Sample Category Title

Elliott Wave Analysis: SPX Close To A Pullback?

SPX short-term Elliott wave view suggests that the rally from 4/02/2018 low (2553.8) is extending higher in 5 waves structure. These 5 waves are expected to be part of a leading diagonal structure within intermediate wave (1) higher. The move higher from 2553.8 low has the characteristic of a diagonal where the internal distribution of each leg higher shows sub-division of 3 waves and there’s an overlap between Minor wave 1 &4 .

The internals of a rally from 2553.8 low ended Minor wave 1 at 2717.49 in 3 waves corrective sequence. Down from there, the pullback to 2594.62 low ended Minor wave 2 as Elliott wave double three structure. Above from there, the rally to 2742.1 high ended Minor wave 3 as Elliott Wave Zigzag structure. Below from there, the pullback to 2676.81 low ended Minor wave 4 as zigzag structure. Near-term focus remains towards 2752.9 – 2765.33, which is 100%-123.6% Fibonacci extension area of Minute wave ((a))-((b)) to end Minor wave 5. The move higher should also complete the cycle from 4/02/2018 low (2553.8) within Intermediate wave (1). Afterwards, the index is expected to do a pullback in Intermediate wave (2) and expected to find buyers in 3, 7 or 11 swings for further upside. We don’t like selling the index.

SPX 1 Hour Elliott Wave Chart

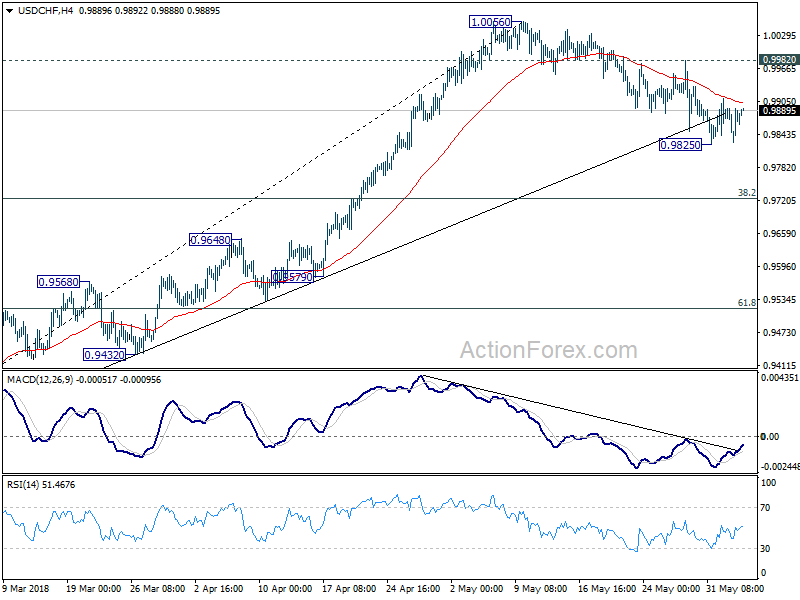

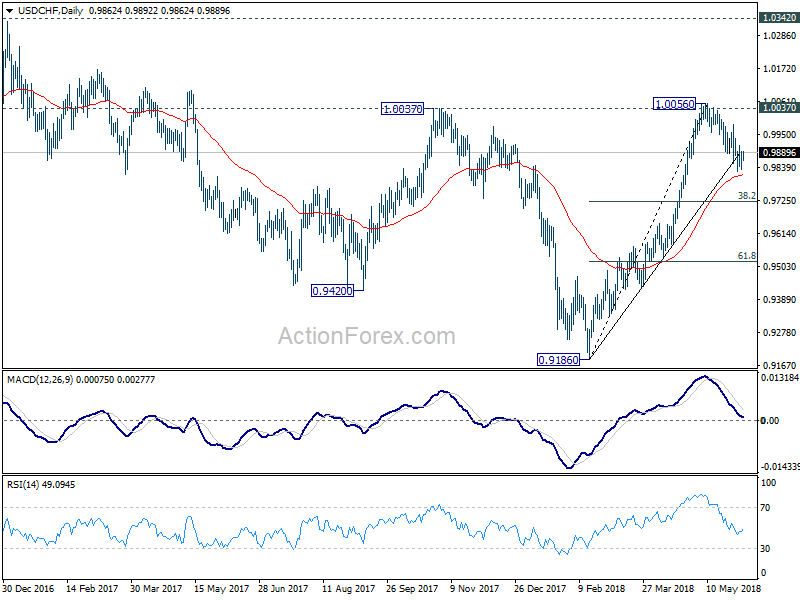

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9842; (P) 0.9868; (R1) 0.9908; More...

