Sample Category Title

Investors Eye Payrolls, Wage Growth Expected To Rise

The U.S. dollar was seen trading flat on Thursday as investors prepared for Friday’s payrolls report. On the political front, the U.S. steel and aluminum tariffs go into effect from Friday. Canada, Mexico and the EU are some of the economies that would be hit by the new tariffs.

EU officials vowed to retaliate against the tariffs which once again raise the specter of a full-blown trade war. On the economic front Canada's GDP increased 0.3% on the month which was better than expected. In the U.S. the core PCE price index showed a 0.2% increase on the month while both personal spending and income grew better than expected.

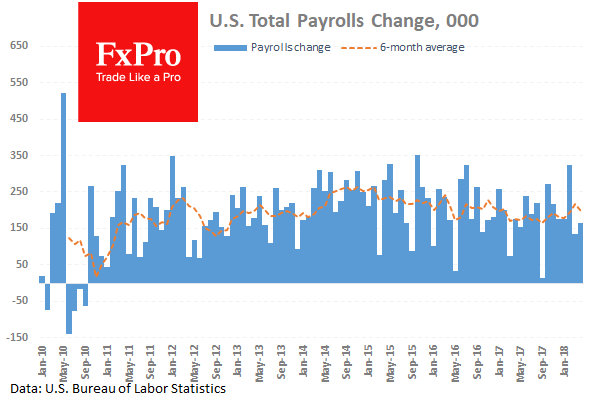

Investors will be geared into the U.S. nonfarm payrolls report that will be released later today. Economists forecast that the U.S. unemployment rate was steady at 3.9% while estimating that the average number of job gains during May increased 189k. This marks a slightly higher print compared to 164k jobs added in April. Wage gains are expected to accelerate at a pace of 0.3% on a month over month basis.

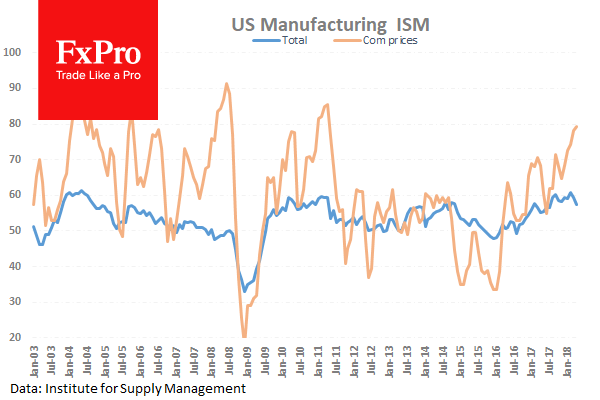

Following the payrolls report, the monthly ISM manufacturing PMI data is expected to be released. Estimates show a rebound in manufacturing activity from 57.3 in April to 58.2 in May.

Data from the Eurozone will see the release of the manufacturing PMI including that from the UK.

Will you be trading the NFP this coming Friday? Register now for our Live NFP Webinar, coming to you before, during and after the release!

Currencies: Easiest Part Of Euro Rebound Behind US?

Rates: Focus on US eco data as Italian political deadlock ends?

The Italian political deadlock ended yesterday evening with a new government sworn in today. We don’t expect a strong relief rally as last week revealed vulnerabilities of (peripheral) government bond markets. Attention could shift to US eco data today with the June 13 FOMC meeting already in mind. The escalating trade conflict is a wildcard.

Currencies: Easiest part of euro rebound behind US?

Yesterday, EUR/USD rebounded temporary to 1.17, but the move stalled. We don’t expect much further support for the euro from the installation of a new government. US Payrolls might be mixed for the dollar. A further flaring up of the trade tensions might weigh slightly more on the euro than on the dollar.

The Sunrise Headlines

- US markets lost ground yesterday with the Dow Jones underperforming (-1%). Asian stock markets are mixed overnight with China underperforming. The Caixin manufacturing PMI stabilized at 51.1 in May.

- Italy’s 5SM and the far-right Lega clinched the approval of president Mattarella for the launch of a populist government, all but ending a political crisis that has gripped the country for nearly 3 months and spooked investors. (FT)

- David Davis is devising a new Brexit plan to break a talks deadlock by giving Northern Ireland joint EU and UK status as well as a border buffer zone so it can trade freely with both. (The Sun)

- Spain's Socialists have enough votes to oust PM Rajoy in a no-confidence vote set for today and replace him with party leader Pedro Sanchez. Reports were denied that Rajoy will resign to avoid defeat, thereby triggering elections. (BB)

- Fed Brainard suggested a policy path that moves gradually from modestly accommodative to neutral and, afterwards, modestly beyond neutral, consistent with sustaining strong labor market conditions and inflation around target.

