Sample Category Title

RBA to Stand Pat with GDP also Eyed; Bank’s Communication to Set Tone for Aussie

The Reserve Bank of Australia will be completing its meeting on monetary policy on Tuesday, with a decision on interest rates scheduled for release at 0430 GMT. No change in rates is anticipated, with positioning on the aussie expected to be dictated by the tone given by the Bank in the statement accompanying the decision. Meanwhile, also of importance out of Australia are Q1 GDP figures due on Wednesday.

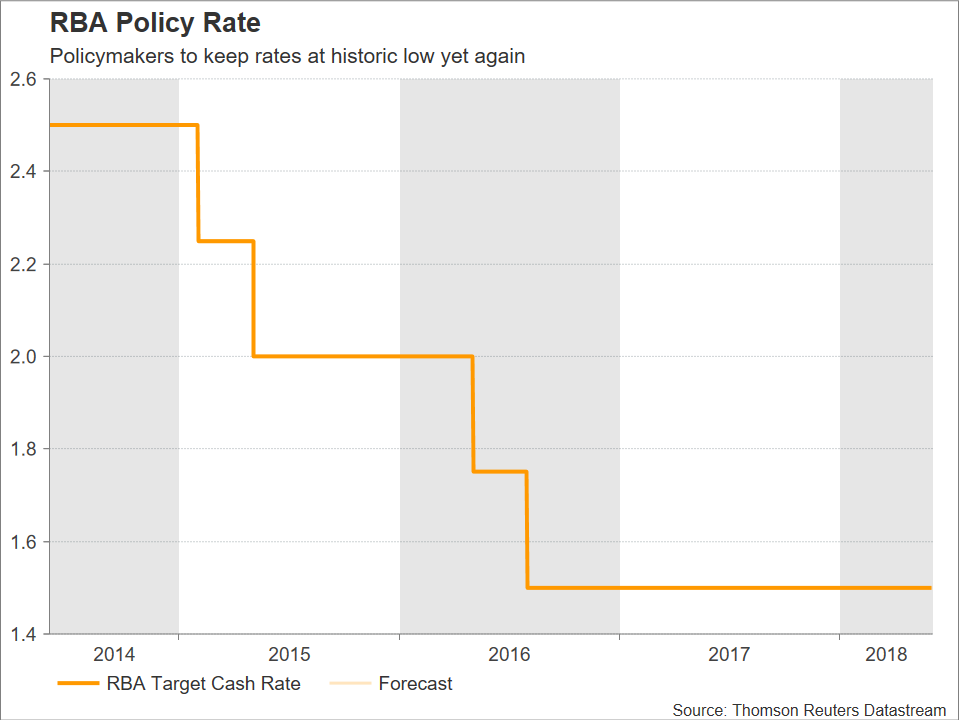

Australian headline inflation remained unchanged at 1.9% y/y in Q1, missing analysts’ forecasts that it would touch the lower band of the RBA’s 2-3% inflation target. The last time inflation growth entered the target band was in Q1 2017, when headline CPI came in at 2.1% y/y. In light of the inflation shortfall, the cash rate, this being the central bank’s policy rate, is widely expected to be maintained at the historic low of 1.50% for the 20th consecutive meeting. This constitutes the longest such stretch without an interest-rate move in the nation’s modern history.

But inflation undershooting the RBA’s target is not the only factor deterring the Bank from entering a rate normalization cycle. Worries over global trade are also an issue of consideration for RBA policymakers, and this was expressed during the Bank’s meeting in April as well. Concerns are justified due to the Australian economy’s status as a major commodity exporter and its close economic ties with China. An escalation of tensions between China and the US that introduces barriers to trade could weigh on Australia’s growth trajectory.

With respect to the latest developments on the trade front, US Secretary of Commerce Wilbur Ross was in Beijing over the weekend for talks with Chinese officials. Discussions failed to lead to a constructive outcome though, with the two parties maintaining a confrontational stance. Nevertheless, the market’s reaction was not a shift to risk-off assets, as it seems investors are getting used to such behavior by the world’s two largest economies; in the absence of conclusive measures against one-another, this was merely interpreted as posturing. Any updates on the topic in the days to come will be closely monitored.

Other RBA problem-areas that are keeping rates on hold, are high household debt levels and tepid wage growth despite overall robust jobs numbers that also pertain to full-time positions which are of more significance compared to part-time ones. Salaries not rising in a considerable fashion are also related to the relatively subdued inflation readings as well.

However, not all is gloomy, and the central bank has recently expressed optimism, projecting GDP growth to surpass potential output during 2018, as well as inflationary pressures as gauged by the CPI to increase gradually to a little above 2% on an annual basis.

Overall, a neutral stance is anticipated by the RBA in the statement justifying the rate decision upon completion of its meeting.

