Sample Category Title

DAX Steady, Euro Retail PMI Pushes Past 50

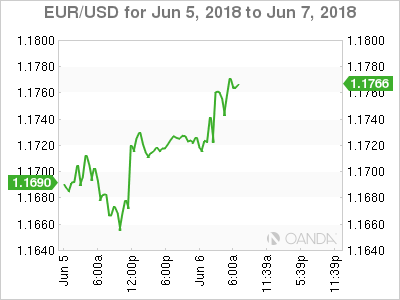

The DAX has posted gains in the Wednesday session. Currently, the DAX is at 12,818 up 0.25% on the day. In economic news, there is just one event on the schedule. Eurozone Retail PMI improved to 51.7 points, pointing to weak expansion. On Tuesday, Germany releases Factory Orders and the eurozone publishes Revised GDP.

The eurozone economy has been performing well and inflation continues to move higher, raising the question of what’s next for the ECB stimulus program. The ECB currently buys EUR 30 billion each month, and the scheme is scheduled to end in September. The bank has extended the program in the past, but stronger economic conditions have strengthened the case to finally end stimulus. The ECB has not formally discussed the issue, leaving the markets to hunt for any clues about the bank’s plans. On Wednesday, ECB chief Peter Praet said that the ECB would commence discussing the issue next week, when the Governing Council meets in Riga, Latvia. Many policymakers favor a gradual reduction in stimulus over several months, rather than completely turning off the tap in September. If the ECB makes any announcements regarding further tapering, we could see some volatility from European the stock markets.

The on-again-off-again Korea nuclear summit is back on, complete with a starting time. The much-heralded meeting between President Trump and President Kim Jong-un will take place in Singapore on June 12, at 9:00 AM sharp. The summit will mark the face ever face-to-face meeting between leaders of the U.S and North Korea, but Trump has tried to lower expectations, saying that he didn’t expect the sides to sign an agreement. Rather, the meeting would mark the start of a process. North Korea is unlikely to agree to denuclearization, but the fact that the two sides are talking is likely to continue boosting the stock markets.

