Sample Category Title

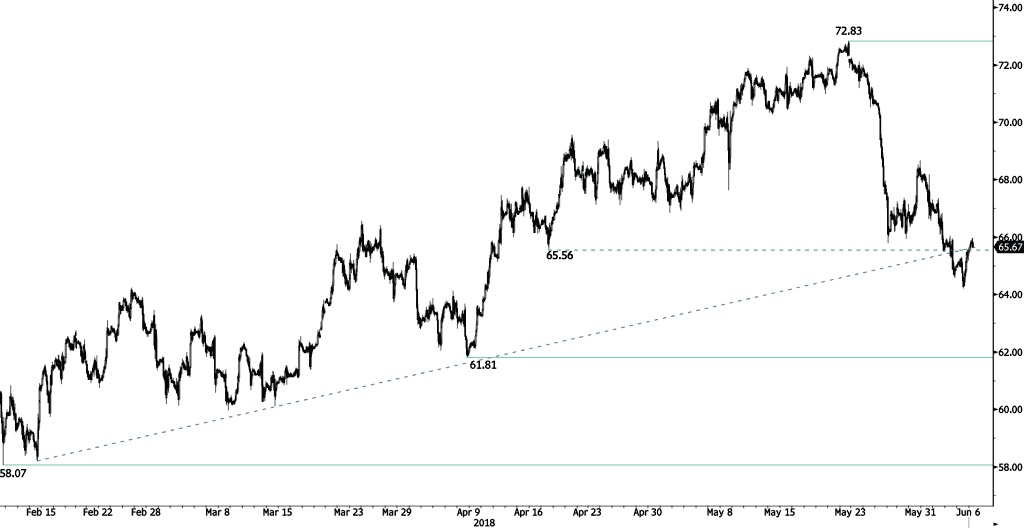

CRUDE OIL Approaching 66

Crude oil bounce from 64.22 (05/06/2018 low) continues, approaching 66. Hourly support and resistance are given at 61.81 (06/04/2018 low) and 72.83 (22/05/2018 high). The technical structure suggests short-term increase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Testing 16.60

Silver strong bounce from 16.36 low continues, trading above 16.55 and heading along 16.60. The short-term succession of higher lows continues to favour a bullish bias as long as uptrend floor holds. Hourly support and resistance are given at 16.05 (01/05/2018 low) and 17.35 (19/04/2018 high). The technical structure suggests short-term upward moves.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009). The pair is trading below its 200 DMA.

GOLD Approaching 1300

Gold strong bounce from 1290 low continues, trading along 1298 and approaching 1301. Hourly support and resistance are given at 1282 (21/05/2018 low) and 1329 (08/03/2018 high). The technical structure suggests further short-term increase.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low). The pair is trading below its 200 DMA.

