Sample Category Title

EURO Intraday Bearish Below 1.1700

The euro currency retains its bearish bias against the US dollar, after a strong technical rejection from the key 1.1700 level on Thursday. The EURUSD pair fell sharply from the 1.1723 level, with price currently trades around the 1.1670 level, after earlier finding support from the 1.1640 level. EURUSD traders now look to the release of key eurozone PMI data and the US Non-farm payrolls job report later today.

The EURUSD pair is intraday bearish while trading below the 1.1700 level. Key support is now located at the 1.1640 and 1.1600 levels.

If the EURUSD pair moves above the 1.1700 level, buyers may push price back towards the 1.1750 and 1.1800 levels.

US Nonfarm Payrolls In The Spotlight On Friday

Investors can expect a steady flow of market-moving events on Friday, culminating in the US Labor Department’s monthly nonfarm payrolls report. Arguably the most closely watched calendar event of the month, nonfarm payrolls provides a timely snapshot of the US labor market and the overall economy.

IHS Markit is scheduled to release a deluge of Eurozone PMI reports beginning at 07:15 GMT covering Spain, Italy, France, Germany and the broader euro area. For the 19-member currency region, Markit’s manufacturing PMI is forecast to read 55.5 for the month of May.

The Italian government is scheduled to release revised first-quarter GDP numbers at 08:00 GMT. The Italian economy is projected to rise 1.4% on the quarter.

US nonfarm payrolls are scheduled for distribution at 12:30 GMT. The May reading is expected to show a net gain of 188,000 jobs for May, compared with 164,000 in April. The jobless rate is projected to hold steady at 3.9%.

Average hourly earnings, a proxy for wage inflation, likely rose 0.2% on month and 2.7% annually.

Elsewhere on the economic calendar, the Institute for Supply Management (ISM) will release its US manufacturing gauge at 14:00 GMT. The manufacturing purchasing managers’ index (PMI) likely strengthened to 58.1 in May from 57.3 in April.

The Commerce Department will round out the data wire with a report on construction spending, which is scheduled for 14:00 GMT.

In terms of monetary policy developments, Federal Open Market Committee (FOMC) member Neel Kashkari will deliver a speech at 12:55 GMT.

EUR/USD

Europe’s common currency extended its rally on Thursday, with prices briefly trading above 1.1700 USD. At the time of writing, EUR/USD was valued at 1.1686, where it was little changed. US nonfarm payrolls will play a major role in how the euro as well as other dollar pairs are priced heading into the weekend. Better than expected results will encourage the bulls while a slower than expected rise may compel the bears to take control. EUR/USD faces immediate support at 1.1660. On the upside, 1.1700 presents an immediate hurdle.

USD/CAD

USD/CAD snapped back to health on Thursday after suffering a 150-pip selloff at the hands of the Bank of Canada. The pair is back to trading in the mid-1.2900 region. A strong jobs report on Friday could generate bids closer to the psychologically important 1.3000 region.

GBP/USD

Cable also backtracked on Thursday after posting large gains the previous session. GBP/USD fell from a high near 1.3350 back down to the 1.3280 region. The pair faces renewed downside risks, with Tuesday’s low of 1.3200 back in focus. On the opposite side of the spectrum, a convincing break above 1.3310 could generate renewed support for cable.