Intraday bias in USD/CHF remains neutral at this point. On the downside, break of 0.9825 will indicate that fall from 1.0056 is correcting whole rise from 0.9186. In that case, deeper decline would be seen to 0.9724 fibonacci level before completion. On the upside, above 0.9982 minor resistance will suggest that the pull back is finished and bring retest of 1.0056.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

Market Morning Briefing: Euro Also Came Close To Testing The 21 Days MA Near 1.176

STOCKS

Dow (24813.69, +0.72%) has tried to move up again towards 24800-25000 resistance levels. Note that a break above or rejection from these levels would be crucial to drive the next course of movement. A break above 25000, if seen would be very bullish for the medium term targeting 25500-25750 while a rejection from 25000 could take it down to 24000 levels.

Dax (12770.75, +0.37%) rose initially but closed in the red. The index could be stuck in the 12900-12500 region for the coming sessions. Important resistance is near 13000-13050 levels and could hold in the medium term to push back the index towards 12500 in the longer run.

Nikkei (22482.85, +0.031%) is headed towards resistance near 22800 and could come off from there in the coming sessions. Overall long term looks bearish but a strong rejection from 22800 is yet to materialize.

Shanghai (3083.82, -0.24%) is trading above 3050 and looks stable for now. Some range-trade in the 3050-3100 region is possible for the near term. A break above 3150 or below 3050 would determine the next course of directional movement. Till then the index is likely to remain in sideways consolidation.

Nifty (10628.50, -0.63%) fell sharply towards our expected 10600-10550 levels. Some more downside towards 10500 is possible in the coming sessions before the index pauses. Sensex (35011.89, -0.61%) also came off sharply and could test immediate support near 34750. The stocks closed lower yesterday, dragged by the financials and amid caution during the RBI's 3-day interest rate setting meeting. The indices could trade lower today also followed by a bounce back by the end of the week.

COMMODITIES

Brent (75.50) has immediate support near 75 and then at lower levels of 74. While these supports hold, we may not see a fall below 74 in the near term and the price may bounce back in the next few sessions towards 77-78.

WTI (65.06) has broken immediate support near 66 on the daily candle chart and while the price trades lower, a test of 63.0-62.50 is possible in the medium term. WTI looks more bearish than Brent just now and in case WTI continues to fall sharply, it could drag Brent also to lower levels.

Gold (1292.04) looks bearish while below 1300. A test of 1270 looks possible on the downside.

Copper (3.1274) has risen and is testing immediate resistance on the daily candles. If this holds, the price could again fall back to 3.05. Else a sharp break on the upside, if seen would be bullish towards 3.15-3.20 levels in the medium term. A rejection from current resistance looks more probable.

FOREX

Dollar index (94.08) almost touched the 21 days MA near 93.6 by seeing a low of 93.66 yesterday. However it quickly rose back again, above support trendline on daily candles near 93.8-94.0. It has been trading below 94.25 for the last 3 sessions but could now move higher than that towards 95. Repeating yesterday's comment: the upside / downside levels for the Dollar Index which, when broken, could confirm bullishness / bearishness in the medium term could be 95.5-96.0 and 93.5-93.0 respectively.

Euro (1.1689): Euro also came close to testing the 21 days MA near 1.176 (as it saw a high of 1.1745). However it again fell to levels below 1.17. It might dip lower over today-tomorrow to levels near 1.163 (as the Dollar Index possibly moves higher towards 94.5). Repeating yesterday's comment: The upside / downside levels for the Euro which, when broken, could confirm bullishness / bearishness in the medium term could be 1.178-1.182 and 1.140-1.135 respectively.

Dollar Yen (109.88) has broken resistance in the downward channel on daily candles near 109.6 and has seen a high near 109.99 already. The 21 days MA near 109.7 could still provide some resistance. But if the Dollar Yen stays above 109.7, it could well go on to test previous highs near 111.40. On the downside, only a break of 108 would confirm medium term bearishness.

