Sample Category Title

Market Morning Briefing: Dollar Yen Had Broken Resistance

STOCKS

Dow and Dax face resistance just above current levels. A break on the upside or a fall would be driving the next course of direction for the medium term. Nikkei is likely to be stable before falling sharply in the longer run while Shanghai looks bullish just now. Indian stock indices looks bullish with immediate support below current levels.

Dow (24799.98, -0.055%) is headed towards resistance near 25000 and while that holds, a small corrective dip is possible. It would be crucial to see if the index is able to break above 25000 to move higher towards 25250+ levels. That if seen would be an important trigger for medium term bullishness.

Dax (12787.13, +0.13%) attempted to rise above 12900 but could not sustain there. The current daily candle with a spike on the upside could indicate some bearishness for the coming sessions with a possible target of 12600-12500. Near term looks bearish.

Nikkei (22575.54, +0.16%) is trading just below the trend resistance as clearly visible on the 3-day charts. Some more sessions of sideways to upside is possible before a sharp corrective fall is seen. Medium term looks bearish.

Shanghai (3116.03, +0.059%) is trying to move up slowly from 3050 support. While the rise continues, the index could move up towards 3150-3175 in the near term.

Nifty (10593.15, -0.33%) is just above immediate support and could bounce back towards 10750 in the near term. Sensex could start moving up towards 35500. Only on a downside break below the current trend supports, we would revisit the lower targets.

COMMODITIES

Worries about supply disruptions in the key Copper producing region pulled up Copper prices. Precious metals are almost stable while crude prices could pose a rise in the coming sessions.

Brent (75.36) tested 73.81 before again moving back to current levels. While above 74, there is scope to move back to 77-78.

WTI (65.70) is trading higher today. It is possible that the crude price falls back from 66 back towards 65.50 in the near term before moving higher in the longer run.

Gold (1297.28) continues to trade within 1285-1310 region. While support in the 1275-1285 region holds, Gold could attempt to move up in the medium term but a failure to rise past 1310 could eventually push down the prices to 1375/70 levels.

Copper (3.1964) finally saw an upward break from the narrow range of 3.05-3.15 region which we thought would come after another down move to 3.05. News states that the rise is attributed to concerns about the potential supply impact of wage negotiations at the world's biggest copper mine. The union at BHP's Escondida facility in Chile said on Friday that it had started the latest round of negotiations with a proposal which includes a bonus of about $34,000 per worker. There could be some corrective dip in the coming sessions but overall a rise towards 3.30 looks possible in the longer run.

FOREX

Dollar index (93.84) has broken below channel trendline on daily candles and has important support at the 21 days MA near 93.65. A break below 93.65 could make it bearish till 93.3-92.8. A break of 92.8 would be very bearish in the medium term.

Euro (1.1723): A breach above 1.175 (21 days MA) would take the Euro higher to 1.181. If 1.181 is breached as well, it could be signs of bullishness for the medium term.

Dollar Yen (109.82) had broken resistance on daily candles near 109.6 yesterday and while above 109.8 (21 days MA), could go on to test crucial long term resistance on weekly line chart near 111. A test of 111 (max 112) should then produce a dip.

Euro Yen (128.74): As mentioned yesterday as well, a bullish Dollar Yen and an upward creeping Euro is taking Euro Yen closer to 129.5-130.0 (crucial resistance level on weekly candles). After a test of 129.5-130.0, Euro Yen could dip. A breach of 129.5-130.0 could make it bullish for the medium term.

Pound (1.3407): Against our expectation, Pound again tested a high near 1.341, thereby testing the 21 days MA. It could either dip from here or from resistance on daily candles near 1.345. A breach of 1.345 could take it higher towards 1.355-1.360.

Dollar Rupee (67.15) : Might dip to 67.10 and lower in case of failure to rise above 67.25 in early trade.

