Sample Category Title

IMF: Canada outlook subjects to significant risks, domestic and external

In a report released yesterday, IMF noted that the 3% growth in 2017 in Canada was the highest among G7 nations in the year. But going ahead, the economic outlook is subject to "significant risks, domestic and external".

Domestically, a key risk is sharp correction in the housing market. That could be triggered by a "sudden shift in price expectations or a faster-than-expected increase in mortgage interest rates". And, the banking system is "heavily exposed to household and corporate debt." Thus, if housing correction is accompanied by rise in unemployment and sharp contraction in private consumption, "risks to financial stability and growth could emerge".

Externally, the medium term impact of US tax cuts could make Canada a "less attractive destination for investment". Failure to reach a NAFTA agreement within a reasonable timeframe could impact investment and growth for an "extended period". And return to WTO rules could cut GDP growth by -0.4%. Other external risks include weaker growth in key advanced economies, sharp slowdown in China, tighter global financial conditions.

Regarding monetary policy, IMF said BoC should tighten "gradually" as "inflationary pressures are building and higher interest rates will help activity and inflation converge toward more sustainable levels." But the current balance of risks warrants "gradual policy normalization."

Full report here.

BoE Tenreyro stood pat in may to wait a little more

BoE MPC member Silvana Tenreyro said yesterday that "much of the downside Q1 GDP news is likely to be erratic". However, that still increased the "possibility of some underlying weakness in demand".

Back in the May meeting, Tenreyo said the costs of waiting-and-see for a short period were relatively slow. And BoE will likely get a "significantly clearer picture of the underlying strength of domestic demand quite soon". Therefore, there were "to leaving policy unchanged."

Overall, Tenreyo said "while I anticipate that a few rate rises will be needed, the timing of those rate rises is an open question."

Tenreyro's messages were consistent with BoE's own forecast in the inflation report that there would be a rate hike in August. That is, BoE opted to wait a little while more in May till August to make a decision. And, that is data dependent.

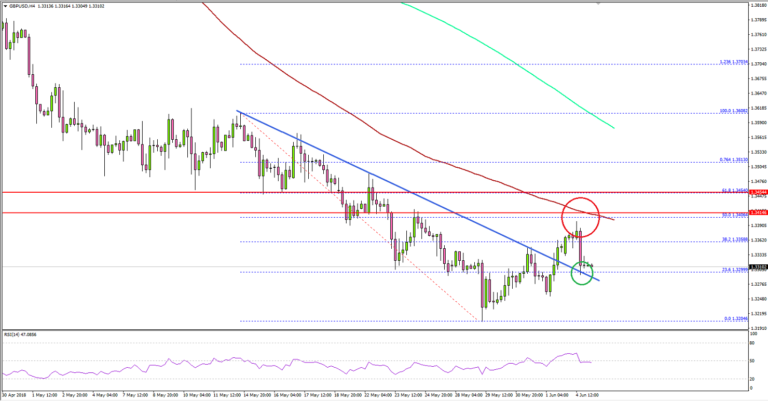

Can GBP/USD Move Past 1.3400?

Key Highlights

- The British Pound recovered recently and moved above the 1.3300 resistance against the US Dollar.

- There was a break above a key bearish trend line with resistance at 1.3310 on the 4-hours chart of GBP/USD.

- The UK Construction PMI in May 2018 remained at 52.5 versus the forecast of 52.0.

- Today in the US, the US Services PMI for May 2018 will be released, which is forecasted to remains at 55.7.

GBPUSD Technical Analysis

The British Pound was rejected from the 1.3200 support area against the US Dollar. The GBP/USD pair climbed higher and broke a few key hurdles, including 1.3300 and 1.3350.

During the upside move, the pair broke the 23.6% Fib retracement level of the last decline from the 1.3608 high to 1.3204 low. More importantly, there was a break above a key bearish trend line with resistance at 1.3310 on the 4-hours chart.

It opened the gates for more gains above the 1.3350 level. However, there are a few important resistances near the 1.3410 level and the 100 (red) simple moving average (4-hour).

