Sample Category Title

German Merkel: We’ll have smart, determined and jointly agreed response to US steel tariffs

German Chancellor Angela Merkel said today in Lisbon that European Union will give a "smart, determined and jointly agreed" response to the US is Trump decides to impose steel and aluminum tariffs on them.

She noted "we don't know the decision yet but if tariffs were to be imposed, then we have a clear stance within the European Union." And she added "we are convinced that these tariffs are not in line with WTO rules."

The temporary exemption of US steel and aluminum tariffs will expire tomorrow. It's widely reported that US will decide to start imposing tariffs on Mexico, Canada and the EU. And the decision would be announced today.

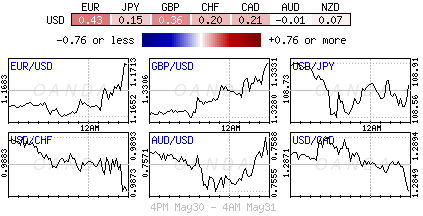

As Risk Sentiment Improves Dollar Bulls Sell

Thursday May 31: Five things the markets are talking about

Global equities are currently receiving some investor appreciation, rebounding from a two-month trough along with the EUR as the political turmoil in Italy that shook financial markets this week shows signs of easing. The ‘big' dollar has edged lower while Italian bond yields have declined again.

Meanwhile in Madrid, parliament is set to vote Friday (June 1) whether to oust Spanish PM Rajoy and replace his center-right government with one led by the center-left Socialist Party after a Spanish court ruled that Mr. Rajoy's Popular Party financially benefited from an illegal kickback scheme.

Stateside, a senior N. Korean official is in New York this week to discuss the upcoming summit, proof that the latest indication that an ‘on-again-off-again' meeting between Trump and Kim Jong-Un may go ahead on June 12 in Singapore.

Amid all this political and trade turbulence, the next focus for investors is tomorrow's non-farm payroll (NFP) report (08:30 am EDT), the last one before the Fed meets next month, when it's expected to hike interest rates.

1. Stocks find support

In Japan, the Nikkei share average overnight bounced back from a six-week low as worries over Italy's political crisis receded. The Nikkei rose +0.83%, while the broader Topix rallied +0.65%.

Down-under, Aussie shares rebounded, led by materials stocks to close higher on Thursday, but health stocks were under pressure, hit by Trump's talk of “voluntary massive drops” in drug prices. The S&P/ASX 200 index rose +0.5%. In S. Korea, the Kospi added +0.5%.

In Hong Kong, stocks rallied, aided by strong China manufacturing data. The Hang Seng index rose +1.4%, while the China Enterprises Index gained +1.8%.

Note: Data overnight showed that China's manufacturing sector grew at the fastest pace in eight-months in May (51.9 vs. 51.4e), beating expectations and easing concerns about an economic slowdown even as risks from trade tensions with the U.S and a crackdown on debt point to pressures.

In China, stronger data supported stocks. The blue-chip CSI300 index rose +2.2%, while the Shanghai Composite Index rose +1.8%.

In Europe, regional indices trade mostly higher led by the Italian FTSE MIB, with developments on the Italian political front continuing to be in focus.

U.S stocks are set to open in the ‘black' (+0.1%).

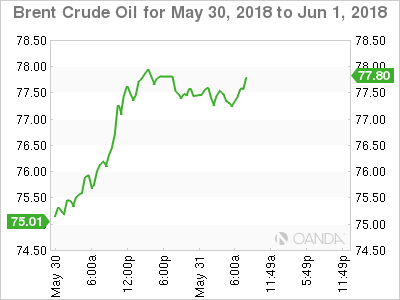

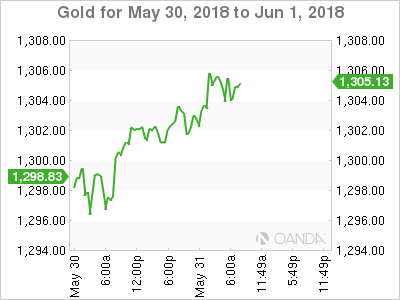

2. Oil prices ease, eyes on OPEC supply, gold higher

Oil prices have eased slightly overnight following a rally yesterday, as investors eyed a surprise increase in U.S crude oil inventories and looked to a possible rise in output when OPEC and other producers meet on June 22.

Brent crude is down -38c, or -0.5%, at +$77.12 per barrel, after settling yesterday's session up +2.8%. U.S West Texas Intermediate crude is down -20c, or -0.3%, at +$68.01 a barrel. In the previous session, it settled up +2.2%, at +$68.21 per barrel.

Note: Global inventories have been broadly falling, but U.S crude stockpiles again rallied +1m barrels in the week to May 25 to +434.9m barrels.

Expect the market to take its cue from today's EIA report (10:00 am EDT) – a day later than usual due to a U.S. public holiday on Monday.

Ahead of the U.S open, gold prices are a tad better bid, as the dollar eased from seven-month highs hit earlier this week, with prices further supported by concerns over Sino/U.S trade. Spot gold has rallied +0.4% to +$1,305.87 per ounce, but is down -0.7% for the month. U.S gold futures for June delivery are +0.3% higher at +$1,305.80 per ounce.

