Sample Category Title

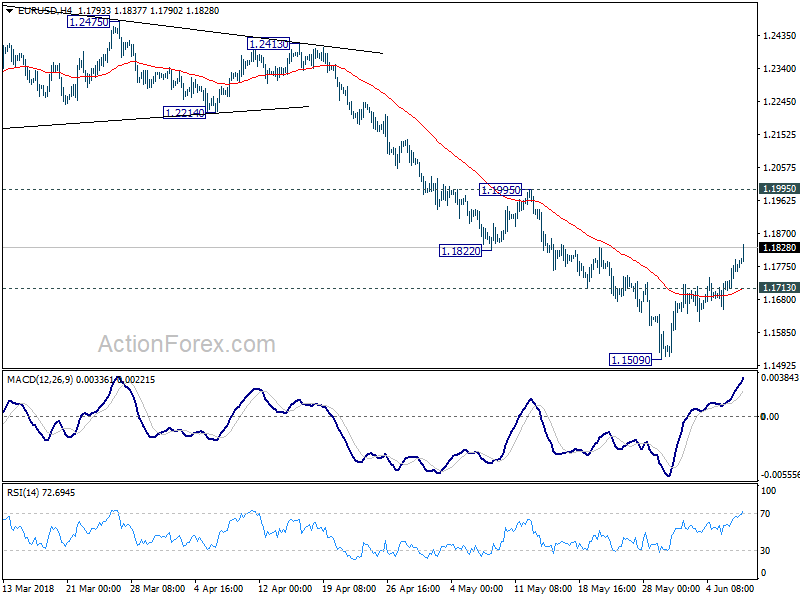

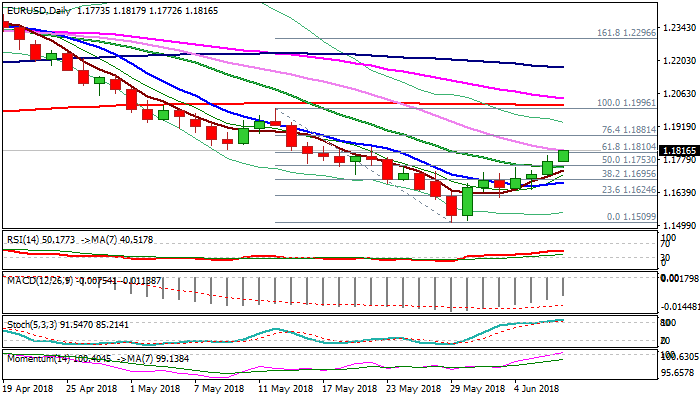

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1727; (P) 1.1761 (R1) 1.1811; More.....

Intraday bias in EUR/USD is mildly on the upside as rebound from 1.1509 extends. Still, such rise is seen as a corrective move. And we'd expect upside to be limited by 1.1995 resistance to bring fall resumption eventually. On the downside, break of 1.1713 minor support will likely resume larger fall from 1.2555 through 1.1509 to 50% retracement of 1.0339 to 1.2555 at 1.1447.