Additionally, the 50% Fib retracement level of the last decline from the 1.3608 high to 1.3204 low at 1.3406 is also a major barrier for buyers. A successful close above 1.3400 and the 100 SMA is needed for further upsides towards 1.3500.

On the flip side, the broken resistance near 1.3310 and 1.3300 are likely to act as supports if the pair corrects lower.

Recently in the UK, the Construction PMI for May 2018 was released by the Chartered Institute of Purchasing & Supply and Markit Economics. The market was looking for a decline in the PMI from the last reading of 52.5 to 52.0.

However, the actual result was above the forecast as there was no decline in the PMI from 52.5. 8. The outcome was positive and it helped GBP/USD to stay in a positive zone above 1.3300.

Economic Releases to Watch Today

- Germany’s Services PMI for May 2018 – Forecast 52.1, versus 52.1 previous.

- Spanish Services PMI for May 2018 – Forecast 56.1, versus 55.6 previous.

- Euro Zone Services PMI for May 2018 – Forecast 53.9, versus 53.9 previous.

- US Services PMI for May 2018 – Forecast 55.7, versus 55.7 previous.

- US ISM Non-Manufacturing Index for May 2018 – Forecast 57.5, versus 56.8 previous.

AUD/USD Perky Ahead Of RBA

Investors utterly unfazed by trade tariffs

Stock market investors remain utterly unfazed by the prospects of trade tariffs or even higher interest rates as consecutive monthly payroll numbers continue to support the Goldilocks economy sweet spot scenario. Employers are aggressively ramping up staff, but wages are rising much less dramatically. So far, investors remain focused on a broader subset of US economic data while concluding that US earnings and the economy are sufficiently robust to keep the equity bull market intact. And for the time being, putting the prospects of higher US interest rates and global trade wars, which usually scare investors stiff, on the back burner.

With very few new developments in play, the markets continue regrouping after last week's Italian tumult, but there's a lot more waiting and watching going on than price action suggests. Many market participants think that by ignoring tariff and higher US interest rates, some investors are viewing the current landscape through rose coloured glasses.

Oil Market

WTI took a deep dive below the key $ 65.00 per barrel level as the long liquidation continues all the while hedge funds continue to increase short bets for the 3rd consecutive week. Again, it's all about supply, whether it's OPEC raising output or US increasing production, all roads lead to higher global oil supplies, which is leaving oil traders shaking in their boots.

There was no pushback after Saturday's meeting between the Saudis and the other Arab producers. Adding to the downward momentum as traders added on more short positions

From a technical perspective, taking out the 100 days moving average for the first time since September 2017, suggests there's more hurt to come.

Gold Market

Demand for safe havens is incredibly soft which is hurting golds appeal more so with investors showing little concern about a trade war. The markets remain on the defensive ahead of next week Fed rate hike and more specifically the Fed's forward guidance after another stellar Non-Farm Payrolls data. With little more than tier two economic to glean while in the midst of the fed blackout period, demand for gold should slow especially as safe haven appeal subsides.

Currency Market

Currency markets played out predictably overnight with the widely expected Euro relief rally triggering broader USD weakness. But with US yield and equities moving higher, the Euro ran out of gas in NY after falling shy of breaking significant topside resistance.

Yesterday's APAC session reluctance to engage USDJPY topside risk gave way to the USDJPY's sensitivity to US yields as the pair tracked US bond yields higher throughout the NY session.

The Australian dollar has been the top performer overnight after domestic retail sales finally showed some Moxy. The Aussie was then further supported by a firm global equities market performance auguring well for FX high beta like the Aussie dollar.

The Ringgit is benefiting from positive global risk sentiment and the positivity surrounding the upcoming Trump-Kim summit slated for June 12 in Singapore.

Eco Data 6/5/18

[php_everywhere instance="1"]

Malmstrom: Pre-measures against US steel tarrifs can be taken in July

More responses from EU on US steel tarrifs.

EU trade Commissioner Cecilia Malmstrom said "we can take pre-measures in July already. This is what we are going to discuss. We want to see the preliminary outcomes of the investigation. It is possible."