3. Bank of Canada a tad ‘hawkish'

Despite holding their overnight lending rate steady at +1.25%, yesterday's Bank of Canada (BoC) rate announcement sent strong signals that another rate increase is imminent. The BoC sounded upbeat and tweaked some of the language it used to describe its approach to rate rises. While the BoC had earlier said it would remain “cautious” about future rate changes, that word did not appear in yesterday's statement. The bank also dropped the words “over time” from a sentence saying higher rates would be warranted, which could suggest that Canadian policy makers are on course for a move at the next meeting.

Elsewhere, the yield on U.S 10-year Treasuries increased +1 bps to +2.86%. In Germany, the 10-year Bund yield fell less than -1 bps to +0.37%, while in the U.K, the 10-year Gilt yield climbed +1 bps to +1.257%. The Italian 10-year yield continues to move away from its recent multi-year high (+3.40%) to test below +2.60%.

4. As risk sentiment improves dollar bulls sell

The continued improvement in risk sentiment is weighing upon the ‘mighty' dollar; the ‘bears' are out in force, the more aggressive selling at market, while the weaker is still looking for upticks to participate.

The EUR/USD (€1.1700) continues its rebound from its recent 10-month low print earlier this week (€1.1506). In the Euro session, some investors have decided to book some profit on their EUR positions with Italian political uncertainties looming in the background and after May's eurozone inflation data came in stronger than expected at +1.9% y/y vs. a forecasted +1.6% rise.

Note: A strong inflation would have otherwise been positive for the common currency if it weren't for Italy, as the ECB would have likely been more willing to show signs of soon exiting their QE program.

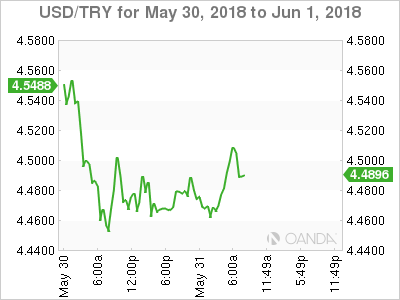

In EM, USD/TRY is trading below $4.50 – a key psychological level. Does this imply that last week's CBRT interest rate hike is a success?

The market's confidence in a sufficiently restrictive monetary policy is crucial for the currency's recovery, and the CBRT must prove this at its meeting on 7 June.

Dollar ‘bulls' will forgot monetary policy, the key to the lira's direction will depend on Turkey's presidential election – what will monetary policy be like after? President Erdogan and his strange monetary policy ideas continue to be the biggest risk factor for the lira. USD/TRY is last up +0.3% at $4.49.

5. U.K consumer credit rebounds, Euro inflation improves

Data this morning shows that the amount that U.K citizens borrowed strongly rebounded last month, after dipping in March.

The amount that U.K consumers borrowed in April jumped to +£1.8B after falling to +£400M in March, which was the lowest in more than five-years. The increase was driven by both credit-card spending and loan uptakes.

Note: The stronger report may strengthen the Bank of England's (BoE) case for raising its key interest rate sooner rather than later – market consensus was expecting the BoE to hike this month. That sentiment, has not disappeared, its just shifted to August, assuming upcoming data remains strong.

Digging deeper, mortgage lending edged lower on the month to +£3.9B from +£4.0B in March, but remained above the average of the past year.

Other data shows that European inflation continues to improve – France, Italy and Eurozone all improved from month-ago levels and above market expectations.

DAX Under Pressure Despite Strong Eurozone Inflation

The DAX has reversed directions on Wednesday and headed lower. Currently, the DAX is at 12,717, down 0.52% on the day. In economic news, Eurozone CPI Flash Estimate jumped 1.9%, above the estimate of 1.6%. Core CPI Flash Estimate improved to 1.1%, above the estimate of 1.0%. On Friday, Germany and the eurozone release manufacturing PMIs.

It's been a rough road for the DAX this week, which is down 2.2 percent. European stock markets are seeing red in response to the continuing political drama in Italy, as efforts continue to form a government. The two largest parties, the League Nord and the Five Star Movement proposed a eurosceptic finance minister, but this was blocked by the pro-European Matterella. This triggered a political crisis which led to a selloff of Italian stocks and bonds. The prime minister-elect, Giuseppe Conte, then announced that he had withdrawn his mandate to form a government, and Mattarella invited Carlo Cottarelli, a former IMF economist, to form a temporary technocrat government. There was talk of an election in the fall or even earlier, but Mattarella has agreed to let the two parties have a second go at forming a coalition government.

German numbers showed some weakness in the first quarter, but there was positive news on Wednesday. Retail sales were unexpectedly strong in April, with a sharp gain of 2.3%. This reading ended a nasty streak of four declines. The gain is the strongest since December, and raises hopes that second quarter growth will rebound after a sluggish first quarter. Inflation is also expected to improve, with German Preliminary CPI forecast to rise to 0.3% in May after a flat reading of 0.0% in April. On the inflation front, Eurostat is projecting a surge this month, with CPI Flash Estimate rising to 1.9%, its highest level since April 2017. Core CPI Flash Estimate improved to 1.1%, marking an 8-month high. Inflation levels are being closely watched by the ECB, which is scheduled to wind up its stimulus program in September. The ECB reduced its stimulus in January, from EUR 60 billion to 30 billion each month. Still, inflation remains well below the ECB target of around 2 percent.

