Sample Category Title

Eco Data 6/7/18

[php_everywhere instance="1"]

Japanese Yen Steady Despite Soft Consumer Report

The Japanese yen has ticked lower in the Wednesday session. In North American trade, USD/JPY is trading at 110.23, up 0.23% on the day. On the release front, Japanese Average Cash Earnings is expected to drop sharply to 0.8%. There are no key U.S indicators on the schedule. On Thursday, the U.S releases unemployment claims and Japan publishes current account and Final GDP.

The Bank of Japan has steadfastly held that it will not exit its massive stimulus until inflation reaches the bank’s target of around 2 percent. Although inflation remains well below this level, a stronger economy has fueled expectations that the termination of stimulus is a question of ‘when’ rather than ‘if’. On Tuesday, Deputy Governor Masazumi Wakatabe said on Tuesday that the bank would not immediately start selling Japanese government bonds after the end of its stimulus scheme. Wakatabe said that a first priority for the BoJ would be taking care of excess liquidity. The cautious BoJ is unlikely to make any dramatic fiscal moves, aware that even slight steps can have a strong impact on the markets and the currency exchange.

Japan is keeping a close eye on the upcoming summit between US President Trump and North Korean President Kim Jong-un next week in Singapore. The meeting will mark the first ever face-to-face meeting between leaders of the U.S and North Korea. Trump has tried to lower expectations, saying the sides are unlikely to reach an agreement on North Korea relinquishing its nuclear weapons. Still, the fact that the two leaders are meeting is a sign that significant progress is being made in the long-standing dispute in the Korean peninsula. North Korean missiles represent a significant threat to Japan’s security, and Japanese Prime Minister Abe is expected to press Japan’s concerns when he meets with Trump ahead of the summit.

Euro’s strength much more convincing than Canadian Dollar’s

For now, Australian Dollar remains the strongest one for today as supported by solid GDP data. Euro and Canadian Dollar are racing for the second strongest one. But there is actually much hesitation in the Loonie. There were talks that Treasury Secretary Steven Mnuchin urged Trump to waive steel tariffs on Canada. But then there was also report by the Washington Post (!?) that Trump is going to confront Canada further by imposing additional tariffs. We usually don't buy into any rumors in the current post-truth world. But Canadian Dollar's lack of direction is a reflection of the vulnerable sentiments on the currencies. Adding to that, WTI crude oil is back under pressure and it's back pressing 64.5 now.

The strength in Euro is much more solid. It's from a trustable authority in ECB chief economic Peter Praet that policy makers are going to debate end of asset purchase program next week. The news took German 10 year bund yield higher to above 0.46 today, up more than 0.09. There is still some room for rally in bund yield before it hits the key level at 0.50. EUR/JPY has indeed broken equivalent level at 128.94 already. EUR/JPY's could be a prelude to further rise in bund yields. Or it could be just a reflection of surge in US 10 year yield too. We'll see.