Euro Yen (128.46) is only moving higher after testing support in downward channel on weekly candles last week. With Dollar Yen seeming bullish, Euro Yen could well move even higher towards 129.5 (seen as crucial resistance level on weekly candles). After a test of 129.5, Euro Yen should dip.

Pound (1.3307): As expected, Pound saw a high near 1.34 yesterday but closed lower near 1.342 (thereby respecting resistance on daily line chart). It could now move lower towards 1.32 in the next 1-2 sessions. We have been expecting Pound to gradually downtrend towards 1.30 (support on weekly candles) in the coming weeks. A break of 1.30 could imply continued bearishness in the medium term.

Dollar Rupee (67.115) : Dollar-Rupee may rise to 67.35-50 over the next few days, which is a super-crucial Resistance. Whether that breaks or holds will set the trend for the medium term.

INTEREST RATES

Last Friday, a strong jobs report and wages data in USA had led to a rise in US Yields, taking the 10 Year yield above 2.9%. Next week might see significant movement in US yields as there are some key data releases (like the US CPI) and also the FOMC meeting. Given that a rate hike is more or less certain and would already have been factored in, a significant rise in yields due to the expected rate hike might not take place.

Our May '18 US Treasury report ( available on demand ) forecasts a near term dip in US yields towards medium term supports near 2.55% (10 Year), 2.9% (30 Year) and 2.2% (5 Year). Dips towards these levels would require some indications of dovishness from the US Fed in next week's meeting. Let's wait and watch.

Current yields: US 10 Year (2.937%), 30 Year (3.079%), 5 Year (2.79%), 2 Year (2.51%)

The US 10 year yield has risen above earlier support trendline on short term chart near 2.90% and did not get resistance from it as we had expected. It is still testing support on medium term chart and could rise some more from here towards 2.97%. The EU Retail sales data later today could have some bearing on German yields, which in turn could also directly impact US Yields

Dollar Higher as US Yields Rebound, Aussie Pares Gain as Neutral RBA Stands Pat

Dollar trades broadly higher today as helped by the rebound in US treasury yields. 10 year yield closed up 0.042 at 2.937 overnight. With a base formed at 2.759 last week, TNX will likely head higher to 3.000 handle. The development would be dollar supportive in near term. Meanwhile, Australia Dollar is paring back some of this week's surprised gains after RBA left cash rate unchanged 1.50% as widely expected. The accompanying statement is largely unchanged from the prior one. RBA reiterated again that pickup in wage growth and inflation will be gradual. Also, the central bank maintained a neutral stance, refraining from indicating a tightening bias.

Technically, USD/JPY's break of 109.82 minor resistance revived bullishness in the pair and more upside could be seen in near term back to 111.39 high. A question is whether the rebound in USD/JPY would take EUR/JPY and GBP/JPY higher through key near term resistance levels at 128.94 and 147.04 respectively. On the other hand, recovery in EUR/USD and GBP/USD appear to have lost steam. Focus will be back on 1.1617 minor support in EUR/USD and 1.3253 in GBP/USD. So it could be the weakness in EUR/USD and GBP/USD that drag down EUR/JPY and GBP/JPY. It's very interactive.

BoE Tenreyro stood pat in may to wait a little more

BoE MPC member Silvana Tenreyro said yesterday that "much of the downside Q1 GDP news is likely to be erratic". However, that still increased the "possibility of some underlying weakness in demand". Back in the May meeting, Tenreyo said the costs of waiting-and-see for a short period were relatively slow. And BoE will likely get a "significantly clearer picture of the underlying strength of domestic demand quite soon". Therefore, there were "to leaving policy unchanged." Overall, Tenreyo said "while I anticipate that a few rate rises will be needed, the timing of those rate rises is an open question."

Tenreyro's messages were consistent with BoE's own forecast in the inflation report that there would be a rate hike in August. That is, BoE opted to wait a little while more in May till August to make a decision. And, that is data dependent.

IMF: Canada outlook subjects to significant risks, domestic and external

In a report released yesterday, IMF noted that the 3% growth in 2017 in Canada was the highest among G7 nations in the year. But going ahead, the economic outlook is subject to "significant risks, domestic and external".

