Sample Category Title

EUR/AUD Weekly Outlook

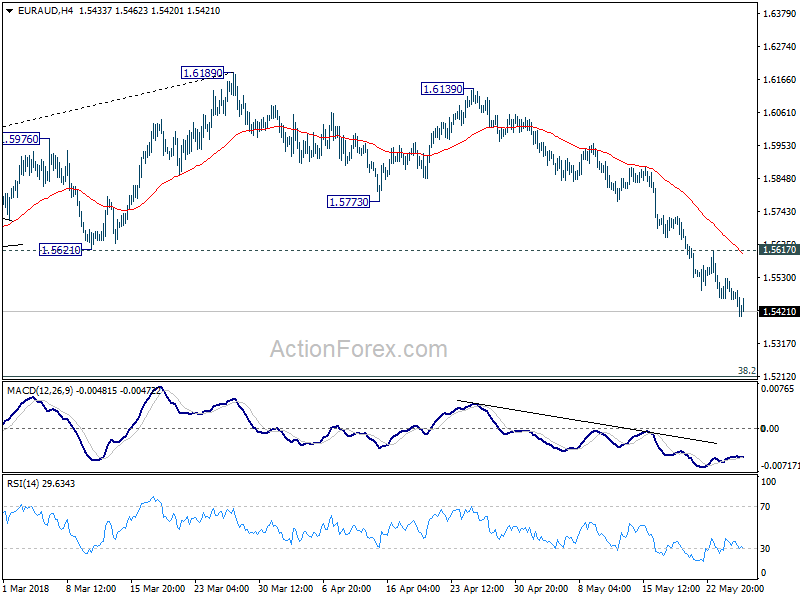

EUR/AUD's decline from 1.6189 continued last week extended to as low as 1.5404 last week. The strong break of 1.5621 support, indicates medium term reversal. Initial bias remains on the downside for 1.5153 key support level next. On the upside, break of 1.5617 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

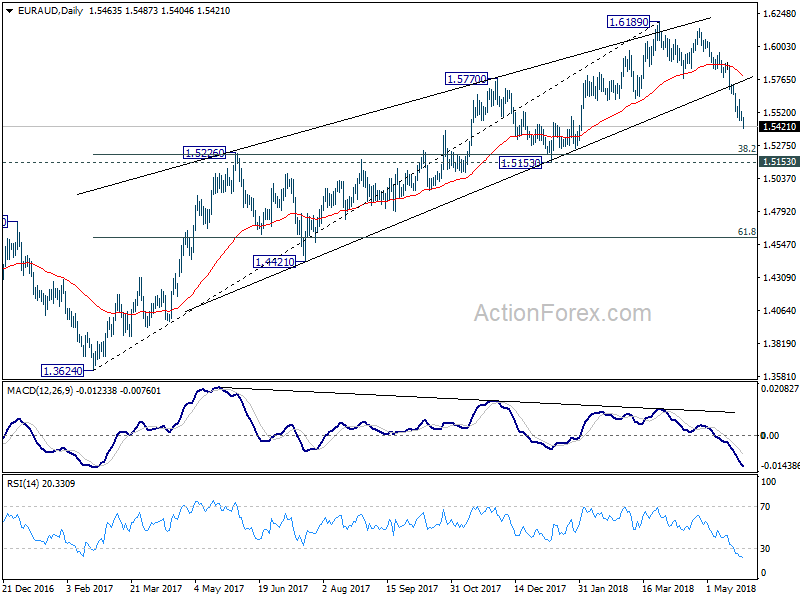

In the bigger picture, rally from 1.3624 (2017 low) should have completed at 1.6189 already, ahead of 1.6587 key resistance (2015 high). 1.6189 is seen as a medium term top. Deeper fall would be seen to 38.2% retracement of 1.3624 to 1.6189 at 1.5209 first. Decisive break there will pave the way to 61.8% retracement at 1.4604. In that case, we'll look for bottoming again below 1.4604. On the upside, firm break of 1.5773 support turned resistance is needed to indicate completion of the fall from 1.6189. Otherwise, further decline is expected in medium term, even in case of strong rebound.

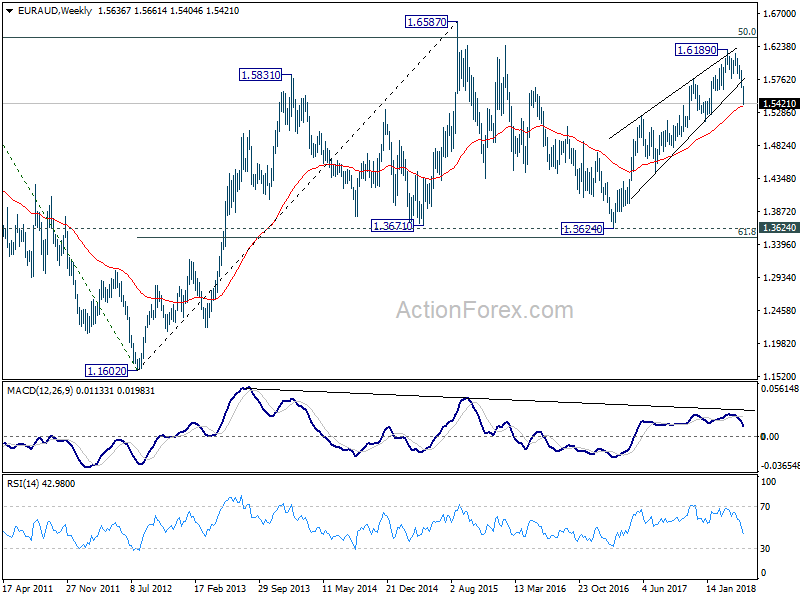

In the longer term picture, the rise from 1.1602 long term bottom (2012 low) isn't over yet. We'll keep monitoring the development but there is prospect of extending the rise to 61.8% retracement of 2.1127 to 1.1602 at 1.7488 and above. However, sustained trading below 1.3624 key support should indicate long term reversal and target 1.1602 long term bottom again.