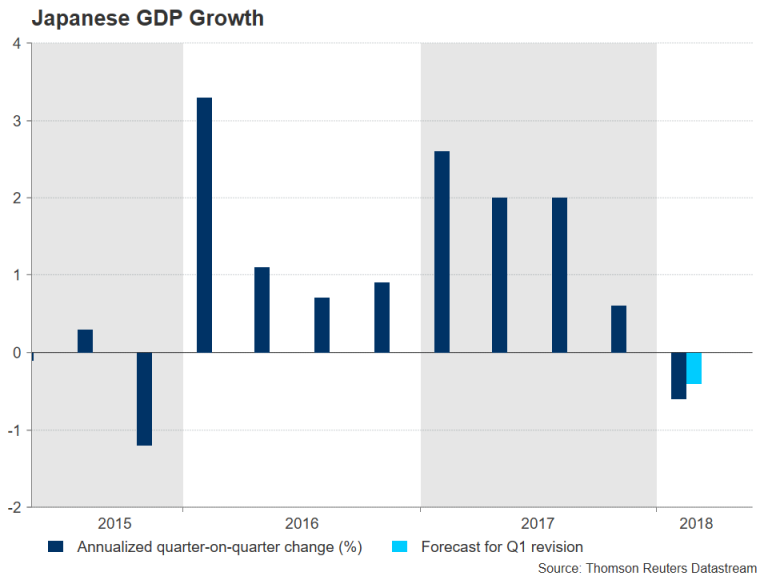

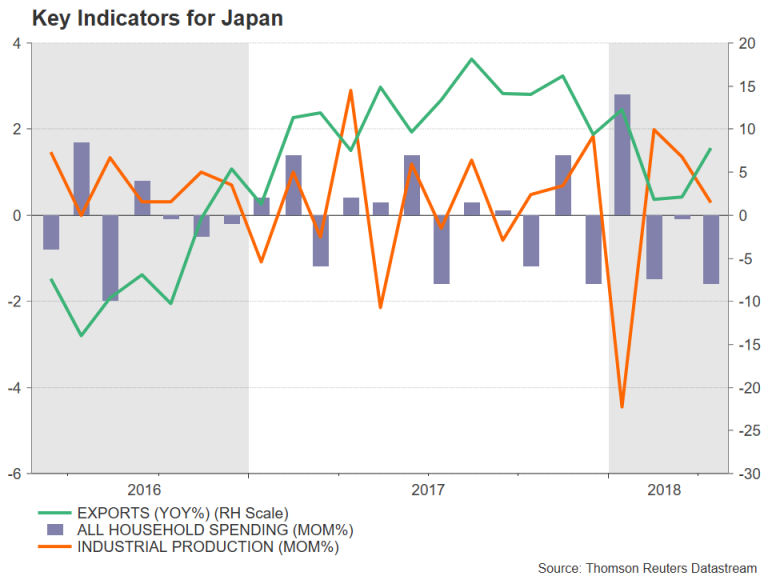

Japan GDP to Show Smaller Contraction But Could Still be Headed for Recession

Japan will publish revised GDP numbers on Friday (Thursday, 23:50 GMT) for the first quarter. Growth is expected to be revised higher on the back of stronger than initially estimated capital expenditure during the period. However, the revision is unlikely to allay fears of a recession unless growth is revised to positive, as household spending remains weak.

The preliminary estimate of GDP showed Japan’s economy ended a streak of eight consecutive quarters of growth – the longest since the 1980s – in the first three months of 2018, by contracting at an annualized pace of 0.6%. That figure is expected to be revised up to -0.4% on Friday, and the quarter-on-quarter rate from -0.2% to -0.1%.

If growth is revised even higher and turns positive, it would eliminate the risk of Japan slipping into technical recession in the second quarter (defined as two consecutive quarters of contraction). While business spending may have supported growth in the first quarter, early indicators point to ongoing weakness in household spending and industrial output going into the June quarter, suggesting no rebound in sight just yet.

Household spending declined for the third month in a row in April, falling by 1.6% month-on-month and confounding forecasts of a 0.7% increase. Industrial production has fared better after a big slump in January, but output growth eased to 0.3% m/m in April, missing expectations of 1.2%. Exports have also been rising at a slower pace following the surge in the second half of 2017, although they did bounce back strongly in April.

But with rising trade tensions weighing on investor sentiment and slowing demand in some parts of the world, the outlook for manufacturers and exports is a bit patchy. There also doesn’t appear to be much relief for consumers anytime soon either as wage growth remains subdued.

Annual growth in real wages was flat in April, dampening expectations of a rebound following a surprise 0.7% rise in March. Wages in Japan have failed to pick up despite a very tight labour market and repeated calls by the Abe government on businesses to award higher pay increases.

Without a recovery in wage growth and in turn, household consumption, Japan’s economy runs the risk of becoming increasingly reliant on exports to drive growth. It also poses a problem for the Bank of Japan as inflation is unlikely to make a sustained move upwards without higher domestic demand, making it difficult for the Bank to exit its massive stimulus program.