Domestically, a key risk is sharp correction in the housing market. That could be triggered by a "sudden shift in price expectations or a faster-than-expected increase in mortgage interest rates". And, the banking system is "heavily exposed to household and corporate debt." Thus, if housing correction is accompanied by rise in unemployment and sharp contraction in private consumption, "risks to financial stability and growth could emerge".

Externally, the medium term impact of US tax cuts could make Canada a "less attractive destination for investment". Failure to reach a NAFTA agreement within a reasonable timeframe could impact investment and growth for an "extended period". And return to WTO rules could cut GDP growth by -0.4%. Other external risks include weaker growth in key advanced economies, sharp slowdown in China, tighter global financial conditions.

Regarding monetary policy, IMF said BoC should tighten "gradually" as "inflationary pressures are building and higher interest rates will help activity and inflation converge toward more sustainable levels." But the current balance of risks warrants "gradual policy normalization."

NZ Treasury: Q1 growth may fall short of 0.7% forecast

In the Monthly Economic Indicator report published today, New Zealand Treasury noted that the tracking of March quarter data suggested real GDP growth may fall short of 0.7% as forecast in the Budget Economic and Fiscal Update (BEFU) 2018. Nonetheless, June quarter activity indicators have been "a little more positive". Subdued wage pressures are likely contributing to low inflation, and the expectation that RBNZ will keep OCR at 1.75% "for some time to come".

Risks are skewed to the downside as led by international developments. In particular, the Treasury noted slowdown in Japan, Eurozone and UK in Q1. And it warned that political instability in Italy will drag Eurozone growth further. Nonetheless, the outlook for China and the US "remains relatively positive".

On the data front

Japan household spending dropped -1.3% yoy in April versus expectation of 0.8% mom. China Caixin PMI services was unchanged at 52.9 in May. Australia current account deficit narrowed to AUD -10.5B in Q1. UK BRC retail sales monitor rose 2.8% yoy in May.

Services data are the major focuses today. In particular, UK PMI services is expected to rise 0.1 in May to 52.9. Eurozone will also release PMI services final. Later in the day, US will release ISM non-manufacturing while Canada will release labor productivity.

