Sample Category Title

Soft response from UK on US steel tariffs, deeply disappointed onlty

More responses on US steel tariffs.

A UK government spokesman said "we are deeply disappointed that the US has decided to apply tariffs to steel and aluminium imports from the EU on national security grounds."

And "the UK and other European Union countries are close allies of the U.S. and should be permanently and fully exempted from the American measures on steel and aluminium."

UK's responses are much softer than EU's.

German BDA, DIHK urged joint strong EU response to counter US steel tariffs

More responses on US steel tariffs.

German BDA employers group President Ingo Kramer said in a statement that "if the U.S. overrides international trade rules, then a strong, but above all, a joint strong EU response is required."

DIHK President Eric Schweitzer said "everyone will lose out" from the U.S. decision. It was important to keep up dialogue. But he also emphasized that "if needed, countermeasures should be taken to strengthen the EU position."

Germany’s steel industry association Wirtschaftsvereinigung Stahl criticized US steel tariffs based on national security concerns is “grotesque”. And, "the U.S. measures are a protectionist intervention in international trade and run counter to the principles of the WTO".

EU Juncker on US steel tariffs: It’s protectionism, pure and simple

In response to US steel and aluminum tariffs, European Commission President Jean-Claude Juncker immediately condemned that as "protectionism, pure and simple". The US actions are "unjustified" and "at odds with WTO rules". “So we will immediately introduce a settlement dispute with the WTO and will announce counter balancing measures in the coming hours.”

https://twitter.com/EU_Commission/status/1002190640753643520

Also, in a press release, Juncker added that the US was "playing into the hands of those responsible for the problem". He pledged that "we will defend the Union's interests, in full compliance with international trade law."

https://twitter.com/JunckerEU/status/1002191498165841920

Trade Commissioner Cecilia Malmstrom also said in the same statement that “the U.S. has sought to use the threat of trade restrictions as leverage to obtain concessions from the EU. This is not the way we do business, and certainly not between longstanding partners, friends and allies.”

She added "now that we have clarity, the EU’s response will be proportionate and in accordance with WTO rules. We will now trigger a dispute settlement case at the WTO, since these U.S. measures clearly go against agreed international rules." And “we will also impose rebalancing measures and take any necessary steps to protect the EU market from trade diversion caused by these U.S. restrictions.”