Euro Edges Higher On Strong Eurozone CPI

EUR/USD has recorded gains in the Thursday session, continuing the upward movement seen on Wednesday. Currently, the pair is trading at 1.1682, up 0.17% on the day. On the release front, Eurozone CPI Flash Estimate jumped 1.9%, above the estimate of 1.6%. Core CPI Flash Estimate improved to 1.1%, above the estimate of 1.0%. In the US, little change is consumer inflation and spending indicators are expected to remain steady. Core PCI Price Index is forecast to gain 0.1%, and the estimate for Personal Spending is 0.4%. As well, unemployment claims are forecast to drop to 228 thousand. On Friday, Germany and the eurozone release manufacturing PMIs. In the U.S, the focus will be on job numbers, with the release of nonfarm payrolls and wage growth.

With Italy gripped in political turmoil, President Sergio Mattarella is looking for a way to avoid new elections, after an inconclusive election in March. The two largest parties, the League Nord and the Five Star Movement proposed a eurosceptic finance minister, but this was blocked by the pro-European Matterella. This triggered a political crisis which led to a selloff of Italian stocks and bonds. The prime minister-elect, Giuseppe Conte, then announced that he had withdrawn his mandate to form a government, and Mattarella invited Carlo Cottarelli, a former IMF economist, to form a temporary technocrat government. There was talk of an election in the fall or even earlier, but Mattarella has agreed to let the two parties again try and form a coalition government.

Eurozone inflation indicators flexed some muscle in May, boosting the euro on Wednesday. Eurostat is projecting a surge this month, with CPI Flash Estimate rising to 1.9%, its highest level since April 2017. Core CPI Flash Estimate improved to 1.1%, marking an 8-month high. Inflation levels are being closely watched by the ECB, which is scheduled to wind up its stimulus program in September. The ECB reduced its stimulus in January, from EUR 60 billion to 30 billion each month. Still, inflation remains well below the ECB target of around 2 percent.

German retail sales were unexpectedly strong in April, with a sharp gain of 2.3%. This reading ended a nasty streak of four declines. The gain is the strongest since December and raises hopes that second quarter growth will rebound after a sluggish first quarter. Inflation is also expected to improve, with German Preliminary CPI forecast to rise to 0.3% in May after a flat reading of 0.0% in April. The story in France, the second largest economy in the eurozone, was not as bright. Consumer spending plunged 1.5% in April, marking a 3-month low. Preliminary GDP fell to 0.2% in March, down from 0.6% a month earlier.

