Sample Category Title

Italian Risks Recede… But Only Temporarily

Yesterday, the push to form a populist government derailed, after President Sergio Mattarella vetoed the Five Star/League choice of euro-sceptic finance minister Paolo Savona, citing concerns about threats to Italy's euro membership and the savings of Italian families. Five Star and the League reacted furiously to the decision, accusing the President of being influenced by Moody's decision on Friday to put Italy on negative watch.

The ball is now with the President again. He has indicated that he might take a few days to consider the request to dissolve parliament and call for new elections. At the time of writing, Mattarella has just given former IMF official Carlo Cottarelli the mandate to try to put together a 'neutral' interim government.

There is heightened uncertainty on what will happen next but we think current developments point to Italy heading to the polls again eventually. The President seems reluctant to call a vote before the 2019 budget is approved in October, preferring an interim government that would last until the end of this year and take the country to new elections in early 2019. However, given opposition from Five Star, the League and Forza Italia, such a technocratic government currently looks unlikely to pass a vote of confidence. This makes new elections in the autumn the more likely option in our view (9 September mentioned as a possible date by Italian media). This said, the power to dissolve parliament and thereby the timing of elections lies with the President (once parliament is dissolved, a vote has to happen within 70 days).

Following the standoff over the finance minister appointment, Five Star has also called for an impeachment of the President. At this stage, we view this as unlikely, as Five Star would need the support of the League as well, which has so far remained silent on the matter and it also risks paving the way for an additional institutional crisis, with a potential voter backlash.

Although the president's move has created some short-term respite in the Italian turmoil, we see a strong possibility that populists will emerge from a new election even stronger (see chart), given the current momentum and mood. This means further market turbulence lies ahead, also because eurosceptic tones are likely to feature even more prominently in the next election campaign, especially from the League.

BTP rally has already petered out

This morning we saw an initial rally in the BTP market on the back of the failure to form a populist government. However, at the time of writing, 10-year Italian yields are once again edging higher. This underlines that the market is still concerned about the political outlook and that a caretaker government or new snap election would not be a silver bullet for solving the political impasse in Italy, especially as both 5SM and the League could benefit from the current situation and the political discussion might increasingly centre on the question of leaving the euro.

We stay on the sidelines with respect to BTP exposure despite the healthy carry on the Italian curve and the imminent lower risk of a populist government. This morning we took a stop/loss on our recommendation to buy 5Y BTP versus 2Y Schatz.

Moody's could still go through with downgrade

Over the weekend, Moody's put Italy on review for possible downgrade. This is very serious as Moody's did this outside the normal rating calendar and it usually takes rating action outside the schedule only if it sees a material change in assumptions regarding the current rating and outlook. Furthermore, it is negative watch, which means it will take action within three to six months. However, Moody's based its update on the programme of the 'old' government. However, if a possible new government continues down the same road, we believe it is likely Moody's would go through with the downgrade.

Possibilities in Spain and Portugal

We have seen some contagion from Italy to Spain and Portugal. In respect of Spain, we see pressure on Prime Minister Mariano Rajoy. However, the political situation is in no way comparable to that in Italy. There is no specific reason why Portugal is spreading out. If we see some weeks of stabilisation, both Spain and Portugal could offer interesting opportunities for bond investors.

