Sample Category Title

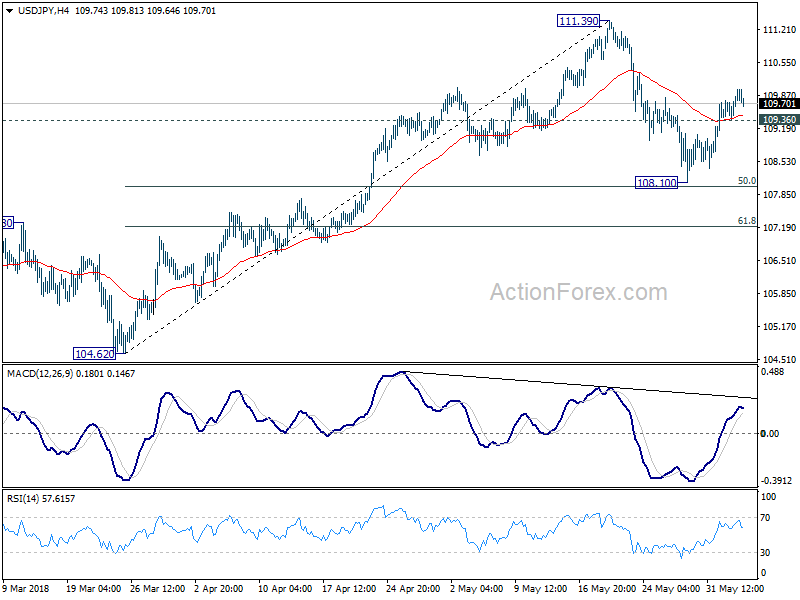

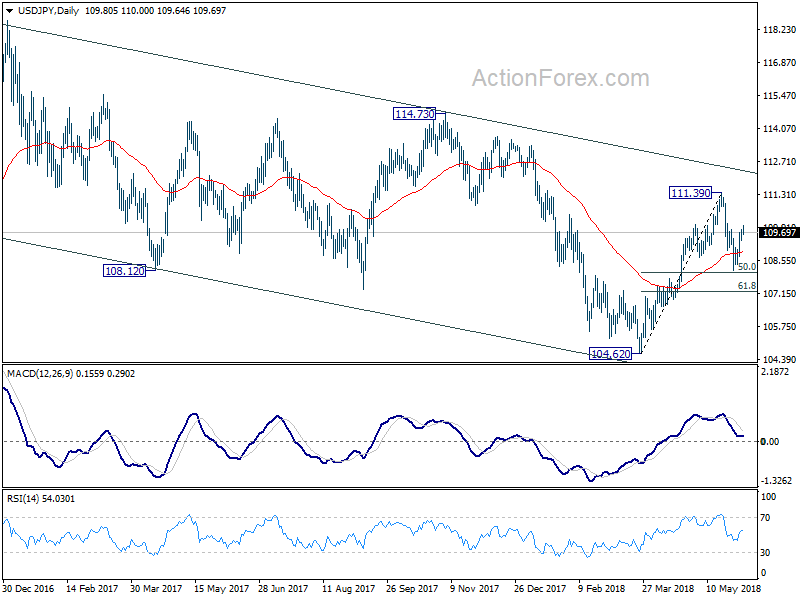

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.50; (P) 109.69; (R1) 110.02; More...

With 109.36 minor support intact, intraday bias in USD/JPY remains mildly on the upside for retesting 111.39. Break will resume the rebound from 104.62 and target a test on 114.73 key resistance level. However, on the downside, below 109.36 minor support will delay the bullish case and turn bias neutral again.

In the bigger picture, at this point , we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