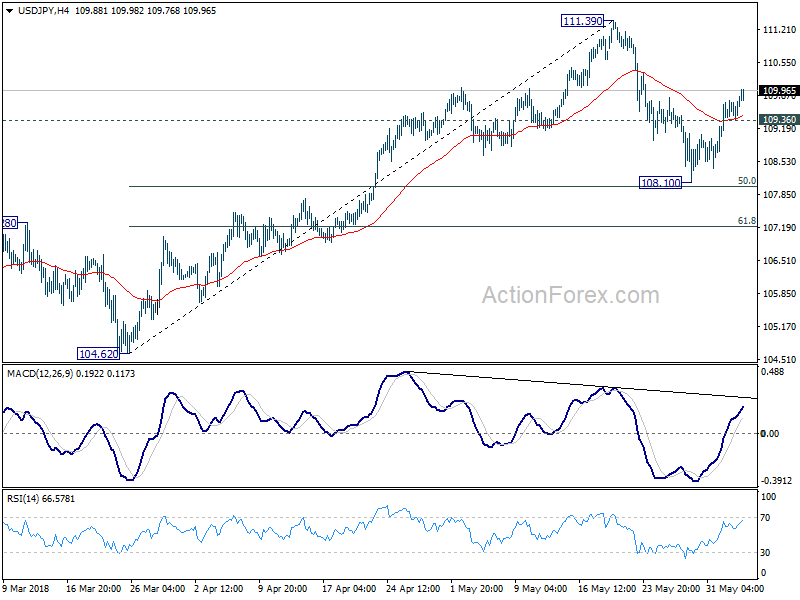

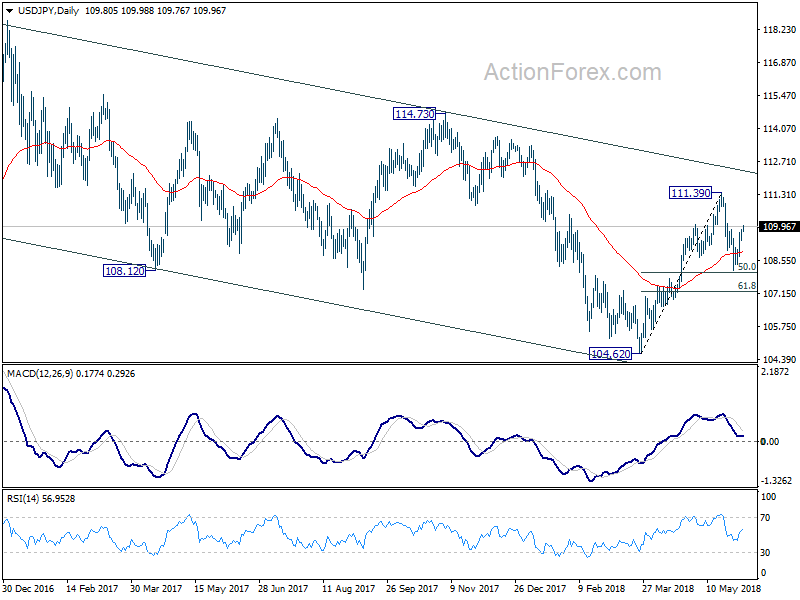

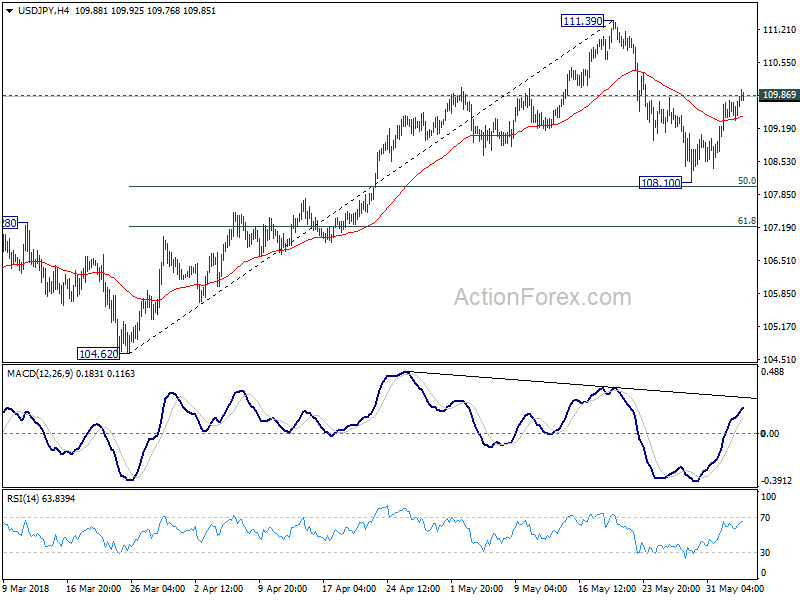

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.50; (P) 109.69; (R1) 110.02; More...

Breach of 109.82 minor resistance suggests that pull back from 111.39 has completed at 108.10 already. ahead of 50% retracement of 104.62 to 111.39. The development revived that case that rebound from 104.62 is still in progress. Intraday bias is back on the upside for 111.39 first. Break will target a test on 114.73 key resistance level. On the downside, though, below 109.36 minor support will delay the bullish case and turn bias neutral again.

In the bigger picture, at this point , we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y May | 2.80% | -4.20% | ||

| 23:30 | JPY | Household Spending Y/Y Apr | -1.30% | 0.80% | -0.70% | |

| 01:30 | AUD | Current Account (AUD) Q1 | -10.5B | -9.9B | -14.0B | -14.7B |

| 01:45 | CNY | Caixin PMI Services May | 52.9 | 53 | 52.9 | |

| 04:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 07:45 | EUR | Italy Services PMI May | 52.9 | 52.6 | ||

| 07:50 | EUR | France Services PMI May F | 54.3 | 54.3 | ||

| 07:55 | EUR | Germany Services PMI May F | 52.1 | 52.1 | ||

| 08:00 | EUR | Eurozone Services PMI May F | 53.9 | 53.9 | ||

| 08:30 | GBP | Services PMI May | 52.9 | 52.8 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | 0.50% | 0.10% | ||