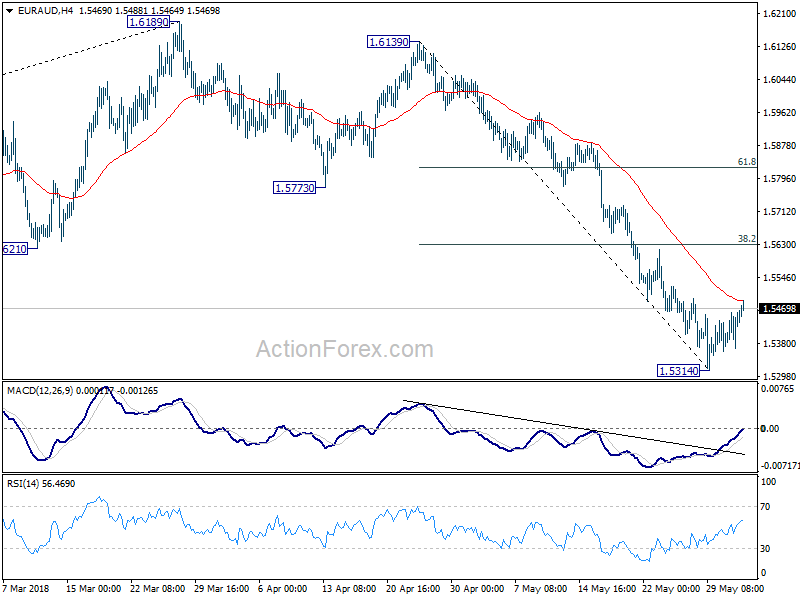

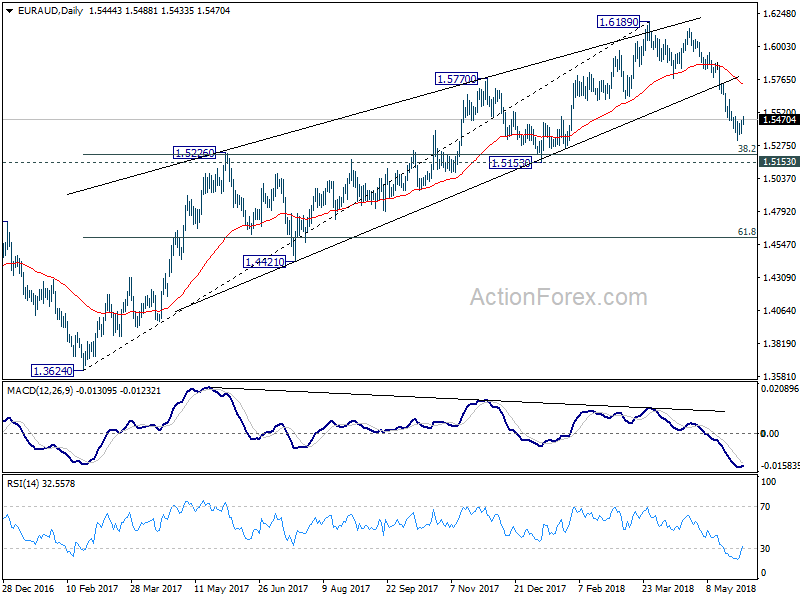

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5392; (P) 1.5428; (R1) 1.5485; More....

Intraday bias in EUR/AUD remains neutral as consolidation from 1.5314 is still in progress. Further recovery could be seen. But upside should be limited by 38.2% retracement of 1.6139 to 1.5314 at 1.5269 to bring fall resumption. Below 1.5314 will resume the decline from 1.6189 and target 1.5153 key support level next.

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further decline is expected in medium term, even in case of strong rebound.

Weighing the Impact of U.S. Steel and Aluminum Tariffs on Canada

The direct impact is manageable, but there's reason to fear a trade escalation

The U.S. looks set to impose steep tariffs on Canadian steel and aluminum products on June 1 after Commerce Secretary Wilbur Ross announced that the temporary exemption Canada had secured would expire as scheduled. The tariffs, which the U.S. will also levy on allies including Mexico and the European Union, will likely have a moderately negative but manageable impact on all countries involved. The broader risk is that the U.S. tariffs, and the retaliatory trade measures they give rise to, will ultimately turn into a global trade war. We're still a long way from that outcome, despite all the rhetoric. But the tariffs just add to uncertainty about the future, and that's not good for business investment.