Forex Analysis: EURUSD Wave Analysis

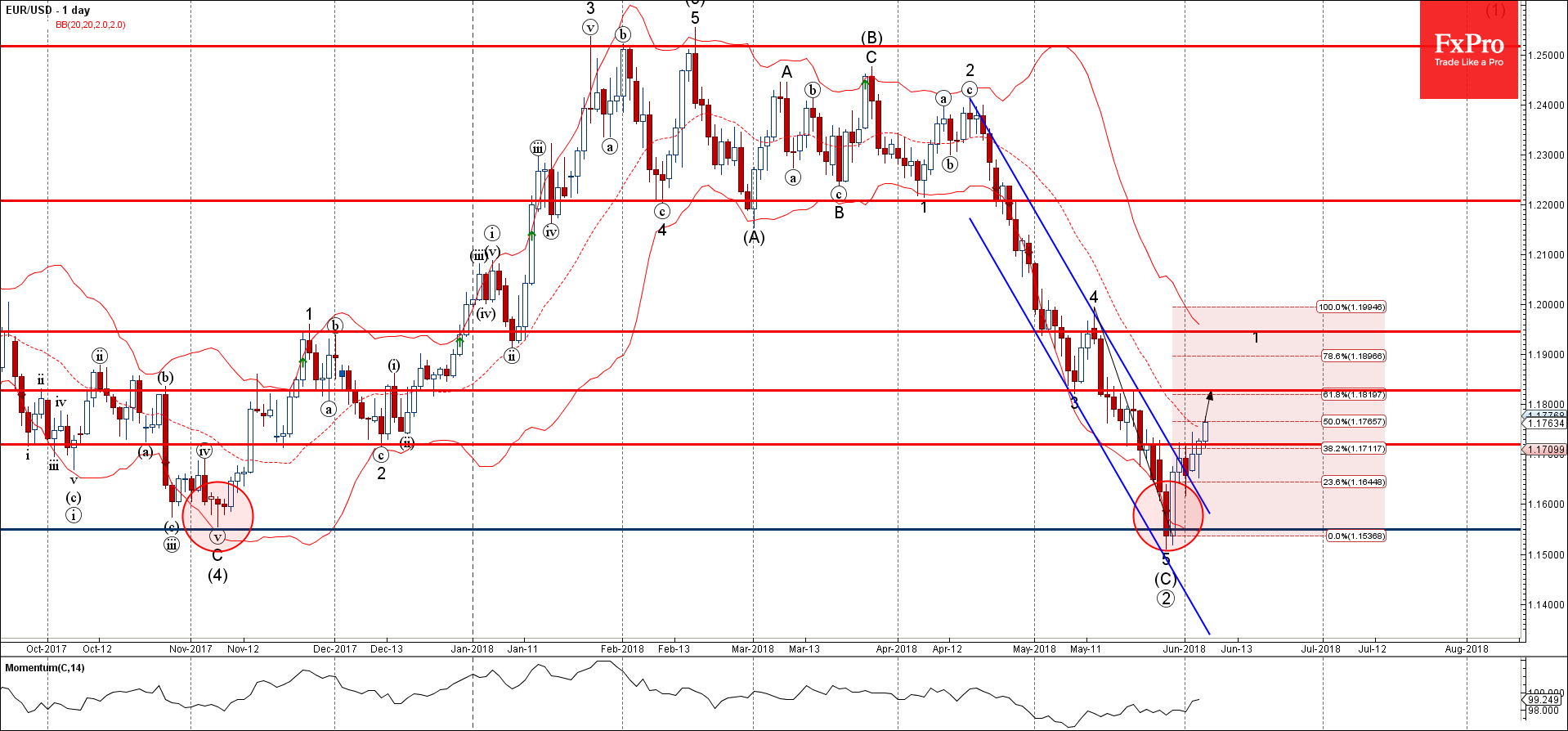

EUR/USD broke resistance zone

Further gains are likely

EUR/USD recently broke the resistance zone lying between the resistance level 1.1720, resistance trendline of the daily down channel from April and the 38.2% Fibonacci correction of the previous downward impulse from the middle of April.

The breakout of this resistance zone should strengthen the active primary impulse wave ③, which started earlier from the long-term support level 1.1550.

With the rising daily Momentum, EUR/USD is expected to rise further and re-test the next resistance level 1.1830 (former support level which stopped the previous minor impulse wave 3 in May).

ECB Out In Force To Defend Its Inflation Outlook, RBI Delivers A Surprise Rate Hike

ECB members out in force (Praet, Hansson, Weidmann, Knot) ahead of the silent period before next week’s decision to reiterate view that inflation would move towards the target

India Central Bank delivers a surprise rate hike

Asia:

- Australia Q1 GDP Q/Q: 1.0% v 0.9%e; Y/Y: 3.1% v 2.8%e (entered its 27th year of growth without a recession)

- Japan wage data highlights that consumer spending could lose momentum (Real Cash Earnings Y/Y: 0.0% v 0.1%e)

Europe:

- ECB reportedly ready to discuss QE exit policy at June 14th meeting. Officials could make a public statement on QE exit strategy at the June 14th MPC meeting

- Italy PM Conte wins Senate confidence vote, as expected (Passed his parliamentary 1st hurdle)

- Italy PM Conte: Euro exit has never been discussed by the govt

- Labour Party reportedly plans to announce shift towards soft Brexit. Labour said to commit to retaining the main elements of the UK’s relationship with the EU after Brexit. The move designed to unite the party and would signal it wanted the softest possible Brexit

Americas:

- US Treasury Sec Mnuchin said to urge Trump to give Canada exemption from tariffs

Energy:

- IAEA confirmed Iran govt delivered letter that described its plans for uranium enrichment. Preparing for possible increase of enrichment capacity if deal failed

Economic Data:

- (IE) Ireland May Services PMI: 59.3 v 58.4 prior, Composite PMI: 57.7 v 57.6 prior

- (NO) Norway Q1 Current Account (NOK): 61.0B v 35.0B prior

- (ES) Spain Apr Industrial Output NSA Y/Y: +11.0% v -3.7% prior; Industrial Output SA Y/Y: 1.9% v 5.1%e; Industrial Production M/M: -1.8% v -0.2%e

- (HU) Hungary Apr Industrial Production M/M: +0.2% v -0.7% prior; Y/Y: 2.9% v 3.8%e

- (CZ) Czech Apr National Trade Balance (CZK): 15.8B v 13.0Be

- (CZ) Czech Apr Industrial Output Y/Y: 5.5% v 9.0%e; Construction Output Y/Y: 7.7%v 0.4% prior

- (CH) Swiss May CPI M/M: 0.4% v 0.3%e; Y/Y: 1.0% v 0.9%e

- (CH) Swiss May CPI EU Harmonized M/M: 0.4% v 0.2% prior; Y/Y: 1.0% v 0.4% prior

- (DE) Germany May Construction PMI: 53.9 v 50.9 prior

- (EU) Euro Zone May Retail PMI: 51.7v 48.6 prior

- (DE) Germany May Retail PMI: 55.5 v 51.0 prior

- (FR) France May Retail PMI: 50.7 v 50.1 prior

- (IT) Italy May Retail PMI: 47.3 v 42.7 prior

- (IN) India Central Bank (RBI) raised its Repurchase Rate by 25bps to 6.25%, not expected

- (IS) Iceland May Preliminary Trade Balance (ISK): -12.8B v -13.4B prior

Fixed Income Issuance:

- (DK) Denmark sold total DKK2.28B in 2020 and 2027 DGB Bonds

- (IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 +0.1% at 387.2, FTSE +0.3% at 7710, DAX +0.4% at 12843, CAC-40 +0.1% at 5467, IBEX-35 +0.2% at 9707, FTSE MIB -1.4% at 21463, SMI +0.2% at 8558, S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European Indices trade mixed coming off the earlier highs tracking the slight pullback in US futures. On the earnings front Voestalpine trades higher after beating on the top and bottom line, with gains also seen for WH Smith and Repsol following their update and outlook. RPC is a notable faller after a drop in Free cash flow; Workspace Group also declines following a secondary offering and results. On the M&A space Smurfit Kappa rises as International Paper confirms it's dropping it's pursuit of the company while BHP trades higher after reports its shale unit has attracted bids in the region of $9B. Looking ahead notable earners include Secureworks, Brown Forman and Vera Bradley.