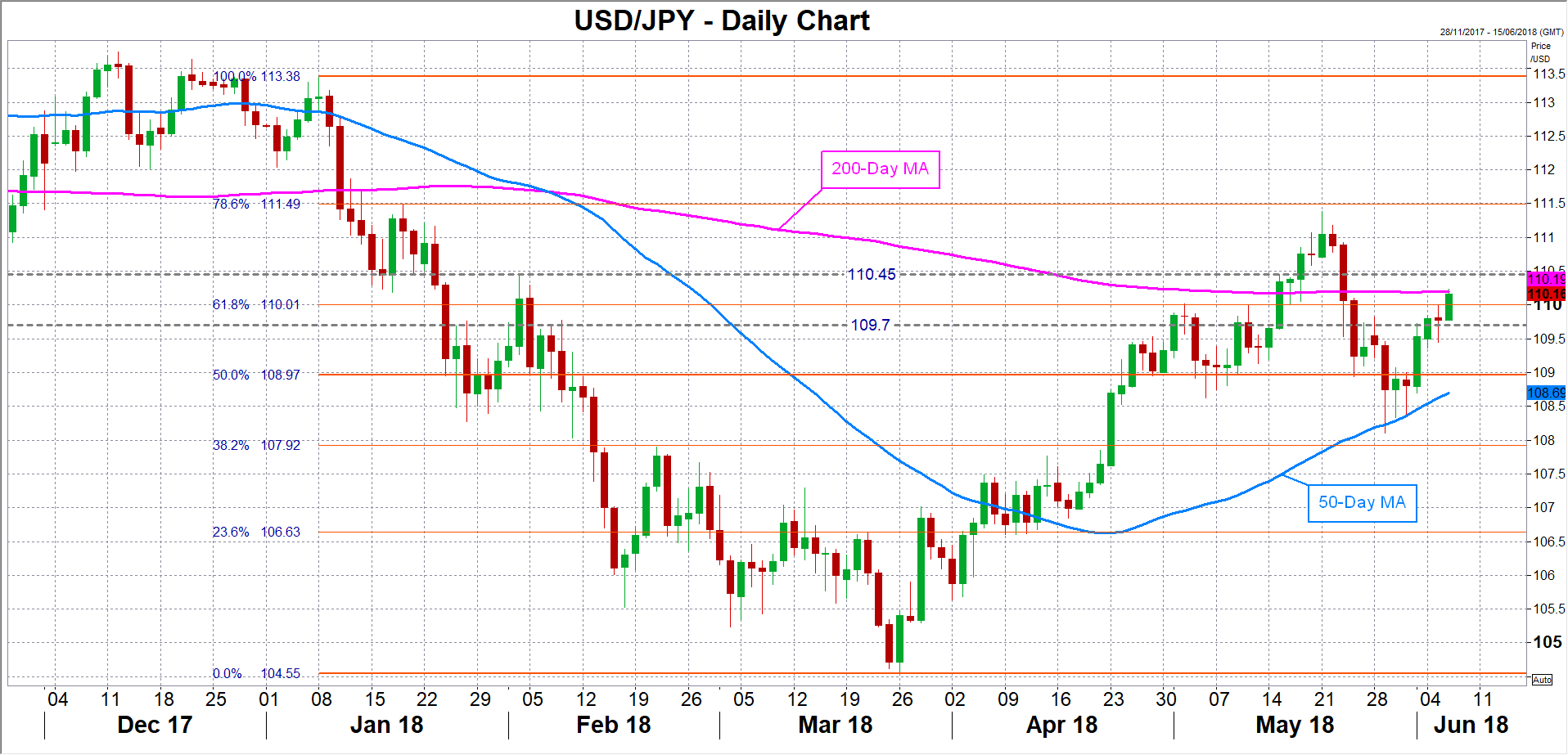

The Japanese yen doesn’t typically see much reaction to domestic data but big surprises in Friday’s numbers could still generate some volatility for the yen crosses if they impact expectations about BoJ policy normalization. If growth is substantially revised higher, dollar/yen could seek support from the 109.70 level – a recent congestion region. A break below this support would see the pair retesting the psychological 109 level, which if breached, would increase the risk of price action dipping below the 50-day moving average.

However, if there is a negative surprise and GDP is revised even lower, dollar/yen could head towards the 110.45 resistance area. A break above this level would open the way towards 111.50, which is the 78.6% Fibonacci retracement of the downleg from 113.38 to 104.55.