Putting steel tariffs in context

Almost 90% of Canadian steel and aluminum exports go to the U.S., so clearly the new tariffs will have an impact on those industries. Steel and aluminum production targeted directly by the new tariffs doesn't represent a big share of the Canadian economy. By our count, about half of Canada's steel and three-quarters of aluminum exports will be impacted by the tariffs — amounting to about 3% of Canada's total exports. Regionally, Ontario and Quebec are disproportionately affected. Ontario accounts for about 80% of Canadian steel exports. Quebec accounts for around 75% of aluminum exports. Combined steel and aluminum production together accounts for about 0.5% of Canadian GDP and jobs.

U.S. producers will probably pay big part of upfront costs

The main impact of higher U.S. tariffs to date has been higher U.S. prices. The U.S. has already imposed significant tariffs on Canadian softwood lumber and newsprint, for example, in addition to steel tariffs levied earlier on a select group of countries, notably China and Russia. U.S. prices have spiked higher for all of those products. Import tariffs are typically framed as an attack on another country's exports. Much of the cost, though, is ultimately paid by domestic rather than foreign producers and consumers. A weaker Canadian dollar could also offset some of the impact on demand for Canadian products from the tariffs.

Downstream impact not necessarily all negative

If they work as intended, the tariffs will hurt Canadian steel and aluminum producers by lowering the price of steel and aluminum in Canada. But for any business using those products as an input, that's actually a good thing — and many more workers are in industries that build things from metal than produce metal themselves. The manufacturing sector, for example, is still ~10% of the Canadian economy. The highly integrated nature of U.S. and Canadian production chains muddy the picture. Steel tariffs will further increase the price of U.S. steel and in highly integrated industries it will be difficult for Canadian businesses to avoid higher prices as U.S. producers are forced to pass on part of their higher raw material costs into prices they charge Canadian customers for intermediate goods further up the value chain. The auto sector, a large consumer of steel, is probably the poster child for this type of disruption.

Part of the secondary impact of the Trump tariffs will also be in the form of higher Canadian import prices, as Canada, along with Mexico and Europe, respond with retaliatory measures. Canada has already announced intentions to levy tariffs on $16.6 billion of goods from the U.S. — matching the value of Canada's 2017 exports impacted by the U.S. tariffs. That will mean higher prices for Canadian importers, but the amount is still only ~2% of Canada's annual imports, so the broader consumer price impact won't be that large. Trade officials are typically savvy enough to design retaliatory measures to have maximum political impact abroad and mini-mum impact on the domestic economy.

The tariffs mean more uncertainty for businesses

Perhaps the most important message from tariffs is that they are based on flimsy rationale — and that makes it difficult to predict which industry might be next. In this case, the U.S. has justified the tariffs on national security grounds, a questionable position giv-en that Canada, Mexico, and Europe are all U.S. allies. The U.S. also explicitly tied the hike in tariffs for Mexico and Canada to fail-ure to come to an agreement on NAFTA before the end of May. But if the point was to target NAFTA partners, then why steel? The U.S. was a net exporter of steel to both Canada and Mexico last year. Not knowing which industry could be next means any industry could be next, and that means more uncertainty for all trade-intensive businesses.

Are we in for a global trade war?

That's a ways off. Yes, the anti-trade rhetoric from the Trump administration represents a sharp departure from what we're used to hearing from U.S. presidents. But even including potential tariffs on $50 billion of imports from China, the effective tariff rate from the U.S. will still be quite low. By our math, custom duties collected could increase to just over 2% of imports based on measures announced to date, up from about 1 1/2% last year. So while, an across-the-board tariff hike of around 0.8 of a percentage point doesn't qualify as a global trade war, sabres are rattling.

