Sample Category Title

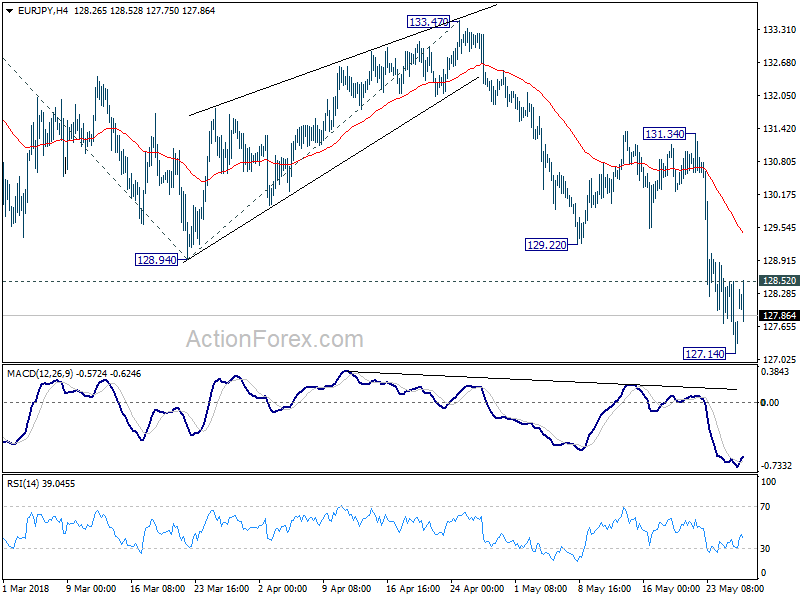

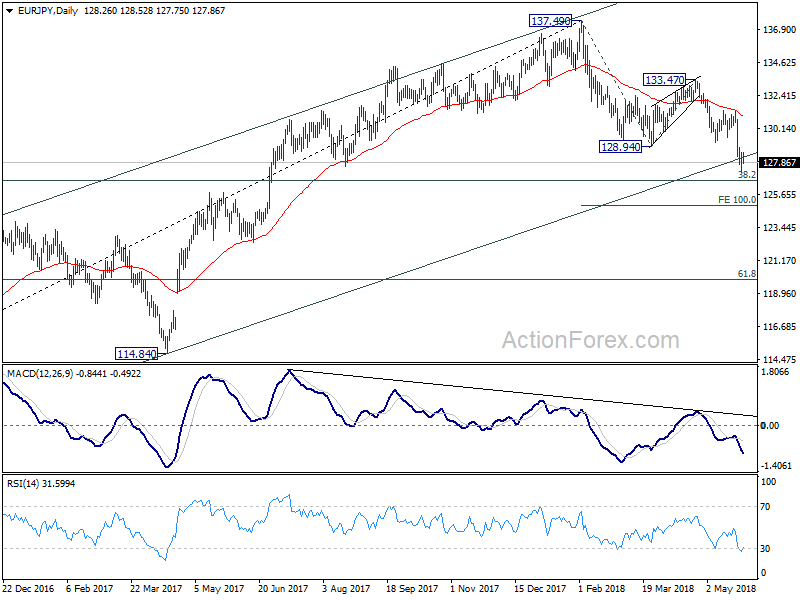

EUR/JPY Daily Outlook

Daily Pivots: (S1) 126.86; (P) 127.70; (R1) 128.25; More....

A temporary low is in place at 127.14 in EUR/JPY and intraday bias is turned neutral first. Some consolidations could be seen. but outlook will stay bearish as long as 131.34 resistance holds. On the downside, below 127.14 will resume the fall from 133.47 to 126.61 medium term fibonacci level. But based on current momentum, EUR/JPY could dive through this level to 100% projection of 137.49 to 128.94 from 133.47 at 124.92.

In the bigger picture, bearish divergence in daily MACD and current strong downside momentum is raising the chance of medium term trend reversal. Sustained break of 38.2% retracement of 109.03 to 137.49 at 126.61 will argue that whole up trend from 109.03 has completed at 137.49 already. And, deeper decline would be seen to 61.8% retracement at 119.90 and below. Though, strong support from 126.61 and rebound from there would revive medium term bullish for another high above 137.49.

