Sample Category Title

EUR/USD: US Durable Goods Orders

The Greenback weakened against the Eurozone's single currency, following the US Durable Goods Orders data release on Friday. The EUR/USD currency pair gained 2 pips, or 0.01%, to continue fluctuating in the 1.1655 area.

The Census Bureau simultaneously released two data sets, where Durable Goods Orders data came out lower-than-expected of negative 1.7%, which was one of the main reason for currency price to weaken.

In the contrary, Core Durable Goods Orders came out better-than-expected of 0.9%, which didn't let the EUR/USD currency pair to weaken too much, leaving the overall price fluctuations flat.

EURUSD Analysis: Pushed Lower By Political Turmoil In Italy

Bears took over the market on Monday, driven by political turmoil in Italy. As a result, the Euro weakened 1.00% against its American counterpart and thus had reached the 1.1607 level by mid-day. The remaining part of that session was spent with low volatility.

From technical point of view, the pair should recover both today and this week. The nearest resistance area is the 55– and 100-hour SMAs circa 1.1680, while the upper channel line and the 220-hour moving average are located near the 1.1750 area.

Nevertheless, fundamental developments in Italy are likely to drive this currency pair for the following trading sessions. In case of negative news, the bearish impact should push the pair down to its 6-1/2-month low or even the weekly S2 at 1.1550 and 1.1527, respectively.

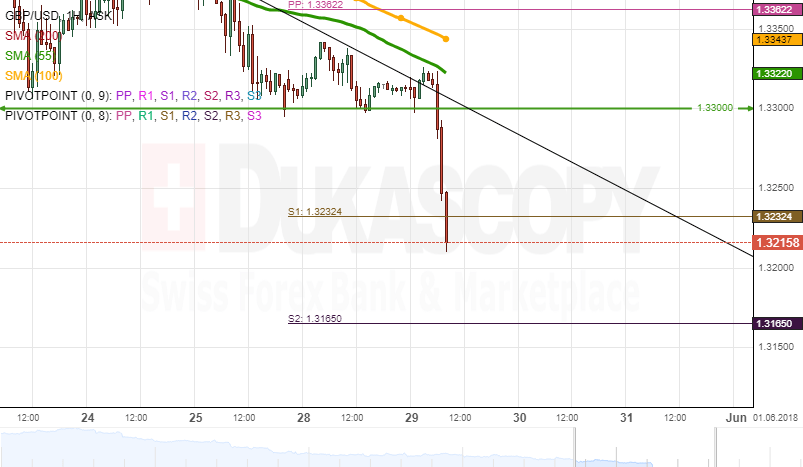

GBPUSD Analysis: Narrows Trading Range

Monday's trading session did not introduce significant changes to the overall price level of GBP/USD, as banks in both the UK and the US were closed. Thus, the pair remained stranded between the 55-hour SMA and its six-month low at 1.33 on Tuesday morning.

It is likely that the rate tries to approach the 1.36 mark within the following trading sessions. Strong appreciation today might be restricted by the combined resistance of the 55– and 100-hour SMAs and the weekly PP circa 1.3360. In case no strong upside momentum drives the Pound today, the 200-hour SMA at 1.34 should not be surpassed.

The 55-hour SMA might also pressure the rate lower past its six-month low; strong decline, however, should be limited near the 1.3250 mark