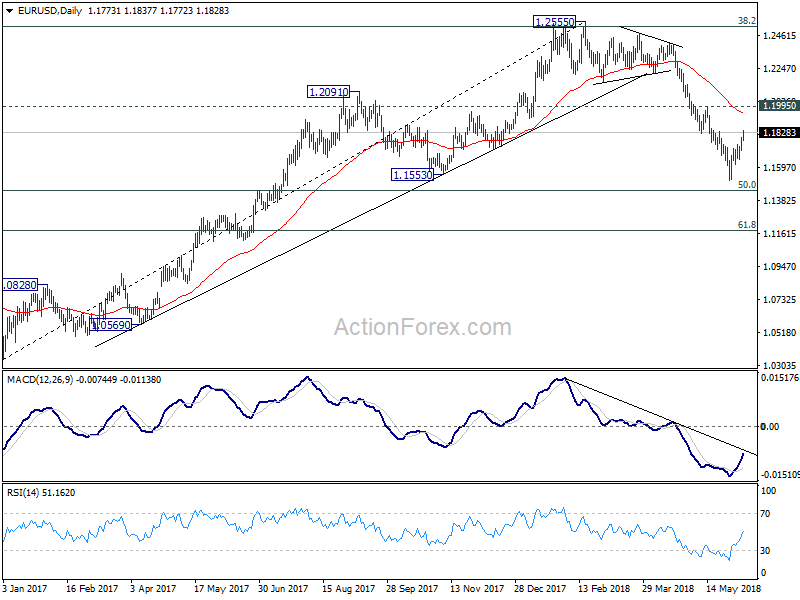

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

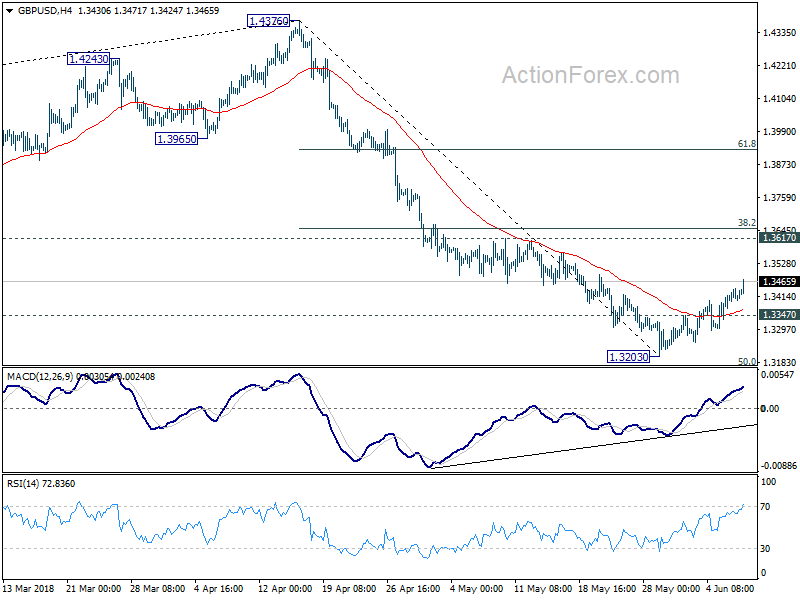

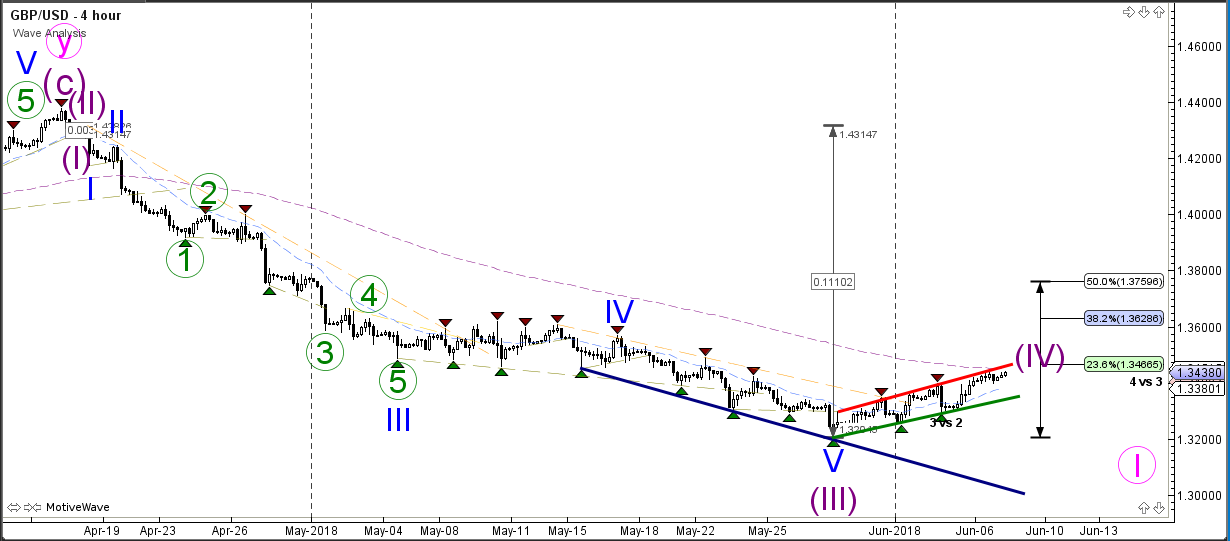

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3380; (P) 1.3412; (R1) 1.3446; More...

