Sample Category Title

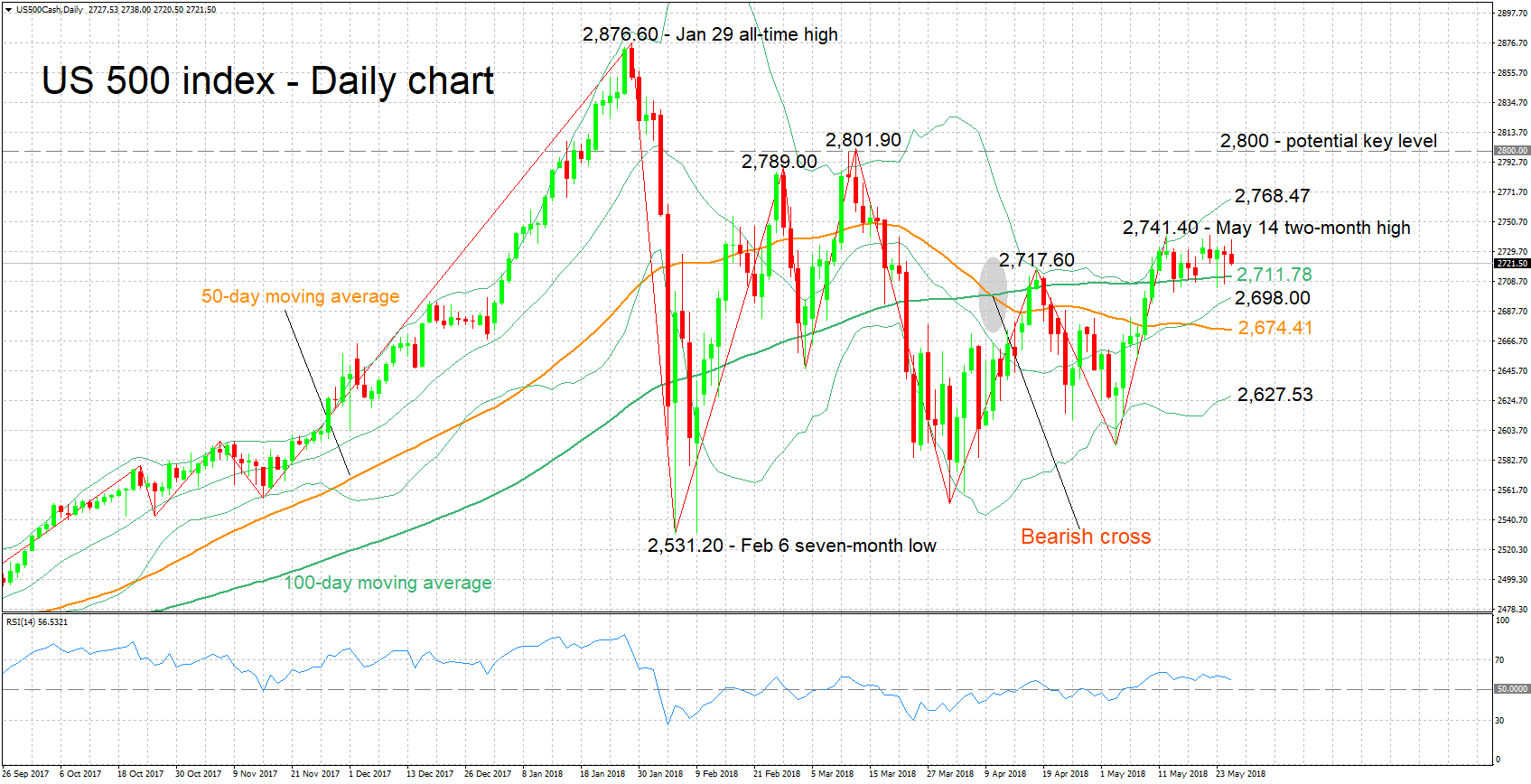

US 500 Index Neutral in the Short-Term, Cautiously Bullish in the Medium-Term

The US 500 index is trading not far below May 14’s two-month high of 2,741.40. Throughout the last couple of weeks the index has been largely moving sideways.

The RSI, which has also been moving sideways to a large extent recently, is painting a mostly neutral picture in the short-term.

Immediate resistance to advances may be coming around May 14’s two-month high of 2,741.40. The upper Bollinger band lies not far above at 2,768.47, while a move off and to the upside of this level would turn the attention to the region around the 2,800 figure, which encapsulates a couple of peaks from previous months (at 2,789.00 and 2,801.90) and may hold psychological importance.