INTEREST RATES

Current yields: US 10 Year (2.93%), 30 Year (3.09%), 5 Year (2.77%), 2 Year (2.49%)

US yields haven't shown any significant movement yet in this week, which might be due to the fact that markets are waiting for the CPI data release and the FOMC meet next week. Moreover, a rate hike is more or less certain and would already have been factored in by the markets.

Any sign of dovishness from the Fed could lead to another dip in US yields and bring into play a downmove towards the following support levels:

2.55% (10 Year), 2.9% (30 Year) and 2.2% (5 Year)

German 10 year yield (0.37%) is testing support on short term chart and could rise from here.

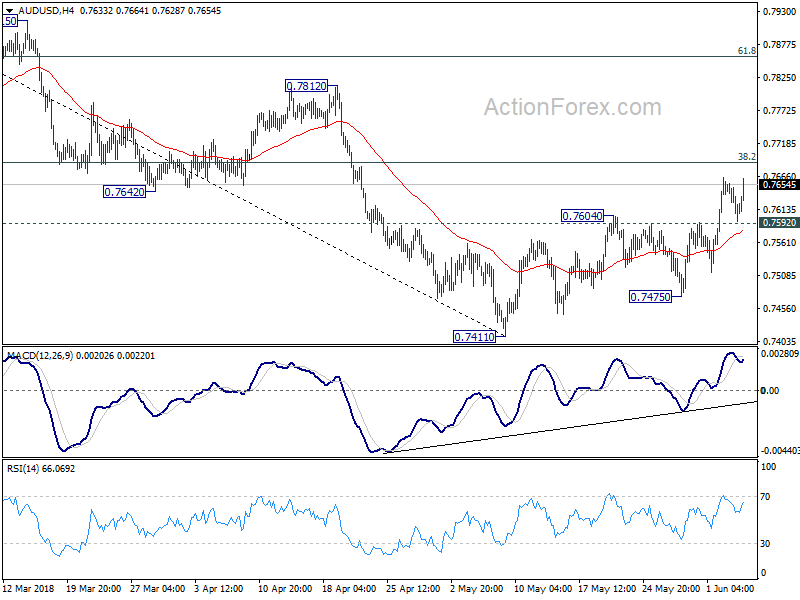

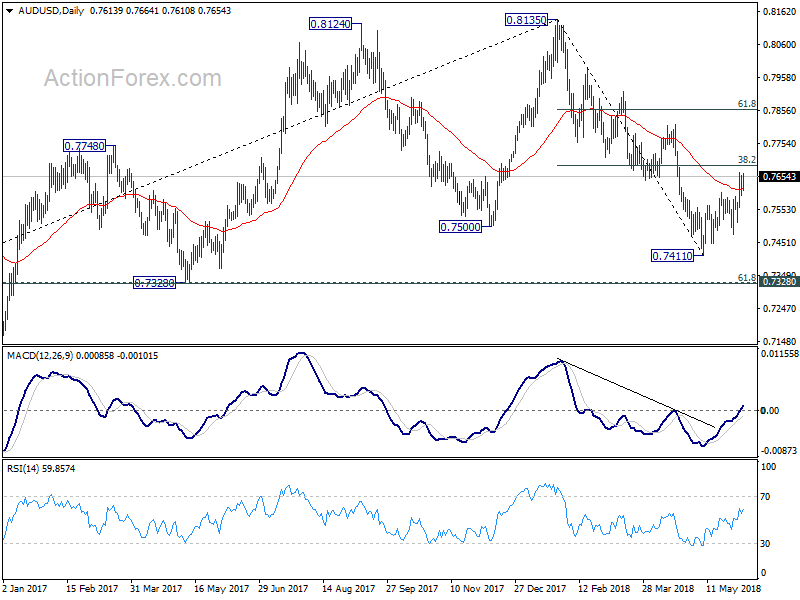

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7588; (P) 0.7622; (R1) 0.7650; More...