Movers

- Consumer Discretionary Hornby [HRN.UK] -5.1% (New borrowing facility), Carpetright [CPR.UK] -1.4% (Results of rights issue), WH Smith [SMWH.UK] +6.3% (Trading update)

- Industrials RPC [RPC.UK] -14% (Earnings), Smurfit Kappa [SKG.UK] +2.9% (IP confirms not to pursue acquisition, Affirms outlook), Voestalpine [VOE.AT] +3% (Earnings)

- Financials Workspace Group [WKP.UK] -5.4% (Earnings, Secondary)

- Materials BHP [BLT.UK] +1.5% (Shale unit said to have bids worth $9B)

- Energy Repsol [REP.ES] +3.5% (Mid term targets)

Speakers

- ECB’s Praet (Belgium, chief economist): Convergence of inflation towards target had been improving. Any decision on QE would hinge on the ultimate judgement of the Governing Council

- ECB's Hansson (Estonia): ECB could raise rates before mid-2019 due to moderately rising inflation

- ECB's Weidmann (Germany) reiterated view that inflation was expected to return to target; market expectations that QE program to end in 2018 was plausible

- ECB’s Knot (Netherlands): Inflation outlook was stable and less dependent on stimulus. Reasonable to signal the end of QE soon

- Russia Central Bank Dep Gov Yudayeva: CPI trends made a rate cut possible. Recent inflation data was in line with our forecasts

- Turkey Dep PM Simsek stated that inflation was rising due to currency shocks and higher oil prices

- Turkey Fin Min Agbal: FX rate developments were negatively affecting inflation; accelerating inflation poised to continue in coming months. To take anti-inflation measures that included tax cuts

- South Africa Mineral Resource Min Mantashe: To publish 1st mines charter during week of Jun 11th. Mines must give 5% of shares to workers

- India Central Bank (RBI) Policy Stated noted that the vote was unanimous (6-0) for the 25bps rate hike but its maintained its neutral policy stance. Geo-political risks, financial market volatility and threat of protectionism posed headwinds for domestic recovery. Maintained its FY18/19 GDP growth forecast at 7.4%

- Indonesia Central Bank Gov Warjiyo: More rate hikes were possible if needed. Hikes would be measured and depend on markets and economy

Currencies

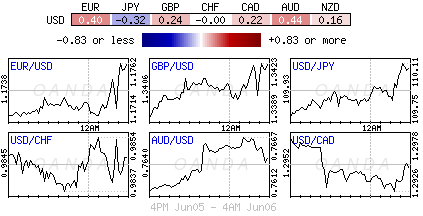

- EUR/USD tested the 1.1750 level for 2-week highs aided by short-covering as market participants looked for clues on the ECB QE decision. Comments from ECB’s Praet helped to strengthen some speculation that ECB was ready to discuss QE exit policy at June 14th meeting as inflation outlook improved. The concerns over the new populist govt in Italy provided some headwinds to the Euro’s advance as BTP yields continued to drift higher

- The South Africa ZAR currency (Rand) weakened against the USD after the govt announced the upcoming release of its Mines charter.

Fixed Income

- Bund Futures trade 44 ticks lower at 160.74 as ECB tapering talk attracts paying and steepening. Upside targets 163.75 followed by 164.50, while a return lower targets the 160.25 level.

- Gilt futures trade at 123.31 lower by 48 ticks as the pound climbs to a 2-week high on dollar weakness. Support continues stands at 122.75 then 122.25, with upside resistance at 124.85 then 126.35.

- Wednesday’s liquidity report showed Tuesday’s excess liquidity rose from €1.918T to €1.923T. Use of the marginal lending facility decreased from €108M to €99M.

- Corporate issuance saw 7 issuers raise $16.0B in the primary market

Looking Ahead

- (UK) Brexit talks continue on future relationship, Ireland and remaining withdrawal in Brussels

- (CN) China May Foreign Reserves: $3.107Te v 3.125T prior (no set time)

- 05:30 (ZA) South Africa May Sacci Business Confidence: No est v 96.0 prior

- 05:30 (DE) Germany to sell €2.0B in 0% Apr 2023 BOBL

- 05:30 (UK) DMO to sell £2.75B in 0.75% July 2023 Gilts

- 05:30 (GR) Greece Debt Agency (PDMA) to sell €625M in 3-month bills

- 05:30 (GR) Greece Debt Agency (PDMA) to sell €1.25B in 6-month bills

- 06:00 (IE) Ireland May Unemployment Rate: No est v 5.9% prior

- 06:00 (PL) Poland Central Bank (NBP) Interest Rate Decision: Expected to leave Base Rate unchanged at 1.50%