On the downside, support could be met at the region around the current level of the 100-day moving average at 2,711.78, which includes a recent top (2,717.60), as well as the 2,700 handle and the middle Bollinger line (2,698.00) – the latter is a 20-day MA line. The 50-day MA is not far below at 2,674.41, while in case of steeper losses the focus would start to increasingly shift to the lower Bollinger band at 2,627.53.

In terms of the medium-term picture, price action seems to challenge the negative signal given by the bearish cross recorded in early April when the 50-day MA moved below the 100-day one. Specifically, trading activity taking place above both the 50- and 100-day MA lines – but not far above the latter – is giving a cautiously bullish medium-term picture. A drop below the 100-day MA (2,711.78) would tilt the outlook more towards neutrality.

Overall, the short-term bias is looking neutral and the medium-term outlook is moderately bullish at the moment.

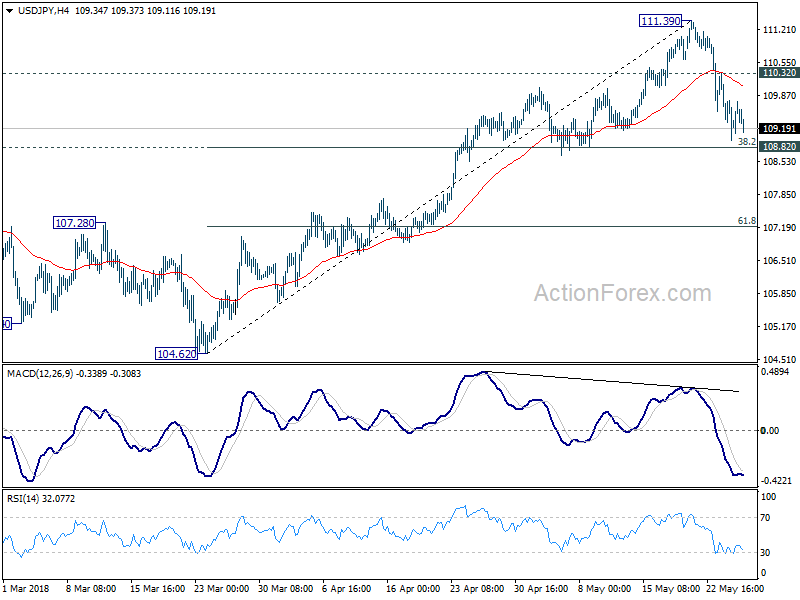

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.76; (P) 109.44; (R1) 109.92; More...

The correction from 111.39 could still extend lower. But we'd expect downside to be contained by 108.82 cluster support (38.2% retracement of 104.62 to 111.39 at 108.80) to bring rebound. On the upside, above 110.32 minor resistance will argue that the pull back is completed. And, in that case, retest of 111.39 high should be seen. However, firm break of 108.82 will dampen our view and bring deeper decline to 61.8% retracement at 107.20 and possibly below.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as108.82 support holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above. However, decisive break of 108.82 will dampen the bullish outlook and revive the case of a break of 104.62 low before bottoming.

