Sample Category Title

Yen Staying Weak on Solid Risk Appetite, Dollar Follows

Japanese Yen is trying to recover in Asian session today but remains the weakest one for the week. Risk appetites have been be strong as risk of trade war is shrugged off by investors. DOW rose 346.41 pts or 1.40% to 25146.39. S&P 500 rose 023.55 pts or 0.86% to 2772.35. NASDAQ gained 51.38 pts or 0.67% to 7689.24. That was also a record close in NASDAQ. At the time of writing, Nikkei is up 0.84% while HSI is up 0.55%.

10 year yield also closed up 0.056 to 2.975 and is on track to 3.000 handle again. But Dollar lagged behind and continues to trade as the second weakest for the week, just next to slightly better than Yen. Euro remains the strongest one for the week as ECB is preparing to debate end of QE at next week's meeting. Australia Dollar follow as the second strongest for the week.

The economic calendar is rather light today and markets should continue to trade with the current theme. Focuses will more be on trade as G7 summit in Canada on June 8-9 looms.

French Macron and Canadian Trudeau united on strong multilateralism

French President Emmanuel Macron and Canadian Prime Minister Justin Trudeau expressed their unified stance on the push for "strong multilateralism" after meeting in Ottawa yesterday, head of the G7 summit. In a joint statement, they pledged to "support a strong, responsible, transparent multilateralism to face the global challenges."

Macon hailed the meeting as "an opportunity to talk about the relations between Canada and France that are going very well, but also to highlight the challenges that we are going to have around the G7 table, and to make sure we are aligned."

The G7 meeting is set to be a confrontation between G6 versus the US on a range of issues, in particular, the US steel and aluminum tariffs on its closest allies. Trudeau said there will be " frank and sometimes difficult discussions around the G7 table, particularly with the US president on tariffs."

German Merkel hints at no joint G6+1 statement

German Chancellor Angela Merkel warned yesterday that there will be difficult discussions at the G7 summit in Canada. She told the parliament that "it is apparent that we have a serious problem with multilateral agreements here, and so there will be contentious discussions." She, though, pledged to go into the meeting with "goodwill".

But Merkel also emphasized that there "must not be a compromise for the sake of a compromise" and there was "no sense in papering over divisions." That's taken as a sign of risk that G7 summit could end without a joint statement first ever, as US will likely clash with all other G6 nations, at least on trade.

Meanwhile, it's reported that Macron has warned the US that he will not sign a joint statement out of the G7 summit if there is no progress on tariffs, Iran nuclear deal and the Paris climate accord.

On the data front

Australia trade surplus narrowed to AUD 0.98B in April versus expectation of AUD 1.03B. Japan leading indicator rose to 105.6 in April. Swiss will release unemployment rate and foreign currency reserves today. Germany will release factor orders while Eurozone will release Q1 GDP final. US will release initial jobless claims later in the day.

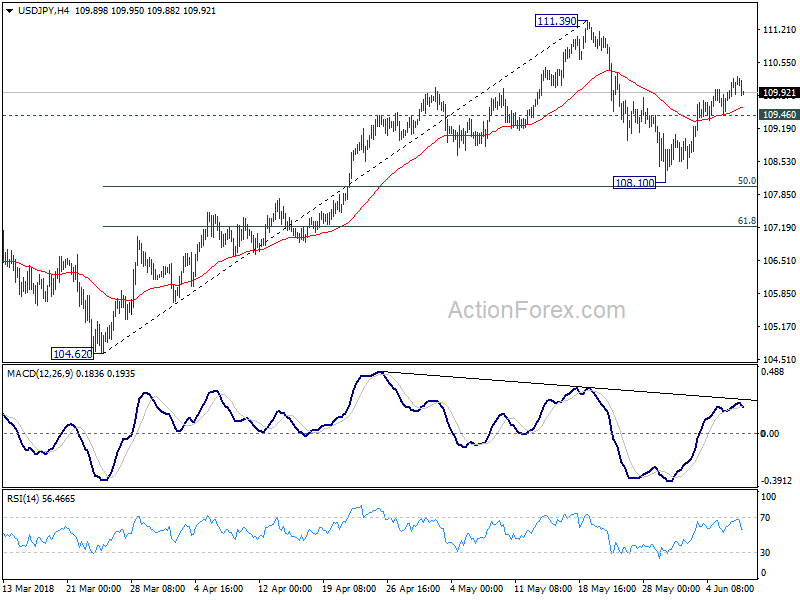

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.88; (P) 110.08; (R1) 110.38; More...

