Sample Category Title

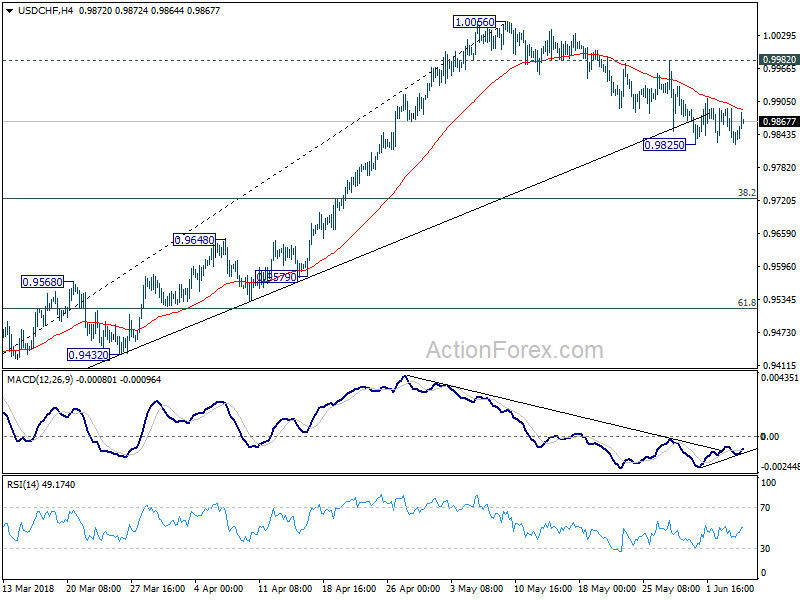

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9821; (P) 0.9857; (R1) 0.9884; More...

No change in USD/CHF's outlook as it's staying in tight range above 0.9825. Intraday bias remains neutral for the moment. On the downside, break of 0.9825 will indicate that fall from 1.0056 is correcting whole rise from 0.9186. In that case, deeper decline would be seen to 0.9724 fibonacci level before completion. On the upside, above 0.9982 minor resistance will suggest that the pull back is finished and bring retest of 1.0056.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

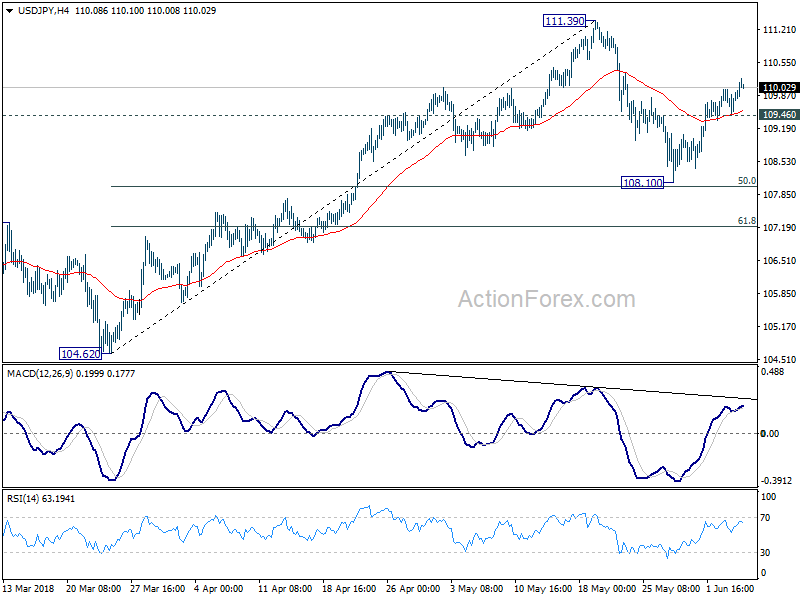

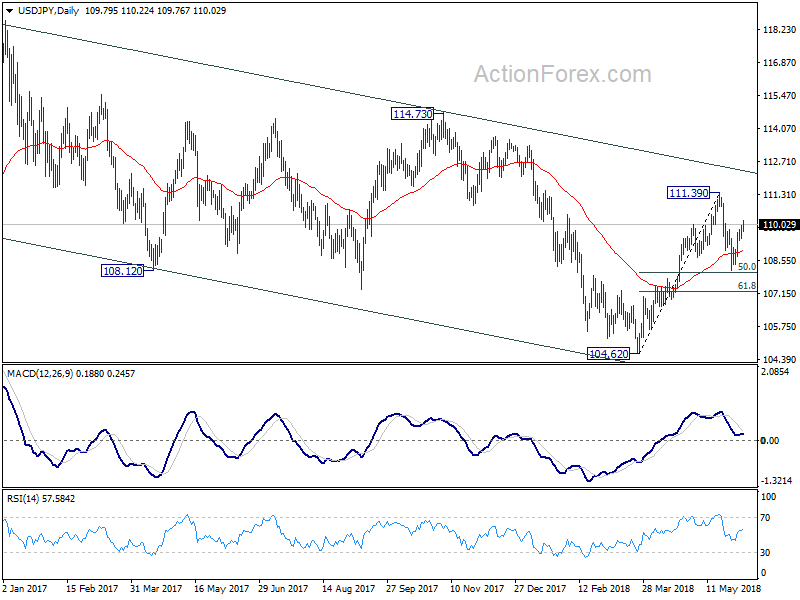

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.50; (P) 109.77; (R1) 110.07; More...