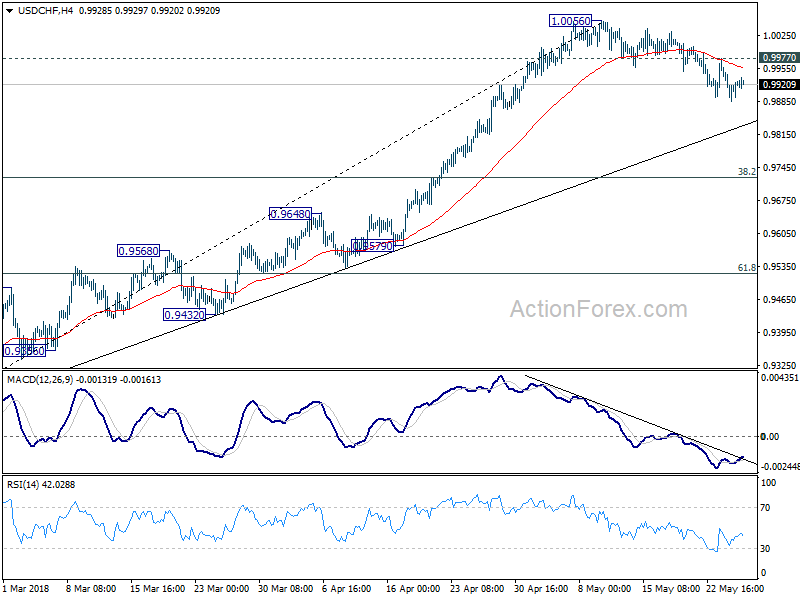

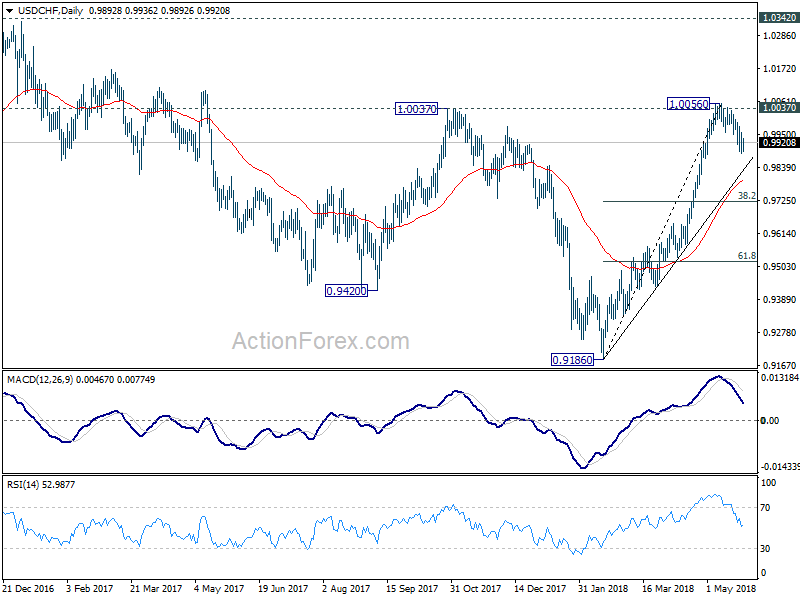

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9877; (P) 0.9921; (R1) 0.9956; More...

No change in USD/CHF's outlook. While downside momentum is diminishing as seen in 4 hour MACD, with 0.9977 minor resistance intact, correction from 1.0056 could extend lower. But we'd expect strong support from trend line (now at 0.9830) to contain downside and bring rebound. On the upside, above 0.9977 will suggest that the pull back is finished and bring retest of 1.0056 high.

In the bigger picture, medium term decline from 1.0342 has completed with three waves down to 0.9186. Rise from there is currently viewed as a leg inside the long term range pattern. Hence, while further rally would be seen, we'd be cautious on strong resistance from 1.0342 to limit upside. For now, further rise is expected as long as 38.2% retracement of 0.9186 to 1.0056 at 0.9724 holds.