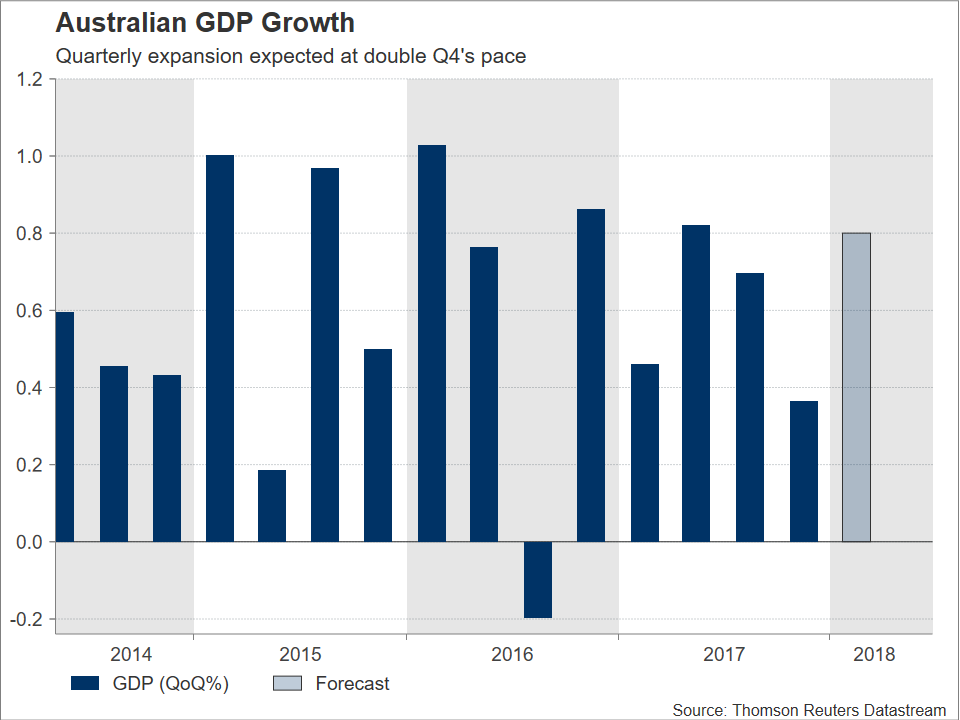

As far as GDP is concerned, the numbers pertaining to the first quarter of the year will be released on Wednesday at 0130 GMT, with growth anticipated to have accelerated during the quarter on both a quarterly (0.8% vs 0.4% in Q4) and yearly (2.7% vs 2.4% in Q4) basis. These are also likely to prove market-sensitive, while it is of note that the prints would add to the impressive more-than-two-decade run without a technical recession, defined as two consecutive quarters of economic contraction.

