Sample Category Title

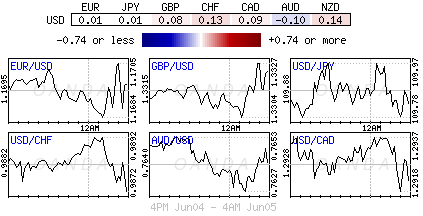

Into US session: Sterling strongest today but no follow through buying seen

Entering into US session, Sterling is so far the strongest one today as lifted by upside surprise in UK services PMI. August BoE hike is back on the table after the current batch of May PMIs. But it's far from being certain. As BoE MPC member Silvana Tenreyro pointed out, BoE opted to wait a little longer in May to have better assessment on the outlook. Her comments argued that August is probably time. But then, it's totally data dependent. The MPC will still have two months of data in June and July to digest. If incoming data doesn't feel right, BoE could decide to wait a little longer again in August after having waited that little longer.

Technically, it should be noted that while GBP/USD rebounded it's kept below yesterday's high at 1.3397. GBP/JPY was a bit better as it breached yesterday's high at 146.88 but there was no follow through buying. EUR/GBP is also held above yesterday's low at 0.8727. So, up still now, the pound's rise is rather forgettable.

Another point to note is that commodity currencies are trading generally lower today, and there is some fresh selling in Canadian Dollar at the time of writing. We'll see if that would drag down the Australian Dollar too.

Improved Mood In Europe On Data And Political Front

Notes/Observations

Asia:

- Major European Services PMI data mixed but remain in expansion (Beats: UK, Spain, Italy, Misses: Euro Zone; in-line: Germany, France)

- Brexit negotiations set to resume ahead of the key EU Leader Summit set for Jun 28-29th

- Italy PM Conte expected to survive upcoming confidence vote in the Senate later today

Asia:

- Reserve Bank of Australia (RBA) left its Cash Rate Target unchanged at 1.50% (as expected)

- China May Caixin PMI Services: 52.9 v 52.9e

- Japan May PMI Services: 51.0 v 52.5 prior

- Bank of Japan (BoJ) Dep Gov Wakatabe: No specific policy tool in mind for future use; not thinking of US treasuries for asset buys

Europe:

- PM May has abandoned plans to present EU leaders with detail blueprint for future UK/EU relationship. The govt to publish 150-page white paper after European Council meeting on June 28/29

- UK govt says Brexit bill to return to House of Commons on Tuesday, June 12th. The House of Lords has passed numerous amendments over the last two months that will be reviewed by the Commons. PM May has a week to reach a compromise with Tory rebels over Brexit after 12 backbenchers threatened to inflict a defeat in a vote over future customs arrangements

- PM May reportedly told business leaders that a decision on the preferred post-Brexit customs option was imminent. Business leaders told PM May that they needed to be able to bring in foreign labor after the Brexit, and that a frictionless border was more important that tariffs in a post-Brexit world

- BOE's Tenreyro: Timing of BOE rate increases is an open question; there is a need for gradual tightening over next 3 years

Americas:

- Mexico responded to US metals tariffs by announcing plan to impose 20% tariff on US pork legs and shoulders; effective from June 6th

Economic Data:

- (IN) India May Services PMI: 49.6 v 51.4 prior (1st contraction in 3 months); PMI Composite: 50.4 v 51.9 prior

- (RU) Russia May Services PMI: 54.1 v 55.2e (28th month of expansion), PMI Composite: 53.4 v 54.9 prior

- (SE) Sweden May Services PMI: 57.0 v 60.1 prior

- (FR) France Apr YTD Budget Balance: -€54.3B v -€33.1B prior

- (HU) Hungary Q1 Final GDP Q/Q: 1.2% v 1.2% prelim; Y/Y: 4.4% v 4.4%e

- (HU) Hungary Apr Retail Sales Y/Y: 6.0% v 7.5%e

- (CZ) Czech Apr Retail Sales Y/Y: 4.7% v 6.6%e

- (ES) Spain May Services PMI: 56.4 v 56.0e (54th month of expansion) , Composite PMI: 55.9 v 55.6e

- (ZA) South Africa May PMI (Whole Economy): 50.0 v 50.4 prior (4th month of non-contraction)

- (SE) Sweden Apr Private Sector Production M/M: 0.3% v 0.6%e; Y/Y: 3.3% v 3.6%e

- (SE) Sweden Apr Industrial Orders M/M: +2.6% v -1.6% prior; Y/Y: +3.2% v -3.2% prior

- (SE) Sweden Apr Industry Production Value Y/Y: 3.6% v 5.9% prior, Service Production Value Y/Y: 3.9% v 3.4% prior

- (IT) Italy May Services PMI: 53.1 v 53.0e (23rd month of expansion), Composite PMI: 52.9 v 52.8e

- (FR) France May Final Services PMI: 54.3 v 54.3e (confirms 23rd month of expansion), Composite PMI: 54.2 v 54.5e