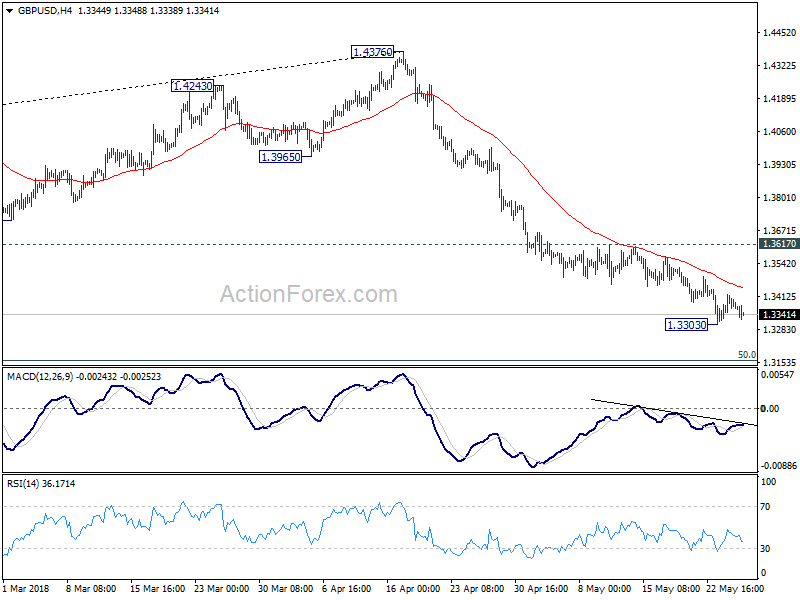

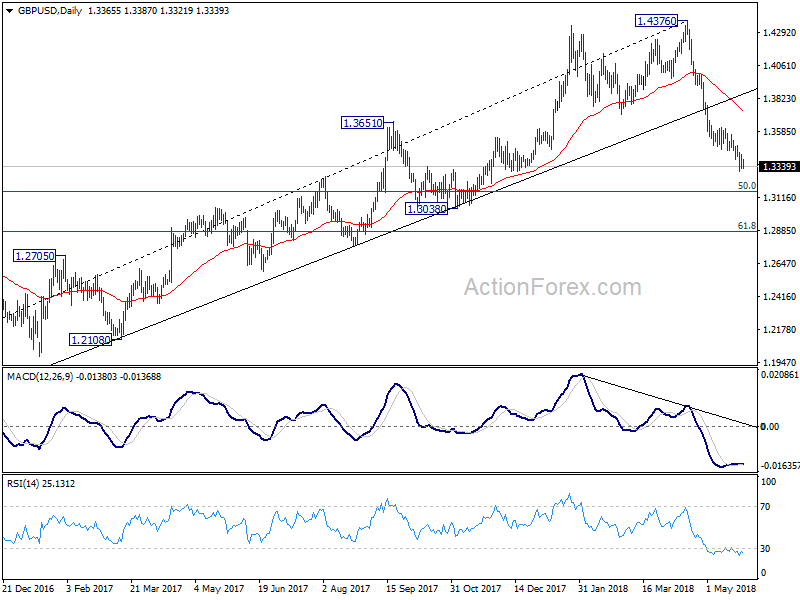

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3333; (P) 1.3377; (R1) 1.3426; More...

GBP/USD is staying in consolidation above 1.3303 temporary low and intraday bias remains neutral. Stronger recovery cannot be ruled out. But upside should be limited by 1.3617 resistance to bring fall resumption. On the downside, below 1.3303 will extend the decline fro 1.4376 to 50% retracement of 1.1946 to 1.4376 at 1.3161. Break will target 61.8% retracement at 1.2874. Nonetheless, firm break of 1.3617 will confirm short term bottoming and bring stronger rebound.

In the bigger picture, current development suggests that whole medium term rebound from 1.1936 (2016 low) has completed at 1.4376 already, with trend line broken, on bearish divergence condition in daily MACD, after rejection from 55 month EMA (now at 1.4249). 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 should now be firmly taken out. Next target will be 61.8% retracement at 1.2874 and below. Outlook will stay bearish as long as 55 day EMA (now at 1.3761) holds, even in case of strong rebound.

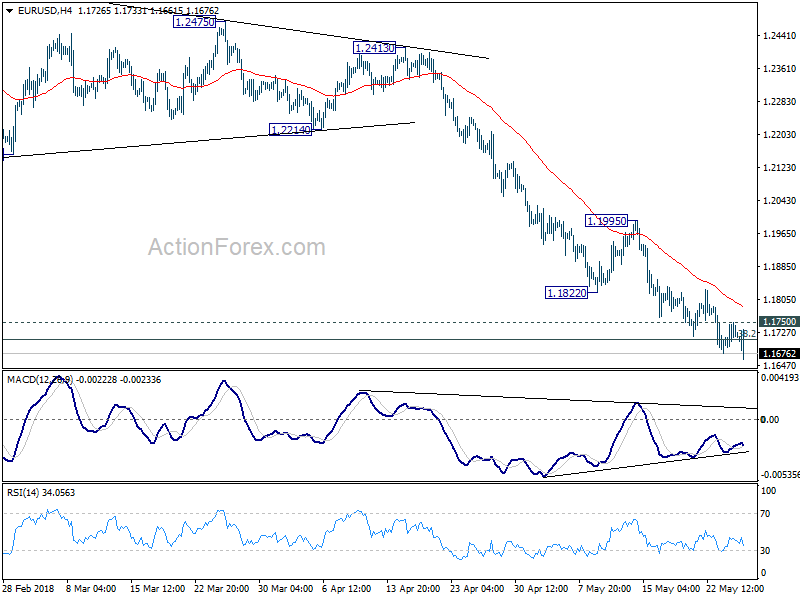

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1691; (P) 1.1720 (R1) 1.1750; More.....