EU's statement here

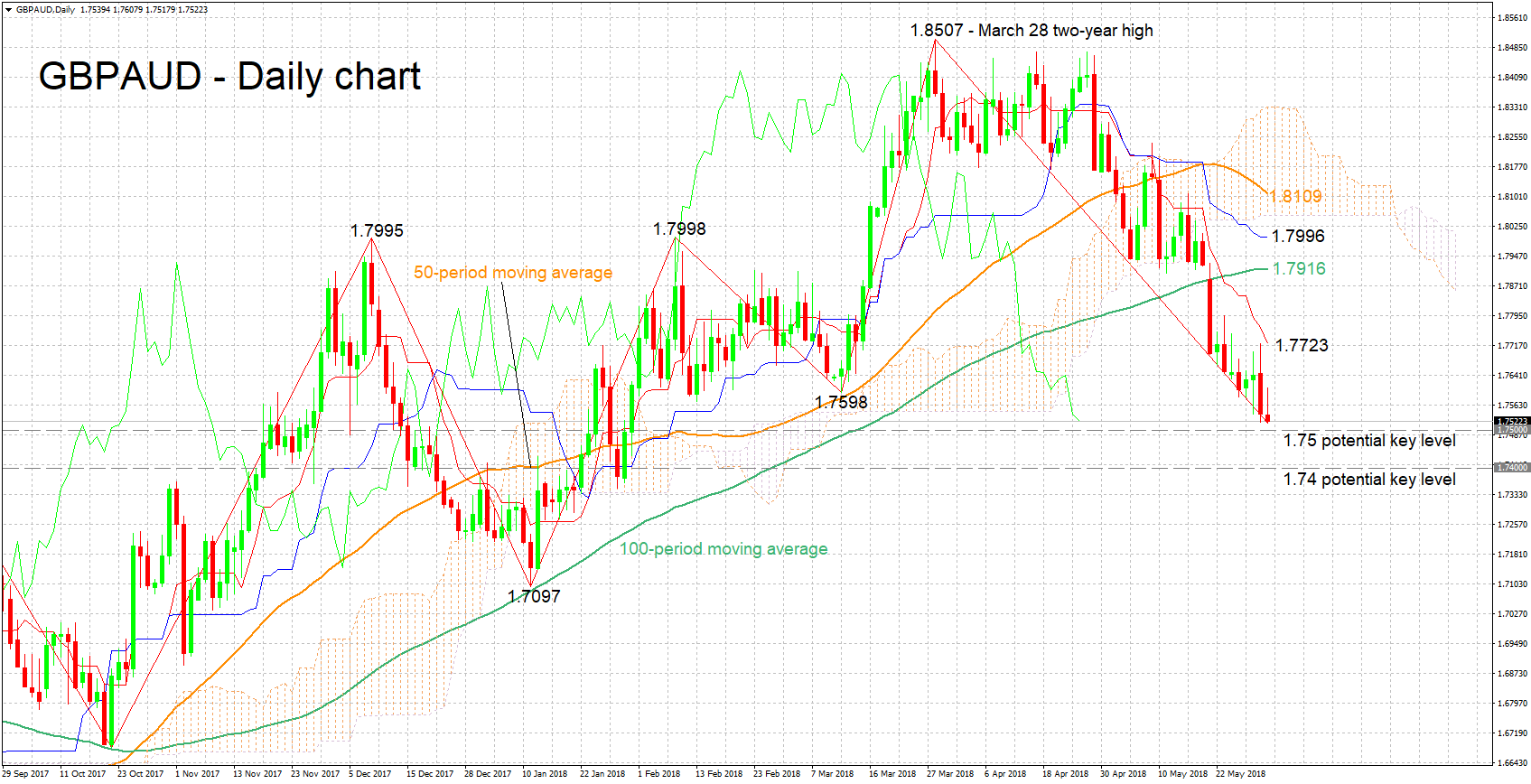

GBPAUD Falls to 4-Month Low, Looks Oversold

GBPAUD has declined considerably after touching a two-year high of 1.8507 in late March. During Thursday’s trading, it posted a four-month low of 1.7516, while it is currently not far above that nadir.

The negatively aligned Tenkan- and Kijun-sen lines serve as a testament to the negative short-term momentum that is in place. The Chikou Span, though, is signaling a potentially oversold market; a near-term reversal should thus not be ruled out.

Immediate support to further declines may be taking place around the 1.75 round figure, while the 1.74 handle could provide additional support in case of steeper losses.

A move to the upside may meet resistance around 1.7598, this being a bottom recorded on March 12, with the area around it also encapsulating the 1.76 handle. The region around the current level of the Tenkan-sen at 1.7723 could act as an additional barrier in case of stronger bullish movement.

The medium-term picture is looking predominantly bearish at the moment, with price action taking place below the 50- and 100-day moving average lines, as well as below the Ichimoku cloud.

Overall, both the short- and medium-term outlooks are currently looking bearish, though caution is warranted in the near-term as there are signs of an oversold market.

U.S. Consumers Back in Full Force in April

Personal income rose 0.3% in April, bang on expectations. Adjusted for inflation and removing taxes, real disposable income was up 0.2% in the month.

Personal spending rose by a robust 0.6% in nominal terms in April, ahead of consensus forecast for a 0.4% gain. Spending on non-durable goods led the way rising by 0.9%, followed by spending on services (+0.5%). Meanwhile, spending on durable goods rose modestly (+0.3%). After stripping out inflation, spending advanced by a solid 0.4% in real terms.

Prices rose by 0.2% on the month, lifted by both energy and food prices, which increased by 1.5% and 0.3%, respectively. On a year-over-year basis, headline inflation remained unchanged at 2%, right on the Fed's target. Core PCE inflation – the Fed's preferred measure of inflation – also rose by 0.2% (month-on-month), but remained unchanged at 1.8% on a year-over-year basis.

The personal saving rate fell by 0.2 percentage points to 2.8% - the lowest level since December 2017.

Key Implications

Two strong back-to-back prints in consumer spending in March and April reaffirm that U.S. consumers left behind their winter blues and are back in full force. Washington's tax cuts were also implemented on employee payrolls part way through Q1, so the recent strength in spending likely reflects consumers starting to spend those slightly larger paychecks. As a result, after expanding by just 1% (annualized) in the first quarter of the year, consumer spending is on track to well surpass the 3% mark in Q2. This bodes well for GDP growth, which is also likely to come in north of 3%.

