Sample Category Title

St. Louis Fed Bullard urged caution on further rate hike with three reasons

St. Louis Fed President James Bullard urged caution on further rate hike in near term in a presentation at a seminar in Tokyo.

And he laid out three reasons for discussions.

First, market-based inflation expectations in the U.S. remain somewhat low.

Second, the current level of the policy rate appears to be neutral, meaning it is putting neither upward nor downward pressure on inflation.

Third, the U.S. nominal yield curve could invert later this year or in 2019, which would be a bearish signal for U.S. macroeconomic prospects,.

Italy: A Crisis In The Making ?

Italy: A Crisis in the making?

Italian politics dominated overnight as the geographical divide between northern Europe wealth and Southern Europe economic struggles play out in the emotionally charged Italian political front. And the Euro is the ultimate pawn trapped between an open and free European market versus the growing waves of national inspired populism that is once again threatening contagion around the Mediterranean. Italy is plummeting into a political crisis.

Yesterday's EUR relief rally quickly gave way to the possibility of another election in Italy. But the significant risk facing the markets is will Italy be another Spain or morph into another Greece?

Things appear to be moving in a positive tangent in North Korea, and given the all the noise this rukus has created over the past fortnight, global markets are happy to see this summit happen. $Asia traded lower across the board yesterday with KRW/IDR/INR in the lead on the improving geopolitical risk and favourable EM high yield scrim. But with the USD reasserting itself overnight vs the EUR as Italian risk crumbles, the market has pulled back on some of the stretched positionings as the US dollar continues to show a strong haven backbone in the G-10 space.

Sticking with the political theme, The Malaysian Ringgit continues to be a no-trade zone despite decent levels. Even more telling, however, was yesterday when regional sentiment was improving with USDAsia moving lower, and Indonesia /India yields also correcting lower, but the Ringgit remained stuck in no man's land on little more than trickles of offshore flow.

Oil Market

Oil prices are falling fast and furious as WTI has plummeted nearly 10 % of its peaks as Saudi Arabia continues to make overtones that Russia and OPEC nations will pump more oil to ease global supply concerns. While all roads are pointing to OPEC raising production, the real question is by how much. Fine tuning the supply calculus is a prudent move given that no one would benefit from a spike to 90+ per barrel. But this should not be confused with a breakdown on OPEC compliance, or should it?

On the other hand, the technical trading overlays are looking quite bearish as the aggressive sell-off is suggesting a significant top if forming on the uber-bearish reversal.

Gold Market

Conflicting signals abound with Italy contagion fears back on the forefront offset by the rising US dollar which remains the primary headwind gold price. But we have a hectic week to navigate chalk full of crucial US data none more significant than the May employment report particularly considering the recent dovish conversation on wage growth in the May 2 FOMC minutes. While the market can agree and disagree on the importance of the geopolitical narratives, what's not debatable will be the US NFP data which could shape up the near-term outlook for the US dollar and gold prices in general.

Certainly, geopolitical risk will point to upside risk, but with the US dollar trade firm and attracting EU risk-off flows, geo-risk won't be a significant game changer until the USD weakens.

Currencies

G-10

EUR: EURUSD continues to buckle on haven USD flows given the heightened Italian political risk. , While near-term growth dynamics based on the recent run of weak economic data in the EU are also providing tailwinds for the USD.

JPY: The Nikkei dynamics look fragile in the face trade issues, and this continues to weigh on USDJPY sentiment. Also, the JPY is attracting EUR haven flows. Despite Abe support waning, however, risk rewards below 109 do not paint a convincing argument suggesting more of the same range trade within the 109 handle.

Asia FX

MYR: The Ringgit is putting in a repeat performance from last week so far as investors remain extremely cautious with the evolving political landscape

KRW: USDKRW longs to unwind yesterday in consort with improving geopolitical risk, but undoubtedly month end exporter flow was a driver with the KOSPI up marginally on muted different stream.