- 06:00 (UK) BOE’s Tenreyro in Belfest

- 06:45 (US) Daily Libor Fixing

- 07:00 (US) MBA Mortgage Applications w/e Jun 1st: No est v -2.9% prior

- 07:00 (BR) Brazil May FGV Inflation IGP-DI M/M: 1.4%e v 0.9% prior; Y/Y: 4.9%e v 3.0% prior

- 07:00 (UK) PM May weekly question time in House of Commons

- 07:00 (RU) Russia to sell combined RUB30B in OFZ bonds (2 tranches)

- 08:00 (HU) Hungary Central Bank (MNB) May Minutes

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Q1 Final Nonfarm Productivity: 0.6%e v 0.7% prelim; Unit Labor Costs: 2.8%e v 2.7% prelim

- 08:30 (US) Apr Trade Balance: -$49.0Be v -$49.0B prior

- 08:30 (CA) Canada Apr Building Permits M/M: -1.0%e v +3.1% prior

- 08:30 (CA) Canada Apr Int'l Merchandise Trade (CAD): -3.4Be v -4.1B prior

- 09:00 (MX) Mexico Mar Gross Fixed Investment: -2.6%e v +4.8% prior

- 10:00 (CA) Canada May Ivey Purchasing Managers Index (Seasonally Adj): No est v 71.5 prior

- 10:00 (PL) Poland Central Bank Gov Glapinski post rate decision press conference

- 10:20 (BR) Brazil May Vehicle Production: No est v 266.1K prior; Vehicle Sales: No est v 217.3K prior; Vehicle Exports: No est v 73.2K prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 11:00 (UK) BOE’s McCafferty (hawk)

Forex Analysis: GBPJPY

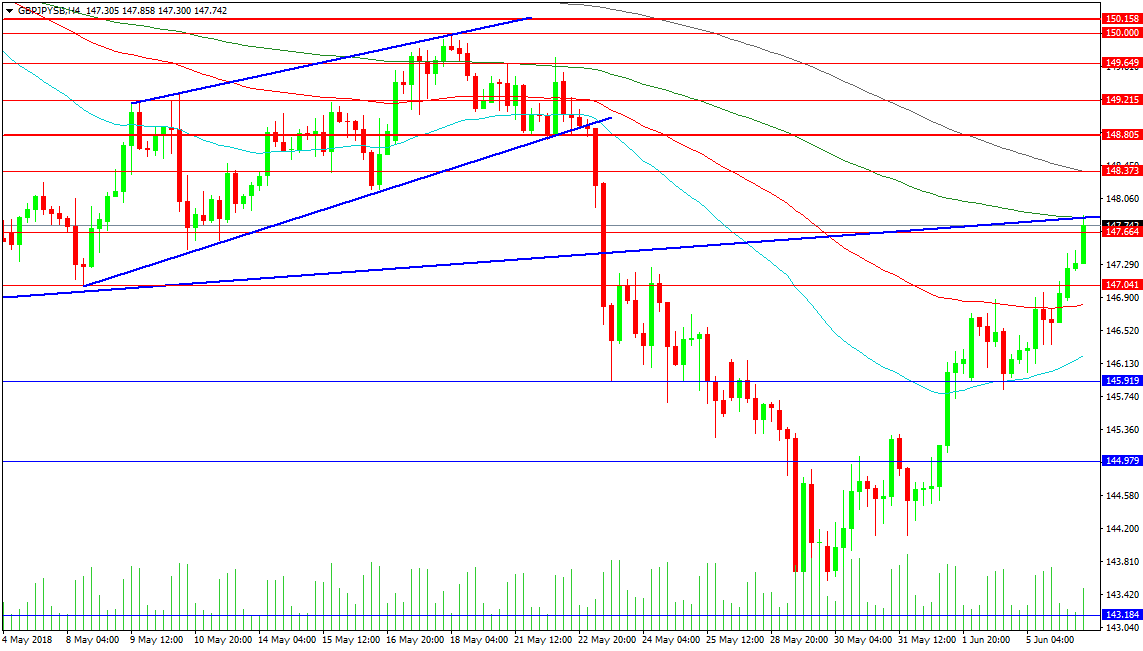

The GBPJPY pair is retesting is rising trend line resistance today at 147.842 which is also the level of its 200 period MA in this 4 hour chart. There has been a spectacular selloff from the 150.000 level all the way to support at 143.184 and a recovery to current price. Resistance comes in at 148.373 where the 200 period Simple MA is found and the 148.805 level which had been supporting the price after the initial retracement from 150.000. There is resistance at 149.215 and 149.649 also from the trading in May. A break above 150.000 can see price push against 150.158 and on to 151.166 followed by the April high of 153.850 in extension.

Support for the pair comes in at 147.000 with the 100 period MA at 146.821 and the 50 period MA at 146.229. There is further support at 145.919 followed by the 145.000 area. A loss of the recent low of 143.184 which was a significant level from summer 2016, would target levels at 141.120 followed by 140.000.