- Canada and Mexico retaliated against the US decision to impose tariffs on steel and aluminum imports and the EU had its own reprisals ready to go, reigniting investor fears of a global trade war. (Reuters)

- Today’s eco calendar contains US payrolls, unemployment rate, average hourly earnings and the manufacturing ISM (US) / PMI (UK). Fed Kaplan and Kashkari speak.

Currencies: Easiest Part Of Euro Rebound Behind US?

Easiest part of EUR/USD rebound behind us

EUR/USD rebounded north of 1.17 yesterday as Italian-related tensions eased further, but the risk on trade petered out. A sharp rise in EMU inflation opened the door for the ECB to reduce its APP programme later this year. For now it didn’t help the euro. US data were good, but near expectations. Later, the US imposed tariffs on steel and aluminium from Canada, Mexico and the EU. There was no unequivocal reaction in global FX. EUR/USD settled in the upper half of 1.16. USD/JPY fell temporary, but closed the session little changed (108.82). The Canadian dollar reversed most of Wednesday’s post-BoC gains.

Asian markets are trading mixed this morning. The reaction to the rising trade tensions remain modest. The BOJ reduced buying of 5 and 10-y bonds in its regular operation (probably as it wants a slightly steeper yield curve). Interesting, the BOJ shift this time didn’t trigger any speculation on a more profound change in BOJ policy further down the road. The yen even declined slightly. USD/JPY rebounded north of 109. EUR/USD is losing a few ticks, indicating some cautious USD bid.

European investors will look for clues on what the policy of the new US government will mean for the budget and what position will take vis-à-vis the EU. After the recent relief rally, we expect investors to take some wait-and –see approach. It might be too soon for further euro gains on Italy. In the US, job growth is expected to rebound from 164K to 190K. A positive surprise might not be that evident. However, AHE (wages) might be at least as important as payrolls growth. For this indicator, consensus expectation (0.2% M/M) is not too high. Even so, it might not be that evident for the payrolls to raise market expectations on a more aggressive Fed at the June meeting. The impact of the trade tensions for global FX trading is diffuse. We hold the working hypothesis that it might be slightly negative for EUR/USD, but maybe also for USD/JPY. From a technical point of view, EUR/USD rebounded off the 1.1510/50 area, but didn’t regain any key technical level. We are not convinced on a protracted euro rebound yet. 1.1830 is first resistance ahead of the 1.1996/1.20 area which we consider not easy to break.

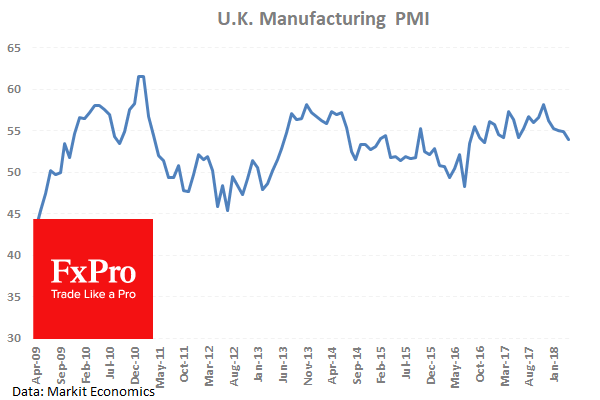

EUR/GBP drifted north yesterday, supported by the EUR/USD rebound. The manufacturing PMI is expected to ease slightly to 53.5 today. A big positive surprise is probably needed to support sterling. We expect sterling to remain relatively weak,

EUR/USD rebound slows ahead of first resistance

UK PMI manufacturing rose to 54.4, rebound far from convincing

UK PMI manufacturing rose to 54.4 in May, up from 53.9 and beat expectation of 53.5. Markit noted in the release that output growth ticks higher despite slower expansion of new work received. And, supply-chain constraints and cost pressures intensify.

Rob Dobson, Director at IHS Markit, which compiles the survey:

"At first glance, the mild acceleration in the rate of output growth and rise in the headline PMI would appear positive outcomes given the backdrop of the slowdown seen in manufacturing since the turn of the year. However, scratch beneath the surface and the rebound in the PMI from April's 17-month low is far from convincing.

"A slowdown in new order inflows meant the expansion in production was achieved only by firms working through their backlogs of work. Weaker than expected sales meanwhile led to the largest rise in unsold stock in the survey's 26-year history. This suggests that manufacturers have yet to fully adjust their production to the weakening trend in new business growth and there will need to be a rapid improvement in demand if output volumes are to be sustained in the coming months.

"Manufacturers will also likely be constrained if the resurgence in both cost inflation and supply-chain pressures becomes more firmly embedded. Input price inflation accelerated for the first time since January as general cost increases, often linked to higher oil prices, were exacerbated by shortages of certain inputs. Average vendor lead times – a key bellwether of supply-side constraints – lengthened to the greatest extent during 2018 so far. These price and supply headwinds, combined with a further slowdown in new order growth, could jeopardise any further expansion of the manufacturing sector."

