Sample Category Title

Market Morning Briefing: Dollar Index Tested The 13 Day Moving Average Near 93.7-93.8

STOCKS

Dow (24415.84, -1.02%) gave back all gains seen yesterday. Unless a break above 25000 is seen, it would be difficult to project bullishness for the Dow for the medium term. While 25000 resistance holds, Dow could be pushed down towards 24000 again and again. Failure to move up immediately and break above 25000 could turn to be consolidative for the Dow next week.

Dax (12604.89, -1.40%) has come down sharply and has scope of testing 12470/60 in the near term. From there we could see a bounce back towards 12600 or higher.

Nikkei (22281.54, +0.36%) has bounced back from 22000 levels seen a couple of days ago. While the rise continues, it could test 22500 in the coming sessions. Near term looks bullish which could pull up Dollar Yen (109.18) also towards 110..

Shanghai (3100.31, +0.16%) continues to trade at higher levels. It could again move up towards 3150 before coming off from there. Overall some more movement in the 3050-3150 region could be possible in the near to medium term.

Nifty (10736.15, +1.15%) moved up sharply yesterday and indicates that the bears are not strong just now, reducing possibility of a sharp fall just now. Some ranged movement within 10850-10400 is possible for some more time before the index decides on further movement. For now, there could be some dip seen today followed by a pickup in the upward rally again by next week. Immediate upside is likely to be limited at 10850-10900 region.

COMMODITIES

Brent (77.51) is slightly up from levels seen yesterday while WTI (66.94) has come off sharply from 68.10 seen in yesterday’s edition. WTI has immediate support near 66 which if holds could push the prices upwards while Brent is stable just now and could see some ranged movement in the 77-79 region for some time.

Gold (1298.32) seems to have bounced a bit from the long term support on the 3-day charts. While that holds, Gold may move up eventually towards 1310-1315 in the coming sessions limiting the downside at 1280.

Copper (3.0616) is almost stable near current levels. While above 3.02, Copper could rise towards 3.20 in the medium term.

FOREX

Dollar index (94.031) tested the 13 day moving average near 93.7-93.8 yesterday and could move lower next week to test the 21 days MA near 93.50. If it breaks 93.5, the Dollar Index might turn bearish for the medium term. However, while above 93.5, it could again rise to test levels near 95. On the 3 day line chart, 96 is seen as a possible resistance level, which might be the maximum upside the Dollar Index sees in the medium term.

Euro (1.1693): As per our expectation, Euro tested the 13 days MA by seeing a high near 1.1724 and has dipped slightly from there. Next week, we could see Euro rising towards the 21 days MA near 1.178, which would be a crucial resistance level. Repeating yesterday’s comment: A rise past 1.182 could make Euro bullish for the medium term. While below 1.179-1.182, Euro could again dip to test levels near 1.15. On the 3 day line chart, 1.135-1.140 is seen as possible support, which could be the maximum medium term downside that the Euro could see. A break of 1.135-1.140 (less preferred currently) would open up possibility of 1.12.

Dollar Yen (109.08) : has stayed above the 21 weeks MA near 108.16 like we have been expecting and seems to be rising for a possible retest of levels near 110-111 next week. However, at the same time, we have to be mindful that the Bank of Japan has announced some tapering of asset purchases, which could well prove to be the trigger that strengthens the Yen in the days to come. On the downside, a break of 107.8 would confirm medium term bearishness for Dollar Yen and could result in a quick downmove to 106-105 (seen as crucial support on weekly candles).

Euro Yen (127.53) : As per expectation, Euro Yen is trading at levels near 127.6 and is thereby respecting support trendline in the downward channel on weekly candles. Although the Dollar Yen looks like it could rise towards 110 next week, the Bank of Japan’s tapering of asset purchases could bring in Yen strength quickly, in which case, we could see Euro Yen moving down towards support on weekly candles once again (near 124). A retest of 1.16 by the Euro and a fall to 107 on the Dollar Yen will make the Euro Yen test levels near 124.

Pound (1.3277): Pound has continued to trade near levels seen yesterday ie around 1.33. Thereby, it is no more respecting resistance in the downward channel on daily candles. However, it still does look bearish towards 1.32 in the near term. We have been expecting it to gradually move lower over the next 1-2 weeks with the next downside target being near 1.30 (support on weekly candles). A break of 1.30 could imply continued bearishness in the medium term.

