Sample Category Title

Dollar Under Broad Based Pressure as Correction Extends, Aussie Hold Gains ahead of RBA

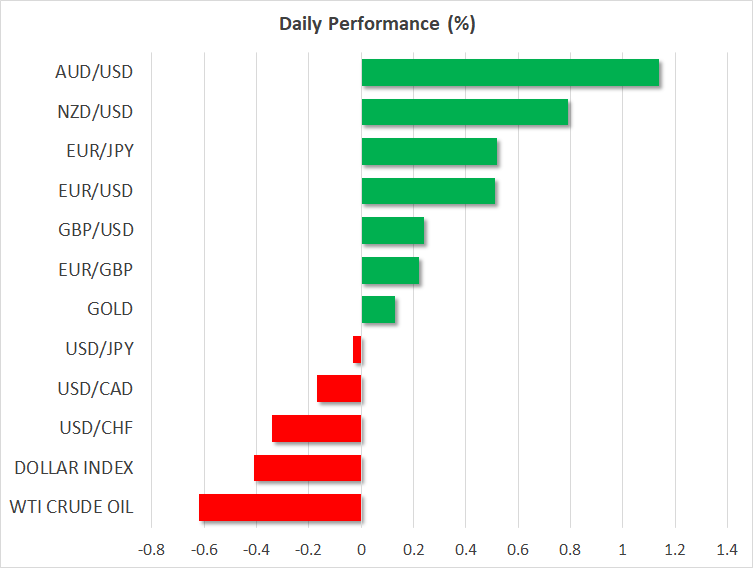

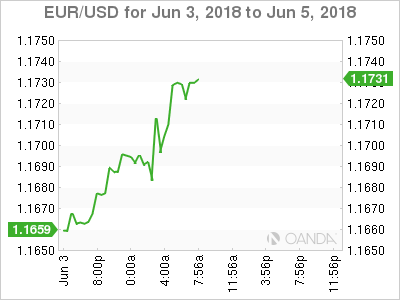

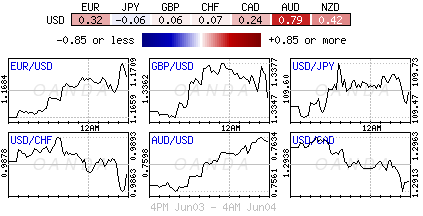

Australian Dollar remains the strongest one today as helped by strong risk appetite. At the time of writing, TSE is trading up 0.55%, DAX up 0.25% and CAC Is up 0.33%. US futures also point to another day of rally. New Zealand Dollar follows as the second strongest. Meanwhile, Euro is the third strongest on easing worries over Italy. Dollar, on the other hand, is trading as the weakest one, followed by Japanese Yen.

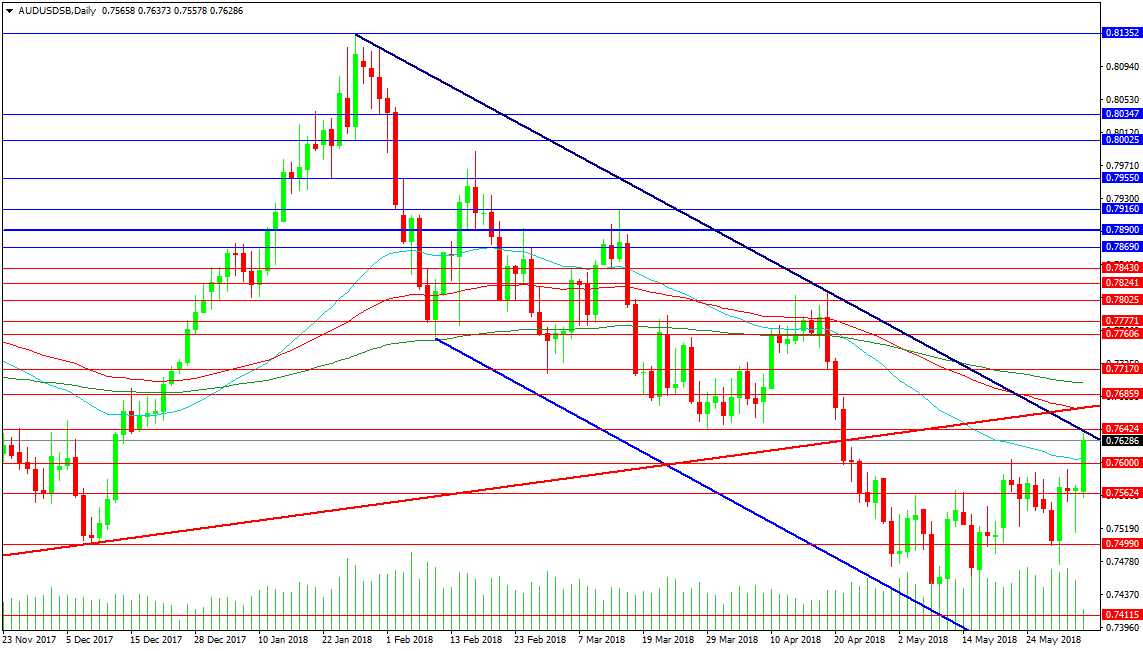

Technically, despite AUD/USD's strong rebound today, rise from 0.7411 is still seen as a corrective move. 0.7688 would be an important near term fibonacci resistance to overcome. RBA rate decision and statement tomorrow would be an important event for the Aussie. But firstly, no one is expecting a chance in interest rate. And secondly, it's unlikely for RBA to chance its neutral, wait-and-see stance. Hence, Wednesday's GDP report could be the one that decides whether AUD/USD could get past the mentioned 0.7688 level.