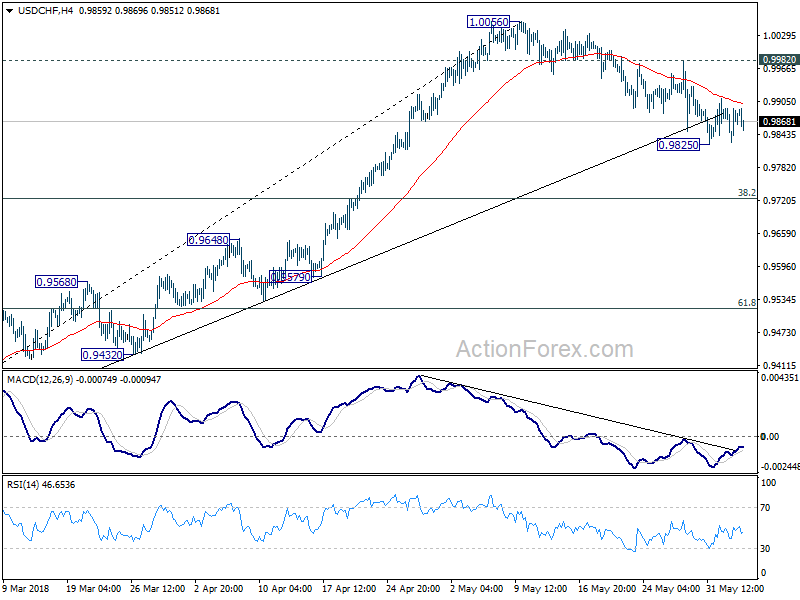

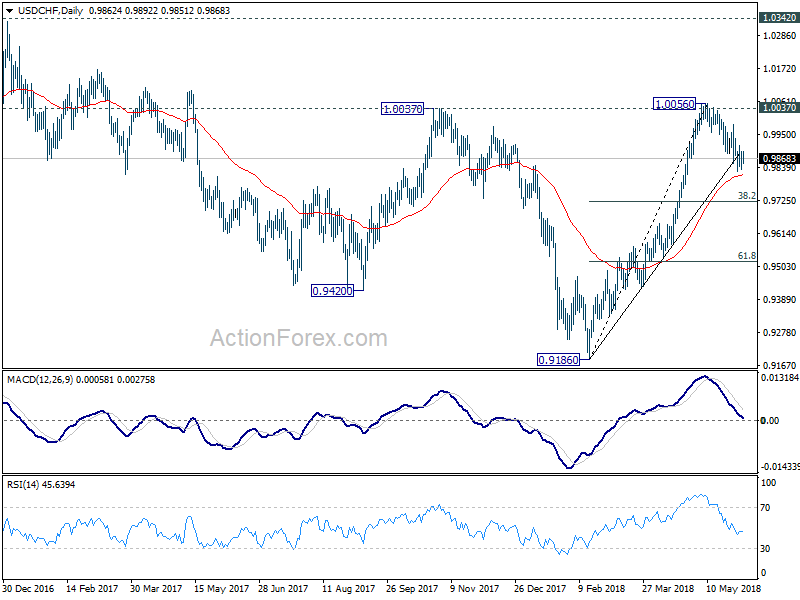

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9842; (P) 0.9868; (R1) 0.9908; More...

Intraday bias in USD/CHF stays neutral as it's bounded in tight range above 0.9825. On the downside, break of 0.9825 will indicate that fall from 1.0056 is correcting whole rise from 0.9186. In that case, deeper decline would be seen to 0.9724 fibonacci level before completion. On the upside, above 0.9982 minor resistance will suggest that the pull back is finished and bring retest of 1.0056.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