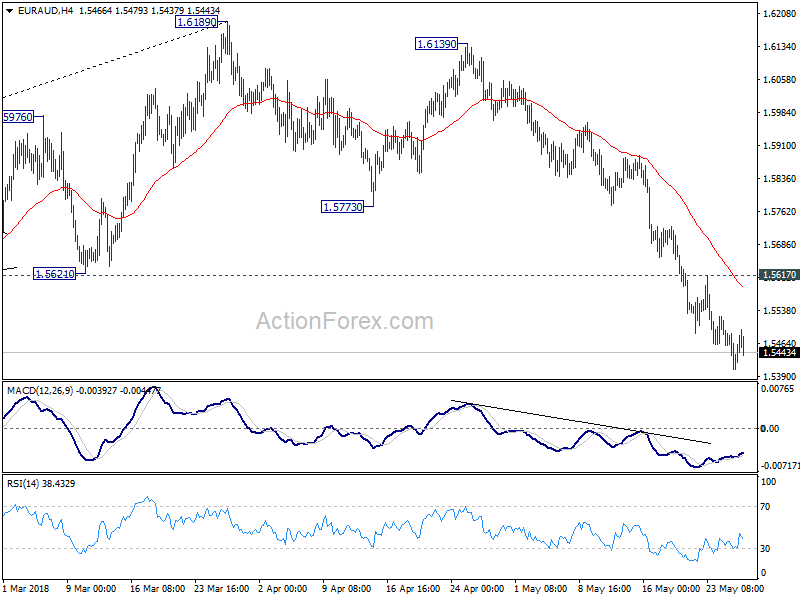

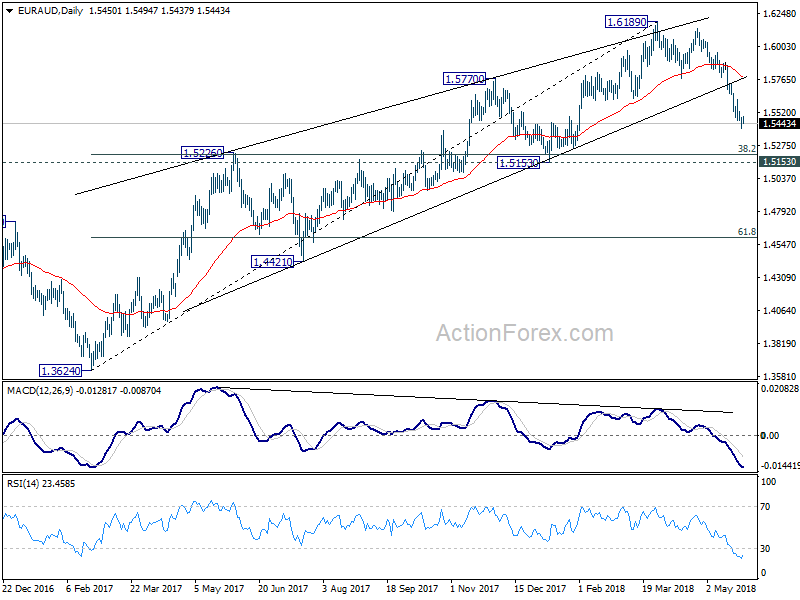

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5397; (P) 1.5443; (R1) 1.5482; More....

Near term outlook in EUR/AUD remains bearish with 1.5617 resistance intact. Current fall from 1.6189 should target 1.5153 key support level next. On the upside, break of 1.5617 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further decline is expected in medium term, even in case of strong rebound.

ECB Hike Has Been Postponed Amid Political Uncertainty In Italy

Market movers today

While the day is thin on data releases, the main focus in financial markets will be political chaos in Italy after the Italian President Mattarella last night opposed the proposal for finance minister for the incoming government of Five Star and the League. This raises the prospect for new elections, which would add to market anxiety toward Italy.

Financial markets will also focus on Spain, where the opposition called on Friday for the resignation of Spanish Prime Minister Rajoy after new corrupt ion allegations against Rajoy's ruling party. Political uncertainty and prospects for new elections in Spain would raise market fears of a prolonged political vacuum, as seen after the last general elect ion.

The key economic releases later in the week include the US job report on Friday, preceded by the euro area HICP release for May on Thursday.

Selected market news

Political uncertainty continues in Italy as premier-designate Giuseppe Conte has given up forming a government after the Italian President Sergio Mattarella last night rejected the proposal for finance minister by the incoming government of Five Star and the League. This raises the prospect for new elections, which would add to market anxiety towards Italy. Moreover, on Friday, Moody's placed Italy's credit rating on negative watch. This is likely to be negative for Italian government bonds when the market opens this morning. After the reject ion of the euro-sceptic Paolo Savona as finance minister, there was some relief in the EUR/USD.

Recently, the market pricing of the first ECB hike has been postponed amid political uncertainty in Italy and the market adapting to a slow normalisation. On Friday, according to Reuters, ECB sources indicated that the growth moderation "has not weakened the ECB's resolve to end a bond-buying scheme later this year but could make it more cautious about signalling interest rate hikes". The first 10bp deposit rate hike was postponed further and is now expected by the market in autumn 2019, and 20bp in spring 2020.