EUR/USD's decline is still in progress and reaches as low as 1.1661 so far. Intraday bias remains on the downside and the fall from 1.2555 should extend to 50% retracement of 1.0339 to 1.2555 at 1.1447 next. On the upside, above 1.1750 minor resistance will turn intraday bias neutral first. Further break of 1.1822 support turned resistance will indicate short term bottoming and bring lengthier consolidation.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will pave the way to 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2049) holds.

Italy Concerns Hammer German Yield and Euro, Canadian Dollar Falls With Oil Price

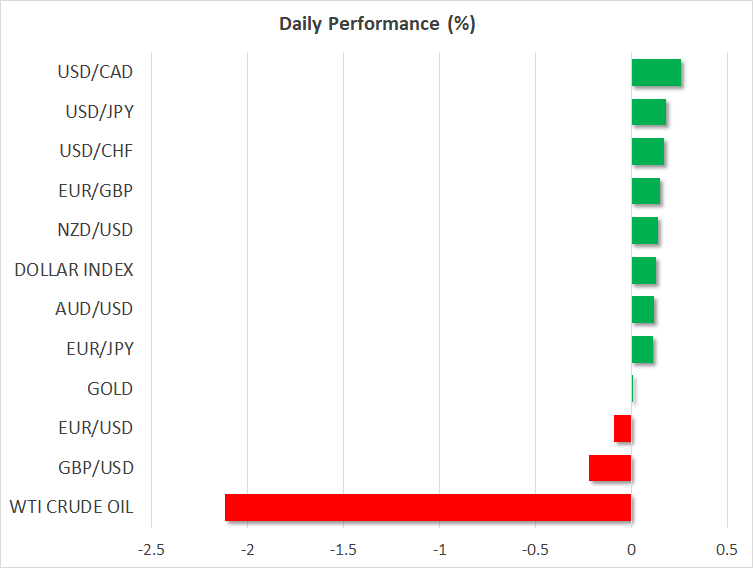

Canadian Dollar, Euro, to a lesser extend Sterling, are the clear losers today. The Loonie is dragged down by oil price as WTI drops through 70 handle. It reaches as low as 68.96 so far on news that OPEC and Russia are considering to raise production. On the other hand, concerns over Italy's new Eurosceptic government sent Italy-Germany yield spread to above 200pts for the first time. German 10 year bund yield dives to as low as 0.422, down more than -0.050 today.

For the week, Yen is emerging as the strongest on as helped by risk aversion, and more so by falling major global treasury yields. It should be noted that US 10 year yield dropped below 3% handle earlier this week and there is no strength for a rebound yet. Aussie is being very resilient, with lack of any news, and would likely end as the second strongest one. Sterling and Euro are the weakest while Dollar is just mixed.

Technically, near term declines in EUR/USD, EUR/JPY, EUR/AUD are extending in early US session. Focuses will be on whether GBP/USD will take out 1.3303 temporary low, and whether GBP/JPY will break 145.67 temporary low. Also, with current upside momentum, USD/CAD could finally take out 1.2996 near term resistance to confirm bullishness.

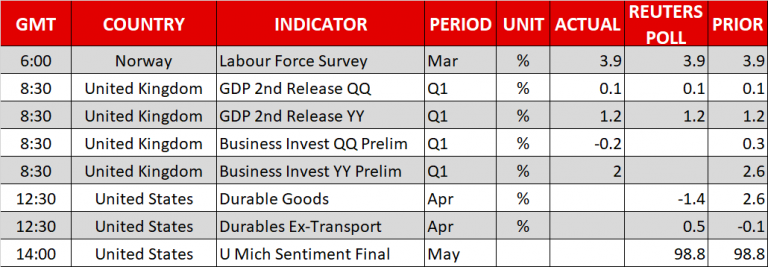

Released from US, durable goods orders dropped -1.7% in April, below expectation of -1.4%. Ex-transport orders rose 0.9%, above expectation of 0.5%.

WTI oil price drops below 70 as OPEC and Russia consider lifting production

WTI crude oil drops below 70 handle on reports that Saudi Arabia and Russia are going to push for lifting production later in the year. The total of boost in production from OPEC and non-OPEC countries could add up to as high as 1 million barrels a day.

Saudi Arabia a Energy Minister Khalid al-Falih is quoted saying in St. Petersburg that the easing of restriction on production would be gradual, so as to avoid shocking the markets. He also added that "all options are on the table" regarding output cuts.

Meanwhile USD 80 a barrel seems to be a psychological level that the oil producing countries want to avoid. The decision could be made as soon as during the next OPEC meeting on June 22 in Vienna.