Despite today's rebound in AUD/USD, 4 hours MACD is staying below sign line. Intraday bias is turned neutral first. As noted before, rebound from 0.7411 is seen as a correction. Hence, upside should be limited by 38.2% retracement of 0.8135 to 0.7144 at 0.7688. On the downside, below 0.7592 minor support will turn bias to the downside for 0.7475 first. Break there will likely resume larger fall through 0.7411 to 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326). However, sustained break of 0.7688 will dampen our bearish view and target 61.8% retracement at 0.7585 instead.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

Aussie Jumps on GDP Upside Surprise, Dollar and Yen Soft

Australian Dollar is back in the driving seat today as GDP beat market expectation. The Aussie is trading as the strongest one for today and for the week. But strength is so far limited as RBA has made its neutral stance very clear again yesterday. While Canadian Dollar follows higher in Asian session, it's near term outlook is more mixed due to NAFTA uncertainty and falling oil price. On the other hand, Yen is staying as the weakest one in the markets. Dollar is back under some pressure as rebound in treasury yields failed to extend.

Technically, GBP/JPY's break of 147.04 resistance now indicates near term reversal and there is prospect of climbing back to 150 and above in near term. A focus in on whether GBP/JPY would take EUR/JPY higher today. On the other hand, USD/JPY's rebound from 108.10 is disappointing as it quickly lost momentum again.

Australia GDP grew 1.0% qoq in Q1, led by exports growth

Australia GDP grew 1.0% qoq in Q1, above expectation of 0.8% qoq. Q4's figure was also revised up from 0.4% qoq to 0.5% qoq.

Chief Economist for the ABS, Bruce Hockman said in release that "growth in exports accounted for half the growth in GDP, and reflected strength in exports of mining commodities." Mining industry Gross Value Added grew 2.9% during the quarter. Production of coal, iron ore and liquefied natural gas showed strong increases.

Meanwhile, private non-financial corporations profits increased by 6.0%. Hockman added that "the rise in profits was consistent with the strong increase in mining exports coupled with a lift in the terms of trade this quarter."

Trump's bilateral NAFTA idea shunned immediately by Canada and Mexico

It's reported that US Treasury Secretary Steve Mnuchin urged President Donald Trump to exempt Canada from the steel and aluminum tariffs at a meeting with director of the National Economic Council Larry Kudlow, Commerce Secretary Wilbur Ross, Trade advisor Peter Navarro, trade representative Robert Lighthizer and chief of staff John Kelly. But Mnuchin's recommendation met opposition from some others in the meeting.

Separately, Kudlow said in on Fox News that Trump is trying to negotiate with Mexico and Canada separately, in bilateral way. But Kudlow emphasized that Trump is "not going to leave NAFTA", but just "going to try a different approach". But the idea was shunned by NAFTA counterparts quickly.

Canada International Trade Minister Francois-Philippe Champagne said "We want a trilateral agreement - we've always said this." And, "we know it works, we know it underpins a very integrated supply chain. So, when you talk about this issue you have to look at reality - the reality is that over the last 24 years we have built a very integrated supply chain, which has been good for (the) economy, good for consumers, good for workers on all sides."

Mexico's Economy Minister Ildefonso Guajardo said NAFTA "has to be a trilateral accord, given the conditions of integration in North America." And, "it must be that way.

Bundesbank Weidmann: Tragic to roll back EU reforms and fiscal consolidations

German Bundesbank President Jens Weidmann said that the Euro currency union is not yet "crisis proof in a durable way". He pointed to the recent financial market turbulence in Italy as it "illustrates" that.

Weidmann also said it would be "tragic" in the reforms and fiscal consolidations achieved during the global financial crisis are rolled back. He supports some of the proposals of German Chancellor Angela Merkel and French President Emmanuel Macron. They include common backstop for failing banks. However, Weidmann disagree to joint insurance for deposits, until the balance sheets are cleaned up.

The reforms will be discussed as a EU summit on June 28-29.