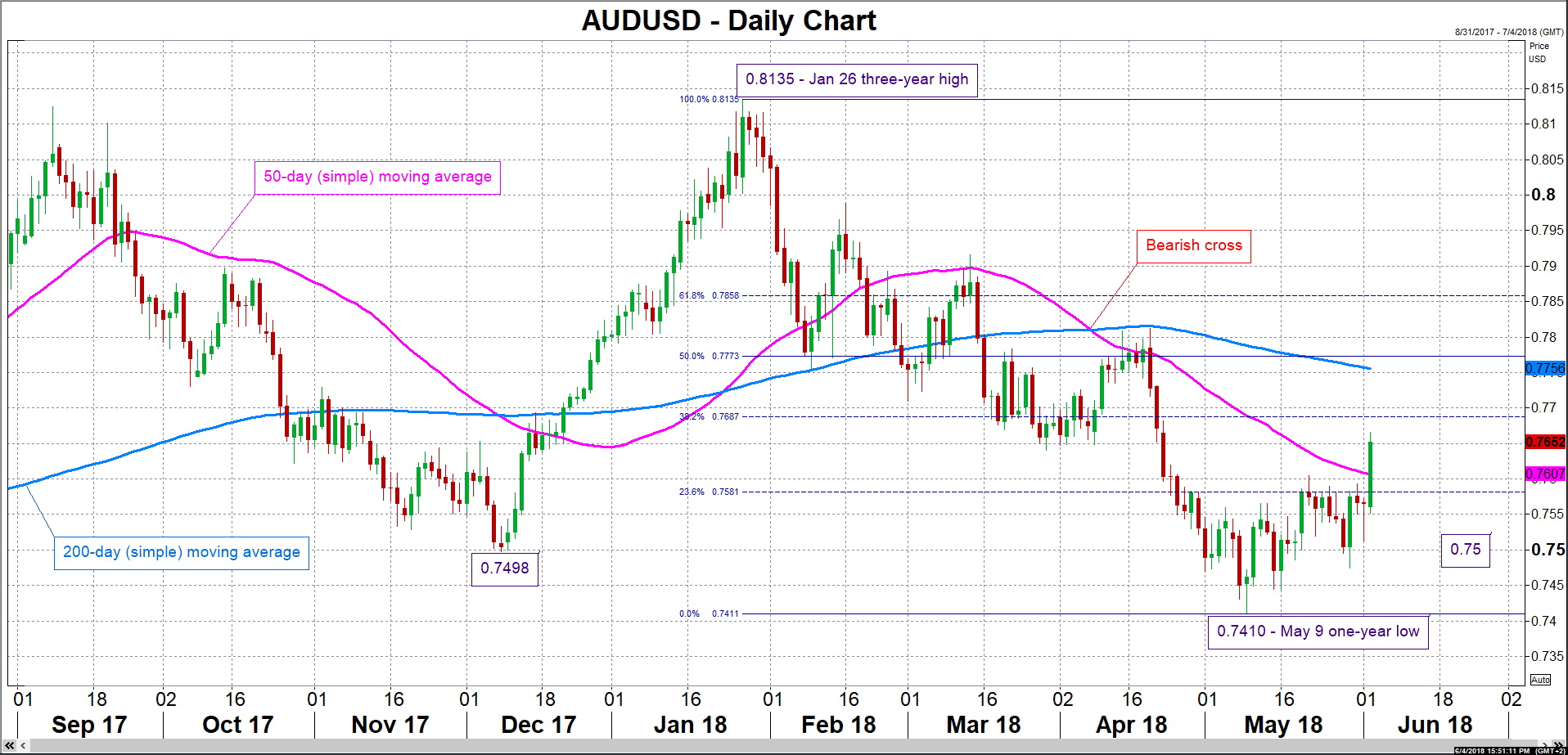

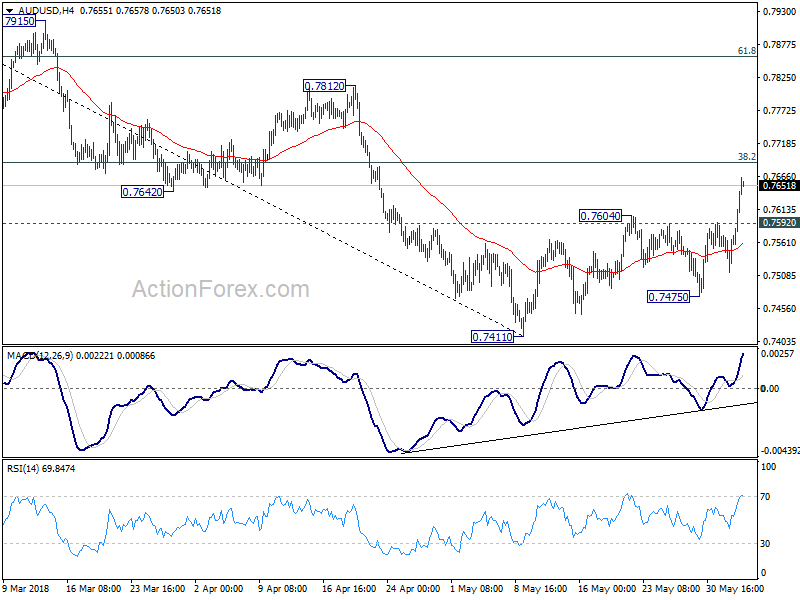

In terms of reaction in the FX markets and focusing on AUDUSD, an upbeat assessment of the Australian economy by the RBA, or a GDP beat, are likely to boost the pair. A barrier to price gains could come around the 38.2% Fibonacci retracement level of the January 26 to May 9 downleg at 0.7687. Notice that the area around this mark was relatively congested between mid-March and early-April, while it also encapsules the 0.77 round figure that may be of psychological importance. Steeper advancing would turn the attention to the region around the 200-day moving average line at 0.7756. Conversely, a cautious tone by the central bank that further pushes back in time market expectations for a rate hike, or disappointing GDP numbers, are expected to exert selling pressure in the aussie/dollar pair. Support to declines could initially emerge around the 50-day MA at 0.7607, including the 0.76 handle. Notice that the 50-day MA failed to act as resistance on the way up earlier on Monday, and may instead act as support. The 23.6% Fibonacci level lies not far below at 0.7581, while more bearish movement would increasingly bring into scope the 0.75 handle, which may also hold psychological significance.

Price action in aussie/dollar saw the pair rise to a six-week high of 0.7659 on Monday, rendering the aussie the strongest performer of the majors as the week got underway. The notable advance – +1.2% at 1251 GMT, the time of writing – partially came on the back of better-than-forecast Australian retail sales data released earlier in the day.

For the record and according to a Reuters poll, analysts do not see the RBA delivering a 25bps rate hike before Q2 2019. This compares to last month’s poll, where the consensus view made reference to a rate increase by March (Q1) next year.

Lastly, at 0130 GMT, a few hours before the RBA meeting concludes, data on Q1’s current account balance and net exports contribution to growth will also be made public out of Australia. These are also of importance and can lead to positioning in the aussie/dollar pair; the numbers can also give an indication regarding Q1 GDP figures due the following day. In the meantime, US releases should also be watched for their influence on the pair; one noteworthy data point on Tuesday’s calendar is the ISM’s non-manufacturing PMI for May.