Full release here.

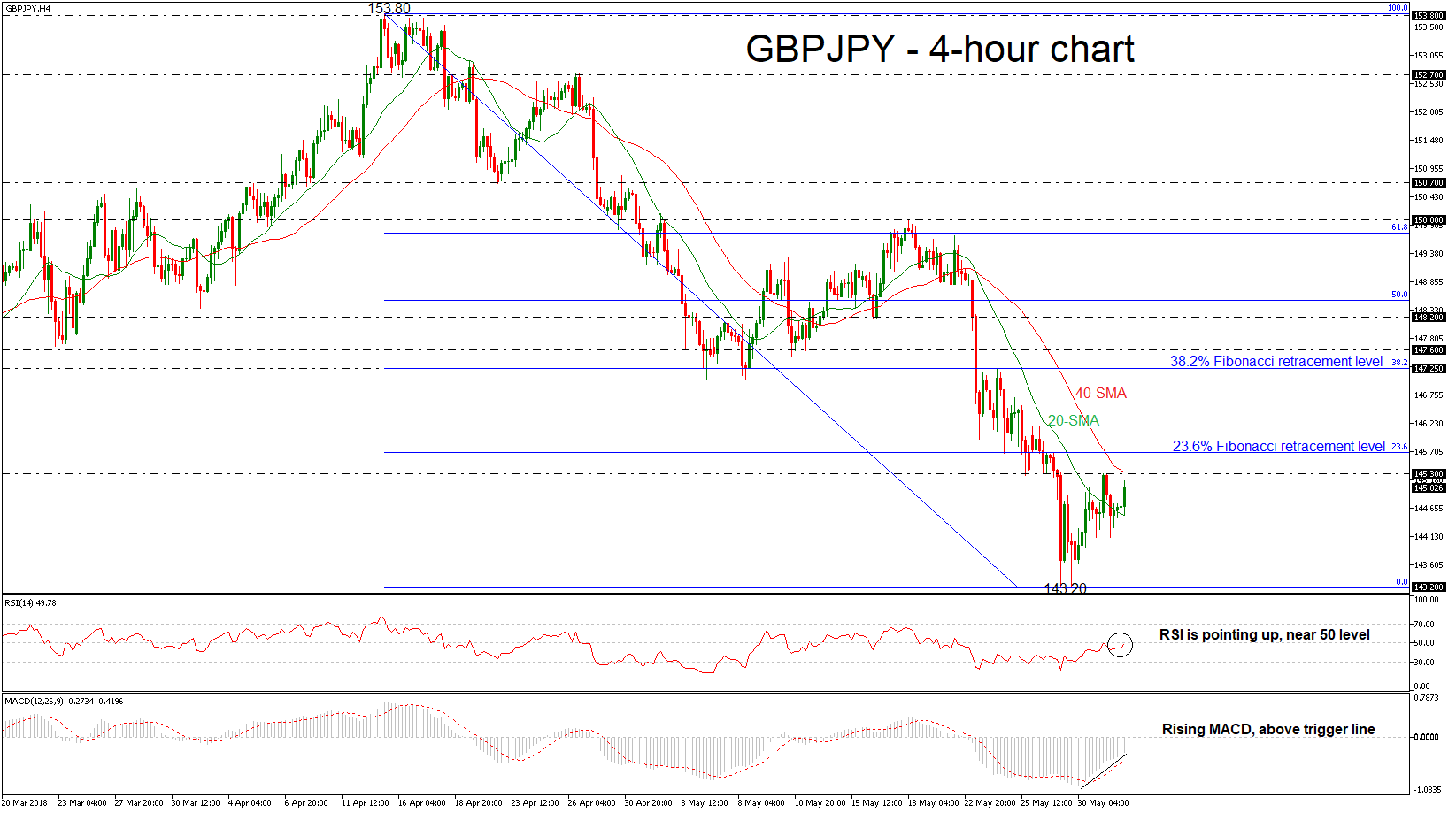

GBPJPY Turns Higher, Momentum Indicators Endorse Bullish Correction

GBPJPY is approaching again the 40-simple moving average (SMA) in the 4-hour chart after the strong rebound on the eight-month low of 143.20 that was reached on May 29. Moreover, the price successfully surpassed the 20-SMA and remains in positive territory.

From the technical point of view, the positive bias in the near term is further supported by the deterioration in the RSI indicator. The index is sloping slightly to the upside near the 50 level, while the MACD oscillator is edging higher above its trigger line but below the zero line.

If prices continue to head higher, resistance should come from the 145.30 hurdle. A climb above this area would reinforce the short-term bullish view and open the way towards the 23.6% Fibonacci retracement level of the downleg from 153.80 to 143.20, near 145.70. More upside movement would send the pair towards the 147.25 resistance, which coincides with the 38.2% Fibonacci.