Meanwhile, Dollar is not as weak as it seems. EUR/USD's rebound from 1.1509, GBP/USD's rebound from 1.3203, USD/CHF's pull back from 1.0056 are all seen as corrective. The greenback is still technically in an up trend against them.

German-Italian spread narrows, markets pricing in ECB 2019 hike again

Markets continued to stabilize further as Italian political turmoil is now a past. Italian 10 year bond yield dropped for another day, by 0.17 so far and is standing at 2.54. German 10 year bund yield, on the other hand, is rising 0.16 and is back above 0.40 at the time of writing. While the spread is still widener than 200, it's much better than the worse day when it was over 300.

Money markets are back pricing in the chance of an ECB hike next year. This is additionally supported by the stronger than expected inflation reading released last week. Now, markets are pricing in around 50% chance of a hike in June 2019. They are also now fully pricing in a 10 bps hike by September 2019.

Salvini to EU: Italy can't be a refugee camp

Just days after its formation, the new Italian eurosceptic government is starting the clash with EU. Interior Minister Matteo Salvini, head of the right-wing League and a deputy prime minister too, declared that the "party is over" for migrants. Salvini said in a radio interview that Italy "can't be transformed into a refugee camp". And he added that it's "clear and obvious that Italy has been abandoned" by the EU. Later Salvini tweeted that "either Europe gives us a hand in making our country secure, or we will choose other methods."

Eurozone Sentix investor confidence dropped sharply to 9.3 as expectation collapsed

Eurozone Sentix Investor confidence dropped sharply to 9.3 in June, down from 19.2 and well below expectation of 18.6. And, for the fifth time in a row, overall index for Germany dropped to its lowest level since July 2016. Expectation "collapsed" to -13.3, hitting the lowest level since August 2012.

In the release, Sentix noted that "it appears that investors still hope that the world's trade dispute with the US will not get out of control. But, they are "far less lenient with developments within the euro zone." It also pointed out that "the new government in Rome is very sceptical. This is so strong that economic expectations in the euro zone are downright tilting."

UK PMI construction unchanged at 52.5, recovery could be short-lived

UK PMI construction was unchanged at 52.5 in May, above expectation of 52.0. Sam Teague, Economist at IHS Markit noted that "activity in May was once again buoyed by some firms still catching up from disruptions caused by the unusually poor weather conditions in March". And, a"a renewed drop in new work hinted that the recovery could prove short-lived."

Australian Dollar lifted by positive economic data

Retail sales rose 0.4% mom in April versus expectation of 0.3% mom, and prior month's 0.0%. The Australian Bureau of Statistics noted that cafes, restaurants and takeaways led the rise assisted by an unusually warm April. But there were likely negative impacts for some businesses in "clothing, footwear and personal accessories and department stores." Company gross operating profits rose 5.9% qoq, 5.8% yoy seasonally adjusted in Q1. Wage growth was slow at 0.8% qoq seasonally adjusted and 5.1% yoy. TD securities inflation gauge, however, was flat 0.0% mom in May versus expectation of 0.3% mom and prior month's 0.5% mom.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1611; (P) 1.1665 (R1) 1.1712; More.....