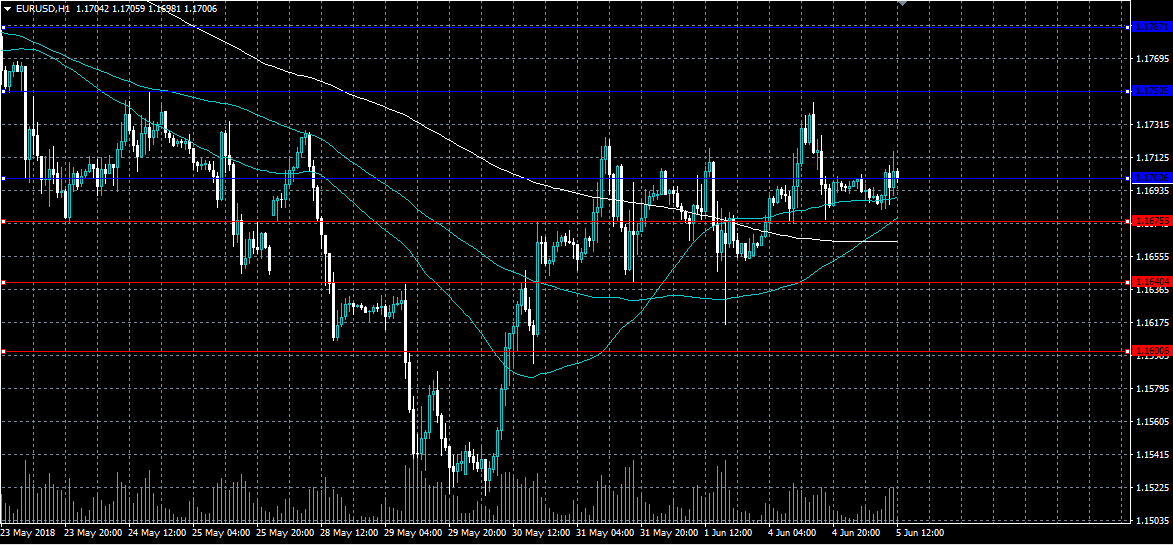

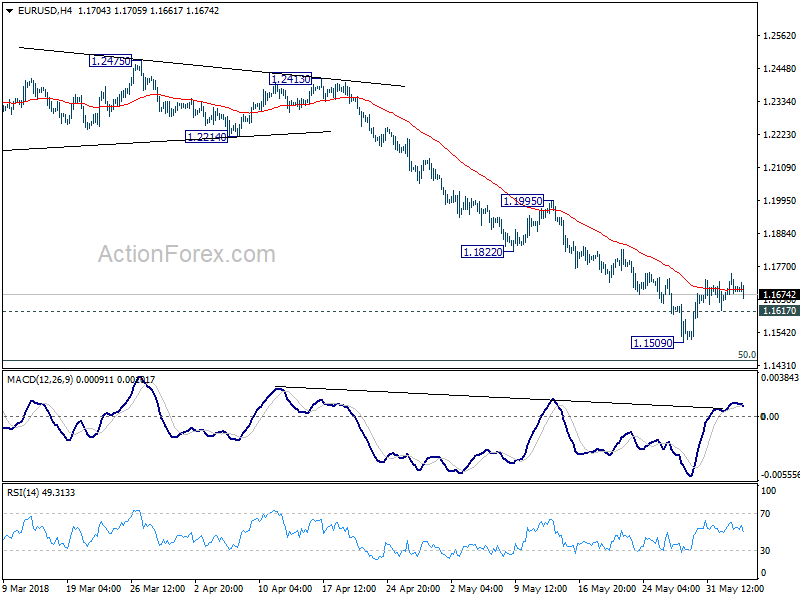

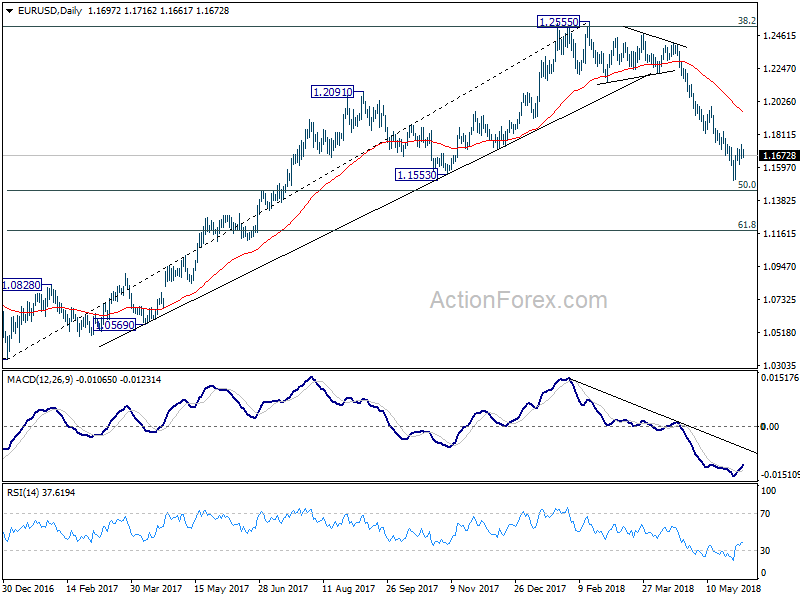

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1655; (P) 1.1700 (R1) 1.1740; More.....

EUR/USD is staying in correction from 1.1509 and outlook is unchanged. Stronger recovery cannot be ruled out. But in that case, upside should be limited by 1.1822/1995 resistance zone to bring fall resumption eventually. On the downside, below 1.1617 minor support will bring retest of 1.1509 low first. Break will resume the decline from 1.2555 and target 50% retracement of 1.0339 to 1.2555 at 1.1447. Break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

Stock Markets Elevated by Tech Bulls, Rand Tumbles

It’s both alarming and somewhat frightening how global equity markets have powered higher despite the simmering trade tensions between the United States and its allies.

While an incredible rally in technology shares has supported global stocks, there is a suspicion that investor complacency towards the renewed trade tensions continues to play a key role. Although stock markets have scope to venture higher amid the apparent appetite for risk, the question is - for how long? It must be kept in mind that President Trump's trade wars remain a major threat to financial markets and this is likely to continue weighing on sentiment. With Trump’s unpredictability fostering a sense of uncertainty over trade developments, stock markets remain vulnerable to losses.