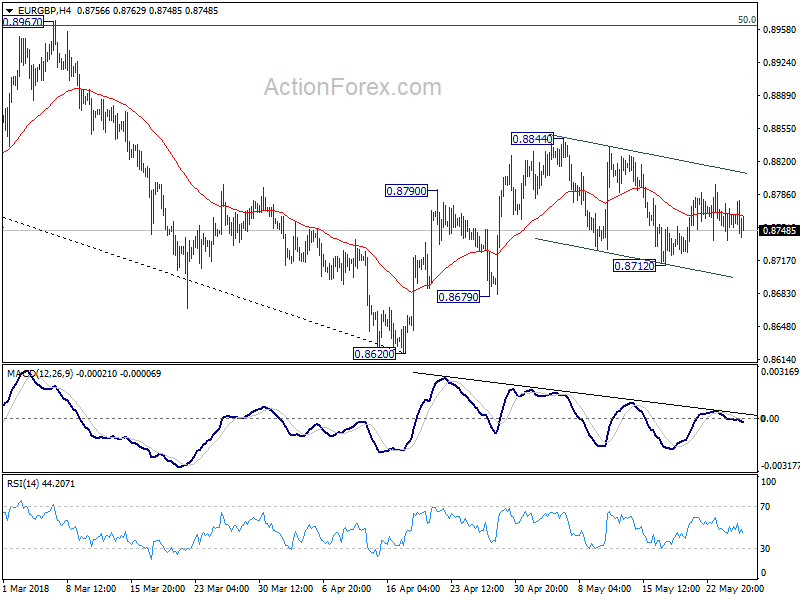

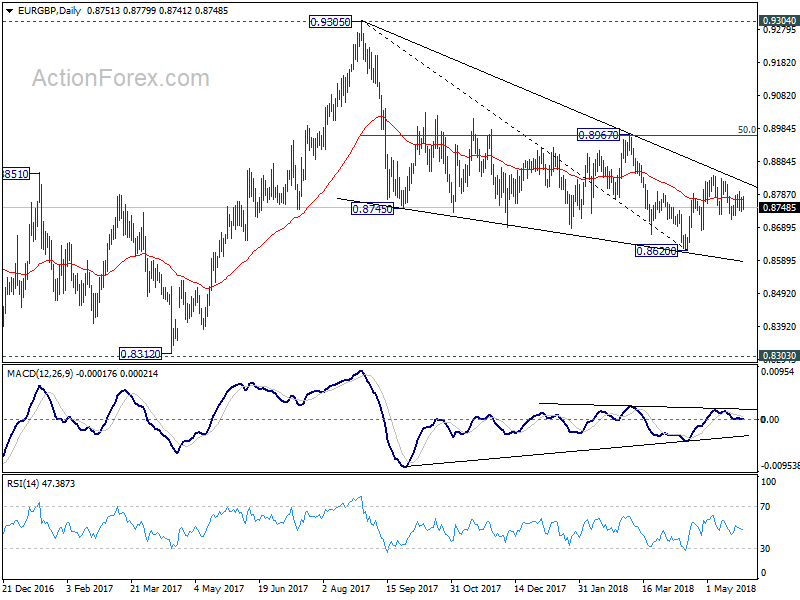

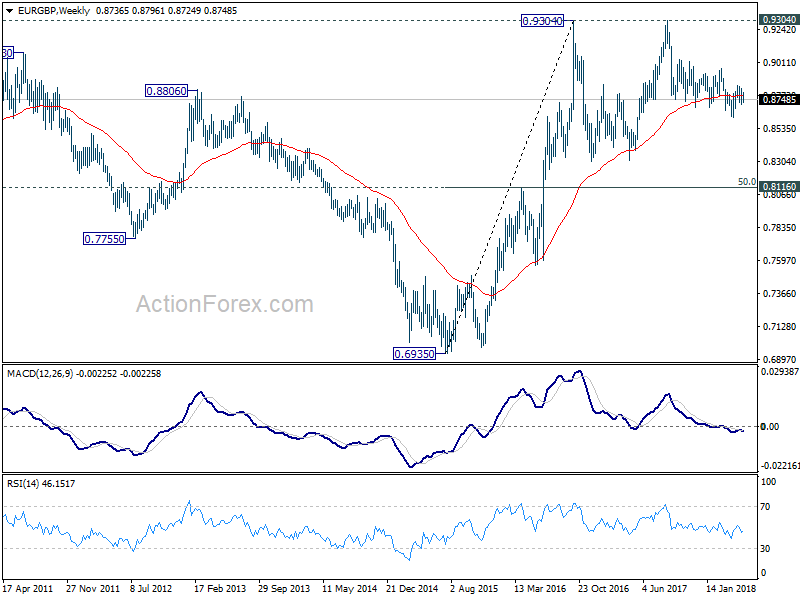

EUR/GBP Weekly Outlook

EUR/GBP gyrated inside range of 0.8712/8844 last week and outlook is unchanged, staying mixed. Initial bias remains neutral this week first. On the upside, break of 0.8844 will resume the rebound from 0.8620. That will also revive the case of larger bullish reversal. EUR/GBP should target target 0.8967 cluster resistance (50% retracement of 0.9305 to 0.8620 at 0.8963) first. However, break of 0.8679 minor support should completion of the rebound form 0.8620. And intraday bias will be turned back to the downside for this support. Whole decline from 0.9305 will likely be resuming too.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

In the long term picture, we're holding on to the view that rise from 0.6935 (2015 low) is resuming the up trend from 0.5680 (2000 low). Hence, after the consolidation from 0.9304 completes, we'd expect another medium term up trend through 0.9799 to 100% projection of 0.5680 to 0.9799 from 0.6935 at 1.1054.

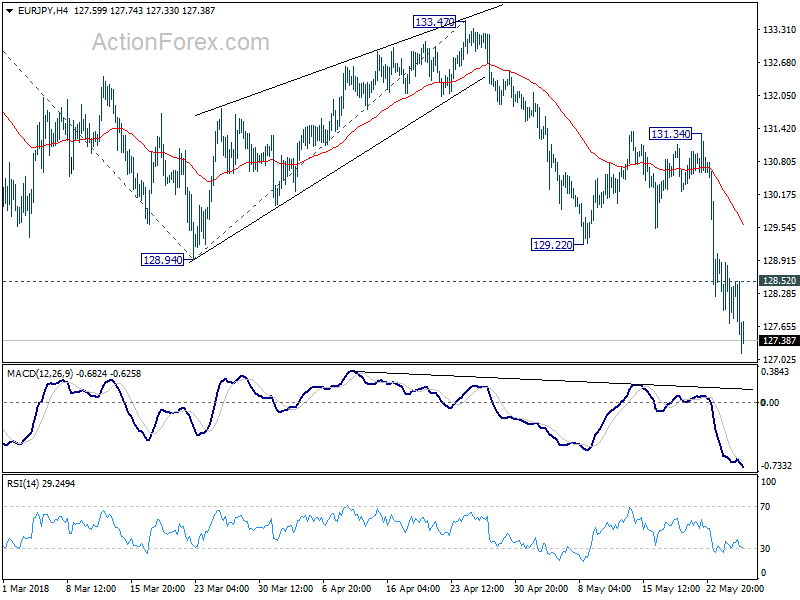

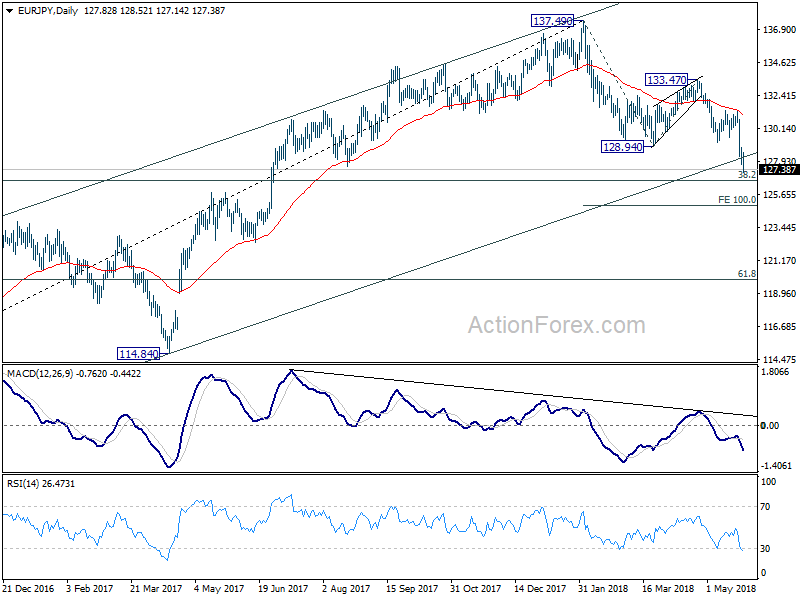

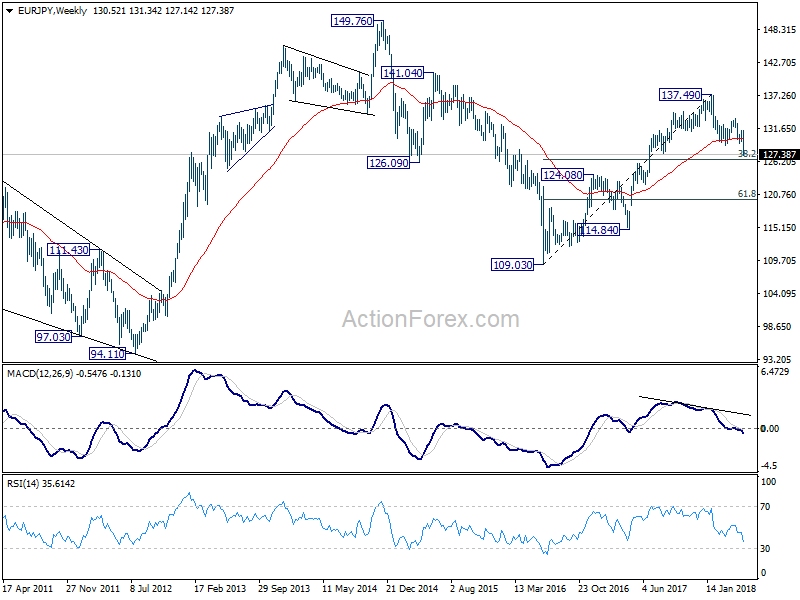

EUR/JPY Weekly Outlook

EUR/JPY's fall from 137.49 resumed last week and dived to as low as 127.14. There is no clear sign of bottoming yet. Initial bias remains on the downside this week for 126.61 medium term fibonacci level. But based on current momentum, EUR/JPY could dive through this level to 100% projection of 137.49 to 128.94 from 133.47 at 124.92. On the upside, above 128.52 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 131.34 resistance holds, even in case of recovery.