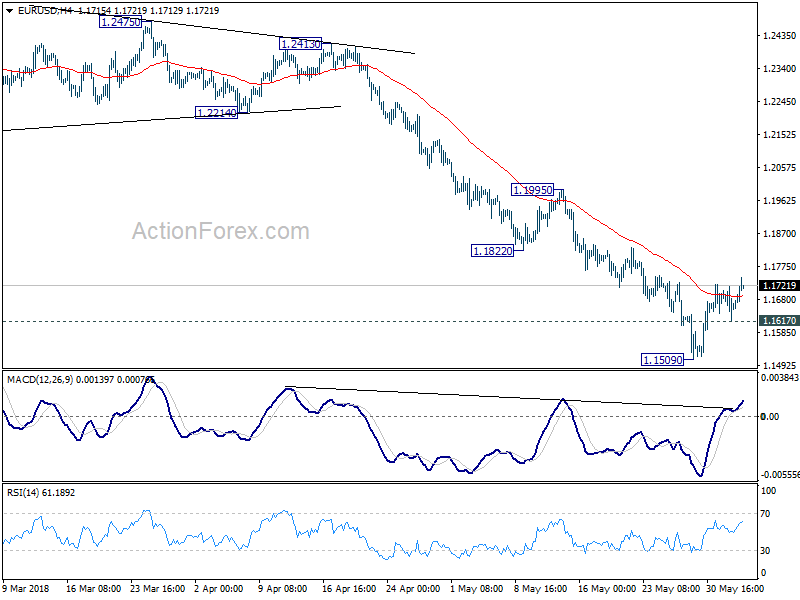

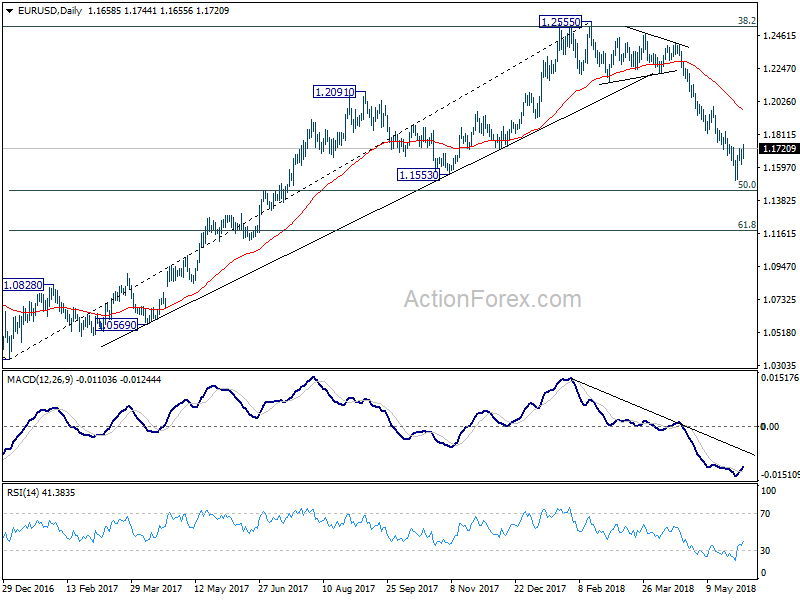

EUR/USD's rebound from 1.1509 extends higher today. But after all it's seen as a correction. Hence, in case of further rally, we'd expect strong resistance from 1.1822/1995 resistance zone to limit upside and bring fall resumption eventually. On the downside, below 1.1617 minor support will bring retest of 1.1509 low first. Break will resume the decline from 1.2555 and target 50% retracement of 1.0339 to 1.2555 at 1.1447. Break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

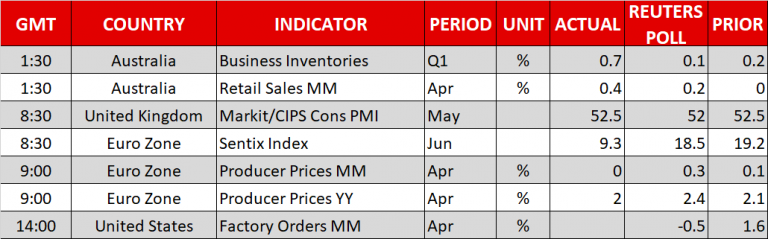

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y May | 8.10% | 7.40% | 7.80% | |

| 1:00 | AUD | TD Securities Inflation M/M May | 0.00% | 0.30% | 0.50% | |

| 1:30 | AUD | Retail Sales M/M Apr | 0.40% | 0.30% | 0.00% | |

| 8:30 | GBP | Construction PMI May | 52.5 | 52 | 52.5 | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jun | 9.3 | 18.6 | 19.2 | |

| 9:00 | EUR | Eurozone PPI M/M Apr | 0.00% | 0.40% | 0.10% | |

| 9:00 | EUR | Eurozone PPI Y/Y Apr | 2.00% | 2.40% | 2.10% | |

| 14:00 | USD | Factory Orders Apr | -0.40% | 1.60% |

Euro Heads North As Investors’ Rate Optimism Resumes, RBA Rate Decision Next

Here are the latest developments in global markets:

FOREX: The Australian dollar continued to outperform its peers rallying by 1.12% against its US counterpart and by 1.20% against the Japanese yen as upbeat retail sales readings and business inventories raised growth prospects ahead of the release of Q1 GDP growth on Wednesday. Its New Zealand cousin was also moving higher, elevated by 0.82% versus the greenback, despite markets in New Zealand being closed for public holiday. Euro/dollar and euro/yen climbed to 1 ½-week highs of 1.1736 (+0.60%) and 128.67 (+0.63%) respectively as the political relief in Italy lifted chances for a 10bps rate hike by the ECB in June 2019. Money markets are now seeing a chance of 50% compared to 30% in the previous week, a month ahead of what they believed last week. Meanwhile, producer prices and the Sentix investor confidence index out of the Eurozone came in lower-than-expected, though the euro shrugged off the miss in data and advanced higher instead. Pound/dollar crawled up to 1 ½-week highs as well, peaking at 1.3397 after May's construction PMIs surpassed forecasts but remained steady at April's levels. Dollar/yen was steady at 109.54, with investors cautious on how the trade story will develop after the US imposed steel and aluminum import tariffs on the EU and its NAFTA partners, Canada and Mexico, with the latter ones having already taken countermeasures. The dollar index was down by 0.43% at 93.78.

STOCKS: European stocks opened higher on Monday supported by gains in the utility sector, while easing political concerns encouraged investors to allocate more funds in riskier assets. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were both up by 0.49% at 0930 GMT. The German DAX 30 rose by 0.25%, the French CAC 40 climbed by 0.44% and the UK's FTSE 100 increased by 0.68%. The Spanish IBEX 35 was the best performer after a tense week, surging by 1.58%, while the Italian FTSE MIB was on the recovery, rising by 0.61%. US stock futures were all flashing green, pointing to a positive open.