Dollar Rupee (67.40) : Dollar Rupee is likely to test 67.90 today. But overall broad sideways movement could continue.

INTEREST RATES

Our May '18 US Treasury report ( available on demand ) forecasts a near term dip in US yields towards medium term supports near 2.55% (10 Year), 2.9% (30 Year) and 2.2% (5 Year). It would have to be seen if the trigger for such a dip could be some dovishness from the US Fed in its June meeting.

Current yields: US 10 Year (2.873%), 30 Year (3.03%), 5 Year (2.71%), 2 Year (2.435%) – US Yields are trading near levels seen yesterday. Repeating yesterday’s comment on the 10 Year yield:

The US 10 year yield might have some horizontal support near 2.75% which is holding for the time being. However, given the earlier break of crucial support trendline near 2.85%, we could see a gradual downmove towards medium term support near 2.55%. Another dip in Brent towards 73-71 might be the trigger for this fall to 2.55%. If that doesn’t happen, the break of 2.85% would have been a false break.

The Bank of Japan has cut the size of its asset purchase programme by 20bn yen, which has led to a rise in Japanese yields. Whether this translates into a rise in yields of other countries is yet to be seen. The Japanese 10 Year bond yield has moved up from 0.03% to 0.046%. It could now move even higher to 0.06% (previous high seen in May).

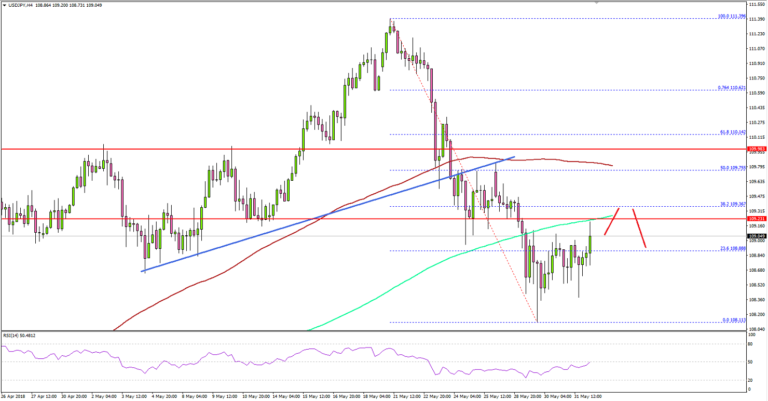

USD/JPY Facing Uphill Task Ahead Of US NFP

Key Highlights

- The US Dollar found support near the 108.10 level and recovered slightly against the Japanese Yen.

- On the upside, there is a strong resistance near 109.75 and the 100 simple moving average (4-hour).

- The US Initial Jobless Claims in the week ending May 26, 2018 declined from 234K to 221K.

- Today in the US, the NFP figure for May 2018 will be released, which is forecasted to post 188K.

USDJPY Technical Analysis

The US Dollar formed a decent support base near the 108.20 level against the Japanese Yen. The USD/JPY started an upside recovery, but the pair is facing many hurdles on the upside near 109.25 and 109.75.

Looking at the 4-hours chart, there was a downside break below a bullish trend line and the pair settled below the 100 (red) and 200 (green) simple moving average (4-hour) and 109.00. Later, it found buyers around 108.20 and staged a comeback.

The pair traded above the 108.50 resistance, but there are many key resistances on the upside. First, the 200 SMA is near the 109.25-30 zone, which was a support earlier. Above 109.30, the 50% Fib retracement level of the last drop from the 111.39 high to 108.11 low is at 109.75.

More importantly, the 100 SMA is positioned above the 109.75 level to prevent gains. Therefore, if the pair continues to move higher, it could face a strong barrier near 109.75 and the 100 SMA.

On the downside, the 108.10-20 zone is a strong support. A break below this may perhaps open the doors for more losses towards 107.50.

Recently in the US, the Initial Jobless Claims figure for the week ending May 26, 2018 was released by the US Department of Labor. The market was looking for a decline from the last reading of 234K to 228K.