Sunset Market Commentary

Markets:

Global core bonds traded directionless today, holding firm amid a positive risk sentiment. Asian and European equities eked out gains despite the collapsed trade talks between the US and China over the weekend and despite hawkish rhetoric from the EU side of the story. Italian BTP’s continued their positive run since the formation of a new government, but didn’t weigh on Bunds. The Italian 10-yr spread vs Germany narrowed by 15 bps to 215 bps, coming from a 290 bps peak at the end of May, but still significantly above levels from last month (114 bps). Spanish and Portuguese spreads narrowed by 12 bps. Disappointing EMU PPI data (0% M/M, 2% Y/Y) went unnoticed while the US eco calendar was empty. The marginal bear flattening of the US yield curve suggests that last week’s strong US eco data are still at work with next week’s FOMC meeting in mind. US yields add 1.6 bps (2-yr) to 0.7 bps (30-yr) at the time of writing. Changes on the German yield curve vary between +0.5 bps (2-yr) +1.8 bps (10-yr).

The risk-on correction from end last week continued today. Easing tensions on Italy and a positive investor reassessment on US/global growth were strong enough positives to outweigh lingering uncertainty on global trade. Strong US payrolls on Friday to some extent raised the probability of three additional Fed rate hikes this year, but didn’t support further USD gains. The further decline in intra-EMU spreads/risk premia supported the modest further short-squeeze in the euro. Investors probably also simply back-tracked on euro shorts that were set up during the Italian crisis during the second half of May. EUR/USD filled offers in the 1.1745 area at the start of US dealings, but the pair reversed part of the earlier gains during the US trading session (currently 1.1710). The swings in USD/JPY were very modest. The pair hovered around the 109.50 pivot. The small move in USD/JPY also suggests that the rise in EUR/USD was mainly a EUR/USD short-squeeze rather than anything else.

Sterling had quite a good run on Friday with EUR/GBP easing to the 0.8730/35 area. However, there was again no follow-through action on this sterling rise today. Euro strength prevailed. The UK construction PMI stabilized at 52.5, slightly better than the consensus estimate (52.0), but didn’t help sterling. EUR/GBP reversed part of Friday’s gain. The pair returned to well-known territory in the mid 0.87 area. The UK is said to come with the new plan on the Irish border in the run-up to the June 28 EU summit. For now, the story doesn’t impress sterling investors.

News Headlines:

Britain’s construction activity steadied in May according to the PMI (52.5 vs 52.0 expected) after a dismal start to the year, but new orders fell and companies grew more pessimistic about the outlook. (FT)

Czech real wages rose at their fastest pace in 15 years last quarter, rising 6.6% and adding to arguments that an interest rate hike may come sooner than anticipated. (Reuters)

UK PM May’s government is preparing to publish its plan to keep the UK under EU customs rules for longer as it seeks to break the Brexit deadlock, people familiar with the matter said. British negotiators expect to send the EU a document this week. (BB)

China's door to talks is open in principle, the country's Foreign Ministry said, a day after Beijing warned that any trade and business deals reached with Washington would be void if the US implemented tariffs. (Reuters).

Gold Calm at Start of Week, Services PMI Ahead

Gold has posted slight gains in the Monday session. In the North American session, the spot price for one ounce of gold is $1296.65, up 0.21% on the day. On the release front, it’s a quiet start to the week, with no major events on the schedule. US Factory Orders expected to decline 0.4%, after a strong gain of 1.6% in the previous release. On Tuesday, we’ll get a look at ISM Non-Manufacturing PMI and JOLTS Jobs Openings.

Are we heading towards a full-blown global trade war? There are some ominous signs that this could be the case, and what would be bad news for the markets could boost gold, which tends to move higher in times of crisis. On Thursday, the Trump administration made good on its threats and imposed stiff tariffs on the European Union, Mexico and Canada. The U.S had granted all three trading partners a temporary extension, but cited insufficient progress on trade talks as the reason for the tariffs. This has triggered promises of retaliatory tariffs on US products, and matters heated up on the weekend at the G-7 meeting of finance ministers in Canada. U.S Treasury Secretary Steve Mnuchin faced sharp criticism from other finance ministers over the tariffs.

A rate hike in June from the Federal Reserve is virtually a given, with the CME Group forecasting a gain of 94%. At the same time, there is increasing talk that the Fed is moving closer to a neutral monetary policy. Recent statements by FOMC policymakers appear to support such a conclusion, which would mean that the Fed would let the economy ‘ride on its own steam’ without intervening by adjusting interest rates. The minutes of the May meeting noted that policymakers would consider allowing inflation to rise above the Fed’s 2 percent target for a temporary period, which means that the Fed would not rush to raise rates based on the inflation target. After June, the Fed is most likely to raise rates in September. Analysts are divided on whether a fourth rate hike will be needed. If the economy is in danger of overheating, policymakers would have to seriously consider another rate increase in December.

IMF hailed France made impressive progress in reforms

IMF hailed in a report that France has made ""impressive progress" in policies that focuses on "addressing long-term challenges and building up resilience to shocks." Additionally, it's reform agenda ahead is "equally ambitious".