No revision in UK Q1 GDP

UK Q1 GDP was left unrevised at 0.1% qoq meeting market consensus, but probably not BoE Governor Mark Carney's expectation. Index of services rose 0.3% mom in March. BBA mortgage approvals rose to 38.0k in April.

German Ifo stopped declining trend

German Ifo business climate rose to 102.2 in May, up from 102.1 and beat expectation of 102.0. Expectations gauge dropped to 98.5, down fro 98.7, met consensus. Current assessment gauge rose to 106.0, up from 105.7, beat expectation of 105.5.

Ifo President Clemens Fuest noted in the release that "the declining trend in the ifo Business Climate has stopped." And, "the current business survey and other indicators point to economic growth of 0.4 percent in the second quarter."

North Korea's response to Trump's "sudden and unilateral" cancellation of summit with Kim

North Korean Vice Foreign Minister Kim Kye Gwan responded today to the Trump's pull out from the June 12 summit in a statement carried by state media. Kim said that Trump's "sudden and unilateral" announcement to cancel the summit is unexpected. And she added that "we cannot but feel great regret for it". Kim also noted North Korea remained open to dialogue with the US "regardless of ways at any time". Also, "the first meeting would not solve all, but solving even one at a time in a phased way would make the relations get better rather than making them get worse." And, the US should "ponder over it".

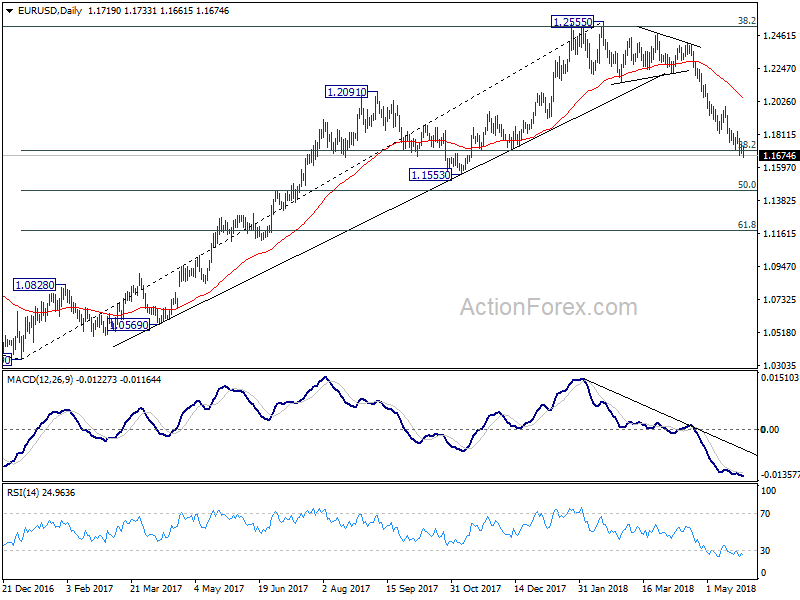

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1691; (P) 1.1720 (R1) 1.1750; More.....

EUR/USD's decline is still in progress and reaches as low as 1.1661 so far. Intraday bias remains on the downside and the fall from 1.2555 should extend to 50% retracement of 1.0339 to 1.2555 at 1.1447 next. On the upside, above 1.1750 minor resistance will turn intraday bias neutral first. Further break of 1.1822 support turned resistance will indicate short term bottoming and bring lengthier consolidation.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will pave the way to 61.8% retracement at 1.1186. For now, even in case of rebound, we won't consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2049) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 0.50% | 0.60% | 0.60% | |