However, the actual result was better as there was a decline in claims to 221K. The report added:

The advance number for seasonally adjusted insured unemployment during the week ending May 19 was 1,726,000, a decrease of 16,000 from the previous week’s revised level.

Today, the US NFP report for May 2018 could impact the market sentiment. Pairs such as EUR/USD and GBP/USD may perhaps recover higher if the outcome disappoints. Alternatively, the US Dollar is likely to resume uptrend if the result beats the forecast.

Economic Releases to Watch Today

- Germany’s Manufacturing PMI for May 2018 – Forecast 56.8, versus 56.8 previous.

- Euro Zone Manufacturing PMI May 2018 – Forecast 55.5, versus 55.5 previous.

- UK Manufacturing PMI for May 2018 – Forecast 53.5, versus 53.9 previous.

- US nonfarm payrolls May 2018 – Forecast 188K, versus 164K previous.

- US Unemployment Rate May 2018 – Forecast 3.9%, versus 3.9% previous.

- US Manufacturing PMI for May 2018 – Forecast 56.6, versus 56.6 previous.

A Tempest In An Espresso Cup

A tempest in an espresso cup

The markets are looking much more constructive to end the week than they did to start, and with trade wars still lingering, that is saying a lot. Mind you, the Italian rumpus, and ensuing blow-off was incredibly intense so investors will be keen to put politics on the back burner, at least for the next 12 hours, and give their undivided attention to the US Non-Farm Payrolls release later tonight.

While the impressive rebound in Eurozone inflation and with Italy well on the way to forging a new government, the appeal of trading EUR from the long side is undoubtedly tempting. But looking at the bewildering cocktail of risk, which has traders going cross-eyed, every minute to two, does paint a different picture. The risk-reward ahead of tonight's AHE, which is bound to be a significant US dollar sentiment shifter, has traders more guarded than usual.

But let's see what Asia brings to the table after New York put in an epic session which began with an intense focus on trade wars only to go one better on Italy.

And despite all the doom and gloom prophesies, the Italian political mind-bender ended up being little more than a tempest in an espresso cup!

Oil markets

Despite the EIA reporting a larger than expected inventory draw, there doesn't appear to be a great deal of interest in pursuing the market higher given that no one wants to be caught long and wrong if OPEC does boost output significantly. Not to mention, the market is confused by OPEC crosscurrents as not all members are in favour of raising production. But frankly, there is nothing more unappealing than trading oil amid OPEC rumours and innuendos which has sidelined a lot of spot oil traders.

But more focus is being centred on WTI -BCO spread as WTI bulls are a bit concerned by both the lack of significant draws in Cushing along with pipeline bottlenecks which are compounded by ports unable to handle the large 2 million-barrel supertankers. So, despite the bountiful bounty, bottlenecks befuddle.

Gold markets

The conciliatory political tone in Italy has slightly tarnished Gold's appeal as the eurozone geopolitical risk premium deflates. But with more than enough geopolitical risk premium to go around, it's highly unlikely gold prices will wonder to far south. Spina will likely see a new PM, Trump-Kim remains a significant work in progress while risk is little more than a tariff and trade headline from falling off the cliff.

Asia Markets

The bright China PMI prints provided some local relief from Italy, but with US equity markets turning sour as trade war reignite, the regions very tight correlation to risk sentiment suggests the market will spend the better part of today's session backpedalling.

There was an encouraging relief rally on the Malaysian bond market yesterday that helped the beleaguered Ringgit halt its recent losing streak. But it came off local demand with barely a trickle of the foreign interest. And given that the MYR is trading very sensitive to global risk sentiment, we should expect USDMYR dips to be supported at least during the Asia session.

While Traders are mindful of the government's pledge to meet deficit targets, it will come down to the proof is in the pudding as far as foreign interest is concerned as actions will speak louder than words.

Dollar Falls As US Fires First In Trade War

The US dollar is lower against most major pairs on Thursday. The United States announced earlier in the day that it would apply tariffs on steel and aluminium imports form EU, Canada and Mexico. The NAFTA pairs depreciated as a wave or retaliatory moves are expected. US Trade Secretary Wilbur Ross said the tariffs are the result of unproductive negotiations on broader trade deals. While this is the first shot in a trade war there is still hope that during the G7 meetings this issue is ironed out with a more positive outcome benefiting the global economy. The Italian political crisis was averted as the coalition got the approval of the Italian President, with a new government to be sworn in the next 24 hours. Up next will be the release of the biggest indicator in the markets the U.S. non farm payrolls (NFP) on Friday, June 1 at 8:30 am EDT.