In the bigger picture, bearish divergence in daily MACD and current strong downside momentum is raising the chance of medium term trend reversal. Sustained break of 38.2% retracement of 109.03 to 137.49 at 126.61 will argue that whole up trend from 109.03 has completed at 137.49 already. And, deeper decline would be seen to 61.8% retracement at 119.90 and below. Though, strong support from 126.61 and rebound from there would revive medium term bullish for another high above 137.49.

In the long term picture, at this point, EUR/JPY is staying in long term sideway pattern, established since 2000. Rise from 109.03 is seen as a leg inside the pattern. As long as 124.08 support holds, further rally is in favor in medium to long term through 149.76 high. However, break of 124.08 could extend the fall through 109.03 low instead.

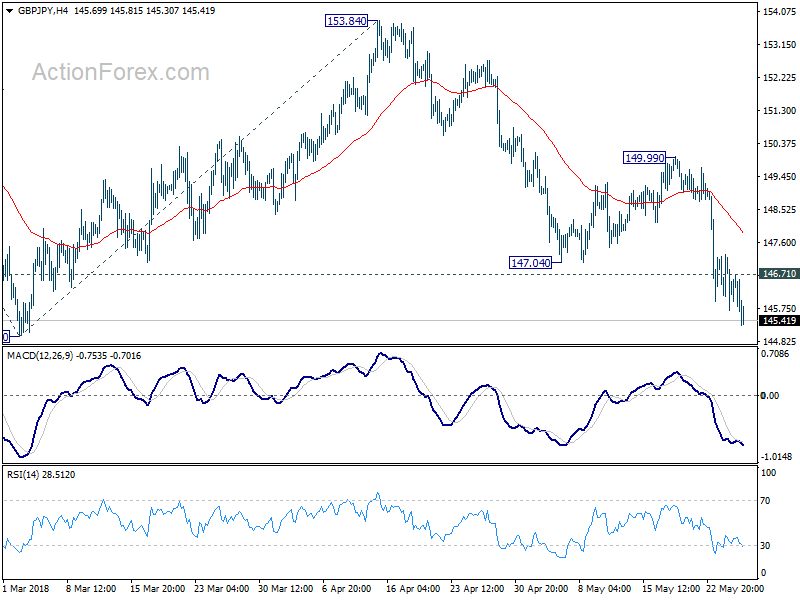

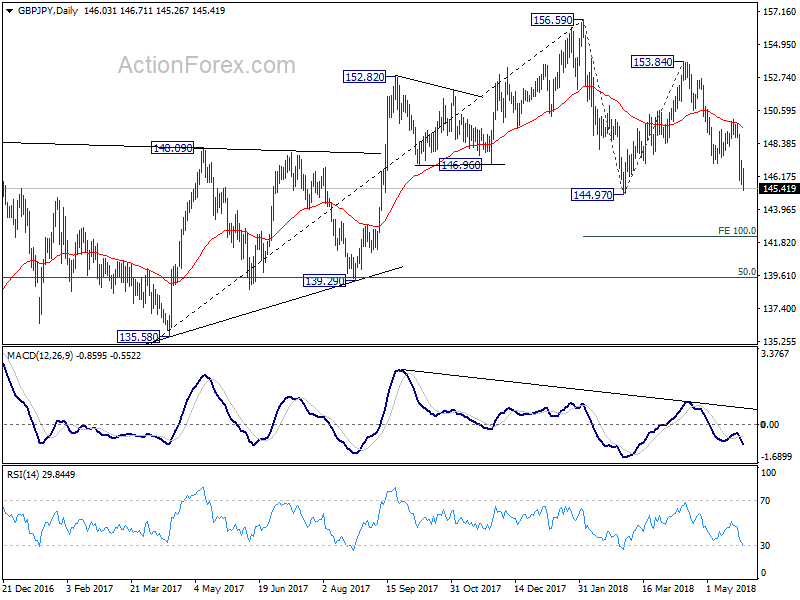

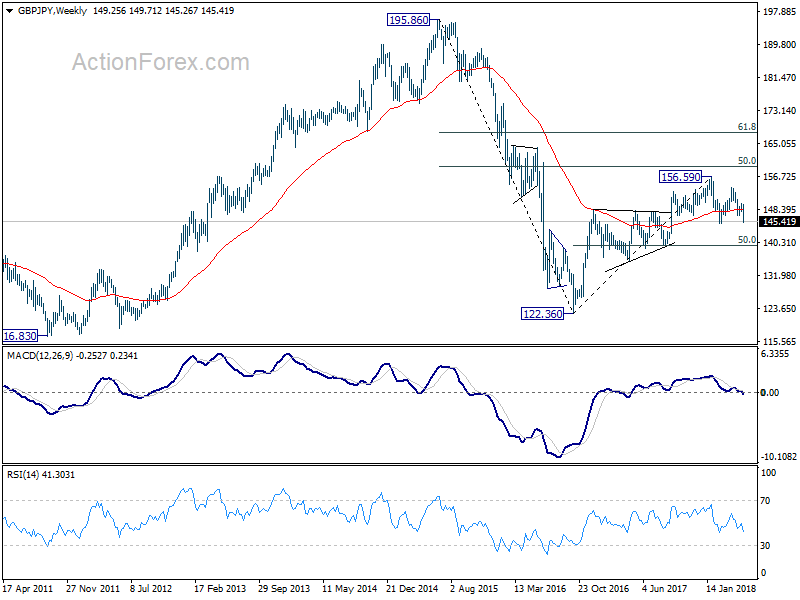

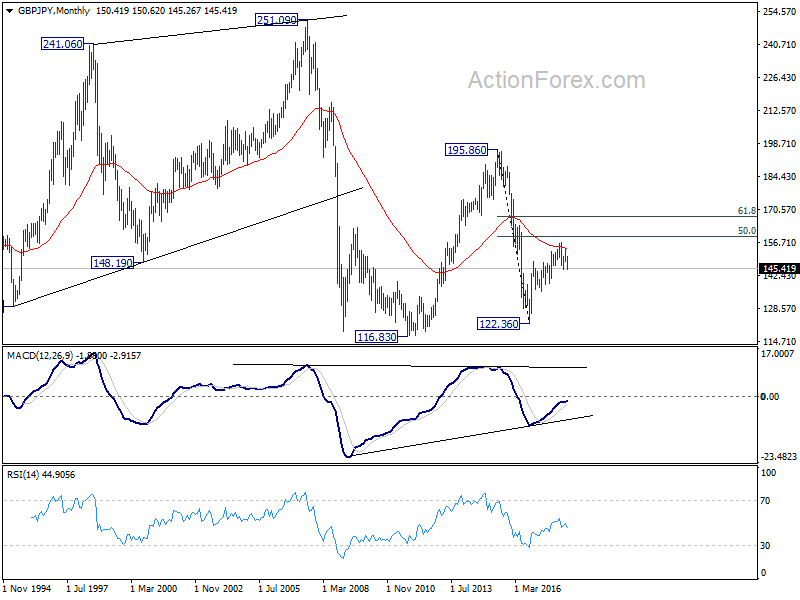

GBP/JPY Weekly Outlook

GBP/JPY's fall from 153.84 resumed last week and dropped to as low as 145.26. Initial bias is on the downside this week for 144.97 support. Decisive break there will resume the decline from 156.69 too and target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next. On the upside, above 146.71 minor resistance will turn intraday bias neutral and bring consolidation. But near term outlook will remain bearish as long as 149.99 resistance holds.