High Yielders are trading positively on the backdrop of lower US 10 year yields.

IDR: Central Bank commitment to monetary policy is making compelling waves in both currency and bond markets. A move designed to get ahead of the Fed curve.

INR: The reversal in Oil prices is the primary driver for improving sentiment

Eco Data 5/29/18

[php_everywhere instance="1"]

Gold Edges Lower on Memorial Day Holiday

Gold is trading quietly in the Monday session, hugging the $1300 level. In the North American session, the spot price for one ounce of gold is $1298.76, down 0.24% on the day. On the release front, U.S banks are closed for the Memorial Day holiday. On Tuesday, the US releases CB Consumer Confidence.

Is the summit on or off? Gold prices dropped close to 1 percent on Thursday, following reports that the summit between President Trump and North Korean leader Kim Jong-un had been canceled. Trump sent a letter to Kim, saying that he could not go ahead with the meeting, scheduled for June 12 in Singapore, after particularly harsh comments by the North Korean leader. For its part, Pyongyang was restrained in its response, saying that it still looked forward to resolving outstanding issues with the US. There are now growing expectations that the summit, scheduled for June 12 in Singapore, could still take place. The White House has sent a team to Singapore in case the summit is back on, and neither side will deny or confirm whether the meeting will take place. Meanwhile, the leaders of South Korea and North Korea met on the weekend. That meeting was completely unexpected and raises hopes of a breakthrough in the long conflict between the two Koreas. If the summit between Kim and Trump does take place, investor sentiment could soar, which could weigh on safe-haven gold.

British Pound Steady as U.S and U.K on Holiday

With U.S and British banks closed for holidays on Monday, the currency markets are having a quiet day. In North American trade, GBP/USD is trading at 1.3309, up 0.06% on the day. There are no British or U.S indicators on the schedule. On Tuesday, the US releases CB Consumer Confidence.

It was a disappointing week for the British pound. GBP/USD declined 1.2% and dropped below the 1.33 line for the first time since November. Investors have their doubts about a rate hike in August, and the BoE has done little to dispel these concerns. Last week, BoE Mark Carney was coy about future rate hikes, saying that “interest rates are more likely to go up than not, but at a gentle rate”. CPI, the primary gauge of consumer inflation, dropped to 2.4%, missing the estimate of 2.5%. This was the lowest rate of inflation since January 2017. If bank policymakers don’t feel confident about economic growth, the bank could remain on the sidelines in August, just as it chose to do at the May policy meeting. This could sour investor sentiment and send the pound lower.

The drama and uncertainty continue to swirl around the upcoming summit between President Trump and North Korean leader Kim Jong-un, which may or may not take place on June 12 in Singapore. Just a few days ago, Trump sent a letter to Kim, saying that Trump was canceling the much-anticipated meeting. However, the response from Pyongyang was restrained, and the White House has sent a team to Singapore in case the summit is back on. Meanwhile, the leaders of South Korea and North Korea met on the weekend. That meeting was completely unexpected and raises hopes of a breakthrough in the long conflict between the two Koreas.

Dollar Pushes Yen Close to 110 in Thin Holiday Trade

It’s a quiet start to the week for the Japanese yen. In Monday’s North American session, USD/JPY is trading at 109.36, down 0.04% on the day. In the Asian session, the pair touched a high of 109.86, close to the symbolic 110 level. On the release front, Japanese inflation was stronger than expected. The Services Producer Price Index posted a strong gain of 0.9% in April, well above the estimate of 0.5%. This marked the highest gain since September. Later in the day, Japan releases the unemployment rate, which is expected to remain pegged at 2.5% for a third straight month. U.S markets are closed for Memorial Day, so there are no U.S events on the schedule. On Tuesday, the US releases CB Consumer Confidence and Japan will publish retail sales. As well, BoJ Governor Haruhiko Kuroda will address a conference in Tokyo.