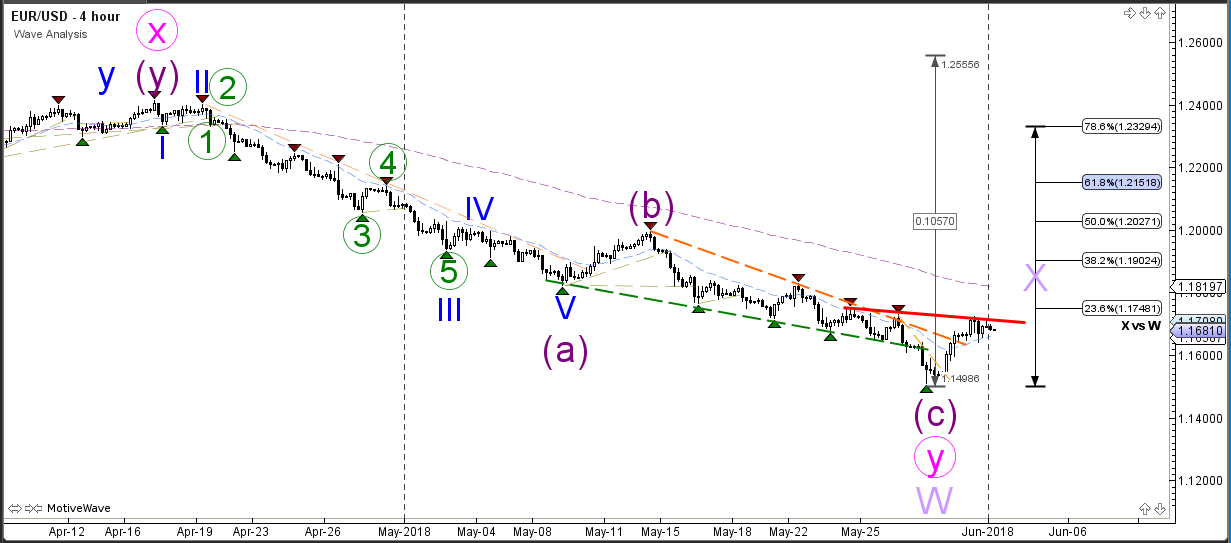

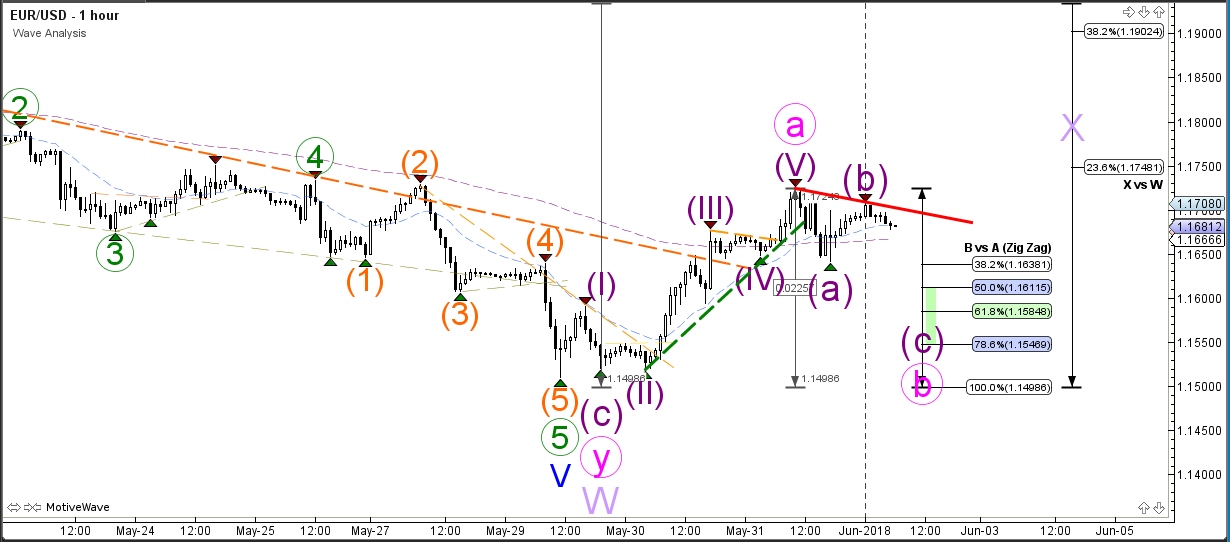

EUR/USD Builds ABC Correction After 5 Bullish Waves?