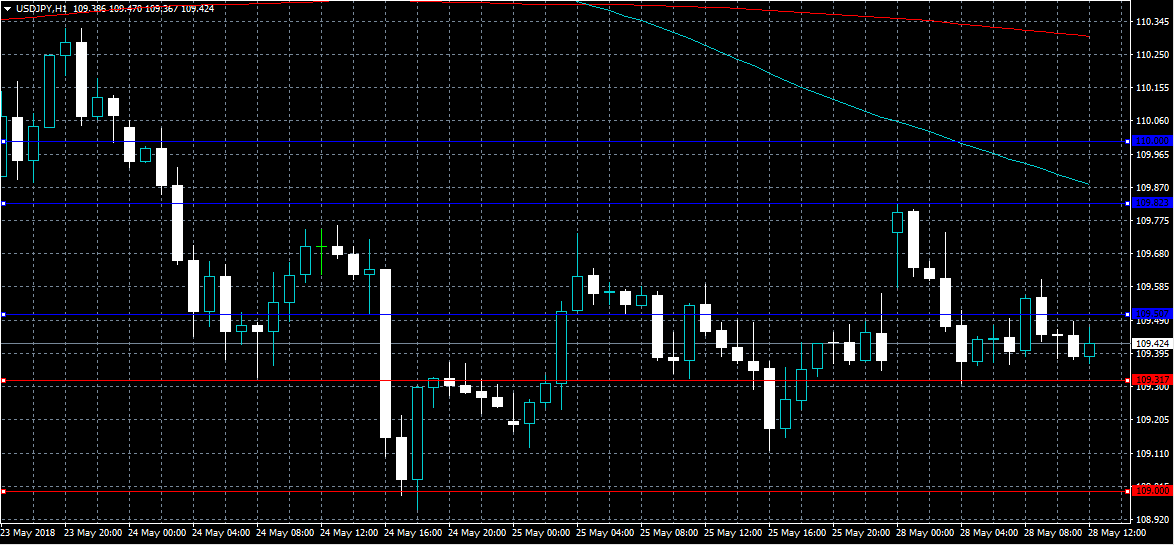

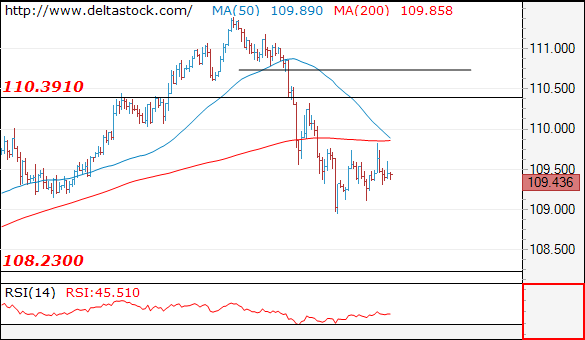

USDJPY Still Under Pressure Below 110.00 Level

The US dollar continues to trade to the downside against the Japanese yen, with the pair confined to the bottom-end of its recent trading-range in thin market trading conditions. The USDJPY pair currently trades around the 109.40 level, with selling pressure still building while price trades below the key 110.00 level. Traders continue to look for any news regarding the upcoming meeting between North Korea and the United States.

The USDJPY pair remains bearish while trading below the 110.00 level, further losses towards 109.31 and 109.00 remains possible.

If USDJPY buyers can move the pair back above 110.00 level, we may see a correction back towards 110.33 and 111.00 levels.