On Friday, the Swedish National Debt Office (SNDO) announced that it is going to position for a stronger SEK. The SNDO argues that because the SEK is weak at present , it would be cost saving to reduce the pace of SEK20bn per year, at which it current ly reduces foreign debt . SNDO's mandate for t his is SEK7.5bn.

On Sunday, US President Donald Trump confirmed the US-North Korean summit in a tweet, making no reference to the recent cancellation.

Key Events To Watch This Week

European politics

After falling to a six-and-a-half month low against the dollar on Friday, the Euro bounced back early Monday following the Italian president, Sergio Mattarella, blocking the formation of a new government supported by anti-establishment parties. Mr. Mattarella’s refusal on Sunday to approve a proposed Eurosceptic economic minister gave the Euro a much-needed push. However, it is far from certain that Mattarella’s current move will end Italy’s drama. In fact, the situation may worsen going forward, as 5 Star leader Luigi Di Maio is planning to request the parliament to have Mattarella impeached. On the other hand, the League leader Matteo Salvini suggested Italians returnto the polls for a re-vote. Such developments will put the third-largest European economy on anuncertain path that will ultimately lead to further pressure on the single currency.

Another looming risk to the Euro this week is Spain, after Pedro Sanchez, the leader of the Socialist Workers' Party, filed a no-confidence motion against the prime minister, Mariano Rajoy. If Sanchez gets the requiredvotes in parliament to replace Rajoy, expect to see a further selloff in Spanish bonds and equities. So, instead of one headache, the European Union will probably need to deal with two now, and with continuing deterioration in economic data, the Euro bounce is likely to be short-lived.

Oil prices

Oil resumed its slide on Monday, following discussions that Russia and Saudi Arabia may restore some of the halted output when OPEC and non-OPEC ministers meet in Vienna on June 22&23. Brent fell 7.45% from its peak of $80.49 recorded on Tuesday, while WTI declined more than 9.6% from Tuesday’s high.

The sustained fall in Venezuelan output helped OPEC and non-OPEC members to significantly exceed the intended total production cuts over the past eight months. Whether only Venezuela’s lost production will be recoveredor more remains unknown, but the impression of easing output cuts onits own is sufficient to put a cap on prices. From now and until the OPEC andnon-OPEC meeting, the ongoing commentary will continue to drive prices.

Trump – Kim Jong-unsummit back on

The summit between Donald Trump and Kim Jong-un could happen after all. After calling off the planned historic summit on Thursday, President Trump tweeted on Sunday “I truly believe North Korea has brilliant potential and will be a great economic and financial Nation one day. Kim Jong-un agrees with me on this. It will happen!”

Hopes that the Singapore summit could still take place may support appetite for risk assets. However, it has become evident that these developments tend to have only a temporary impact on equities and investors should not be distracted from the fundamental drivers.

Non-Farm Payroll report

Whether the dots on the Fed’s plot chart will move upwards or downwards when the Fed meets on June 12 & 13 will depend largely on this week’s economic data. Friday’s Non-Farm Payroll reportis expected to show an increase of 185,000 for the month of May, up from 164,000 in April. Average hourly earnings are also expected to improve slightly, rising 0.2% in May from 0.1% in the previous month. If these figures donot deviate widely from expectations, I don’t think the shape of the dot plot will change a lot. Another important indicator for the Fed will be the Personal Consumption Expenditure due on Thursday, which if begins to overshoot the 2% target, will imply faster tightening in the coming months.

Indian Bond Prices Rise As Oil Moves Lower

General Trend:

- Asian equity markets trade mostly higher amid renewed hopes for June US/North Korea summit and US holiday; Kospi outperforms

- Energy prices extend losses seen on Friday’s session amid production increase speculation based on comments from Russia and Saudi Arabia; WTI Crude Futures lower by over 2%, Brent Crude Futures down over 1%

- Hang Seng Utilities index declines over 1%; China announced increase in gas prices

- Indonesian assets rally as central bank announces ‘additional’ meeting: 10-year bond yield declines over 15bps, Rupiah (IDR) rallies

- Indian bond prices rise as oil moves lower

- Japanese Yen (JPY) trades generally weaker, JPY/KRW -0.5%: US President Trump noted ‘productive talks’ about reinstating June 12 summit with North Korea

- EUR/JPY and EUR/USD trade higher: Italy’s President rejected Savona for economy minister position

- PBoC raised rates on 28-day reverse repo operation (in line with increases in the 7 and 14-day rates)