| 08:00 | EUR | German IFO Business Climate May | 102.2 | 102 | 102.1 | |

| 08:00 | EUR | German IFO Expectations May | 98.5 | 98.5 | 98.7 | |

| 08:00 | EUR | German IFO Current Assessment May | 106 | 105.5 | 105.7 | |

| 08:30 | GBP | BBA Loans for House Purchase Apr | 38.0K | 37.5K | 37.6K | |

| 08:30 | GBP | Index of Services 3M/3M Mar | 0.30% | 0.30% | 0.40% | 0.50% |

| 08:30 | GBP | GDP Q/Q Q1 P | 0.10% | 0.10% | 0.10% | |

| 12:30 | USD | Durable Goods Orders Apr P | -1.70% | -1.40% | 2.60% | |

| 12:30 | USD | Durables Ex Transportation Apr P | 0.90% | 0.50% | 0.10% | |

| 14:00 | USD | U. of Mich. Sentiment May F | 98.8 | 98.8 |

Gold Pushes Past $1300 After Trump Cancels Summit

Gold has steadied in the Friday session, after posting strong gains on Thursday. Currently, the spot price for one ounce of gold is $1306.01, up 0.09% on the day. On the release front, it’s a busy day. The focus is on durable goods reports, with expectations of mixed results. Core durable goods orders is expected to climb to 0.5%, but the markets are braced for a decline of 1.3% from durable good orders. If the indicator posts a sharp drop, gold prices could respond with gains. The US will also release UoM Consumer Sentiment, is expected to remain unchanged at 98.8 points.

Gold prices slipped 0.09% on Thursday, following reports that the summit between President Trump and North Korean leader Kim Jong-un had been canceled. Trump sent a letter to Kim, saying that he could not go ahead with the meeting, scheduled for June 12 in Singapore, after particularly harsh comments by the North Korean leader. For his part, Pyongyang was restrained in its response, saying that it still looked forward to resolving outstanding issues with the US. Rising tensions between the US and North Korea have rattled investors in recent months, boosting gold, which is a traditional safe-haven in times of crisis. If tensions worsen between the US and North Korea, investor risk appetite could wane and gold could be the big winner.

The Federal Reserve released the minutes from its May meeting. In the minutes, some Fed policymakers said they favored removing the phrase that “the stance of monetary policy remains accommodative”. Not surprisingly, the minutes didn’t shed light on the Fed’s plans, saying that another rate hike would occur “soon”, on the assumption that the US economy continues to perform as expected. Still, a quarter-point rate hike in August is virtually a given, with the CME Group setting the odds of a hike at 95 percent. This would mark a second hike in 2018. After that? The Fed projection remains at three rates hikes in 2018, but some analysts are predicting four increases this year.

Into US session: CAD the weakest on oil, EUR and GBP follow as yields dive

Entering into US session, CAD, EUR and GBP are trading as the strongest ones, while USD, AUD and JPY are the strongest. Some note that USD is the strongest one. Yes, admitted it is. But considering the USD/JPY is lacking follow through buying through 109.50, and AUD/USD is also held in tight range, it should be more about the weaknest of CAD, EUR and GBP, rather than strength of USD.

CAD is clearly weighed down by falling oil price as WTI drops below 70 handle on talk that OPEC and Russia are going to raise production. USD/CAD would soon be retesting 1.2996 resstance.

Meanwihle, we believe that the free falls in German and UK yields are the reasons dragging EUR and GBP down. Data from both countries together are not bad and won't add to more dovish ECB or BoE expectation.

Instead, we've noticed that Italian 10 year yield has another day of strong rally today to 2.481, up 0.081 at the time of writing. German 10 year bund yield is down -0.048 at 0.426. The Italy-German yield spread surpassed 200 pts level for the first time since last June. The decline in German bund yield is particularly serious if we consider that it it as high as 0.583 earlier this week. Concerns over the new Italian government is the driving force in the markets.

UK 10 year gilt yields also dropped -0.50 to 1.351 so far.

Oil Loses Ground as Russia and Saudi Arabia Discuss Supply Increases

Here are the latest developments in global markets:

FOREX: The US dollar rose 0.18% versus the yen after three straight days of declines. Meanwhile, the US dollar index jumped by 0.13% to 93.87. Euro/dollar fell by 0.09% and is set to complete the sixth week of declines in a row as concerns over Italy’s debt outlook weighed on sentiment. Pound/dollar moved lower by 0.21% to 1.3347 on Friday as investors eyed UK GDP data for signs of whether the BOE will raise interest rates. The British economy expanded 0.1% q/q in the first three months of 2018 according to updated estimates, in line with the flash estimates and well below the 0.4% in the previous quarter. The antipodean currencies are heading higher with aussie/dollar rising by 0.17% to 0.7587 and kiwi/dollar climbing by 0.17% to 0.6932. Dollar/loonie advanced by 0.24% and is slightly above the 1.2900 handle.