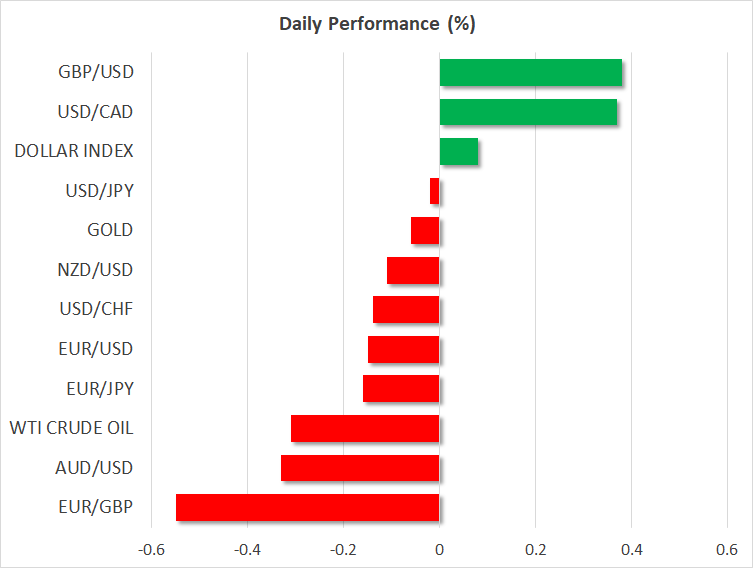

Sterling boosted by positive services data

The British Pound appreciated against the Dollar after UK services accelerated in May, easing some concerns over the health of the UK economy.

The Purchasing Manager’s Index for UK services exceeded expectations in May by rising to 54.0 from April’s 52.8. While the recovery in services is encouraging and may stimulate expectations of a BoE rate hike later this year, Brexit-related uncertainties continue to weigh on sentiment.

Taking a look at the technical picture, the GBPUSD remains bearish on the daily charts despite the recent rebound. The upside momentum could send prices towards 1.3450 before the bearish trend resumes. Alternatively, a breakdown below 1.3300 could encourage a decline towards 1.3210.

Dollar waits for ISM Non-Manufacturing PMI

The Dollar held steady during Tuesday’s trading session as investors awaited the US ISM Non-Manufacturing PMI figures for May which could provide fresh insight into the health of the US economy.

Markets expect the ISM Non-Manufacturing PMI index to rise 58.00 in May, which could boost optimism over the US economy being on a track for a solid second quarter. The Dollar is likely to receive a boost if the data exceeds market expectations.

Focusing on the technical picture, the Dollar Index remains bullish on the daily charts. Prices have scope to attack 95.00 as long as bulls can defend 94.00. Alternatively, sustained weakness below 94.00 could invite a decline towards 93.40.

Rand tumbles on disappointing GDP data

Buying sentiment towards the South African Rand sharply deteriorated following reports of the South African economy suffering its worst quarterly growth in almost a decade.

The economy shocked markets by shrinking 2.2% on an annualized basis during the first quarter of 2018. This was a complete turnaround to the positive end of 2017 where final quarter growth rose 3.1%. With the GDP report heavily disappointing, sentiment towards the South African economy is likely to receive a heavy blow with the Rand on the receiving end.

Could the abysmal GDP reading be attributed to the weakening of the “Ramaphosa effect” that was noticed when Cyril Ramaphosa became the President of South Africa? This is the question everyone is asking.

Focusing on foreign exchange, the USDZAR has jumped towards 12.700 as of writing and has scope to challenge 12.750 if the Rand continues to depreciate.

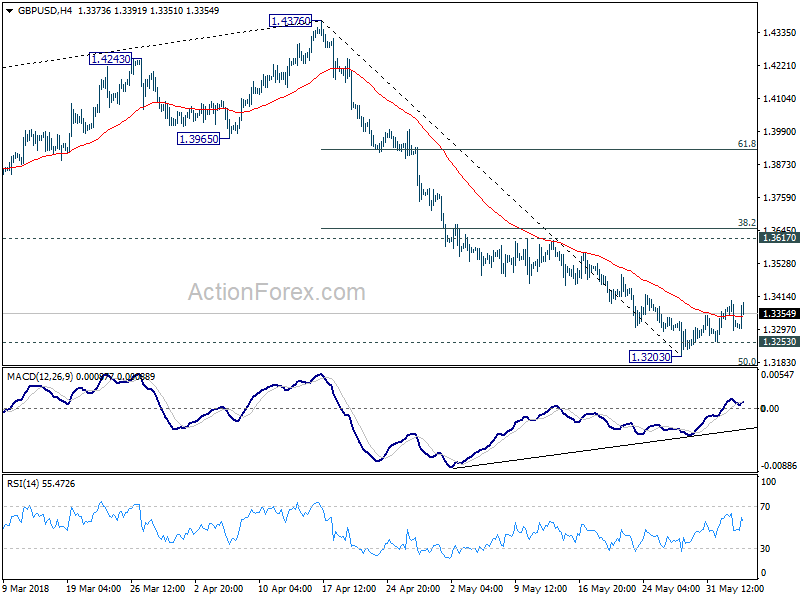

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3272; (P) 1.3335; (R1) 1.3376; More...