- (DE) Germany May Final Germany Services PMI: 52.1 v 52.1e (Confirms 59th month of expansion), Composite PMI: 53.4 v 53.1e

- (TW) Taiwan May CPI Y/Y: 1.6% v 2.0%e, Core CPI Y/Y: 1.0% v 1.4%e; WPI Y/Y: 5.6% v 2.5% prior

- (BR) Brazil May FIPE CPI (Sao Paulo): 0.2% v 0.1%e

- (EU) Euro Zone May Final Services PMI: # v 53.9e, Composite PMI: # v 54.1e

- (UK) May New Car Registrations Y/Y: 3.4% v 10.4% prior

- (TW) Taiwan May Foreign Reserves: $457.3B v $457.1B prior

- (UK) May Services PMI: 54.0 v 53.0e, Composite PMI: 54.5 v 53.4e

- (EU) Euro Zone Apr Retail Sales M/M: 0.1% v 0.5%e; Y/Y: 1.7% v 1.7%e

Fixed Income Issuance:

- (ID) Indonesia sold total IDR11.7T in 3-month, 9-month Bills, 5-year, 10-year and 20-year Bonds

- (AT) Austria Debt Agency (AFFA) sold €1.15B vs. €1.15B indicated in 2023 and 2028 RAGB bonds

- (CH) Switzerland sold CHF365.65 in 3-month Bills; Yield: -0.861% v -0.853% prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 0.2% at 3,478, FTSE -0.6% at 7,694, DAX +0.4% at 12,823, CAC-40 +0.3% at 5,490; IBEX-35 +0.3% at 9,775, FTSE MIB +0.5% at 22,118, SMI -0.4% at 8,599 , S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European stocks open slightly lower across the board reversing to trade mixed as the session progressed; Italy best performer as PM faces first round of confirmation votes; Consumer goods best performing sector; Media underperforming; Denmark closed for holiday; airlines impacted after IATA cuts global airline profit outlook; UK government sells 7.7% stake in RBS; upcoming earnings expected in the US session include Navistar and Summer Therapeutics

Equities

- Consumer discretionary: Hermes RMS.FR -1.1% (analyst action); International Consolidated Airlines IAG.UK -3.0% (discussion with Norwegian Air), Johnston Press JPR.UK -17.7% (trading update)

- Financials: Royal Bank of Scotland RBS.UK -3.4% (government sells stake)

- Industrials: Smurfit Kappa SKG.UK +0.8% (rejects offer)

- Technology: ASM International ASMI.NL +3.3% (analyst action)

Speakers

- ECB's Smets (Belgium): Rates might not be the best tool to ensure financial stability, could lead to spillovers in other countries

- Turkey Central Bank: TRY currency (Lira) weakness had a negative impact on basic good inflation. Strong durable good price increases continued in May

- Czech Central Bank Gov Rusnok stated that he now saw room for an earlier Czech rate hike citing wage data and weakness in CZK currency

- China FX Regulator SAFE reiterated its stance to prevent cross-border capital flow risk, facilitate trade and investment

- Malaysia Central Bank Gov Muhammad Ibrahim said to have resigned

Currencies

- The USD remained steady in price action during the session but remained off its recent cycle highs against the European pairs.

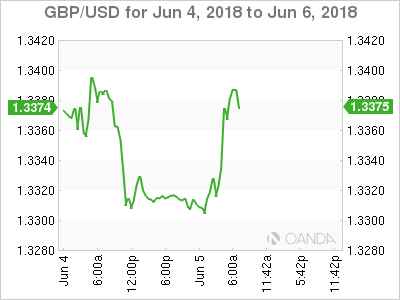

- The GBP was slightly higher as Brexit talks on the future relationship between the UK and EU were set to resume in Brussels. UK govt stated that the Brexit withdrawal bill would return to the House of Commons on Tuesday, June 12th setting up a showdown as about a dozen backbenchers threatened to inflict a defeat in a vote over future customs arrangements. The EU has previously asked for clarity on Brexit from the UK as the run-up to the EU Summit on June 28 and 29th. UK May PMI Services data beat expectations and giving some credence to the BOE assessment that the slowdown in Q1 was temporary. GBP/USD at 1.3360, +0.3% just ahead of the NY morning.

Fixed Income

- Bund Futures trade 29 ticks higher at 160.97 as the 10-year yield continues to trade around the 0.40% level. Upside targets 163.75 followed by 164.50, while a return lower targets the 160.25 level.

- Gilt futures trade at 123.47 lower by 9 ticks after better than expected Services PMI data. Support continues stands at 123.75 then 123.25, with upside resistance at 125.85 then 127.35.

- Tuesday’s liquidity report showed Monday’s excess liquidity fell from €1.925T to €1.918T. Use of the marginal lending facility decreased from €128M to €108M.