In the bigger picture, for now, we're treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

In the longer term picture, the failure to sustain above 55 month EMA (now at 153.94) is mixing up the outlook. Nonetheless, as long as 139.29 holds, rise from 122.26 is in favor to extend to 50% retracement of 195.86 (2015high) to 122.36 (2016 low) at 159.11, and possibly further to 61.8% retracement at 167.78 before completion. However, firm break of 139.29 will turn focus back to 116.83/122.36 support zone instead.

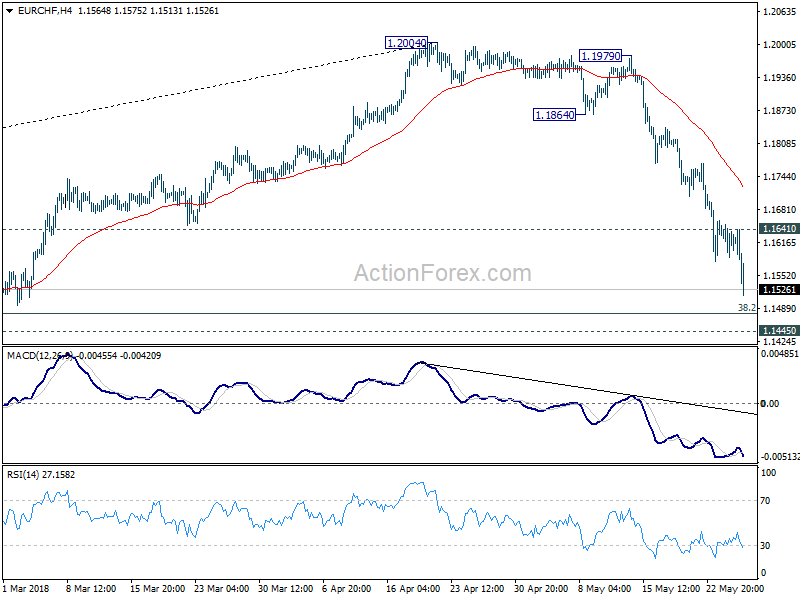

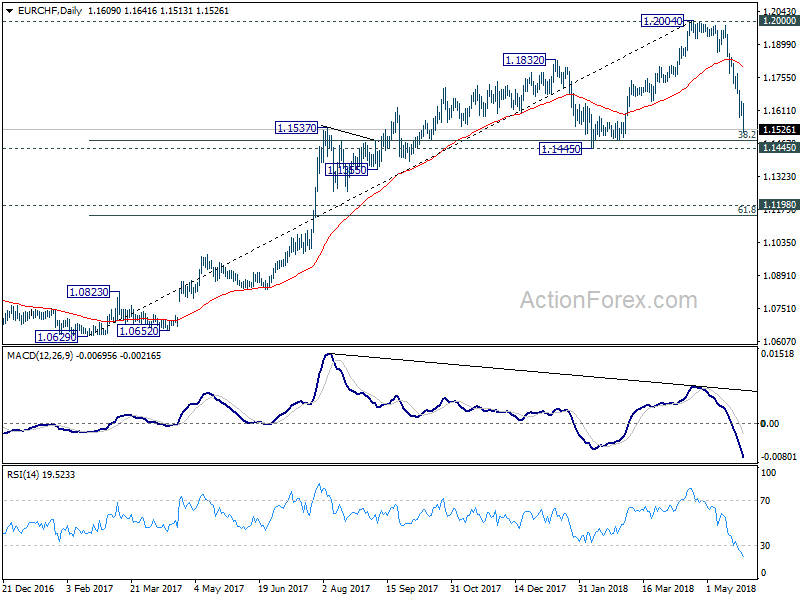

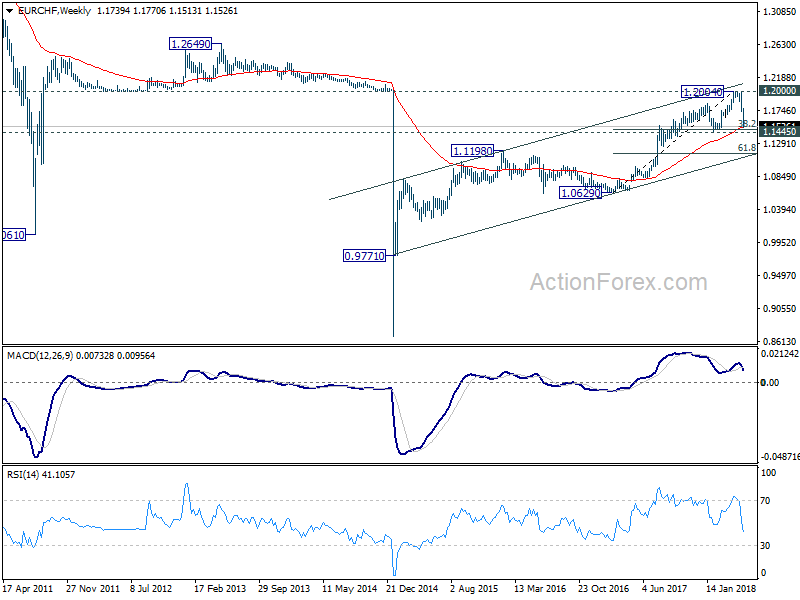

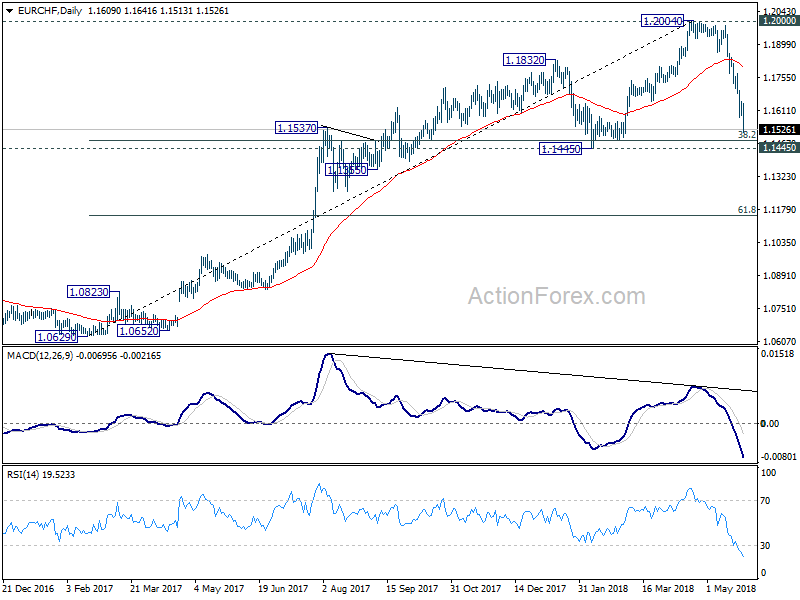

EUR/CHF Weekly Outlook

EUR/CHF's fall from 1.2004 accelerated steeply to as low as 1.1531 last week. The development confirmed medium term topping at 1.2004. Initial bias is on the downside this week for 1.1445 key support zone. For now, we'd expect strong support from 1.1445 to contain downside, at least on first attempt, to bring rebound. On the upside, above 1.1641 minor resistance will turn bias to the upside for rebound.