- Analysts continue to push back BoJ rate hike calls into 2019

- US May jobs report due for release on Friday, June 1st

- MSCI expected to add China large-cap A-shares to EM index at the end of this week

- US Commerce Sec Ross scheduled to visit China from June 2-4th to discuss trade

Headlines/Economic Data

Japan

- Nikkei 225 opened +0.2%; closed +0.1%

- TOPIX Real Estate index +1.1%, Electric Appliances +0.3%; Marine Transportation -1.4%, Securities -0.5%, Info & Communications -0.5%

- (JP) JAPAN APR PPI SERVICES Y/Y: 0.9% V 0.5%E

- (JP) Japan PM Abe cabinet approval rating flat at 42% - Nikkei

- Nomura, 8604.JP Said to consider delaying EPS target of ¥100/share, cites markets – press

- Kansai Electric, 9503.JP Exec: To cut spot purchases of LNG and will likely not sign any long term LNG contracts as it moves to make nuclear power the largest part of its mix - financial press

- (JP) Japan PM Abe: Automakers have created jobs and made huge contributions to US economy; TPP is best trade format for japan and US and will keep explaining it to President Trump

Korea

- Kospi opened +0.2%

- (KR) North Korea state news: leader Kim expressed "his fixed will" for a summit with Pres Trump; Kim and S Korea Pres Moon agreed to high level talks on June 1st

- (KR) Pres Trump tweets that US is having "productive" talks about reinstating June 12 summit with North Korea; says no disagreement in the White House about how to deal with North Korea

- (KR) Follow Up: US Senior Diplomat Sung King said to be in North Korea for meetings related to the coordination of US/North Korea summit – US financial press

- (KR) South Korea President Moon met with N. Korea leader Kim in a surprise meeting over the weekend; Kim affirms commitment to complete denuclearization and meeting with Trump - press

- (KR) South Korea President Moon may join President Trump for a 3-way summit with N. Korea Kim - Korean press; Follow up: South Korea Govt: Trilateral meeting depends on result of meeting between N. Korea Kim and President Trump

- (KR) South Korea to require tougher mortgage rules in H2 of this year as part of govt effort to reduce household debt - Korean press

- (KR) Bank of Korea (BOK) sells 1-yr Monetary Stabilization Bonds (MSB) at 1.89% v 1.88% prior

- (KR) South Korea sells KRW1.65T v KRW1.65T indicated in 3-yr govt bonds at 2.235%

China/Hong Kong

- Hang Seng opened +0.6%, Shanghai Composite -0.1%

- Hang Seng Industrial Goods index +1.5%, Services +1.4%, Consumer Goods +1.3%, Financials +0.5%; Utilities -0.7%, Energy -0.3%

- 763.HK Pres Trump defends his strategy on ZTE and says the company will pay a $1.3B fine

- (CN) US pressuring China to sign long term import agreements – FT

- Alibaba, Tencent, Baidu to each hold 3.7% stakes in Foxconn Industrial Internet - SCMP

- (CN) Yuan to remain stable with two way fluctuations - China Securities Journal

- (CN) CHINA APR INDUSTRIAL PROFITS Y/Y: 21.9% V 3.1% PRIOR (6-month high)

- (CN) China should prevent bond default's market impact; gov't said to examine rules aimed at limiting bond default risk - Chinese press

- (CN) China PBoC Open Market Operation (OMO): Injects CNY30B in 7-day and 28-day reverse repos v skips prior; Net: injects CNY30B v CNY0B prior

- (CN) PBOC RAISES OPEN MARKET OPERATION (OMO ) RATE ON 28-DAY REVERSE REPO BY 5BPS TO 2.85% FROM 2.80% (AS EXPECTED)

- (CN) China PBoC sets yuan reference rate at 6.3962 v 6.3867 prior

Australia/New Zealand

- ASX 200 opened -0.2%, closed -0.5%

- ASX 200 Energy index -3%, Resources -2.2%, Telecom -1%, Financials -0.3%; Utilities +1%, REIT +0.7%

- Wesfarmers, WES.AU In exclusive talks with KKR about hotel and retail liquor portfolio - Australian

- IGO.AU Announces agreement to divest Jaguar operations for A$73.2M cash to unit of Washington H. Soul Pattinson, Copperchem

- APN Outdoor, APO.AU Guides FY18 (A$) EBITDA 92-96M; CAPEX 25-30M; Guides H1 Rev tracking mid-single digit growth y/y

- Investa office Fund,[+11%], IOF.AU Receives A$5.25/share cash proposal from Blackstone (~13.4% premium to prior close)