- Corporate issuance saw 10 issuers raise $10.0B in the primary market

Looking Ahead

- (UK) Brexit talks on future relationship, Ireland and remaining withdrawal issues to resume in Brussels

- 05:30 (ZA) South Africa Q1 GDP Annualized Q/Q: -0.5% v +3.1% prior; Y/Y: 1.8%e v 1.5% prior

- 05.30 (UK) Weekly John Lewis LFL sales data

- 05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

- 05:30 (DE) Germany to sell Inflation-linked 2030 and 2046 bonds (Bundei)

- 05:30 (EU) ECB allotment in 7-day Main Financing Tender (prior €1.6B with 30 bids recd)

- 05:30 (ZA) South Africa to sell ZAR2.4B in 2035, 2040 and 2044 bonds

- 05:30 (BE) Belgium Debt Agency (BDA) to sell 3-month and 6-month Bills

- 05:30 (AT) ECB's Nowotny (Austria) at conference

- 06:00 (IT) New Italy PM Conte in Senate

- 06:00 (IE) Ireland Apr Industrial Production M/M: No est v -7.0% prior; Y/Y: No est v -9.7% prior

- 06:30 (EU) ESM to sell €2.0B in 3-month bills

- 06:45 (US) Daily Libor Fixing

- 07:30 (TR) Turkey May Effective Exchange Rate (REER): No est v 81.71 prior

- 07:45 (US) Weekly Goldman Economist Chain Store Sales

- 08:00 (HU) Hungary Central Bank (MNB) May Minutes

- 08:00 (BR) Brazil Apr Industrial Production M/M: +0.5%e v -0.1% prior; Y/Y: 7.9%e v 1.3% prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (CL) Chile Apr Economic Activity Index (Monthly GDP) M/M: No est v 0.5% prior; Y/Y: 5.5%e v 4.6% prior

- 08:30 (CA) Canada Q1 Labor Productivity Q/Q: No est v 0.2% prior

- 08:30 (RU) Russia announces weekly OFZ bond auction (held on Wed)

- 08:55 (US) Weekly Redbook Sales

- 09:00 (EU) Weekly ECB Forex Reserves

- 09:00 (MX) Mexico May Consumer Confidence: 85.5e v 85.8 prior

- 09:00 (BR) Brazil May Services PMI: No est v 50.0 prior, Composite PMI: No est v 50.6 prior

- 09:30 (NZ) Fonterra Global Dairy Trade Auction: Dairy Trade price index

- 09:45 (US) May Final Markit Services PMI: 55.7e v 55.7 prelim, Composite PMI: No est v 55.7 prelim