In the bigger picture, current development suggests solid rejection by prior SNB imposed floor at 1.2000. Considering bearish divergence condition in daily MACD, 1.2004 should be a medium term top. And price action from 1.2004 is correcting the up trend from 1.0629. Hence, for now, deeper fall could be seen back to 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479. We'd expect strong support from there to bring rebound to extend the medium term corrective pattern. However, sustained break of 1.1445 will target next key cluster level at 1.1198 (2016 high), 61.8% retracement of 1.0629 to 1.2004 at 1.1154.

Yen Surged Again as Italy, Protectionism, Geopolitics and Central Bank Expectations Weighed on Yields

Yen ended as the strongest one last week followed by Swiss Franc. Meanwhile Sterling was the weakest one, followed by Euro, Canadian and then US Dollar. A number of factors were behind such development and they're all inter-related. The most direct one is decline in major European and US treasury yields. Concerns on the new government of Italy is a main driver to the steep widening of German-Italian yield spread. On the background, the weak batch of Eurozone economic data raised questions on whether ECB would end the asset purchase program this year. Weaker than expected inflation data from UK also lowered the chance of an August BoE hike and sent UK yields lower

In the US, 10 year yield failed to sustain above 3% level and dropped sharply as markets saw some dovish tweak in the FOMC minutes. Indeed, markets have pared back some of the bets on Fed's tightening path. US President Donald Trump order commerce secretary Wilbur Ross to start a Section 232 national security investigation on auto imports. And he's considering to impose as much as 25% tariffs on imported cars. That could have a big impact of major car exporters to the US, including Mexico, Canada, Japan and Germany.

Also Trump cancelled his summit with North Korean leader Kim Jong Un after North Korea attacked Vice President Mike Pence. But then Trump said on Saturday that he's working on reinstating the June 12 Summit. Trade negotiations with China seemed to be heading to the right direction but Trump said he's "dissatisfied". Adding to these factors, oil price tumbled sharply as OPEC and Russia could raise production later this year. Falling oil price is for certain not a positive drive in inflation expectations.

All those factors, geopolitical risks, protectionism, economic outlook, inflation expectations, central bank expectations etc, prompted rush to safe haven in bonds. Yen and Swiss Franc surged, following the sharp decline in yields.

Moody's put Italy's rating on review, that said it all about new Italian government

The representative of the 5-Star Movement and the League coalition Giuseppe Conte was given a mandate by Italian President Sergio Mattarella to form a government. The direction of the coalition's fiscal policy is very clear. In the "Contract for the Government of Change" agreement, it's already said that "the government's actions will target a programme of public debt reduction not through revenue based on taxes and austerity, policies that have not achieved their goal, but rather through increased GDP by the revival of internal demand."

Rating agency Moody's on Friday put Italy's "Baa2" debt rating on review for a possible downgrade. And the move is quite representative of what the markets think about the coalition. Moody's said in the statement that "far from offering the prospect of further fiscal consolidation, the 'contract' for government signed by the two parties includes potentially costly tax and spending measures, without any clear proposals on how to fund those." And, the country is facing "significant risk of a material weakening" in its fiscal strength.

Italy 10 year yield jumped -0.23% over the week to close at 2.46% as sell off in Italian bonds extended. , hitting the highest level in four years.

At the same time, German 10 year bund yield closed the week down -0.17% to 0.41%, breaking 0.50% key support level. And that's nearly half of February's high at 0.77

At the same time, German 10 year bund yield closed the week down -0.17% to 0.41%, breaking 0.50% key support level. And that's nearly half of February's high at 0.77

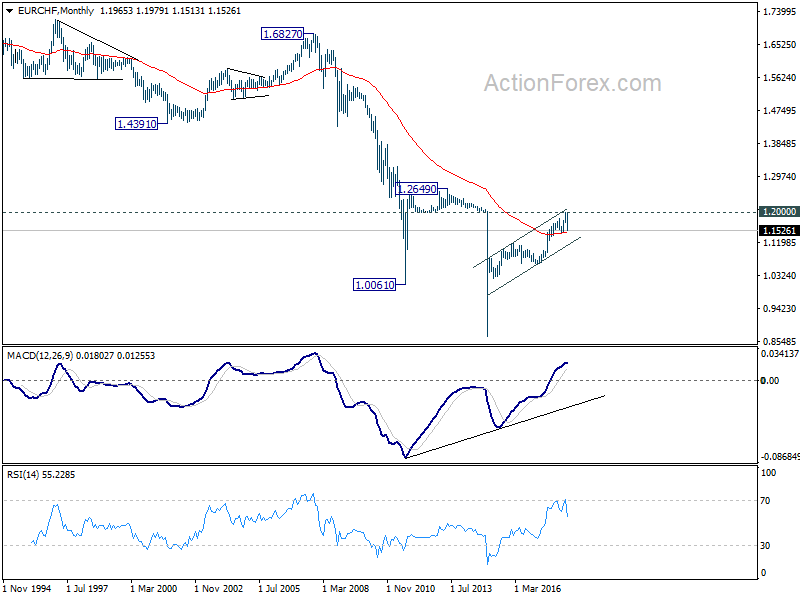

The development is clearly mirrored in EUR/CHF as the fall from 1.2004 accelerated to close at 1.1526, after rejection by 1.2000 handle. For now, we'd still expect strong support from 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479, to bring rebound. But we'll see if it's developing into a deeper fall and larger down trend.

The development is clearly mirrored in EUR/CHF as the fall from 1.2004 accelerated to close at 1.1526, after rejection by 1.2000 handle. For now, we'd still expect strong support from 1.1445, which is close to 38.2% retracement of 1.0629 to 1.2004 at 1.1479, to bring rebound. But we'll see if it's developing into a deeper fall and larger down trend.

Eurozone data continued to indicate slowdown, but pace might be troughing

Staying in the Eurozone, in the April meeting accounts, ECB offered not nothing new to the markets, but just a little more cautiousness. Despite recent moderation in activity, data remained consistent with "solid and broad-based expansion". And underlying economic strength added to the Governing Council's "confidence" that inflation will "gradually" move back to 2% target over medium term. But since underlying inflation remain subdued, without signs of sustained upward trend, "patience, persistence and prudence with regard to monetary policy remained warranted."

Risks to outlook remain "broadly balanced". But ECB pointed to "risks related to global factors, including the threat of increased protectionism". ECB noted that those risks "had become more prominent and warranted monitoring with regard to their implications for the medium-term outlook for growth and prices.

Though, economic data from Eurozone offered some hope. Eurozone PMI manufacturing dropped to 55.5 in May, down from 56.2, missed expectation of 56.0, hitting 15-month low. PMI services dropped to 53.9, down from 54.7, missed expectation of 54.7, hitting, 16-month low. PMI composite dropped to 54.1, down from 55.1, hitting 18-month low. But as Markit noted, "despite the headline PMI dropping to an 18-month low, the survey remains at a level consistent with the Eurozone economy growing at a reasonably solid rate of just over 0.4% in the second quarter."

German Ifo business climate rose to 102.2 in May, up from 102.1 and beat expectation of 102.0. Ifo President Clemens Fuest noted in the release that "the declining trend in the Ifo Business Climate has stopped." And "the current business survey and other indicators point to economic growth of 0.4 percent in the second quarter." There could be a turn around in the next batch of data.

Chance of BoE August hike got slimmer after mixed data

From UK, headline CPI slowed for the third month in a row to 2.4% yoy in April, down from 2.5% yoy and missed expectation of 2.5% yoy. Core CPI also slowed to 2.1% yoy, down from 2.3% yoy and missed expectation of 2.2.% yoy.

Headline retail sales was a present surprise as they jumped 1.6% mom in April, much higher than expectation of 0.7%. However, as ONS noted, "the effects of the adverse weather on sales introduces further volatility to the monthly growth rate in April 2018." And, "combining March and April to compare the two months with the same two months a year earlier provides a more stable picture of the year-on-year growth". Combining both March and April, sales grew 1.3% in 2018, much lower than 2.9% back in 2017.