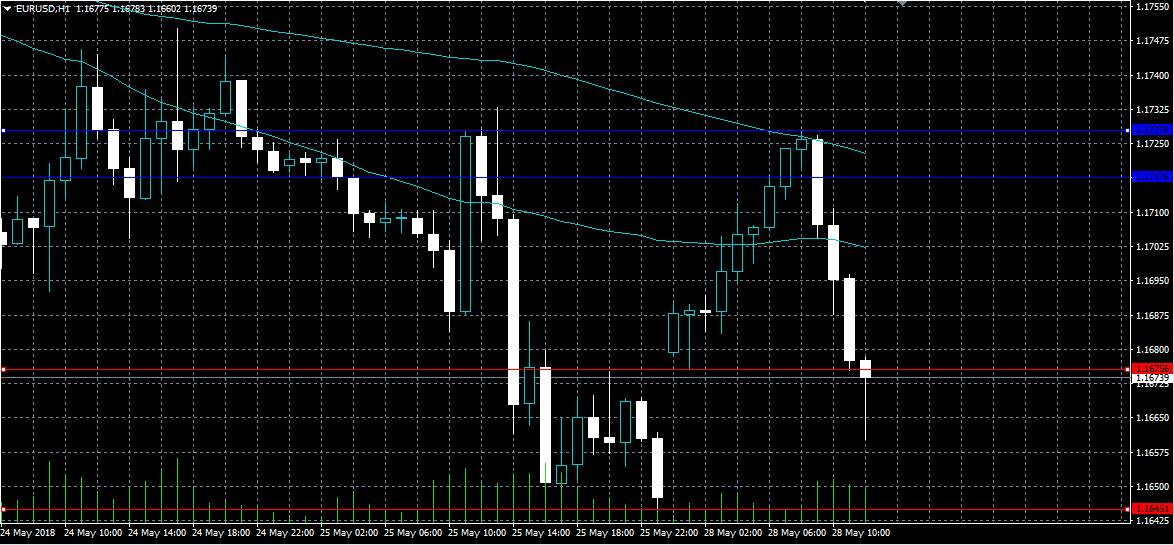

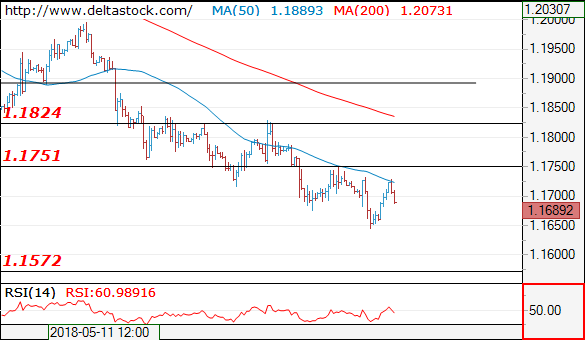

Further EURUSD Losses LIkely Below 1.1675

The euro currency has come under further selling pressure against the US dollar during today’s European selling, with price strongly rejected from the 1.1727 level. The EURUSD pair currently trades around the 1.1670 level, after finding interim support from the 1.1660 level so far this morning. With a lack of macroeconomic news today, technical traders will look for further euro weakness below the 1.1675 level.

The EURUSD is likely to come under further selling pressure while trading below the 1.1675 level. Key support is found at the 1.1645 and 1.1615 levels.

If the EURUSD pair moves above the 1.1675 level, price may correct back towards the 1.1700 and 1.1727 levels.

Euro back under pressure as German-Italian spread widens again

After brief lift, EUR/USD is back under pressure and breached Friday's low at 1.1643. The pair was initially lifted briefly by news that the antiestablishment coalition of 5-star movement and the League failed to form a government.

But quickly into European sessions, sentiments turned sour again as markets weigh the chance and impact of a new election that could happen as soon as in August.

Italian 10 year government bond yield dipped to 2.35 but is now back at 2.590, up 0.038.

German 10 year bund yield initially rose to 0.463 but reversed to 0368 so far, down -0.037.

Widening German-Italian yield spread is now pressuring Euro broadly again. Euro is trading down against all but swiss Franc and Canadian Dollar.

Cottarelli accepted mandate to form an interim Italian government

In swift arrangements, former IMF Director of the Fiscal Affairs Carlo Cottarelli accepted Italian President Sergio Mattarella's appointment to form an interim government. That came after Giuseppe Conte abandoned the effort to form a new coalition government of the 5-Star Movement and the League, following Mattarella's veto of eurosceptic Paolo Savona as the as economy minister.

The Prime Minister designate Cottarelli said that "I'll present myself to parliament with a program which - if it wins the backing of parliament - would include the approval of the 2019 budget. Then parliament would be dissolved with elections at the beginning of 2019."

Or, "in the absence of (parliament's) confidence, the government would resign immediately and its main function would be the management of ordinary affairs until elections are held after the month of August,"

BOC Likely Stands on Sideline This Month as More Data and Trade Outlook Awaited

Bank of Canada (BOC) would most likely leave its policy rate unchanged at 1.25% in May. Following two rate hikes in 2017 and one more in January this year, BOC has kept its powder dry since then. In April, the central bank cautiously noted that future monetary policy change would be “guided by incoming data” and directed by the future of trade policy.

Inflation Not as Dovish as Market Perceived

Inflation data April was a mixed bag. Headline CPI eased to +2.2% in April, from +2.3% a month ago. Expectations for a rate hike this month dropped sharply to 35% after the report, from 50% before that. Yet, we do not view the inflation report with dovish tone as the current level of inflation has stayed above the +2% target. Meanwhile, the average of the BOC’s three measures of core inflation, which exclude volatile components including oil prices, has just breached +2% for the first time since February 2012. We would not object a hike if the decision is just made based on this parameter alone.