| 12:30 | CAD | Labor Productivity Q/Q Q1 | 0.30% | 0.20% | ||

| 13:45 | USD | US Services PMI May F | 55.7 | 55.7 | ||

| 14:00 | USD | ISM Non-Manufacturing Composite May | 57.4 | 56.8 |

Italy’s New Government Formed Eventually. Next Uncertainty is Economic Reform

Political deadlock in Italy was broken last week as President Mattarella approves the new cabinet after the euro-sceptic finance minister candidate, Paolo Savona, was replaced by Giovanni Tria. Tria supports that Italy should remain in the Eurozone, despite his call for reforms to the single currency. He is also supportive of the League's heavily simplified tax rate, while worries about M5S's plans to introduce a form of universal basic income. Savona will stay in the cabinet, taking up the role of European Affairs Minister. Other members in the cabinet are the same as the original plan with Giuseppe Conte being the prime minister. Financial markets calmed with bond yields of Italy, as well as those in peripheral European economies, easing and stock markets recovering. The single currency also recovered. Despite better sentiment, ongoing political uncertainty in peripheral Europe still warrants attention, in particular economic policy of the new Italian populist government and the upcoming snap election in Spain.

The parliamentary confidence vote would be held Tuesday and Wednesday. It would likely be supported by M5S and the League only. Other parties either reject or abstain. For instance, we expect Brother of Italy would not support but might not vote openly against it. Meanwhile, relations between the League and Forza Italia has turned sour as the former’s strong commitment to combat corruption included in the joint economic policy has displeased Forza Italia’s leader Berlusconi.

The situation reflects the difficulty in pushing the economic reform proposed by the populist duo, with its thin majority in the parliament. The new government would find the challenge of withstanding political and market pressures. The thin majority could disappear if just a few M5S/League members dissent on the more controversial policies. Moreover, President Matterela retains the veto power of government bills which are deemed “unconstitutional”. According to Article 81 of the Constitution, he could reject fiscal measures which could jeopardize the stability of public finance at risk. As we mentioned in the previous report, the latest version of the economy policy might result in a deficit slippage of 108-125B euro (6-7% GDP), in addition to the current 30B euro (1.7% GDP). Given the controversial nature of the economic plan, we doubt how many of the proposed policies could be approved. Implementation of the reform directly affects support or, hence the durability of, the new government. On the other hand, the government plans, if fully implemented, would result in major deterioration in the outlook of the country’s sovereign debt. Investors would price in more credit risk for Italy’s sovereign and higher spreads would follow.

Spain

In Spain, the political drama resumed. Socialist Pedro Sanchez has become the Prime Minister of the country as Mariano Rajoy was ousted after the vote of no confidence on June 1. Rajoy’s People’s Party was found guilty by the court last month of illegal party funding. The dust is far from settled as Sanchez is leading a minority government with Socialist’s 25% of seats in the Congress. The possibility of a snap election cannot be ruled out.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.50; (P) 109.69; (R1) 110.02; More...

Breach of 109.82 minor resistance suggests that pull back from 111.39 has completed at 108.10 already. ahead of 50% retracement of 104.62 to 111.39. The development revived that case that rebound from 104.62 is still in progress. Intraday bias is back on the upside for 111.39 first. Break will target a test on 114.73 key resistance level. On the downside, though, below 109.36 minor support will delay the bullish case and turn bias neutral again.

In the bigger picture, at this point , we're slightly favoring the case that corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Above 111.39 will affirm this view and target 114.73 for confirmation. However, it should be noted that USD/JPY is bounded in medium term falling channel from 118.65 (2016 high). Sustained break of 61.8% retracement of 104.62 to 111.39 at 107.20 will likely resume the fall from 118.65 through 104.62 low.

RBA left cash rate unchanged at 1.50%, full statement

RBA left cash rate unchanged at 1.50%, full statement below:

Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus and further steps in this direction are expected.

Financial markets have been affected by political developments in the eurozone, particularly in Italy. There are also concerns about the direction of international trade policy in the United States and economic developments in a few emerging market economies. Long-term bond yields in most major economies have declined recently and there has been some widening of corporate credit spreads. Overall, though, financial conditions remain expansionary. Conditions in US dollar short-term money markets have eased recently, although they are tighter than earlier in the year, with US dollar short-term interest rates having increased for reasons other than the increase in the federal funds rate. The higher rates in the United States have flowed through to higher short-term interest rates in a few other countries, including Australia.

The price of oil has increased over recent months, as have the prices of some base metals. Australia's terms of trade are expected to decline over the next few years, but remain at a relatively high level.

The recent data on the Australian economy have been consistent with the Bank's central forecast for GDP growth to pick up, to average a bit above 3 per cent in 2018 and 2019. Business conditions are positive and non-mining business investment is increasing. Higher levels of public infrastructure investment are also supporting the economy. Stronger growth in exports is expected. One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high.

