Sample Category Title

Sentiment Mixed As North Korea Offers Olive Branch

It's remarkable that just hours after President Donald Trump suddenly axed his highly anticipated June summit with Kim Jong-Un in Singapore, North Korea unexpectedly offered an olive branch.

North Korea has stated that they remain open-minded in giving “time and opportunity” to the United States and are willing to meet Trump “at any time in any way”. With the nation also calling the planned summit “desperately necessary” to mend the US-North Korea relationship, the doors could still be open for a summit to take place. Markets will be paying very close attention to how the Trump administration responds to North Korea's conciliatory stance. Any further signs of de-escalating tensions between the US and North Korea could revive risk sentiment.

Asian stocks were on the defensive during early trade, as North Korea's measured response to the abrupt summit cancellation slightly soothed investor jitters. European markets rebounded after the olive branch from North Korea and this improving sentiment could support Wall Street in the afternoon.

Sterling quivers as GDP disappoints

This hasalready been a terrible trading week for the Pound, as cooling inflation figures dented expectations over the Bank of England raising UK interest rates in August.

Matters worsened on Friday following reports that UK economic growth dropped to its lowest rate since 2012. UK GDP growth slowed to 0.1% in the first quarter of 2018 according to the second estimate, which immediately damaged buying sentiment towards the Pound. Today's disappointing growth figures may weigh heavily on sentiment while also forcing investors to scale back bets on a BoE rate hike anytime soon.

Taking a look at the technical picture, the GBPUSD remains bearish on the daily charts as there have been consistently lower lows and lower highs. Repeated weakness below the 1.3400 level could invite a decline towards 1.3320 and 1.3250, respectively.

Dollar steady ahead of Powell speech

King Dollar was steady against a basket of major currencies this morning ahead of the upcoming speech from Fed Chair Jerome Powell.

He will be addressing financial stability and central bank transparency before the Sveriges Riksbank Conference in Stockholm later today. The Greenback could appreciate further is Powell sounds hawkish and offers fresh insight into the Fed's monetary policy tightening path beyond June. With the widening interest rate differential still favouring the Dollar and expectations elevated over an interest rate hike in June, Dollar strength is likely to remain a dominant market theme.

Taking a look at the technical picture, the Dollar Index remains heavily bullish on the daily charts. A decisive breakout above 94.00 could encourage an incline higher towards 94.20 and 94.50, respectively.

Is the Oil bull run over?

The prospect of OPEC and Russia easing supply curbs to counterbalance falling output from Venezuela and potential decline in Iranian exports has exposed oil to downside risks.

Price action suggests that bulls may be struggling to find support from geopolitical risk factors to sustain the current rally. While initially speculation of tighter global supply was a theme that heavily supported oil, the fundamental drivers could change if OPEC and co. easesupply curbs. With the possibility of rising production from Russia, OPEC and US Shale renewing oversupply concerns, Oil remains exposed to downside risks.

In regard to the technical perspective, WTI Crude is at risk of sinking towards $68 if bulls are unable to maintain control above $70.

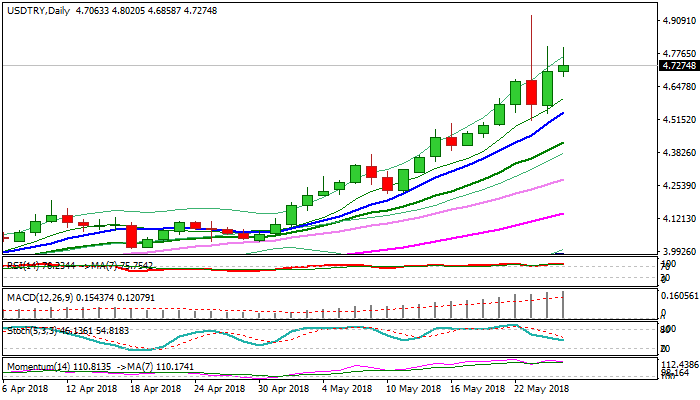

USDTRY Outlook: Rate Hike Provided Temporary Relief But Short-Term Future Could Be Turbulent