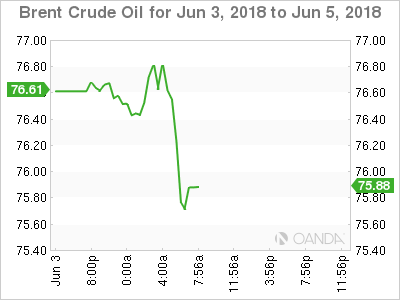

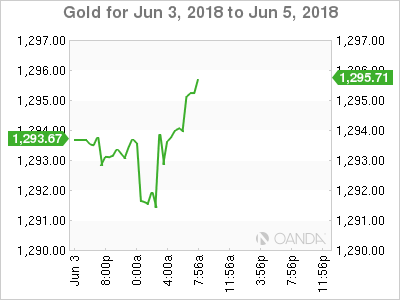

COMMODITIES: Oil prices were on the back foot, with WTI crude oil being down by 0.11% at $65.74 per barrel and the London-based Brent lower by 0.44% at $76.45. On Friday, Baker Hughes showed an increase in US oil rigs, which drove the total count of rigs to the highest since March 2015. Investors were also worried that the falls in Venezuelan and Iranian output, as well as Washington's concerns about oil's recent rally, which was characterized as taken too far, could persuade OPEC members to raise supply at their policy meeting on June 22. In precious metals, gold was steady at $1,293.80 per ounce.

Day Ahead: US factory orders to gather attention before RBA statement

Looking ahead, the rest of the day will be fairly quiet, while the aussie and the dollar will attract some attention by investors as economic releases out of Australia and the US later in the day might bring volatility to the currencies.

In the US, factory orders will be the only major pending figures (1400 GMT). The numbers published by the US Census Bureau are expected to show a contraction of 0.5% m/m in new manufacturing orders in April after growth of 1.6% in the prior month. The US currency would be eyed ahead of the releases.

As for central bank meetings, the Reserve Bank of Australia (RBA) will announce its rate decision during the Asian trading session on Tuesday, at 0430 GMT. Policymakers are widely anticipated to keep interest rates unchanged to 1.5% and as such, attention will turn to the phrasing of the accompanying statement. Although the RBA is expected to remain concerned about low inflation and wage growth, it will likely reaffirm its positive growth outlook. Net exports contribution data for the first quarter will be closely watched ahead of the rate decision, with scope to push the aussie higher if the numbers, which are a good indication to GDP growth due on Wednesday, surprise to the upside. Analysts believe that the measure will rebound by 0.5% q/q after contracting by an equivalent percentage in the previous quarter.

Chinese Caixin Services PMI are also due on Tuesday at 0145 GMT.

In terms of public appearances. At 1700 GMT Bank of England Member of Monetary Policy Committee Silvana Tenreyro will speak in Guildford.

A speech by the ECB President Mario Draghi on Tuesday on the occasion of the Bank's 20th anniversary in Frankfurt, Germany has been canceled.

Dollar Dips On Trade Worries

Monday June 4: Five things the markets are talking about

Last week, geopolitical events again captured the attention of capital markets even though critical economic data had been released.

With political concerns about the eurozone having somewhat eased by week’s end – in Italy, nationalist parties finally took power, while in Spain, the Socialist led-opposition ousted PM Rajoy with a no-confidence vote Friday – market attention turns back to trade this week as the U.S is headed for a showdown with its G7 allies at a summit in Quebec, Canada (June 8-9).

After the U.S imposed steel and aluminum tariffs on E.U, Canadian and Mexican imports, political tensions and the risk of a global trade war are back in focus, making this week’s summit more important than usual.

Overnight, global equities rallied as investor optimism for the U.S economy trumped investors’ concerns over tariffs and protectionism. U.S Treasuries slipped alongside the ‘mighty’ dollar, while sterling (£1.3389) and the EUR (€1.1724) found some traction.

1. Stocks see the light

In Japan, the Nikkei share average rallied overnight, tracking Friday’s Wall Street’s gains after May’s NFP report pointed to further strength in the U.S economy, while a weaker yen (¥109.60) supported stocks of Japanese exporters. The Nikkei ended up +1.37%, while the broader Topix gained +1.46%.

Down-under, Aussie shares rallied on Monday led largely by financials as the country’s big banks settled money-laundering complaints. The S&P/ASX 200 index rose +0.6%. The benchmark lost -0.4% on Friday. In S. Korea, the Kospi rallied +0.36%.

Note: Reserve Bank of Australia’s (RBA) monetary policy decision is out Tuesday.

In Hong Kong, stocks followed Asian markets higher on stronger U.S data. The Hang Seng index rose +1.7%, while the China Enterprises Index gained +1.9%.

In China, stocks ended higher overnight, supported by a rebound in consumer and real estate shares. However, gains are capped as worries over credit risks persist and as investors watched the development of Sino/U.S trade talks. The blue-chip CSI300 index rose +1.0%, while the Shanghai Composite Index rose +0.5%.

Note: China warned the U.S yesterday that any agreements reached on trade and business between the two countries will be void if Washington implements tariffs.

In Europe, regional bourses opened higher and have continued in the ‘black,’ supported in general by positive sentiment following resolution of the political situation in Italy and Spain.

U.S stocks are set to open higher (+0.3%).

Indices: Stoxx600 +0.9% at 386.35, FTSE +0.6% at 7725, DAX +0.8% at 12709, CAC-40 +1.1% at 5457; IBEX-35 +1.4% at 9594, FTSE MIB +2.7% at 22373, SMI +1.4% at 8571, S&P 500 Futures +0.3%

2. Oil is steady as extra U.S supply balances strong demand, gold unchanged

Oil prices trade steady as U.S production hit a record high and OPEC considered boosting supply to balance rising global demand.

Brent crude oil is unchanged at +$76.79 a barrel, while U.S light crude (WTI) is up +5c at +$65.86 a barrel.

Note: Last week, the U.S contract lost -3%, adding to a near -5% decline from the week before.