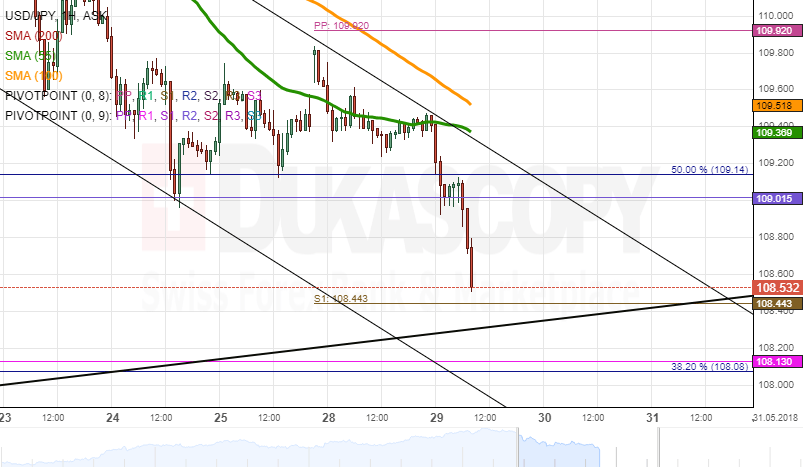

USDJPY Analysis: Fails To Surpass 55-Hour SMA

Monday's trading session was very calm for the USD/JPY exchange rate with the pair trading in an extremely narrow range slightly below the 55-hour SMA. This situation changed on Tuesday morning when risk-averse investors shifted their funds to the Yen as a safe-haven currency. Thus, the rate returned to its two-week low of 109.00.

It is more likely that the given pair falls even lower, as the 200-period SMA on the 4H chart was surpassed earlier in the day. This would push the rate closer to the weekly S1 near 108.50. This bearish scenario should likewise be confirmed by the US Dollar failing to surpass the 55– and 100-hour SMAs circa 109.50.

In case this area is breached, the rate should target the weekly PP or the 200-hour SMA at 109.90 and 110.20, respectively.

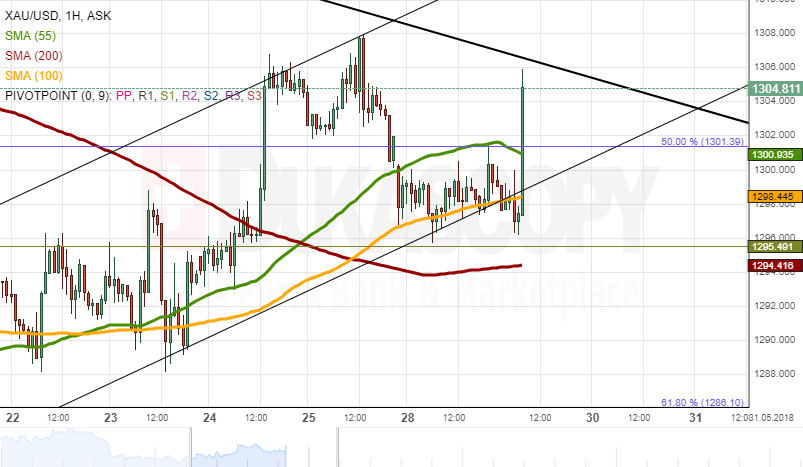

Gold Analysis: Moves Sideways

The yellow metal was trading sideways against the US Dollar on Monday stranded between the 55– and 100-hour SMAs. In addition, the pair was likewise moving along the bottom boundary of a junior two-week channel up.

The rate lingering near this line suggests that a downside breakout is likely to occur today. This would send the pair lower down to the 200-hour SMA at 1.294.00. This level might likewise be surpassed in case of sluggish US CB Consumer Confidence data at 1400GMT. The ultimate daily low should be 1,290.00.

Meanwhile, Gold moving above the 55-hour SMA should also result in a bullish breakout of the seven-week channel at 1,305.00. A subsequent surge is likely to follow, thus setting the 1.317.00 level as the next possible target.

Euro Retreat In Full Swing As Italian Political Uncertainties Dominate

Here are the latest developments in global markets:

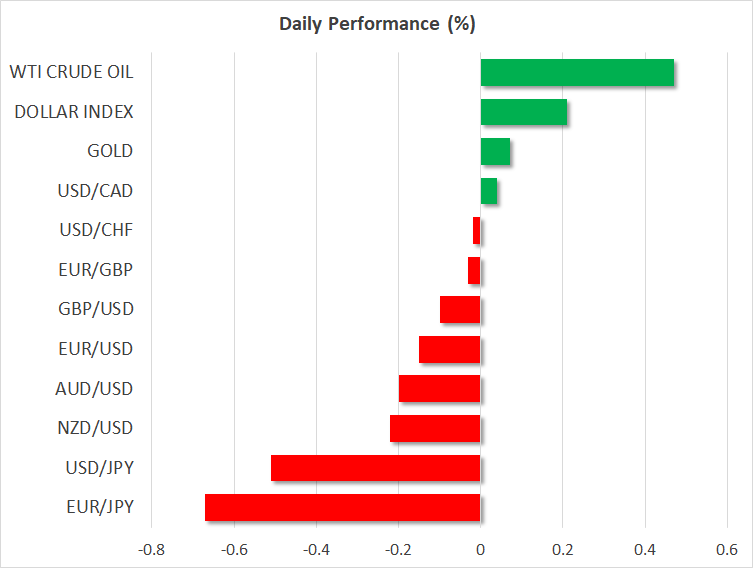

FOREX: The US dollar index – which tracks the greenback’s performance against a basket of six major currencies – edged 0.2% higher on Tuesday, touching its best levels since November. The euro meanwhile remained on the back foot, as the increasing probability for early elections in Italy dampened the currency’s appeal.

STOCKS: US markets remained closed on Monday in celebration of the Memorial Day holiday. They look set to open lower today, as futures tracking the Dow Jones, S&P 500, and Nasdaq 100 are all currently flashing red. The prospect for early elections in Italy appears to be overshadowing positive signals on the geopolitical front that the US-North Korea summit may still happen as early as next month. The negative sentiment was evident in Asia, where most markets closed lower. In Japan, the Nikkei 225 and the Topix fell by 0.55% and 0.48% respectively, as the yen’s recent surge will likely cloud the outlook for Japanese exporting firms. Meanwhile in Hong Kong, the Hang Seng was down by 0.92%. In Europe, futures tracking all the major indices were a sea of red, pointing to a much lower open for all these benchmarks today amid political uncertainties in Italy.

COMMODITIES: Oil prices are higher on Tuesday, with WTI and Brent climbing by 0.5% and 0.35% respectively, both recovering some of the astounding losses they posted on Monday and Friday. The losses came on the back of hints from Saudi Arabia and Russia that they could soon increase their production in order to offset any potential supply outages from Venezuela and Iran, pouring cold water on expectations for reduced supply in the market. In precious metals, gold is higher today, but by less than 0.1%. The metal has crossed back below the psychological $1,300 territory, after it met resistance at its 200-day moving average on Friday. Gold continues to remain unfazed by uncertainties in the European political spectrum, with investors seemingly preferring the Japanese yen as a safe-haven play.

Major movers: Euro continues to bleed on Italian politics; yen extends rebound

The single European currency continued its downfall on Monday, losing ground against all its major counterparts as the uncertainty surrounding the Italian political scene reached new peaks. It appears the nation will head to early elections, as the two anti-establishment parties abandoned their attempts to form a coalition government. This came after Italian President Mattarella rejected their proposed candidate for Economy Minister, who was seen as holding Eurosceptic views.

The market response of pushing the euro lower appears justified, as this story is shaping up to be one more existential threat for the Eurozone. In the event of early elections, Eurosceptic and populist parties could gain an even bigger share of the voting pie, increasing the risk that policies like calling a referendum on the euro start being discussed again in Eurozone’s third largest economy. Early elections are rumored to take place between August and September. Yields on Italian 10-year bonds raced even higher, touching highs last seen in 2014, as investors continued to flee the nation’s bond market.

As for the euro, while its longer-term outlook remains relatively bright, the currency’s near-term prospects continue to be clouded by a combination of political uncertainties, a European economy losing momentum, and an ECB that appears increasingly more cautious to normalize. More downside cannot be ruled out in the near-term, especially if the Italian political narrative remains at the forefront and the ECB remains “hesitant” to act.

Turning to the yen, which is perceived as a safe-haven asset, it has probably been the biggest beneficiary from uncertainties in Europe. Euro/yen is down nearly 0.7% on Tuesday, touching a fresh 11-month low. Meanwhile, dollar/yen is lower by 0.5% as well, even despite the dollar posting modest gains against other currencies.

In fact, the dollar index reached its highest level since November yesterday and is building on those gains today, climbing by another 0.2%. The latest surge may be viewed more as euro weakness rather than dollar strength, considering that the euro holds more than 50% of the weight in the dollar index.