- 10:00 (US) May ISM Non-Manufacturing Composite: 57.6e v 56.8 prior

- 10:00 (US) Apr JOLTS Job Openings: 6.350Me v 6.55M prior

- 11:30 (US) Treasury to sell 4-Week Bills

- 15:00 (MX) Mexico Citibanamex Survey of Economists

- 16:30 (US) Weekly API Oil Inventories

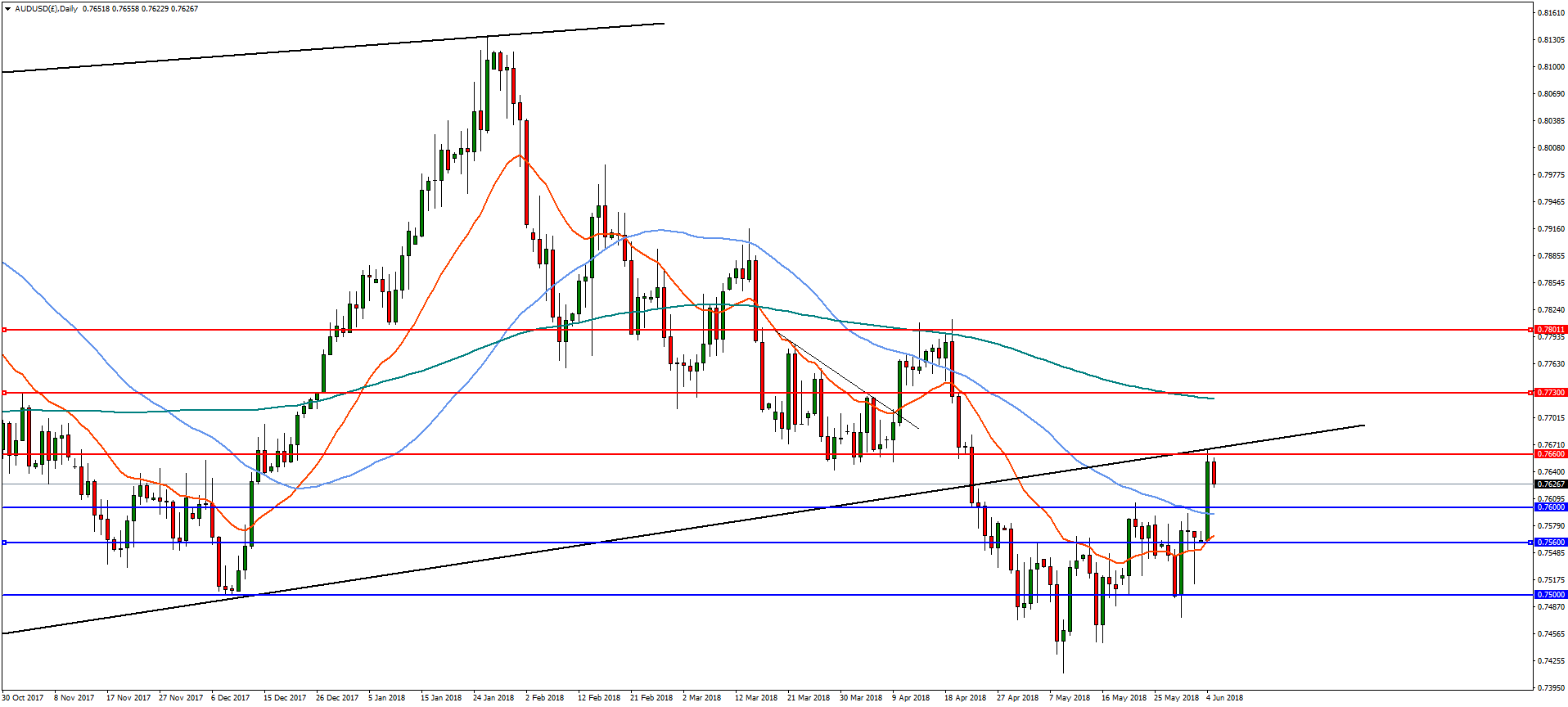

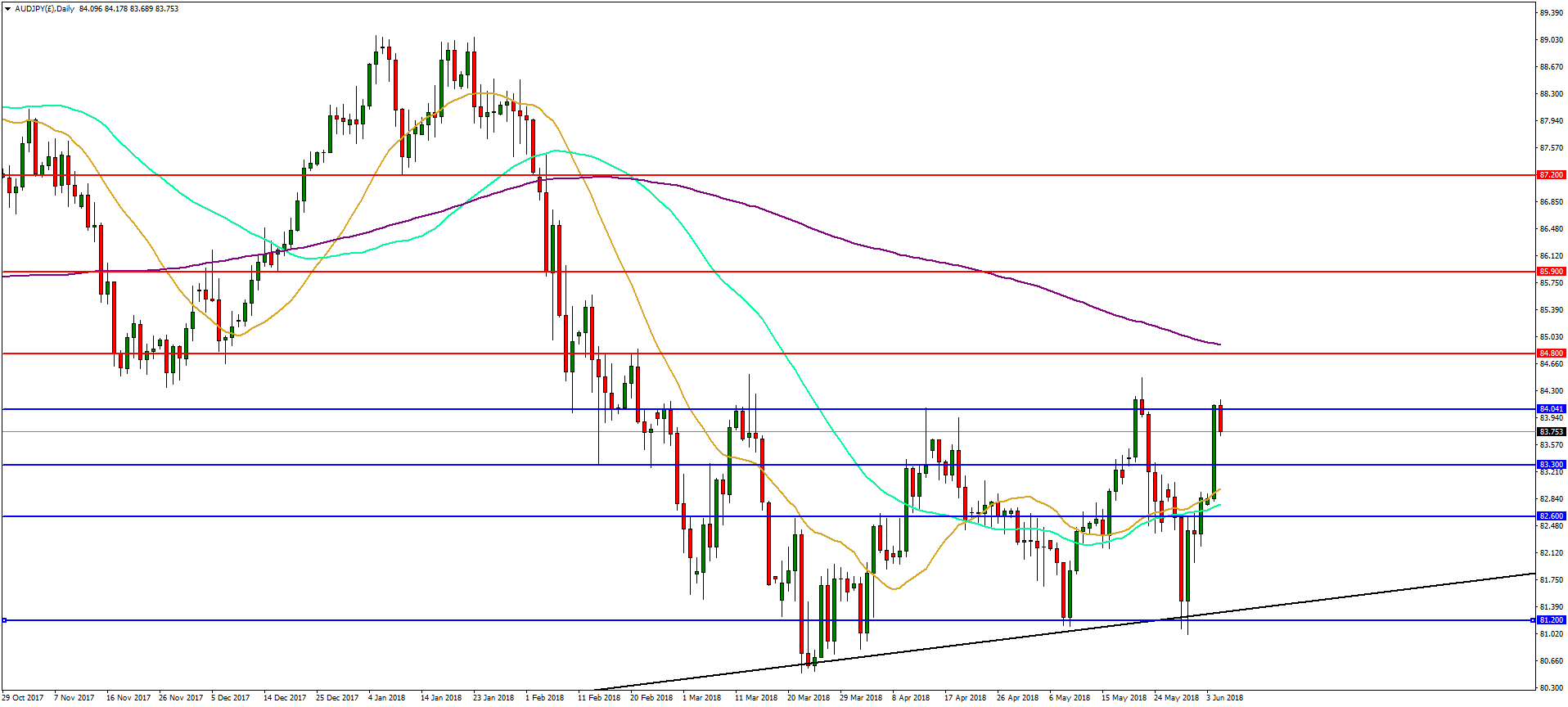

Forex Analysis: AUDUSD And AUDJPY

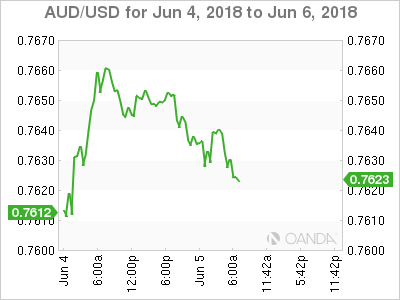

The Australian Dollar (AUD) dripped after the Reserve Bank of Australia (RBA) held its interest rate steady at the record low of 1.5%. The RBA is waiting for signs of wage growth which should improve consumer spending and support inflation. The RBA statement comes after a data release yesterday showing Australian retail sales rising faster than was expected during April. Important economic data in the shape of first-quarter GDP growth will be released on Wednesday. However, the RBA is not expected to hike rates until mid-2019 and so the policy divergence with the U.S. Federal Reserve will exert bearish pressure on the Aussie.

AUDUSD

On the daily chart, the AUDUSD recovery has run into trend line and horizontal resistance at 0.7660. A break of this level could see additional upside to resistance at 0.7730 and 0.7800. However, if the resistance holds, the pair could resume the longer term downtrend with supports at 0.7600 and then 0.7560.

AUDJPY

The sharp rally in AUDJPY over the past month has, once again, stalled at 84.00. In the daily timeframe, AUDJPY needs a decisive break of the 84.00 level to open the way for continued upside to resistance at the 50% retracement of the highs from January at 84.80 followed 85.90. On the flip-side, a bearish reversal from 84.00 could see declines towards 81.20 with support at 83.30 and 82.60.

Italy PM Conte pledges to eliminate the gap in growth between Italy and the EU

Confidence votes on the new Italian government is set to take place in the upper house today and the lower tomorrow. New Prime Minister Giuseppe Conte addressed the upper house today and expressed he's proud of the "radical change", referring to the anti-establishment coalition.

Conte also pledged to reduce public debt, but by growth of the economy, not through austerity. The government's objective is to eliminate the gap in growth between Italy and the EU and he emphasized that must be followed in a framework of financial stability and the trust of markets. He added that Italian debt is fully sustainable today but reduction must still be pursued.

Conte pledged to put an end to the immigration business which has grown out of control. This echoed comment by Interior Minister Matteo Salvini, head of eurosceptic right-wing league that Italy "can't be transformed into a refugee camp".