Euro Strength Prevailed Again Today

Markets:

Global core bonds lost ground today with German Bunds underperforming US Treasuries. The downleg in the Bund started yesterday evening after the official European close following rumours that next week’s ECB meeting is a “live” one. The Italian mini political crisis in May made the ECB disappear from investors’ radar with some even suggesting a blackout until after the Summer. Yesterday’s rumours met with rapid follow-up comments this morning from the likes of ECB Praet (“clear that the ECB will have to assess on June 14 whether to unwind the APP”; “signals of convergence of inflation with aim have improved”), ECB Weidmann (“market expectations for bond-buying to end this year are plausible”), ECB Knot (“reasonable to announce an end to asset purchases soon) and ECB Hansson (“higher rates are possible before mid-2019”). Risks increase that the ECB will effectively announce a new forward guidance for APP already next week instead of the traditional preannouncement first (base scenario with effective measures in July). German yields rise by 4.5 bps (2-yr) to 8.3 bps (10-yr). The belly of the curve underperforms the wings. US yields gain 2 bps (2-yr) to 2.9 bps (10-yr). 10-yr yield spread changes vs Germany range between -3 bps (Portugal) and +2 bps (Italy).

Euro strength prevailed again today even as market nervousness on Italy persisted. The focus of FX traders was on the developing debate on ECB policy normalization after yesterday’s rumours that next week’s ECB meeting was a ‘live’ meeting. It’s unsure that the ECB will already formally announce a change in APP starting in September. However, the internal debate is ongoing. Those rumours already propelled the euro yesterday evening. The euro rally continued today after ECB Praet and other MPC members confirmed that ECB is pondering the (timing of) of the next steps in policy normalization. There are still plenty of potentially euro negative factors/USD positives (Italy, strong US data in the run-up to the Fed meeting, trade tensions). However, the rising chance of a less is easy ECB policy is a good enough reason for a further EUR/USD short squeeze in a market that still was/is positioned quite short euro. The pair trades currently in the 1.1770 area. The first intermediate resistance in the 1.1830 area is gradually coming within reach. The rise in core yields (both in the US and Europe) widens interest rate differentials against the yen. USD/JPY regained the 110 barrier. There was little in the way of UK specific news today. EUR/GBP basically followed the broader rise of the euro. EUR/GBP trades currently in the 0.8770 area. So, most of yesterday’s EUR/GBP decline in the wake of a decent UK PMI was undone. In broader perspective, EUR/USD continues to hold in well-known territory.

News Headlines:

Yesterday it got clear that UK PM May will not present a blueprint on future UK-EU relationships at the summit in Brussels later this month. Today she refused to commit to a date for publishing this plan. Officials stated earlier this week that the publishing is planned for right after the summit, but that remains highly uncertain.

The Central Bank of India has raised its benchmark interest rates for the first time since 2014 by 0.25%. The raise stems from concerns about inflationary pressures, due to the oil price, and the recent weakening of the Indian Rupee. The rate increase follows after the RBI governor Patel expressed his concerns about the turbulence in the emerging markets, partially due to a strong dollar.

The US trade deficit fell to $46.2bn in April from a $47.2bn deficit a month earlier. Boosted by higher exports and a fall in imports, the market expectations of $49bn were outperformed. The further decrease of the trade deficit is good news for President Trump, who made it an electoral priority to narrow the gap.