USD/JPY's rebound from 108.10 continues today and intraday bias stays on the upside. Retest of 111.39 resistance should be seen next. Break will resume the rebound from 104.62 and target a test on 114.73 key resistance level. However, on the downside, below 109.36 minor support will delay the bullish case and turn bias neutral again.

In the bigger picture, at this point , we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

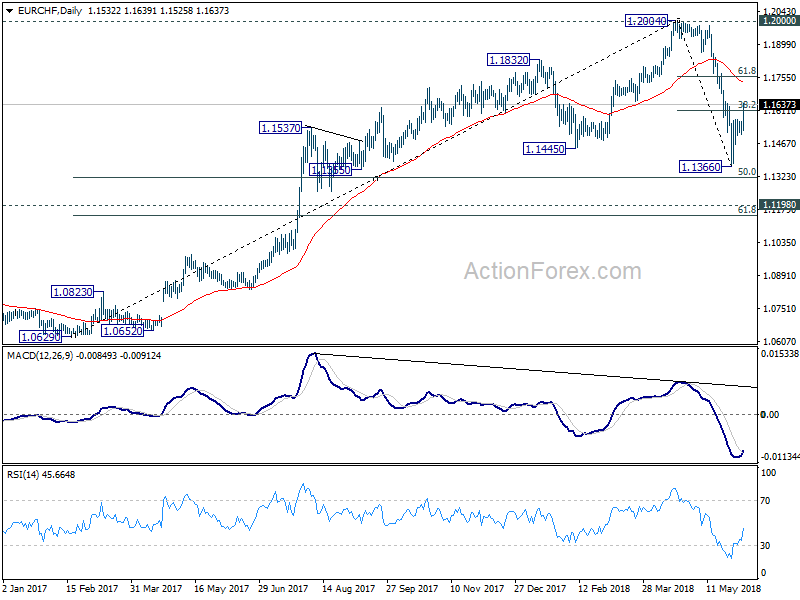

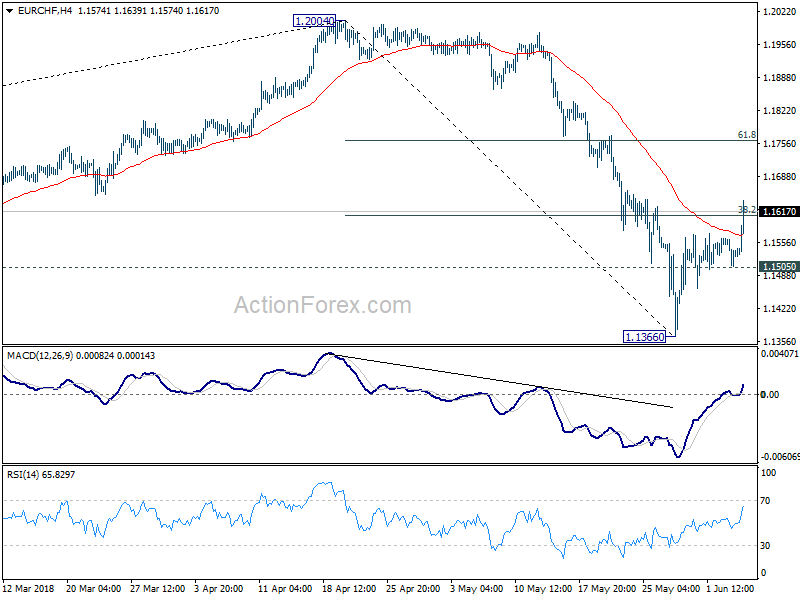

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1510; (P) 1.1538; (R1) 1.1570; More....

EUR/CHF surges to as high as 1.1639 so far today. The strong break of 38.2% retracement of 1.2004 to 1.1366 at 1.1610 suggests that decline from 1.2004 has completed at 1.1366 already. Intraday bias is now on the upside further rise to 61.8% retracement at 1.1760 and above. On the downside, break of 1.1505 support is needed to confirm completion of the rebound. Otherwise, further rally will remain mildly in favor even in case of retreat.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

Markets Eye G7 Summit, Dollar Softens

A cavalry of leaders from the world’s seven most powerful industrialized countries is set to congregate on Friday at the hotly anticipated G7 summit in Quebec.

Investors should buckle up for a potential showdown as trade is expected to be a major talking point throughout the summit. With escalating trade tensions seen as a significant threat to global economic growth, this could be a G7 meeting like no other. Leaders may use this gathering of heavyweights to address President Donald Trump’s decision to impose steep tariffs on steel and aluminium imports. The session could produce serious fireworks if the talks descend into arguments and disagreements on trade. Markets will be closely watching to see if G7 leaders will have the ability to persuade Trump to reverse his steel and aluminium tariffs on three of America's biggest trading partners.

Whatever the outcome of the summit, it most likely will have a lasting impact on global sentiment.

Dollar declines on profit-taking

It is slowly shaping up to be bearish trading week for the Greenback and there is a strong suspicion that this has nothing to do with a change of sentiment towards the currency.

According to official reports released yesterday, the ISM Non-Manufacturing PMI exceeded market expectations, by rising to 58.6 in May. With the US economy’s steadily expanding services sector boosting speculations of higher US interest rates, one would expect the Dollar to continue extending gains. Price action suggests that the culprit behind the Dollar’s depreciation could be a bout of profit-taking by investors. While the Dollar has scope to trade lower in the short term, the bullish fundamentals are likely to limit the downside.