USD/JPY lost some upside momentum after hitting 110.26. But still, rebound from 108.10 is expected to continue with 109.46 minor support intact. Further rally would be seen back to retest 111.39 resistance. Break will resume the rebound from 104.62 and target a test on 114.73 key resistance level. However, on the downside, below 109.36 minor support will delay the bullish case and turn bias to the downside for 108.10 support again.

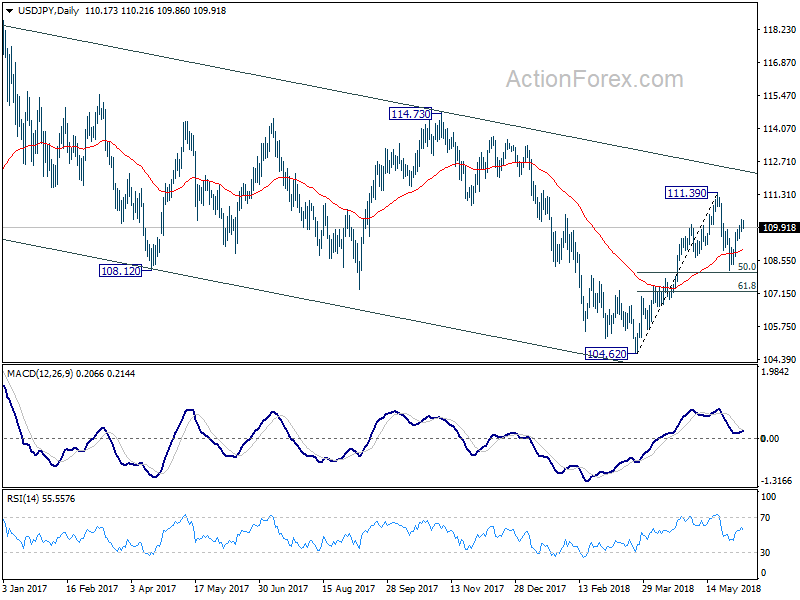

In the bigger picture, at this point , we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | Trade Balance (AUD) Apr | 0.98B | 1.03B | 1.53B | 1.73B |

| 5:00 | JPY | Leading Index CI Apr P | 105.6 | 105.6 | 104.4 | |

| 5:45 | CHF | Unemployment Rate May | 2.60% | 2.70% | ||

| 6:00 | EUR | German Factory Orders M/M Apr | 0.70% | -0.90% | ||

| 7:00 | CHF | Foreign Currency Reserves (CHF) May | 757B | |||

| 7:30 | GBP | Halifax House Prices M/M May | 1.10% | -3.10% | ||

| 9:00 | EUR | Eurozone GDP Q/Q Q1 F | 0.40% | 0.40% | ||

| 12:30 | USD | Initial Jobless Claims (2 JUN) | 225K | 221K | ||

| 14:30 | USD | Natural Gas Storage | 96B |

NASDAQ hit record while Dollar stays weak

US equities were strong over night while treasury yield also jumped. DOW rose 346.41 pts or 1.40% to 25146.39. S&P 500 rose 023.55 pts or 0.86% to 2772.35. NASDAQ gained 51.38 pts or 0.67% to 7689.24. 10 year yield also closed up 0.056 to 2.975 and is on track to 3.000 handle again. But Dollar lagged behind and continues to trade as the second weakest for the week, just next to slightly better than Yen.

NASDAQ's performance was impressive as it made new record high. For the near term, further rise is expected for sure. But it's possible that the consolidation pattern this year, from 7505.77 with five waves to 6026.97, is a triangle pattern in wave four position. If that's the case, rise from 6026.97 will be a strong but short lived thrust as the fifth wave to complete a larger up move. We'll see whether the scenario plays out like this. But 8000 handle will be a key to watch.

German Merkel hints at no joint G6+1 statement

German Chancellor Angela Merkel warned yesterday that there will be difficult discussions at the G7 summit in Canada. She told the parliament that "it is apparent that we have a serious problem with multilateral agreements here, and so there will be contentious discussions." She, though, pledged to go into the meeting with "goodwill".