According to EIA data last week, U.S crude production climbed in March to +10.47m bpd, a new monthly record, while U.S drillers added two oilrigs in the week to June 1, bringing the total to +861, the most since March 2015. That is the eighth time U.S drillers have added rigs in the past nine-weeks.

On the weekend, OPEC ministers from Saudi Arabia, the United Arab Emirates, Kuwait and Algeria along with their counterpart from non-OPEC Oman met “unofficially” in Kuwait and agreed on the need for continued cooperation between members.

Note: OPEC will meet formally on June 22 to set oil policy. It is expected to agree to raise output to cool the market amid worries over Iranian and Venezuelan supply.

Ahead of the U.S open, gold prices trade in a tight range as persistent concerns about trade wars between the U.S and the rest of the world offset expectations of a U.S interest rate hike this month. Spot gold is unchanged at +$1,293.23 per ounce, after hitting its lowest in two weeks at +$1,289.12 in Friday’s session.

3. Southern euro sovereign yields fall, while G7 climb

Italy’s bond market continued its recovery this morning as investors took comfort, for now, from the creation of a government in Rome that ends months of political turmoil, while the risk of more U.S rates hikes added to a selloff in German debt.

Short and long-dated Italian bond yields, which aggressively backed up last week on fears that the possibility of a new election might have effectively become a referendum on euro membership, have eased – Italy’s 2-year bond yield is down -23 bps at +0.79%, having briefly surged last week to 5-year highs around +2.7%.

Elsewhere, the yield on 10-year Treasuries has climbed +2 bps to +2.92%, the highest in a week. In Germany, the 10-year Bund yield has backed up +1 bps to +0.39%, the highest in more than a week, while in the U.K, the 10-year yield has increased +2 bps to +1.297%, the highest in a week.

4. Dollar dips on trade worries

The ‘mighty’ USD (€1.1724, £1.3389, ¥109.63 and C$1.2914) is a tad softer starting a new week. Aside from the cited reasons above, the dollar has come under pressure after the White House Economic Advisor Kudlow publically warned, over the weekend, that trade escalation might weaken the U.S economy.

Not helping the dollar’s cause is the U.S Treasury yield curve has undergone a “bear flattening” following the release of Friday’s strong U.S payrolls (+223k and +3.8% unemployment).

Note: Fixed income dealers are now pricing in a fourth Fed hike for this year.

EM currencies are also firmer outright. The TRY ($4.6211) has found support after stronger than expected inflation data suggested that the CBRT could again act and show its independence this Thursday (June 7). However, consensus is expecting the CBRT will leave the one-week repo rate – which is now its key policy rate – unchanged at +16.50%

5. Eurozone producer prices flat, while U.K construction PMI higher

E.U data this morning showed that prices of goods leaving the eurozone’s factory gates were unchanged in April. This would suggest that inflationary pressures remain modest despite a recent rise in energy prices. The market consensus was expecting a +0.5% rise on month.

Note: Data last week showed that CPI hit the ECB’s target for the first time in more than a year during May, but that was largely due to a jump in energy prices.

In the U.K, the details of the Markit survey (construction PMI 52.5 vs. 52) revealed that commercial activity growth accelerated to a three-month high in May, but showed “softer expansions” in residential and civil engineering activity. Digging deeper, new order books meanwhile contracted for the fourth time in the past five months.

ECB 2019 hike pricing is back as Italy worry faded and inflation jumped

Markets continued to stabilize further as Italian political turmoil is now a past. Italian 10 year bond yield dropped for another day, by 0.17 so far and is standing at 2.54. German 10 year bund yield, on the other hand, is rising 0.16 and is back above 0.40 at the time of writing. While the spread is still widener than 200, it's much better than the worse day when it was over 300.

Money markets are back pricing in the chance of an ECB hike next year. This is additionally supported by the stronger than expected inflation reading released last week. Now, markets are pricing in around 50% chance of a hike in June 2019. They are also now fully pricing in a 10 bps hike by September 2019.

Japanese Yen Yawns To Start Week, Household Spending

The Japanese yen is unchanged in the Monday session. In North American trade, USD/JPY is trading at 109.52, down 0.01% on the day. On the release front, there are no U.S or Japanese events on the schedule. In the U.S, Factory Orders is expected to decline 0.4%, after a strong gain of 1.6% a month earlier. Japan will release Household Spending, with the markets expecting a gain of 0.8% after two straight declines. On Tuesday, the U.S releases manufacturing and employment reports.

Is the Federal Reserve moving closer to a neutral monetary policy? Recent statements by FOMC policymakers appear to support such a conclusion, which would mean that the Fed would let the economy ‘ride on its own steam' without intervening by adjusting interest rates. In the meantime, the Fed continues to project two more rate hikes in 2018, after raising rates by a quarter-point in March. The most likely dates for a rate hike are June and September. A fourth hike in December is possible, with a likelihood of about 40%. The minutes of the May meeting noted that policymakers would consider allowing inflation to rise above the Fed's 2% target for a temporary period, which means that the Fed would not rush to raise rates based on the inflation target.

The U.S released strong employment numbers on Friday, but USD/CAD was unchanged on the day. Wage growth improved to 0.3%, up from 0.1% a month earlier. Nonfarm payrolls jumped from 189 thousand to 164 thousand and the unemployment rate dropped to a sizzling 3.8 percent. All three indicators beat their estimates and are indicative of a labor market running at full capacity.