Regarding the economy, IMF noted that France is benefitting from a "broad-based recovery". Outlook is "positive" even though risks are "tilted to the downside". 2018 and 2019 growth is expected to "remain robust" even though less buoyant than 2017.

But there are domestic risks "if the pace of reforms slows" or "if reforms prove less effective than expected".

Externally, "increasing trade tensions, geopolitical uncertainty, or an erosion of confidence in the European project could negatively affect exports and growth". Faster than expected interest rate normalization could also weigh on public and private balance sheets.

Here is the full report.

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7531; (P) 0.7553; (R1) 0.7590; More...

AUD/USD's rebound form 0.7411 extends to as high as 0.7665 so far today. And intraday bias stays on the upside for further rally. Still, such rebound is see as a correction. Therefore, we'd expect strong resistance from 38.2% retracement of 0.8135 to 0.7144 at 0.7688 to limit upside. On the downside, below 0.7592 minor support will turn bias to the downside for 0.7475 first. Break there will likely resume larger fall through 0.7411 to 0.7328 cluster support (61.8% retracement of 0.6826 to 0.8135 at 0.7326). However, sustained break of 0.7688 will dampen our bearish view and target 61.8% retracement at 0.7585 instead.

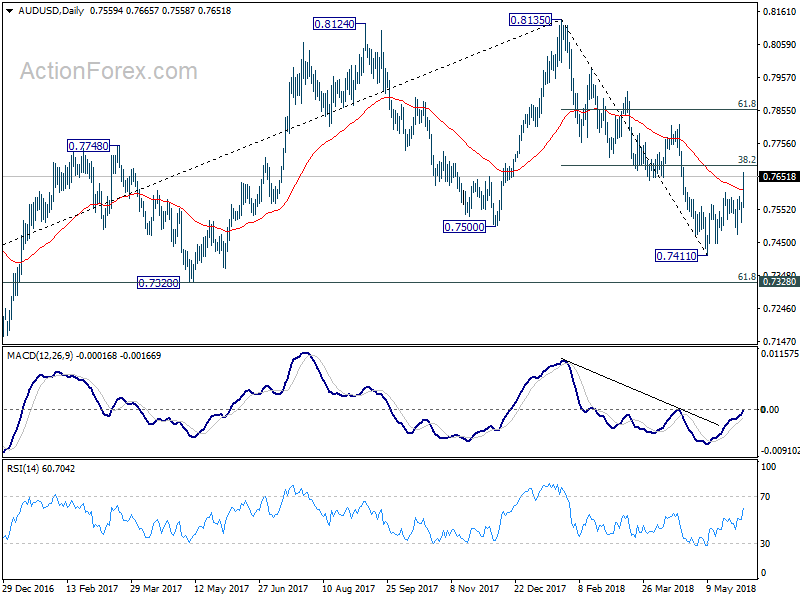

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.92; (P) 109.32; (R1) 109.93; More...

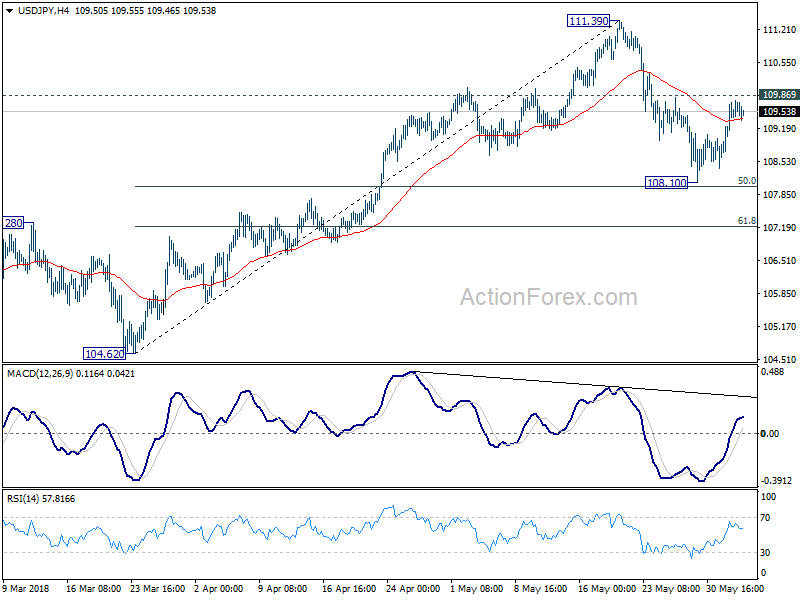

No change in USD/JPY's outlook. Intraday bias remains neutral with focus on 109.82 minor resistance. Break there will indicate completion of the pull back from 113.39. And that will revive the bullish case that rise from 104.62 is still in progress. Retest of 111.39 should be seen first. On the downside, though, break of 108.10 will extend the fall from 108.10 to 61.8% retracement of 104.62 to 111.39 at 107.20 instead.