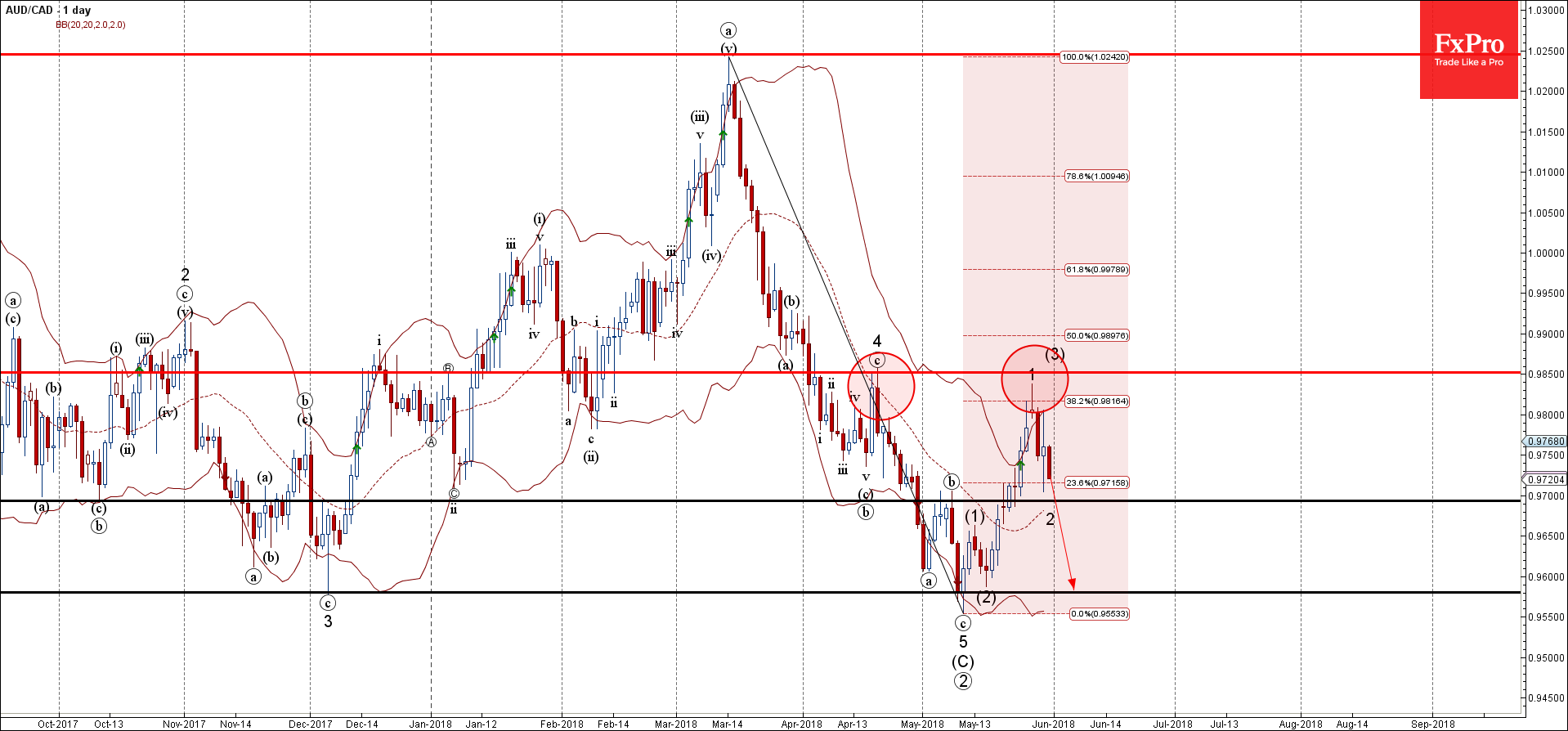

Forex Analysis: AUDCAD Wave Analysis

AUD/CAD falling inside minor correction 2

Further losses are likely

AUD/CAD recently reversed down from the resistance zone lying between the resistance level 0.9850 (top of the previous correction 4), upper daily Bollinger Band and the 38.2% Fibonacci retracement of the previous downward impulse C rom March.

The downward reversal from this resistance zone created the daily Japanese candlesticks reversal pattern Evening Star – which started the active minor correction 2.

AUD/CAD is likely to continue to fall toward the next support level 0.9700 (former resistance from the start of May) – the breakout of which can lead to further losses toward the key support at 0.9580.

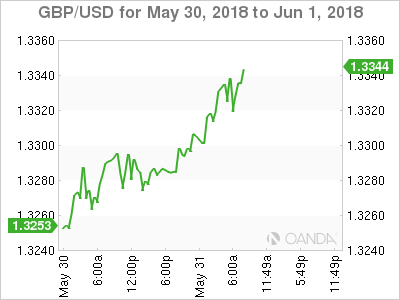

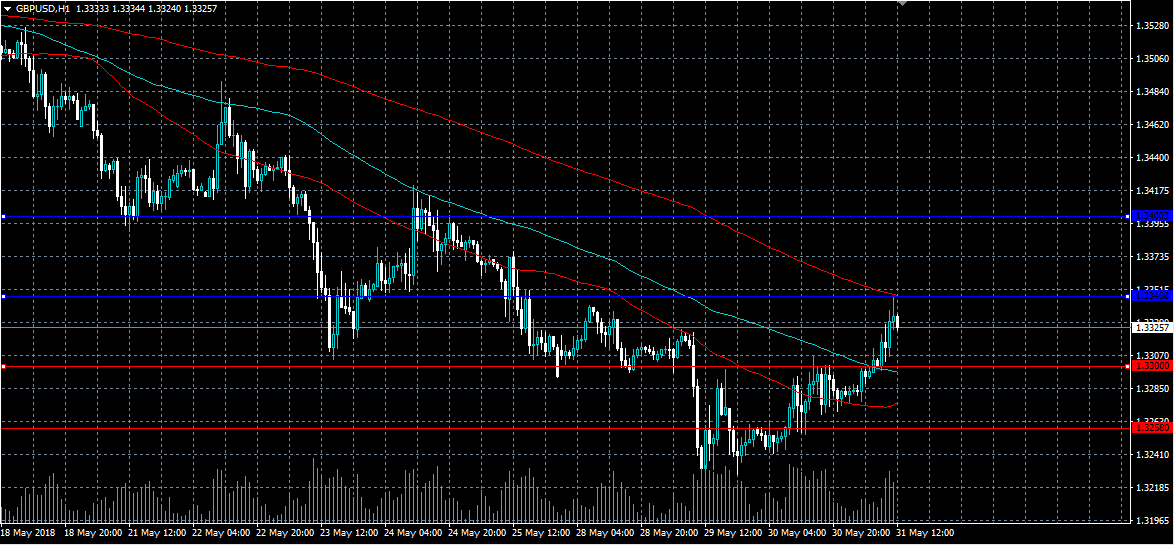

GBPUSD Intraday Bullish Above 1.3300

The British pound has moved well above the 1.3300 level against the US dollar, over positive developments coming from the Italian economy and general weakness in the greenback. The GBPUSD pair currently trades around the 1.3320 level, and has so far found interim technical resistance from the 1.3346 level. Sterling traders now await key PMI data from the United Kingdom economy and the release of the U.S. Non-farm payrolls job report.

The GBPUSD pair is intraday bullish while trading above the 1.3300 level, key intraday resistance is located at the 1.3347 and 1.3400 levels.