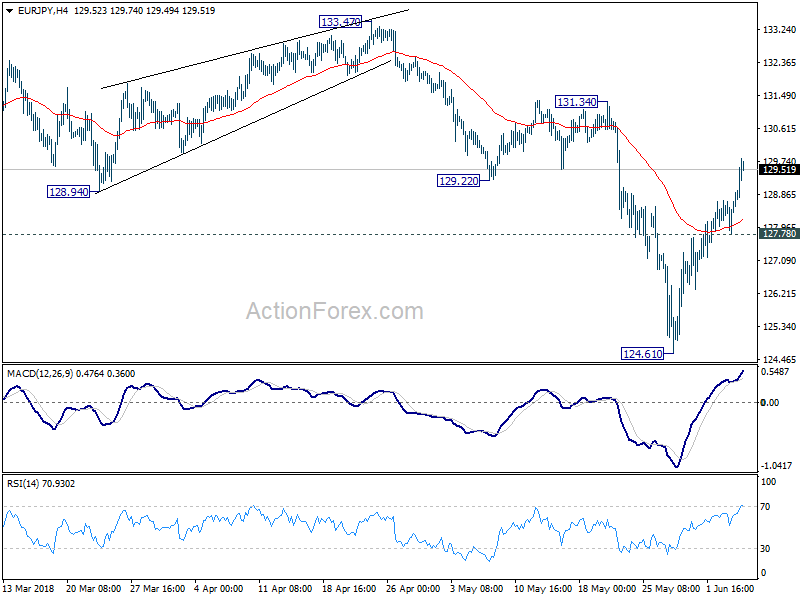

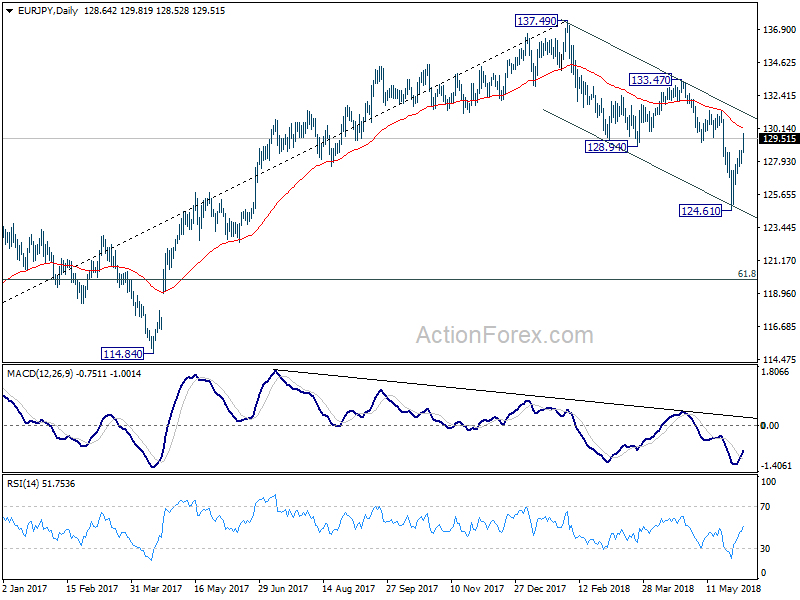

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 128.06; (P) 128.38; (R1) 128.98; More....

EUR/JPY's strong rally today and firm break of 128.94 support turned resistance suggests that decline from 137.49 has completed at 124.61 already. The three wave structure in turn suggests that it's a correction. And that larger rise is not finishe3d yet. Intraday bias in now on the upside for 131.34 resistance first. Break will target 133.47 key resistance next. On the downside, break of 127.78 support is now needed to indicate completion of the rebound. Otherwise, outlook will stay cautiously bullish in case of retreat.

In the bigger picture, as long as 124.08 resistance turned support holds, medium term rise from 109.03 (2016 low) is still in progress and another high above 137.49 would be seen. Nonetheless, considering bearish divergence condition in daily MACD, decisive break of 124.08 will confirm medium term reversal and target 61.8% retracement of 109.03 to 137.49 at 119.90 and below.

Canada’s Trade Deficit Shrunk Sharply in April

Highlights:

- Canada’s nominal trade deficit narrowed sharply in April, to $1.9 billion from $3.9 billion in March

- Export volumes rose 1.3% to build on a 3.3% March increase. Import volumes fell 1.9% but that only partially retraced a 4.7% jump the prior month.

- Non-energy export volumes rose 1 1/2% in April to build on a 2 1/2% increase in March — although were still up just 1 1/2% from a year ago.

Our Take:

The improvement in the nominal trade deficit to $1.9 billion more-than-retraced a surprisingly large deterioration to $3.9 billion in March from $2.7 billion in February — and with relatively solid underlying details. The 1.6% increase in nominal exports built on a 4% increase in March and was largely the result of higher volume sales rather than prices. The 1.3% increase in export volumes was led by a 1 1/2% rise in non-energy sales abroad that built on a 2 1/2% March increase. The almost 2% drop in import volumes only partially retraced a 4.7% gain the prior month as motor vehicle and consumer goods purchases eased lower after big March gains. Equipment import volumes, a key indicator of domestic investment spending, also ticked lower but the April level was still above its Q1 average.