The EUR/USD stopped at the previous highs (red) and 23.6% Fibonacci retracement level of wave X (purple). Price could bounce back down at this resistance zone but if it fails to break below the previous bottom, then price could build a larger wave X (purple) correction as indicated in the image. Keep in mind that today there is a news event in the US with new non-farm pay roll (NFP) figures and unemployment rates coming out.

The EUR/USD bullish price action seems to have completed 5 waves and could now be building an ABC (purple) correction. The Fibonacci levels of wave B could act as support but a break below the 100% Fib invalidates the current expected zigzag pattern within wave X (purple). A break above the resistance trend line (red) could also indicate a breakout towards the Fib targets of wave X (purple).

GBP/USD Bounces At Fib Levels And Breaks Support Line

The GBP/USD made a bearish bounce at the resistance trend line and could be expanding the downtrend.A bearish break below the round level of 1.3250 and the previous bottom could see price move towards the Fibonacci targets of wave 5 (blue).

The GBP/USD could either be completing a wave 5 of a larger wave 1 or price is in a strong momentum as part of a wave 3 (current chart)

The GBP/USD bounced and turned at the 38.2-50% Fibonacci levels of wave 4 (green) which means that price is not in an ending diagonal. Price does seem to have completed a wave 4 though and GU broke below the support trend line (dotted green) after the Fib bounce. Price will need to break below the 1.3250 round level but keep in mind that today offers high impact news from the US with non-farm payroll (NFP) figures and unemployment rate.

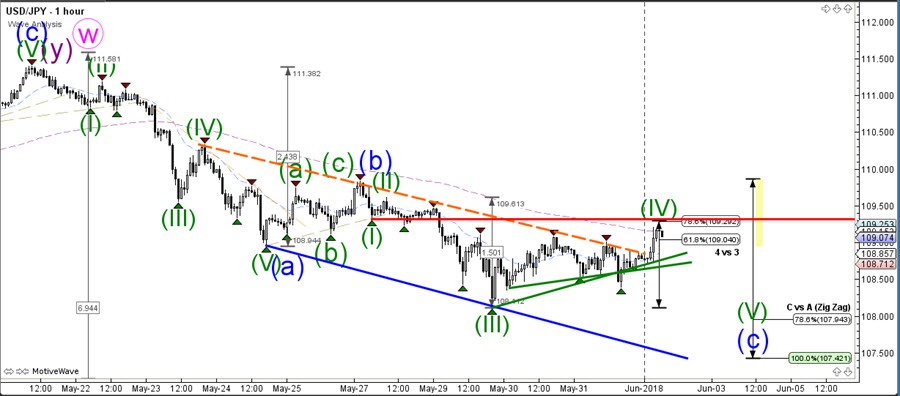

USD/JPY Ready For Bullish Or Breakout During NFP Event

The USD/JPY is approaching a key resistance level (red) which offers a critical bounce or break spot. The news from the US regarding unemployment rates and non-farm payroll data (NFP) could fuel a larger move too.

A bullish breakout could indicate the end of the ABC (blue) zigzag pattern and start of larger move up within wave D (purple). A bearish bounce could indicate the continuation of the wave C (blue).

The USD/JPY is testing the bottom of the wave 1 which is indicated by the resistance trend line (red). A break above it could indicate a bullish breakout potential whereas a break below support (green) could see price move towards the Fib targets of wave C.

Elliott Wave View: USDJPY Calling For Bounces To Fail Ahead Of NFP?

USDJPY Short-term Elliott Wave view suggests that the rally to 111.40 on May 21 ended intermediate wave (A) as a Diagonal structure coming from March 26 low (104.52) cycle. Pair is currently correcting cycle from 3/26 low within Intermediate wave (B). The pullback shows overlapping price structure suggesting that it is taking the form of a corrective structure i.e either as W,X,Y or W,X,Y,X,Z structure.