Intraday bias in GBP/USD remains on the upside as the corrective rebound from 1.3203 extends. Further rally could be seen but as it's seen as a correction, upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3347 minor support will likely resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

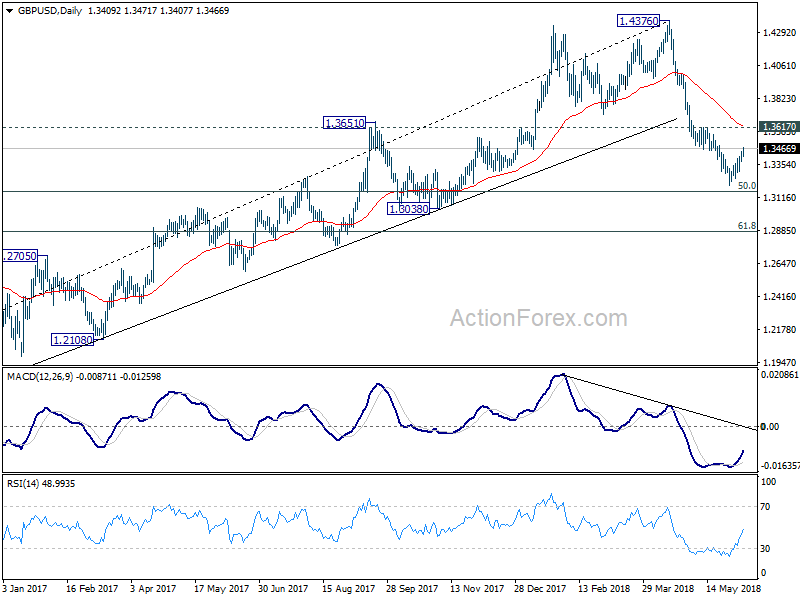

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3648) holds, even in case of strong rebound.