Forex Analysis: USDCAD

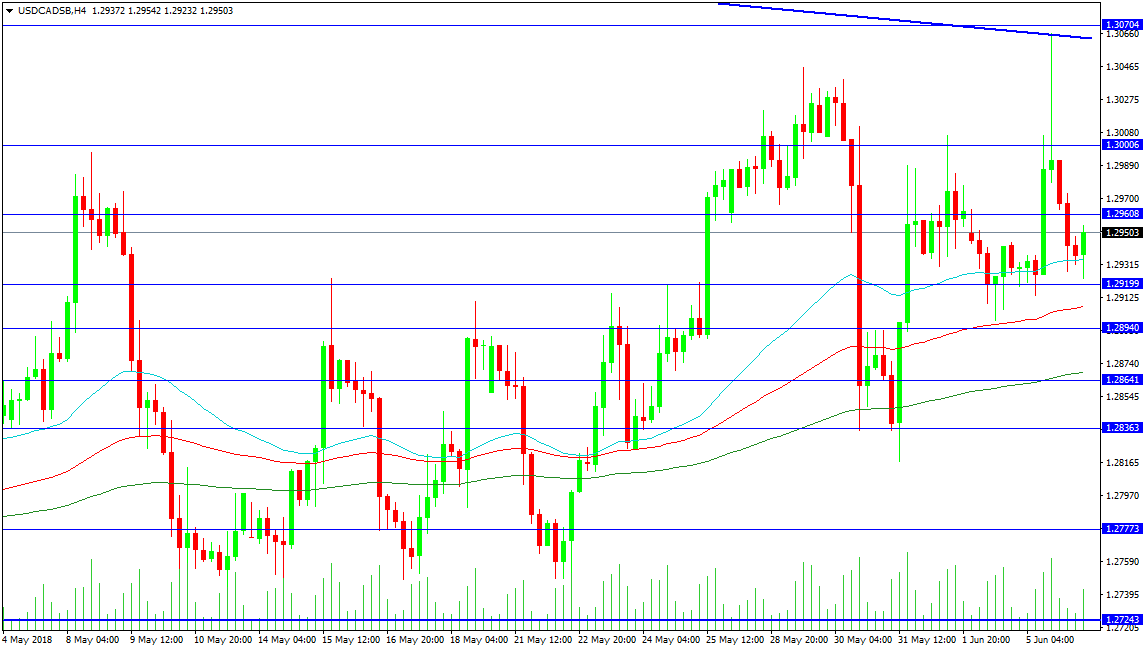

The private Oil data yesterday showed an unexpected draw in inventories of -2.028M and we await data this afternoon to support that view. There is also Canadian Trade, Building Permits and PMI data being released today. USDCAD advanced to trend line resistance yesterday where sellers forced price down creating a pin bar on the 4 hour chart. Price is currently trading around 1.29500 and resistance is clearly defined at 1.30000 and the 1.30600 area. A break above this zone would target 1.31000 followed by 1.32200.

There were reports out yesterday that US Treasury Secretary Mnuchin urged President Trump to exempt Canada from the Steel and Aluminium tariffs which also added to the moves in the pair. A continuation of the downward move needs to break under 1.29200 followed by the 100 period MA at 1.29068 and clear 1.28940 in order to keep the pressure on longs. There is the 200 period MA at 1.28700 which is supporting price at 1.28641 but really the 1.28363 level is needed to see a move down to test 1.27777 followed by 1.27243.

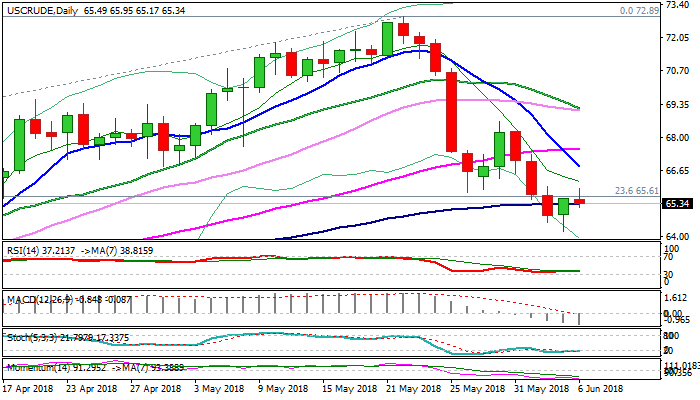

WTI Oil Outlook – Bearish Bias Favors Renewed Attempt Below Daily Cloud

WTI oil price spiked to $65.95 on Wednesday but was unable to hold gains and extend recovery rally from Tuesday’s new nearly two-month low at $64.21.

Initial probe below daily cloud base (which marks strong support at $64.64) failed as subsequent bounce, supported by draw in oil stocks (API report on Tuesday showed draw of 2.02 million barrels vs previous week’s build of 1 million barrels) lacked momentum for stronger recovery.

Overall picture remains bearish (daily MA’s in negative setup and south-heading momentum) and favors further downside on eventual break below daily cloud, for test of next pivot at $63.73 (Fibo 61.8% of $58.06/$72.89).