- (AU) Reserve Bank of Australia (RBA) Harper: Wage 'hot spots' are not obvious, wage growth 'is all slow'; RBA has 'steady as she goes' policy approach

Europe

- (UK) UK government is said to not have a plan for a Brexit 'no deal' - FT

- (UK) Foreign Sec Johnson Op Ed reiterates call for UK to leave the customs union – Telegraph

- (IT) Italy President Mattarella on Sunday blocked the formation of a new government amid concerns that the coalition could hurt the country's membership in the Euro; Italy President and Cottarelli expected to meet on Monday - US financial press

- (IT) Moody's puts Italy's Baa2 rating on downgrade review (Fri, after the close)

Levels as of 02:00ET

- Hang Seng +0.7%; Shanghai Composite -0.1%; Kospi +0.7%

- Equity Futures: S&P500 +0.4%; Nasdaq100 +0.6%, Dax +0.4%; FTSE100 +0.3%

- EUR 1.1727-1.1652; JPY 109.83-109.31; AUD 0.7581-0.7547;NZD 0.6957-0.6915

- Jun Gold -0.5% at $1,297/oz; Jul Crude Oil -2.5% at $66.22/brl; Jul Copper +0.5% at $3.09/lb

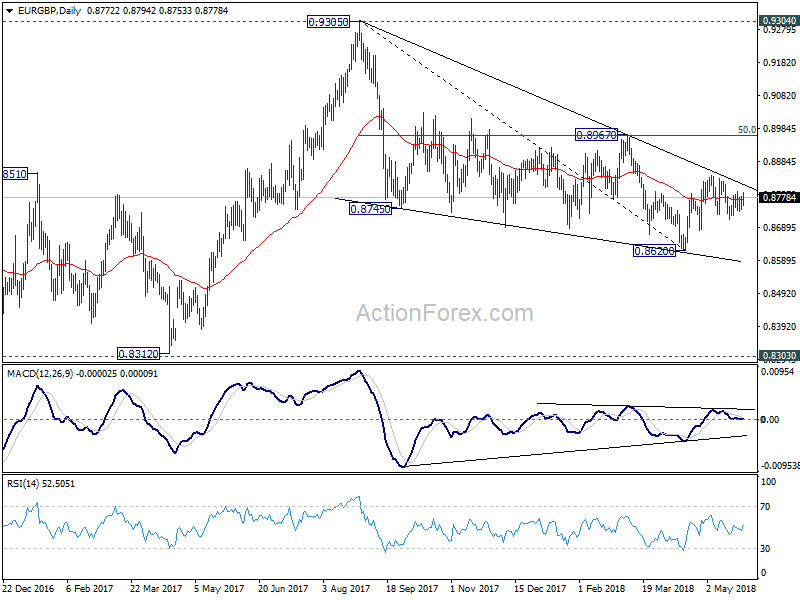

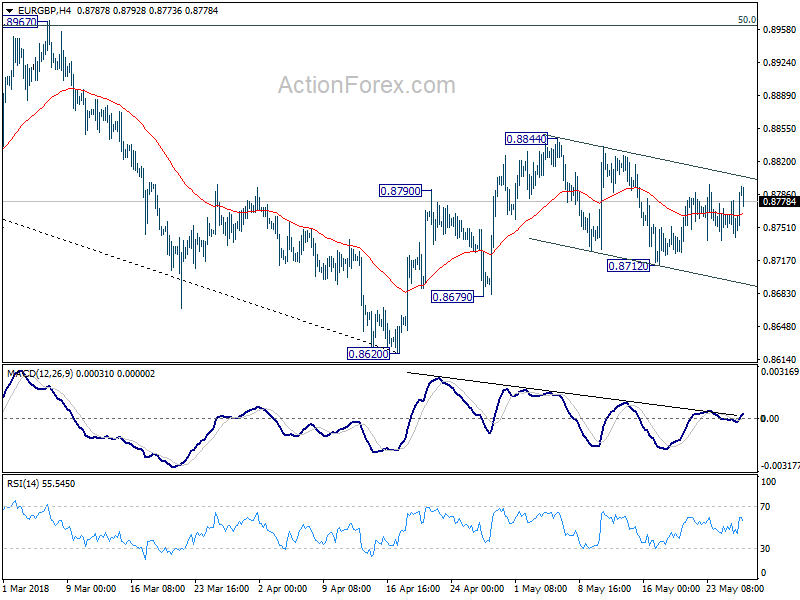

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8741; (P) 0.8763; (R1) 0.8784; More...