But Merkel also emphasized that there "must not be a compromise for the sake of a compromise" and there was "no sense in papering over divisions." That's taken as a sign of risk that G7 summit could end without a joint statement first ever, as US will likely clash with all other G6 nations, at least on trade.

Meanwhile, it's reported that Macron has warned the US that he will not sign a joint statement out of the G7 summit if there is no progress on tariffs, Iran nuclear deal and the Paris climate accord.

French Macron and Canadian Trudeau united on strong multilateralism

French President Emmanuel Macron and Canadian Prime Minister Justin Trudeau expressed their unified stance on the push for "strong multilateralism" after meeting in Ottawa yesterday, head of the G7 summit. In a joint statement, they pledged to "support a strong, responsible, transparent multilateralism to face the global challenges."

Macon hailed the meeting as "an opportunity to talk about the relations between Canada and France that are going very well, but also to highlight the challenges that we are going to have around the G7 table, and to make sure we are aligned."

The G7 meeting is set to be a confrontation between G6 versus the US on a range of issues, in particular, the US steel and aluminum tariffs on its closest allies. Trudeau said there will be " frank and sometimes difficult discussions around the G7 table, particularly with the US president on tariffs."

EUR/GBP Upsides Remain Capped Near 0.8800

Key Highlights

- The Euro remained confined in a broad range below the 0.8800 resistance against the British Pound.

- There is a major bearish trend line in place with resistance near 0.8800 on the 4-hours chart of EUR/GBP.

- On the downside, supports are seen near the 0.8720 and 0.8700 levels.

- Today in the Euro Zone, the GDP report for Q1 2018 will be released, which is forecasted to post an increase of 0.4% (QoQ).

EURGBP Technical Analysis

The Euro was rejected from the 0.8700 support recently and traded higher against the British Pound. The EUR/GBP pair gained traction and moved above the 0.8720 resistance.

However, the upside move was limited by the 0.8800 resistance. There is also a major bearish trend line in place with resistance near 0.8800 on the 4-hours chart of EUR/GBP.

It seems like there is a large consolidation phase forming around the 0.8720-40 zone. On the upside, a break and close above the 0.8800 resistance level is needed for more gains. A successful close above 0.8800 could open the doors for a push towards the 0.9000 level.

On the flip side, if there is a downside correction, the pair will most likely find support near the 0.8720 level. Below this, the 0.8700 level is a crucial support and a pivot level. Should there be a downside break below 0.8700, the pair may perhaps trade down sharply towards 0.8600.

Today, there is a major release in the Euro Zone as the GDP report for Q1 2018 will be released. If the actual result beats the forecast of +0.4%, the Euro may perhaps gain traction in the near term.

EUR/USD recently settled above the 1.1700 barrier, which could help the overall market sentiment for the Euro in the near term.

Economic Releases to Watch Today

- German Factory Orders for April 2018 (MoM) – Forecast +0.8%, versus -0.9% previous.

- Euro Zone Gross Domestic Product Q1 2018 (QoQ) – Forecast 0.4%, versus 0.4% previous.

- Euro Zone Gross Domestic Product Q1 2018 (YoY) – Forecast 2.5%, versus 2.5% previous.

- US Initial Jobless Claims – Forecast 225K, versus 221K previous.

Market Morning Briefing: Dollar Index Has Broken Below The 21 Days MA Near 93.68

STOCKS

Dow shows initial signal of a bullish breakout which if sustains could take it higher in the medium term. Dax is stable just now.

Asia Pac is up. Nikkei is trading at immediate resistance and could break on the upside while Shanghai is trading higher. Nifty is likely to move up.

Dow (25146.39, +1.40%) has broken above 25000 and could possibly move up above the interim resistance at 25250 also. This could be an indication of a sharp bullish break after a contracting zone (could be referred to as a triangle formation). The current rise, if continues could take the index towards 26000 in the coming sessions.

Dax (12830.07, +0.34%) looks a little dicey just now. Although there is some space on the upside towards 13000-13100, the index is unable to rise sharply and sustain at higher levels. While below 12900, the index could come down towards 12600 in the medium term.