Day ahead: US consumer confidence due; Italian politics and geopolitics closely monitored

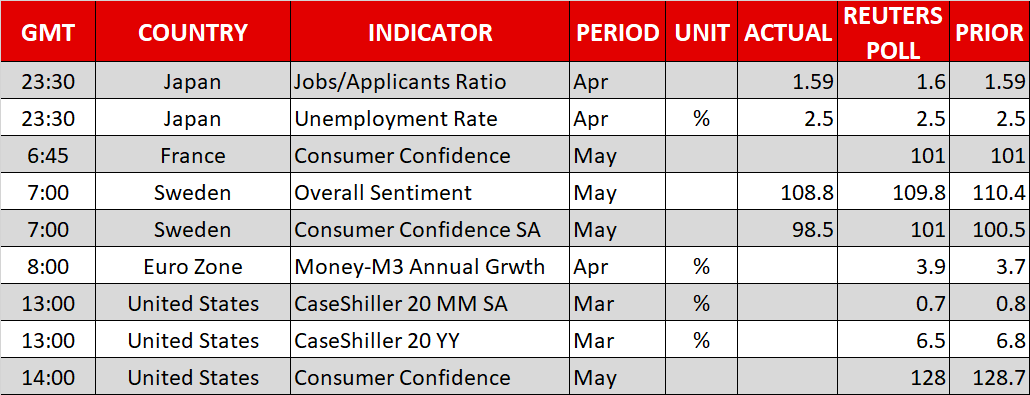

Tuesday’s calendar is relatively quiet in terms of releases, with consumer confidence data out of the US perhaps being the reading attracting most attention. Beyond economic data, the political situation in Italy and other geopolitical developments will be eyed; these maybe have the greatest capacity to act as market movers in today’s trading.

The ECB will be releasing monthly data on lending and money supply at 0800 GMT, while the Bank’s board member Sabine Lautenschlager will be speaking about monetary policy in Frankfurt at 1530 GMT; the city is hosting a Finance Summit.

Data on US housing prices for March as gauged by the CaseShiller indices will be made public at 1300 GMT, while consumer confidence figures out of the world’s largest economy are scheduled for release at 1400 GMT. The index measuring consumer morale is projected to fall to 128.0 in May, from April’s 128.7.

Italian President Sergio Mattarella’s decision to veto the 5-Star Movement and League’s nominee for the position of economy minister – on the grounds of him being a critic of the euro currency – was not well received by the two parties, which now seem to be preparing for fresh elections. The two anti-establishment parties have been gaining momentum lately and new elections may see them come out even stronger. The euro is expected to be sensitive to updates on the issue, which will be closely monitored by market participants.

In geopolitics, a US-North Korea summit may not be dead after all, with the parties involved seemingly making efforts to revive the Trump-Kim meeting. Meanwhile, the stage is set for more trade talks between the US and China in the day to come.

It is important to note that political and geopolitical developments are not just of interest to currency traders, but also to equity and fixed income ones.

