Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3242; (P) 1.3274; (R1) 1.3315; More...

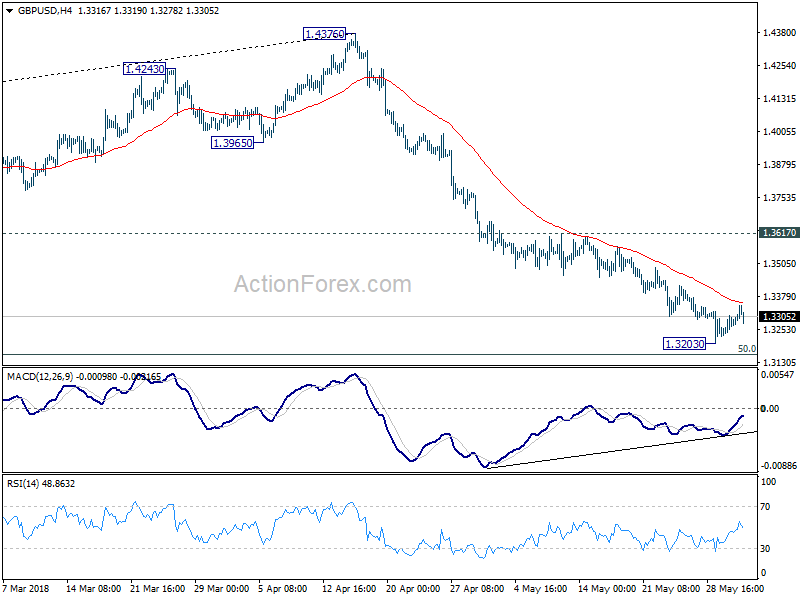

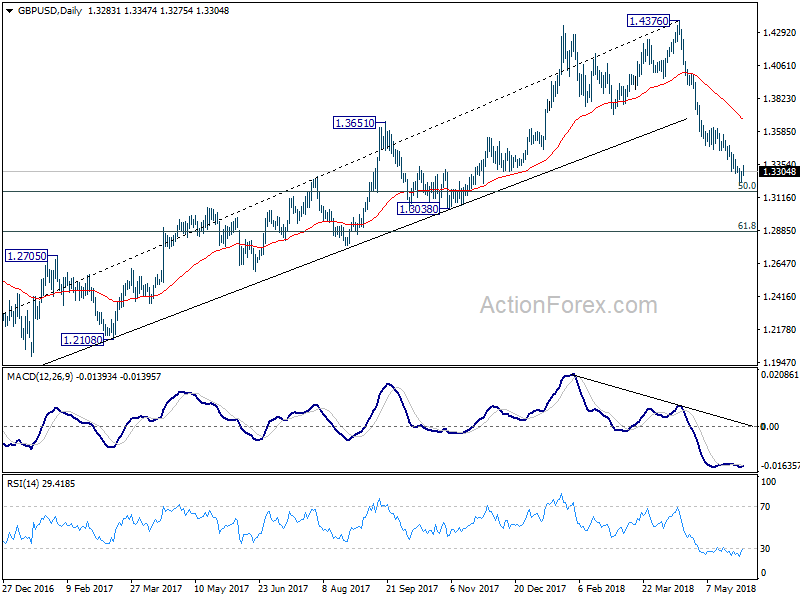

Intraday bias in GBP/USD remains neutral as consolidation from 1.3203 is in progress. Further recovery cannot be ruled out. But near term outlook will remain bearish as long as 1.3617 resistance holds. Fall from 1.4376 is expected to resume later. Below 1.3203 will target 50% retracement of 1.1946 to 1.4376 at 1.3161 first. Break will target 61.8% retracement at 1.2875 next.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3730) holds, even in case of strong rebound.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9868; (P) 0.9902; (R1) 0.9927; More...