DAX Jumps As New Italian Government, Korea Summit Stokes Optimism

The DAX has posted sharp gains in the Tuesday session. Currently, the DAX is at 12,897, up 0.99% on the day. In economic news, German Final Services PMI dropped to 52.1, matching the forecast. It was a similar story with Eurozone Final Services PMI, which fell to 53.8, just shy of the estimate of 53.9 points. Eurozone retail sales disappointed, posting a weak gain of 0.1% for a third straight month, but missed the estimate of 0.5%.

Investors have given a thumbs up to developments in Italy, as the county finally has a government after months of political drama. The new coalition is made up of two euro-sceptic parties, the League and the Five-Start Movement, which is likely to cause tensions between Rome and the European Union. After President Sergio Matterella vetoed the choice for finance minister last week, it appeared that the country might be headed for another election and more political uncertainty, and Italian stocks and bonds dropped sharply. However, the crisis is over after the prime minister-elect, Giuseppe Conte, found another candidate for the key finance post. The new government has said it will drastically reduce immigration and raise spending, planks which could put it at odds with EU policy. Although the League and Five Star Movement have not issued any threats to withdraw from the EU or even hold a referendum, there is concern that the fourth largest economy in the eurozone is being steered by a government with a populist, anti-establishment platform.

The on-again-off-again Korea nuclear summit is back on, complete with a starting time. The much-heralded meeting between President Trump and President Kim Jong-un will take place in Singapore on June 12, at 9:00 AM sharp. The summit will mark the face ever face-to-face meeting between leaders of the U.S and North Korea, but Trump has tried to lower expectations, saying that he didn’t expect the sides to sign an agreement. Rather, the meeting would mark the start of a process. North Korea is unlikely to agree to denuclearization, but the fact that the two sides are talking is likely to continue boosting the stock markets.

Euro Calm As German, Euro Services PMIs Within Expectations

EUR/USD is unchanged in the Monday session. Currently, the pair is trading at 1.1697 down 0.01% on the day. On the release front, the focus is on the service sector. Eurozone and German Final Services both dropped in May, but met expectations. Eurozone retail sales remained unchanged at 0.1%, but this missed the forecast of 0.5%. In the US, the ISM Non-Manufacturing PMI is expected to rise to 57.9 points. We’ll also get a look at JOLTS Job Openings, which is expected to drop to 6.49 million.