The drama and uncertainty continue to swirl around the upcoming summit between President Trump and North Korean leader Kim Jong-un, which may or may not take place on June 12 in Singapore. Just a few days ago, Trump sent a letter to Kim, saying that Trump was canceling the much-anticipated meeting. However, the response from Pyongyang was restrained, and the White House has sent a team to Singapore in case the summit is back on. Meanwhile, the leaders of South Korea and North Korea met on the weekend. That meeting was completely unexpected and raises hopes of a breakthrough in the long conflict between the two Koreas.

The Bank of Japan remains officially committed to continuing its radical easing policy and negative interest rates until inflation rises closer to the bank’s target of around 2 percent. At the same time, BoJ policymakers have been looking for ways to move away from radical easing, in part because ultra-low interest rates have hurt the profits of financial institutions. Last week, BoJ Governor Haruhiko Kuroda promised that the bank would be transparent with regard to an exit from its radical easing policy, but added that the markets shouldn’t hold their breath for any dramatic announcements. Kuroda said that the BoJ would “communicate specifics on how we plan to exit once inflation accelerates toward 2 percent, but reiterated that there would be no departure from policy until the inflation target was met. That goal remains elusive, as underscored by recent inflation indicators. Last week, both BoJ Core CPI and Tokyo Core CPI dropped to 0.5%, missing their estimates of 0.6 percent.

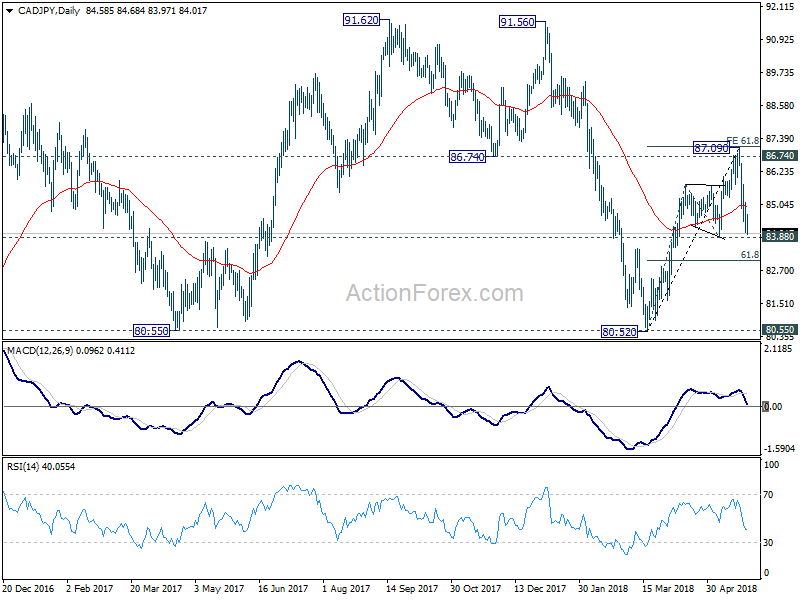

CADJPY shows some text book style chart analysis examples

Selloff in Canadian Dollar finally takes off with USD/CAD breaking 1.3 handle. The development now also makes CAD/JPY an interesting pair to study.

Rebound from 80.52 completed at 87.09, just ahead of 61.8% projection of 80.52 to 85.75 from 83.86 at 87.11. Together with the three wave structure, they make the move from 80.52 to 87.09 corrective. That is, the larger trend is bearish.

While CAD/JPY breached 86.74 but could not sustain above and reversed. 86.74 is the neck line of the double top pattern of 91.62, 91.56. This classic neck line rejection suggests that the down trend is not over.

There is also a potential head and shoulder pattern with ls at 88.90, 91.62 and 91.56 double top as head, and 87.09 as rs. That suggests there is more downside potential ahead.

For now, as the fall fro 87.09 is sort of runaway already, it's not an ideal time to short CAD/JPY. But this pair is worth monitoring for short opportunities ahead.