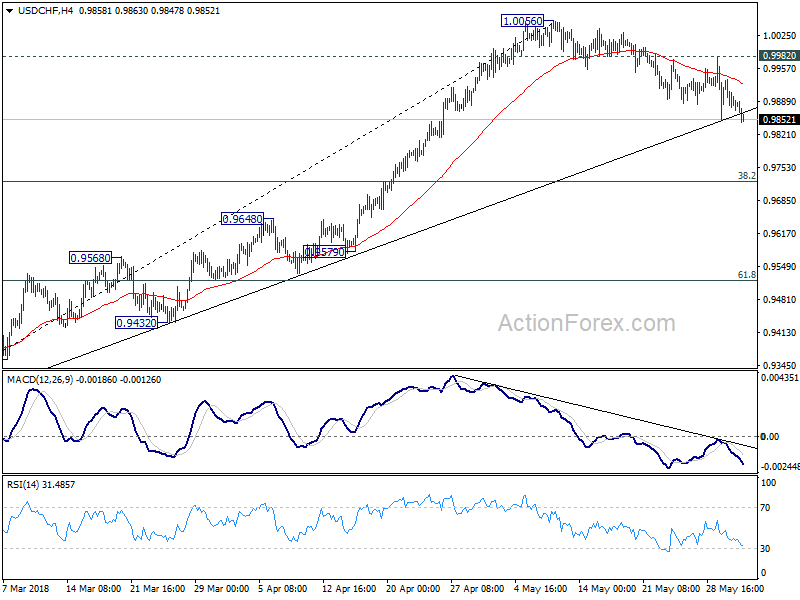

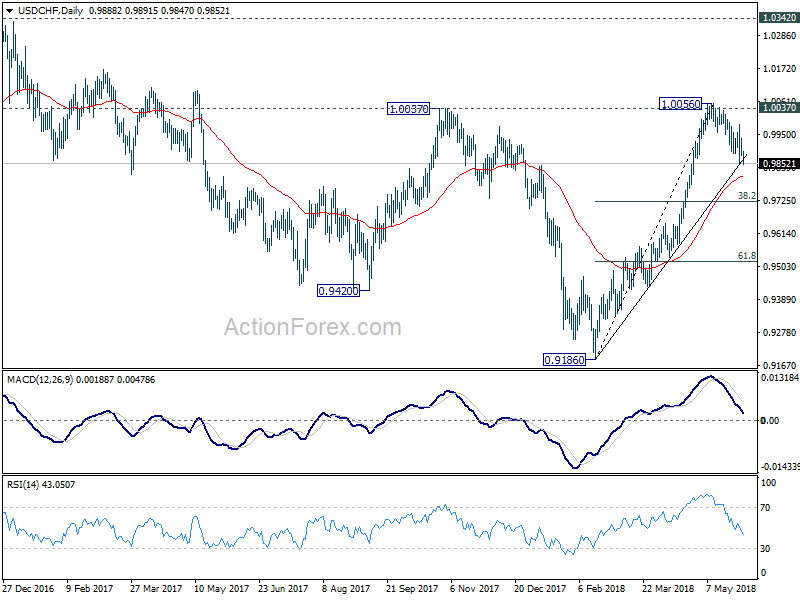

Intraday bias is back on the downside in USD/CHF with focus on trend line support (now at 0.9865). Sustained trading below there will indicate that fall from 1.0056 is a larger scale correction, correcting rise from 0.9186. And deeper fall would be seen back to 0.9724 fibonacci level before completion. Though, rebound from current level, followed by break of 0.9982 minor resistance will bring retest of 1.0056 high.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.47; (P) 108.78; (R1) 109.20; More...

Intraday bias in USD/JPY remains neutral as consolidation from 108.10 temporary low is still in progress. Another recovery cannot be ruled out. But upside should be limited by 109.82 resistance to bring fall resumption. Below 108.10 will target 61.8% retracement of 104.62 to 111.39 at 107.20. Break will likely resume larger decline from 118.65 for a new low below 104.62.

In the bigger picture, USD/JPY remains bounded in medium term falling channel from 118.65 (2016 high). The development. Current deeper than expected fall from 111.39 argues that fall from 118.65 is not finished. Break of 104.62 low would target 98.97 or even below. Though, break of 111.39 will revive the case that fall from 118.65 has completed and turn focus to 114.73 for confirmation.

Trump Escalates Trade Tension by Imposing Steel Tariffs on Allies EU, Canada and Mexico

Euro has been strong most of the day as Italian political risk temporarily receded. Stronger than expected Eurozone CPI reading also provided some support to the common currency. But it's Yen that's taking the spotlight again in early US session on risk aversion. DOW opened losing triple digits and stays in red after US announced the decision on steel and aluminium tariffs on Canada, Mexico and the EU. The temporary exemption will expire at midnight. 25% tariffs on steel and 10% on aluminum will then be imposed. For now, Canadian Dollar is having the biggest reaction to the decision with USD/CAD trading back above 1.2950. The pair could have its sight back on 1.3 handle.

US Commerce Secretary Wilbur Ross said earlier that "if there is an escalation it will be because the EU would have decided to retaliate." No matter whether Ross believes in what he said or not, the tension has already escalated. And now it's time for the EU, Canada and Mexico to announce their retaliation in response to escalation of trade tension by the US.