The euro remains calm this week, as Italy appears to have wrapped up months of political turmoil, as the country finally has a government. The new coalition is made up of two euro-sceptic parties, the League and the Five-Start Movement, which is likely to result in friction between Rome and the European Union. After President Sergio Matterella vetoed the choice for finance minister last week, it appeared that the country might be headed for another election and more political uncertainty, and Italian stocks and bonds dropped sharply. However, the crisis is over after the prime minister-elect, Giuseppe Conte, found another candidate for the key finance post. The new government has said it will drastically reduce immigration and raise spending, planks which could put it at odds with EU policy. Although the League and Five Star Movement have not issued any threats to withdraw from the EU or even hold a referendum on EU membership, there is plenty of concern among investors that the fourth largest economy in the eurozone is being steered by a government with a populist, anti-establishment platform.

Is a new global trade war brewing? There are some ominous signs that the US and some major trading partners are headed in that direction, after the Trump administration slapped tariffs on the European Union, Mexico and Canada on Thursday. The U.S had granted all three trading partners a temporary extension but cited insufficient progress on trade talks as the reason for the tariffs. This has triggered promises of retaliatory tariffs on US products, and tempers were short at the G-7 meeting of finance ministers in Canada on the weekend. U.S Treasury Secretary Steve Mnuchin faced sharp criticism from other finance ministers over the tariffs. The leaders of the G-7 meet in Canada on June 8, and European leaders want to take trade and try to find some compromise with the U.S in order to remove the tariffs.

Dollar Moves Confined As Investors Look For Clues

The risk rally remains afloat despite last week’s geopolitical concerns and pending global tariff fall out.

Capital markets seem content to regroup after recent developments. However, with President Trump stepping up his aggressive trade policies and the ‘populists,’ who are poised to start, governing in Italy, there remains plenty of reasons for caution.

For the intraday investor, the global landscape has not been easy to navigate, since market’s flutter day-over-day from risk-aversion and risk-on while ignoring most economic fundamentals. Aside from Trump drive by tweets, interest rate differentials and politics continue to be the biggest supporter for volumes.

Overnight, Euro and Asian shares were either small down, or trading in a holding patter, while sovereign bond moves have been mixed. G7 currencies again have been confined to a tight range as crude oil climbs.

On tap: U.S. ISM non-manufacturing index is released at 10:00 am EDT. Consensus is looking for signs of growth for the first time in four-months (57.9e vs. 56.8).

1. Stocks confined to tight ranges

Japanese stocks ran into resistance overnight, as its 25-day average, nevertheless, underlying market sentiment remains supportive by last week’s U.S job data and a weakening yen. The Nikkei share average closed +0.3% higher, while the broader Topix was unchanged.

Down-under, Aussie equities again underperformed Asia-Pacific counterparts, dented by an early overnight slip in commodities. The S&P/ASX 200 ended down -0.5% to erode most of previous sessions rebound. In S. Korea, the Kospi lost –o.15%.

In Hong Kong, stocks rallied a tad, with sentiment aided by a private survey showing China’s services sector expanded at a steady pace last month. The Hang Seng index rose +0.3%, while the China Enterprises Index gained +0.1%.

Note: China’s services sector expanded at a solid pace last month, with companies accelerating hiring on the back of the strongest optimism for future growth in 11-months.

In China, the blue-chip CSI300 index rose +1.0%, while the Shanghai Composite Index ended up +0.7%.

In Europe, regional stocks opened slightly lower across the board and have since reversed to trade mixed. Currently, Italy is the best performer as PM faces first round of confirmation votes.

U.S stocks are set to open in the ‘black (+0.1%).

Indices: Stoxx50 0.2% at 3,478, FTSE -0.6% at 7,694, DAX +0.4% at 12,823, CAC-40 +0.3% at 5,490; IBEX-35 +0.3% at 9,775, FTSE MIB +0.5% at 22,118, SMI -0.4% at 8,599, S&P 500 Futures +0.1%.

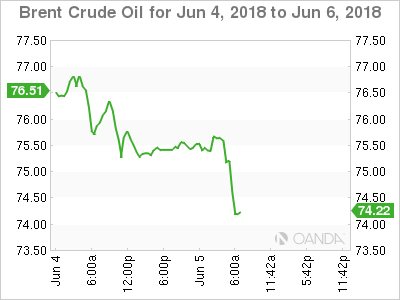

2. Oil rises on expected stockpile drop, gold higher

Oil prices have rebounded a tad on expectations that U.S inventories may decline, but increasing U.S production and concerns that OPEC may raise output continue to provide resistance.

Brent crude futures have added +25c, or +0.33%, to +$75.53 a barrel, after settling down -2% at +$75.29 yesterday. U.S West Texas Intermediate (WTI) crude is up +44c, or +0.68%, at +$65.19 a barrel. It finished the previous session +1.6% lower at +$64.75.

OPEC is due to meet in Vienna on June 22 to decide whether the group, including Russia, will raise output to ease concerns over potential supply shortfalls from Iran and Venezuela.

Investors will take their cues from this week’s production and supply data. U.S stocks, the world’s biggest oil consumer, are expected to fall about -2.5m barrels on average in the week ended June 1.