However, should a downside reversal take form, immediate resistance will likely come from the 143.20 support. A break below this level could open the way for an extension of the bearish pressure, with the next support coming from the 141.20 region, identified by the September 2017 low.

In the medium-term, the pair is continuing the negative outlook after the bounce off the 153.80 resistance level on April 13.

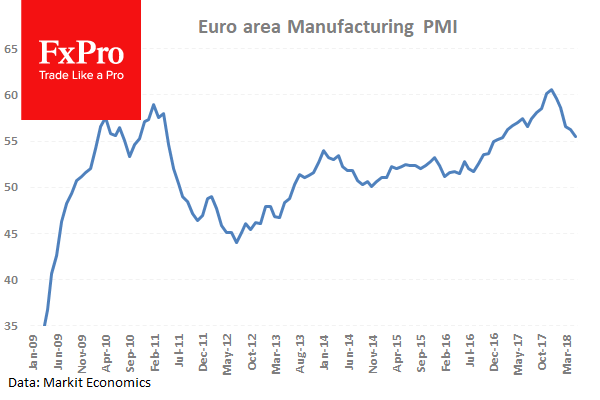

Eurozone PMI manufacturing finalized at 55.5, 15-month low

Eurozone PMI manufacturing was finalized at 55.5, unrevised from initial reading.

The Netherlands, Germany and Austria remain strongest performing nations despite some deterioration. Netherlands PMI manufacturing, despite hitting an 8-month low, was at 60.3. Austria PMI manufacturing hit 14-month low at 57.3. Germany PMI manufacturing hit 15 month low at 56.9.

Commenting on the final Manufacturing PMI data, Chris Williamson, Chief Business Economist at IHS Markit said:

Commenting on the final Manufacturing PMI data, Chris Williamson, Chief Business Economist at IHS Markit said:

"The eurozone manufacturing sector reported its weakest expansion for 15 months in May. Some of the weakness may have been related to a higher than usual number of holidays during the month, but risks appear tilted towards growth remaining subdued or even cooling further in coming months.

"Slowing export sales have been a key drag on both production and order book growth, with the May survey indicating that new export orders rose at the weakest rate for nearly two years, linked in part to the appreciation of the euro alongside reports of weakened demand for imports from key markets, notably the US.

"There are signs that the soft patch has further to run. Despite the production trend slowing markedly in recent months, the order book slowdown has been even sharper. Output has consequently grown at a faster rate than new orders in each of the past six months, which suggests that manufacturers will come under pressure to rein-in production and staffing levels in coming months unless demand revives. Not surprisingly, manufacturers' expectations of future production have sunk to a 20-month low, underscoring the gloomier economic picture."

Full release here.