If the GBPUSD pair moves below the 1.3300 level, we may see a technical correction back towards the 1.3258 and 1.3240 levels

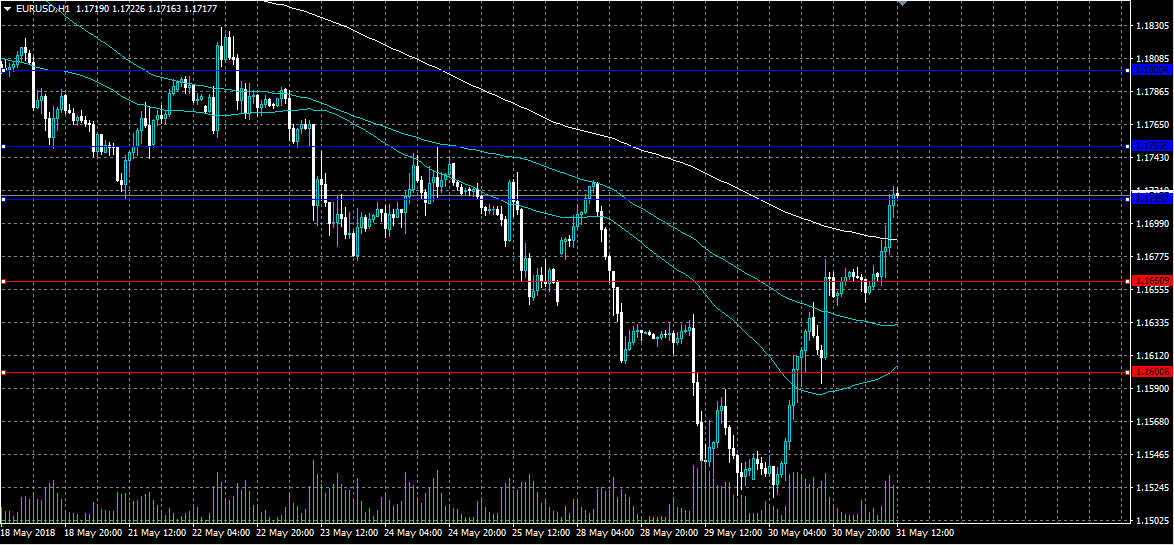

EURUSD Weekly Bullish Above 1.1715 Level

The euro continues to correct higher against the US dollar, as Italy’s two leading anti-establishment parties hope to enter into coalition talks to settle the current crisis on Italian politics. The EURUSD pair has surged higher on the news, with price now trading well-above the 1.1700 level, marking a dramatic weekly turn-around for the single currency. Bullish momentum in the EURUSD pair is likely to strengthen while price holds above the key 1.1715 technical level.

The EURUSD pair is strongly intraday bullish while trading above the 1.1715 level. Key resistance is now located at the 1.1750 and 1.1800 levels.

If the EURUSD pair moves below the 1.1700 level, we may see sellers push price towards the 1.1660 and 1.1600 level.

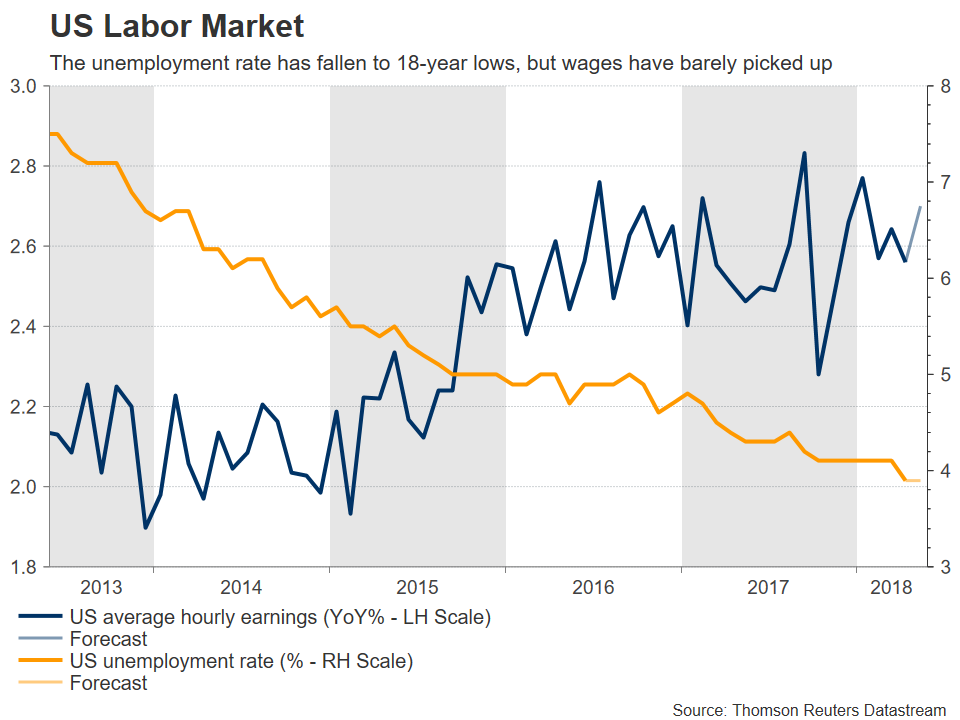

US Employment Report To Give Markets A Break From Politics

After trading almost solely on politics over the past few days, financial markets will probably turn their gaze back to economics on Friday, when the US releases its employment data at 1230 GMT. Forecasts point to a solid report overall, which could cement market expectations for a June hike – that has come under some doubt lately – and perhaps help the dollar extend its winning streak.