The monthly trade data is notoriously volatile, and non-energy export volumes were still up just 1 1/2% from a year ago in April, despite an improved global trade backdrop. Exports going forward will also have to contend with new U.S. steel and aluminum tariffs in June — although we continue to think the broader macroeconomic impact of those will be limited. Nonetheless, improvement in the trade data over recent months adds to the evidence that Canadian economic growth picked up in Q2 after a sharp pullback in home resales alongside transitory disruptions to oil production and transportation backlogs combined to weigh on Q1. We continue to expect a 2 1/2% increase in Q2 GDP following the 1.3% Q1 gain.

Canada’s Goods Trade Deficit Narrows by Half to $1.9 Billion in April

Canada's goods trade deficit narrowed by about half to reach $1.9bn, from a revised $3.9bn in April (previously $4.1bn). The result was better than the narrowing to $3.4bn expected by Bay Street. Exports recorded another increase (+1.6%), led by metal and non-metallic mineral products and consumer goods. Imports fell 2.5% in the month, held back by motor vehicles and parts as well as consumer goods.

The story was little changed after accounting for monthly price changes. In real or volume terms, exports rose by a slightly less pronounced 1.2%. At the same time, imports too fell by a touch less, down 2.4% on the month.

Exports rose for the sixth time in seven months to a record high and are up 3.1% from the same time last year. Shipments of metals and non-metallic minerals increased 9.1%, more than reversing the 7.8% slump experienced in February, helped along by strong sales of intermediate metals including unwrought gold. Consumer good exports were also up a solid 5.4% on the month, led by a one-third surge in pharmaceuticals. Exports of autos and parts was up 1.3% on the month while other transport products (including aircraft) were down 14.2% after two exceptional monthly gains of more than 20% apiece – related to sales of boats and other personal transportation equipment to Saudi Arabia and aircraft parts to the U.S.

Imports declined after two consecutive months of increases. Autos and parts (-5.8%) declined, offsetting two strong months during which the category rose more than 10%. Other transport equipment imports also pulled back, down 3.9% in April, after three consecutive monthly gains. A similar story emerged for consumer goods imports (-4.9%) with the pull-back appearing to be related to past strength.

Canada's merchandise trade surplus with the U.S. widened for the first time in six months, nearly doubling from $2.0bn to $3.6bn in April on higher crude and bitumen exports and lower auto imports.

Key Implications

This was a solid report all things considered, with a good showing for exports highlighting the improving global demand. At the same time, the pull-back in imports appears more related to unsustainable gains in previous months than a beginning of a worrying trend.

The figures provide further evidence that after some softness in the first quarter, growth in the second quarter has rebounded, with our current tracking pointing to a near-3% pace.

Despite the good monthly print Canadian exporters are in for a rough ride in the coming months, and perhaps quarters. The recently imposed tariffs on aluminum and steel, together with retaliatory Canadian tariffs, will likely hold back movement of metals and metal products across the border and be a drag on economic activity – particularly in Quebec and Ontario. The tariffs also throw a wrench into the already difficult NAFTA negotiations, with any agreement looking less likely over the near-term – something that's not going to do anything for business confidence on either side of the border.

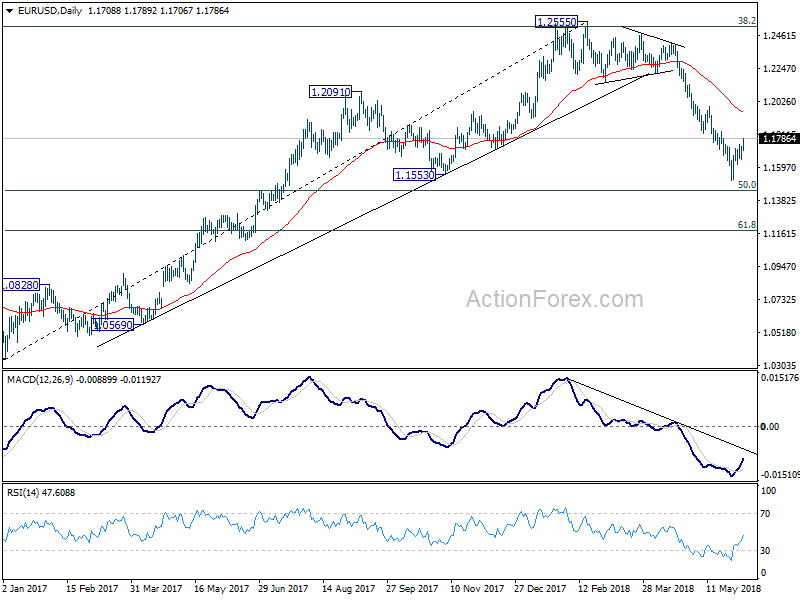

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1668; (P) 1.1701 (R1) 1.1749; More.....