British trade minister Liam Fox said "it is right to seek to defend our domestic industries from both the direct and indirect impacts of these U.S. tariffs. The response must be measured, and proportionate, and it's important that the United Kingdom and the EU work within the boundaries of the rules-based international trading system,"

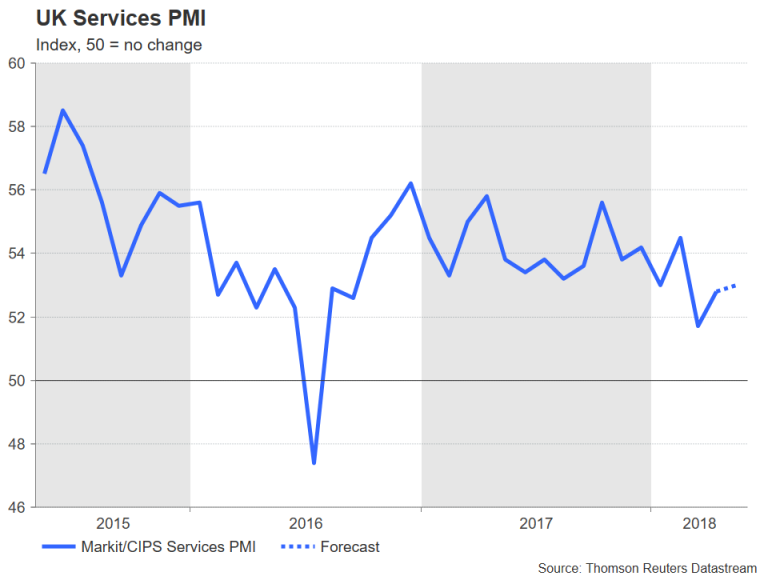

UK Services PMI Unlikely to Provide Much Relief to Pound as Brexit Tensions Brew

The Markit/CIPS services PMI will be the main data release out of the UK this week. The closely monitored index is expected to show a further improvement in the UK’s dominant services sector in May when it’s released on Tuesday at 08:30 GMT. However, any potential boost to the pound will likely be short-lived as the British government heads for a showdown with the European Union over Brexit.

Activity in the services sector decelerated to a 20-month low in March, in line with a broader slowdown in the economy, before recovering slightly in April. It is expected to improve further in May, with the services PMI forecast to rise from 52.8 to 53.0. While an increase in the PMI reading would be a welcome sign that economic growth is starting to pick up in the second quarter, the index remains below the average of 54.2 in 2017.