April Payrolls Surprised to Downside

However, one would agree that it is prudent for BOC to remain cautious and wait for more clarity. The country’s employment market has been improving. However, payroll change in April was disappointing. Government data showed that the number of jobs surprisingly fell -1.1K last month, the second decline since mid-2016. The market had anticipated an increase of 20K. Indeed, at the Monetary Policy Report accompanying April’s policy announcement, BOC, while acknowledging absorption of excessive slack, reminded that “the long-term unemployment rate is still relatively high, the youth participation rate has room to increase” and “the oil- and gas-producing regions continue to point to remaining labour market slack”.

First Quarter GDP Growth Closely Watched

Released earlier this month, GDP expanded +0.4% m/m in February, compared with consensus of +0.3% and a contraction of -0.1% in January. The March, as well as the first quarter growth data, would be due May 31. The market expects a +0.2% m/m growth in March and an annualized growth rate of +1.9% for 1Q18, compared with +1.7% in the prior quarter. It would probably Should the data came in inline with expectations

Trade Policy Direction Highly Uncertain

Besides economic developments, what warrants vigilance is the highly uncertain direction of trade policy. Last Wednesday, the US suddenly announced to launch a national security investigation, under Section 232 of the Trade Expansion Act, into car and truck imports. This could lead to new US tariffs similar to those imposed on imported steel and aluminum in March. As US Commerce Secretary Wilbur Ross noted in a statement, “there is evidence suggesting that, for decades, imports from abroad have eroded our domestic auto industry". Before the announcement, the White House noted that the move was partly aimed at pressuring Canada and Mexico to make concessions in talks to update the NAFTA, as well as pressuring Japan and the EU.

We do not expect NAFTA would be scrapped eventually. However, what and how much concession the parties involved would have to be made to secure is a contentious topic. It should cause much volatility in market sentiment and the financial markets, in particular Canadian dollar and yields.

DAX Slightly Lower, Investors Eye Italian Crisis

The DAX has edged lower in the Monday session. Currently, the DAX is at 12,921, down 0.13% on the day. There are no German or eurozone events on the schedule, so traders can expect the DAX to have a quiet day.

The twists and turns of Italian politics continue, and an extraordinary weekend may have triggered a fresh political crisis. On Sunday, President Sergio Mattarella vetoed the choice of economic minister by the two parties entrusted with forming a coalition, the League Nord and the Five Star Movement. Mattarella rejected the suggestion of Paolo Savona for economic minister, given that Savona is a firm critic of the euro and supports Italy exiting from the eurozone. The head of the Five Star Movement demanded that Mattarella be impeached, charging that the president was taking orders from Brussels. On Friday, Moody’s rating agency said that it could reduce Italy’s sovereign debt rating over fears of the new government’s fiscal policies. The current impasse may result in another general election, which could sour investor sentiment and send the euro lower.

What can we expect from the ECB? The bank is scheduled to wind up its massive stimulus program in September, but weak growth in the first quarter has raised speculation that the bank could decide to extend the program, a tactic it has often used in the past. Still, most analysts believe that the ECB will go ahead and terminate stimulus, but there is more uncertainty regarding future rate hikes. Higher oil prices and a weaker euro will likely mean that inflation is moving upwards, but core inflation projections, which ECB policymakers are most interested in, are expected to remain below the ECB inflation target of just below 2 percent. Investors will be keeping a close look at upcoming rate statements, looking for clues regarding the wind-up of the stimulus scheme.

Euro Subdued, U.S Markets Closed For Holiday

EUR/USD has posted slight gains in the Monday session. Currently, the pair is trading at 1.1644, down 0.03% on the day. There are no eurozone or U.S events on the schedule. U.S markets are closed for Memorial Day, so traders can expect a quiet day from the pair. On Tuesday, the U.S releases CB Consumer Confidence, which is expected to dip to 128.7 points.

Italian politics often provides dramatic moments, but even by Italian standards, the events on the weekend were truly extraordinary. Italy lurched into political crisis, as President Sergio Mattarella vetoed the choice of economic minister by the two parties entrusted with forming a coalition, the League Nord and the Five Star Movement. Mattarella rejected the suggestion of Paolo Savona for economic minister, given that Savona is a firm critic of the euro and supports Italy exiting from the eurozone. The head of the Five Star Movement demanded that Mattarella be impeached, charging that the president was taking orders from Brussels. On Friday, Moody’s rating agency said that it could reduce Italy’s sovereign debt rating over fears of the new government’s fiscal policies. The current impasse may trigger new elections, which could sour investor sentiment and send the euro lower.