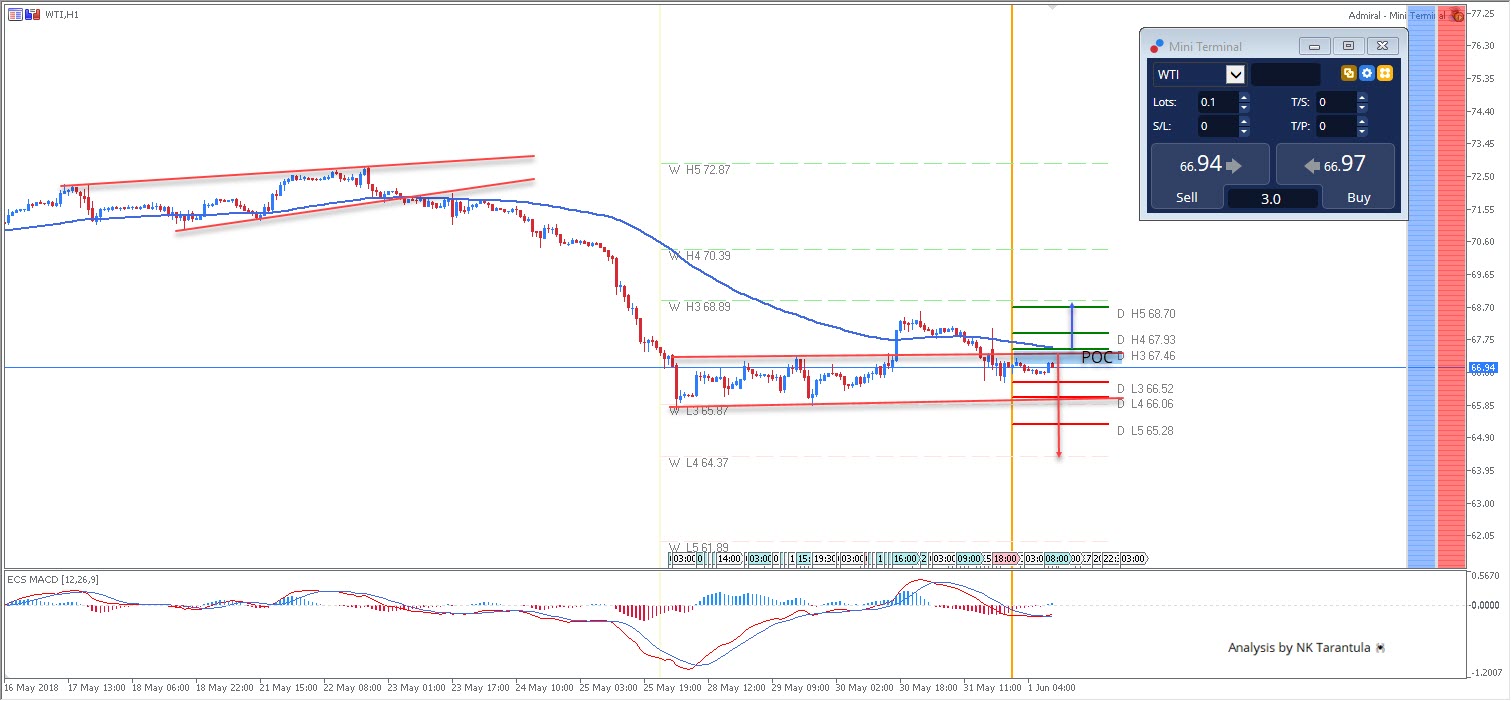

WTI Horizontal Channel Congestion Prior To Breakout

The WTI started a bearish move at the break of bullish wedge top and now it is trading within the horizontal channel. However, the price is currently below the EMA89 and MACD is below zero line so we might see another drop. 67.20-40 is the POC zone. Rejections from the zone should target 66.52 and 66.06. Below the channel targets are 65.28 and 64.37. However a spike above 67.55 will change the tide and targets are 67.93 and 68.70. This might likely happen on profit taking – if shorts start to close their positions today. Pay attention to the POC zone.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

U.S. And Europe Inflation Threats Troubling Markets

Tariffs pressure markets

On Thursday the markets failed to develop growth momentum. Investors favoured a cautious tone towards riskier assets as the US imposed import tariffs on Canada, Mexico and the EU. Initial reaction from the markets was subdued, as traders had already priced in such a move. With US inflation close to central bank targets the new tariffs could pose significant economic risks. The threat of a more vigorous increase in interest rates from the Fed becomes more of a reality. In addition to external factors, such as soaring energy prices and new tariffs, there are increased internal price drivers. On Thursday the Bureau of Economic Analysis reported an increase in consumer spending by 0.6% in April.

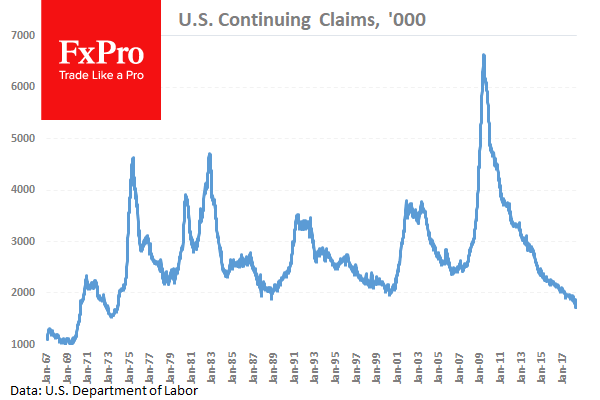

Unemployment Claims were lower than expected and that is another sign of a tight labour market where companies have to compete for workers. Whether this spike occurred in May will be revealed later today as wages data is released.

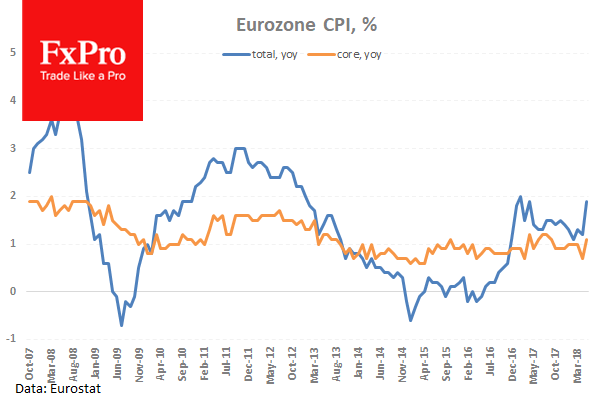

large euro area economies were marked by a powerful (by 0.4%-0.6%) prices increase, speeding annual inflation growth from 1.2% to 1.9%. Confirmation of this fact helped to pull EURInflation surge in Europe higher on Thursday, although it has not become such a surprise as it was on Wednesday. Core CPI (excluding food and energy) accelerated from 0.7% YoY to 1.1% YoY. It seems that inflation is returning to Europe much earlier than expected which could quickly lead to a tightening in the ECB’s rhetoric.