Note: The number of rigs drilling stateside is up by two in the week to June 1, bringing the total to 861, the most since 2015.

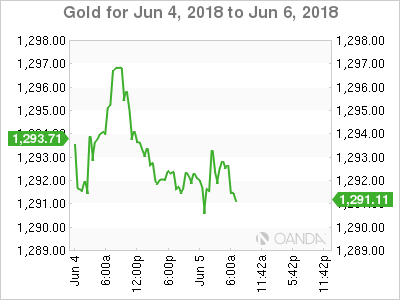

Ahead of the U.S open, gold prices are little changed overnight, after closing lower in three previous sessions, as investors seem to be opting for riskier assets amid increasing prospects of another Fed hike following strong economic data. Spot gold is flat at +$1,291.51 per ounce, while U.S gold futures for August delivery are down -0.1% at +$1,295.60 per ounce.

3. Yields back up

U.S government bonds weakened again yesterday as investors look ahead to next week’s Federal Open Market Committee (FOMC) meeting next week at which policy makers are expected to raise interest rates.

The yield on the benchmark U.S 10-year Treasury note has backed up to +2.925%. The yield on the two-year Treasury note, which is more sensitive to expectations for Fed policy, has backed up +2 bps to +2.496%.

Higher yields are being supported by Fed funds futures, which are showing an increase in the odds the Fed will raise interest rates three more times this year. That probability has rallied to +40% yesterday from +34% on Friday.

Note: They odds fell as low as +13% last week after the minutes from the Fed’s May meeting reflected a preference for a gradual path of rate increases, and concerns about Italy’s antiestablishment coalition government rose.

Elsewhere, eurozone periphery government bonds – Italy, Spain and Portugal -trade slightly weaker this morning, indicating the fragility of the recovery from massive selloffs at the beginning of last week.

The 10-year Italian BTP’s is trading +4 bps higher at +2.59%, the 10-year Portuguese yield is up +2.6 bps at +1.81% and the 10-year Spanish bond yield is up +1.9 bps at +1.36%.

As expected, the Reserve Bank of Australia (RBA) kept overnight rates on hold at +1.5%. Their June policy statement last night was generally in line with the previous months, however it noted the political situation in Italy and economic developments in emerging markets. The central bank also alluded, for the first time, to the misbehaviour of domestic banks.

4. Dollar confined for the time being

The USD remains steady in a tight range overnight, but is off its recent cycle highs against G7 currency pairs.

The GBP (£1.3378) is slightly higher on stronger U.K services PMI print (see below). Brexit talks on the future relationship between the U.K and EU are set to resume in Brussels this week. U.K government has stated that the Brexit withdrawal bill would return to the House of Commons on Tuesday, June 12 setting up a showdown as about a dozen backbenchers threatened to inflict a defeat in a vote over future customs arrangements.

Note: The E.U has previously asked for clarity on Brexit from the U.K as the run-up to the EU Summit on June 28 and 29th.

5. U.K. services PMI picked up in May

U.K data from Markit this morning showed that activity in the U.K’s dominant services sector picked up last month, adding to recent indications the economy is rebounding from a weak start to the year. Their measure of activity rose to 54.0 in May from 52.8 in April, it’s highest for three-months.

Note: The U.K economy slowed sharply in Q1, prompting the BoE to forgo an expected rate hike at their May meeting. However, officials signalled that they still expect to tighten policy if that slowdown proves to be short-lived.

A similar survey of manufacturers released last Friday also pointed to a May pickup.

Markit’s chief business economist stated that “the signs of economic growth rebounding in Q2 will likely up the odds of the BoE hiking interest rates again in coming months, likely August.”

Nevertheless, the outlier for many remains Brexit, U.K businesses continue to look clarity and direction from policy makers with Brexit less than a year away.

UK Services Data Supportive For Rate Hike This Year

- Investors Buoyed By Easing Political Threat From Europe;

- UK Services Data Supportive For Rate Hike This Year;

- US PMIs in Focus as Investors Eye Second Quarter Pick Up.

US equity markets are poised to open a little higher again on Tuesday, buoyed again by an apparent easing of political stress in Europe which was weighing on sentiment last week.

Ahead of the G7 meeting, there is plenty to be wary about for investors, most notably the threat of a full blown trade war with Donald Trump having dealt the first blow with tariffs on the European Union, Canada and Mexico. Right now though, investors appear to be taking it in their stride with indices continuing their gradual recovery from the sell-off earlier in the year.

A rally in the pound is weighing on the FTSE early in the European session, leaving it as the only major index in the red, down almost half a percentage point. The sterling gains came on the back of a stronger than expected services PMI report for May, with the survey rising from 52.8 to 54. Better weather and the Royal wedding likely contributed to rebound in what is by far the most important sector for the UK economy but there were other interesting takeaways as well.

Not only did we see an uptick in business activity, which will be welcomed after a tough first quarter that was severely hampered by bad weather, but there was also mention of companies having to pay higher salaries due to a lack of skilled staff. This will be music to the ears of Bank of England policy makers who are clearly intent on raising interest rates this year, despite having pushed it back in May after the first quarter slowdown.