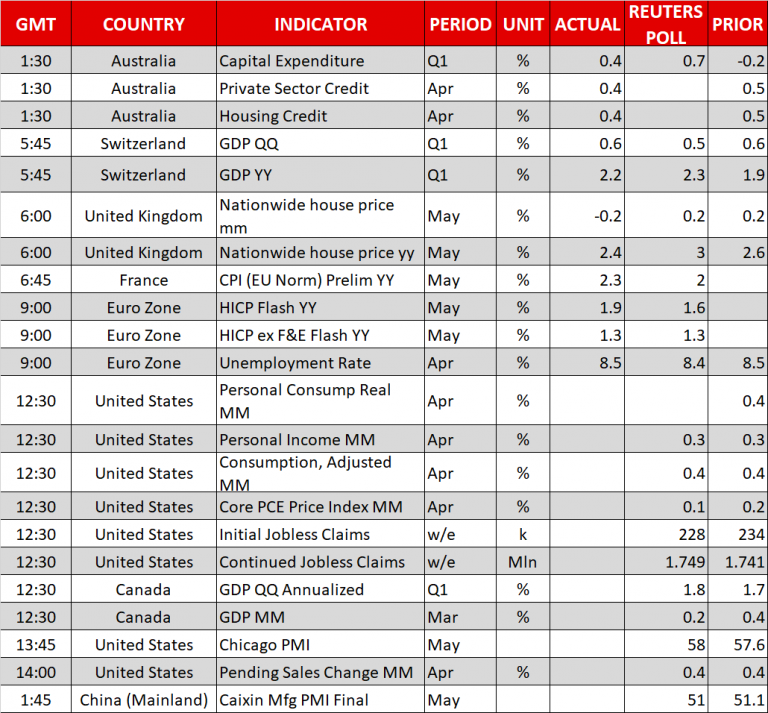

Released from US, personal income rose 0.3% in April, matched expectation. Personal spending rose 0.6%, above expectation of 0.4%. Headline PCE deflator rose 0.2% mom, 2.0% yoy, in line with consensus. Core PCE rose 0.2% mom, 1.8% yoy in April, versus expectation of 0.1% mom, 1.8% yoy.

Initial jobless claims dropped -13k to 221k in the week ended May 26 versus expectation of 230k. Four week moving average rose 2.5k to 222.25k. Continuing claims dropped -16k to 1.726m in the week ended May 19. Four week moving average of continuing claims dropped -8.5k to 1.7435m, lowest level since December 1973

From Canada, GDP grew 0.3% mom in March, in line with expectation.

German Merkel: We'll have smart, determined and jointly agreed response to US steel tariffs

German Chancellor said today in Lisbon that European Union will give a "smart, determined and jointly agreed" response to the US is Trump decides to impose steel and aluminum tariffs on them.

She noted "we don't know the decision yet but if tariffs were to be imposed, then we have a clear stance within the European Union." And she added "we are convinced that these tariffs are not in line with WTO rules."

The temporary exemption of US steel and aluminum tariffs will expire tomorrow. It's widely reported that US will decide to start imposing tariffs on Mexico, Canada and the EU. And the decision would be announced today.

Euro maintains gain as CPI rose to 1.9%, beat expectation

Flash Eurozone CPI accelerated to 1.9% yoy in May, up from 1.2% yoy and came in well above expectation of 1.6%. Core CPI rose to 1.1% yoy, up fro 0.7% yoy and beat expectation of 1.0% yoy. Unemployment was unchanged at 8.5% in April, above expectation of 8.4%.

Reactions in the Euro is relatively muted as the higher than expected inflation was actually expected after upside surprise in both German and French CPI reading. Nonetheless, the solid rebound in inflation in Q2 should have eased much of ECB policy makers' worries. The data add to the case for completing the asset purchase program this year. The question is whether it would end after September. President Mario Draghi could give some hints at the June 14 press conference.

Also released in European session, Swiss GDP rose more than expected by 0.6% qoq in Q1. Swiss retail sales dropped -2.2% yoy in April, below expectation of -1.4% yoy. UK mortgage approvals dropped to 62k in April. UK M4 money supply rose 0.2% mom in April.

China official PMI manufacturing rose to 51.9 as part of short-term fluctuation

The China official PMI manufacturing rose to 51.9 in May, up from 51.4, and beat expectation of 51.4. PMI non-manufacturing rose to 54.9, up from 54.8 and beat expectation of 54.8. In the release, contributing analyst Zhang Liqun noted that the slight increase in PMI was just "short-term fluctuation" and carries "no trend significance". The rise in export orders showed there is no chance in the growing trend. Rise in purchase prices and ex-factory prices suggested that the decline in PPI could be coming to an end. In short, the data suggested that the economy continued to grow steadily in May.

Released from Japan, industrial production rose less than expected by 0.3% mom in April. Housing starts rose 0.3% yoy.

ANZ business confidence: Fairly uninspiring reading

New Zealand ANZ business confidence dropped to -27.2 in May, down from -23.4. That is, a net 27% of businesses are pessimistic about the year ahead. Views on their "own activity" also dipped from 18 to 14. ANZ noted in the release that "the survey made for fairly uninspiring reading this month, with all aggregate activity indicators flat to falling. The economy still has good tailwinds in the form of fiscal stimulus and the record-high terms of trade, but may be tiring nonetheless." Meanwhile, ANZ's composite growth indicator, a combination of business and consumer confidence, is consistent with around 2% y/y growth.

Released from Australia, private sector credit rose 0.4% mom in April as expected.