GBP/USD rebound notably today but it's limited below yesterday's high at 1.3397 so far. Outlook remains unchanged too. Above 1.3397 will extend the corrective rise from 1.3203. But upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3253 minor support will likely resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

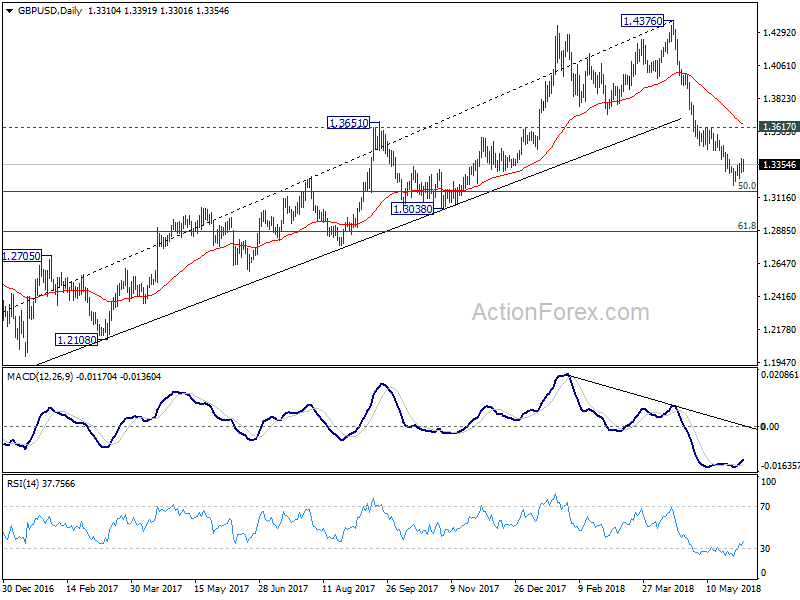

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3648) holds, even in case of strong rebound.

Sterling Lifted by Services PMI But Buyers Hesitate

Sterling is so far the strongest major currency today. Better than expected UK services PMI raised the chance of an August BoE hike. But there is no follow through buying in the Pound yet. BoE's decision will be heavily data dependent, and there are still two more months of data to go. Meanwhile, Australian Dollar continues to pare back this week's gain as RBA statement provided little inspiration. The Aussie will turn to Q1 GDP to be released in the upcoming Asian session.

Canadian Dollar follows Aussie as the second weakest one. Today's decline in oil price is a factor that's weighing on the Loonie. Bloomberg reported that the US has requested OPEC to raise output by 1m barrels a day. Talking about the US, dollar is trading mixed for the moment. Rebound in treasury yields gave the greenback a lift yesterday. And Dollar will look into yields for some more fuel again today.

UK PMI services rose to 54.0, up the odds of BoE August hike

UK PMI services rose to 54.0 in May, up from April's 52.8, above expectation of 52.9. Markit Chief Business Economist Chris William said in the release that the three PMI surveys indicate that GDP looks set to rise by 0.3-0.4% in Q2. And, signs of rebound in growth in Q2 will likely "up the odds of the Bank of England hiking interest rates again in coming months, likely August". Though, he warned that "forward looking indicators suggesting that the economy could relapse, a rate rise is by no means assured."

Eurozone PMI composite hit 1.5 year low, outlook darkened dramatically

Eurozone PMI services was finalized at 53.8 in May, revised down from 53.9, vs April's 54.8. PMI composite was finalized at 54.1, down from April's 55.1, hitting one-and-a-half year low. Markit's Williamson noted in the released that "the region is on course for its worst quarter since 2016". Though, Eurozone growth would still hit 0.4-0.5% in Q2. He added that "with the economic indicators turning down at the same time as political uncertainty has spiked higher, the eurozone's outlook has darkened dramatically compared to the sunny forecast seen at the start of the year."

Also from Eurozone, Italy services PMI rose to 53.1 in May, up from 52.6. France services PMI was finalized at 54.3, unrevised. Germany services PMI was finalized at 52.1, unrevised. Eurozone retail sales rose 0.1% mom in April, below expectation of 0.5% mom.

Italy PM Conte pledges to eliminate the gap in growth between Italy and the EU

Confidence votes on the new Italian government is set to take place in the upper house today and the lower tomorrow. New Prime Minister Giuseppe Conte addressed the upper house today and expressed he's proud of the "radical change", referring to the anti-establishment coalition.