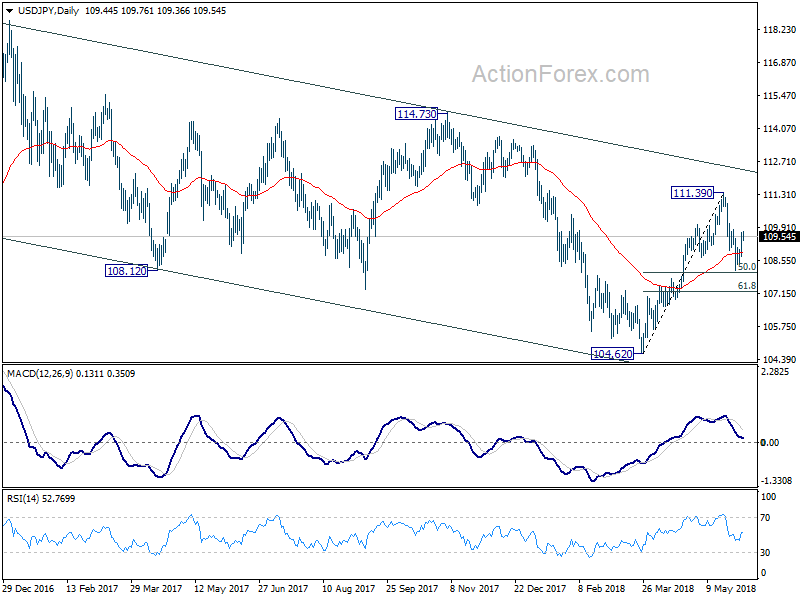

In the bigger picture, at this point w;'re slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this week and target 114.73 for confirmation. However, it should be noted that USD?JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

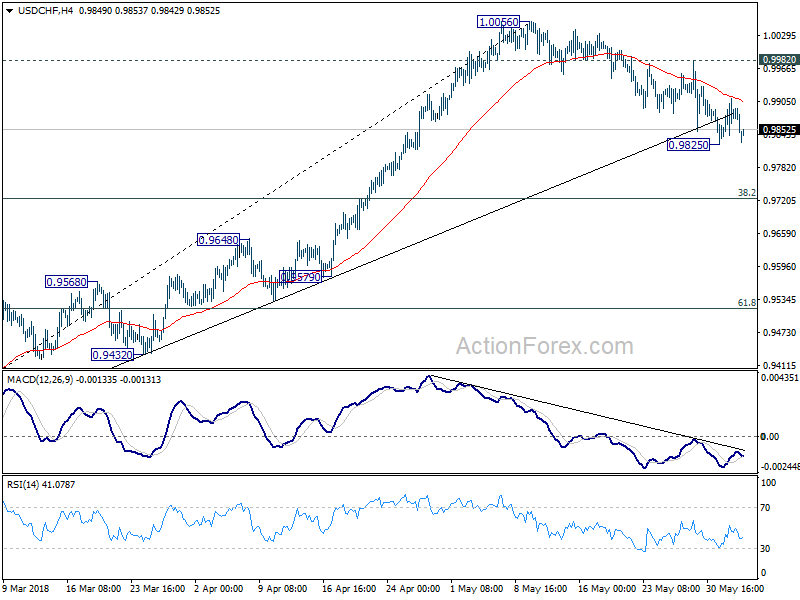

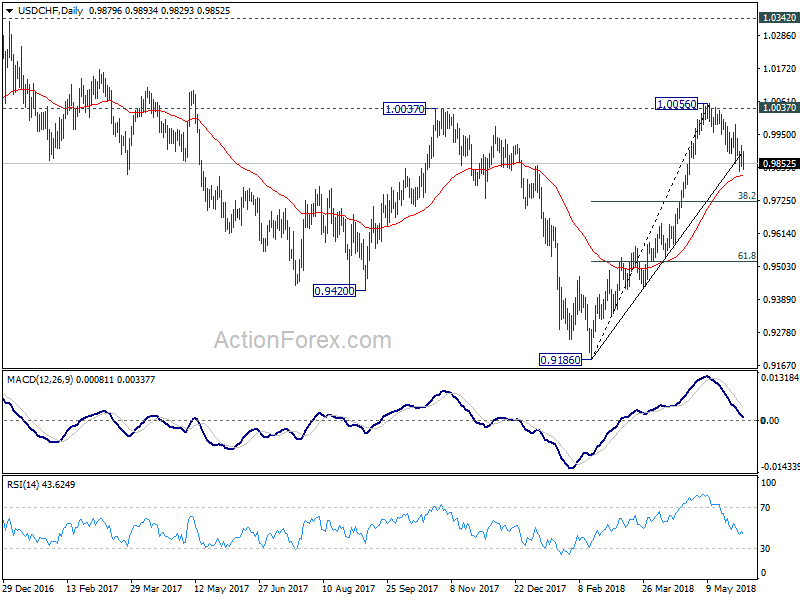

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9842; (P) 0.9878; (R1) 0.9914; More...