Meanwhile, there was some hope for an upward revision in the dismal 0.1% qoq growth in Q1. But it's left unrevised in the second revision. For now, there is not much chance of an August hike by BoE, even though a November hike is still on the table.

UK 10 year gilt yield also tumbled sharply and lost -0.18% over week to close at 1.32%. The break of March low at 1.35% also suggests resumption of the down trend from February's high at 1.65%. That's a factor pounding GBP/JPY down -2.54%, as the worst performer of the week.

Traders paring Fed hike bet after FOMC minutes and political developments

In the US, FOMC minutes are seen as giving some dovish tweaks to the markets. In particular, the minutes emphasized "the aim of keeping inflation near its longer run symmetric objective", suggesting that a certain degree of inflation overshoot would be tolerable. Meanwhile, the Fed appeared to have confirmed that a June rate hike is in place. Yet, it made no indication on the path after that. Adding to that there were increased talks on the topic of neutral rate. It's being seen as between 2.50-3.00% by Fed officials. That is, federal funds rate, currently at 1.50-1.75%, could be just 4 hikes away from neutral. 2019 could mark the end of Fed's tightening cycle.

The FOMC minutes and political developments in the US prompted traders to pare back some of Fed hike expectation. Fed fund futures are now pricing just 90% chance of a June hike to 1.75-2.00%, down from prior week's 100%.

For September meeting, fed fund futures are pricing in 54.84% chance of hiking to 2.00-2.25% or higher. That compares to prior week's pricing of over 80% chance.

10 year yield rejected by key long term resistance zone

10 year yield tumbled sharply to close at 2.931 last week, taking out 3.000 handle rather decisively. The development confirmed short term topping at 3.115. Some support might be seen from 55 day EMA (now at 2.918) initially. But the correction will likely extend back to 2.701/717 support zone (38.2% retracement of 2.033 to 3.115 at 2.701) before completion. For now, we'd not expect a firm break of 3.115 high in near term. Instead, even in case of rebound, it should just be part of a correction pattern.

We'd also like to reiterated that TNX has just touch a key long term resistance zone. 2013 high at 3.036 marks the start of the zone. On the upside, it's the multi-decade trend line resistance at around 3.20. Sustained break of this resistance zone will confirm reversal of this multi-decade trend, with a double bottom pattern (1.394, 1.336) in the monthly chart. That would mark the end of an era of persistently falling US yields.

Current pull back is not unexpected based on the importance of this resistance zone. From a medium term point of view, we'll stay bullish in TNX and expect an eventual upside breakout as long as it stays above the flat 55 month EMA (now at 2.267).

Dollar index pressing 94.19 fibonacci level

Dollar index is pressing an important fibonacci level at 38.2% retracement of 103.82 to 88.25 at 94.19. Upside momentum is seen diminishing in daily MACD. The index is vulnerable to a pull back and break of last week's low at 93.75 could start a correction back towards 92.24 support. Nonetheless, before that, further rise is still expected. Sustained break of 94.19 will pave the way to 97.87.

Oil slump dragged down Canadian Dollar, BoC and trade development watched

Finally, we'd like to have a look at oil price. WTI crude oil lost -4.8% over the week to close at 67.88 level. Talk of OPEC and Russia raising production is a key factor. The total of boost in production from OPEC and non-OPEC countries could add up to as high as 1 million barrels a day. The decision could be made as soon as during the next OPEC meeting on June 22 in Vienna. Meanwhile USD 80 a barrel seems to be a psychological level that the oil producing countries want to avoid.

Technically, considering bearish divergence condition in daily MACD, 72.83 is likely a medium term top. For now, we'd see price actions from 72.83 as correcting the rise from 42.05 only. For now, some support could be seen from 55 day EMA (now at 67.58). But eventually, deeper fall should be seen to 38.2% retracement of 42.05 to 72.83 at 61.07 before completing the correction.

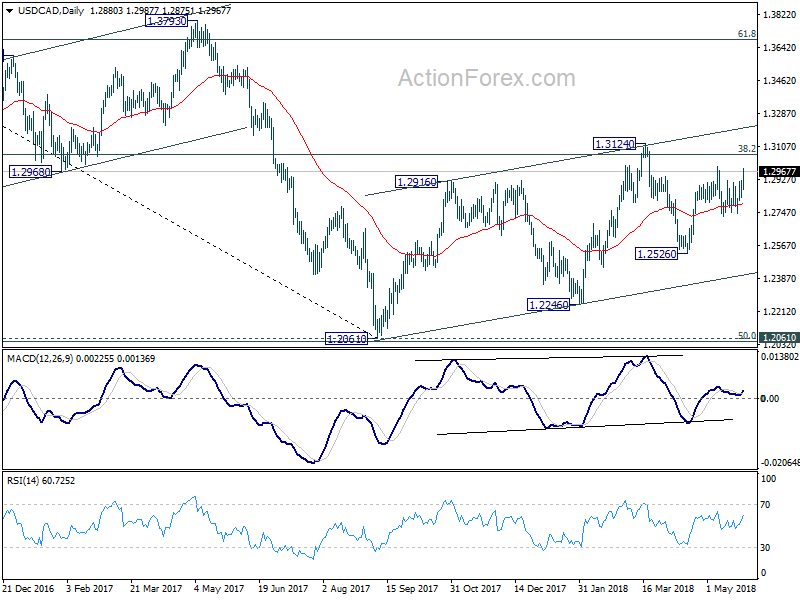

USD/CAD jumped sharply last week following the sharp fall in crude oil. The support from 55 day EMA affirmed our bullish view that rise from 1.2061 is still in progress for above 1.3124. Canadian dollar will be facing risk of BoC rate decision this week. This is little chance for BoC to hike from the current 1.25%. The Canadian economy is current clouded with a lot of uncertainties. NAFTA negotiation is still dragging on. It's unsure what comes next when the temporary exemption on US steel tariffs expire on June 1. And, Trump's push in auto tariffs could also have an impact. Canadian Dollar could be vulnerable to another fall on BoC statement, trade relationship with the US and oil price.

EUR/JPY Weekly Outlook

EUR/JPY's fall from 137.49 resumed last week and dived to as low as 127.14. There is no clear sign of bottoming yet. Initial bias remains on the downside this week for 126.61 medium term fibonacci level. But based on current momentum, EUR/JPY could dive through this level to 100% projection of 137.49 to 128.94 from 133.47 at 124.92. On the upside, above 128.52 minor resistance will turn intraday bias neutral first. But near term outlook will remain bearish as long as 131.34 resistance holds, even in case of recovery.

In the bigger picture, bearish divergence in daily MACD and current strong downside momentum is raising the chance of medium term trend reversal. Sustained break of 38.2% retracement of 109.03 to 137.49 at 126.61 will argue that whole up trend from 109.03 has completed at 137.49 already. And, deeper decline would be seen to 61.8% retracement at 119.90 and below. Though, strong support from 126.61 and rebound from there would revive medium term bullish for another high above 137.49.

In the long term picture, at this point, EUR/JPY is staying in long term sideway pattern, established since 2000. Rise from 109.03 is seen as a leg inside the pattern. As long as 124.08 support holds, further rally is in favor in medium to long term through 149.76 high. However, break of 124.08 could extend the fall through 109.03 low instead.

Trump in very productive talks with North Korea to reinstate the summit with Kim

After a week of exchange in words, the summit between Trump and Kim Jong Un is back on the table. Trump tweeted

https://twitter.com/realDonaldTrump/status/1000174070061813761

Trump suddenly pulled out of the summit on Thursday, after strong words from North Korean Vice Foreign Minister Choe Son-Hui issued a strong statement criticizing US Vice President Mike Pence. Trump sent an open letter to Kim Jong Un through the White HOuse announcing the cancellation.

But North Korea responded by hailing that “we have inwardly highly appreciated President Trump for having made the bold decision, which any other U.S. presidents dared not, and made efforts for such a crucial event as the summit.” Though, “His sudden and unilateral announcement to cancel the summit is something unexpected to us and we can not but feel great regret for it."