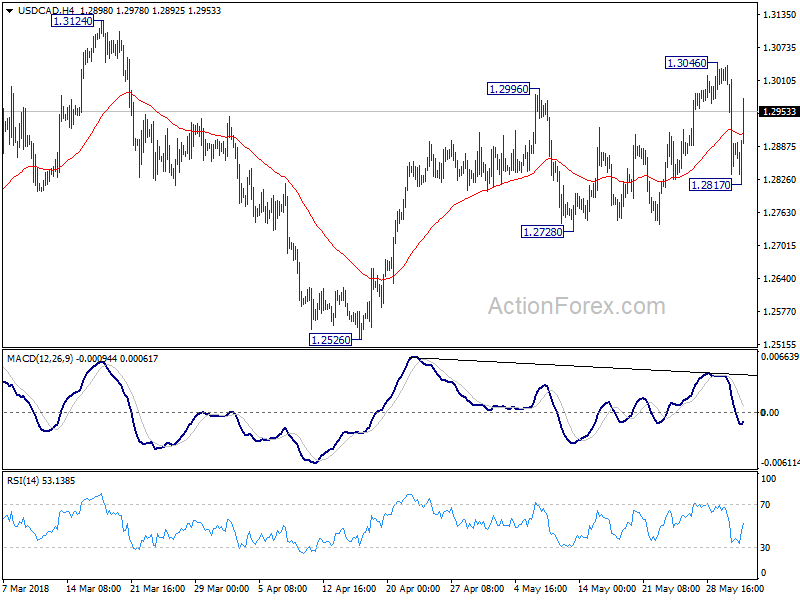

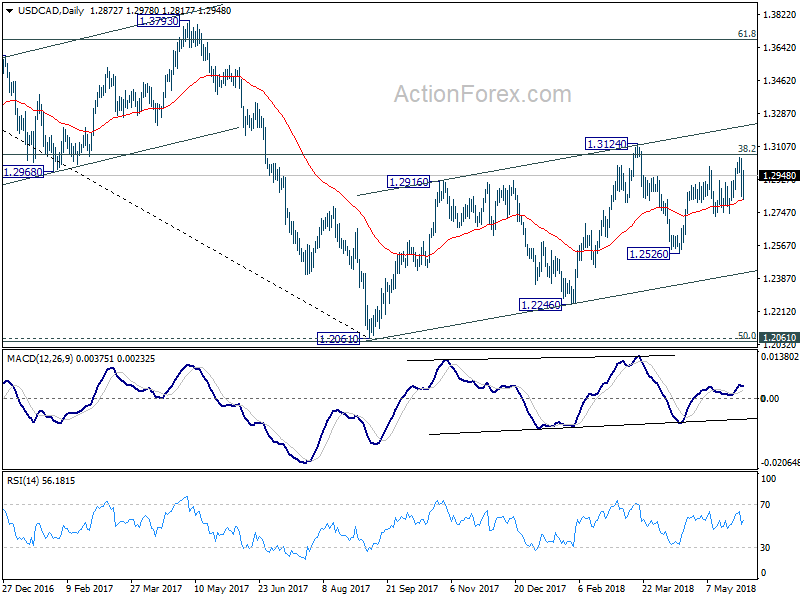

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2977; (P) 1.3013; (R1) 1.3056; More.....

USD/CAD rebounds strongly after hitting 1.2817, as supported by 55 day EMA, and intraday bias is turned neutral again. With 1.2728 support intact, our bullish view is kept alive and focus is back on 1.3045. Break will resume the rise from 1.2526 and target 1.3124 key resistance. Decisive break there will confirm medium term reversal. Nonetheless, break of 1.2728 will indicate completion of the rebound from 1.2526 at 1.3046. And in that case, deeper fall would be seen back to 1.2526 and below.

In the bigger picture, we're favoring the case that that rebound from 1.2061 has not completed yet. But there is no follow through upside momentum so far. Focus remains on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence May | -7 | -8 | -9 | |

| 23:50 | JPY | Industrial Production M/M Apr P | 0.30% | 1.40% | 1.40% | |

| 01:00 | NZD | ANZ Business Confidence May | -27.2 | -23.4 | ||

| 01:00 | CNY | Manufacturing PMI May | 51.9 | 51.4 | 51.4 | |

| 01:00 | CNY | Non-manufacturing PMI May | 54.9 | 54.8 | 54.8 | |

| 01:30 | AUD | Private Sector Credit M/M Apr | 0.40% | 0.40% | 0.50% | |

| 05:00 | JPY | Housing Starts Y/Y Apr | 0.30% | -8.90% | -8.30% | |

| 05:45 | CHF | GDP Q/Q Q1 | 0.60% | 0.50% | 0.60% | |

| 07:15 | CHF | Retail Sales Real Y/Y Apr | -2.20% | -1.40% | -1.80% | -1.10% |

| 08:30 | GBP | Mortgage Approvals Apr | 62K | 63K | 63K | |

| 08:30 | GBP | Money Supply M4 M/M Apr | 0.20% | -1.10% | -1.40% | |

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 8.50% | 8.40% | 8.50% | 8.60% |