Taking a look at the technical picture, the Dollar Index is under pressure on the daily charts with prices trading marginally below 93.70 at the time of writing. The downside momentum could drag the Dollar towards 95.00. A breakdown below this level may invite a further decline towards 93.35.

Commodity spotlight – Gold

There is a possibility that safe-haven Gold could be waiting for the G7 summit on Friday to make its next big move.

Although global trade fears remain a dominant market theme, the yellow metal clearly needs a fresh catalyst to accelerate the flight to safety. This much-needed catalyst could come in the form of Donald Trump if he creates chaos and uncertainty during the summit. A fresh wave of risk aversion birthed from heightened trade fears could elevate Gold towards $1300 and beyond.

Focusing on the technical picture, Gold remains on standby on the weekly charts with $1300 acting as a psychological level. A solid breakout above $1300 could encourage an incline higher towards $1324. Alternatively, sustained weakness below this level may open a path back towards $1280.

Euro Surges as ECB Praet Hints at Judgement Call on QE Next Week

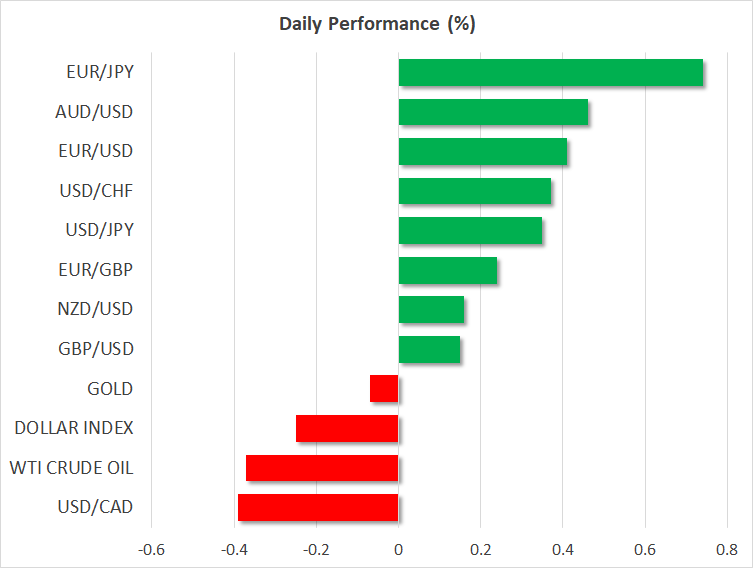

Canadian Dollar, Australian Dollar and Euro are the strongest major currencies today. Meanwhile, Swiss Franc, Yen and Dollar are the weakest one. The reason for the strength in Loonie is not exactly clear. But Canadian could be benefiting from report that US Treasury Secretary Steve Mnuchin urged President Donald Trump to exempt Canada from the steel and aluminum tariffs. Euro is clearly lifted by hawkish comments from ECB officials that raised of announcing the end of QE in next week's meeting. meanwhile, Australian Dollar continues to stay firm after today's GDP upside surprise.

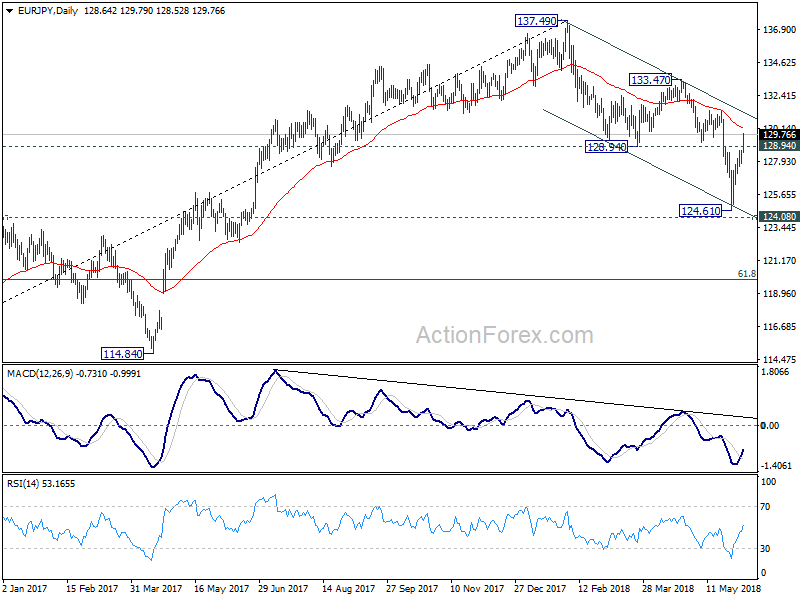

Technically, EUR/JPY's strong break of 128.94 support turned resistance argues that the correction from 137.49 has completed with three waves down to 124.61. Further rise is likely for 133.47 resistance in near term. EUR/CHF's strong break of 38.2% retracement of 1.2004 to 1.1366 at 1.1610 also suggests that the pull back from 1.2004 already. The question now is whether EUR/GBP will finally make up its mind and commit to a direction.