The USDTRY bounced from post-CBRT low at 4.5119 but upside attempts were repeatedly capped at 4.80 zone signaling that the rate hike two days ago managed to reduce the pace of lira's fall which approached psychological 5.00 barrier, hours before the central bank's action on Wednesday. Rate hike helped to temporarily stop lira's fall, with recent weakness of oil prices and threats of further easing, expected to support troubled Turkish currency, but another hike on CBRT's regular meeting on 07 June, is needed to generate stronger bullish signal for lira. On the other side, markets remain strongly concerned over coming elections in Turkey (24 June) and President Erdogan's plans to take more control of the economy, which would further weaken central bank's position and signal turbulent period ahead. Such scenario, accompanied with further rise of oil prices would have negative impact and send lira back into uncharted territory. Meanwhile, the pair may hold in extended consolidation which should remain capped at 4.80/90 zone and supported by rising 10SMA (currently at 4.5420). Only break below 10SMA would sideline upside threats and risk dip towards pivotal support at 4.4644 (Fibo 38.2% of 2018 rally from 3.7153 to 4.9273).

Res: 4.8040, 4.9000, 4.9273, 5.0000

Sup: 4.6858, 4.6413, 4.6374, 4.6000

German IFO Shows Stabilization, UK GDP Q1 Confirmed At 5-Year Low

Notes/Observations

- Italian political concerns linger

- German May Business Climate beats expectations

- UK Q1 GDP 2nd reading in line with expectations at confirms annual pace at a 5-year low

Asia:

- North Korea Vice Foreign Min Kim Kye Gwan: Willing to talk with US at 'any time'; no change in will to do the best for peace (Reminder: On Thursday, US President Trump sent a letter to North Korea's leader Kim, cancelling the June 12 summit)

Europe:

- Eurogroup chair Centeno: encouraged Greece to continue reform efforts; there had been some convergence in debt discussions

- BOE Gov Carney: the gentle path for rate hikes expected by BOE is dependent on GDP growing faster than the 1.5% trend rate

- UK officials said to have warned the EU that its approach to Brexit negotiations risks damaging its security and economic relationship

- EU official said to have dismissed many of the UK’s plans for their post Brexit relationship as little short of fantasy. Little progress has been made on the most important issue of a hard Irish border

- Spain PSOE Leader Sanchez (opposition) reportedly considering triggering no confidence vote against Spain PM Rajoy following corruption verdict

- Italy PM designate Conte: talks with the political parties on forming a govt have been fruitful

Americas:

- Fed's Harker (non voter, moderate): getting close to neutral rate; if inflation were to accelerate would be open to 4th rate hike this year. Still sticking to baseline forecast of 3 hikes this year; possible that 2019 could see the end of the rate tightening cycle

- Mexico reportedly makes US an offer in bid to reach NAFTA agreement. Could be more flexible on automotive wages and content in exchange for US withdrawing most disruptive proposals

Energy:

- Russia Energy Min Novak: OPEC+ to discuss easing caps at the Jun meeting. Russia to maintain 100% compliance to agree upon cuts in both May and Jun period

Economic Data:

- (NO) Norway Mar AKU Unemployment Rate: 3.9% v 3.9%e

- (AT) Austria Mar Industrial Production M/M: -1.6% v +0.3% prior; Y/Y: 3.9% v 5.1% prior

- (ES) Spain Apr PPI M/M: +0.7% v -1.0% prior; Y/Y: 1.9% v 1.3% prior

- (CN) Weekly Shanghai copper inventories (SHFE): 268.4K v 268.5K tons prior

- (DE) Germany May IFO Business Climate: 102.2 v 102.0e, Current Assessment: 106.0 v 105.5e, Expectations Survey: 98.5 v 98.5e

- (PL) Poland Apr Unemployment Rate: 6.3% v 6.3%e, Q1 Unemployment Rate: 4.2% v 4.4%e