Looking ahead

Swiss will release CPI in European session and Eurozone will release retail PMI. Canada will release trade balance, building permits and Ivey PMI later today. US will release trade balance and non-farm productivity.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7588; (P) 0.7622; (R1) 0.7650; More...

Despite today's rebound in AUD/USD, 4 hours MACD is staying below sign line. Intraday bias is turned neutral first. As noted before, rebound from 0.7411 is seen as a correction. Hence, upside should be limited by 38.2% retracement of 0.8135 to 0.7144 at 0.7688. On the downside, below 0.7592 minor support will turn bias to the downside for 0.7475 first. Break there will likely resume larger fall through 0.7411 to 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326). However, sustained break of 0.7688 will dampen our bearish view and target 61.8% retracement at 0.7585 instead.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y Apr | 0.80% | 1.40% | 2.10% | 2.00% |

| 01:30 | AUD | GDP Q/Q Q1 | 1.00% | 0.80% | 0.40% | 0.50% |

| 07:15 | CHF | CPI M/M May | 0.00% | 0.20% | ||

| 07:15 | CHF | CPI Y/Y May | 0.80% | 0.80% | ||

| 08:10 | EUR | Eurozone Retail PMI May | 48.6 | |||

| 12:30 | CAD | International Merchandise Trade (CAD) Apr | -4.1B | |||

| 12:30 | CAD | Building Permits M/M Apr | 2.80% | 3.10% | ||

| 12:30 | USD | Nonfarm Productivity Q1 F | 0.70% | 0.70% | ||

| 12:30 | USD | Unit Labor Costs Q1 F | 2.70% | 2.70% | ||

| 12:30 | USD | Trade Balance Apr | -50.0B | -49.0B | ||

| 14:00 | CAD | Ivey PMI May | 69.7 | 71.5 | ||

| 14:30 | USD | Crude Oil Inventories | -3.6M |

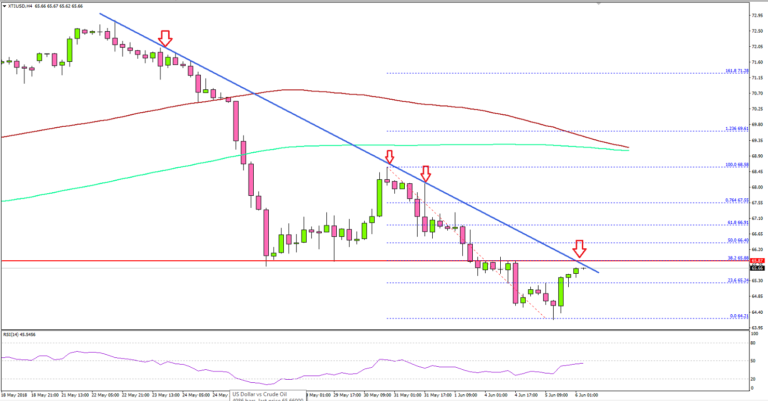

Crude Oil Price Turned Bearish Below $66.00?

Key Highlights

- Crude oil price started a fresh downside move and declined below the $66.00 support against the US dollar.

- There is a major bearish trend line in place with resistance at $65.90 on the 4-hours chart of XTI/USD.

- The US Services Purchasing Managers Index (PMI) in May 2018 increased to 56.8 from 55.7.

- Today in the US, the Trade Balance figure for April 2018 will be released, which is forecasted to post a deficit of $-49.0B.

Crude Oil Price Technical Analysis

After a nice upside move, crude oil price topped around the $73.00 level against the US Dollar. The price started a major bearish wave and tumbled below the $70.00 and $68.00 support levels.

Looking at the 4-hours chart of XTI/USD, the price moved into a bearish zone with a break and close below the $66.00 support. It also settled below the 100 (red) and 200 (green) simple moving averages (4-hours).