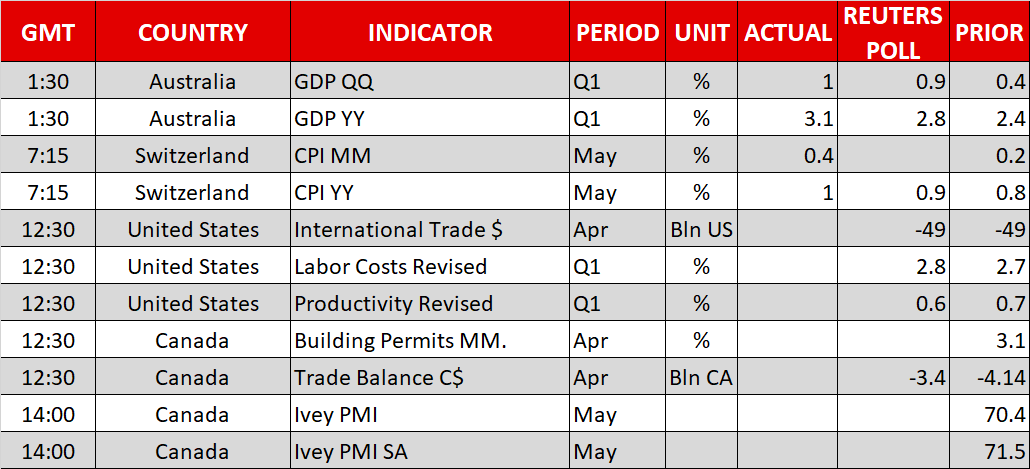

Released in the US session, US trade deficit narrowed to USD -46.2B in April. Non-farm productivity was finalized at 0.4% in Q1, unit labor costs at 2.9%. Canada trade deficit narrowed to CAD -1.9B in April, building permits dropped -4.6% mom.

ECB Praet: ECB to make judgement call next week

ECB chief economist Peter Praet sounded upbeat in his speech today in general. He pointed out that the "main intersection" between growth and inflation formation lies in the labor market". He said that "a look at the sectoral make-up of the most recent developments in the job market is encouraging". PMIs continued to signal employment creation across sectors and countries. And, measures of labour market titaness show "upward trend" has steepened over the past year. Measures of slack also showed improvement.

And at the same time "there is growing evidence that labour market tightness is translating into a stronger pick-up in wage growth". Annual wage growth rose to 1.9% in Q1, up from Q4's 1.6%. The upsurge was due to sharp rise in 2.3% in negotiated wages in Germany. And rising wage pressures are starting to feed into producers prices too.

Praet added that "signals showing the convergence of inflation towards our aim have been improving, and both the underlying strength in the euro area economy and the fact that such strength is increasingly affecting wage formation supports our confidence that inflation will reach a level of below, but close to, 2% over the medium term. "

Most importantly, Praet said "next week, the Governing Council will have to assess whether progress so far has been sufficient to warrant a gradual unwinding of our net purchases." And, it will be a "judgement" call.

ECB governing council member Klass Knot also reiterated that the central bank should wind down the asset purchase program as soon as possible.

Eurozone retail PMI rose to 51.7, driven by sharp rise in Germany

Eurozone retail PMI rose to 51.7 in May, hitting a 3-month high, indicating higher monthly sales. By country, Germany retail PMI rose to 13-month high at 55.5. France retail PMI rose to 3-month high at 50.7. Italy retail PMI stayed in contraction at 47.3.

Markit economist Alex Gill said in the released that "the latest PMI data signalled a more positive month for the eurozone retail sector, with sales returning to growth on both a monthly and annual basis. In turn, this contributed to the sharpest round of job creation in the current 31-month sequence of hiring".

However, he added that "the positive trends were lop-sided when looking at country data, however. The rise in monthly sales was driven by a sharp rise in Germany, though a slight increase was also recorded in France. Meanwhile, Germany was the only country to register a rise in year-on-year sales, while Italy recorded a marked decline."

Swiss CPI rose 0.4% mom, 1.0% yoy. Import prices led

Also released in European session, Swiss CPI rose 0.4% mom, 1.0% yoy in May, above expectation of 0.0% mom, 0.8% yoy. Core CPI rose 0.1% mom, 0.4% yoy. Domestic products CPI rose 0.2% mom, 0.4% yoy. Imported products CPI rose 0.8% mom, 2.7% yoy.

Germany, France and Britain seek US sanction exemptions in Iran

Reuters reported that Germany, France and Britain sent a letter to US Treasury Secretary and Secretary of State on June 4, requesting US sanction exemptions in EU companies in Iran.

The letter state that "as close allies, we expect that the extraterritorial effects of U.S. secondary sanctions will not be enforced on EU entities and individuals, and the United States will thus respect our political decisions." EU expected exemptions on

pharmaceuticals, healthcare, energy, automotive, civil aviation, infrastructure and banking companies.

The ministers also warned that "an Iranian withdrawal from the (nuclear agreement) would further unsettle a region where additional conflicts would be disastrous." And they emphasized that the 2015 JCoPA was "the best basis on which to engage Iran and address those concerns".

Japan PM Abe: G7 should play a role in free and fair global economic development

Japan Prime Minister Shinzo Abe warned today that "no country benefits from retaliatory trade restrictions." And, ahead of the G7 leaders summit on June 8-9, Abe said "my message is G7 should play a role in free and fair global economic development."