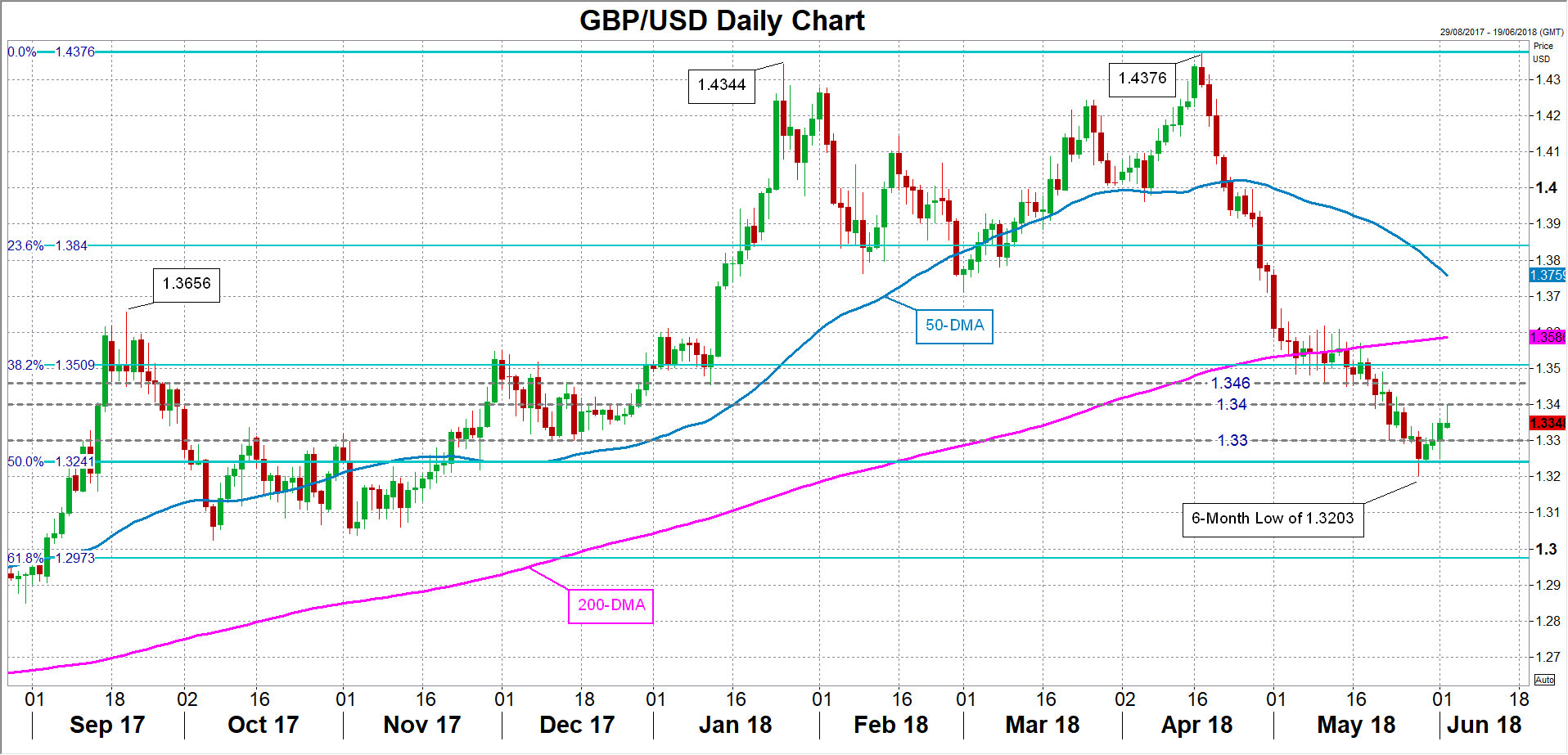

There are tepid signs that growth is gaining momentum in the second quarter. Both the manufacturing and construction PMIs released in the past few days beat expectations in May and a CBI survey of UK firms published on Sunday pointed to rising output in the three months to May. The encouraging data has helped the pound to regain some positive footing against the dollar. The British currency had tumbled to a 6-month low of $1.3203 last week but has since rebounded to just below the $1.34 level.

Another data beat on Tuesday could lift sterling above $1.34 towards potential resistance barriers at the $1.3460 and $1.3510 levels. A disappointing PMI report, however, could lead to a reversal of the pound’s recent gains with the $1.33 support level coming back into scope. A breach of this support would open the way towards the critical 50% Fibonacci retracement of the upleg from $1.2108 to $1.4376, around 1.3240.

While more positive indicators in the coming weeks would boost expectations of a Bank of England rate hike in August, the pound looks set for a choppy ride as Brexit returns to the limelight ahead of an EU summit on June 28-29. The government has said it will publish its plans on how to avoid a hard border between Northern Ireland and the Republic of Ireland in the coming days. The Irish government has given the UK two weeks to put forward proposals on resolving the border problem. However, with the EU adopting an increasingly uncompromising position, a breakthrough on the issue doesn’t seem very likely before the summit.

Another sticking point in the negotiations, which has been complicated by the Northern Irish border issue, is the UK’s plans for a customs partnership and how it will achieve frictionless trade with the EU, having opted not to remain within the European single market. The UK is reportedly working on two versions of a customs model, which will be outlined in the coming weeks. However, hopes for a near-term agreement are low after Michel Barnier, the EU’s chief negotiator, was quoted as saying “Neither of those proposals are operational or acceptable to us”.