After a brief hiatus, the markets are again facing the nasty reality of a trade war between the U.S. and its major trading partners, which could be bad news for the export-reliant Japanese economy. On Thursday, the Trump administration made good on its threats and imposed stiff tariffs on the European Union, Mexico and Canada. The U.S had granted all three trading partners a temporary extension, but cited insufficient progress on trade talks as the reason for the tariffs. This has triggered promises of retaliatory tariffs on US products, and matters heated up on the weekend at the G-7 meeting of finance ministers in Canada. US Treasury Secretary Steve Mnuchin faced sharp criticism from other finance ministers over the tariffs. There are fears that the escalating trade tensions could trigger a global trade war.

Canadian Dollar Gains Ground, Investors Look For Cues

The Canadian dollar has said the new trading week with gains. In Monday’s North American session, USD/CAD is trading at 1.2915, down 0.30% on the day. There is just one event on the calendar, with US Factory Orders expected to decline of 0.4%, after a strong gain of 1.6% in the previous release. On Tuesday, Canada releases Labor Productivity and the U.S publishes ISM Non-Manufacturing PMI and JOLTS Jobs Openings.

After a brief hiatus, the markets are again facing the nasty reality of a trade war between the U.S. and its major trading partners, which could be devastating news for the export-reliant Canadian economy. On Thursday, the Trump administration made good on its threats and imposed stiff tariffs on the European Union, Mexico and Canada. The U.S had granted all three trading partners a temporary extension, but cited insufficient progress on trade talks as the reason for the tariffs. There are renewed fears that these moves could trigger a global trade war. This has triggered promises of retaliatory tariffs on US products, and matters heated up on the weekend at the G-7 meeting of finance ministers in Canada. US Treasury Secretary Steve Mnuchin faced sharp criticism from other finance ministers over the tariffs. On Thursday, Canadian Prime Minister Trudeau tweeted that the tariffs were “unacceptable” and said that Canada would “impose dollar for dollar tariffs for every dollar levied against Canadians by the US.”

The U.S released strong employment numbers on Friday, but USD/CAD was unchanged on the day. Wage growth improved to 0.3%, up from 0.1% a month earlier. Nonfarm payrolls jumped from 189 thousand to 164 thousand and the unemployment rate dropped to a sizzling 3.8 percent. All three indicators beat their estimates and are indicative of a labor market running at full capacity.

The Canadian dollar was almost unchanged last week, but showed some volatility during the week. After a sharp drop on Wednesday, the currency reversed directions on Thursday, after the Bank of Canada sounded positive about the economy. The bank statement noted that inflation was higher than expected and the export sector remained robust. As expected, the bank maintained the benchmark rate at 1.25 percent. Inflation has moved closer to the BoC target of 2 percent and economic growth has been steady, so the BoC will be giving serious consideration to a rate hike this summer. Some analysts are even predicting that the bank will raise rates twice in the second half of 2018.

Salvini to EU: Italy can’t be a refugee camp

Just days after its formation, the new Italian eurosceptic government is starting the clash with EU. Interior Minister Matteo Salvini, head of the right-wing League and a deputy prime minister too, declared that the "party is over" for migrants.

Salvini said in a radio interview that Italy "can't be transformed into a refugee camp". And he added that it's "clear and obvious that Italy has been abandoned" by the EU.

Later Salvini tweeted that "either Europe gives us a hand in making our country secure, or we will choose other methods."

S&P 500 And Nasdaq 100 Analysis

US equities ended last week higher after a stronger than expected jobs report. The risk-on sentiment is set to continue today even though the world’s two largest economies are on track to commence a $100bn trade war after China-US trade negotiations ended on Sunday. However, geopolitical concerns regarding North Korea have subsided as US and North Korea leaders are to meet on 12 June in Singapore as planned. Over in Italy, a deal to form a government has been reached which has helped to diminish fears of an Italian exit from the Eurozone and improved sentiment for stocks in Europe.

As trading for the month of June begins, it is worth looking at seasonality. For the S&P 500 index, the month of June is historically rather dull. The average monthly return recorded since the 1960s, is 0%. The best performance for the month of June was 5% which is the lowest of any month.

S&P 500

On the daily chart, the S&P500 (SPX) tested the downside last week but recovered sharply from support at 2680. The index is now attempting to break higher and a close above 2740 would open the way for a continuation towards 2800 with resistance at 2760 and 2785. However, a reversal below 2715 would change the outlook with support 2680 and then 2663.

Nasdaq 100

On the daily chart, the Nasdaq 100 (NDX) finally broke the psychologically important 7000 level after a number of attempts. The index is now trying to clear the resistance at 7090 with the possibility of a move to new all time highs. However, a reversal and break of support at 7000 will likely lead to declines towards 6780 followed by 6780.

Receding Political Concerns Aids Risk Sentiment

Asia:

- 3rd round of trade talks between China and US ended without a deal: China official stated that the two sides had made "concrete progress"; any move by the US to impose punitive tariffs would derail the negotiations

- North Korea top three military officials said to have been removed from their posts ahead of Trump/Kim summit.