Intraday bias in EUR/GBP remains neutral as range trading continues inside 0.8712/8844. On the upside, break of 0.8844 will resume the rebound from 0.8620. That will also revive the case of larger bullish reversal. EUR/GBP should target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963) first. However, break of 0.8679 minor support should completion of the rebound form 0.8620. And intraday bias will be turned back to the downside for this support. Whole decline from 0.9305 will likely be resuming too.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

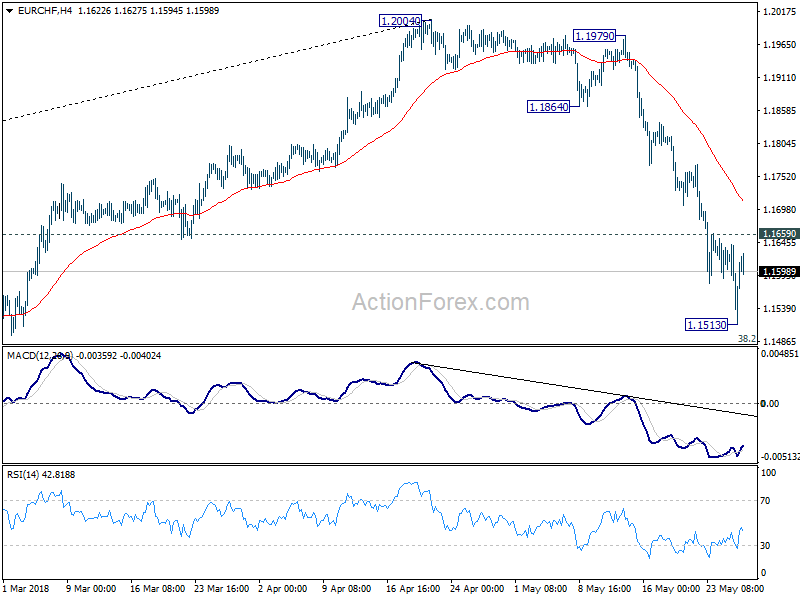

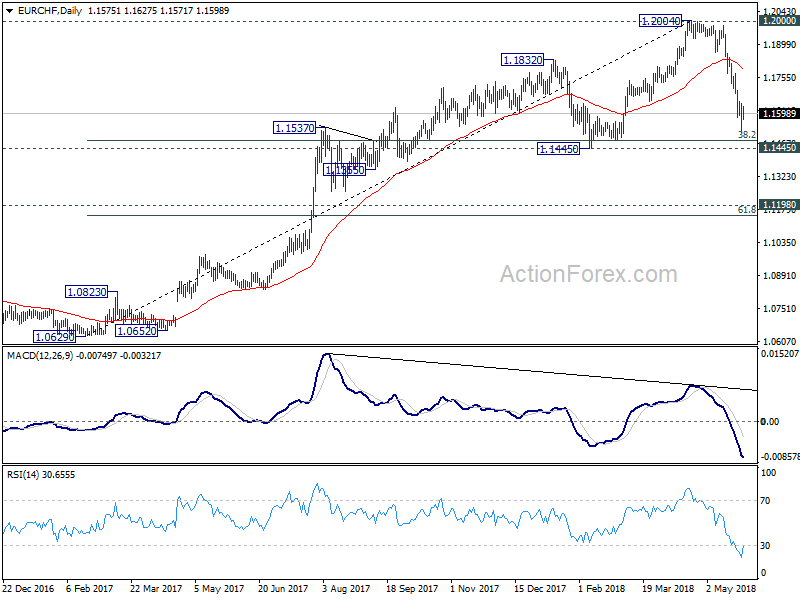

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1496; (P) 1.1570; (R1) 1.1609; More....

Strong rebound in EUR/CHF suggests temporary bottoming at 1.1513. Intraday bias is turned neutral first. While another fall cannot be ruled out yet, we'd expect strong support from 1.1445 to contain downside, at least on first attempt, to bring rebound. On the upside, above 1.1659 minor resistance will turn bias to the upside for rebound.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Hence, for now, deeper fall could be seen back to 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern. However, sustained break of 1.1445 will target next key cluster level at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154.