Nikkei (22834.40, +0.92%) has also moved up and is trading just below trend resistance on the daily candles. If the resistance holds, the index could be pushed off towards 22400 again; else a sharp break on the upside could prove to be bullish for the medium term, thus also pulling up Dollar Yen to higher levels.

Shanghai (3121.58, +0.21%) is heading towards 3150 in the next few sessions. Watch price action near 3150. A break on the upside would be bullish else another dip back to 3050 is possible.

Nifty (10684.65, +0.86%) rose from 10550 support on the daily candles and while that holds, could move up to test 10750-10800 again on the upside. This could be the last leg of a near term rise within the 10550-10800 range. Thereafter a break on either side would set the direction for the long term.

COMMODITIES

Copper and Brent is bullish while WTI could see some pause or dip in the near term. Gold is stable and may not see much movement this week.

Buying momentum picked up after break of key levels yesterday in Copper as worries over supply lingered on disruptions in the mines at Chile and India. Copper (3.2754) has risen towards our expected 3.30 yesterday. 3.30-3.35 could be the near term targets for now.

WTI (64.96) is down from levels above 65 seen yesterday. 66 is an immediate support turned resistance and while the crude price remains below 66, it could attempt lower levels of 63.50-64.00 before attempting to move up again. Brent (75.67) on the other hand is trading slightly up. A rise towards 77 looks likely while above 74.

Gold (1297.15) is stable without any major movement. Trade within 1300-1280 is possible in the coming sessions.

FOREX

Dollar index (93.51) has broken below the 21 days MA near 93.68. It could either rise again from 93.3, or further below, from levels near 92.8. A break below 92.8 will make the Dollar Index bearish in the medium term.

Euro (1.1792): Euro has breached the 21 days MA near 1.175 and has already tested a high of 1.18. A breach of 1.181 could take it higher towards the 8 weeks MA near 1.19. A breach of 1.19, if it happens, should make the Euro bullish in the medium term.

Dollar Yen (109.96) is continuing its rise towards crucial long term resistance on weekly line chart near 111 (which could be tested next week). A test of 111 (max 112) should then produce a dip.

Euro Yen (129.66): As per our expectation yesterday, Euro Yen is testing crucial resistance level (seen on daily, 3 day and weekly candles) near 129.5-130.0. We had mentioned yesterday that it could dip from here; however, with Dollar Yen still bullish towards 111 and Euro showing some possibility of a further rise towards 1.19, Euro Yen could move higher to test 131.0-131.5 (higher resistance on weekly candles). A breach of 131.5 should make it bullish for the medium term.

Pound (1.3427): Pound has moved higher towards resistance on daily candles (near 1.345). It should dip after testing 1.345. However, a breach of that level could take it higher towards 1.355-1.360.

Dollar Rupee (66.92) : May test 66.80 today. Failure to rise above 67.00-10 by Friday can also make the Dollar vulnerable to a further drop towards 66.60-50 next week.

INTEREST RATES

Current US yields: US 10 Year (2.97%), 30 Year (3.12%), 5 Year (2.81%), 2 Year (2.52%)

The US 10 Year yield is seeing a rise from support on short term chart. As markets wait for the CPI data release and the FOMC meet next week, it might not see a test of 3% immediately. As mentioned yesterday, any sign of dovishness from the Fed next week could lead to another dip in US yields and bring into play the following support levels on medium term chart:

2.55% (10 Year), 2.9% (30 Year) and 2.2% (5 Year)

German 10 year yield (0.47%), as per expectation, has risen from support on short term chart and could move higher towards 0.55-0.60 by next week.

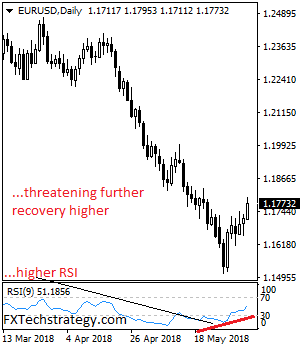

EURUSD Builds Up On Bull Pressure

EURUSD - The pair faces further recovery higher in the days ahead as it saw more bull pressure on Wednesday. On the upside, resistance comes in at 1.1800 level with a cut through here opening the door for more upside towards the 1.1850 level. Further up, resistance lies at the 1.1900 level where a break will expose the 1.1950 level. Conversely, support lies at the 1.1750 level where a violation will aim at the 1.1700 level. A break of here will aim at the 1.1650 level. Below here will open the door for more weakness towards the 1.1600. All in all, EURUSD faces further upside pressure on recovery.