USD/CHF is staying in tight range above 0.9825 and intraday bias remains neutral. On the downside, break of 0.9825 will indicate that fall from 1.0056 is correcting whole rise from 0.9186. In that case, deeper decline would be seen to 0.9724 fibonacci level before completion. On the upside, above 0.9982 minor resistance will suggest that the pull back is finished and bring retest of 1.0056.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

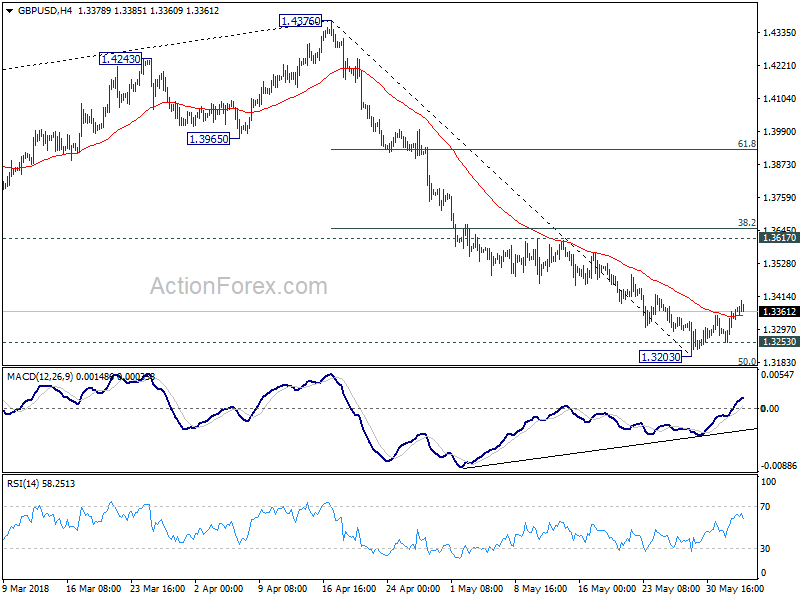

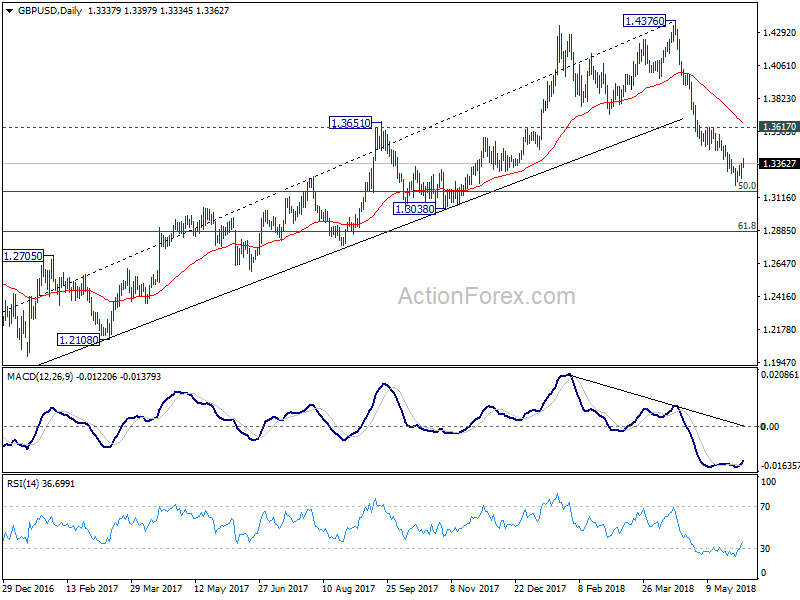

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3280; (P) 1.3322; (R1) 1.3389; More...

GBP/USD's recovery from 1.3203 is still in progress and could extend higher. But as it's seen as a correction, upside should be limited by 1.3617 resistance to bring reversal. On the downside, break of 1.3253 minor support will likely resume the fall from 1.47376 through 1.3203 for 50% retracement of 1.1946 to 1.4376 at 1.3161 first, and 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3648) holds, even in case of strong rebound.

British Pound Higher as Construction PMI Beats Estimate

The British pound has moved upwards at the start of the week. In Monday’s North American session, GBP/USD is trading at 1.3384, up 0.25% on the day. On the release front, British Construction PMI remained unchanged at 52.5 in April, above the estimate of 52.0 points. There is just one event on the calendar, with US Factory Orders expected to decline of 0.4%, after a strong gain of 1.6% in the previous release. On Tuesday, the focus will be on the services sector. The U.K releases Services PMI and the U.S publishes ISM Non-Manufacturing PMI and JOLTS Jobs Openings.

A rate hike in June from the Federal Reserve is virtually a given, with the CME Group forecasting a gain of 94%. At the same time, there is increasing talk that the Fed is moving closer to a neutral monetary policy. Recent statements by FOMC policymakers appear to support such a conclusion, which would mean that the Fed would let the economy ‘ride on its own steam’ without intervening by adjusting interest rates. The minutes of the May meeting noted that policymakers would consider allowing inflation to rise above the Fed’s 2 percent target for a temporary period, which means that the Fed would not rush to raise rates based on the inflation target. After June, the Fed is most likely to raise rates in September. Analysts are divided on whether a fourth rate hike will be needed. If the economy is in danger of overheating, policymakers would have to seriously consider another rate increase in December.