The ECB is scheduled to wind up its massive stimulus program in September, but weak growth in the first quarter has raised speculation that the bank could decide to extend the program, a tactic it has often used in the past. Still, most analysts believe that the ECB will go ahead and terminate stimulus, but there is more uncertainty regarding future rate hikes. Higher oil prices and a weaker euro will likely mean that inflation is moving upwards, but core inflation projections, which ECB policymakers are most interested in, are expected to remain below the ECB inflation target of just below 2 percent. Investors will be keeping a close look at upcoming rate statements, looking for clues regarding the wind-up of the stimulus scheme.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1689

My outlook remains bearish, for a continuation of the slide towards 1.1570 zone. Crucial on the upside is 1.1750 resistance

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1750 | 1.2000 | 1.1640 | 1.1680 |

| 1.1830 | 1.2160 | 1.1570 | 1.1480 |

USD/JPY

USD/JPY

Current level - 109.43

Allow another intraday rise, which should be limited below 110.40 and should provoke another sell-off, towards 108.20 area. Trigger on the downside is 109.12.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.80 | 111.40 | 109.12 | 108.30 |

| 110.40 | 114.40 | 108.30 | 107.00 |

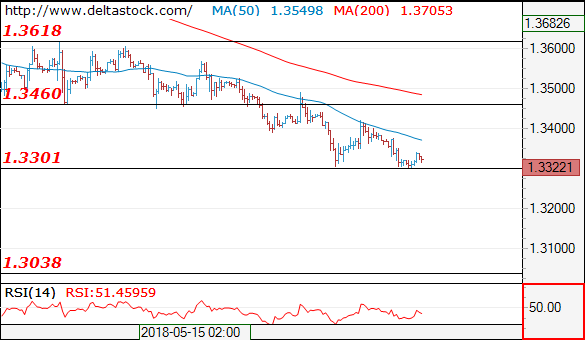

GBP/USD

Current level - 1.3322

The general downtrend is intact, ready for a break through 1.3300, towards 1.3040 area. Minor intraday resistance lies at 1.3375 and crucial on the upside is 1.3421.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3370 | 1.3990 | 1.3300 | 1.3300 |

| 1.3421 | 1.4100 | 1.3210 | 1.3040 |

Italy Under The Spotlights

Italy's political turmoil is not over

The market greeted Sergio Mattarella's decision to reject euro-sceptic Paolo Savona as Finance Minister. After falling as much as 0.65% last Friday, the single currency bounced back on Monday morning and reached 1.1728, up 0.55% on the session. Similarly, selling pressures on Italian bonds eased significantly with the 2-year yield falling 15bps to 0.335%, while the 10-year one gave up 9.5bps and slid to 2.365%. On the equity market, the FTSE MIB jumped to 22,760 points, up 340 points or 1.50%.

By blocking the formation of the government, Italy's president played the card of prudence as he feared it could endanger the country's membership in the European Union. Even though, the pressure seems to have eased for now, Italy is far from being out of trouble. Indeed, both the 5-Star Movement and the League called for fresh elections, arguing that Mattarella didn't respect the decision of the people to go with a eurosceptic and anti-establishment coalition government. Sergio Mattarella would most likely face an impeachment request from the populist parties.

Uncertainties may have eased in the short-term but in the longer-term this is a different story as the political mess may increase ahead of fresh election. For now, the single currency takes a breather as EUR/USD rose 0.40% to 1.17, while EUR/CHF climbed back to 1.16.

Risk Apppite rallies in Asia

With participants on the long weekend, liquidity in the FX markets remains low. Hence volatile news flow continues to drive pricing. In reaction to signs that the US-North Korea summit would move forward Asian currency gained across the board. In unpreceded language North Korean leader, Kim Jong Un stated he was committed to 'complete' denuclearization on the Korean Peninsula. In addition, Kim said he would end the history of war and bring prosperity. The sound bit was enough to send risk appetite higher despite Kims checker past with commitments. Elsewhere in Asian, Indonesian IDR rallied from a weak position as the Central bank called an additional Board Meeting 30th May. We now anticipate the central bank will make a pre-emptive strike by hiking policy rate further 25bps at this meeting to highlight commitment to currency stability.