The US labor market is expected to have printed another decent month in May. Nonfarm payrolls (NFP) are forecast to have risen 188k, more than April’s mildly disappointing 164k, and a print consistent with further tightening in the jobs market. The unemployment rate is projected to have held steady at April’s 18-year low of 3.9%, while average hourly earnings are expected to have picked up some speed. In yearly terms, wages are anticipated to have clocked in at 2.7%, from 2.6% in April, and on a monthly basis the print is expected to have risen by 0.2%, up from 0.1% previously.

Similar to recent employment reports, the lion’s share of attention will probably fall on earnings. While payrolls and the unemployment rate are of course extremely important, a strong set of numbers on those fronts would simply confirm what markets and policymakers already know; that jobs growth remains robust. Conversely, wage growth is the missing piece of the puzzle for the Fed; it has long been expected to pick up drastically as the labor market continued to tighten and workers found it easier to demand a pay increase, but it has accelerated only slightly. Remember that higher wages are considered a precursor to higher inflation down the road, so the Fed keeps a very close eye on them. In this light, stronger-than-expected earnings figures could stoke speculation for a more aggressive rate-hike path by the central bank, which would likely be positive for the dollar, and vice versa.

Looking at market pricing, investors have recently become much more skeptical regarding how many hikes the Fed will deliver this year. Whereas just a few weeks ago markets had fully priced two more 25bps rate hikes by the Fed and also saw a 20% probability for a third one, now that pricing has slipped materially; only one 25bps rate hike is fully factored in, and the Fed funds futures imply an 85% likelihood for a second one. Thus, although the debate until lately was whether the Fed would deliver two or three additional hikes this year, now even the prospect of two more has come under some doubt. Correspondingly, the probability for a rate increase at the June meeting has slipped to 82%, from nearly 100% previously.

Turning to gauges of the labor market, initial jobless claims remained quite low for most of May, supporting the case for a strong NFP number. Something similar was signaled by the Markit preliminary Composite PMI, which showed that “a solid rate of employment growth was maintained across the private sector in May”. The ISM surveys – which markets typically pay more attention to – haven’t been released yet. Meanwhile, the private ADP employment report that is traditionally considered a tracker of the official NFP print also came in at a solid 178k, though it should be noted that the correlation between the two figures has not been that strong lately.