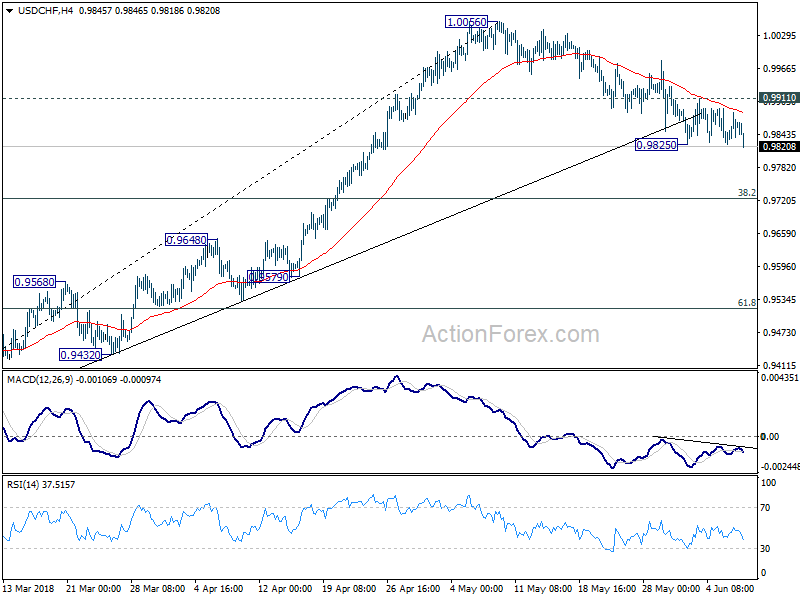

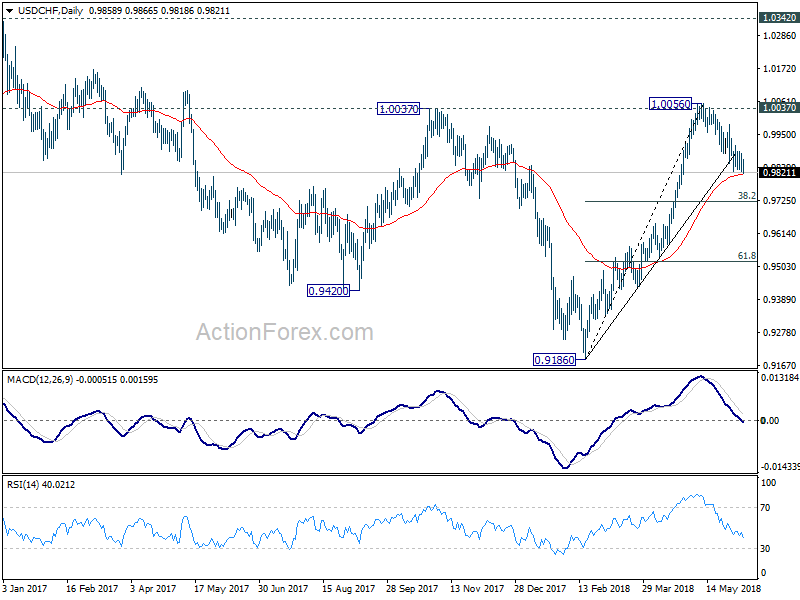

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9838; (P) 0.9863; (R1) 0.9890; More...

USD/CHF's break of 0.9825 finally indicates resumption of the correction decline from 1.0056. As it's seen as correcting rise from 0.9186, intraday bias is now on the downside for 0.9724 fibonacci level. On the upside, break of 0.9911 minor resistance is needed to indicate completion of the fall. Otherwise, near term outlook will remain mildly bearish in case of recovery.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds. However, sustained break of 0.9724 will dampen this bullish view and would at least bring deeper fall to 61.8% retracement at 0.9518.

Eurozone GDP Is Expected To Soften Today Following Weak Q1 Economic Data

At 08:30 GMT, UK Halifax House Price Index (MoM) (May) is expected to be 2.0% against -3.1% previously. UK Halifax House Price Index (3m/YoY) (May) is expected to be 2.4% against 2.2% previously. This data has been declining since hitting a high of 3.9% in June 2014 and is expected to rebound from a multi-year low last month. GBP crosses can be affected by this data release.

At 09:00 GMT, Eurozone Gross Domestic Product s.a. (QoQ) (Q1) is expected to be 0.4%from 0.4% previously. Gross Domestic Product s.a. (YoY) (Q41is expected to be 2.5% from 2.5% previously. This data can see moves in the EUR currency crosses. The QoQ number has been holding steady around 0.6% for 2017 but this is expected to drop down to 0.4% showing a decline in growth across the Eurozone. The YoY number is also expected to drop down to 2.5% after weakening Eurozone data.

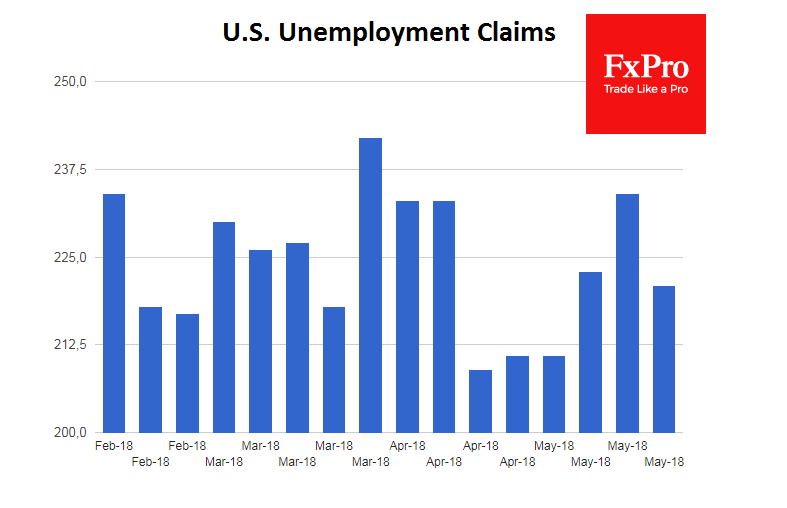

At 12:30 GMT, US Continuing Jobless Claims (May 25) is expected to be 1.738M against 1.726M previously. Initial Jobless Claims (Jun 1) is expected to come in at 225K against 221K previously. This data is showing an increase in the number of people who are jobless. USD crosses may be heavily traded as a result of these data points.