- NFP Report expected to show a gain of 189,000 jobs in US

- US Wages forecasted to rise 0.3 percent

- Unemployment rate in US to remain at 3.9 percent

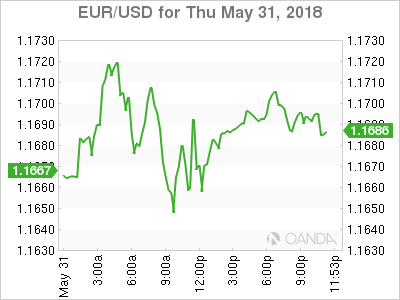

EUR Higher as Italian Crisis Ends but Trade War Begins

The EUR/USD gained 0.25 percent on Thursday. The single currency is trading at 1.1690 after getting a boost from the end of a short lived but impactful crisis in Italy. The coalition between the 5 Star movement and the League was momentarily derailed with a new round of elections a possibility. Both parties tweaked their list of ministers and this time it was approved by Italian President Sergio Mattarella.

European inflation surprised to the upside with the CPI flash estimate up 1.9 percent on a 1.6 percent forecast and the core CPI (food, energy, alcohol, and tobacco) up 1.1 percent. The rise in the cost of living will put some pressure on the European Central Bank (ECB) to give further details on its monetary policy plans after its QE program ends in September. The Italian near crisis reminded everyone of the high levels of debt in the country and the last thing needed at this point is higher rates, but inflation might be pushing the ECB towards that path.

The president of the European commission, Jean-Claude Juncker announced that retaliation to US products will be in effect if the US moves forward with the 25% duty on steel and a 10% duty on aluminium. The tariffs were announced two months ago, but US allies were excluded, but given he slow progress of the trade conversation with the EU, Canada and Mexico that exemption has been lifted.

While trade war headlines will splash across financial news sites the market will be anticipating the release of the U.S. non farm payrolls (NFP). The employment component has been the strongest pillar of the US comic recovery. The current unemployment rate is the lowest since the year 2000 and wages are starting to grow after stagnating after the recession.

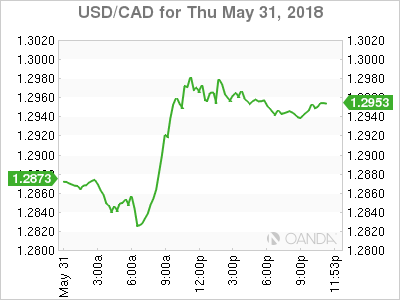

Loonie Lower as Canada to Retaliate Against US Tariffs

The USD/CAD gained 0.72 percent in the last 24 hours. The currency pair is trading at 1.2966 after the exception for Canadian steel and aluminium exports to the US was lifted. Canadian Prime Minister Justin Trudeau said the move was unacceptable. Canadian Economy Minister Freeland said that a matching tariff will be imposed on US products, with additional duties for food products such as orange juice and whisky.

Canadian Finance Minister Bill Morneau stressed the need to defend the interests of Canada. The US is calling the need for tariffs one of national security with the Canadian PM calling it absurd as the nation has been a steadfast ally in times of war and peace. The loonie had gained momentum after the Bank of Canada (BoC) rate statement on Wednesday. Although the central bank did not lift its interest rate it was hawkish enough that a July move was on the table. The CAD fell after the possibility of a trade war with the US after a long but unfruitful negotiation of NAFTA could mean the end of the treaty.

The currency is near the 1.30 price level as the trade agreement is under serious threat as the White House is once again playing hard ball.