Meanwhile, oil price may hold in extended consolidation, signaled by oversold slow stochastic, before bears continue.

Falling 10SMA ($66.82) and daily cloud top ($66.93) are expected to cap extended upticks and keep bears in play.

Focus is turning towards US EIA weekly crude stocks report which could provide fresh signals.

US crude inventories are expected to fall by 1.82 million barrels, compared to 3.62 million barrels draw previous week, which may not be enough to offset negative impact on oil prices from rising US production and fears of easing OPEC’s deal about reducing production in order to tighten oil market.

Res: 65.95, 66.86, 66.93, 67.56

Sup: 65.17, 64.74, 64.21, 63.73

A Hawkish ECB Backs Up Yields And Supports EUR

Wednesday June 6: Five things the markets are talking about

Global equities have extended their limited gains overnight on signs that major economies will avoid a fallout trade war.

An outlier was Euro equities, which have stalled as the ‘single’ unit strengthened and government bonds declined amid some ‘hawkish’ messages from the ECB.

Note: The formation of a new government in Italy should help reduce market concerns as elections have been avoided for now, however, the political outlook is still challenging.

Most commodities have rallied, with crude on course to rise for a second consecutive day. Digging deeper, Italian bonds slipped again even after the new PM indicated that any euro exit by the country had “never been discussed.”

The market is looking ahead to this weekends G6 + 1 meeting in Quebec, Canada, that may shed some light on global trade tensions, as well as policy meetings from the Fed and the ECB this month for any guidance on the trajectory of global interest rates.

1. Stocks mixed results

In Japan, the Nikkei share index touched a two-week high overnight as technology stocks edged up after their U.S peers rallied. The Nikkei ended up +0.38%, while the broader Topix added +0.15%.

Note: Both Trump and PM Abe will meet on June 7 and a U.S/North Korea summit is scheduled on June 12.

Down-under, Australia’s S&P ASX 200 was up +0.5%, supported by gains in energy and materials companies, while in S. Korea the Kospi was up+0.25%.

In Hong Kong, equities ended higher overnight, reporting a fifth consecutive session of gains, with investors keeping an eye on the latest developments in Sino-U.S. trade talks. The Hang Seng index rose +0.5%, while the China Enterprises Index gained +0.2%.

In China, stocks ended flat on Wednesday, as gains in transport and material firms were offset by losses in banking and real estate shares. The blue-chip CSI300 index ended -0.2% lower, while the Shanghai Composite Index closed flat.

In Europe, regional bourses trade mixed coming off the earlier highs tracking the slight pullback in U.S futures.

U.S stocks are set to open in the black (+0.1%).

Indices: Stoxx600 +0.1% at 387.2, FTSE +0.3% at 7710, DAX +0.4% at 12843, CAC-40 +0.1% at 5467, IBEX-35 +0.2% at 9707, FTSE MIB -1.4% at 21463, SMI +0.2% at 8558, S&P 500 Futures +0.1%

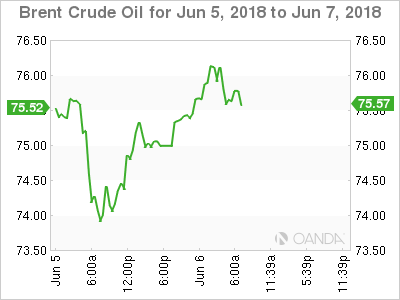

2. Oil rises amid Venezuela oil export concerns

Crude futures remain better bid after Venezuela raised the prospect of halting some crude oil exports, but gains were capped amid reports the U.S government has asked Saudi Arabia and some other OPEC producers to increase output.

Brent crude is up +78c to +$76.16 a barrel after dropping to its lowest since May 8 yesterday. U.S West Texas Intermediate (WTI) crude futures are up +33 c at +$65.85 a barrel, having touched a near two-month low yesterday.

The OPEC and Russia will meet on June 22-23 to decide how much production they will increase as global inventories have tightened while Venezuela’s production has dropped more than expected. U.S. sanctions on Iran are also threatening to reduce oil exports from the OPEC producer.

U.S API data yesterday showed that crude inventories fell by -2m barrels, compared with analyst expectations for a decrease of -1.8m.

Expect investors to take their cues from today’s official DoE EIA energy report at 10:30 am EDT.

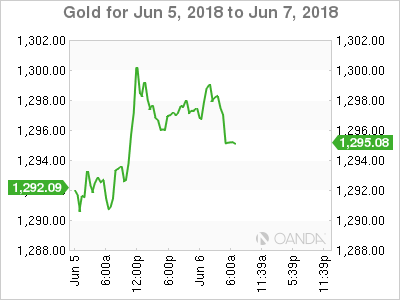

Ahead of the U.S open, gold prices have inched higher overnight on a weaker U.S dollar and lower treasury yields, but expectations of a U.S rate hike next week is keeping a lid on gains. Spot gold is up +0.3% at +$1,298.98 per ounce. U.S gold futures for August delivery are up +0.1% at +$1,303.10 per ounce.