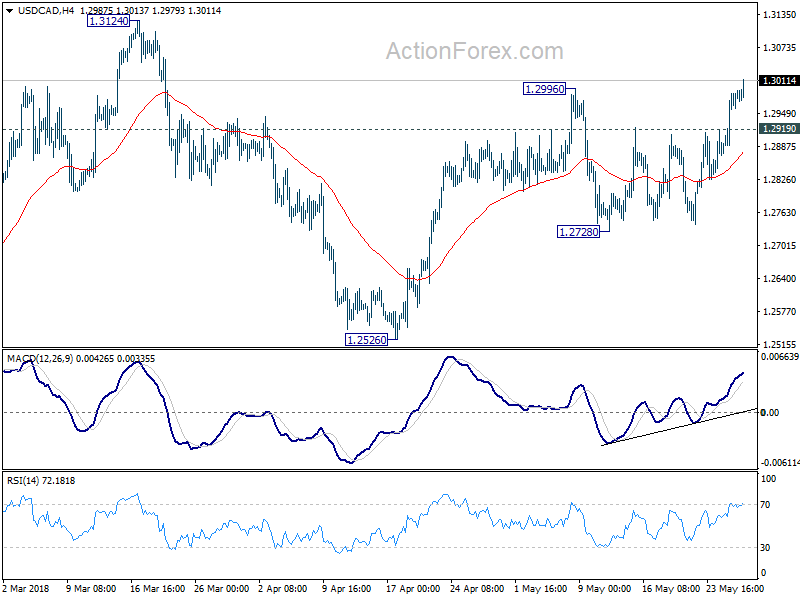

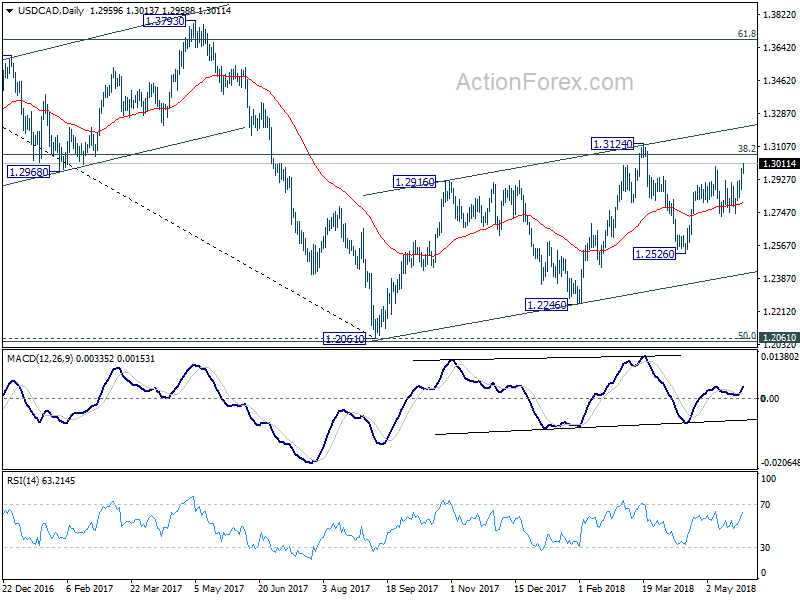

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2898; (P) 1.2945; (R1) 1.3020; More.....

USD/CAD's break of 1.2996 resistance finally suggests resumption of rise from 1.2526. Intraday bias is back on the upside for 1.3124 resistance next. Decisive break there should confirm medium term trend reversal. On the downside, below 1.2919 minor support will dampen the bullish view and turn bias neutral again.

