after Italian PM Conte's maiden speech in parliament stressed willingness to execute the Lega-5SM coalition agreement without a doubt. Brent crude initially lost more than $1.5/barrel before rebounding into the US close. Core bonds topped off in European after trade on rumours that the next week's ECB meeting is a "live" one. ECB President Draghi will probably refrain from announcing changes to the ECB's policy, but might commit to doing so in June. The rumours stopped yesterday's remarkably slow decline in EUR/USD, pushing the pair back above 1.17. They had a similar effect on EUR/GBP which faced bigger selling pressure after a stronger than expected UK services PMI. The pair closed the session at 0.8751, coming from 0.8789.

Risk sentiment is positive overnight. Most Asian stock markets gain ground, outperforming a mixed WS (bar Nasdaq). The US Note future slides lower while USD/JPY continues this month's early rebound, testing the 110 mark. The Bund will probably open lower, taking into account the ECB gossip. Today's eco calendar only contains second tier eco data, suggesting sentiment-driven trading. Core bonds have more downside potential going into the Fed and ECB with the US central bank potentially hinting at an acceleration of its tightening cycle and the ECB possibly preannouncing a policy change in July. From a technical point of view, we expect the US 10-yr yield to move towards 3% going into the Fed meeting, while first resistance for the German 10-yr yield kicks in at 0.5%. More stress in the BTP market is a wildcard. We advised against buying into any short term relief rally. Yesterday's action strengthens our belief. A normalization of credit premiums was long overdue in a stretched EMU government bond market. Today's story is less straightforward for FX markets. ECB rumours might be sufficient to keep EUR/USD more or less in balance the next days. More specifically, we eye a 1.1540-1.1830 trading range. Sterling remains locked in the tight 0.87-0.88 range.

The Aussie dollar sets a new short term high this morning after stronger than expected Q1 GDP data (1% Q/Q & 3.1% Y/Y). Q4 2017 GDP growth was upwardly revised from 0.4% to 0.5%. AUD/USD rises above 0.7650.

News Headlines

Jens Weidmann, head of Germany's central bank and possible successor of Draghi, has expressed his doubts on Macron's proposal for reforming the currency bloc, stating that the Eurozone could create dubious incentives if it introduced a greater degree of fiscal risk sharing. His comments underline German skepticism on the proposal.

In the US, the job openings rose, for the first time since this record-keeping started in 2000, above the unemployment. The historically tight labor market and stronger inflation is forcing the Fed to watch closely. If more signals appear of an overheating market, they might need to raise interest rates more aggressively than previously stated.

After statements that President Trump is considering negotiating with Canada and Mexico separately, Treasury Secretary Mnuchin urged the President to exempt Canada from steep steel and aluminum tariffs at a White House trade meeting on Tuesday. Not all advisors were in agreement, leaving Trump yet to be undecided.

ECB Praet: ECB to make judgement call next week

ECB chief economist Peter Praet delivers a speech titled "Monetary policy in a low interest rate environment" at the Congress of Actuaries, Berlin today.

There, he noted that "the key question for monetary policy is: will growth remain sufficiently strong for the ongoing pressure on resource utilisation to continue to nudge inflation along a pathway that rises fast enough towards our objective?"

In Praet's view, the "main intersection" between growth and inflation formation lies in the labor market. He said that "a look at the sectoral make-up of the most recent developments in the job market is encouraging". PMIs continued to signal employment creation across sectors and countries. And, measures of labour market titaness show "upward trend" has steepened over the past year. Measures of slack also showed improvement.

And at the same time "there is growing evidence that labour market tightness is translating into a stronger pick-up in wage growth". Annual wage growth rose to 1.9% in Q1, up from Q4's 1.6%. The upsurge was due to sharp rise in 2.3% in negotiated wages in Germany. And rising wage pressures are starting to feed into producers prices too.

Praet added that "signals showing the convergence of inflation towards our aim have been improving, and both the underlying strength in the euro area economy and the fact that such strength is increasingly affecting wage formation supports our confidence that inflation will reach a level of below, but close to, 2% over the medium term. "

Full speech here

Praet also added that "next week, the Governing Council will have to assess whether progress so far has been sufficient to warrant a gradual unwinding of our net purchases." And, it will be a “judgement” call.