Employment has grown strongly over the past year, although growth has slowed over recent months. The strong growth in employment has been accompanied by a significant rise in labour force participation, particularly by women and older Australians. The unemployment rate has been little changed at around 5½ per cent for much of the past year. The various forward-looking indicators continue to point to solid growth in employment in the period ahead, with a gradual reduction in the unemployment rate expected. Wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation is low and is likely to remain so for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

The Australian dollar remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

The housing markets in Sydney and Melbourne have slowed. Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. Housing credit growth has slowed over the past year, especially to investors. APRA's supervisory measures and tighter credit standards have been helpful in containing the build-up of risk in household balance sheets, although the level of household debt remains high. While there may be some further tightening of lending standards, the average mortgage interest rate on outstanding loans is continuing to decline.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

(RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus and further steps in this direction are expected.

Financial markets have been affected by political developments in the eurozone, particularly in Italy. There are also concerns about the direction of international trade policy in the United States and economic developments in a few emerging market economies. Long-term bond yields in most major economies have declined recently and there has been some widening of corporate credit spreads. Overall, though, financial conditions remain expansionary. Conditions in US dollar short-term money markets have eased recently, although they are tighter than earlier in the year, with US dollar short-term interest rates having increased for reasons other than the increase in the federal funds rate. The higher rates in the United States have flowed through to higher short-term interest rates in a few other countries, including Australia.

The price of oil has increased over recent months, as have the prices of some base metals. Australia's terms of trade are expected to decline over the next few years, but remain at a relatively high level.

The recent data on the Australian economy have been consistent with the Bank's central forecast for GDP growth to pick up, to average a bit above 3 per cent in 2018 and 2019. Business conditions are positive and non-mining business investment is increasing. Higher levels of public infrastructure investment are also supporting the economy. Stronger growth in exports is expected. One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high.

Employment has grown strongly over the past year, although growth has slowed over recent months. The strong growth in employment has been accompanied by a significant rise in labour force participation, particularly by women and older Australians. The unemployment rate has been little changed at around 5½ per cent for much of the past year. The various forward-looking indicators continue to point to solid growth in employment in the period ahead, with a gradual reduction in the unemployment rate expected. Wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation is low and is likely to remain so for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

The Australian dollar remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

The housing markets in Sydney and Melbourne have slowed. Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. Housing credit growth has slowed over the past year, especially to investors. APRA's supervisory measures and tighter credit standards have been helpful in containing the build-up of risk in household balance sheets, although the level of household debt remains high. While there may be some further tightening of lending standards, the average mortgage interest rate on outstanding loans is continuing to decline.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

Rebound in 10 year yield lifts USDJPY

Dollar trades broadly higher in Asian session as the rebound extends. Meanwhile, Australian Dollar is losing some some steam just ahead of RBA rate decision and statement.

Dollar is supported by the rebound in treasury yield. 10 year yield closed higher by 0.042 overnight at 2.937. As noted in our weekly report, TNX should have stabilized after climax decline to 2.759. And the range for consolidation is set between 2.7 and 3.1. Current rebound would likely extend through 3.0 handle. But it may start to feel heavy approaching 3.115 high.

The rebound in TNX lifted USD/JPY with 109.86 minor resistance breached. The development argues that pull back from 111.39 has completed at 108.10 already. And further rise is in favor to retest 111.39. But a break there is unlikely for the moment unless TNX makes a decisive move through 3.115 too.

NZ Treasury: Q1 growth may fall short of 0.7% forecast

In the Monthly Economic Indicator report published today, New Zealand Treasury noted that the tracking of March quarter data suggested real GDP growth may fall short of 0.7% as forecast in the Budget Economic and Fiscal Update (BEFU) 2018. Nonetheless, June quarter activity indicators have been "a little more positive". Subdued wage pressures are likely contributing to low inflation, and the expectation that RBNZ will keep OCR at 1.75% "for some time to come".

Risks are skewed to the downside as led by international developments. In particular, the Treasury noted slowdown in Japan, Eurozone and UK in Q1. And it warned that political instability in Italy will drag Eurozone growth further. Nonetheless, the outlook for China and the US "remains relatively positive".

Full report here.