In the bigger picture, we're favoring the case that that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

Sunset Market Commentary

Markets:

Risk sentiment improved this morning as the US/North Korean Summit is back alive and as the worst case short term scenario on the Italian political scene was avoided. However, it soon turned out to be a sucker’s rally, as we feared this morning. More repositioning has to be done. Italian President Matterella’s veto halted 5SM-Lega’s coalition efforts, but risks strengthening their hand after new snap elections in September/October by giving them a stronger political mandate to pursue policies in conflict with E(M)U treaties rather than just fiscal stimulus. The Italian 10-yr yield spread added another 29 bps, hitting the highest level (235 bps) since the end of 2013. There’s no point in catching the falling BTP knife. Other peripherals suffered from spill-over effects (Portugal +18 bps, Spain +13 bps, Greece +12 bps). Even semi-core spreads widened (Ireland +6 bps, Belgium +4 bps and France +3 bps). Spanish political developments (see headlines) cause no specific underperformance. Any possible Spanish snap election doesn’t risk triggering a systemic European institutional crisis like in Italy. The German Bund played his role as safe haven. German yields decline by 4.7 bps (30-yr) to 6 bps (5-yr) with the belly of the curve outperforming the wings. Volumes were high even with UK (Spring Bank Holiday) and US (Memorial Day) markets closed. Next support for the German 10-yr yield kicks in at 0.3%.

EMU political event risk remained the major driver for trading in the major euro and USD cross rates today. European investors initially saw the glass half full. Italian assets rebounded and so did the euro. Markets apparently hoped that Italian President Mattarella vetoing the appointment of Eurosceptic Paolo Savona as Finance minister, would bring some calm to European markets. This hope was clearly in vain. The European risk-off trade resumed soon. The sell-off in Italian equities and bonds resumed. Bund are propelled by a new safe haven bid, interest rate differentials between the US and EMU/Germany widen further, resulting in ‘logical’ further decline of the single currency. EUR/USD traded in the 1.1730 area at the start of European dealings, but is again losing more than a full big figure. The pair is trading in the 1.1615/20 area. USD/JPY traded with a slightly negative intraday bias, but is holding north of the 108.85/109 support area. It will take till tomorrow when US markets are again fully operational to see which part of the safe haven flow away out of the euro will go to the dollar or to the yen.

UK markets were also closed today. EUR/GBP mainly followed the intraday price swings of the EUR/USD headline pair. EUR/GBP traded near the 0.88 big figure this morning, but tumbled in line with the global intraday euro sell-off. Scottish first minister Sturgeon in a meeting with EU Chief Brexit negotiator Barnier indicated that Scotland prefers to remain part of the EU customs union/single market. This debate illustrates the complex internal political situation that PM May faces domestically. However, the focus is currently on the euro issues, not on Brexit.

News Headlines:

The no-confidence vote to oust Spanish PM Rajoy, called for by opposition Socialists last week, will take place on Friday, according to leading Spanish newspaper El País. Ciudadanos’ leader Rivera said that they won’t back the no-confidence vote and issued an ultimatum to call snap elections instead. If Rajoy agrees to a ballot in fall, they’ll ensure an orderly end to the legislature, helping the final passage of the 2018 budget. If not, he’ll the votes in parliament for an election anyway (FT + BB)

Turkey’s central bank has decided to more than double its one-week repo rate to 16.5% from June 1, equalizing that rate with the current main funding rate and setting it as the new benchmark. That will bring monetary policy simplification to a completion after about two years of planning. Overnight borrowing and overnight lending rates will be set 150 bps below and above the one-week repo rate. EUR/TRY dropped from 5.5 towards 5.35. (BB)