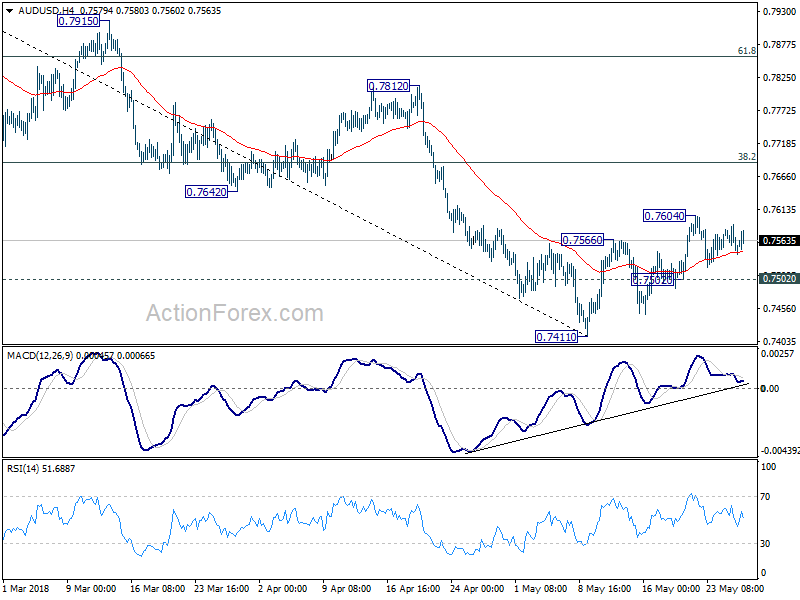

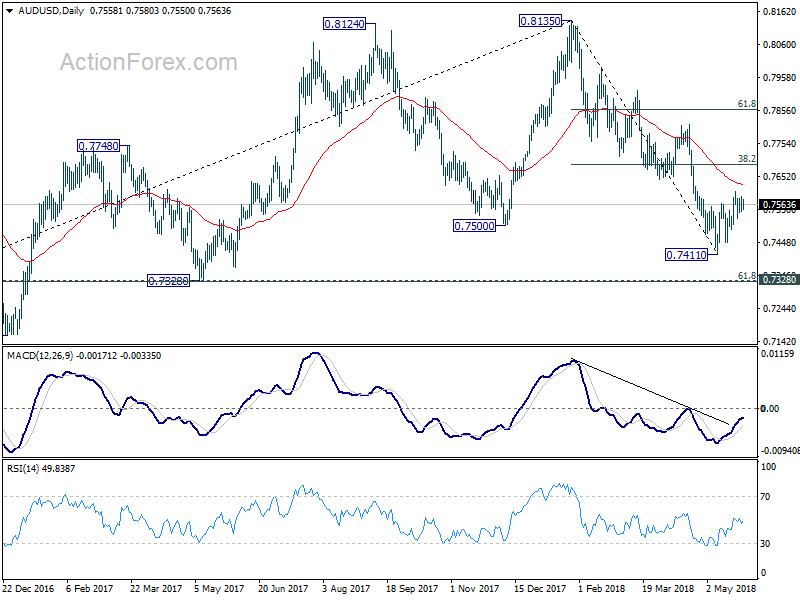

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7529; (P) 0.7560; (R1) 0.7578; More...

Intraday bias in AUD/USD remains neutral at this point. On the downside, break of 0.7502 minor support will suggest that the corrective recovery from 0.7411 has completed. Intraday bias would be turned back to the downside for 0.7411 and below to resume the larger decline from 0.8135 to cluster support at 0.7328 (61.8% retracement of 0.6826 to 0.8135 at 0.7326). Above 0.7604 will extend the corrective rise. But we'd expect strong resistance from 38.2% retracement of 0.8135 to 0.7144 at 0.7688 to limit upside.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Prior break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