It remains to be seen whether the summit will happen on not.

The Weekly Bottom Line: Markets Respond to Geopolitics and the Fed

U.S. Highlights

- U.S. trade tensions with China have temporarily subsided, however they have flared up elsewhere, as President Trump ordered a review of U.S. automotive imports.

- Trade tensions were also flagged as a key risk in the latest FOMC minutes. However, the Committee remained in agreement that it would soon need to "take another step" in removing monetary accommodation.

- Falling affordability and lack of inventory, continued to weigh on the U.S. housing market activity. After a weak first quarter, existing home sales have started the second quarter on a weak footing, falling 2.5% in April. Sales of new homes also declined during the same month.

Canadian Highlights

- Oil was driving Canadian markets, as indications from OPEC and Russia that more supply may be coming sent the benchmark WTI contract below U.S. $69/barrel. This weakened the S&P/TSX index, and shaved a cent from the loonie.

- On the economic data front, it was a quiet week as wholesale trade reaffirmed the theme of solid economic data for March. Canada seems to have shaken off the soft start to the year. Real GDP for the first quarter is expected to be reported at 1.8% q/q annualized, with solid momentum heading into the second quarter.

- External developments were less constructive. U.S. threats of auto tariffs have thrown yet another wrench into NAFTA renegotiations, further dimming the prospects for a near-term conclusion.

U.S. - Markets Respond to Geopolitics and the Fed

The FOMC minutes, renewed trade tensions and a cancellation of the June summit with North Korea made the week anything but boring for investors. It was also a politically-charged week across the Atlantic. U.K. negotiations with the EU soured over U.K.'s participation in the Galileo satellite project, while the new Italian Eurosceptic government appointed Giuseppe Conte as prime minister.

Financial markets rallied on Monday on the news of positive weekend developments in the U.S.-China trade dispute. Details of the agreement were vague and largely unquantifiable as far as trade deficit reduction targets are concerned. In the follow-up statement China agreed to "meaningfully" increase imports of U.S. agricultural and energy products, and lowered tariffs on imports of autos and parts. These relatively limited concessions were sufficient to put the proposed tariffs on $50 billion worth of Chinese goods set to take effect on May 21 on hold.

Although U.S. trade tensions with China have eased for now, they have flared up elsewhere, weighing on market sentiment later in the week. On Wednesday President Trump ordered a review of automotive imports, citing national security concerns. The decision drew sharp international criticism and warnings of retaliatory tariffs, but was also opposed domestically. Automakers as well as Republican lawmakers expressed concerns that, if imposed, auto tariffs will raise auto prices for consumers, disrupt supply chains, start trade wars and alienate U.S. allies.

Worries about trade also showed up in the FOMC minutes. Specifically, the FOMC members acknowledged that trade uncertainty could hurt business sentiment and investment intentions. As for the monetary policy discussion, the FOMC members agreed that they would soon need to "take another step" in removing monetary accommodation, with a June rate hike looking like a done deal. At the same time they stressed that the Fed's inflation objective is "symmetric", suggesting they will allow inflation to temporarily overshoot 2%. All told, we remain of the view that a total of three rate hikes this year is the most likely outcome.

Higher interest rates will certainly have an impact on the housing market. After declining by 6% in the first quarter, existing home sales have started the second quarter on a weak footing as activity fell 2.5% in April. Sales of new homes also took a break in April, declining by 1.5%. Since the start of the year, the average rate on a 30-year mortgage rose by 70 basis points. Rising rates alongside brisk growth in home prices have dented affordability; however, this is only part of the story behind relatively tepid home sales. Low inventory of houses on the market has been the most important factor restraining resale activity (Chart 1), but the pace of construction remains modest and will likely be contained by labor shortages and rising input costs. The price of American steel rose 40% this year, while lumber prices are up 34%. Some relief to the housing shortage may come as more existing homeowners, with fully rebuilt home equity (Chart 2), become encouraged to list their homes. However, the overall pace of activity in the housing market will likely once again remain modest this year.

Canada - Solid Data, Shaky Backdrop

The shortened trading week saw oil prices once again in the driver's seat for Canadian markets. OPEC and Russia indicated a willingness to expand supply by around 1 million barrels per day to offset production losses elsewhere. Traders reacted by sending the benchmark West Texas Intermediate (WTI) contract lower. After starting the week north of U.S. $72 per barrel, it now looks set to end it south of $69. This adjustment pushed the TSX composite index slightly lower. The bigger impact was on the loonie, which was down more than a cent at the time of writing, appearing set to end the week around 77 cents U.S.

In contrast to market developments, the past week was a bit quiet on the data front, but continued the recent theme of outperformance. A 0.8% gain in wholesale trade volumes rounded out the 'real' data for March, joining other indicators in breaking out from recent trends (Chart 1). As expected, it's now clear that the slow start to the year was a reflection of one-off factors rather than any dramatic shift in underlying economic conditions.

That said, the improvement in Canada's recent economic performance has come a bit too late to meaningfully impact first quarter growth. Next Thursday's GDP data is expected to reveal a 1.8% annualized pace of growth, driven by consumer spending and non-residential investment. This is a bit above initial expectations and in-line with Canada's trend pace. Importantly, the same report should reveal solid momentum heading into the second quarter. Regardless, it will be a day late for the Bank of Canada to incorporate in next Wednesday's interest rate decision. First quarter growth may be set to come in above their April forecast, but with housing markets still in an adjustment phase and considerable external uncertainties, no change in monetary policy is expected.

To this point, it is hard to see many signs of improvement in the external backdrop. President Trump this week announced a review of auto imports along national security lines – similar to the process that led to aluminum and steel tariffs (of note, Canada's exemption is set to expire next Friday, June 1). While an exemption for Canada is possible, it represents another, much larger threat to Canadian exporters. With highly integrated supply chains across North America, auto tariffs of up to 25% (as reported) would have a disastrous impact on all NAFTA members (Chart 2). Not only are motor vehicles an important part of North American trade, imported vehicles, regardless of origin, remain in demand, as shown by U.S. sales figures. About half of the new vehicles sold in the U.S. in 2017 were imported (roughly 1 in 4 from Mexico or Canada). Any tariff, let alone one of 25%, will be felt by U.S. consumers.

President Trump's latest threat may ultimately prove to be another negotiating tactic in the ongoing NAFTA saga, particularly since such a visible price increase is unlikely to be popular among voters. But, it adds yet another challenge to already difficult negotiations. Not only does the auto file remain murky, there have been few signs of progress in other contentious areas, such as dispute resolution. Given the realities of the North American political calendar (Mexican presidential elections in July, U.S. midterms in November) it appears that this cloud of uncertainty will be sticking around for some time to come.

U.S.: Upcoming Key Economic Releases

U.S. Employment - May

Release Date: June 1, 2018

Previous Result: 164k; unemployment rate: 3.9%

TD Forecast: 200k, unemployment rate: 3.9%

Consensus: 190k, unemployment rate: 3.9%

We expect nonfarm payrolls to pick up by 200k in May. The weaker than expected sub-200 prints over March and April partly reflected weather related impacts, suggesting some giveback. However, limiting the rebound is the late stage of this expansion which has contributed to the steady fall in the average pace of payrolls gains (190k vs its peak of 260k in early 2015). Employment surveys (ISM non-manufacturing in particular) also point to more moderate job gains in the months ahead. We therefore see limited scope for substantial upside above 200k.

We expect the unemployment rate to stabilize at 3.9% assuming a stable participation rate, which inched lower in the prior month. We expect average hourly earnings to rise 0.2% m/m. With the 12th of the month landing on Saturday, reference week effects point to a weak print. However, mean reversion from the weak m/m April gain does bias the increase upward. A 0.2% m/m gain should keep the y/y pace unchanged at 2.6% y/y.