Renewed outflow from EM

Developing markets are responding negatively to the increase in global inflation resulting in Investors withdrawing money from emerging markets as the difference in profitability with American assets has continued to decline. TRY, MXN and RUB fell on Thursday, and remain under pressure early on Friday.

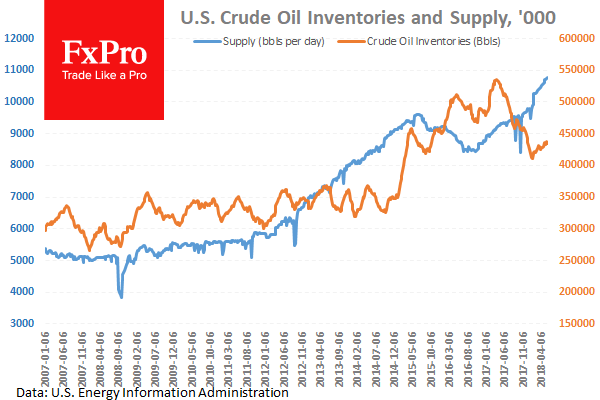

The growth in production has seen Oil prices experience downward pressure.

In addition to the increased demand for safe assets, pressure for Crude Oil increased after recent weekly data on U.S. inventories. Although inventories declined higher than expected by 3.6 mln. barrels , Crude Oil supply for the week grew from 10.73 mln. barrels per day to 10.77 man bpd. Following the data release Brent fell 2.8% to 76.90 but has since stabilised to trade around $77.40.

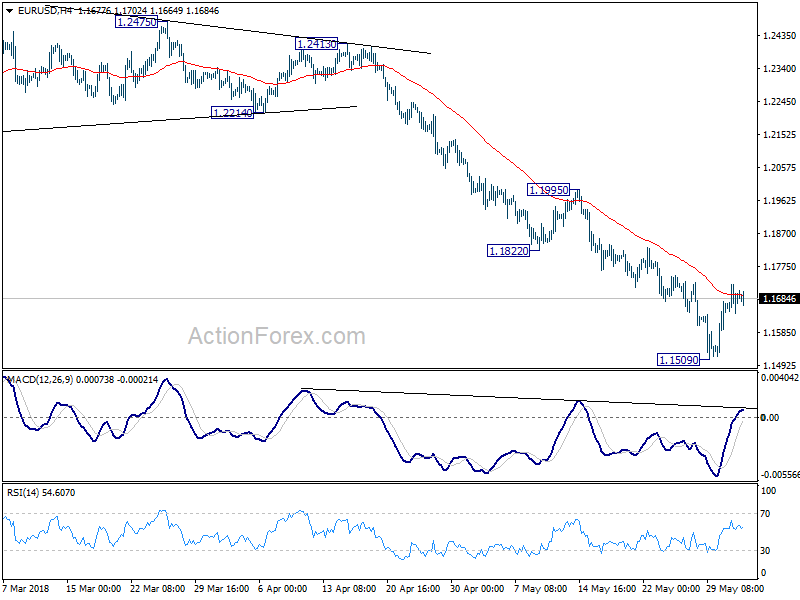

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1648; (P) 1.1686 (R1) 1.1732; More.....

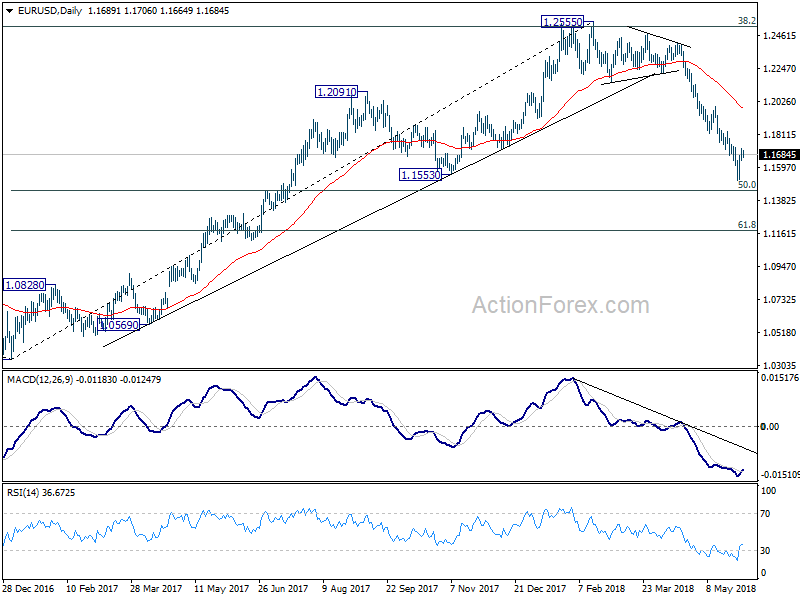

EUR/USD is staying in consolidation from 1.1509 and intraday bias remains neutral. Further rise cannot be ruled out. But upside should be limited by 1.1822/1995 resistance zone to bring fall resumption. Below 1.1509 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 first. Break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 1.1995 resistance holds.