| 09:00 | EUR | Eurozone CPI Estimate Y/Y May | 1.90% | 1.60% | 1.20% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y May A | 1.10% | 1.00% | 0.70% | |

| 12:30 | CAD | GDP M/M Mar | 0.30% | 0.30% | 0.40% | |

| 12:30 | USD | Personal Income Apr | 0.30% | 0.30% | 0.30% | 0.20% |

| 12:30 | USD | Personal Spending Apr | 0.60% | 0.40% | 0.40% | 0.50% |

| 12:30 | USD | PCE Deflator M/M Apr | 0.20% | 0.20% | 0.00% | |

| 12:30 | USD | PCE Deflator Y/Y Apr | 2.00% | 2.00% | 2.00% | |

| 12:30 | USD | PCE Core M/M Apr | 0.20% | 0.10% | 0.20% | |

| 12:30 | USD | PCE Core Y/Y Apr | 1.80% | 1.80% | 1.90% | 1.80% |

| 12:30 | USD | Initial Jobless Claims (26 MAY) | 221K | 230K | 234K | |

| 13:45 | USD | Chicago PMI May | 62.7 | 58 | 57.6 | |

| 14:00 | USD | Pending Home Sales M/M Apr | -1.30% | 0.50% | 0.40% | |

| 14:30 | USD | Natural Gas Storage | 100B | 91B | ||

| 15:00 | USD | Crude Oil Inventories | -0.4M | 5.8M |

Trump to impose steel and aluminum tariffs on Canada, Mexico and the EU, effective midnight

Trump administration announced to put tariffs on steel and aluminum imports from Canada, Mexico and the EU. That will come into effect as the temporary exemption expires at midnight. Tariffs on steel imports are 25% and that on aluminum is 10%.

Commerce Secretary Wilbur Ross criticized that NAFTA negotiations are "taking longer than we had hoped". While talks with EU have "made some progress", they haven't gone far enough to warrant more relief from tariffs.

Ross added that "we look forward to continued negotiations both with Canada and Mexico on the one hand, and with the European Commission on the other hand, because there are other issues that we also need to get resolved."