U.S. ISM Manufacturing Sales - May

Release Date: June 1, 2018

Previous Result: 57.3

TD Forecast: 58.2

Consensus: 58.0

We expect ISM to rebound to 58.2 in May, partially reversing its slide and leaving the index at a solid level consistent with above-trend growth. Regional surveys continued to paint a robust picture (Empire and Philly). Confirmation of a pickup would assuage concerns that sentiment is weakening, as indicated by our US survey surprise index, though risks like trade policy still remain.

Canada: Upcoming Key Economic Releases

Canadian Real GDP - Q1 & March

Release Date: May 31, 2018

Previous Result: 1.7% q/q (saar), 0.4% m/m

TD Forecast: 1.8% q/q (saar), 0.2% m/m

Consensus: 2.0% q/q (saar), 0.2% m/m

Soft data early in the quarter should hold Canadian growth to an on-trend pace of 1.8% (q/q, annualized). Beneath the modest headline are divergent domestic and external paths. Final domestic demand is expected to record a solid 3.5% expansion, while net exports are expected to drag on growth as outgoing shipments of goods were effectively flat. Healthy aggregate income growth and solid retail sales figures (notably auto sales) point to a roughly 3% pace of consumer spending. Residential investment is expected to record a 10.5% decline as a significant pullback in resale activity swamps still healthy construction activity. Conversely, a healthy, 4.5% pace of expansion in non-residential investment is likely, with broad-based gains anticipated as firms continue to recover from the pull-back of 2015/2016.

Industry-level GDP should post a 0.2% advance in March on strength from services with goods output impacted by maintenance shutdowns in the oil sands. Residential construction investment also decelerated in March, showing early signs of stress in response to the slowdown in the resale market. Manufacturing output should anchor the goods sector after a solid advance in factory sales and exports, while utilities should also contribute positively. On the other side of the ledger, services should benefit from strong retail and wholesale activity while ongoing housing market softness will continue to exert a drag on real estate. A 0.2% print would provide a decent hand-off to Q2, where GDP growth is tracking in line with the Bank of Canada's 2.5% estimate.

Summary 5/28 – 6/1

Monday, May 28, 2018

[php_everywhere instance="1"]

Tuesday, May 29, 2018

[php_everywhere instance="2"]

Wednesday, May 30, 2018

[php_everywhere instance="3"]

Thursday, May 31, 2018

[php_everywhere instance="4"]

Friday, Jun 1, 2018

[php_everywhere instance="5"]

Geopolitical Tensions Moderate Ahead of US Jobs Week

The US dollar was up against majors pairs on Friday ahead of the release of employment data in America. On a weekly basis the greenback gained against the CAD, EUR and GBP but lost ground against the JPY, AUD and CHF after five days that featured various geopolitical developments. Holidays in the United Kingdom and the United States will make for a short trading week, but one that will be filled with economic data releases alongside new reports from US-China and US-North Korea relations.

- Bank of Canada (BoC) to keep rate unchanged at 1.25%

- G7 Finance meetings to kick off on May 31

- NFP to add 190,000 jobs to US economy on Friday

Dollar Bounced Back as Tensions Ease on Friday

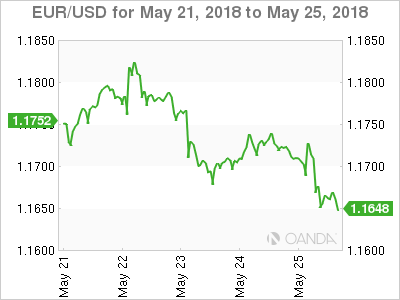

The EUR/USD lost 0.88 percent in the last five days. The single currency is trading at 1.1665 after the dollar recovered some ground after North Korea issued some comments that indicated that the June 12 meeting is still a possibility even if the US is not a part of the peace process and would be willing to meet with President Trump. The US Central bank made it clear it is willing to let economy run hot which was taken as a dovish statement by the markets. The Fed notes from the May Federal Open Market Committee (FOMC) meeting were not as hawkish as expected but central bank members still see the need to keep hiking rates albeit rising inflation would not be a deciding factor at this time to dictate the pace of rate hikes. A June rate lift has been fully priced in by the market with another two more rate hikes this year a strong possibility.

The Fed’s minutes were slightly dovish, the European Central Bank (ECB) notes from the lates monetary policy meeting were also released the same week with a very neutral view on the European economy. On the one hand growth could slow down further button the other the current expansion remains solid. The ECB continued to not give any hints on what it plans to do in September when its massive quantitive easing program comes to an end. The central bank has a new headache as it has begun to lock horns with the newly formed Italian government’s plans to approve new spending projects that could break the EU budget rules.

Italy has a 132 percent debt to GDP ratio which is above the 60 percent permitted by the EU. Greece has a similar ratio which in itself will be a mark against the EUR as the EU will face its toughest challenge from a euro sceptic government in the new 5 Star movement and League coalition.

The biggest economic release in the market will come on Friday, June 1 with the publication of the U.S. non farm payrolls (NFP) report at 8:30 am EDT. The forecast is calling for a gain of 190,000 jobs after a strong 164,000 gain last month. Hourly wages will be in focus with a gain of 0.3 percent expected. The Fed is not worried about the US economy staying above 2 percent for long but it will be a decisive factor in the number of rate hikes in 2018.

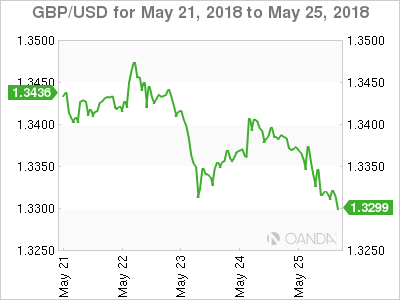

Pound Lower as BoE Warns of Brexit Disruption

The GBP/USD lost 1.06 percent during the week. The currency pair is trading at 1.3315 after Bank of England (BoE) Governor Mark Carney issued a warning on the dangers of Brexit. The more disruptive the breakup, the more exceptional the measures from the central bank will have to be in order to shield the economy from the negative effects.

The pound is down 1.06 percent versus the dollar this week and 0.27 versus the euro as talks between London and Brussels ended in friction on Thursday. Governor Carney said that if there is a smooth transition the central bank could take a more traditional path, but if there is a disorderly exit the BoE would have to act with a potential rate cut in the cards similar to the post Brexit referendum outcome in 2016.

Yen Stumbles on Friday but Still Gaining on Uncertainty

The USD/JPY lost 1.17 percent during the past five trading sessions. The currency pair is trading at 109.45 with the Yen one of the biggest beneficiaries of risk aversion. US President Donald Trump put the peace summit on standby on Thursday after accusing North Korea of anger and hostility. The meeting would have marked the first time a sitting president of the US met with his North Korean counterpart.

The market reacted with investors selling riskier assets and looking for safe havens. Stocks fell while metals gained. Gold broke above $1,300. In the currency market the Japanese yen rose 1.14 percent versus the US dollar.

Market events to watch this week:

Tuesday, May 29

- 10:00am USD CB Consumer Confidence

- 5:00pm NZD RBNZ Financial Stability Report

- 8:00pm JPY BOJ Gov Kuroda Speaks

Wednesday, May 30

- 8:15am USD ADP Non-Farm Employment Change

- 8:30am USD Prelim GDP q/q

- 10:00am CAD BOC Rate Statement

- 10:45am CHF SNB Chairman Jordan Speaks

- 9:00pm NZD ANZ Business Confidence

- 9:30pm AUD Private Capital Expenditure q/q

Thursday, May 31

- All Day G7 Meetings

- 8:30am CAD GDP m/m

- 11:00am USD Crude Oil Inventories

Friday, June 1

- 4:30am GBP Manufacturing PMI

- All Day G7 Meetings

- 8:30am USD Average Hourly Earnings m/m

- 8:30am USD Non-Farm Employment Change

- 8:30am USD Unemployment Rate

- 10:00am USD ISM Manufacturing PMI

*All times EDT