Conte also pledged to reduce public debt, but by growth of the economy, not through austerity. The government's objective is to eliminate the gap in growth between Italy and the EU and he emphasized that must be followed in a framework of financial stability and the trust of markets. He added that Italian debt is fully sustainable today but reduction must still be pursued.

Conte promised to put an end to the immigration business which has grown out of control. This echoed comment by Interior Minister Matteo Salvini, head of eurosceptic right-wing league that Italy "can't be transformed into a refugee camp".

RBA stands pat and maintains neutral stance

RBA left the policy rate unchanged at 1.50% today as widely expected, and made no change to the monetary policy guidance. The central bank remained confident over the global economic outlook. Indeed, it has so far not commented about the slowdown in economic activities in the Eurozone, UK and Japan, etc. At home, the members continued to expect growth to pick up and average a bit above 3% in 2018 and 2019.

Meanwhile, the sluggish improvement in wage growth and inflation would continue to some time. An interesting reference RBA made was that "while there may be some further tightening of lending standards, the average mortgage interest rate on outstanding loans is continuing to decline". This appears to be a response to those proposing a rate cut to offset the current tightening in credit condition. In short, the RBA should leave the policy rate unchanged for the rest of the year.

More in RBA Left Cash Rate Unchanged, Affirmed that Credit Condition Remained Accommodative.

NZ Treasury: Q1 growth may fall short of 0.7% forecast

In the Monthly Economic Indicator report published today, New Zealand Treasury noted that the tracking of March quarter data suggested real GDP growth may fall short of 0.7% as forecast in the Budget Economic and Fiscal Update (BEFU) 2018. Nonetheless, June quarter activity indicators have been "a little more positive". Subdued wage pressures are likely contributing to low inflation, and the expectation that RBNZ will keep OCR at 1.75% "for some time to come".

Risks are skewed to the downside as led by international developments. In particular, the Treasury noted slowdown in Japan, Eurozone and UK in Q1. And it warned that political instability in Italy will drag Eurozone growth further. Nonetheless, the outlook for China and the US "remains relatively positive".

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3272; (P) 1.3335; (R1) 1.3376; More...

GBP/USD rebound notably today but it's limited below yesterday's high at 1.3397 so far. Outlook remains unchanged too. Above 1.3397 will extend the corrective rise from 1.3203. But upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3253 minor support will likely resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3648) holds, even in case of strong rebound.

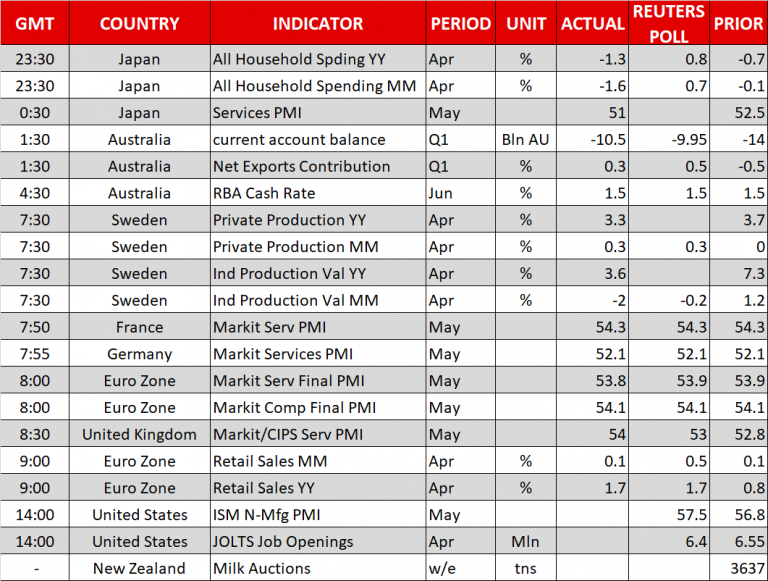

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y May | 2.80% | -4.20% | ||

| 23:30 | JPY | Household Spending Y/Y Apr | -1.30% | 0.80% | -0.70% | |

| 1:30 | AUD | Current Account (AUD) Q1 | -10.5B | -9.9B | -14.0B | -14.7B |

| 1:45 | CNY | Caixin PMI Services May | 52.9 | 53 | 52.9 | |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 7:45 | EUR | Italy Services PMI May | 53.1 | 52.9 | 52.6 | |

| 7:50 | EUR | France Services PMI May F | 54.3 | 54.3 | 54.3 | |

| 7:55 | EUR | Germany Services PMI May F | 52.1 | 52.1 | 52.1 | |

| 8:00 | EUR | Eurozone Services PMI May F | 53.8 | 53.9 | 53.9 | |

| 8:30 | GBP | Services PMI May | 54 | 52.9 | 52.8 | |

| 9:00 | EUR | Eurozone Retail Sales M/M Apr | 0.10% | 0.50% | 0.10% | |

| 12:30 | CAD | Labor Productivity Q/Q Q1 | 0.30% | 0.20% | ||

| 13:45 | USD | US Services PMI May F | 55.7 | 55.7 | ||

| 14:00 | USD | ISM Non-Manufacturing Composite May | 57.4 | 56.8 |

Canadian Dollar and oil dip as US forces OPEC to raise output

The dip in Canadian Dollar today is apparently due to the fall in oil prices. At the time of writing, WTI crude oil is down -0.5 at 64.25.