Down from 111.40 high, the decline to 108.94 low ended Minute wave ((a)) of W in 5 waves. The bounce to 109.83 high then ended Minute wave ((b)) of W in 3 waves bounce. Afterwards, the decline to 108.10 low ended Minute wave ((c)) and also completed Minor wave W as an Elliott Wave Zigzag structure. Up from there, Minor wave X bounce is in progress to correct the cycle from 111.40 high. The rally should fail in 3, 7 or 11 swings for further downside correction as far as pivot at 111.4 high stays intact. Near-term focus remains towards 109.35-109.59 to finish Minor wave X. This is the 100%-123.6% Fibonacci extension area of Minute wave ((a))-((b)) of a zigzag structure. Once wave X is complete, pair should resume lower provided the pivot at 111.40 high stays intact or should react lower in 3 swings at least. We don’t like buying the proposed rally.

USDJPY 1 Hour Elliott Wave Chart

US Employment Data And Political Situation In Italy

General Trend:

- Equity markets trade mixed following declines in the US

- Italy’s League and Five Star parties reach agreement on cabinet, formally given mandate from President to form coalition government

- Chinese equities open lower following MSCI changes

- May Macau Gaming Rev below ests, casino names decline

- Samsonite rallies over 9% in Hong Kong, board named new CEO and refuted claims from short seller

- Bank of Japan (BoJ) trims purchases of 5-10 yr JGBs in daily operation, USD/JPY and JGB yields rise

- Japan Q1 Capex growth slows

- Australia housing values decline y/y in May for first time since Oct 2012 (CoreLogic)

- New Zealand Q1 terms of trade declines for first time since 2016; dairy product export prices -6.7%

- Various global officials comment amid G7 summit including BoJ Gov Kuroda, Germany Fin Min Scholz

- There was no debate on bilateral free trade agreement (FTA) or FX in the talks between Japan Finance Minister Aso and US Treasury Sec Mnuchin, said a Japan official

- US Commerce Sec Ross confirmed he is still scheduled to travel to China later this week

- Upcoming US May employment data in focus

- Australia Q1 GDP data due next week (Wed, June 6th)

Headlines/Economic Data

Australia/New Zealand

- ASX 200 opened -0.1%; closed -0.3%

- ASX 200 Telecom index -0.9%, Financials -0.8%, Utilities -0.7%, Energy -0.7%; Resources +0.3%

- ANZ Bank [ANZ.AU] declines over 1% after disclosing criminal cartel probe

- (AU) Australia minimum wage to increase by 3.5% to A$24.30/week - Fair Works Council (FWC)

- (AU) Australia May CoreLogic House Price M/M: -0.2% v -0.3% prior

- (AU) Australia to sell A$2.5B of May 21 2030 bonds on June 8th

- (NZ) New Zealand Q1 Terms of Trade Index Q/Q: -1.9% v -2.0%e (first decline since Q3 2016)

- (NZ) New Zealand ANZ May Consumer Confidence Index: 121.0 v 120.5 prior; m/m: +0.4% v -5.9% prior

China/Hong Kong

- Shanghai Composite opened -0.4%, Hang Seng +0.3%

- Hang Seng Services index -2.4%, Consumer Goods -1.1%, Industrial Goods -1%, Materials -0.8%, Financials -0.4%; Telecom +0.4%

- (US) Commerce Sec Ross: Still scheduled to travel to China this week; Exploring options that may include keeping ZTE open

- (CN) China PBoC may additionally cut the reserve ratio requirement (RRR) by 50-150bps by the end of 2018 - Chinese Press

- (CN) CHINA MAY CAIXIN PMI MANUFACTURING: 51.1 V 51.2E

- (CN) For the week, the PBoC injects a net of CNY410B through open market operations (OMOs) v CNY30B net drain w/w