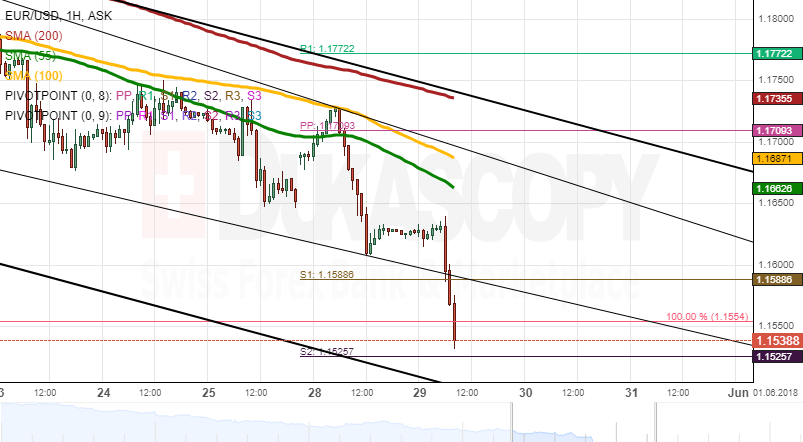

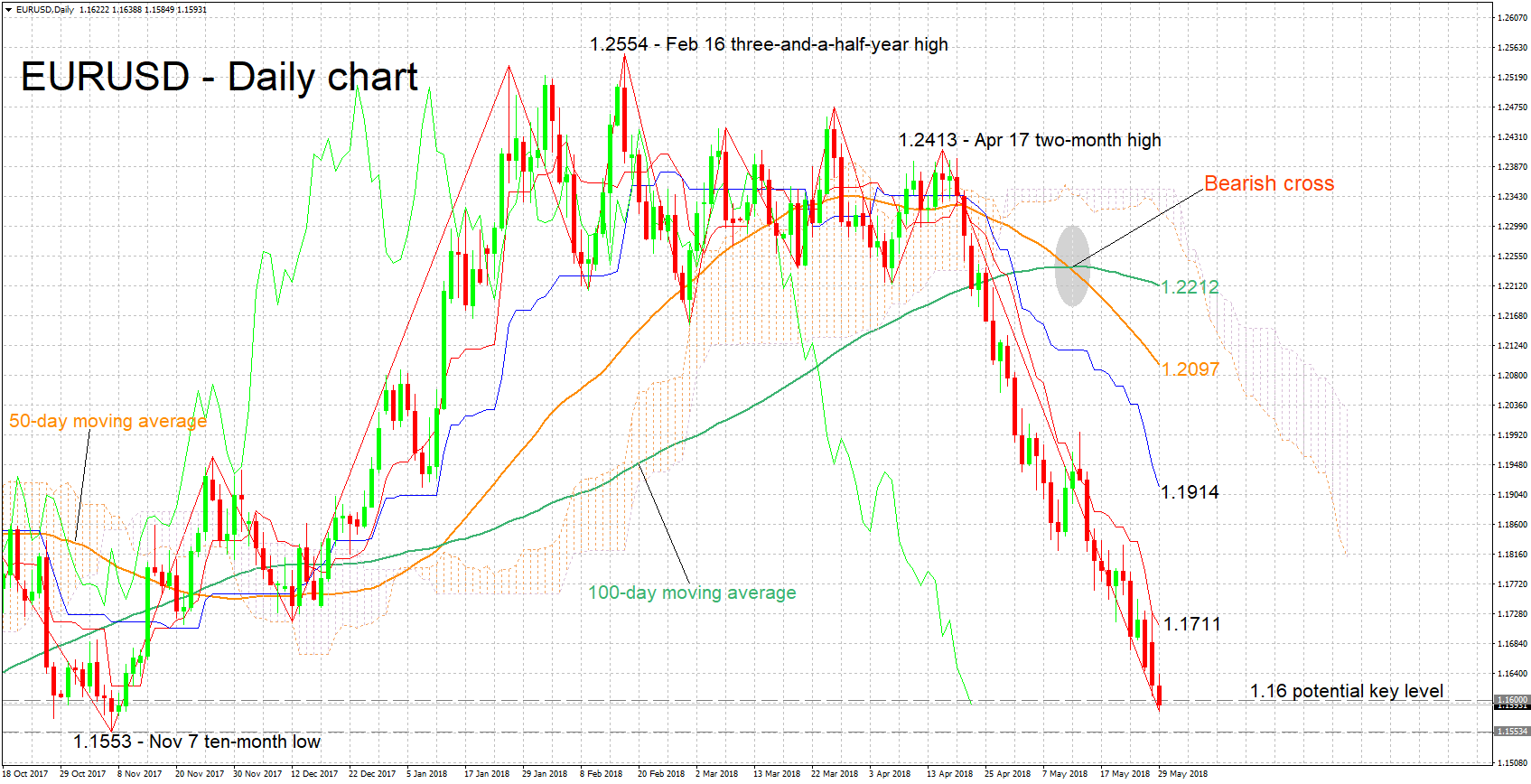

Technical Analysis: EURUSD hits near 7-month low; looking oversold

EURUSD fell to a near seven-month low of 1.1585 earlier on Tuesday, while it is currently trading not far above that nadir. The Tenkan-sen is below the Kijun-sen and both lines maintain a steep negative slope; this is indicative of the bearish short-term momentum. The Chikou Span, though, is pointing to an oversold market.

Developments in Italian politics that are seen as undermining the EU, and more specifically the eurozone, are likely to push the pair further down. Support to declines may come around the 10-month low of 1.1553 recorded in early November and further below from the 1.15 round figure.