It seems like there could be more declines in the near term towards the $62.50 and $61.00 levels. On the upside, there is a major bearish trend line in place with resistance at $65.90 on the 4-hours chart of XTI/USD.

As long as the price is below the trend line and the $66.00 pivot level, it remains in a downtrend. Above $66.00, the next barrier for buyers are at $67.50 and $68.00.

Recently in the US, the Services PMI for May 2018 was released by Markit Economics. The market was looking for no change in the PMI from the last reading of 55.7.

However, the actual result better than the forecast as there was a rise in the PMI to 56.8, which means output growth was strongest in over three years. Commenting on the same, Chief Business Economist at IHS Markit, Chris Williamson, stated:

The US economy kicked up a gear in May. A markedly improved service sector performance takes the final composite PMI reading above the flash estimate and to its highest for over three years.

Overall, the US Dollar remained in control versus other majors such as the Euro and the British Pound. Oil and gold prices may also come under bearish pressure in the short term.

Economic Releases to Watch Today

- US Trade Balance April 2018 – Forecast $-49.0B, versus $-49.0B previous.

- Canada’s Ivey PMI May 2018 – Forecast 69.7, versus 71.5 previous.

- Canada’s Building Permits April 2018 (MoM) – Forecast +2.0%, versus +3.1% previous.

Australia GDP grew 1.0% qoq in Q1, led by exports growth

Australia GDP grew 1.0% qoq in Q1, above expectation of 0.8% qoq. Q4's figure was also revised up from 0.4% qoq to 0.5% qoq.

Chief Economist for the ABS, Bruce Hockman said in release that "growth in exports accounted for half the growth in GDP, and reflected strength in exports of mining commodities." Mining industry Gross Value Added grew 2.9% during the quarter. Production of coal, iron ore and liquefied natural gas showed strong increases.

Meanwhile, private non-financial corporations profits increased by 6.0%. Hockman added that "the rise in profits was consistent with the strong increase in mining exports coupled with a lift in the terms of trade this quarter."

Full release here.

USD Can’t Find A Grip

USD can't find a grip

In the absence of Fed speak and tier one economic data, the US dollar is struggling to find a grip. Not to unexpected mind you, as traders continue to rebalance from last weeks global risk meltdown. And not to harp on existing risks, but what really matters is how the market is perceiving next weeks forward guidance from the Fed. So therein lies the conundrum. Despite the steady uptrend in US economic data, in the absence of inflation, no one, and I mean no one, is betting on an aggressive shift if Fed policy.

Gold is maintaining its tight correlation with the greenback, and despite the absence of escalating geopolitical risk, traders are all too knowing that we're little more than a spark away from re-igniting a free for all, whether its EU political risk, trade wars or the more probable escalation in middle east tensions. But for now, nothing else matters other than the Goldilocks syndrome.

Oil market

Too far too soon. As hedge funds trip over each other to get in front of a probable shift in OPEC supply. Calmer heads prevail realising that while OPEC might compensate for the Venusaulain shortfall, it's highly unlikely their robust compliance on supply curbs is going to fall by the wayside. But this is in no way to suggest we're not in for a bumpy ride pre-Vienna.

Gold market

What the dollar gives up, gold traders make up. There remains far to much geopolitical risk on the table to lose the plot on the long gold trade. So buy on dip mentality even in the absence of risk aversion suggests gold traders are banking on the USD correction to extend further ahead of the Fed meeting.

Currency market

The current currency market narrative is all about corrections and rebalancing ahead of the next weeks Fed decision which points to a USD correction with the EUR driving the bus.

British Pound Gains Ground On Strong Services PMI

The British pound has moved higher in the Tuesday session. In North American trade, GBP/USD is trading at 1.3376, up 0.46% on the day. On the release front, British Services PMI improved to 54.0, marking a 3-month high. This beat the estimate of 52.9 points. On the release front, U.S manufacturing and employment reports were sharp. The ISM Non-Manufacturing PMI climbed to 58.6, beating the estimate of 57.9 points. JOLTS Job Openings improved to 6.70 million, crushing the estimate of 6.49 million.