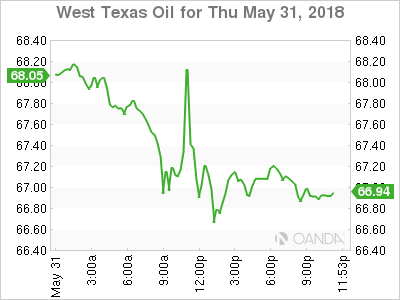

Oil falls on Trade Concerns

Despite the comments from the G7 Finance meeting in Canada on global growth the fact remains that trade wars are bad for business. Crude has been on decline as the Organization of the Petroleum Exporting Countries (OPEC) and Russia are considering easing some of the production limits they agreed to stabilize prices. The release of the weekly crude stock data in the US was on Thursday to account for the long weekend. A larger than expected drawdown of 3.6 million barrels should have been supportive of higher crude prices. And that was the case at the 11:00 am EDT mark, but as trade concerns rose, the black stuff went the other way.

Market events to watch this week:

Tuesday, May 29

8:00pm JPY BOJ Gov Kuroda Speaks

Wednesday, May 30

8:15am USD ADP Non-Farm Employment Change

8:30am USD Prelim GDP q/q

10:00am CAD BOC Rate Statement

10:45am CHF SNB Chairman Jordan Speaks

9:00pm NZD ANZ Business Confidence

9:30pm AUD Private Capital Expenditure q/q

Thursday, May 31

All Day G7 Meetings

8:30am CAD GDP m/m

11:00am USD Crude Oil Inventories

Friday, June 1

4:30am GBP Manufacturing PMI

All Day G7 Meetings

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

8:30am USD Unemployment Rate

10:00am USD ISM Manufacturing PMI

Gold Sticks To $1300, Investors Await Non Farm Payrolls, Wage Growth

Gold has posted gains in the Thursday session. In the North American session, the spot price for one ounce of gold is $1301.14, unchanged on the day. On the release front, consumer data was positive, as Personal Spending and PCE Price Index both beat their estimates, with readings of 0.2% and 0.6%, respectively. There was more good news as unemployment claims dropped sharply to 221 thousand, beating the estimate of 228 thousand. On Friday, British Manufacturing PMI is expected to dip to 53.5 points. In the U.S, the focus will be on employment data, with the release of nonfarm payrolls and wage growth.

The political uncertainty which has gripped Italy has shaken up the markets and boosted gold prices this week. President Sergio Mattarella is looking for a way to avoid new elections, after an inconclusive election in March. The two largest parties, the League Nord and the Five Star Movement proposed a eurosceptic finance minister, but this was blocked by the pro-European Matterella. This triggered a political crisis which led to a selloff of Italian stocks and bonds. The prime minister-elect, Giuseppe Conte, then announced that he had withdrawn his mandate to form a government, and Mattarella invited Carlo Cottarelli, a former IMF economist, to form a temporary technocrat government. There was talk of an election in the fall or even earlier, but Mattarella has agreed to let the two parties again try and form a coalition government. The twists and turns in this saga will likely continue to have an impact on the direction of gold prices.

Is the Federal Reserve moving closer to a neutral monetary policy? Recent statements by FOMC policymakers appear to support such a conclusion, which would mean that the Fed would let the economy ‘ride on its own steam’ without intervening by adjusting interest rates. In the meantime, the Fed continues to project two more rate hikes in 2018, after raising rates by a quarter-point in March. The most likely dates for a rate hike are June and September. A fourth hike in December is possible, with a likelihood of about 40%. The minutes of the May meeting noted that policymakers would consider allowing inflation to rise above the Fed’s 2% target for a temporary period, which means that the Fed would not rush to raise rates based on the inflation target.

Eco Data 6/1/18

[php_everywhere instance="1"]

Economics professor Giovanni Tria might replace Paolo Savona as Italian Economy Minister

It's reported that Italy’s anti-establishment 5-Star Movement and the far-right League party are close to finding that "point of compromise" in replacing Paolo Savona as economy minister in the government.

The name of economics professor Giovanni Tria flow around in the media. Meanwhile, law professor Giuseppe Conte will likely remain as prime minister. Decision could come as soon as on Friday. And if these names are accepted by President Sergio Mattarella, a snap election could be averted and a coalition government would finally be formed.