At 15:00 GMT, UK MPC Member Ramsden is expected to speak at the Barclays Inflation Conference, in London. GBP crosses may be affected by any comments made.

At 15:15 GMT, Bank of Canada Governor Poloz is due to hold a press conference about the Financial System Review, in Ottawa. CAD pairs can be influenced by comments made

At 19:00 GMT, Consumer Credit Change (Apr) is expected to come in at $13.75B from a previous reading of $11.62B. This data shows that consumer credit has been falling in recent months and has come in under expectations for four months in a row. The expectation is again for an increase in the number today. Increases in this metric are a sign of consumer confidence as consumers take on more debt and lenders feel confident issuing loans. USD pairs can be moved by this data.

Markets In Risk On Mode Ahead Of The G7 Meeting Tomorrow

While the 'Risk On' rally continues in global stocks the Chinese markets are lagging behind over fears of trade tensions and high levels of maturing debt. In stark contrast US markets were higher adding to the gains made in the Asian session over the last four days. European markets are trying to make up lost ground but progress is slow compared to global counterparts. Oil has stabilised this week after its fall from $72.80 and is encamped at the $65.00 level. The USD is softer against most other currencies bar the AUD with the pair down -0.09% to 0.76604. Tomorrow the G7 meeting will begin which are set to dominate headlines into the weekend.

US Nonfarm Productivity (Q1) came in at 0.4% against an expected 0.6% from 0.7% previously, showing efficiency slipping and ultimately upward pressure on inflation. Unit Labour Costs (Q1) were 2.9% against an expected 2.8% from 2.7% prior, showing what has become a seasonal increase expected in this metric but these cost can be passed onto consumers. There is growing evidence, albeit anecdotal that labour costs are increasing as workers are becoming harder to find. Trade Balance (Apr) was $-46.2B versus an expected $-49.0B against a previous $-49.0B which was revised up to $-47.2B, rebounding off the low levels, at -57.6%, not previously seen since 2008. EURUSD fell from 1.17793 to 1.17614 following this data release.

Canadian International Merchandise Trade (Apr) was $-1.90B versus an expected $-3.40B against $-4.14B previously which was revised up to $-3.93B. This fell to match the low of November 2016 last month and it is now off the lows, but still at very low levels. USDCAD fell from 1.29090 to 1.28577 following this data release. Ivey Purchasing Managers Index s.a. (May) was 62.5 against an expected 69.7 from a previous 71.5. Ivey Purchasing Managers Index (May) was 69.5 against 70.4 previously. The data came in under last month’s reading which was the highest since 2011 and greatly exceeded expectations. This data is showing robust growth, continuing one of the longest positive runs with over 20 months above 50.0 and is now back into the previous range. USDCAD moved higher from 1.28615 to close the session at 1.29615 after the data release.

EURUSD is up 0.27% overnight, trading around 1.18047.

USDJPY is down -0.21% in the early session, trading at around 109.946

GBPUSD is up 0.18% this morning trading around 1.34345.

Gold is up 0.03% in early morning trading at around $1,296.88

WTI is down -0.22% this morning, trading around $65.17

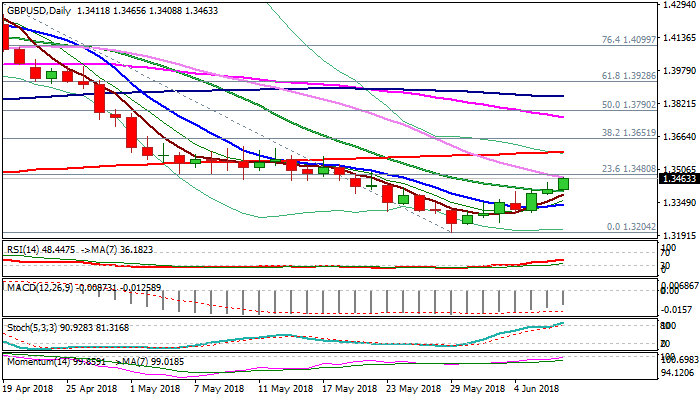

GBPUSD Outlook: Break Above Falling 30SMA Will Generate Next Bullish Signal For Extension Towards 200SMA

Cable extends higher in early European trading on Thursday and pressures falling 30SMA (1.3467) after bullish signal was generated Wednesday’s close above pivotal 1.3401/10 barriers (20SMA/50% retracement of 1.3617/1.3204 bear leg).