Separately, Abe said that ahead of the Kim-Trump summit in Singapore on June 12, he will meet Trump to "coordinate in order to advance progress on the nuclear issue, missiles and – most importantly – the abductees issue." A sticky point is that upon declaring peace in the Korean peninsula, UK could eventually have to reduce military forces in South Korea. And Japan's constitution, diplomatic policies and national security policies all will have to be totally reviewed for the completely new situation.

Australia GDP grew 1.0% qoq in Q1, led by exports growth

Australia GDP grew 1.0% qoq in Q1, above expectation of 0.8% qoq. Q4's figure was also revised up from 0.4% qoq to 0.5% qoq.

Chief Economist for the ABS, Bruce Hockman said in release that "growth in exports accounted for half the growth in GDP, and reflected strength in exports of mining commodities." Mining industry Gross Value Added grew 2.9% during the quarter. Production of coal, iron ore and liquefied natural gas showed strong increases.

Meanwhile, private non-financial corporations profits increased by 6.0%. Hockman added that "the rise in profits was consistent with the strong increase in mining exports coupled with a lift in the terms of trade this quarter."

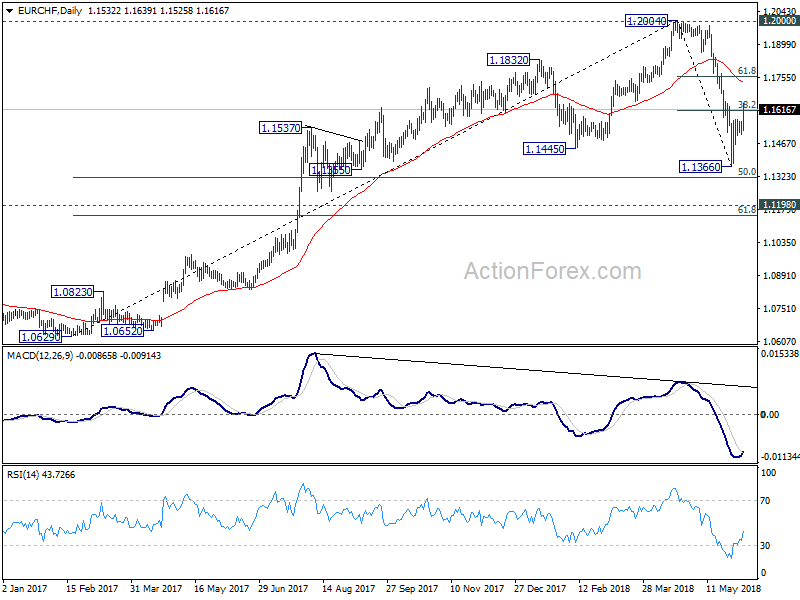

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.1510; (P) 1.1538; (R1) 1.1570; More....

EUR/CHF surges to as high as 1.1639 so far today. The strong break of 38.2% retracement of 1.2004 to 1.1366 at 1.1610 suggests that decline from 1.2004 has completed at 1.1366 already. Intraday bias is now on the upside further rise to 61.8% retracement at 1.1760 and above. On the downside, break of 1.1505 support is needed to confirm completion of the rebound. Otherwise, further rally will remain mildly in favor even in case of retreat.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily and weekly MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Such correction is expected to extend for a while and therefore, we're not anticipating a break of 1.2004 in near term. Another decline cannot be ruled out yet. But in that case, strong support should be seen at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154 to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y Apr | 0.80% | 1.40% | 2.10% | 2.00% |

| 01:30 | AUD | GDP Q/Q Q1 | 1.00% | 0.80% | 0.40% | 0.50% |

| 07:15 | CHF | CPI M/M May | 0.40% | 0.00% | 0.20% | |

| 07:15 | CHF | CPI Y/Y May | 1.00% | 0.80% | 0.80% | |

| 08:10 | EUR | Eurozone Retail PMI May | 51.7 | 48.6 | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Apr | -1.9B | -3.4B | -4.1B | -3.9B |

| 12:30 | CAD | Building Permits M/M Apr | -4.60% | 2.80% | 3.10% | 1.30% |

| 12:30 | USD | Nonfarm Productivity Q1 F | 0.40% | 0.70% | 0.70% | |

| 12:30 | USD | Unit Labor Costs Q1 F | 2.90% | 2.70% | 2.70% | |

| 12:30 | USD | Trade Balance Apr | -46.2B | -50.0B | -49.0B | -47.2B |

| 14:00 | CAD | Ivey PMI May | 69.7 | 71.5 | ||

| 14:30 | USD | Crude Oil Inventories | -2.0M | -3.6M |

Germany, France and Britain seek US sanction exemptions in Iran

Reuters reported that Germany, France and Britain sent a letter to US Treasury Secretary and Secretary of State on June 4, requesting US sanction exemptions in EU companies in Iran.

The letter state that "as close allies, we expect that the extraterritorial effects of U.S. secondary sanctions will not be enforced on EU entities and individuals, and the United States will thus respect our political decisions."

EU expected exemptions on pharmaceuticals, healthcare, energy, automotive, civil aviation, infrastructure and banking companies.

EU ministers also warned that "An Iranian withdrawal from the (nuclear agreement) would further unsettle a region where additional conflicts would be disastrous." And they emphasized that the 2015 JCoPA was "the best basis on which to engage Iran and address those concerns".