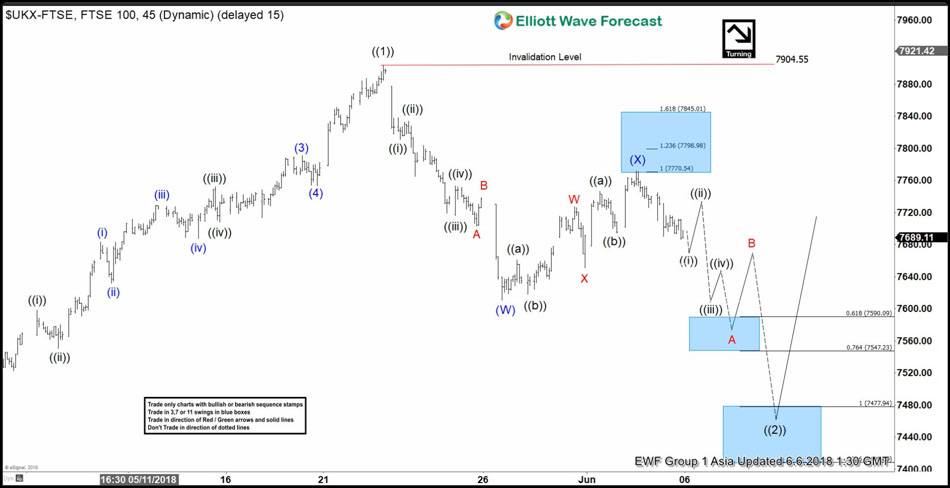

Elliott Wave View: FTSE Buying Opportunity Soon

FTSE short-term Elliott wave view suggests that the rally to 7903.50 high on 5/22/2018 peak ended primary wave ((1)). This rally to 7903.5 starts from 3/23/2018 low and took the form of an impulse Elliott wave structure. The index is currently in Primary wave ((2) pullback to correct cycle from 3/23/2018 low.

So far the decline from the peak shows an overlapping internal structure, suggesting the index is pulling back in corrective sequence i.e either as W,X,Y or W,X,Y,X,Z structure. Down from 7903.5 high, the decline to 7610.66 low ended the first leg of the pullback in Intermediate wave (W). The internals of Intermediate wave (W) unfolded as Elliott wave Zigzag structure where Minor wave A ended at 7703.26, Minor wave B ended at 7738.46, and Minor wave C of (W) ended at 7610.66.

Above from 7610.66, the bounce to 7772.12 high ended Intermediate wave (X). The internals of Intermediate wave (X) unfolded as Elliott wave double three structure where Minor wave W ended at 7727.45, Minor wave X ended at 7651.412, and Minor wave Y of (X) ended at 7772.12. Near-term, while below 7772.12 Intermediate wave (X) high, expect the Index to extend lower in Intermediate wave (Y). Intermediate wave (Y) should see more downside towards 7477.94-7408.77, which is 100%-123.6% Fibonacci extension area of Intermediate wave (W)-(X). This move lower should also end Primary wave ((2)) pullback & Index should resume higher again. We don’t like selling the index.

FTSE 1 Hour Elliott Wave Chart

Aussie GDP Beats Expectations, Sending A$ higher

General Trend:

- Asian equity markets trade generally higher following another record high for the Nasdaq

- Japanese equities gain as the Yen trades broadly weaker

- Commodity and tech related sectors outperform

- Nikkei weighted Fanuc [6954.JP] declines over 2% after cautious broker commentary

- Sony names current Chief Information Officer as new CFO

- China telecom ZTE said to have signed agreement in principle to settle with the US Commerce Dept.

- US Treasury Sec Mnuchin said to urge Trump to exempt Canada from tariffs; CAD and MXN trade higher

USD/JPY hovers below ¥110

- Australia Q1 GDP beat ests amid strength in commodity exports; Aussie gains, this starts the 27th consecutive year with no recession, data also marked the fastest annual pace in nearly 2 years

- New Zealand Q1 value of buildings unexpectedly declined, non-residential construction dropped

- PBoC offers medium-term lending facility (MLF) at unchanged rate; skips daily OMO

- China Central Bank speculated to raise MLF and reverse repo rates in the future (Chinese Press); Next week’s Fed meeting in focus (June 12-13th)

- Reserve Bank of India (RBI) to hold rate decision later today (unchanged is the consensus)

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.1%; closed +0.4%

- TOPIX Real Estate index +1%, Information & Communications +0.8%, Marine Transportation +0.6%

- Toyota Motors rises over 1%

- (JP) JAPAN APR LABOR CASH EARNINGS Y/Y: 0.8% V 1.3%E; REAL CASH EARNINGS Y/Y: 0.0% V 0.1%E

- (JP) Japan FSA may start probe into money laundering among domestic banks - Japanese Press