It wasn’t all good news though, with businesses citing Brexit uncertainty as being responsible for lower levels of spending, something that will likely continue to weigh this year until we have more clarity on the future relationship with the EU. The BoE will still likely push on with raising interest rates regardless of this, assuming negotiations don’t collapse, which is why we’re seeing such positive moves in the pound this morning. The inverse relationship with the FTSE 100 due to the amount of profits generated abroad for companies in the index is why we’re seeing such a negative response here.

We’ll also get survey’s from the US today with the Markit Services and ISM non-manufacturing PMIs both being released. As with the UK, the services sector is a huge component of the US economy and investors are looking for further evidence that the country continues to perform strongly and is coping with a rising interest rate environment. Growth in the first quarter was relatively modest but we’re expecting a strong performance in the March to June period.

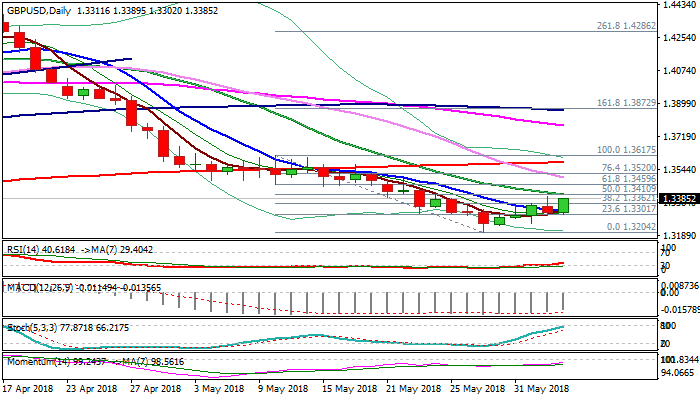

GBPUSD Outlook: Rises On Upbeat UK Services PMI Data, Focus Turns Towards Key 1.3410 Barrier

Cable rallied on higher than expected UK Services PMI data which rose to 54 in May (the highest since Feb) beating forecast at 52.9. Fresh bullish acceleration from pre-data low at 1.3333 hit session high at 1.3384 and also broke above cracked barrier at 1.3362 (Fibo 38.2% of 1.3617/1.3204) with eventual close above here (following repeated failures on Fri/Mon) to generate bullish signal. Near-term picture improved on fresh rally, turning near-term bias higher, however, close above Monday's spike high at 1.3398 is seen as minimum requirement to keep bullish bias for test of key barrier at 1.3410 (50% of 1.3617/1.3204 / falling 20SMA). Firm break here would signal continuation of recovery from 1.3204 (29 May low). Converged 5/10SMA are attempting to form bull-cross and mark solid support at 1.3325 which is expected to contain extended dips.

Res: 1.3398, 1.3410, 1.3459, 1.3499

Sup: 1.3362, 1.3333, 1.3302, 1.3253

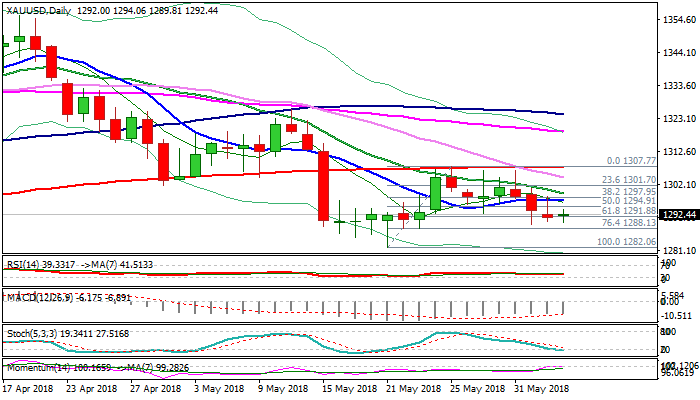

Spot Gold Outlook – Directionless Between $1291 Fibo Support And 10SMA At $1297

Spot Gold holds in a narrow range on Tuesday and confirms indecision after Monday’s action ended in Doji candle with long upper shadow.

Overall structure remains bearish, but the price is struggling at $1291 pivot (Fibo 61.8% of $1282/$1307 bull-leg) following repeated failure to close below cracked support.

Strong momentum and slow stochastic entering oversold zone may keep the downside limited further, but recent upside attempts were repeatedly capped by 10SMA ($1297) and also weighed by 4-hr cloud (spanned between $1294 and $1299).

Break and close above 10SMA is needed to ease downside pressure and signal higher base formation for possible further recovery.

On the other side, easing concerns about geopolitical tensions between the US and North Korea reduced safe-haven demand, while gold also faces further pressure on strong expectations of US rate hike this month.

Bearish scenario sees eventual close below $1291 pivot as a trigger fresh weakness which could extend towards key support at $1282 (21 May low).

Res: 1294, 1297, 1300, 1304

Sup: 1291, 1288, 1285, 1282