Euro Up As ECB Oofficials See End Of QE

Here are the latest developments in global markets:

FOREX: The dollar unlocked a fresh two-week high of 110.16 (+0.34%) against the Japanese yen early in the European afternoon as another round of data released yesterday enhanced once again optimism on the US economy despite trade risks hanging in the background. The dollar index, though, which gauges the strength of the dollar versus six major currencies was down on the day at 93.65 (-0.27%) thanks to the rising euro and pound. Euro/dollar was in bullish mode for the third consecutive day, peaking at a fresh two-week high of 1.1773 today. Buying interest for the euro widened further after the head of Germany’s central bank, Jens Weidmann, and the ECB chief economist, Peter Praet send a message on Wednesday that end to the QE program could be possible by December, a decision probably taken at next week’s ECB policy meeting. The former also expressed confidence that inflation would return to the target. Meanwhile on the trade front, the European Commission announced that countermeasures against the US protectionism would come into effect in July. Pound/dollar was also enjoying gains today, trading at a two-week high of 1.3432 (+0.26%) as recent figures indicated that the economic slowdown in Q1 could be temporary. However, Brexit uncertainties were keeping investors cautious. Euro/pound changed hands higher as well at 0.8760 (+0.14%). In antipodean currencies, upbeat Q1 GDP growth readings in Australia kept aussie/dollar on the upside, with the pair last seen at 0.7649 (+0.49%). Kiwi/dollar was in the green too, trading at 0.7035 (+0.19%). Loonie/dollar declined further to 1.2920 (-0.39%) following after sources said yesterday that the US Treasury Secretary Mnuchin had asked Trump to exempt Canada from the recent metal tariffs. Moreover, other headlines stated that Canada is against of bilateral trade relations with the US, while is willing to continue negotiations on NAFTA.

STOCKS: European stocks were mostly in the green at 1100 GMT except the Italian FTSE MIB 100 which dipped by 0.16%, after the Italian new Prime Minister showed little willingness at his first speech in Parliament that he would scale back from the populist agenda. The pan-European STOXX 600 inched up by 0.09% with basic materials, energy, and technology sectors driving the index up, while the blue-chip Euro STOXX 50 was marginally down by 0.07%. The German DAX 30 rose 0.41%, extending gains since May 31, the French CAC 40 climbed by 0.06% and the Spanish IBEX 35 went up by 0.82%. UK’s FTSE 100 head up by 0.30%, while futures tracking US stock indices were pointing to a positive open.

COMMODITIES: Oil prices were weighing concerns on rising supply and hopes of lower exports in Venezuela, with WTI crude and Brent being down by 0.66% and 0.09% at $65.09/barrel and $75.32/barrel respectively. Particularly worries were based on news that OPEC could raise its output at its two-day policy meeting on June 23-24 in an attempt to slow down the recent rally in prices which was characterized as taken too far. Yesterday reports stating that the US is planning to ask OPEC for a 1 million output hike added further pressure to markets. However, today’s headlines announcing that Venezuela, a major energy supplier to the US and the biggest hub of reserves, considers halting its export production provided some support to the market. In precious metals, gold was moving sideways around $1,2950/ounce.

Day Ahead: US & Canadian trade data awaited

For the remainder of the day, the US will see the release of April’s trade balance at 1230 GMT which is forecasted to remain unchanged at -49.00bn. Also, the Unit Labor Costs index for Q1 is anticipated to inch up to 2.8% q/q from 2.7%.

At the same time, Canada will be publishing figures on trade balance as well, with forecasts being for trade deficit to narrow in April from 4.14bn to 3.40bn. Building permits and Ivey PMI out the country will be also available at 1230 GMT and 1500 GMT respectively, though trade stats will probably attract a greater attention amid rising trade uncertainties between the US and the rest of the world.

In energy markets, investors will look through the EIA report on US crude oil inventories. According to forecasts, crude stocks will drop by 1.824 million barrels in the week ending June 1 compared to a fall of 3.620 million in the preceding week. On the other hand, gasoline inventories and distillate stocks are anticipated to increase though not by much.

Investors are turning their attention to the Group of Seven meeting later this week that may give any clues on global trade tensions, as well as policy meetings from the European central bank and Federal Reserve next week month for any guidance for the next interest rates decisions.

In terms of public appearances, the ECB Members of the Supervisory Board Pentti Hakkarainen and Ignazio Angeloni will give speeches at 1330 GMT and 1710 GMT respectively. Meanwhile, Bank of England MPC member Ian McCafferty will be taking part in a Q&A session with listeners of LBC radio.

Forex Analysis: EURUSD And EURJPY

The Euro is strengthening after comments by ECB speakers have hinted that the central bank may look to announce an end to Quantitative Easing (QE), possibly as early as at the June meeting. Coordinated comments made by Praet, Hansson, and Weidmann all indicate a potentially upbeat projection by the ECB with inflation rising back to its target. In particular, Peter Praet, a member of the Executive Board of the ECB, gave a strong hint that the June meeting would see the ECB signal the end the QE programme in September. A rate hike was expected for Q3 2019 but this is now being brought forward with the probability of a hike in June 2019 rising to 70%.