In a further headache for Prime Minister Theresa May, the EU Withdrawal bill, which suffered 15 amendments in the House of Lords (the UK’s upper chamber), will return to the House of Commons in the next fortnight. One of the amendments was for the UK to remain in the European Economic Area, which in effect means staying in the single market. If MPs vote in favour of the amendment, it would take the choice on the type of post-Brexit customs arrangement away from the government and force May’s hands into remaining inside the single market.

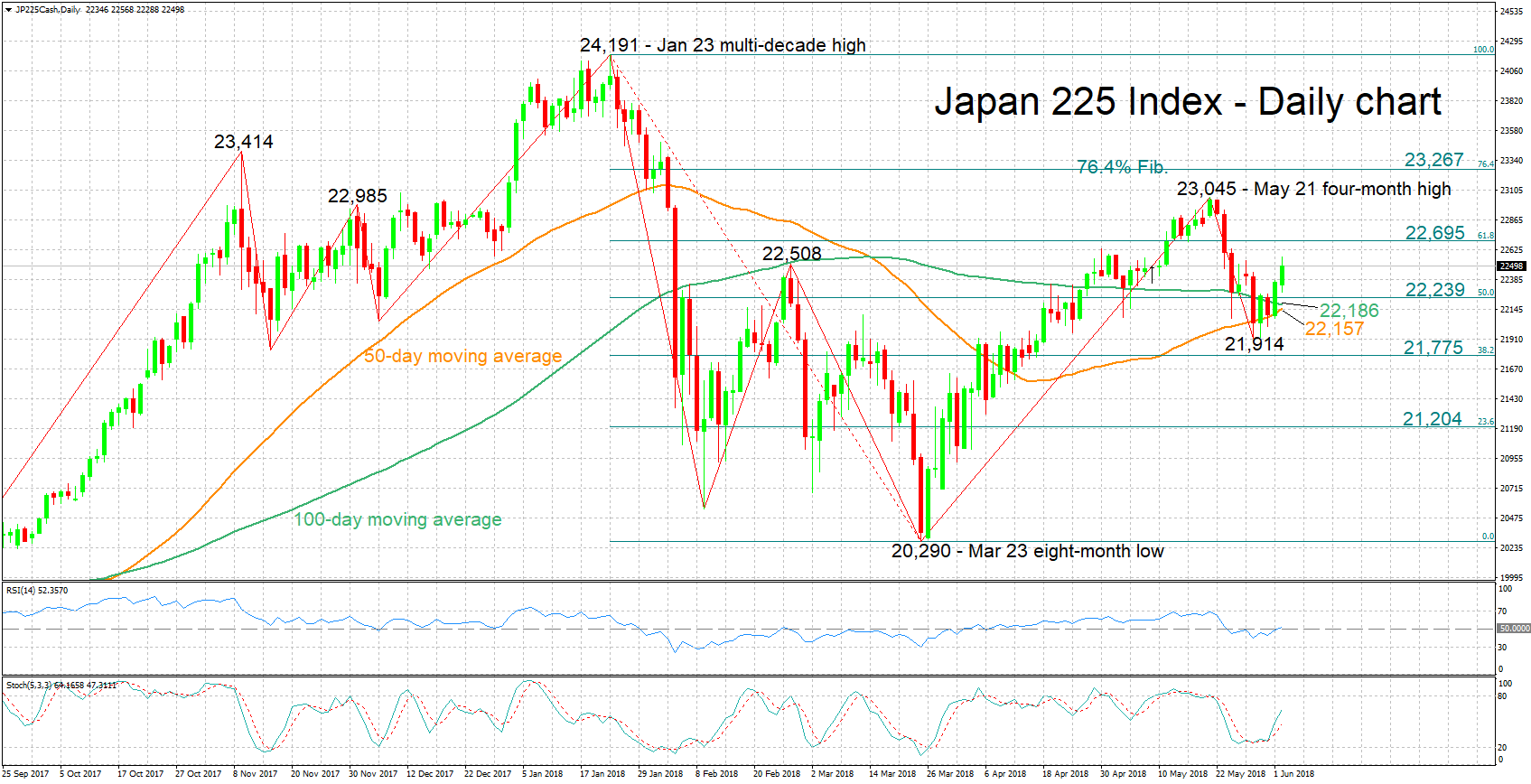

Japan 225 Index Looking Bullish in the Short-Term, Crosses above MAs

The Japan 225 index has risen by around 600 points after hitting a one-and-a-half-month low of 21,914 last Tuesday.