The U.S published strong employment numbers on Friday, but the releases provided only a small boost for the US dollar. Wage growth improved to 0.3% in May, up from 0.1% a month earlier. Nonfarm payrolls jumped from 189 thousand to 164 thousand and the unemployment rate dropped to a sizzling 3.8 percent. All three indicators beat their estimates and are indicative of a labor market running at full capacity midway through the second quarter.

With the European Union finding itself embroiled in an escalating trade war with the Trump administration, Brexit supporters are no doubt wishing that the U.K had its own trade agreement with the U.S. Although Britain has one foot out of the EU, any tariffs applied to the EU could cost British jobs.

On Thursday, the Trump administration made good on its threats and imposed stiff tariffs on the European Union, Mexico and Canada. The U.S had granted all three trading partners a temporary extension, but cited insufficient progress on trade talks as the reason for the tariffs. This has triggered promises of retaliatory tariffs on US products, and matters heated up on the weekend at the G-7 meeting of finance ministers in Canada. U.S Treasury Secretary Steve Mnuchin faced sharp criticism from other finance ministers over the tariffs. There are fears that the escalating trade tensions could trigger a global trade war.

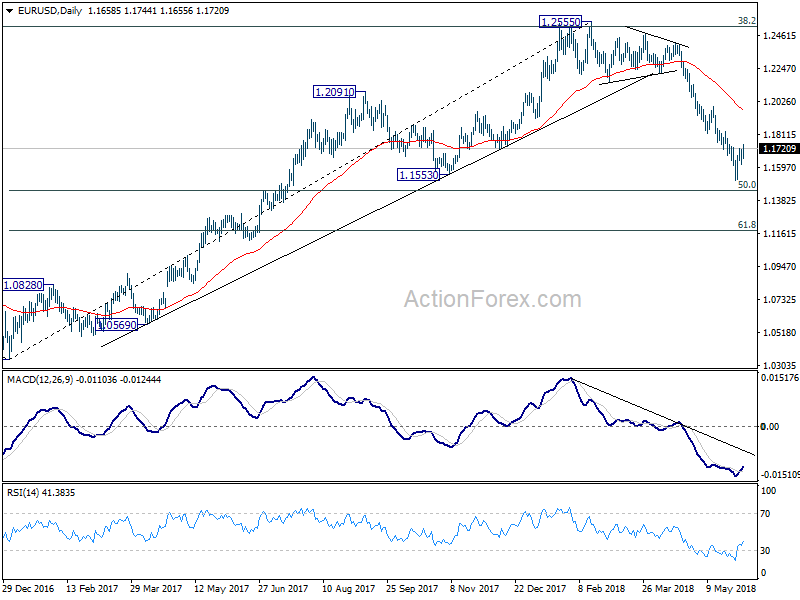

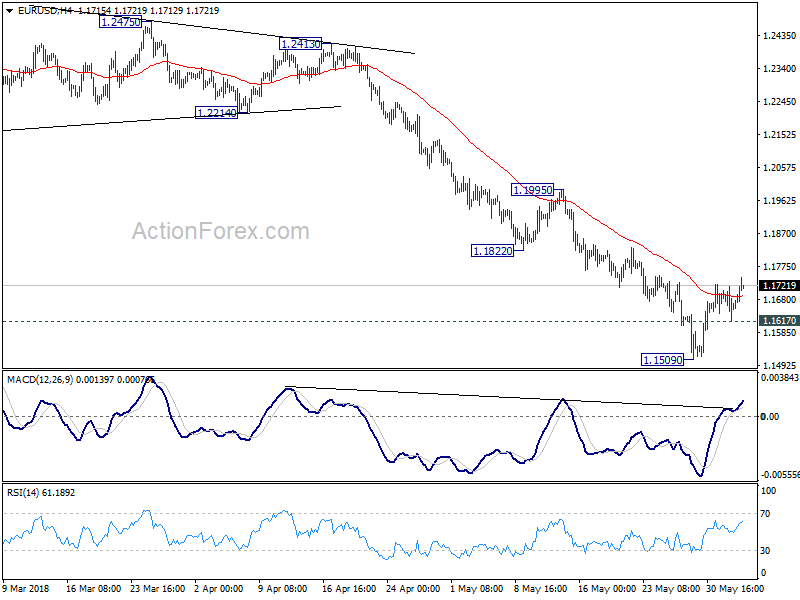

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1611; (P) 1.1665 (R1) 1.1712; More.....

EUR/USD's rebound from 1.1509 extends higher today. But after all it's seen as a correction. Hence, in case of further rally, we'd expect strong resistance from 1.1822/1995 resistance zone to limit upside and bring fall resumption eventually. On the downside, below 1.1617 minor support will bring retest of 1.1509 low first. Break will resume the decline from 1.2555 and target 50% retracement of 1.0339 to 1.2555 at 1.1447. Break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.