Strong momentum continues to support rally, but strongly overbought slow stochastic warns of corrective action in the near-term.

Bulls need close above 30SMA to further strengthen for eventual attack at 200SMA (1.3583), violation of which would generate stronger bullish signal for reversal.

Broken 20SMA (1.3401) is expected to ideally keep the downside protected and keep bulls intact.

Res: 1.3480, 1.3520, 1.3588, 1.3617

Sup: 1.3401, 1.3384, 1.3362, 1.3337

EURUSD Outlook – Bulls Probe Through Key Fibo/30SMA Barriers, Strong Bullish Signal Seen On Firm Break

The Euro maintains bullish tone on Thursday and tests strong Fibo barrier at 1.1810 (Fibo 61.8% of 1.1996/1.1509 bear-leg, also pressuring falling 30SMA (1.1817) which reinforces resistance.

Bulls were boosted by positive signal generated on Wednesday’s close above 20SMA (1.1749) and double-Fibonacci barrier at 1.1753/56 (50% retracement of 1.1996/1.1509 and 23.6% of larger 1.2555/1.1509 fall).

North-heading momentum enters positive territory with 5/10/20 SMA’s in bullish setup, maintaining positive environment for further gains.

Formation of reversal pattern above weekly Ichimoku cloud top also underpins the advance.

Sustained break above 1.1810/17 pivots would generate fresh bullish signal and open targets at 1.1881 (Fibo 76.4% of 1.1996/1.1509) and 1.1909 (Fibo 38.2% of 1.2555/1.1509).

Broken 20SMA marks solid support (reinforced by rising 5SMA which is looking to form a bull-cross) which is expected to protect the downside.

EU GDP data are key event of the European session today ( annualized Q1 f/c 2.5% vs 2.5% prev).

Res: 1.1830, 1.1881, 1.1909, 1.1996

Sup: 1.1772, 1.1750, 1.1733, 1.1683

Global Core Bonds Lost Significant Ground Yesterday

Markets

Global core bonds lost significant ground yesterday with German Bunds underperforming US Treasuries. The down leg started on Tuesday evening following rumours that next week’s ECB meeting is a “live” one. Comments by several ECB governors, including chief economist Praet, nurtured expectations further yesterday morning. Risks increase that the ECB will effectively announce a new forward guidance for APP already next week instead of issuing the “traditional” preannouncement first. More specifically, we expect APP to be tapered out by €10/bn month in Q4 2018. German yields rose by 5.1 bps (2-yr) to 9.6 bps (10-yr) on a daily basis. Changes on the US curve varied between +2.4 bps (2-yr) and +4.4 bps (10-yr). 10-yr yield spread changes vs Germany closed nearly unchanged with Italy underperforming (+5 bps). The new government is expected to ruffle quite some European feathers soon and the ECB’s normalization process spells double trouble. A short squeeze propelled the euro higher yesterday. EUR/USD moved from the low 1.17 to the high 1.17 area, fending off several other factors working in the opposite direction (Italy, strong US eco data, approaching Fed meeting). EUR/GBP followed the move higher in EUR/USD with the pair moving from 0.8740 towards 0.8780.

Most Asian stock markets trade positive overnight, in line with WS’s performance. Chinese bourses underperform (slight losses). Other risk indicators, the US Note future and USD/JPY, send a different signal, suggesting a more neutral opening for the Bund. Today’s eco calendar remains rather dull with EMU Q1 GDP details and US weekly jobless claims. The latter are expected to continue to hover near all-time highs. Overall, we expect next week’s ECB and Fed policy meetings to dominate trading. The former could make the next move in its normalization process while the latter could step up the tightening cycle. Both developments play in the disadvantage of core bonds. The German 10-yr yield is closing in on 0.5% resistance while the US 10-yr yield is bound for >3% levels. We hold our negative bias for core bonds. We think peripheral bond markets will remain under pressure. A normalization of credit premiums was long overdue in these stretched markets. The ECB and Fed could keep EUR/USD in check (ST) within the 1.1540-1.1830 trading range. Sterling remains locked in the tight 0.87-0.88 corridor.