- (RU) Russia Narrow Money Supply w/e May 18th: 10.05T v 9.96T prior

- (TW) Taiwan Q1 Final GDP Y/Y: 3.0% v 3.0%e

- (UK) Q1 Preliminary GDP (2nd reading) Q/Q: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e

- (UK) Q1 Preliminary Private Consumption Q/Q: 0.2% v 0.1%e; Government Spending Q/Q: 0.5% v 0.3%e; Gross Fixed-Capital Formation Q/Q: +0.9% v -0.2%e; Exports Q/Q: -0.5% v +0.4%e; Imports Q/Q: -0.6% v +0.1%e

- (UK) Q1 Preliminary Total Business Investment Q/Q: -0.2% v +0.3% prior; Y/Y: 2.0% v 2.6% prior

- (UK) Mar Index of Services M/M: 0.1% v 0.1%e; 3M/3M: 0.3% v 0.3%e

- (UK) Apr BBA Loans for House Purchases: 38.1K v 37.4Ke

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 +0.6% at 3,544, FTSE +0.3% at 7,741, DAX +0.9% at 12,976, CAC-40 +0.6% at 5,581; IBEX-35 +0.4% at 10,034, FTSE MIB +0.1% at 22,756, SMI +0.6% at 8,821 , S&P 500 Futures +2.0%]

- Market Focal Points/Key Themes: European indices opened broadly higher and continued to move further into positive territory; geopolitical concerns keep risk sentiment low after President Trump cancels planned meeting with North Korea; Italy continues to underperform as designated PM tries to form government; best performing sector travel and leisure; Wesfarmers withdraws from UK market supporting shares in Kingfisher and Travis Perkins; Argentina closed for holiday; upcoming earnings expected in the US session include Foot Locker and Buckle

Equities

- Consumer Discretionary: Compagnie Des Alpes CDA.FR +0.8% (results), GVC Holdings GVC.UK +1.9% (trading update)

- Healthcare: Astrazeneca AZN.UK +0.9% (study results), Celyad CYAD.BE +7.6% (analyst action)

- Materials: Centamin CEY.UK -17.6% (outlook), Eramet ERA.FR -1.2%(outlook, bid rejection)

- Telecom: Orange Belgium OBEL.BE +3.6% (agreement)

Speakers

- German IFO Economists commented that the domestic economy was the main contributor to stabilization in sentiment although it could not see any euphoria in the export sector

- Italy PM designate Conte said to have pledged to help bank victims a priority. Looking after savings of people hurt by bank defaults

- Sweden Nation Debt Office (NDO): stated that it would take position for stronger SEK currency (Krona) against the Euro. To build up position gradually at various exchange rate levels and could increase the position to SEK7.0B

- Spain PSOE party (opposition)confirmed registering a no-confidence vote against PM Rajoy (as expected)

- Turkey Central Bank (CBRT) fixed repayments of rediscount loans for exporters at 4.2 Lira per USD

- Turkey Dep PM Simsek: Central bank will continue to act and its showed that it was independent

- Fitch: Another interest rate hike by Turkey Central Bank was possible at its scheduled Jun meeting. Continued TRY currency (Lira) weakness could weight upon Turkey's sovereign rating

- Russia Fin Min Siluanov stated that the country would not have a sales tax

- Russia Central Bank 1st Dep Gov Yudaeva reiterated view that could either hold or cut interest rates

- Indonesia Central Bank reiterates its view that Q2 GDP growth improving q/q and it was expected to be closer to ~5.2%

- China govt said to encourage private investment in govt carmakers

- OPEC and non-OPEC said to be considering raising output by ~1M bpd; final decision to be taken in June

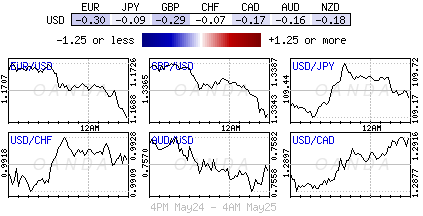

Currencies

- USD was firmer against the major pairs

- EUR/USD was poised for its 6th straight week of losses as concerns over the new Italian govt lingered. The Italian 10-year BTP yield was back above the pivotal 2.40% level

- GBP was hampered by recent negotiation in the Brexit talks and confirmation of its GBP hitting a 5-year low.