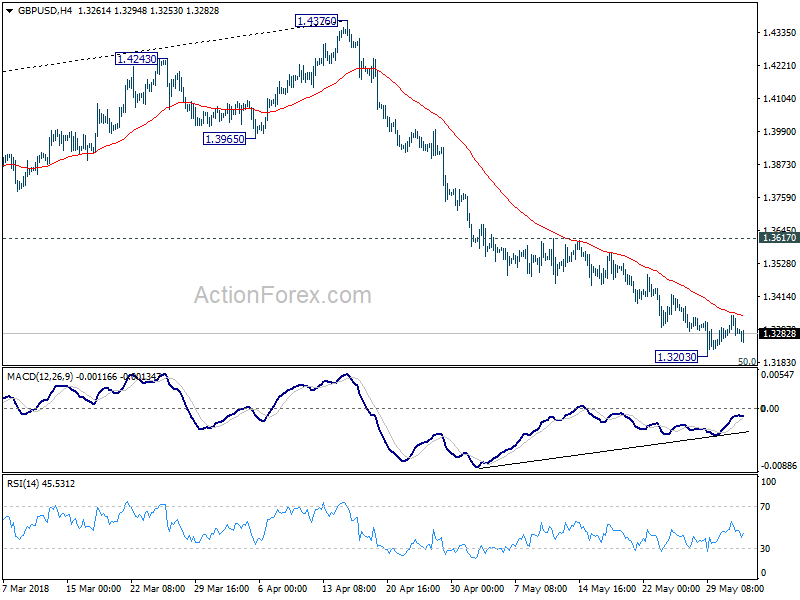

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3265; (P) 1.3306; (R1) 1.3336; More...

GBP/USD's consolidation from 1.3203 is still in progress and intraday bias remains neutral. Further recovery cannot be ruled out. But near term outlook will remain bearish as long as 1.3617 resistance holds. Fall from 1.4376 is expected to resume later. Below 1.3203 will target 50% retracement of 1.1946 to 1.4376 at 1.3161 first. Break will target 61.8% retracement at 1.2875 next.

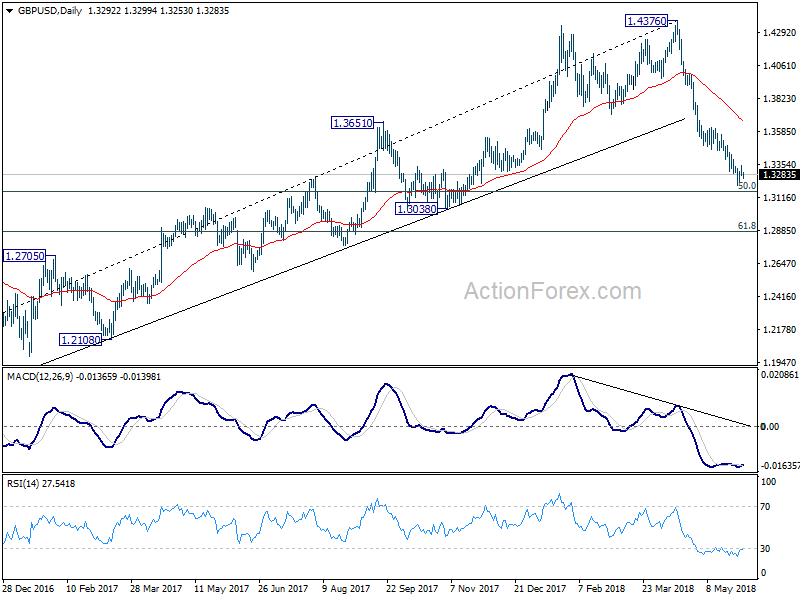

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken firmly, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4223). 61.8% retracement of 1.1936 (2016 low) to 1.4376 at 1.2874 is the next target. We'll pay attention to the reaction from there to asses the chance of long term down trend resumption. For now, outlook will stay bearish as long as 55 day EMA (now at 1.3730) holds, even in case of strong rebound.

European PMIs Set The Stage For US NFP And Earnings Today

The G7 is meeting today in Canada for a second day. Any comments made by participants can result in market moves.