Conversely, a (relatively more) euro-friendly outcome is expected to boost EURUSD. Resistance could be met around the 1.16 handle which failed to provide support earlier in the day and may instead act as a barrier to advances. Further above, additional resistance may come around the current level of the Tenkan-sen at 1.1711 (including the 1.17 mark).

US consumer confidence data and other US-related developments can also lead to positioning on the pair.

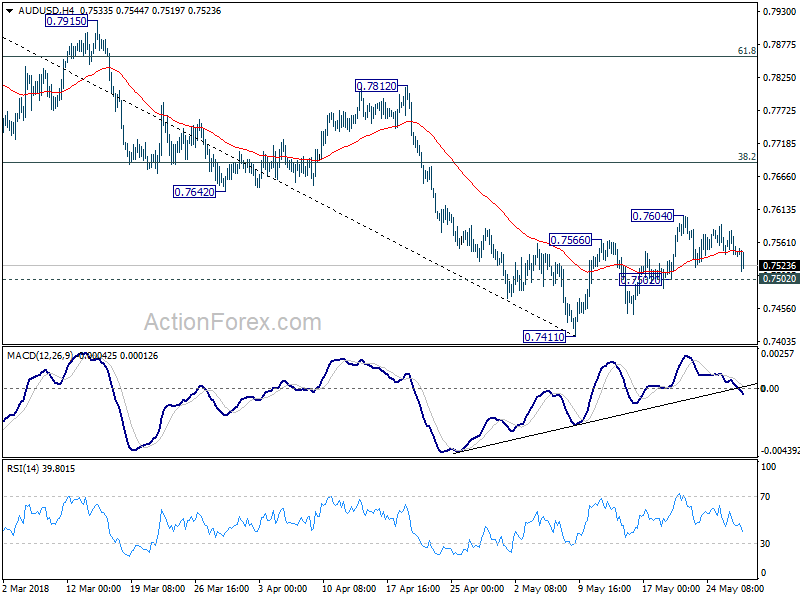

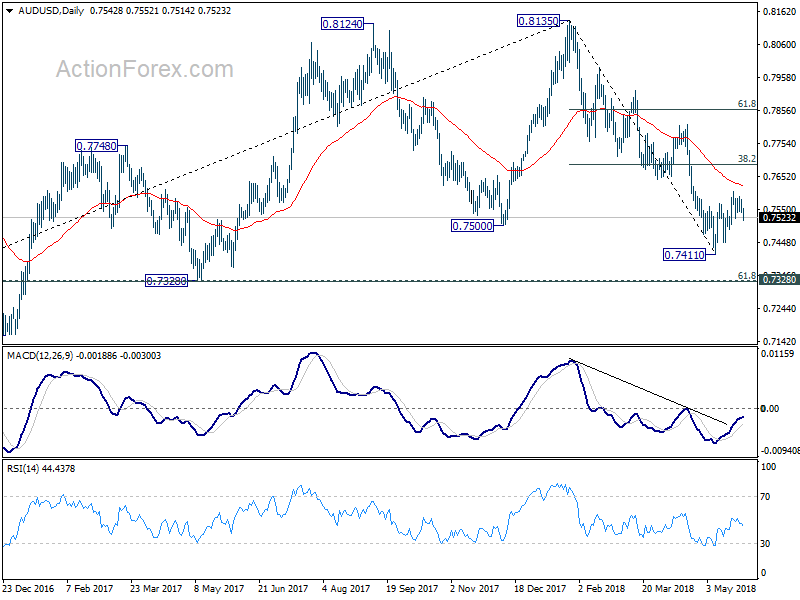

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7529; (P) 0.7560; (R1) 0.7578; More...

AUD/USD is staying in tight range between 0.7502 and 0.7604 and intraday bias remains neutral first. On the downside, break of 0.7502 minor support will suggest that the corrective recovery from 0.7411 has completed. Intraday bias would be turned back to the downside for 0.7411 and below to resume the larger decline from 0.8135 to cluster support at 0.7328 (61.8% retracement of 0.6826 to 0.8135 at 0.7326). Above 0.7604 will extend the corrective rise. But we'd expect strong resistance from 38.2% retracement of 0.8135 to 0.7144 at 0.7688 to limit upside.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

Prolonged Political Uncertainty in Italy Sparks Fear of Financial Market Contagion to Neighbors

(Updated on 0230 GMT, May 30) 10-year Italy-Germany yield spread jumped further to 2.83%, highest since 2013, on May 29.