EURUSD

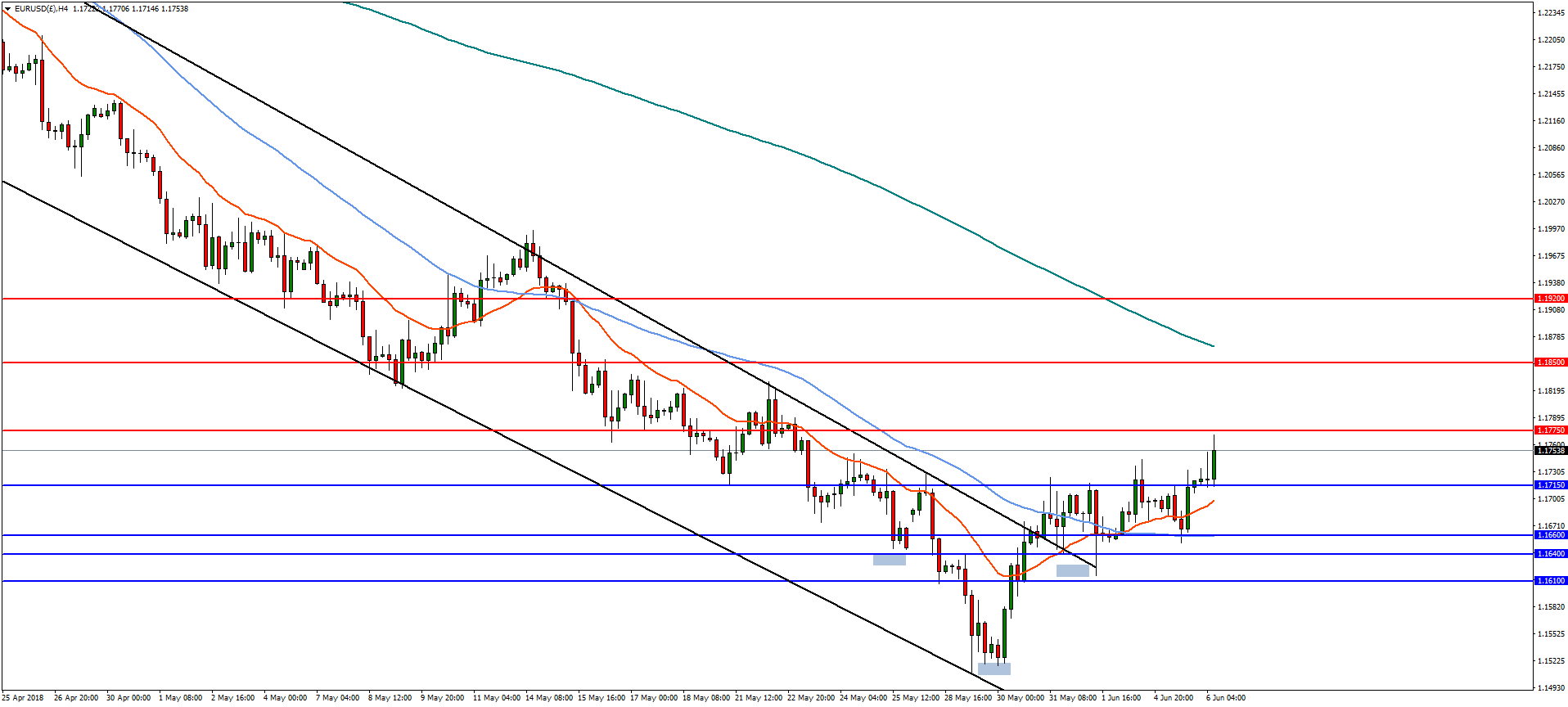

On the 4-hourly chart, EURUSD has broken out of the descending trading channel and has formed an inverted head and shoulders pattern with a measured target of 1.1920 with resistance at 1.1775 and the 38.2% retracement of the April highs at 1.1850. A reversal below the neckline at 1.1715 would negate the bullish outlook and the pair could continue to the downside with support at 1.1660.