- (JP) World Bank: Cuts Japan 2018 GDP estimate to 1.0% from 1.3%

Korea

- Kospi closed for holiday

- (KR) South Korea Ministry of Trade, Industry and Energy: Have attracted ~$500M of investment from China investors in the areas of next-generation technologies, including chips, bio, automobiles and robots, through a ministerial roundtable - Korean press

China/Hong Kong

- Hang Seng opened +0.2%, Shanghai Composite -0.2%

- Hang Seng Materials index +1.3%, Industrial Goods +1.2%, Info Tech +1.1%, Energy +0.7%, Services +0.7%Financials +0.2%

- (CN) China speculated to cut RRR and raise yields on the medium term lending facility (MLF) and reverse repo - China Securities Journal

- (CN) China PBoC sets yuan reference rate at 6.4040 v 6.4157 prior

- (CN) China PBoC Open Market Operation (OMO): Skips v CNY120B injected in 7 and 28-day reverse repos prior: Net: drain CNY0B v CNY30B injected prior

- (CN) CHINA PBOC CONDUCTS CNY463B IN 1-YEAR MEDIUM-TERM LENDING FACILITY (MLF) V CNY156B PRIOR AT 3.30% V 3.30% PRIOR

- (CN) China debt cutting moves are harming private companies, while debt heavy state firms are carrying on. Of the seven companies that experienced their first bond default this year, six were privately owned - SCMP

- (CN) China securities regulator (CSRC) may approve CNY300B in funds related to CDRs on Wed - China Securities Times

Australia/New Zealand

- ASX 200 opened +0.1%, closed +0.4%

- ASX 200 Energy index +2.5%, Resources +2%, Utilities +0.6%; Financials -0.8%

- BHP [BHP.AU]: Said to receive bids which value shale unit at up to $9.0B - US financial press

- (NZ) Reserve Bank of New Zealand (RBNZ): To consult on new capital adequacy documents in late 2018; intention is not to change policy content of framework

- (NZ) New Zealand Fin Min Robertson: Debt forecast offers room against shocks

- (AU) AUSTRALIA Q1 GDP Q/Q: 1.0% V 0.9%E; Y/Y: 3.1% V 2.8%E

- (NZ) New Zealand to sell NZ$100M in 2040 inflation indexed bonds June 7th

Other Asia

- (ID) Indonesia Central Bank Gov Warjiyo: Expects Rupiah currency (IDR) to appreciate if inflows continue

- (MY) Malaysia Central Bank Chief Ibrahim said to have offered to resign in relation to state investment fund 1MDB - financial press

North America

- US equity markets ended mostly higher: Dow -0.1%, S&P500 +0.1%, Nasdaq +0.4%, Russell 2000 +0.7%

- S&P500 Materials +0.8%, Consumer Discretionary +0.6%

- (US) Weekly API Oil Inventories: Crude: -2M v +1.0M prior

- (VE) Venezuela PDVSA said to consider force majeure on oil exports, if terminal tanker congestion worsens unless customers accept ship to ship transfer – US financial press

- (CA) US Treasury Sec Mnuchin said to urge Trump to give Canada exemption from tariffs - Local Media

- (G7) Canadian G-7 official: G-7 currently working to reconcile gaps for a final communique; doesn't commit to G-7 releasing a final communique

- UPS [UPS]: Freight and package workers vote to authorize strike; The Teamsters suggested that the vote does not mean that a strike is imminent.

- World Bank updates 2018 global forecast: risks to global economy tilted to downside; maintains global GDP estimate at 3.1%

- US primary senate election results show democratic strength

- FB Confirms data sharing partnerships remain with Lenovo, Oppo and TCL, to wind down with Huawei by the end of the week - NYT

Europe

- (EU) ECB reportedly ready to discuss QE exit policy at June 14th meeting – press

- (EU) ECB's Weidmann (Germany): European reforms must fit into the existing framework; A rainy day fund is worthy of consideration

- (UK) Labour Party reportedly plans to announce shift towards soft Brexit - UK press

- (IT) Italy PM Conte wins Senate confidence vote, as expected - press

- (IT) Italy PM Conte: Euro exit has never been discussed by the govt; We should not make bond spread our only reference point

- Smurfit Kappa [SKG.UK]: International Paper to withdraw offer for Smurfit Kappa - press

Levels as of 02:00ET

- Hang Seng +0.7%; Shanghai Composite -0.2%; Kospi +0.3%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.3%; FTSE100 +0.2%

- EUR 1.1734-1.1714; JPY 109.97-109.79; AUD 0.7672-0.7615;NZD 0.7048-0.7025

- Aug Gold -0.0% at $1,302/oz; Jul Crude Oil +0.6% at $65.89/brl; Jul Copper -0.5% at $3.19/lb