STOCKS: European stocks traded significantly higher during Friday’s session but were on track to finish the week weaker on the back of trade risks and heightened political uncertainty in the Eurozone. The pan-European Stoxx 600 was up 0.37% at 1030 GMT, with almost all sectors in positive territory. The blue-chip Euro STOXX 50 was higher, being up by 0.23% at 1030 GMT. The German DAX 30 surged by 1.00%, while the Italian FTSE MIB 100 declined by 0.28%. The French CAC 40 gained 0.53% and the British FTSE 100 was also in positive territory, jumping by 0.18%. Moreover, the Spanish IBEX 35 moved down by 0.72% as the Spanish Prime Minister could face a no-confidence vote in the coming days (see below). Futures tracking US stock indices were flashing red, pointing to a negative open.

COMMODITIES: Oil prices fell aggressively on Friday as Russia and Saudi Arabia are considering to increase OPEC/non-OPEC supply by 1 million barrels per day on worries the recent rally in oil prices has been overstretched. West Texas Intermediate (WTI) and Brent crude oil plummeted by 1.80% and 1.98%, to $69.44 and $77.25 respectively. Gold struggled below the 200-day simple moving average on Friday after the sharp buying interest yesterday when the US President Donald Trump decided to cancel the meeting with North Korean leader Kim Jong Un. The precious metal moved marginally higher today by 0.08%, at $1,304.90 per ounce.

Day ahead: US durable goods orders pending; eyes on Fed speakers

A few economic releases are scheduled for the remainder of the day, with the spotlight turning to several speeches by a handful of policymakers. Political developments and updates on the trade front are also expected to attract attention in the following days.

At 1230 GMT, the US will report on new orders for durable goods for the month of April and analysts expect the measure to decline by 1.4% m/m compared to a growth of 2.6% in the previous month. Excluding transportation, though, forecasts are for an expansion of 0.5% m/m compared to a contraction of 0.1% (revised downwards from +0.1%) in March. Later at 1400 GTM, the University of Michigan will publish its final findings on US consumer confidence for May, with the number expected to come at 98.8 as it was initially released.

Besides the data, investors will keep a close eye on any geopolitical headlines. The US President, Donald Trump, decided on Thursday to cancel a planned summit with North Korea’s Kim Jong Un scheduled for June 12, due to North Korea’s recent “tremendous anger and hostility”. North Korea perhaps surprisingly responded with a measured tone, expressing instead its willingness to meet with US officials at any time. This helped turn stock markets back to the upside after a strong sell-off in the wake of the news and tempered demand for safe havens.

Trade developments will be of interest as well since fears over a global trade war have not faded yet. Although the US and China agreed to put trade frictions on hold, Trump expressed his dissatisfaction a few days after, stressing that talks with China need a “different structure”. At the same time, his request to start an investigation into automobiles imports, which would significantly affect EU companies, raised speculation that further tariff threats by the US could come in play.

Meanwhile, uncertainties around Italy’s potential fiscal reforms under the new coalition government could continue to weigh on the euro, while political conditions in Spain are likely to attract attention after sources stated that the Socialists, the biggest opposition party, were planning for a no-confidence vote against the Spanish Prime Minister, Mariano Rajoy. The announcement came after the Spanish Court delivered fines and prison sentences to Rajoy’s conservative party members over illegal practices.

In oil markets, the Baker Hughes report on the number of US oil rigs due out at 1700 GMT has the potential to move oil prices.

As for today’s public appearances, Fed Chair, Jerome Powell, will be participating in the panel discussion on “Financial Stability and Central Bank Transparency” before the Sveriges Riksbank Conference in Sweden at 1320 GMT. Elsewhere, regional Fed presidents, Raphael Bostic, Charles Evans and Robert Kaplan will be making comments before the Federal Reserve Banks of Dallas and Atlanta “Technology-Enabled Disruption: Implications for Business, Labor Markets and Monetary Policy” conference at 1545 GMT. Kaplan will be also giving closing remarks at the conference at 1830 GMT.

On Saturday, the Russian President, Vladimir Putin, will be holding a meeting with the Japanese Prime Minister, Shinzo Abe.

WTI oil price drops below 70 as OPEC and Russia consider lifting production

WTI crude oil drops below 70 handle on reports that Saudi Arabia and Russia are going to push for lifting production later in the year. The total of boost in production from OPEC and non-OPEC countries could add up to as high as 1 million barrels a day.

Saudi Arabia a Energy Minister Khalid al-Falih is quoted saying in St. Petersburg that the easing of restriction on production would be gradual, so as to avoid shocking the markets. He also added that "all options are on the table" regarding output cuts.

Meanwhile USD 80 a barrel seems to be a psychological level that the oil producing countries want to avoid.

The decision could be made as soon as during the next OPEC meeting on June 22 in Vienna.