- China Q2 GDP growth expected to com e in between 6.7-6.8% range (vs. 6.8% in Q1)

- Australia Apr Retail sales M/M: 0.4% v 0.3%e

Europe:

- Spain Socialist leader Pedro Sanchez was sworn in as PM (over the weekend)

- EU's Juncker: European Commission to be at Italy's side on its reform path and on proposals for EU's future. Saw no threat of a new euro crisis despite situation in Italy

- S&P: formation of new government in Italy should have no immediate effect on its credit rating

- S&P affirmed Ireland sovereign debt rating at A+; outlook Stable- Fitch affirmed Portugal sovereign rating at BBB; outlook Stable

- Fitch affirmed Belgium sovereign rating at AA-; outlook Stable

Americas:

- G7 Finance Minister meeting, 6 countries (ex the US) issued a formal statement which expressed their unanimous concern and disappointment with the US steel and aluminum tariffs

- President Trump: We will have the meeting with North Korea's Kim on June 12th in Singapore

- US Commerce Sec Ross said to left China without any firm commitments on imports

Energy:

- OPEC+ Monitoring Committee: Need to maintain cooperation to stimulate adequate investments for a stable oil supply

Economic Data:

- (CZ) Czech Q1 Average Real Monthly Wage Y/Y: 6.6% v 6.2%e

- (TR) Turkey May CPI M/M: 1.6% v 1.6%e; Y/Y: 12.2% v 12.2%e; CPI Core Index Y/Y: 12.6% v 12.5%e

- (TR) Turkey May PPI M/M: 3.8% v 2.6% prior; Y/Y: 20.2% v 16.4% prior

- (ES) Spain May Net Unemployment M/M: -83.7K v -101.3Ke

- (SE) Sweden Q1 Current Account Balance (SEK): 21.9B v 37.0B prior

- (CH) SNB Total Sight Deposits for Week Ended Jun 1st (CHF): 576.5B v 576.6B prior

- (UK) May Construction PMI: 52.5 v 52.0e

- (EU) Euro Zone Jun Sentix Investor Confidence: 9.3 v 18.5e

- (GR) Greece Q1 Final GDP Q/Q: 0.8% v 0.3%e; Y/Y: 2.3% v 1.9% prior

- (EU) Euro Zone Apr PPI M/M: 0.0% v 0.2%e; Y/Y: 2.0% v 2.4%e

Fixed Income Issuance:

- (NO) Norway sold NOK3.0B vs. NOK3.0B indicated in 6-month bills; Avg Yield: 0.71% v 0.61% prior; Bid-to-cover: 2.63x v 1.61x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

- EquitiesIndices [Stoxx50 +0.7% at 3,474, FTSE +0.7% at 7,757, DAX +0.2% at 12,750, CAC-40 +0.3% at 5,483; IBEX-35 +1.3% at 9,757, FTSE MIB +0.3% at 22,185, SMI +0.3% at 8,646 , S&P 500 Futures +0.3%]

- Market Focal Points/Key Themes: European markets opened higher and continued positive as the session progressed; equities in general buoyed by positive sentiment following resolution of political situation in Italy and Spain; utilities and banks best performers; Ireland closed for holiday DS Smith offers to buy Europac; potential acquisition of Unicredit by SocGen; Accor working on collaboration with Air France-KLM; Delacaux to return to market pricing IPO; earnings expected in the upcoming US session include Dell Technologies and Palo Alto Networks; Colombia and Venezuela closed for holiday; attention turning to upcoming Fed meeting later in the week

Equities

- Consumer discretionary: Accor AC.FR -4.2% (potential collaboration with Air France), Air France AIR.FR +5.9% (potential collaboration with Accor), Cybergun CYB.FR -7.8% (potential bond issue)

Energy: Saipem SPM.IT +0.4% (contract win)

- Financials: Vastned VASTN.NL -0.4% (analyst action), CYBG PLC CYBG.UK +1.5% (progress on Virgin Money deal), Societe Generale GLE.FR +1.8% (potential merger with Unicredit), Unicredit UCG.IT -1.2% (potential merger with SocGen)

- Healthcare: Innate Pharma IPH.FR +4.2% (study results)

- Industrials: DS Smith SMDS.UK +3.3% (acquisition), Europac PAC.ES +8.2% (takeover offer), Fiat Chrysler FCA.IT -1.6% (5-year plan)

- Materials: Sunrise Resources SRES.UK +9.7% (potential sale)

- Technology: STMicroelectronics STM.FR +0.3% (analyst action)

- Utilities: Iberdrola IBE.ES +2.6% (analyst action)

Speakers

- Spain PM Sanchez Cabinet said to be ready in a few days

- Spain People's Party (PP) official: Senate group will amend the budget

- Russia Econ Min Orehskin: 2018 GDP growth was seen between 1.6-2.1% range. 2018 average oil price seen between $65-70/barrel

- Russia Central Bank 1st Dep Gov Yudaeva reiterated view that year-end CPI was seen closer towards the 4% inflation target

- Turkey Dep PM Simsek: Top priority was for price stability for sustainable high growth; Inflation could rise further in the short-term. Downtrend in inflation to begin in H2. Monetary and fiscal coordination to continue to increase

- Japan Fin Min Aso: No plans to resign over Moritomo land scandal, altered documents were regrettable. To create new procedure about document handling. Confirmed to return 1-year of his pay due to scandal (as speculated)

Currencies

- The USD was softer in the session. Dealers noted that White House Economic Advisor Kudlow made the media rounds over the weekend and warned that trade escalation might weaken the US economy. The US Treasury yield curve has undergone a bear flattening following the release of strong US labor market data last week to also weigh upon the greenback. Dollar unable to make fresh cycle highs despite a beat on the recent payroll data that now priced a 4th hike in 2018

- Emerging market currencies were firmer against the USD. The TUR currency (Lira) was fomer after hotter inflation data suggested that the Turkey Central Bank could again act and show its independence (Next rate decision on Thursday).