EURJPY

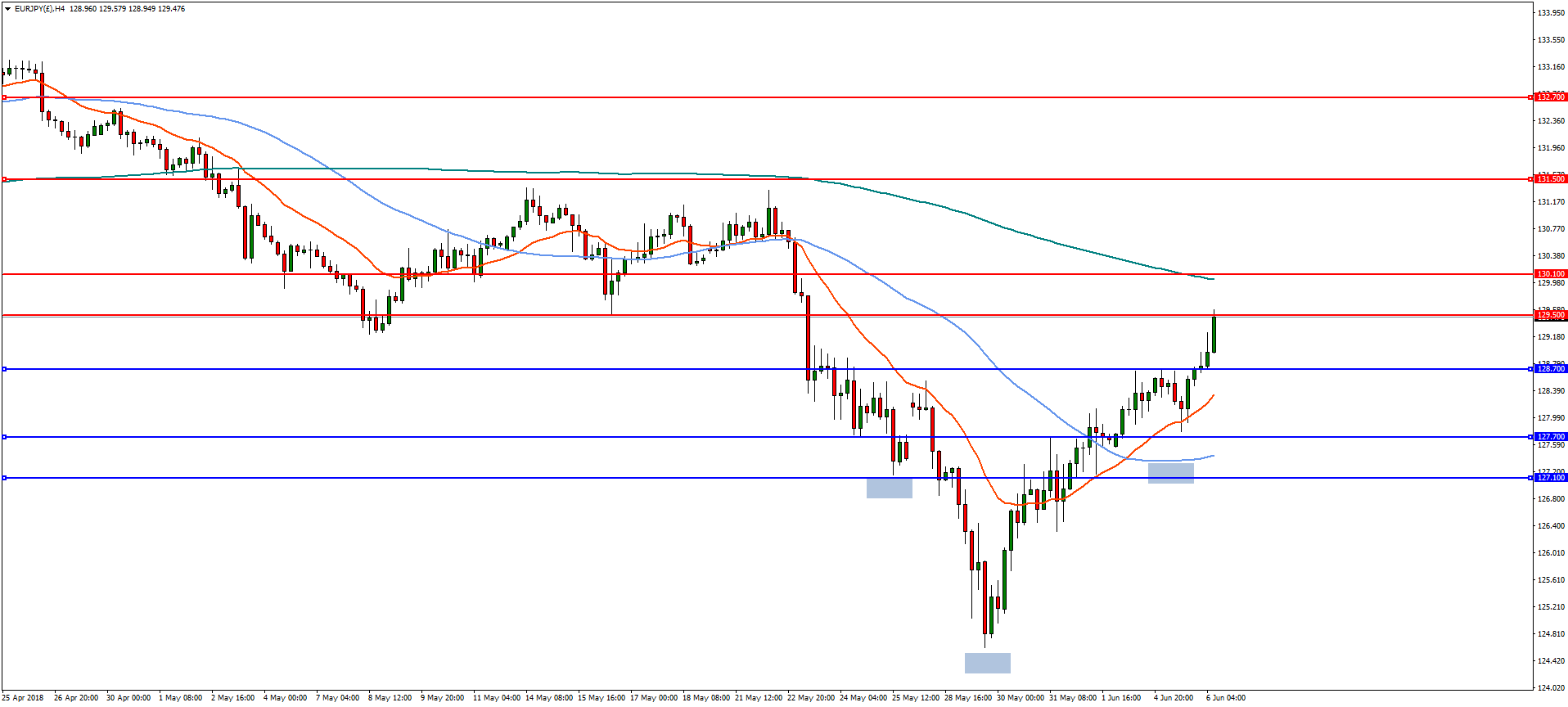

The recent weakness in JPY has helped the EURJPY pair stage a sharp rally. In the 4-hourly time frame, EURJPY has also formed and inverted head and shoulders pattern with a measured target of 132.70. Upside resistance is likely at 129.50 and the 61.8% retracement from the highs in April at 130.10. On the flip-side, a reversal should find support at 128.70 and then 127.70.

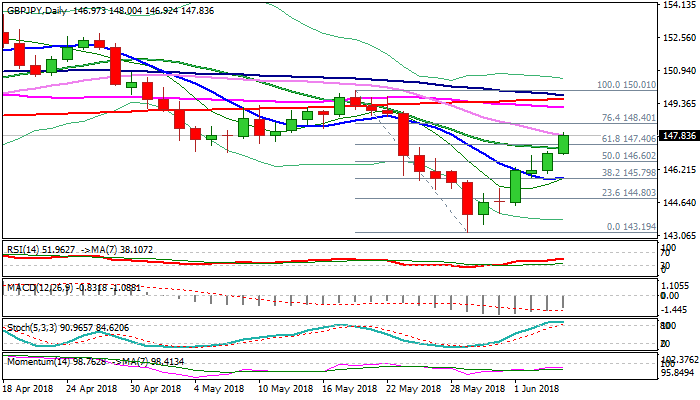

GBPJPY Levels: Recovery May Extend Further But Corrective Dips Can Precede Fresh Rally

The cross holds firm tone on Wednesday and extends recovery rally from 143.19 (29 May low) into sixth straight day.

Bulls probe through falling 30SMA after taking out pivots at 147.21/40 (20SMA/Fibo 61.8% of 150.01/143.19 bear-leg) earlier today.

North-heading daily RSI broke above the 50 midpoint and supports the advance, while momentum is in sideways mode and slow stochastic is overbought, which may slow the rally. Bulls eye Fibo 76.4% barrier at 148.40 and may extend towards a cluster of daily MA’s (55/200/100) in 149.20/77 zone which guard psychological 150 barrier.

Dips should be ideally contained by broken 20SMA (147.21) to keep immediate bulls intact, however, deeper correction towards north-turning 10SMA (145.81) which marks pivotal support, cannot be ruled out.

Res: 148.00, 148.40, 149.20, 149.59

Sup: 147.40, 147.21, 146.92, 146.03

Into US session: Euro strong on ECB expectation, except versus Aussie

Entering into US session, Australian Dollar remains the strongest one, riding on today's better than expected GDP data. Euro is closely following as lifted by ECB expectations. Meanwhile, Yen is the weakest one, followed by Swiss Franc.

ECB chief economist Peter Praet is clear in his comment that "next week, the Governing Council will have to assess whether progress so far has been sufficient to warrant a gradual unwinding of our net purchases." And, it will be a "judgement" call.

ECB governing council member Klass Knot also reiterated that the central bank should wind down the asset purchase program as soon as possible.

Technically, EUR/JPY's strong break of 128.94 support turned resistance argues that the correction from 137.49 has completed with three waves down to 124.61.

EUR/CHF's strong break of 38.2% retracement of 1.2004 to 1.1366 at 1.1610 also suggests that the pull back from 1.2004 already. More upside is now in favor for the Euro in near term.