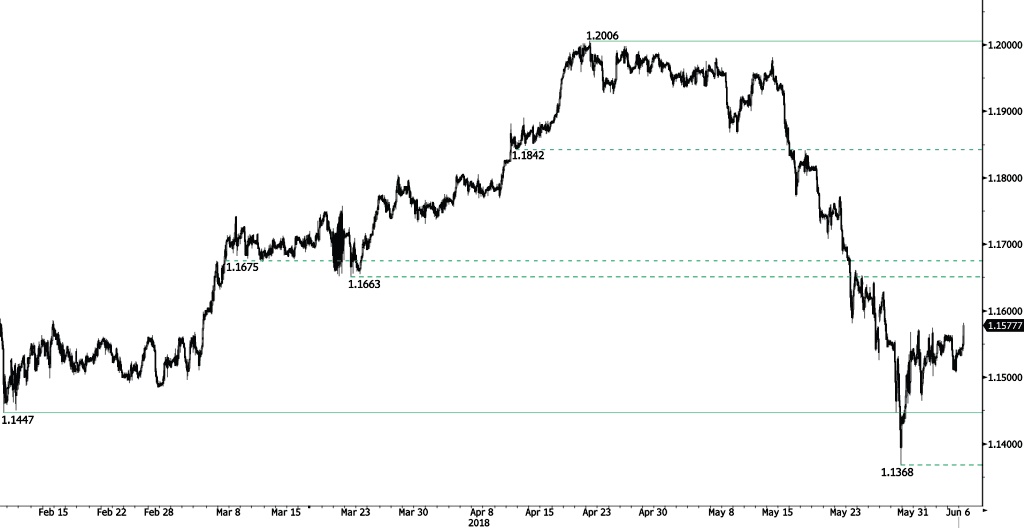

EUR/CHF Trading Above 1.1575

EUR/CHF is bouncing off from 1.1507 low, trading above 1.1575 and heading along 1.1590. EUR/CHF bearish trend started mid-May is however maintained. Hourly support and resistance are given at 1.1447 (08/02/2018 low) and 1.2006 (20/04/2018 high). The technical structure suggests short-term upward moves.

In the longer term, the technical structure has reversed. Strong resistance at 1.20 (level before the unpeg) is now at reach. The ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support and resistance can be found at 1.0624 (24/06/2016 low) and 1.2097 (18/12/2014 high).

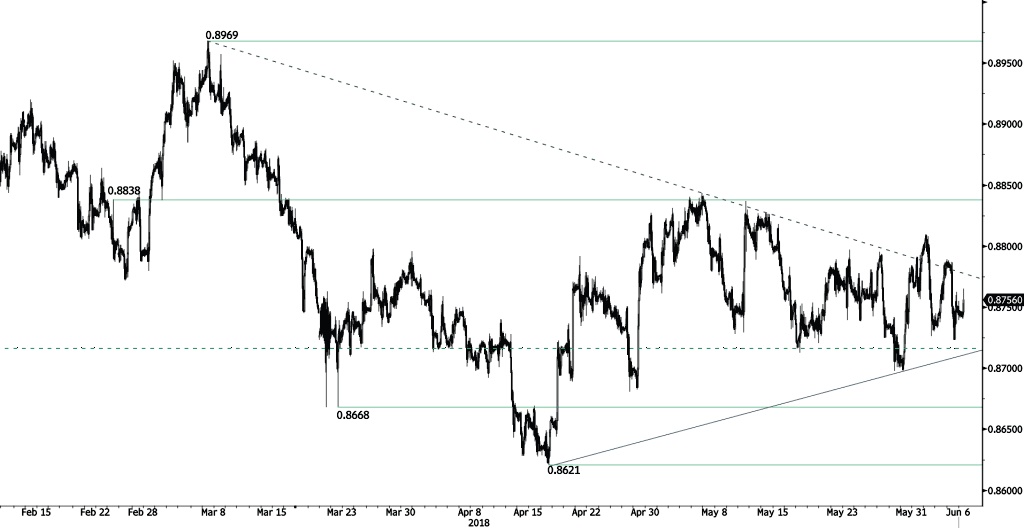

EUR/GBP Edging Higher

EUR/GBP strong bounce continues, trading above 0.876 and heading along 0.878. Hourly support and resistance are given at 0.8668 (22/03/2018 low) and 0.8838 (23/02/2018 high). The technical structure suggests short-term increase.

In the long-term, the pair has largely recovered from 2015 lows. The technical structure suggests further upside pressure. Strong resistance can be found at 0.9500 (psychological level) while support remains at 0.8304 (05/12/2016 low). The pair is trading below its 200 DMA.

USD/JPY Trading Above 110

USD/JPY strong bounce from 108.39 (31/05/2018 low) continues, the pair is trading above 110, approaching 110.20. Strong support and resistance are located at 108.05 (09/02/2018 low) and 111.48 (18/01/2018 high). The technical structure suggests short-term increase.

We favor a long-term bearish bias. A gradual rise towards major resistance at 125.86 (05/06/2015 high) seems unlikely. The pair is expected to decline further along long-term support at 101.20 (09/11/2016 low). The pair trades at its 200 DMA.