The selloff in oil comes after Bloomberg reported that the US is trying to force OPEC to raise output by 1m barrels a day. While the US government has regularly encouraged OPEC to rise production, it's unusual to put up a number. There is no details on why there was such a request, what ground the US was on, what the US was going to exchange for the production hike, and why 1m barrels but not other numbers, who were in touch with OPEC and raised the request, through what mechanism was the request made. Based on such non-existing transparency, it seems like OPEC as a cartel is no different from OPEC + US as another cartel.

It's also reported that the request of the US was debated at a meeting of some Arab oil ministers over the weekend in Kuwait city. And a statement came after that pledging to "ensure stable oil supplies are made available in a timely manner to meet growing demand and offset declines in some parts of the world."

Pound Wins on Services PMI; Oil Down ahead of US Oil Inventories

Here are the latest developments in global markets:

FOREX: The British pound was the best performer during the early European afternoon, trading 0.55% higher against the dollar on the day at 1.3387 after the UK’s services PMI reading rose more than expected. This was also perceived as a sign of economic strength that could persuade BoE policymakers to raise interest rates in August. Versus the Japanese yen, sterling picked up by 0.44% to 146.80. On the other hand, an upward revision to previous Eurozone retail sales figures didn’t help euro/dollar, with the pair edging down to 1.1690 (-0.07%). May’s retail sales came in line with expectations on a yearly basis, whereas on monthly terms they missed forecasts. In Italy, the new Prime Minister, Giuseppe Conte, expressed in Parliament that Italy’s interests coincide with European ones, saying at the same time that the country’s public debt is sustainable. Euro/pound declined by 0.56% to 0.874, erasing yesterday’s gains. Dollar/yen was flat at 109.75 in the absence of major economic announcements and ahead of data releases later today. The dollar index was also moving sideways, changing hands at 94.02. The loonie was on the back foot, retreating by 0.30% versus the greenback. Yesterday, the IMF said that policymakers need to enhance their policy buffers and plan structural reforms as the risk is high due to trade uncertainties and the impact of US tax cuts. In antipodean currencies, auddie/dollar remained on the downside, last seen at 0.7617 (-0.34%), after the RBA’s rate statement reiterated worries on wage growth and inflation earlier today. Kiwi/dollar eased to 0.7021 (-0.11%) before the release of global dairy prices later today.

STOCKS: European stocks were all in the green at 0900 GMT except Britain’s FTSE 100 which dipped into losses, losing 0.38%, after an upbeat services PMI survey pushed the pound higher. Loses in the financial sector were also weighing on Britain’s FTSE following the UK government’s sale of its stake in the Royal Bank of Scotland. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.26% and 0.14% respectively. The German DAX 30 surged by almost 1.0% with tech stocks leading the gains, the French CAC 40 rose by 0.58%, while the Italian FTSE MIB 100 continued to pare losses linked to last week’s political risks, climbing by 0.77%. Spain’s IBEX 35 was also on the recovery, increasing by 0.58%. Futures tracking US stock indices were flashing green, pointing to a positive open.

COMMODITIES: Oil prices were on the backfoot as supply concerns continued to weigh, with investors speculating that OPEC could raise its output this month at its policy meeting at a time when US production is rising to near record levels. WTI crude was last seen slightly down on the day at $64.77/barrel, while the London-based Brent posted sharper losses, falling by 0.94% to $74.58/barrel. Meanwhile the Saudi Arabian energy minister stated today the supply release will be gradual, while Bloomberg headlines reported that the US is planning to ask OPEC for an output hike of 1 million bpd. In precious metals, gold was moving sideways at $1,292.04/ounce.

Day Ahead: US ISM non-manufacturing PMI & JOLTS job openings in spotlight; Global dairy auction coming up

In terms of economic data, one of the major releases left on the agenda today is the US ISM non-manufacturing PMI, which is due at 1400 GMT. Expectations are for the print to reach 57.5 in May, from 56.8 previously. A stronger than expected reading could provide a further boost to the US dollar, which was trying to regain its positive footing against the Japanese yen in the previous couple of days. Additionally, a bit earlier, the US will see the release of May’s final Markit services and composite PMI’s at 1345 GMT. The services PMI is expected to remain the same at 55.7 as the preliminary reading.