A rebound in spending and inflation was already baked into the FOMC's thinking, as evident from the latest FOMC minutes. As a result, there's not much new in this release for the FOMC committee, with a June hike likely a done deal. However, with core inflation still running below 2%, there are few signs that the economy is overheating, which allows the Fed to continue with their gradual pace of rate normalization.

That being said, the risk of trade wars muddies the water on the inflation outlook. If imposed, tariffs will lead to higher prices for American consumers. As such, trade developments will be closely followed by the Federal Reserve in the coming months.

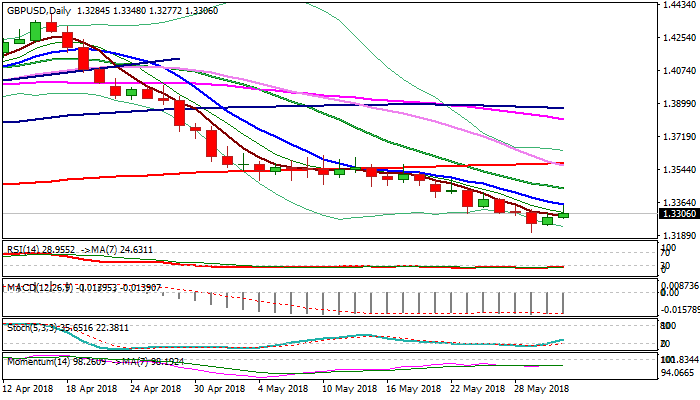

GBPUSD Outlook: Falling 10SMA Caps Recovery for Now; Stronger Dollar Adds Pressure on Sterling

Cable dipped below 1.33 handle in early hours of US trading after bullish acceleration earlier today faced strong headwinds from falling 10SMA (1.3351). Stronger dollar on upbeat US consumer spending which registered biggest gain in past five months, added to renewed pressure on sterling. As mentioned in the morning's report, bearish setup of daily techs favors fresh weakness and sees 10SMA as ideal cap. Daily close below 10 SMA would be initial negative signal which needs extension below broken 5SMA (1.3293) to re-expose key support at 1.3205 (top of weekly cloud / 29 May low). Alternatively, close above 10SMA would sideline downside risk and signal stronger recovery.

Res: 1.3351; 1.3410; 1.3441; 1.3459

Sup: 1.3293; 1.3277; 1.3241; 1.3205

Canadian GDP Records a Soft Pace in Q1 But With Decent Details

The Canadian economy grew by 1.3% q/q annualized in the first quarter, a bit slower than the prior quarter's 1.7% pace. Price gains were fairly modest as well, sending nominal GDP to 2.6%.

Non-residential business investment helped send output higher. Structures investment grew by a healthy 6.3% pace, but even more impressive was an 18.1% climb in investment in machinery and equipment, assisted by a surge in business spending on vehicles.

In contrast, consumer spending, although positive, came in below expectations, rising just 1.1%. Spending on goods was effectively flat, while service consumption held up (+2.1%)

On the negative side of the ledger were, as expected, housing and trade. Residential investment fell 7.2% owing entirely to a 44% drop in ownership transfer costs (i.e. resale activity). In contrast, new construction and renovation activity both performed well, up 5% and 5.9% respectively.

The writing was on the wall for international trade, but the final figures were not as bad as might have been expected. Exports rose 1.7%, helped by a 6.8% gain in services (goods exports were effectively flat), while imports rose 4.9%.

While output disappointed, incomes managed to hold up. The aggregate measure of employee compensation was up 4.0%. Household disposable income gained 3.7%, not quite enough to keep the (revised) savings rate flat, as it fell one tick to 4.4%.

The quarter ended on something of a positive note. Monthly GDP for March was up 0.3% m/m, with 15 of 20 major industries recording growth and solid gains in both the goods-producing (+0.6%) and services-producing (+0.2%) sectors of the economy.

Key Implications

This is another 'more than meets the eye' GDP report. Beneath modest headline growth were some relatively encouraging details. Business investment continued to climb, partially offsetting the more modest pace of consumer spending. Income gains also remained solid. Plus, March's solid monthly performance indicates that momentum continued to build through the quarter, setting the Canadian economy up for an acceleration in output in Q2.

What's more, even the weak spots in today's report shouldn't last. The poor performance of housing was confined to the resale market. This can be attributed by and large to the B-20 mortgage underwriting changes implemented on January 1st, the worst impacts of which are likely behind us. On the trade front, fog continues to hang over the horizon, but the robust U.S. growth outlook provides a decent backdrop going forward, suggesting that the sector should at least cease to be a drag on growth.