US Equity Markets Defy Gravity

Equity Markets

US equity markets continue to defy gravity and extending the recent winning streak to four straight sessions. It was all about the financials as a series of coordinated hawkish comments from ECB members, that the end of QE will be top of the to-do list with some suggesting that the ECB could actually move ahead of the curve.

So as investors remain jittery over trade and tariff, higher Global bond yields on the hawkish ECB inference are driving financials higher. And while interest rates are usually a negative for equity markets, investors are viewing higher interest rates in a favourable light, reflective of surging economic growth and not as a buffer against inflation.

Oil Market

After yet another unexpected jump in domestic crude inventories, oil prices came off intersession highs with WTI taking another deep dive towards $64 per barrel only to retrace back to the critical $65.00 level in into the NY close.

I suspect there are two exogenous factors in play that are keeping oil prices bid on dips. One, China consumption remains exceptionally high, and the markets could be underestimating this demand component in the global supply and demand equation. Two, traders realise that price at the time of the Vienna meeting will have as much to do with OPEC supply rebalancing act as global supplies themselves. So oil traders continue to respect this $ 64-65 per barrel support level.

While oil prices may have seen their near-term peaks, it’s highly unlikely prices will collapse but rather OPEC, through gradual supply increases, will guide prices low enough so US consumers will not feel the pinch, yet remain high enough to benefit the industry going forward.

Gold Market

Gold prices have been very steady despite the lack of safe-haven demand. While haven flows are tepid around 1,300 gold continues to remain bid on the dip as traders know we are little more than a spark away from igniting another risk aversion free for all. Besides, traders are taking cues from the DXY index which is trading lower again as demand for the Greenback remains exceptionally sluggish this week. Not to mention there is growing consensus amongst currency traders that the USD may be topping out.

There are some significant events on the horizon none more so than the Trump-Kim summit which suggests trader’s angst will be running high as we approach June 12 and should attract some attention from gold hedgers.

But in general, as with most cross-asset classes, we remain in a wait and see mode ahead of the US Federal Reserve Board( Fed) and European Central Bank policy announcements next week. But since no one is really expecting a hawkish shift from the Fed, this to could prove to be a blessing for Gold bulls

G-10 Currency Market

EUR: The Euro has moved predictably higher as after ECB Preaet suggesting that a September taper is very much on the cares and surprising markets given the political turmoil in Italy and a weaker series of economic data release of late. But the ECB hawks are seizing the opportunity from last week’s uptick in EU inflation to push through the long-awaited pullback in Eurozone QE. And despite the markets tendency get overly giddy about a possible ECB policy shift, but the ever-present “Draghi Put” has traders not exactly tripping over themselves to get in front of this policy shift, but instead are conservatively positioning for a subtle ECB shift in guidance in June. But we could very well see a test of 1.1800 soon

AUD: Australia GDP recorded a small beat as had been widely expected. Still, with virtually zero rate hike expectations priced into the domestic STIRT curve, the Aussie extended it’s gain to six weeks highs as traders scrambled to cover short positions. Also, the Aussie was then further supported by a firm global equities market performance auguring well for FX high beta like the Aussie dollar. Growth assets and hard commodities are performing well in this environment.

Asian currencies

Asian currencies have been benefiting from a sluggish USD, robust equity sentiment and all the positivity emanating from the planned US-North Korea summit next week.

KRW: The Won continues to attract attention to strong equity inflow.

THB: With the USD momentum waning there has been a gradual reduction of bearish regional bets. But given the lack of tier one economic data and the fed blackout period, the dollar is finding little support so far, this week.

INR: A slightly weaker USD, lower oil prices and the RBI raised its repo rate by 25bps to 6.25% has the USDINR trading below the 67 level this morning. The RBI rate hike was widely priced and was discounted as more or less a one and done and not a hawkish rate hike, so external factor like oil and US yields will continue to drive sentiment.