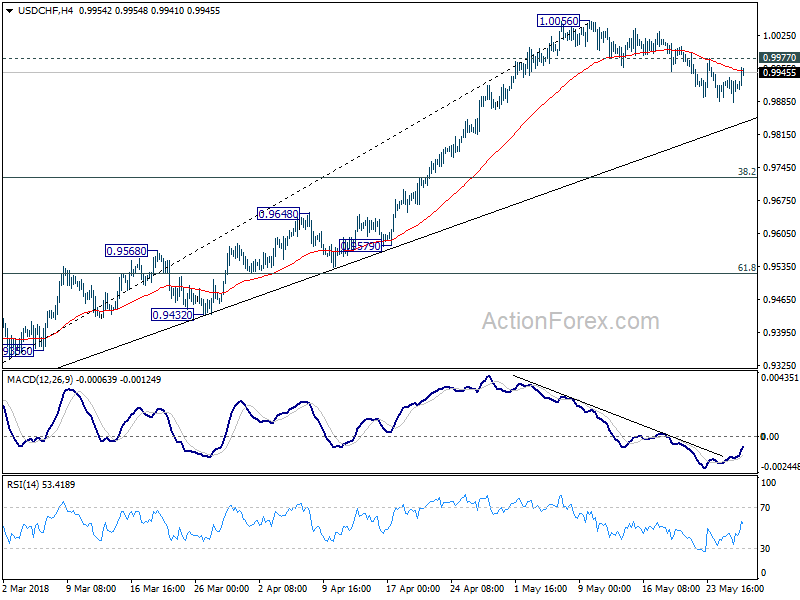

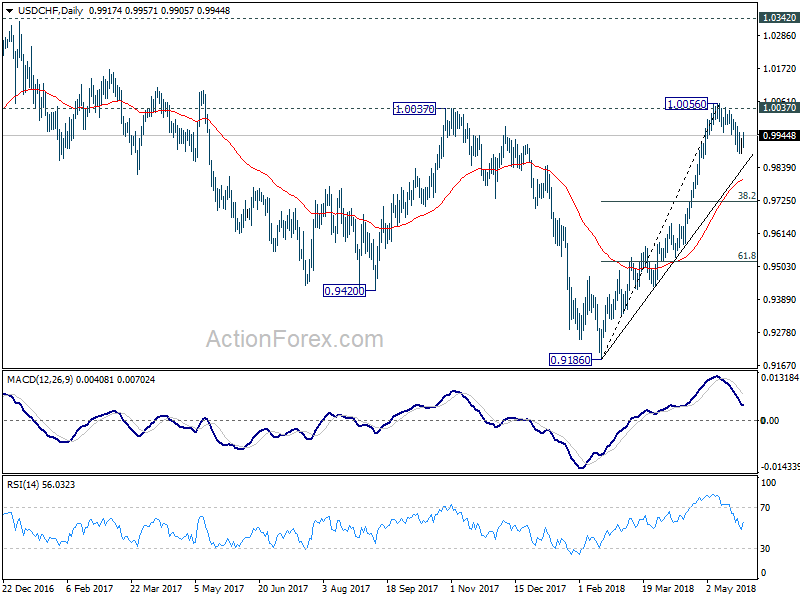

USD/CHF could be ready to resume recent rally

Taking a look at the D heat map for today, we can see that Euro is trading broadly lower. A surprise is that Swiss Franc is even weaker despite risk aversion. That prompts us to have a look at USD/CHF to see if there is some underlying weakness in the Franc.

From USD/CHF action bias table, we can see that the pair is maintaining solid upside W action bias. D action bias stayed neutral for more than nine bars, arguing that it's in a shallow consolidation pattern. This consistent with the "look" in D action bias chart.

6H action bias chart showed that there were downside attempts but failed. But there is no clear sign of rally yet. Now, with H action bias turned upside blue for in the last four bars there is "prospect" of rally resumption. USD/CHF is worth a watch now. There will be more confidence on a bullish view if 6H action bias turns upside blue too.

Taking a look at the regular OHLC chart, it's early to tell if the pull back from 1.0056 has completed. But when that's confirmed, there is potential to extend recent rise fro 0.9186 to 1.0342 key resistance. So, a way to trade this is, buy on a break of 0.9980 (slightly above 0.9977 minor resistance). Stop would be put at 0.9880, below today's low. Target will be 1.0342. Ideally, we should see 6H action bias turns blue too on next rise.