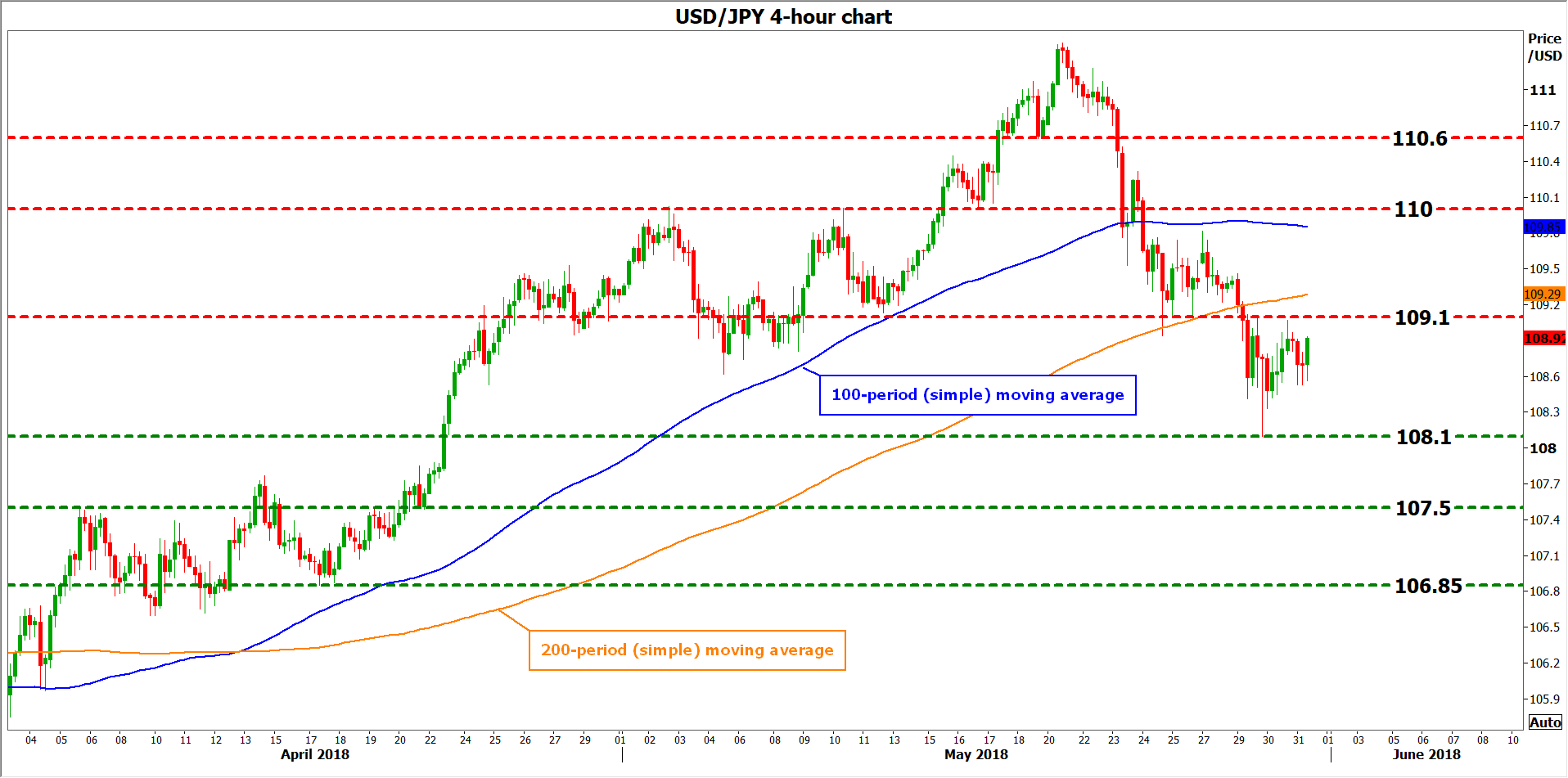

In case these data come in above expectations, particularly on the earnings front, then the dollar could extend its recent gains as investors become more confident in the Fed delivering at least two more rate increases this year. Looking at dollar/yen, immediate resistance to advances could come near 109.10, the low of May 11. An upside break of that zone could aim for the round figure of 110.00, marked by the highs of May 2 and 10. Even higher, attention would shift to the 110.60 line, defined by the low of May 18.

On the downside, and in case a disappointment in these figures casts further doubt on how many hikes the Fed will deliver, support to declines may come at 108.10, the trough of May 29. If the bears manage to break below it, focus would increasingly turn to the 107.50 barrier, identified by the peaks of April 5. Lower still, buy orders may be found around 106.85, the bottom of April 17.