The RSI is on the rise, having entered bullish territory above 50; this is painting a positive short-term picture. The bias in the very short-term is also bullish as indicated by the stochastics oscillator: the %K line has moved above the slow %D one, with both lines continuing to head higher.

Additional gains may meet resistance around the 61.8% Fibonacci retracement level of the January 23 to March 23 downleg at 22,695, with stronger bullish movement turning the attention to May 21’s four-month high of 23,045; the region around this also includes the 23,000 round figure that may hold psychological significance.

On the downside, support could come around the 50% Fibonacci mark at 22,239. The 100- and 50-day moving average lines at 22,186 and 22,157 respectively, as well as last week’s one-and-a-half-month low of 21,914 lie not far below, while sharper losses would shift the focus to the 38.2% Fibonacci level at 21,775.

In terms of the medium-term picture, it is looking mostly bullish, with price action moving above both the 50- and 100-day MA lines recently. However, the positive outlook remains fragile with trading still not far above the two MAs; a drop towards and below the two MAs – notice that they roughly coincide at the moment – would paint a more neutral medium-term picture.

Overall, both the short- and medium-term outlooks are looking bullish, with the latter only marginally so at the moment.

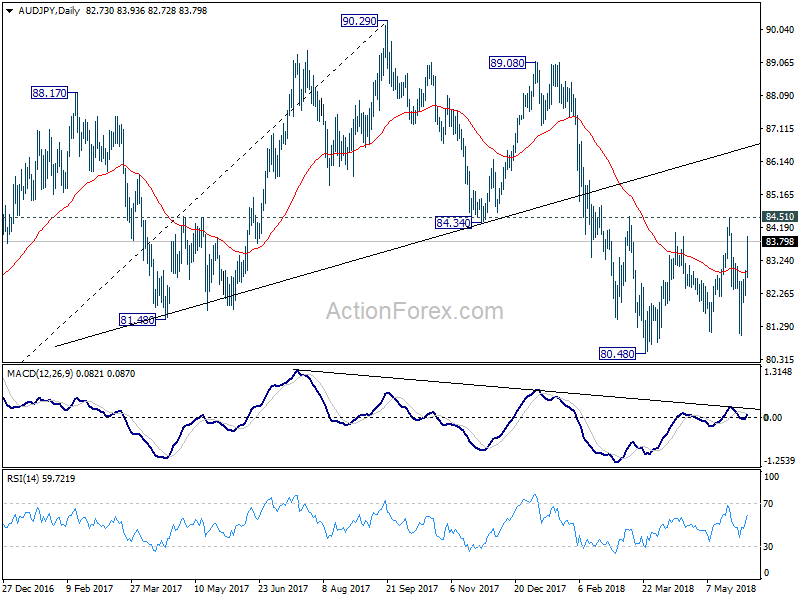

A look at AUD/JPY ahead of RBA

We've covered AUD/CAD earlier today and it's doing well as expected. Let's have a look at AUD/JPY

AUD/JPY action bias table shows persistent upside blue bars in H action bias. 6H action bias also stays upside blue for three bars. However D action bias has just turned blue with a down side red bar two bars ago. W action bias is also neutral all the way with two red bars in the middle.

The table suggests that current rise could be just a leg in side a short to medium term consolidation pattern. And this is consistent with D action bias chart. So we'll tend not to chase the rally in AUD/JPY, at least until a sustained break of 84.51 resistance, or until W action bias also turns blue.

US-China Trade Talks: Why Things are Getting Tricky

- Unfortunately, the positive developments in the US-China trade conflict did not last long. The risk of going into renewed escalation over the coming weeks is going up.

- The key challenge is how Trump can both satisfy a strong domestic call for tariffs on Chinese technology without China leaving the negotiation table and go back to retaliation.