Hopes of forming a populist coalition government in Italy hit the rocks as President Sergio Mattarella rejected eurosceptic Paolo Savona’s nomination as the next finance minister. Yet, he has invited Carlo Cottarelli, a former IMF official, to take the post of the prime minister and form an interim technocrat government that would lead the country to new elections. Giuseppe Conte, the prime minister-designate, quitted after the President’s veto. Euro initially jumped but gains were erased later in the day with EURUSD plunging to the lowest level since November 9, 2017. Italian bonds plummeted, lifting yields. The 10-year Italy-Germany yield spread widened to 2.34%, a level not seen since early February 2014, on Monday. It was remarkable jump from 2.05% last Friday. With both the UK and US closed for public holidays on Monday, the repercussion of the stalemate remains to be seen. What is certain is that the euro and Eurozone’s financial markets (peripherals in particular) would face huge volatility as we head to the new election.

President Mattarella’s decision has by no means helped alleviate the political turmoil. In his proposal, new elections would be held after the approval of the 2019 government budget, probably at the end of this year or the start of next year. However, a technocrat government would need approval from both houses of the parliament. Cottarelli, known as “Mr Scissors” for his cuts to the country's public spending in the past, would hardly win a vote of confidence in a parliament controlled by Five Star Movement (M5S) and the League (LN), the populist duo failing to form the coalition government. In this case, new elections would have to take place much earlier, say, around the end of the summer.

Worse still, new elections do not seem to be a way to resolving the current stalemate. Opinion polls indicate that support for LN has soared since the March election. Poll of polls has shown that as of May 25, support for the party has risen to 23%, compared with the 17% of votes the party secured at the March election. Support for M5S has stayed largely unchanged at 32%. Concerning other major parties, supports for the Democratic Party (PD) and Forza Italy (FI) came in at 18% and 12%, compared with 19% and 14%, respectively, at the March election. This signals that new elections would likely again result in a hung parliament and require M5S and LN to form a coalition government, recurring what has happened after the March election. Political situation in Italy would remain uncertain for a considerable time.

The most disastrous part of the European sovereign debt crisis back in 2009 was the contagious effect in peripheral economies. The latest selloff in Italian bonds has shown initial signs of spreading to other peripheral economies. The chart below illustrates the rapid widening of yield spreads between peripheral bonds and German bund.

Take a look at another parameter- Credit Default Swaps (CDS). Italy’s debt insurance costs in the 5 -year CDS jumped to a one-year high of 175.24 bps on Monday, while those for Spain and Portugal have risen to highest levels so far this year. Spain has its own political difficulties as the country might hold an early election in coming months. Prime Minister Mariano Rajoy’s minority government is having great challenge as it struggle to pass the 2018 budget in the Parliament. The current economic and financial situation is much better than the one a decade ago and we see the chance of falling back to a debt crisis remote. Yet, instability has high chance to delay ECB’s schedule to normalize its accommodative policy.