Fixed Income

- Bund Futures trade 34 ticks lower at 161.05 following Treasuries and as BTPs rise for a fourth consecutive day. Upside targets 163.75 followed by 164.50, while a return lower targets the 160.25 level.

- Gilt futures trade at 123.74 lower by 10 ticks after better than expected construction data. Support continues stands at 123.75 then 123.25, with upside resistance at 125.85 then 127.35.

- Monday’s liquidity report showed Friday’s excess liquidity rose from €1.890T to €1.925T. Use of the marginal lending facility decreased from €145M to €128M.

- Corporate issuance saw 2 issuer raise $0.5B

Looking Ahead

- (BR) Brazil Apr CNI Capacity Utilization: No est v 78.2% prior

- (RO) Romania May International Reserves: No est v $37.2B prior

- (UR) National Bank of Ukraine (NBU) Minutes

- 05:30 (NL) Netherlands Debt Agency (DSTA) to sell €1.0-2.0B in 6-month bills

- 06:00 (SE) Sweden Central Bank (Riksbank) Gov Ingves speech on E-money

- 06:45 (US) Daily Libor Fixing

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 08:00 (ES) Spain Debt Agency (Tesoro) announces of upcoming issuance

- 08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

- 08:05 (UK) Baltic Dry Bulk Index

- 08:55 (FR) France Debt Agency (AFT) to sell combined €4.3-5.5B in 3-month, 6-month and 12-month BTF Bills

- 09:00 (MX) Mexico Apr Leading Indicators M/M: No est v -0.02 prior

- 09:00 (SG) Singapore May Purchasing Managers Index (PMI): 53.0e v 52.9 prior; Electronic Sector: No est v 52.2 prior

- 09:30 (EU) ECB announces Covered-Bond Purchases

- 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

- 10:00 (US) Apr Final Durable Goods Orders: No est v -1.7% prelim; Durables Ex Transportation: No est v 0.9% prelim; Capital Goods Orders (Non-defense/ex-aircraft): No est v 1.0% prelim; Capital Goods Shipments (Non-defense/ex-aircraft): No est v 0.8% prelim

- 10:00 (US) Apr Factory Orders: -0.5%e v +1.6% prior; Factory Orders (Ex-transportation): No est v 0.9% prior

- 10:00 (DK) Denmark May Foreign Reserves (DKK): 467.5Be v 467.5B prior

- 12:00 (IS) Iceland Q1 Current Account Balance (ISK): No est v 3.0B prior

- 16:00 (US) Weekly Crop Progress Report

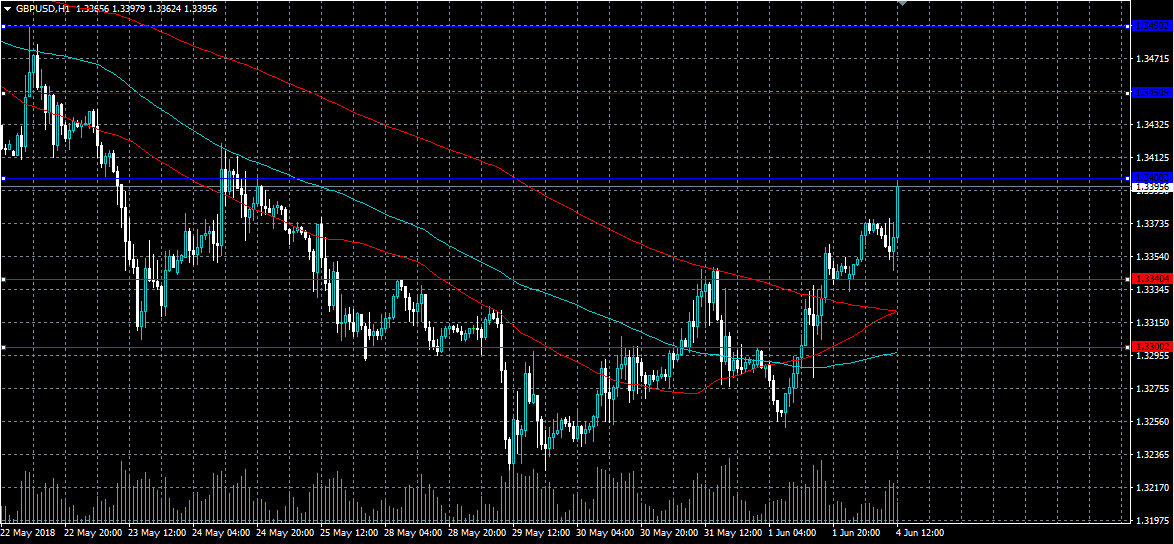

GBPUSD Further Bullish Above 1.3400 Level

The British pound has moved sharply higher against the greenback, following a stronger than expected UK Construction PMI and a reversal lower in the value of the US dollar index. The GBPUSD pair currently trades close to the key 1.3400 resistance level, with bullish trading momentum building across medium-term RSI and Stochastic indicators. Traders now await the release of US Factory Orders data and the intraday direction of the US dollar index.

The GBPUSD pair is strongly bullish while trading above the 1.3400 level, key resistance is located at the 1.3450 and 1.3490 levels.

If GBPUSD buyers fail to move price above the 1.3400 level, key technical support is found at the 1.3340 and 1.3300 levels.