- While we still believe the ultimate solution will not entail a trade war, the probability that things will get worse in the short run is clearly going up. In addition, it highlights that this theme will continue probably for a long time. Keep an eye on China's response on 15 June when Trump plans to announce the specific list of targeted goods for USD50bn of Chinese imports.

- A return to a 'tit-for-tat' pattern would increase the fear of a trade war and probably give a hit to risk appetite.

What just happened?

Two weeks ago things started to look good in the US-China trade conflict with the deal between US and China in which China agreed to 'substantially reduce' its trade surplus with the US, see US-China trade talks: 'Grand bargain' moving closer, 22 May 2018. China also committed to strengthen protection of intellectual property rights and open up more investments. After the deal the US Treasury Secretary said on Fox News 'We're putting the trade war on hold, so right now we have agreed to put the tariffs on hold while we try to execute the framework.'

This was all good news. However, it did not last long. Trump immediately faced strong criticism at home from fellow Republicans and Democrats for being too soft on China. Republican Senator Marco Rubio for example tweeted 'Sadly China is out-negotiating the administration & winning the trade talks right now… This is #NotWinning'. Things are not made easier by the fact that the US midterm elections are coming up in November, the protectionist forces are strong in some states and the Republicans are way behind in the opinion polls.

On 29 May, one week after Mnuchin said the trade war was on hold, Trump announced tariffs on Chinese goods worth USD50bn in a press statement headlined 'President Donald J. Trump is Confronting China's Unfair Trade Policies'. It seems the announcement is a direct response to the criticism of China out-negotiating the US. The list of products subject to tariffs will be presented on 15 June and will be products primarily within the 'Made-in-China 2025' strategy, which is dominated by technological products.

China said in response that it 'urged US to keep its promise…' and that it would take 'resolute and forceful' measures to protect its interests, see Reuters. Over the weekend the Chinese leadership then warned the US that the trade promises will 'not go into effect' if the US puts any sanctions - including additional tariffs - back on the table, see SCMP. The negotiations over the weekend when US Commerce Secretary Wilbur Ross was in Beijing were mainly about the details of China's increased purchases of US products within energy and did not as such bring new things on the table.

Escalation to come

The development puts the negotiations in a very difficult state. It looks very difficult for Trump to move back from the USD50bn of tariffs on Chinese technological products. This would trigger significant criticism from both other Republicans as well as Democrats.

Could China offer something to avoid the tariffs? We doubt this. China has already gone a long way to meet Trump. It has thus promised to buy more US products, has announced a reduction in tariffs on a long list of products, committed to increased protection of intellectual property rights and opened up further for investments into China. The US tariff also serves to limit China's technological development, which means it may not matter how much China offers on the trade front.

We thus find it likely that we could soon end in a situation of further escalation. We expect China to do what it says and take the offer off the table and may even retaliate by putting tariffs on US products worth USD5bn as well. This would take us back to the original scenario when Trump first announced tariffs on China. Could China choose not to respond? We do not see this as very likely as it would undermine their credibility and cause a loss of face. They are willing to meet Trump and give concessions at the negotiating table. But China will not allow itself to be 'bullied' by Trump, as it would be seen in China.

Another key question then becomes, how would Trump respond to Chinese retaliation? There is a risk that he pulls out the USD100bn of Chinese exports subject to tariffs once again to step up the pressure on China. And then we are back in the 'tit-for-tat' pattern that could take us into trade war. If Trump really believes the US would win a trade war as he again tweeted this weekend, then he might choose that road.

'Grand bargain' further away - but you never know with Trump

The recent developments has, in our view, clearly put the risk of a trade war back on the table. If this is confirmed later this month, we expect it to hit risk appetite. The 'Grand bargain' that we have argued for may be further away than we thought.

Given the costs of a prolonged trade war, our baseline is still, though, that some kind of deal will be struck eventually but the latest development highlights that this theme will probably haunt us for a long time, as trade wars are slowly fought. There is also the caveat that you never know what the next step is with Trump and whether it is all just part of a negotiation game. The North Korea talks are also coming up on 12 June adding another dimension to the situation. So stay tuned. The pendulum could suddenly swing in the other direction again as seen a few times before.