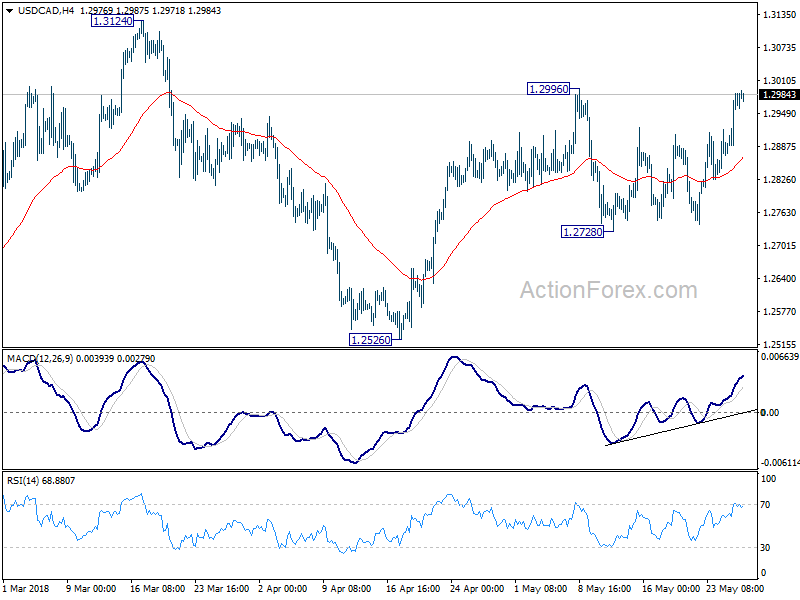

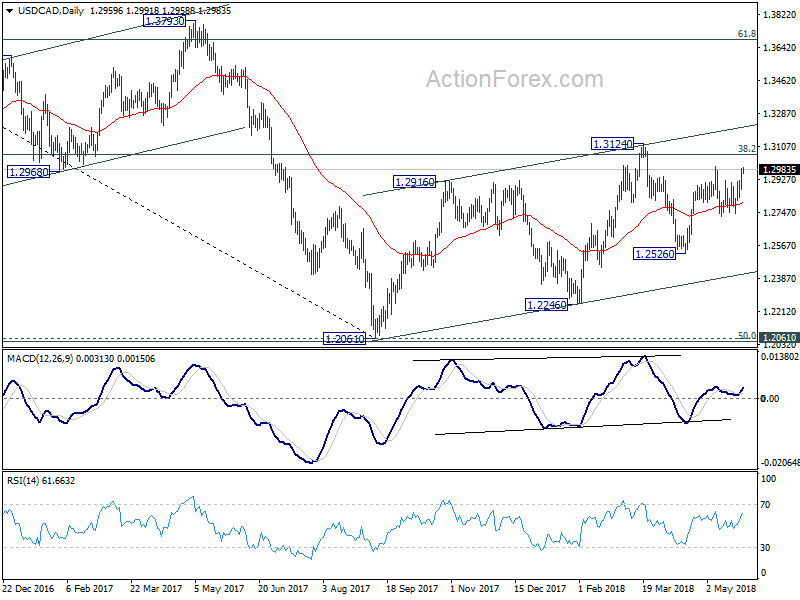

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2898; (P) 1.2945; (R1) 1.3020; More.....

At this point, USD/CAD is staying below 1.2996 resistance. Thus, intraday bias remains neutral first. Overall, we're holding on to the bullish view that rises from 1.2526, 1.2246, 1.2061 are not completed yet. Break of 1.2996 should confirm our view. In that case, intraday bias will be turned back to the upside for 1.3124 high next. Nonetheless, break of 1.2728 will dampen this bullish view and bring deeper fall back to 1.2526 and possibly below.

In the bigger picture, we're favoring the case that that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685. However, break of 1.2526 support will dampen this bullish view again. And, focus will be back on 1.2061 key support level, which is close to 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048.

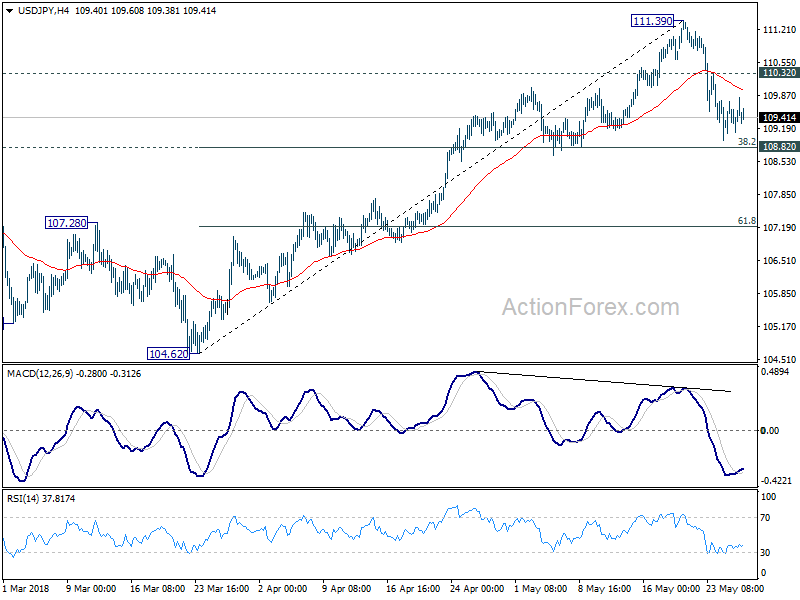

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.10; (P) 109.42; (R1) 109.71; More...

No change in USD/JPY's outlook. The correction from 111.39 could extend. But we'd expect support from 108.82 cluster support (38.2% retracement of 104.62 to 111.39 at 108.80) to bring rebound. On the upside, above 110.32 minor resistance will argue that the pull back is completed. And, in that case, retest of 111.39 high should be seen. However, firm break of 108.82 will dampen our view and bring deeper decline to 61.8% retracement at 107.20 and possibly below.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as108.82 support holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above. However, sustained break of 108.82 will dampen the bullish outlook and revive the case of a break of 104.62 low before bottoming.