GBP/USD Increasing

GBP/USD is increasing further, trading above 1.34 and heading along 1.3430. The short-term bearish trend started in mid-April 2018 is maintained. Key support and resistance are given at 1.3062 (13/11/2017 low) and 1.3613 (03/01/2018 low). The technical structure suggests short-term upward moves.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Heading Higher

EUR/USD strong bounce resumes, the pair is trading higher, approaching the 1.1770 range. The short-term trend remains negative as long as prices remain below hourly resistance at 1.1993 (14/05/2018 high). Hourly support is given at 1.1510 (29/05/2018 low).

In the longer term, the momentum is turning largely negative. We favor a continued bearish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

China’s PMIs in May Suggest Government’s Pro-Growth Policy Shift At Work

China’s official PMI report (focusing on big companies) signals improvement in both manufacturing and services sector. The Caixin/ Markit data (focusing on SMEs) suggest both sectors remained resilient in May. We believe the government’s policy shift, to prioritize over domestic growth from deleveraging, has proved effective so far. The official report indicates limited impact of the recent US-China trade tension, while the Caixin/ Markit report suggests that new export orders stayed in contraction territory. The trade balance data due Friday would give more hints on the country’s exports sector.

Manufacturing sector

The official data, by the National Bureau of Statistics, shows that the manufacturing PMI increased to 51.9 in May, beating consensus of 51.4 and April’s 51.9. This marks the second highest reading since 2012 and the highest for the month of May since 2011. The improvement was broadly based, led by production and new orders. The sub-index for the form rose +1 point to 54.1 while that for the latter gained +0.9 point to 53.8 for the month. Trade-related sub-indices stayed under the spotlight as US-China trade friction remain elevated. Yet, the report indicates limited impact on China’s exports so far. In May, new export orders sub-index added +0.2 point to 51.2 while the import sub- index rose +0.7 point to 50.9. Meanwhile, input prices show signs of picking up, of which the sub-index rebounded, for the first time this year, to 56.7 from 53 in April. The significance of the jump might also reflect in the pickup in PPI inflation.

The manufacturing PMI by Caixin/ Markit steadied at 51.1 in May, slightly missing consensus of 51.2. Concerning the sub-indices, output and new order increased while employment dropped. The sub-index for new export orders improved in May but remained in contraction territory, suggesting that the impacts of trade tensions have been more serious on SMEs, than on large corporations. As the agency concludes, “operating conditions across the manufacturing sector remained stable. The growth in the price of industrial products has gained momentum, however, the export situation was still disappointing”.

Services Sector

The official data shows that the non-manufacturing PMI edged +0.1 point higher to 54.9 in May. This came in higher than consensus of 54.8. According to NBS, consumption growth was the main factor supporting service sector activity, which was the key contributor the pickup in non-manufacturing PMI last month. Separately, the Caixin/ Markit services index steadied at 52.9 in May. Looking into the details, the employment sub-index continued to rise, while the new business sub- index slipped slightly. According to the agency, these suggest “a positive change on the supply side and marginally weaker demand across the service sector”. The changes led to “a softer rise in prices charged, easing the upward pressure on service prices”. Yet, input costs show an accelerated pace of increase after slowing for three consecutive months.

Eurozone retail PMI rose to 51.7, driven by sharp rise in Germany

Eurozone retail PMI rose to 51.7 in May, hitting a 3-month high, indicating higher monthly sales. By country, Germany retail PMI rose to 13-month high at 55.5. France retail PMI rose to 3-month high at 50.7. Italy retail PMI stayed in contraction at 47.3.

Alex Gill, economist at IHS Markit which compiles the Eurozone Retail PMI, said:

"The latest PMI data signalled a more positive month for the eurozone retail sector, with sales returning to growth on both a monthly and annual basis. In turn, this contributed to the sharpest round of job creation in the current 31-month sequence of hiring.

"The positive trends were lop-sided when looking at country data, however. The rise in monthly sales was driven by a sharp rise in Germany, though a slight increase was also recorded in France. Meanwhile, Germany was the only country to register a rise in year-on-year sales, while Italy recorded a marked decline."

Full release here.