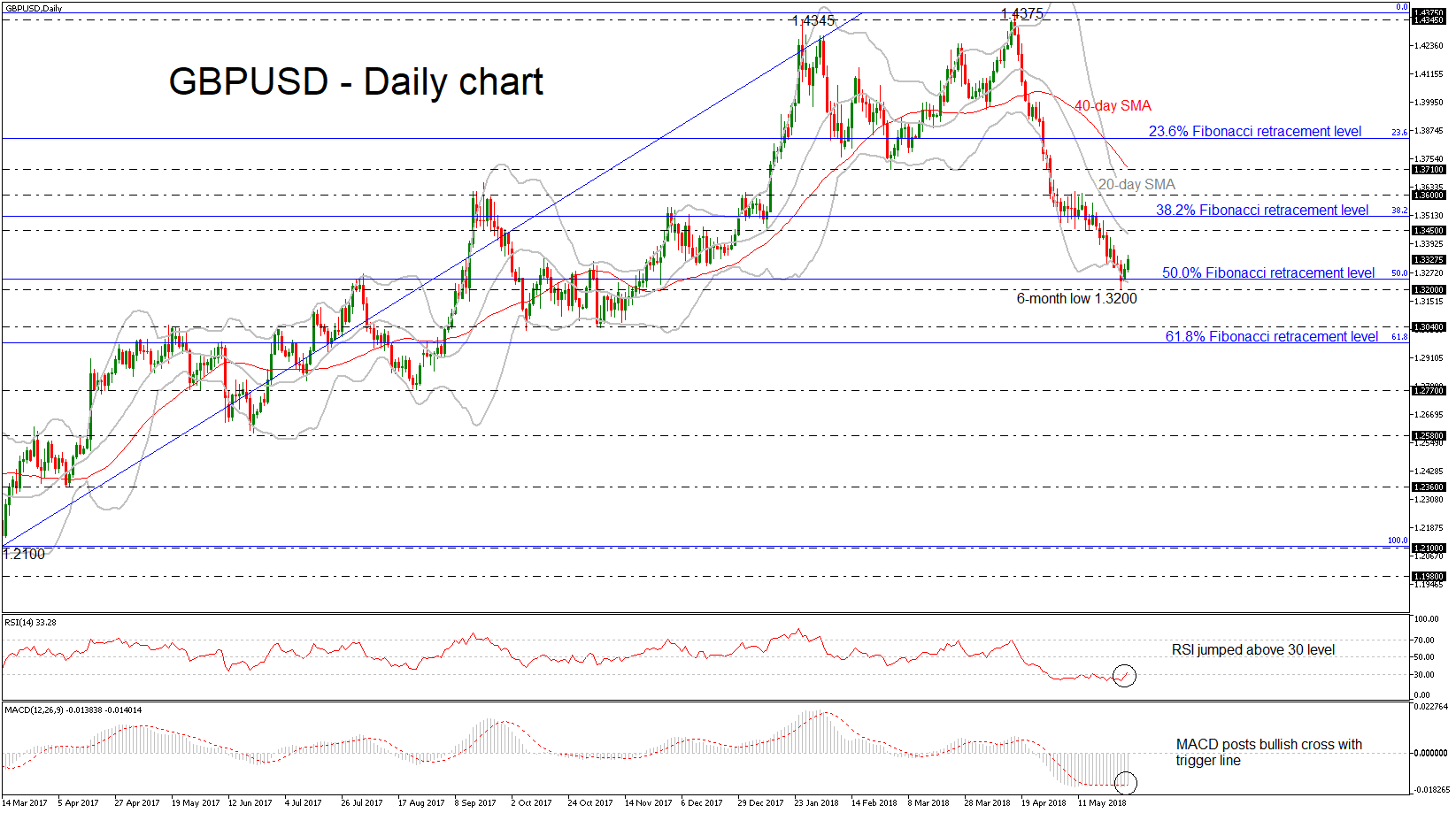

GBPUSD Recovers after Touching 6-Month Low; Next Level to Watch 1.3450

GBPUSD has advanced after the pullback on the six-month low near the 1.3200 psychological level. The price started Wednesday’s trading session above the 50.0% Fibonacci retracement level of the upleg from 1.2100 to 1.4375, suggesting that the market would increase bullish movements.

Looking at momentum indicators, the RSI is moving higher, having crossed above the 30-oversold level. In addition, the MACD oscillator is moderately rising and posted a bullish crossover with its trigger line.

In the wake of positive pressures, the market could meet resistance at the mid-level of the Bollinger Band (20-day simple moving average) near the 1.3450 barrier. A successful close above this region could see a retest of the 38.2% Fibonacci near 1.3510, while in case of further gains, the 1.3600 handle would come into scope.

Conversely, a move to the downside and below the aforementioned six-month low could see the 1.3040 support. Should the market increase negative momentum below this area, the 61.8% Fibonacci of 1.2973 could be the next level in focus.

Turning to the medium-term picture, the market seems to be in bearish mode given that the pair trades below the moving averages.

US PCE core unchanged at 1.8% yoy, initial jobless claims at 221k

A batch of economic data coming from the US. Personal income rose 0.3% in April, matched expectation. Personal spending rose 0.6%, above expectation of 0.4%.

Headline PCE deflator rose 0.2% mom, 2.0% yoy, in line with consensus.

Core PCE rose 0.2% mom, 1.8% yoy in April, versus expectation of 0.1% mom, 1.8% yoy.

Initial jobless claims dropped -13k to 221k in the week ended May 26 versus expectation of 230k. Four week moving average rose 2.5k to 222.25k. Continuing claims dropped -16k to 1.726m in the week ended May 19. Four week moving average of continuing claims dropped -8.5k to 1.7435m, lowest level since December 1973

From Canada, GDP grew 0.3% mom in March, in line with expectation.

Reactions are muted as the markets await US decisions on steel and aluminum tariff temporary exemptions.

Euro Holds Up On Political Relief, US Core PCE Inflation Ahead

Here are the latest developments in global markets:

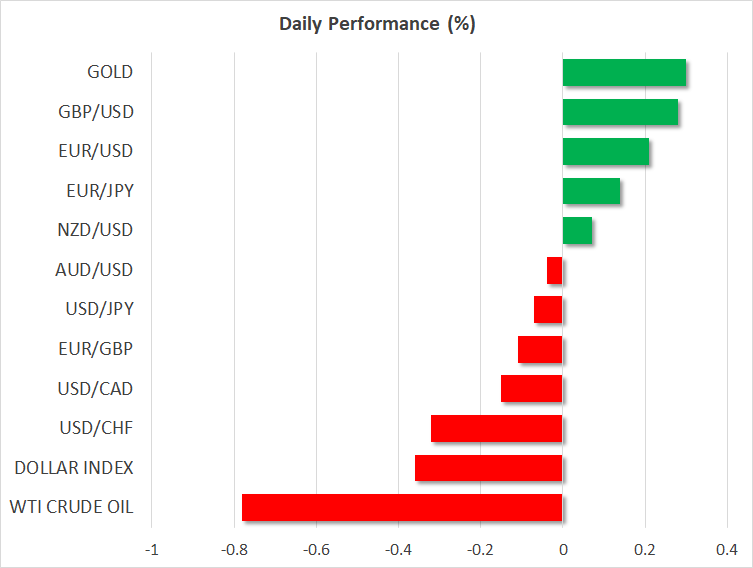

FOREX: The euro extended its gains on Thursday by 0.33% against the US dollar as Italian bond yields fell amid signs that Italy is trying to form a government, potentially avoiding an early election. In terms of data, the Eurozone CPI rose by 1.9% y/y in May above April’s growth mark of 1.2%, while the unemployment rate decreased to 8.5% in April, following an upwardly revised 8.6% in March, compared with the forecast of 8.4%. Dollar/yen moved lower by 0.06% at 1100 GMT, while the US dollar index is set to post the second red day in a row (-0.34%). Pound/dollar advanced by 0.33% and jumped above the 1.3300 handle following the rebound from a 6-month low on Tuesday. The antipodean currencies traded mixed with aussie/dollar down at 0.7574 (-0.03%) and kiwi/dollar slightly up, near the 3-week high of 0.7003 (+0.07%). Dollar/loonie recorded one of the biggest sell-off days in two weeks yesterday after the BoC’s more-hawkish-than-expected rate statement. Today, the pair dipped by 0.21% to 1.2841.

STOCKS: European stocks were moving up at 1100 GMT except the German DAX 30 as the Italian political environment calmed due to new plans for a coalition government. The benchmark European STOXX 600 and the blue-chip Euro STOXX 50 inched up by 0.14% and 0.05% respectively. The German DAX 30 dived by 0.47%, weighed by consumer cyclicals and utilities, while the French CAC 40 gained 0.18%. The Spanish IBEX 35 increased by 0.45% and the British FTSE 100 edged up by 0.16%. Futures tracking US stock indices were flashing green, pointing to a positive open after a strong bullish day.

COMMODITIES: West Texas Intermediate (WTI) and Brent crude oils dropped on Thursday, after the aggressive rally in the previous session, weighed on by a surprise increase in US API crude oil inventories. There is a possibility that OPEC and other producers may increase output at the June 22 OPEC meeting. WTI plunged by 0.79% to $67.67 and Brent dipped by 0.53% to $77.09. In precious metals, gold prices traded higher by 0.31%, jumping above $1,300 again.

Day ahead: US personal spending, personal income and core PCE index in the spotlight; Canadian GDP growth pending

US personal income and personal spending figures as well as the Fed’s favorite inflation measure, the core Personal Consumption Expenditure index (PCE), will take center stage in the remainder of the day. April’s stats due at 1230 GMT, are expected to show no change in personal spending and income, with the former rising by 0.4% m/m and the latter by 0.3%, as in March. Forecasts for the core PCE index though, suggest a moderate slowdown to a growth of 1.8%y/y compared to a rise of 1.9% in March, the highest mark recorded since July 2012. In case the data surprise to the upside – especially on the consumption front – the dollar could benefit on speculation that the Fed would be more prepared to raise interest rates at least two more times this year. Investors will also take a look at the US Chicago PMI and pending home sales at 1345 GMT and 1400 GMT respectively.

However, gains on the dollar could prove short-lived if uncertainties around US trade protectionism heighten ahead of Friday’s deadline for a waiver from US import tariffs on steel and aluminum. The US had temporarily exempted Canada, Mexico, and the EU from metal import tariffs a month ago, postponing the imposition until June 1. But yesterday a report by the Wall Street Journal stated that Washington was not planning to give away a permanent exemption to its EU counterparts. The announcement on the matter is expected to come later today at a time when the US Commerce Secretary, Wilbur Ross, is preparing to hold a second round of trade talks with Beijing this weekend. Tensions with China intensified yesterday as well, after China responded to US trade threats, saying that it will fight back if the US is looking to start a trade war. On Tuesday, Trump signaled he would move on with new import tariffs on China as a step to protect US intellectual property rights.

Meanwhile regarding the North Korean story, US and North Korean officials are meeting in New York to discuss the future of Pyongyang’s nuclear program as well as a potential summit between the US President, Donald Trump, and the North Korean leader, Kim Jong Un which was canceled by Trump last week. The two-day meeting will conclude today.

In Canada, the focus will turn to GDP growth readings due at 1230 GMT after the Bank of Canada left interest rates unchanged at 1.25% as expected but surprisingly appeared more hawkish on the path of future rate hikes, dropping some cautious wordings from the rate statement. Analysts believe that the economy expanded by 1.8% q/q on an annualized basis in the first quarter of the year, faster than in the previous quarter when it grew by 1.7%. Month-on-month, though, they anticipate GDP growth to ease from 0.4% to 0.3% in March. In case the numbers overcome forecasts, the loonie could extend its rally.

In Italy, political updates will continue to affect the euro as the markets await the League’s leader, Matteo Salvini, to announce whether he is willing to renew efforts to form a new government with the Five-Star Movement, a proposal made on Wednesday by the leader of the Five Star Movement party, Luigi Di Maio. Spain’s political drama is another headwind to the euro. On Friday, the Spanish Prime Minister, Mariano Rajoy will face a no-confidence vote against him, with the parliamentary debate starting from today.