At 1400 GMT, the US JOLTS job openings will be the figures likely to attract some interest as well. Specifically, the report published by the Burau of Labor Statistics is likely to show that 6,400 million positions opened in December compared to 6,550 million seen in the preceding month.

In energy markets, investors will look forward to the API weekly report due at 2030 GMT which tracks the level of the US crude, gasoline and distillates stocks, as concerns over rising US output linger in the market.

In other commodities, global milk auctions will be also eyed, probably, bringing some volatility to the kiwi as New Zealand is a major dairy exporter. However, the release time is tentative.

Overnight, aussie traders are likely to turn their attention on the Australian GDP figure for the first quarter of 2018 (0130 GMT). According to the forecasts, the Australian economy will likely have expanded by 0.9% q/q in the March quarter from 0.4% in the previous quarter. On a yearly basis, the GDP growth is projected to tick higher to 2.8% from 2.4% before. On Monday, the Australian dollar hovered near a 6-week high following a flurry of upbeat data releases.

The time of the meeting between the US President, Donald Trump, and the North Korean leader, Kim Jong Un in Singapore on June 12 has been set at 1700 GMT.

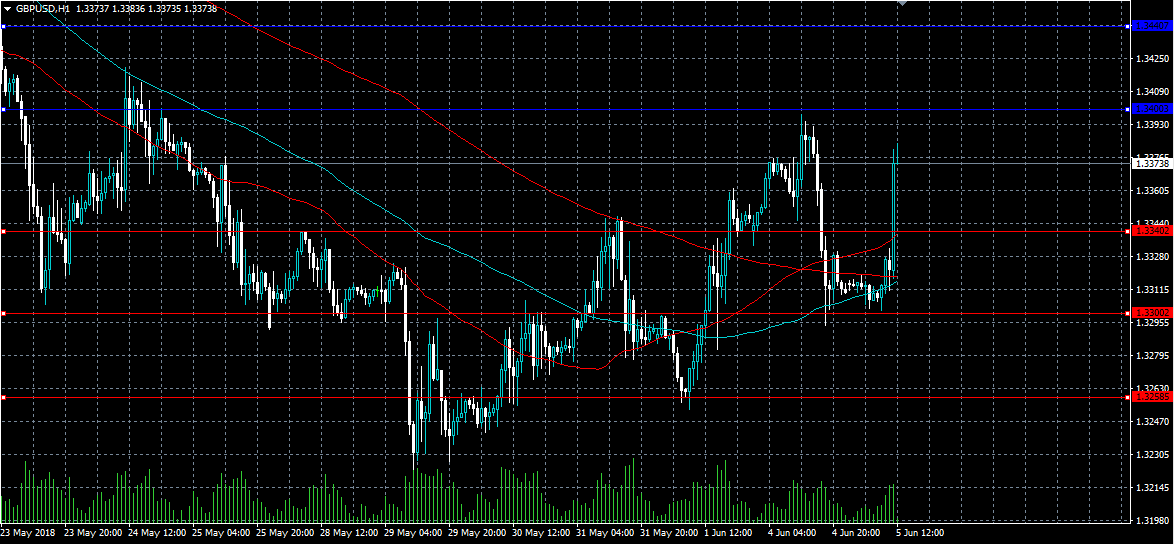

GBPUSD Now Bullish Above 1.3340 Level

The British pound has moved sharply higher against the US dollar, following the release of much better than expected PMI Services data from the United Kingdom economy. The GBPUSD pair currently trades around the 1.3370 level, after finding strong dip-buying demand from the 1.3300 level earlier today. Traders now look for further sterling gains above the 1.3400 level and the release of high-impacting economic data from the United States.

The GBPUSD pair is intraday bullish while trading above the 1.3340 level, key resistance is now located at the 1.3400 and 1.3440 levels.

If the GBPUSD pair moves below the 1.3340 level, we may see sellers testing the 1.3300 support level once again.

EURUSD Only Bearish Below 1.1700 Level

The euro continues to hold around the 1.1700 level against the US dollar, after buyers failed to build on bullish trading momentum above the 1.1715 level. The EURUSD pair is likely to see selling interest accelerate while trading below the 1.1700 level, with strong support found below at the 1.1675 level. Traders now look towards the release of high-impacting Jobs, Services and Manufacturing data from the United States economy.

The EURUSD pair is intraday bearish while trading below the 1.1700 level. Key support is located at the 1.1675 and 1.1640 levels.

If the EURUSD pair moves above the 1.1700 level, buyers may push price towards the 1.1750 and 1.1787 resistance levels.