British Pound Trading Sideways, Manufacturing PMI Next

The British pound is almost unchanged in the Thursday trade. In the North American session, GBP/USD is trading at 1.3300, up 0.013% on the day. On the release front, British GfK Consumer Confidence remains weak, pointing to a glum British consumer. The indicator came in at -7, just above the estimate of -8 points. In the US, Personal Spending and PCE Price Index both beat their estimates. Unemployment claims dropped sharply to 221 thousand, beating the estimate of 228 thousand. On Friday, British Manufacturing PMI is expected to dip to 53.5 points. In the U.S, the focus will be on employment data, with the release of nonfarm payrolls and wage growth.

Is the Federal Reserve moving closer to a neutral monetary policy? Recent statements by FOMC policymakers appear to support such a conclusion, which would mean that the Fed would let the economy ‘ride on its own steam’ without intervening by adjusting interest rates. In the meantime, the Fed continues to project two more rate hikes in 2018, after raising rates by a quarter-point in March. The most likely dates for a rate hike are June and September. A fourth hike in December is possible, with a likelihood of about 40%. The minutes of the May meeting noted that policymakers would consider allowing inflation to rise above the Fed’s 2% target for a temporary period, which means that the Fed would not rush to raise rates based on the inflation target.

With the Brexit deadline of March 2019 creeping ever closer, the May government still does not have a coherent plan regarding its departure from the EU. The European Council meets next month, and Brexit is sure to be high up on the agenda. The Europeans have often expressed exasperation at a lack of direction from the British, as there are deep divisions in the May cabinet between the ‘hardliners’ and those who favor a softer Brexit, with close links to the continent. Some lawmakers are raising their voices, calling on May to seek a ‘sensible’ deal with Europe. One vexing issue is the status of the Irish border – how to maintain an open border between Ireland and Northern Ireland when the UK leaves the EU. May has proposed a “new customs partnership” between Northern Ireland and Ireland, but the Europeans have rejected this idea as being unworkable, and want the U.K to simply copy EU trade rules. This suggestion has been rejected by Brexit hardliners, who don’t want to follow orders from Brussels.

Japanese Yen Steady, Housing Report Sparkles

The Japanese yen has posted gains in the Thursday session. In North American trade, USD/JPY is trading at 108.62, down 026% on the day. On the release front, it’s a busy day. Japanese Housing Starts surprised with a gain of 0.3%, ending a nasty streak of nine straight declines. This easily beat the estimate of -8.8 percent. Later in the day, Japan releases Capital Spending, which is expected to drop to 3.2%, and Final Manufacturing PMI, which is forecast to fall to 52.5 points.

Is the Federal Reserve moving closer to a neutral monetary policy? Recent statements by FOMC policymakers appear to support such a conclusion, which would mean that the Fed would let the economy ‘ride on its own steam’ without intervening by adjusting interest rates. In the meantime, the Fed continues to project two more rate hikes in 2018, after raising rates by a quarter-point in March. The most likely dates for a rate hike are June and September. A fourth hike in December is possible, with a likelihood of about 40%. The minutes of the May meeting noted that policymakers would consider allowing inflation to rise above the Fed’s 2% target for a temporary period, which means that the Fed would not rush to raise rates based on the inflation target.

The Bank of Japan remains officially committed to continuing its radical easing policy and negative interest rates until inflation rises closer to the bank’s target of around 2 percent. At the same time, BoJ policymakers have been looking for ways to move away from radical easing, in part because ultra-low interest rates have hurt the profits of financial institutions. BoJ Governor Haruhiko Kuroda has promised that the bank would be transparent with regard to an exit from its radical easing policy, as Kuroda is well aware that even a slight change in fiscal or monetary policy can have a dramatic impact on the markets, a scenario that the BoJ is keen to avoid.

Mexico to hit back US on agricultural and steel products

Mexican Economy Ministry said there are wide-range "equivalent" measures to counter the US steel tariffs. It's reported that Mexico will target agricultural products that could hit Trump's base states. And the measures will be in place until the US stops its tariffs.

It said in a statement that "Mexico profoundly regrets and condemns the decision by the United States to impose these tariffs on imports of steel and aluminum from Mexico."

"Mexico reiterates its openness to constructive dialogue with the United States, its support for the international commerce system and its rejection of unilateral protectionist measures."

The Ministry also said Mexico buys more steel and aluminum from the US than it sells. And it's the top buying of US aluminum and second buyer of US steel.