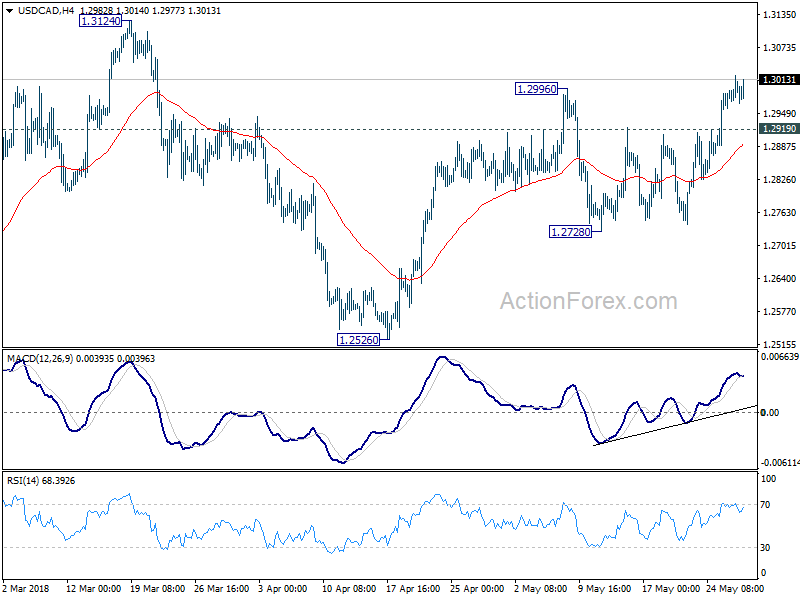

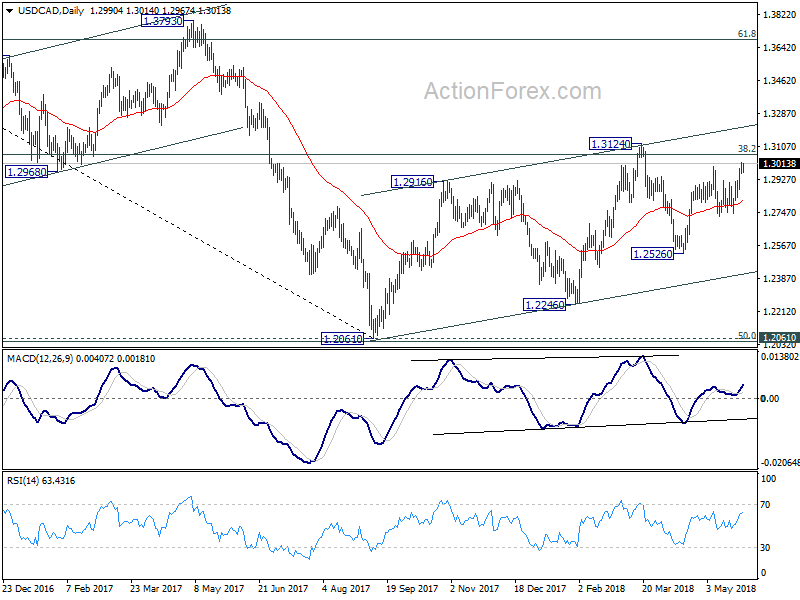

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2961; (P) 1.2994; (R1) 1.3026; More.....

Intraday bias in USD/CAD remains on the upside for the moment. Rise from 1.2526 has just resumed and should target a test on 1.3124 resistance next. Decisive break there should confirm medium term trend reversal. On the downside, below 1.2919 minor support will dampen the bullish view and turn bias neutral again.

In the bigger picture, we're favoring the case that that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

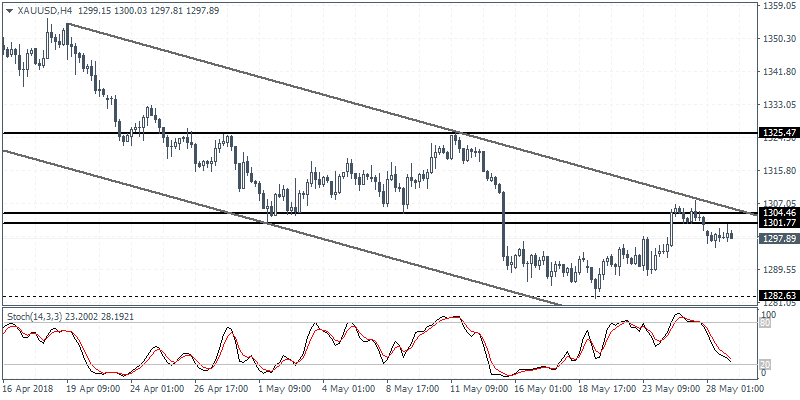

XAUUSD Intraday Analysis

XAUUSD (1297.89): Gold prices were broadly muted on Monday with price action trading below the resistance level of 1304 - 1301 level. Failure to breakout above this level has kept price action muted with the potential to test the lower support at 1282 once again. To the upside, only a strong close above 1304 level could trigger an upside correction. The resistance level at 1325 is expected to be the next level of target.