The bottom line is that the Canadian economy clearly still has some gas left in the tank. We remain confident that economic growth will remain modestly above potential for 2018 as a whole. Accordingly, conditions will stay supportive of a Bank of Canada hike at its next meeting in July.

Canadian GDP Up 1.3% in Q1 But With Stronger Details

Highlights:

- Canadian Q1/18 GDP rose 1.3%, less than the 1.9% expected by markets but with a more solid composition.

- Q1 GDP weakness was entirely concentrated in a 0.2% drop in January output. GDP rose 0.4% in February and 0.3% in March, leaving stronger momentum going into the second quarter.

- Final domestic demand rose 2.1%, led by a big 10.9% jump in business investment.

Our Take:

The 1.3% increase in GDP in Q1 was a bit softer-than-expected — both by markets and the Bank of Canada who it turns out could have stuck with their 1.3% call from January rather than hinting at some upside risk in yesterday’s policy rate announcement. Notwithstanding the headline miss, though, details were relatively solid. On a monthly basis, weakness was concentrated in January with March output rising 0.3% after a 0.4% February gain to leave stronger momentum entering the second quarter. Final domestic demand rose a solid 2.1% in Q1, led by a big 10.9% jump in business investment. Residential investment fell 7.2%, but that was expected given the big drop in home resales earlier this year. Consumer spending rose just 1.1% on a quarter-over-quarter basis but was still up almost 3% from a year ago. Net trade was the main drag on growth but largely because all of that domestic demand growth boosted imports which more than offset an unexpected (albeit still modest) export rise.

If there was a soft spot, it was perhaps on some of the wage measures released today. The national accounts data alongside the March ’SEPH’ employment earnings numbers also out this morning left the Bank of Canada’s closely-watched ’wage-common’ measure of wage growth tracking closer to 2 1/2% by our count than the 3% pace we were tracking ahead of today’s release. The broader trend nonetheless remains upward. BoC Deputy Governor Leduc’s speech later today may give some hints about how today’s releases impact the Bank’s thinking, but in general it looks like there is enough good in today’s data to leave a July rate hike in play after yesterday’s no-change decision.

Sunset Market Commentary

Markets:

Investors tune their trading behavior solely to Italian BTP’s these days. Italian yields declined further during the first half of European trading as new elections might be avoided. 5SM Di Maio and President Mattarella’s proposal only need the green light from Lega Salvini. The latter, up unitl now, seems to favour a new poll though given his impressive gain in opinion polls compared to the March vote. German yields mirror Italian ones in this positive risk sentiment and rose further until around European noon. Eurostat in the meantime released a significant surge in May EMU CPI data, both headline and core, but they didn’t really impact trading. Underlying inflation pressure seems to be building in EMU and suggest that a window of opportunity is opening up for the ECB to announce (in July) the future of its APP programma (end by YE2018?). Italian yields bottomed around noon which also marked a turning point in core bond trading, with both the Bund and the US Note future starting to gain ground. Media reports suggesting that Trump wants to ban German cars from the US might have been at work as well. US eco data were good, but printed too close to expectations to stop the rebound of the US Note future. US investors probably also look more forward to tonight’s speech by Fed Brainard and to tomorrow’s ISM and payrolls. Brainard’s voice is currently seen as representing the consensus view around the FOMC table. She’ll probably suggest two more rate hikes this year, but will she keep the option of 3 open? Changes on the German yield curve currently range between -2 bps (5-yr) and -4.6 bps (30-yr). The US yield curve flattens with yield changes ranging between +0.8 bps (2-yr) and -2.1 bps (30-yr). 10-yr yield spread changes vs Germany vary between -4 bps (Italy) and Greece (+4 bps).

The above outlined story counts for EUR/USD trading as well. The euro remained in pole position ahead of European noon until Italian BTP’s made an intraday turnaround. Investors are perhaps losing their patience with Salvini’s opaqueness. Anyway EUR/USD tried to retake the 1.17 barrier, but failed, returning towards the 1.1650 area at the time of writing. EUR/GBP showed the similar bump in trading, but swings were much smaller with the pair locked between 0.8760 and 0.8780.

News Headlines:

Inflation in the Eurozone accelerated sharply this month, mainly due to energy (6.2% Y/Y). The annual inflation rose to 1.9% Y/Y in May from 1.2% Y/Y in April. Core inflation, which excludes volatile components like food and energy, clocked in at 1.1% Y/Y, from 0.7% Y/Y in April. Both are at the highest levels since last year. Rising service inflation (1.6% Y/Y) also suggest that underlying price pressure is building.