- (CN) China PBoC Open Market Operation (OMO): To inject CNY80B in 7, 14 and 28-day reverse repos v CNY220B injected in 7, 14 and 28-day reverse repos prior: Net: injection CNY80B v CNY180B injected prior

- (CN) China PBoC sets yuan reference rate at 6.4078 v 6.4144 prior

Japan

- Nikkei 225 opened -0.3%; closed -0.1%

- TOPIX Securities index +1.1%, Marine Transportation +0.7%, Iron & Steel +0.7%, Electric Appliances +0.5%

- Toyota trades higher by over 3%; says it is considering various options to enhance competitiveness

- (JP) (JP) BoJ announcement related to daily bond buying operation; Trims planned 5-10 year JGB purchase to ¥430B v ¥450B prior [Reminder: In the past, BoJ officials have said the daily bond buying operations are not intended to signal monetary policy changes]

- (JP) US Treasury Sec Mnuchin and Japan Finance Min Aso held talks at the G-7 meeting (in line with recent press speculation) – Japanese Press; Japan MOF official says there was no debate on FX

- (JP) Japan Q1 Capital Spending (Capex) Ex Software: 2.1% v 3.8%e; Capital Spending Y/Y: 3.4% v 3.1%e

- (JP) Japan May Final PMI Manufacturing: 52.8 v 52.5 prelim (confirms a 7-month low)

- (JP) BoJ Gov Kuroda: Global trade supports global economy; No big impact likely from political situation in Italy - G7 Comments

Korea

- Kospi opened -0.1%

- (KR) North Korea's Kim Jong Un: hopes North Korea-US ties will be solved step by step - press

- (KR) Sec of State Pompeo: after talks with senior North Korea official, he is confident things are going in the right direction

- (KR) South Korea May CPI M/M: 0.1% v 0.2%e; Y/Y: 1.5% v 1.7%e

- (KR) South Korea Q1 Final GDP Q/Q: 1.0% v 1.1%e; Y/Y: 2.8% v 2.8%e

- (KR) South Korea May Trade Balance: $6.7B v $6.6Be; Exports Y/Y: 13.5% v 10.5%e

- (KR) South Korea May PMI Manufacturing: 48.9 v 48.4 prior (3rd straight contraction)

Other

- (PH) Philippines May PMI Manufacturing: 53.7 v 52.7 prior

- (TH) Thailand May CPI M/M: 0.6% v 0.4%e; Y/Y: 1.5% v 1.3%e

- (TH) Thailand May PMI Manufacturing: 51.1 v 49.5 prior

- (TW) Taiwan May PMI Manufacturing: 53.4 v 54.8 prior

- (VN) Vietnam May PMI Manufacturing: 53.9 v 52.7 prior (highest since April 2017)

North America

- US equity markets ended lower: Dow -1%, S&P500 -0.7%, Nasdaq -0.3%, Russell 2000 -0.9%

- S&P500 Consumer Staples -1.6%, Industrials -1.5%

- (US) Fed's Brainard (voter, dove): gradual rate increases are appropriate in light of tight labor market; alert to emerging risks to adjust policy as needed; Trade is clouding the outlook and could be disruptive; A broader pullback in emerging markets bears watching

- (US) Fed's Quarles (hawk, FOMC voter): trade measures haven't had big macro effect; There's reason to think neutral rate is rising; We need to watch Italy but hasn't changed outlook yet

- (US) Fed's Mester (hawk, FOMC voter): Italy political situation hasn't changed view of US economic fundamentals

- (US) Fed Bullard (dove, non-voter): Trade talks creating more uncertainty in economy; difficult to see if too much will change after talks

- (US) DOE CRUDE: -3.6M V -0.5ME

Europe

- (IT) Northern League party official confirms Five Star and League have reached agreement on an cabinet, including Economist Giovanni Tria as Fin Min

- (IT) Italy Pres formally gives PM-designate Conte mandate to form a Five Star/League coalition govt - press