3. Eurozone yields jump as ECB seen disusing QE next week

Hawkish comments by the ECB yesterday has pushed borrowing costs across the region higher overnight, with the impact felt deepest in Italy where markets continue to suffer from the prospect of big spending policies from a new government.

Earlier this morning, ECB chief economist Peter Praet said the “central bank was increasingly confidant that inflation is rising back to its target and will next week debate whether to gradually unwind bond purchases.”

Ten-year German Bund yields have backed up +5 bps to +0.42%, its biggest daily rise in a week.

Note: With the exception of Italy’s BTP’s, eurozone bond yields are +5-9 bps higher on the day across the bloc.

Elsewhere, the yield on 10-year Treasuries has gained +1 bps to +2.94%, while in India, the Reserve Bank of India (RBI) hiked rates for the first time in four-years. The central bank raised its main lending rate by +25 bps to +6.25% this morning, after inflation picked up following a recent surge in crude-oil prices.

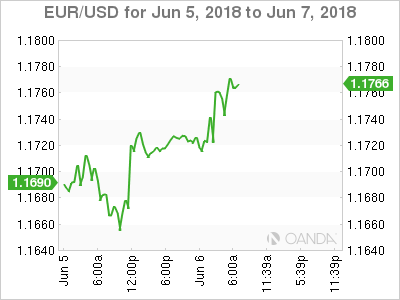

4. U.S dollar remains on the soft side

The EUR is benefiting from reports that the next ECB meeting on June 14 may be when an exit from quantitative easing (QE) will be discussed, while the dollar continues to struggle slightly.

EUR/USD is up by +0.4% at €1.1762, while the ‘big’ dollar continues to fall against the AUD (A$0.7646) and CAD (1.2949) after strong Q1 Aussie GDP and on reports that U.S. Treasury Secretary Steven Mnuchin told President Trump to exclude Canada from the aluminum and steel tariffs.

Note: The ECB’s chief economist Peter Praet signalled this morning that officials are increasingly confident that eurozone inflation will return toward target amid strong underlying economic growth and rising wages, suggesting the bank could phase out its giant bond-buying program this year.

Sterling (£1.3416) is likely to be driven by Brexit negotiations in the run-up to the E.U Summit on June 28 and 29. Investors may price out interest rate expectations going further, but any positive developments should outweigh the negatives related to BoE’s monetary policy. If the Irish border issue turns out to be solved in the coming weeks, EUR/GBP could fall. But if the U.K. and the E.U fail to reach an agreement, it would cause investors to price in a higher risk premium for the pound.

5. German engineering orders surge in April

Data from the VDMA showed that orders for Germany’s plant and machinery industry jumped +12% on year in April amid strong domestic demand.

Digging deeper, domestic orders surged +20% from April of last year, reflecting a pickup in investments in Germany, says the VDMA’s chief economist.

Orders from countries outside the eurozone increased +12%, while eurozone demand slipped -2% compared with April 2017.

The VDMA also confirmed its 2018 production forecast. German plant and machinery output is expected to increase by +5% compared with 2017, in real terms.

Euro Improves To 2-Week High As Eurozone Retail PMI Climbs

EUR/USD has posted gains in the Wednesday session. Currently, the pair is trading at 1.1770, up 0.43% on the day. On the release front, there are no major events in the Eurozone or U.S. Eurozone Retail PMI improved to 51.7 points. On Wednesday, the U.S releases unemployment claims.

With the eurozone economy continuing to improve and inflation moving higher, ECB policymakers are focused on the question of whether it’s time to wind up the bank’s bond purchase program. The ECB currently buys EUR 30 billion each month, and the scheme is scheduled to end in September. The bank has extended the program in the past, but stronger economic conditions have strengthened the case to finally end stimulus. The ECB has not formally discussed the issue, leaving the markets to hunt for any clues about the bank’s plans. On Wednesday, ECB chief Peter Praet said that the ECB would commence discussing the issue next week, when the Governing Council meets in Riga, Latvia. Many policymakers favor a gradual reduction in stimulus over several months, rather than completely turning off the tap in September. If the ECB makes any announcements regarding further tapering, we could see some strong movement from EUR/USD.

The on-again-off-again Korea nuclear summit is back on, complete with a starting time. The much-heralded meeting between President Trump and President Kim Jong-un will take place in Singapore on June 12, at 9:00 AM sharp. The summit will mark the face ever face-to-face meeting between leaders of the U.S and North Korea, but Trump has tried to lower expectations, saying that he doesn’t expect the sides to sign an agreement. Rather, the meeting would mark the start of a process. North Korea is unlikely to agree to denuclearization, but the fact that progress is being made could boost investor risk appetite.

EUR Better Bid, Ram-Euphoria Eases

EUR better bid despite Italian uncertainties

The single currency extended gains on Wednesday with EUR/USD finally breaking the 1.1745 resistance to the upside and EUR/CHF climbing towards 1.16. The fact that the euro is not getting under more significant pressures could be surprising, especially after the new Italian government won the Senate confidence vote. However, Giuseppe Conti, the prime minister, said his government has no intention to leave the Eurozone but called for a redistribution of asylum seekers around the EU. In his first speech before the senate, he reiterated the anti-austerity calls of the coalition and a friendlier stands towards Russia.