IDR: Yield in Asia continue to march higher adjusting to returns in both Europe and the US supporting the typical low yields while the high yielders like IDR and INR continue to benefit from better global risk sentiment

Malaysia

On the central bank changes, while Ibrahim was instrumental in defeating the NDF markets, so with the changing of the guard at BNM NDF’s have been a conversation amongst Singapore traders. Will the new governor be more open to NDF?? Unlikely as one of the deputy governors will take charge and I think it’s safe to say that PM Mahathir is not a big fan of currency traders either while during the Asia crisis he labelled currency traders as “unscrupulous profiteers” in an “immoral” line of work.

Possible policy shifts?? The economy is doing very well domestically, and external trade is robust. So, if it is not broke. Don’t fix it. Inflation is running well below target, so BNM does not need to raise rates.

Appointing a deputy governor suggests the status quo. Both candidates Nor Shamsiah or Sukhdev Singh are excellent choices, and the market will be happy that the Central Bank policy will remain in skilful hands.

MYR: Continues to play second fiddle in regional sentiment as the fiscal policy overhang continues to weigh on sentiment

Slight Gains For Gold Against Sluggish Greenback

Gold has posted slight gains in the Wednesday session. In the North American session, the spot price for one ounce of gold is $1299.37, up 0.24% on the day. On the release front, there are no major US events. We’ll get a look at unemployment claims on Wednesday.

As fears of a global trade war increase, gold could be the big winner if the world’s major economies don’t sit down and settle their disagreements, without resorting to stiff tariffs against their competitors. A major test for the world’s biggest economies will take place in Canada on June 8, as the G-7 leaders meet. Last week, finance ministers from six members of the G-7 were united in their criticism of US Treasury Secretary Steve Mnuchin over the brewing trade war. The trouble started last week, when the Trump administration slapped stiff tariffs on Canada, Mexico and the European Union. This resulted in promises of retaliation, and Canada and Mexico have already announced duties on U.S products. The trade spat is sure to dominate the summit, but will the leaders resolve matters? If not, investors could head for the hills and dump their riskier assets in favor of save-haven gold.

After weeks of speculation, the much-anticipated summit between the US President Trump and North Korean President Kim Jong-un is back on. The two leaders will meet on June 12 in Singapore, marking the first ever face-to-face meeting between leaders of the U.S and North Korea. Trump has tried to lower expectations, saying the sides are unlikely to reach an agreement over North Korea relinquishing its nuclear weapons. Still, the fact that the two leaders are meeting is a sign that significant progress is being made in the long-standing dispute between the two Koreas.

Pound Slightly Higher, Investors Look For Economic Cues

The British pound has posted slight gains on Wednesday, continuing the upward trend which marked the Tuesday session. In North American trade, GBP/USD is trading at 1.3409, up 0.11% on the day. On the release front, there are no major events out of the U.S or Britain. On Thursday, the U.K releases Halifax HPI and the U.S publishes unemployment claims.

PMI reports, which provides a barometer of the health of the British economy, were positive in May. Last week, Manufacturing PMI rose to 54.4, above the estimate of 53.5 points. Construction PMI remained unchanged at 52.5, beating the estimate of 52.0 points. Services PMI also pointed upwards and hit a 3-month high. The indicator improved to 54.0, which beat the forecast of 52.9 points. All three indicators continue to point to expansion at a crucial time, as the U.K continues to grapple with Brexit, which has raised considerable apprehension about how the economy will fare when the U.K departs the European Union. With the services, construction and manufacturing sectors generally in good shape, sentiment towards the British pound should remain positive.

Canada is the host of the G-7 meetings this year, and finance ministers from six countries were united in their criticism of US Treasury Secretary Steve Mnuchin over a brewing trade war. Last week, the Trump administration imposed stiff tariffs on Canada, Mexico and the European Union. Prime Minister May expressed her disappointment with the U.S move in a conversation with President Trump. Canada will host the G-7 leaders on June 8, with the U.S tariffs sure to be high on the agenda. If the trade battle escalates, the result will be a lose-lose and thousands of British jobs could be at stake.

After weeks of speculation, the much-anticipated summit between the US President Trump and North Korean President Kim Jong-un is back on. The two leaders will meet on June 12 in Singapore, marking the first ever face-to-face meeting between leaders of the U.S and North Korea. Trump has tried to lower expectations, saying the sides are unlikely to reach an agreement on North Korea relinquishing its nuclear weapons. Still, the fact that the two leaders are meeting is a sign that significant progress is being made in the long-standing dispute between the two Koreas.