Italy’s political fate rests on the next move by Matteo Salvini, the leader of the far-right Lega, who must either accept a last-minute compromise to launch a populist government or force new elections later this year (FT).

Washington will announce plans to impose tariffs on EU steel and aluminium imports as early as today, two sources said, while a magazine reported President Trump was now focused on pushing German cars from the country. (Reuters)

US eco data were close to expectations to slightly stronger than expected. April personal income rose by 0.3% M/M as forecast, but spending increased by 0.6% M/M (vs 0.4% M/M consensus). Weekly jobless claims continue to hover near historically low levels (221k). PCE deflators matched projections at 2% Y/Y for the headline reading and 1.8% Y/Y for the core measure. The May Chicago PMI surged from 57.6 to 62.7 (vs 58.3 forecast).

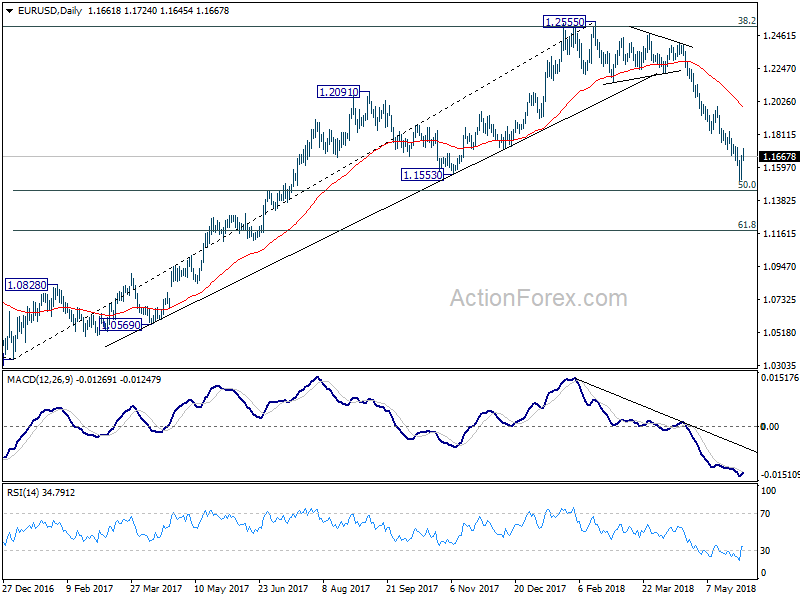

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1563; (P) 1.1620 (R1) 1.1720; More.....

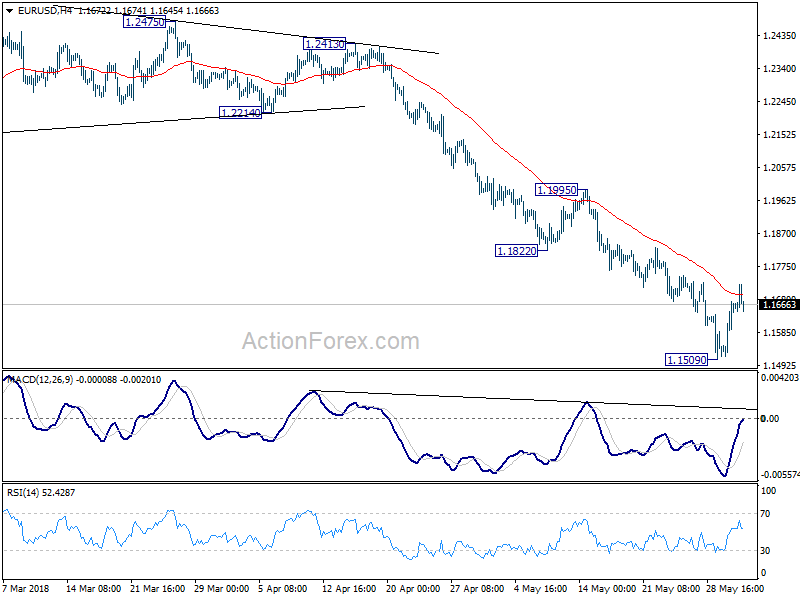

EUR/USD's recovery from 1.1509 extend to 1.1724 so far and breached 4 hour 55 EMA. Further rise cannot be ruled out. But upside should be limited by 1.1822/1995 resistance zone to bring fall resumption. Below 1.1509 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 first. Break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.