EUR/USD's rebound from 1.1509 extends higher today and further rise would be seen. But still, it's seen as a corrective move. Hence, upside should be limited by 1.1822/1995 resistance zone to bring fall resumption eventually. On the downside, below 1.1651 minor support will bring retest of 1.1509 low first. Break will resume the decline from 1.2555 and target 50% retracement of 1.0339 to 1.2555 at 1.1447. Break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

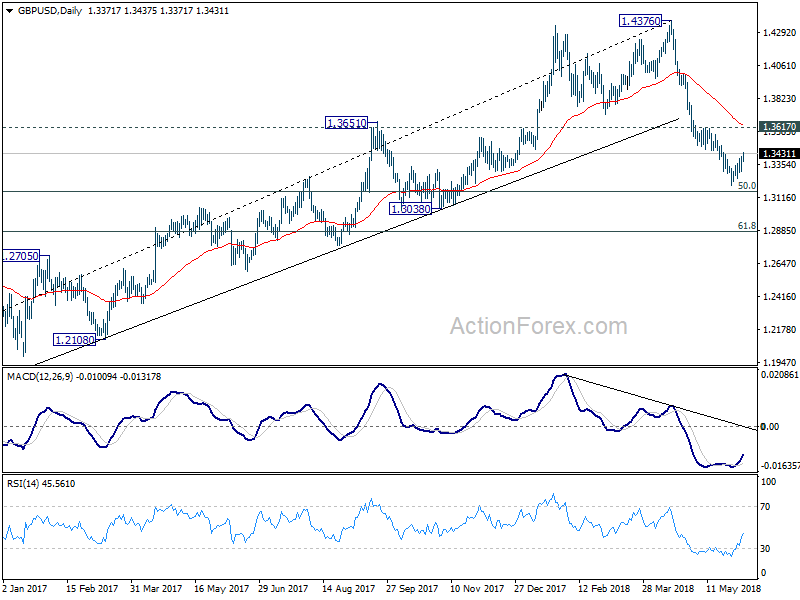

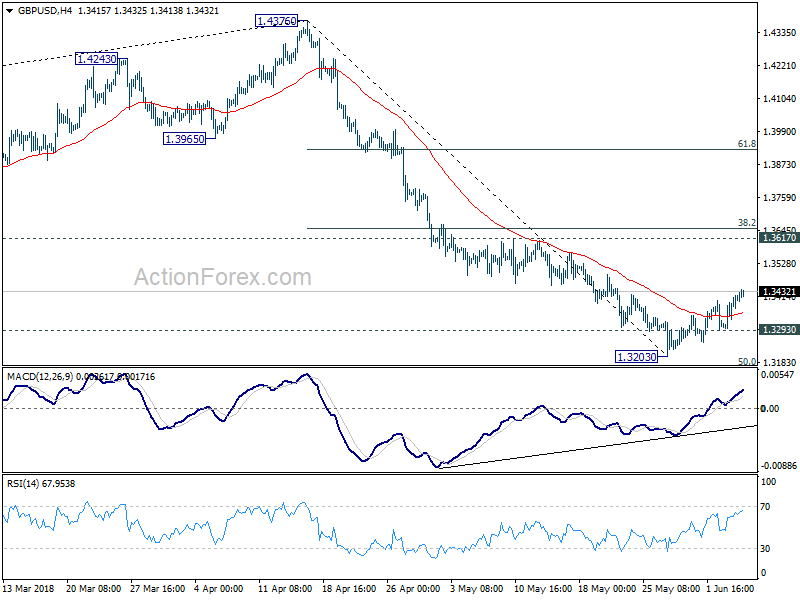

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3328; (P) 1.3369; (R1) 1.3436; More...

GBP/USD's rebound from 1.3203 is still in progress and further rise could be seen.. But it's seen as a correction and therefore, upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3293 minor support will likely resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3648) holds, even in case of strong rebound.