- The USD/JPY was higher in the session. The JPY currency fought off risk aversion flows after President Trump cancelled the planned Jun 12th summit in Singapore. North Korea showing an openness to hold the talks helped to soften the yen currency

Fixed Income

- Bund Futures trade 31 ticks higher at 160.45 as German IFO Business Climate beats expectations. Upside targets 160.75 followed by 161.50, while a return lower targets the 158.25 level.

- Gilt futures trade at 122.89 higher by 33 ticks following the unrevised second GDP reading, which kept the annual pace at a 5-year low. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Friday’s liquidity report showed Thursday’s excess liquidity stayed rose from €1.838T to €1.840T. Use of the marginal lending facility decreased from €295M to €197M.

- Corporate issuance saw 1 deal priced for $600M

Looking Ahead

- 05:30 (IN) India to sell combined INR120B in 2022, 2028, 2035 and 2046 bonds

- 05:30 (ZA) South Africa to sell ZAR600M in I/L bonds

- 06:00 (UK) DMO to sell combined £3.0B in 1-month, 6-month and 12-month Bills (£0.5B, £1.0B and £1.5B respectively)

- 06:30 (IS) Iceland to sell Bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil May FGV Construction Costs M/M: 0.4%e v 0.3% prior

- 07:30 (TR) Turkey May Capacity Utilization: No est v 77.3% prior

- 07:30 (TR) Turkey May Real Sector Confidence (Seasonally Adj): No est v 106.8 prior; Real Sector Confidence (unadj): No est v 111.2 prior

- 07:30 (IN) India Weekly Forex Reserves

- 08:00 (IN) India announces upcoming bill issuance (held on Wed)

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 (US) Apr Preliminary Durable Goods Orders: -1.3%e v +2.6% prior; Durables Ex Transportation: 0.5%e v 0.1% prior, Capital Goods Orders (Non-defense/ex-aircraft): +0.7%e v -0.4% prior, Capital Goods Shipments (Non-defense/ex-aircraft): +0.4%e v -0.8% prior

- 09:00 (US) Fed chair Powell at the Riksbank's 350th Anniversary Conference

- 09:00 (MX) Mexico Apr Trade Balance: $0.6Be v $1.9B prior

- 10:00 (US) May Final University of Michigan Confidence: 98.8e v 98.8 prelim

- 10:00 (MX) Mexico Q1 Current Account: -$4.7Be v -$3.2B prior

- 10:00 (US) Revisions: Retail Sales & Wholesale Trade

- 11:00 (EU) Potential Sovereign ratings after European close (South Africa Sovereign Debt to be rated by S&P; Austria Sovereign Debt to be rated by Moody's

- 11:45 (US) Fed members Kaplan (dove, non-voter); Evans (dove, non-voter), Bostic (voter, hawk) at Dallas Fed conference

- 12:30 (PT) EU chief Brexit negotiator Barnierin Lisbon

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 14:30 US) Fed Kaplan (dove, non-voter)