In oil markets, the Energy Information Administration will deliver its weekly report on US oil inventories at 1500 GMT. Projections are for US crude oil inventories to post a decline in the week ending May 25.

As of today’s public appearances, BoC Deputy Governor Sylvain Leduc will be speaking about the Economic Progress Report at 1635 GMT, while at 1700 GMT, Fed Board Governor Lael Brainard, will be commenting at the Forecaster’s Club of New York luncheon. A G7 meeting between finance ministers and central bankers with a theme “Investing in Growth that Works for Everyone” will be also in focus. The meeting is scheduled to conclude on June 2.

Early on Friday at 0130 GMT, Asian traders will see the release of the Chinese Caixin Manufacturing PMIs.

Risk Appetite Remains as Italian Talks Continue

- Markets Remain Buoyed By Potential Progress in Italy;

- Euro Rebounds on Prospect of No Second Election;

- Plenty of US Data on the Agenda.

US futures are trading flat ahead of the open on Thursday, with Europe mostly a little higher as negotiations continue to avoid another election in Italy.

Not too long ago, a coalition government in Italy consisting of two eurosceptic populist parties was a feared and unlikely prospect that many believed would majorly concern investors. While much of this remains true, it is also currently viewed as the least unattractive and feasible outcome for markets, with the other alternative being fresh elections and the possibility that the parties are given an even stronger and potentially less euro-friendly mandate.

Italy's President, Sergio Mattarella, may have believed he was acting in the best interest of the country when he rejected to populists choice of Finance Minister but the reality is that in doing so, he has given both parties more ammunition with which to attack the euro. Mattarella has already been accused of acting on behalf of Germany and others while Brussels has been accused of interference, it all feeds very well into the eurosceptics message that the country no longer even has control over its domestic politics.

Should the country move straight on to another election, both Five Star Movement and Lega will look to take advantage of any fury linked to perceived meddling and could significantly add to their numbers. All of a sudden, the worst case scenario prior to the election looks tolerable compared to what could come from another. With both parties now in discussions again, there is a hope that the political impasse can be resolved which is helping to lift sentiment in the near-term. That said, a positive outcome now poses many further risks in the long-term.

While Italian assets have bore the brunt of the pain from the latest period of political instability and uncertainty, there has been a negative impact on the wider markets including the euro which dropped to a 10-month low against the dollar. While we're still far away from the days of the debt crisis and the risk of a breakup, a second election was being portrayed as a vote on the euro which seems drastic and probably overhyped but it certainly hit the single currency.

We've seen the euro bounce back over the last 24 hours although it has come off its highs this morning in response to the higher than expected unemployment reading. Interestingly, inflation did come in above expectations at 1.9% overall and 1.1% on a core basis although this appears to have been largely shrugged off.

There's plenty more data to come today with inflation, income, spending, jobless claims, pending home sales and the Chicago PMI due from the US. We'll also hear from some Federal Reserve policy makers – James Bullard, Lael Brainard and Robert Kaplan – which will be of interest ahead of the meeting in two weeks, at which the central bank is widely expected to raise interest rates for the second time this year.

European Markets: The Rebound Is In Town | Gold In Familiar Territory

- Investors are set to build on gains and pick up the momentum from Wall Street

- Focus remin on protection, trade war and tariffs

- Weakness in dollar working for gold

The Euro is in the green territory so the European markets. Investors are set to build on gains and pick up the momentum from Wall Street. In simple terms, the optimism around the Italian government has brought the bulls back in the market. The FTSE MiB has been under tremendous selling pressure and when there is such a strong steep sell-off, opportunities represent themselves.

This doesn’t mean that the political situation over in Italy is smooth now. Of course not, it is only a siesta time. Investors have gone in wait and see more while bargain hunters want to jump on the bandwagon because prices are out of whack.

One can always hope that the Italian political situation would take a direction under which both parties; The Five Star Movement and The League can keep their differences to a level which can save the borrowing cost for the country - the bond yields, below the record levels.

Over in the US, investors have their focus on protection, trade war and tariffs. Speaking of tariffs, the deadline is looming under which the US has to decide about its waiver of steel and aluminium tariffs on the EU. It is more than likely that he will kick the can down the road because taking any aggressive measure right now will only elevate the tensions between the US and the EU. Perhaps, that may not be the best policy because the current relationship between the US and the EU is already being tested due to the ongoing sanctions situation in Iran.

The price territory is very familiar when it comes to the gold price, there seems to be no strong reason which can anchor the demand for the precious metal. The dollar index has given up some of its gains and this is working in favour of gold price. However, the upcoming inflation data remain a gauge of significant importance. Any uptick in US core PCE index would surely add fuel for the dollar rally as the bar is already set low. The forecast is for 0.1% while the previous reading was at 0.2%.