News Headlines

French President Emmanuel Macron has stated that he will not sign a joint statement at the G7 summit in Quebec of 8-9 June, unless progress is made on tariffs, the Iran nuclear deal and Paris climate accord. With his statements he joins German Chancellor Angela Merkel to challenge Trump on a number of current affairs at the summit later this week.

The Polish MPC has announced that it will keep borrowing costs unchanged. Governor Glapinski announced they will keep the benchmark at a record-low 1.5% and will ‘most probably’ maintain this level until the end of 2019. This is in contrast with Czech Republic and Romania, where monetary policy was tightened earlier this year.

Higher US yields and a stronger USD accelerate the sell-off in emerging markets currencies ahead of next week’s FED meeting, with the Brazilian Réal suffering the biggest loss. Domestic political issues (petrol strike) amplify the sell-off. Turkish Lire remains under pressure too. Turkish Central Bank meets today. Will they hike policy rates, like India did yesterday, to abate the pressure?

GBP/USD Bear Flag Completes Wave C At 1.35 Resistance

The GBP/USD is building a bear flag chart pattern within a wave 4 (purple) correction. The Fibonacci levels of wave 4 could act as resistance and a break below the channel could indicate the end of wave 4 and the start of wave 5. A break above the 50% makes a wave less likely.

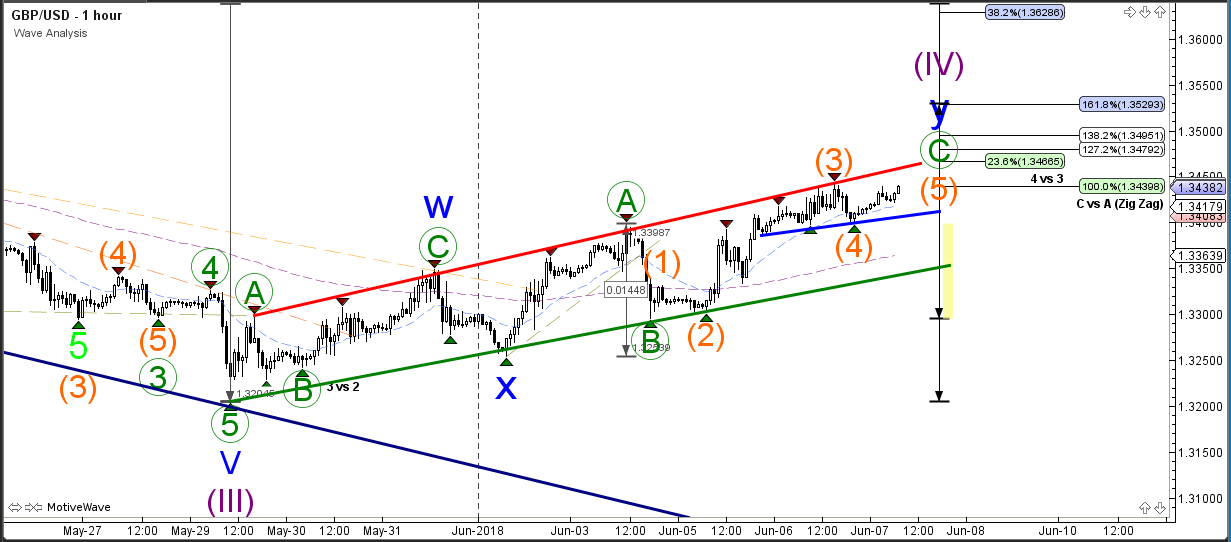

The GBP/USD is expanding the bullish wave 5 (green) after bouncing at support (blue). Price is now approaching a confluence of resistance at the Fibonacci targets and trend channel top, which offers a new bounce or break zone.

EURUSD Wave C Momentum Breaks 1.1750 Resistance

The EUR/USD broke above the key 1.1750 resistance and 23.6% Fibonacci retracement level and is now moving up towards the next 38.2% Fib.

The EUR/USD is probably building a bullish wave 4 pattern which is expected to turn back down at or below the 50% Fib. A break above the 50% indicates that another wave count is more likely.

The EUR/USD made a bullish breakout yesterday and is building a potential wave C (blue). The ABC zigzag could complete a larger WXY correction within wave 4.