Canada is the host of the G-7 meetings this year, and finance ministers from six countries were united in their criticism of US Treasury Secretary Steve Mnuchin over a brewing trade war. Last week, the Trump administration imposed stiff tariffs on Canada, Mexico and the European Union. Prime Minister May expressed her disappointment with the U.S move in a conversation with President Trump. Canada will host the G-7 leaders on June 8, with the U.S tariffs sure to be high on the agenda. If the trade battle escalates, the result will be lose-lose and thousands of British jobs could be at stake.

A rate hike in June from the Federal Reserve is virtually a given, with the CME Group forecasting the odds of a rate hike at 94%. At the same time, there is increasing talk that the Fed is moving closer to a neutral monetary policy. Recent statements by FOMC policymakers appear to support such a conclusion, which would mean that the Fed would let the economy ‘ride on its own steam’ without intervening by adjusting interest rates. The minutes of the May meeting noted that policymakers would consider allowing inflation to rise above the Fed’s 2 percent target for a temporary period, which means that the Fed would not rush to raise rates based on the inflation target. After June, the Fed is most likely to raise rates in September. Analysts are divided on whether a fourth rate hike will be needed. If the economy is in danger of overheating, policymakers would have to seriously consider another rate increase in December.

The on-again-off-again Korea nuclear summit is back on, complete with a starting time. The much-heralded meeting between President Trump and President Kim Jong-un will take place in Singapore on June 12, at 9:00 AM sharp. The summit will mark the face ever face-to-face meeting between leaders of the U.S and North Korea, but Trump has tried to lower expectations, saying that he doesn’t expect the sides to sign an agreement. Rather, the meeting would mark the start of a process. North Korea is unlikely to agree to denuclearization, but the fact that progress is being made could boost investor risk appetite and weigh on the safe-haven Japanese yen.

Bundesbank Weidmann: Tragic to roll back EU reforms and fiscal consolidations

German Bundesbank President Jens Weidmann said that the Euro currency union is not yet "crisis proof in a durable way". He pointed to the recent financial market turbulence in Italy as it "illustrates" that.

Weidmann also said it would be "tragic" in the reforms and fiscal consolidations achieved during the global financial crisis are rolled back. He supports some of the proposals of German Chancellor Angela Merkel and French President Emmanuel Macron. They include common backstop for failing banks. However, Weidmann disagree to joint insurance for deposits, until the balance sheets are cleaned up.

The reforms will be discussed as a EU summit on June 28-29.

Trump’s bilateral NAFTA idea shunned immediately by Canada and Mexico

It's reported that US Treasury Secretary Steve Mnuchin urged President Donald Trump to exempt Canada from the steel and aluminum tariffs at a meeting with director of the National Economic Council Larry Kudlow, Commerce Secretary Wilbur Ross, Trade advisor Peter Navarro, trade representative Robert Lighthizer and chief of staff John Kelly. But Mnuchin's recommendation met opposition from some others in the meeting.

Separately, Kudlow said in on Fox News that Trump is trying to negotiate with Mexico and Canada separately, in bilateral way. But Kudlow emphasized that Trump is "not going to leave NAFTA", but just "going to try a different approach". But the idea was shunned by NAFTA counterparts quickly.

Canada International Trade Minister Francois-Philippe Champagne said "We want a trilateral agreement - we've always said this." And, "we know it works, we know it underpins a very integrated supply chain. So, when you talk about this issue you have to look at reality - the reality is that over the last 24 years we have built a very integrated supply chain, which has been good for (the) economy, good for consumers, good for workers on all sides."

Mexico's Economy Minister Ildefonso Guajardo said NAFTA "has to be a trilateral accord, given the conditions of integration in North America." And, "it must be that way.

Eco Data 6/6/18

[php_everywhere instance="1"]