At 07:55 GMT, German Markit Manufacturing PMI (May) is expected to be 56.8 against the previous 56.8. This data set seems to have peaked in January at 63.3, when it exceeded the 2011 high of 62.7. The last four readings have shown a softening in the data with an expectation for this reading to fall again today. EUR traders will be closely following this data release.

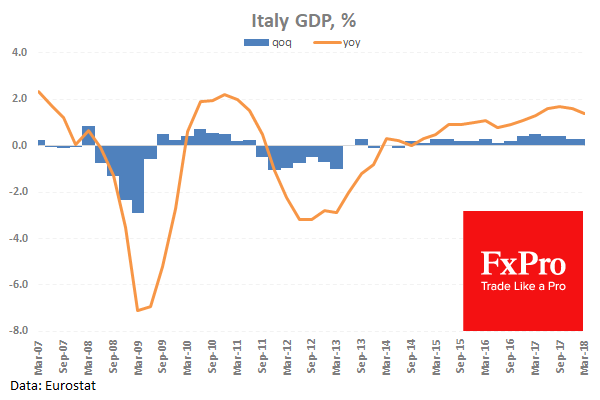

At 08:00 GMT, Italian Gross Domestic Product (YoY) (Q1) is expected to be 1.4% against the previous 1.6%. Gross Domestic Product (QoQ) (Q1) is expected to be 0.3% against the previous 0.3%. This data is more relevant given the spotlight on the Political crisis in Italy. The yearly reading is expected to show a softening in the data but the quarterly reading is expected to hold steady. EUR assets may see an increase in volatility following this data release.

At 09:00 GMT, Eurozone Markit Manufacturing PMI (May) is expected to be 55.5 against the previous 55.5. This data set reached its peak in January at 60.6, when it exceeded the 2011 high of 62.7. The last four readings have shown a softening in the data, indicating a slowing of the manufacturing industry is on the cards. EUR crosses can be impacted by this data release.

At 09:30 GMT, UK Markit Manufacturing PMI (May) will be out with an expected headline number of 53.5 and 53.9 prior. The consensus is for a reading generally in line with other releases this morning and for a further softening from the high created in December at 58.2. Slower output growth was a factor cited in the weakening number despite stronger new order inflows, strengthening job creation and demand. GBP pairs may see prices move following this data release.

At 12:30 GMT, US Non-Farm Payrolls (May) is expected at 188K from a prior 164K. This measures the change in the number of employed people in May. The Unemployment Rate (May) is expected at 3.9% with a prior of 3.9%. This measures the percentage of the total workforce unemployed and actively seeking employment during May. Average Hourly Earnings (YoY) (May) is expected to be 2.7% against 2.6% previously. Average Hourly Earnings (MoM) (May) is expected to be 0.2% against 0.1% previously. Average Weekly Hours (May) is expected to be 34.5 against a previous 34.5. Labour Force Participation Rate (May) is expected to be 62.6% against a prior reading of 62.8%. This data can have a large impact on markets as the tight labour market has yet to show its impact with an increase in earnings. This would lead to an increase in inflation which markets have reacted negatively to recently. USD crosses could experience volatility around these data releases.

At 13:30 GMT, Canadian Markit Manufacturing PMI (May) is expected to be 55.4 against the previous 55.5. This data set seems to have peaked in February at 55.9, when it matched the April 2017 number. The last four readings have shown a softening in the data with an expectation for this reading to fall again today. CAD pairs may see prices move after this data release.

At 14:00 GMT, US ISM Prices Paid (May) is due out with a consensus of 78.2 expected. The previous reading was 79.3 and this shows a slight drop in the cost of goods and services. ISM Manufacturing PMI (May) is also out at this time with an expectation for a number of 58.1 v 57.3 prior. This number is falling after reaching a high of 60.8 in February. USD crosses can be impacted by this data release following earlier US data and turbulent price action can result.

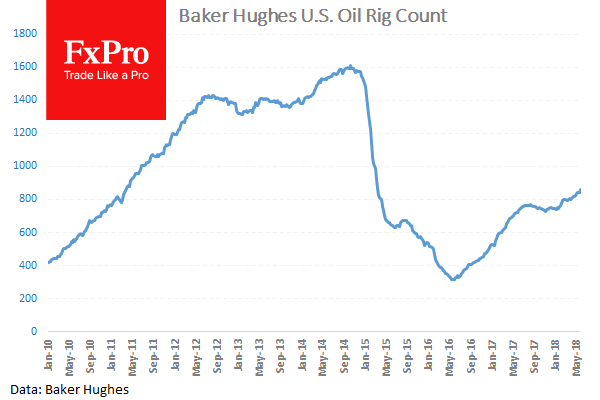

At 17:00 GMT, Baker Hughes US Oil Rig Counts is due to be released with a headline number from last week of 859. Oil prices fell last Friday with the announcement of a relaxing of production cuts but the increase in rig counts also added to the fall. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.