- (IT) PM-designate Conte and his govt will be sworn in on Friday 11:00CET (05:00ET), and will face confidence votes on Monday and Tuesday

- (ES) Spain PM Rajoy reportedly does not plan to resign his post ahead of confidence vote on Friday - Spanish press

- (DE) Germany Fin Min Scholz: Implementation of US tariffs is wrong and illegal – G7 Comments

- (DE) Germany Government Official: Finance Min Scholz had open and honest talks with US Treasury Sec Mnuchin

- (UK) Brexit Min Davis reportedly devising new plan that would give Northern Ireland joint EU/UK status and border buffer zone - UK press

- (UK) BOE's Carney: In current US trade dispute, the focus on trade balance in goods is not the right focus

- Airbus [AIR.FR]: President said to tell workers that it will be difficult to meet 2018 delivery target - financial press

Levels as of 02:00ET

- Hang Seng -0.1%; Shanghai Composite -0.8%; Kospi +0.7%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.2%, Dax +0.1%; FTSE100 flat

- EUR 1.1665-1.1707 ; JPY 108.72-109.26 ; AUD 0.7538-0.7575 ;NZD 0.6984-0.7021

- Jun Gold -0.3% at $1,297/oz; Jul Crude Oil -0.3% at $66.83/brl; Jul Copper -0.2% at $3.058/lb

US ISM Manufacturing Probably Rose

Market movers today

Significant market attention will be on the new government in Italy that was formed last night and what policy signals it will send with regard to its economic and EU policy programme.

The market will also focus on trade tensions between the US and EU countries, Canada and Mexico.

On the data front, the most important release of the day is the US jobs report for May. Once again, average hourly earnings is the key number to watch . We estimate wages rose +0.2% m/m in May, in line with the recent trend, implying an unchanged annual growth rate of 2.6% y/y. We estimate that nonfarm payrolls rose 190,000 and the unemployment rate was unchanged at 3.9%.

Based on the regional PMIs and Markit PMI manufacturing, US ISM manufacturing probably rose and we think it may have rebounded from 57.3 to 58.0. This does not change our overall view that the US manufacturing indices should move lower in 3-6M.

In the UK , we also get the PMI manufacturing index for May. The UK index is more volatile (bigger swings) than the equivalent index for the euro area, and since it fell in May, the UK index may very well follow. We estimate a fall to 53.6 from 53.9.

Selected market news

Things move fast in Italy and yesterday Five Star and the League announced they would form a new government. Paolo Savona, who the President rejected as finance minister and has very EU-sceptical views, would be minister of EU affairs, which may create tensions between Italy and the EU down the road. Markets have calmed down somewhat with 2yr yields now at 1% compared to nearly 3% at some point, but still significantly above the levels before the election.

The trade war escalated yesterday as the Trump administration announced it would impose tariffs on steel and aluminium imports from the EU, Mexico and Canada for national security reasons. The EU said it regrets the decision and would retaliate by imposing tariffs on products such as bourbon, jeans and Harley Davidson bikes (products from Republican states) and mainstream Republicans such as House Speaker Paul Ryan are clearly against Trump's decision. Mexico and Canada also aim to retaliate against Trump's measures. Trump later threatened to leave NAFTA altogether yesterday. All in all this is bad for consumers and businesses, as it would only lead to higher prices. The risk is that the trade war could escalate further, not only between the US and China but also between the US and other western countries.

In Spain , Prime Minister Rajoy is likely to lose the no-confidence vote today. Socialist leader Pedro Sanchez would likely become the new prime minister but has previously said he wants new elections, although he could stay until 2020 when new elections must be held. It is the first time a prime minister would be ousted this way, which makes it more difficult to predict what could happen. While political uncertainty is negative, the situation in Spain does not seem comparable with the one in Italy (at least right now), as there is no indication that Spain would follow the same route of saying it wants to leave the euro and wants debt relief.