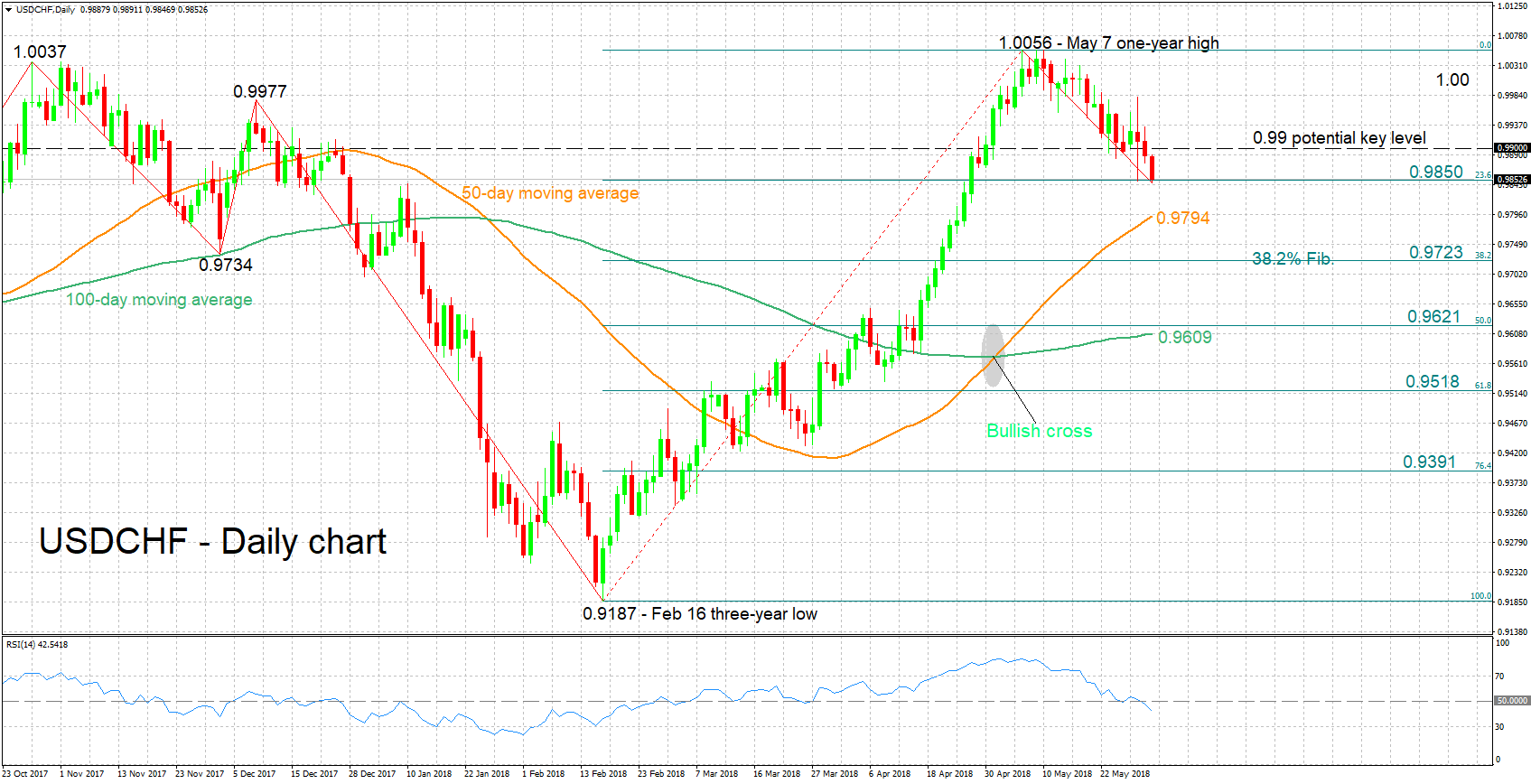

USDCHF Hits One-Month Low, Medium-Term Outlook Still Positive

USDCHF has lost 2% of its value after reaching a one-year high of 1.0056 in early May. Earlier on Thursday, the pair touched a one-month low of 0.9847.

The RSI continues to fall, having crossed below the 50 neutral-perceived level. This is indicative of the bearish short-term bias that is in place.

The region around the 23.6% Fibonacci retracement level of the February 16 to May 7 upleg at 0.9850 seems to be providing immediate support; this mark was violated earlier in the day, but the price subsequently moved back above it. Steeper losses might meet additional support around the current level of the 50-day moving average at 0.9794 – including the 0.98 round figure – and the 38.2% Fibonacci mark at 0.9723.

On the upside, resistance may come around the 0.99 handle which may be of psychological importance. The 1.00-parity level would be eyed next in case of stronger bullish movement, with May 7’s one-year high of 1.0056 lying not far above.

In terms of the medium-term outlook, it continues to look mostly positive with price action still taking place above both the 50- and 100-day MA lines – a bullish (golden) cross was also recorded in early May when the 50-day MA moved above the 100-day one. However, the declines from recent weeks have brought the price not far above the 100-day MA. A drop below this level would set a more neutral picture in the medium-term.

Overall, the short-term outlook is looking bearish and the medium-term outlook appears predominantly bullish.

EUR Better Bid As Tensions Ease

Italian political situation improves as negotiations may restart

Financial markets continued to benefit from easing political tensions in Italy after Luigi Di Maio, leader of the 5-Star Movement, said he was ready to go back on his decision to pick economist Paolo Savona for finance minister. Nevertheless, he will stick to Giuseppe Conte for prime minister. The single currency extended gains on Thursday and rose 0.45% to 1.1715 this morning (up 1.75% from yesterday low 1.1519). Italian equities were also better bid with the FTSE MIB rising 0.85% to 21,980 points. Italian sovereign bonds also found a stronger demand: the 2-year yield fell to 1%, compared to 2.8% two days ago, while the 10-year one eased to 2.68%, compared to 3.43%.

After climbing 0.90% yesterday, EUR/CHF rose another 0.25% this morning to 1.1565 amid improving global risk sentiment. The US dollar also paid the cost of improving mood across financial markets. The dollar index extended losses on Thursday morning and hit 93.73.

The immediate future is uncertain now as it is still unclear whether Matteo Salvini, leader of the League, will go back to the negotiation table and form a new government. Indeed, on Wednesday, he called for snap elections and claimed that he did everything he could to help resolve this political impasse but it was never enough for President Mattarella.

However, Mattarella announced yesterday he would give more time to the League and 5-star to form a government and avoid snap election. This is the wiser solution for the President as fresh elections would most likely be beneficial to the two populist parties and would generate more uncertainty regarding Italy’s future. Luigi Di Maio said that in case of no agreement between President Mattarella, the league and 5-stars, he would go for snap elections, which could potentially take place early July.

Strong US, weaker USD

While the market focused on Italy, the US released some interesting data yesterday. ADP for May reported a marginally weaker result than expected 178k verse 190k exp. The BEA dropped Q1 real GDP to 2.2% q/q against 2.3% exp from previously reported 2.3% q/q. Personal consumption expenditure (PCE) was reduced 1.0%, confirming 1Q economic weakness. Despite the softer read, we anticipate a healthy recovery in 2Q as consumer fundamentals were solid. As stated by the ADP release the US labor markets, the bedrock for optimism in household, continue to produce. In addition, overall, economic momentums remain intact and accommodative financial conditions and friendly fiscal policy will support outlook. Core PCE inflation for Q1 revised lower to annualized 1.6% from 1.7% in Q1. The slight reduce will lower Fed rate expectation, allowing risk asset to improve. Finally, Fed Beige Book for the 12-13 FOMC meeting indicate few changes in the momentum of growth outlook. There was a bit of natural softening in consumer activity but nothing that would shift expectations. With outlook for employment and wage growth expected to remain strong but not to accelerate we should see weaker USD on macro backdrop improvements.