Even though everything seems to go well in the FX market, the same cannot be said for the bond market. Indeed, Italian yields climbed further yesterday and the move continued on Wednesday with the 2-year and 10-year rates rising as much as 1.49% and 2.96%, respectively. Market participants also dumped Italian equities as the FTSE MIB fell more than 1% during the European morning.

Therefore, it looks like investors do not believe the Italian situation will affect negatively the entire EU but will remain contained to Italy. Investors are fleeing Italian assets but not European one, for now at least. Against such a backdrop, we would rather remain cautious regarding a return of EUR/CHF around 1.20 in the short-term. On the other hand, believe that that there is room for further appreciation in EUR/USD as the trade war between the USA and its allies will weigh on the greenback.

Swiss CPI higher

In a surprise move Switzerland consumer price inflation rose higher then forecasts. The move will certain triggers speculation of quicker normalization of extreme policy. Swiss May CPI came in at 0.4% m/m vs. 0.3% m/m exp (1.0% y/y vs. 0.9% y/y) while core CPI climbed 0.1% m/m and 0.4% y/y. The higher read was spread around underlying components indicating a continue of strong trend since Feb 2016. Yet simple projections have inflation reaching the SNB target around late 2019, so the central banks is unlikely to panic when it see these numbers. Call to push forward the tightening cycle is likely to fall on deaf ears. With political risk rising in Europe resulting into a stronger CHF, the SNB will stay steadfast in current defensive policy mix. In fact at 21st June rate decision we will likely hear further commitment by the SNB to weaken “overvalued” CHF, rather than acknowledging inflations pressures.

The SNB has played a dangerous game with extreme policy actions, unwinding these actions will come with significant certainties. Even subtle changes in languages could be the catalyst to reloading CHF long by investors who have long abandoned the currency due to high carry costs. EURCHF was higher on the news as trades remain focused on the short term positive news out of Italy over the long play of SNB policy.

Ramaphoria effect is subdued

Cyril Ramaphosa’s challenge is lively. Since his appointment as South African President on 15. February 2018, the Head of State is facing a strong economic downturn, with Q1 economic output given at 9-year low (-2.20%; prior: 3.10%), strongly impaired by most relevant industries and specifically Agriculture, Forestry, Fishing (-24.20%), Mining & Quarrying (-9.90%) and Manufacturing (-6.40%) compared to Q4 2017.

Indeed, the recent development in GDP will probably deteriorate business and consumer confidence, putting into question Ramaphosa’s capability to reform the country appropriately. We would however balance the statement due to current geopolitical tensions and underlying trade tensions incurred by most economic partners and particularly South Africa’s first trade partner, China. South African economic growth remains fragile and the situation exceeds the range of actions of its leaders.

Accordingly, market reactions were swift after the publication. The rand weakened further, decreasing by 2.01% against the greenback, valued at 12.8575 and trading at mid-December 2017 range. The pair is expected to strengthen further, approaching the 12.90 range in the mid-term.

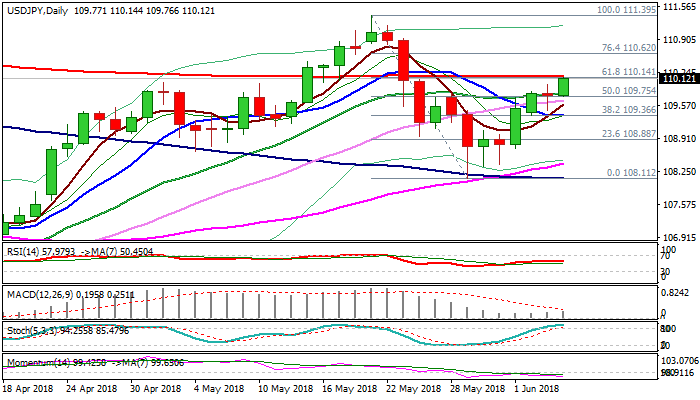

USDJPY Outlook – Bulls Need Clear Break Above 200SMA To Resume, Corrective Dips May Precede

The pair is up on Wednesday after bulls took a breather on Tuesday (Doji candle) and attack key barrier at 110.14 (Fibo 61.8% of 111.39/108.11, reinforced by 200SMA).

Break and close here is needed to strengthen bulls and generate strong signal for continuation of recovery leg from 108.11 (29 May) towards 110.62 (Fibo 76.4%) and psychological 111.00 barrier.

Bullish setup of daily MA’s supports, however, flat momentum and overbought slow stochastic warn that bulls may show stronger hesitation to clear key obstacles.

Top of thick 4-hr cloud (also session low) marks initial support at 109.75, followed by converging 5/30SMA’s (109.60/66), where dips should find footstep to keep bulls intact.

Res: 110.14, 110.62, 111.00, 111.39

Sup: 109.75, 109.60, 109.38, 109.12