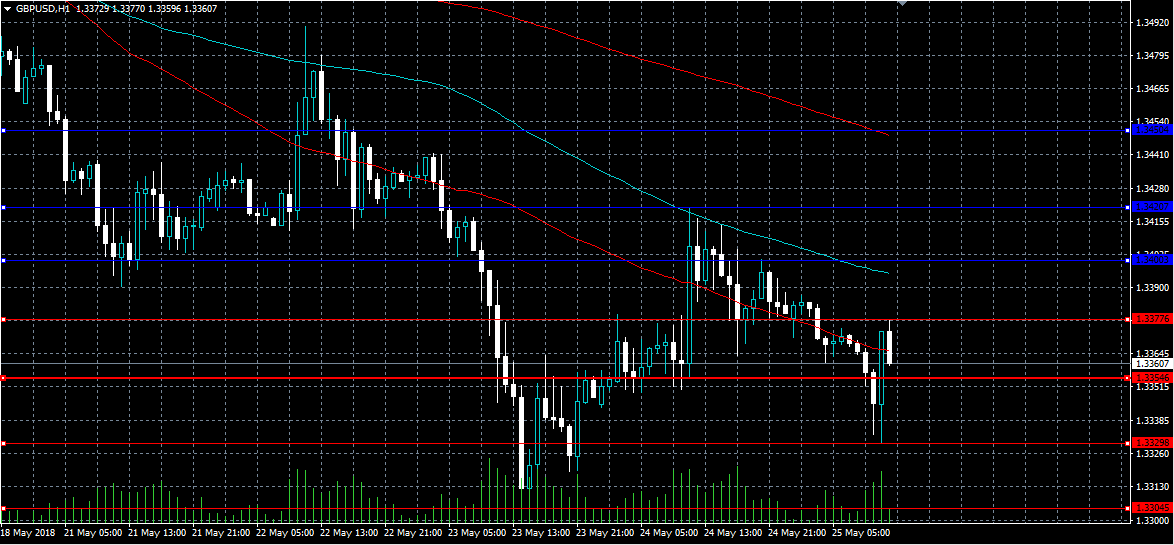

GBPUSD Back Under Pressure

The British pound has come under a fresh round of selling pressure against the US dollar on Friday, after buyers failed to move price back above the 1.3400 level. The GBPUSD pair currently trades around the 1.3360 level, after earlier meeting strong selling interest from the 1.3377 resistance level. Moving into the US trading session, traders look towards the release of US Durable Goods Orders and a scheduled speech from FED Chair Jerome Powell.

The GBPUSD pair is bearish while trading below the 1.3400 level, key intraday technical support is located at the 1.3329 and 1.3304 levels.

If the GBPUSD pair moves above the 1.3377 level, buyers may test towards the 1.3400 and 1.3420 resistance levels.

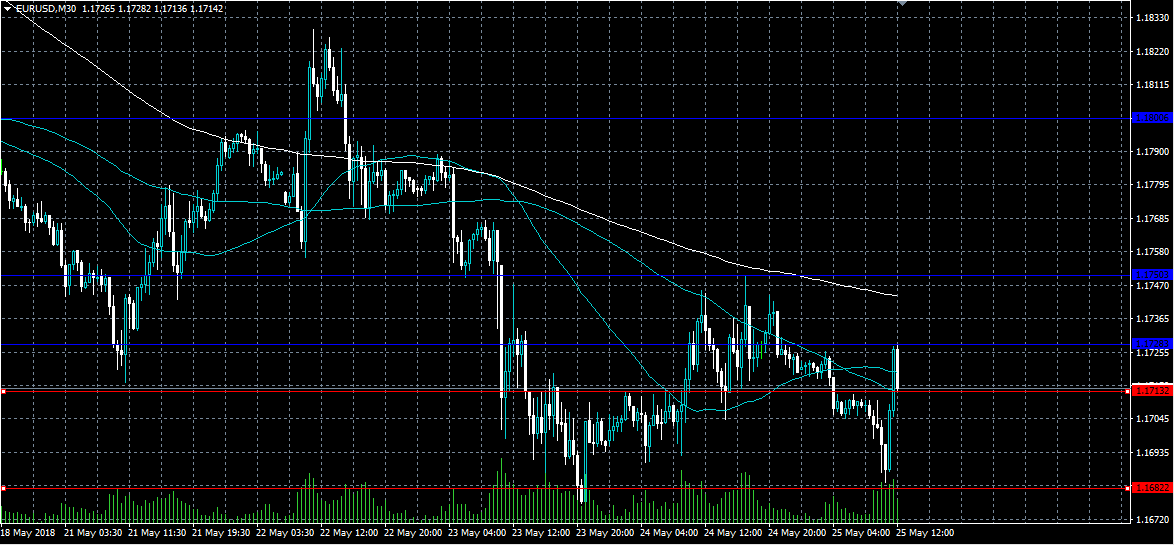

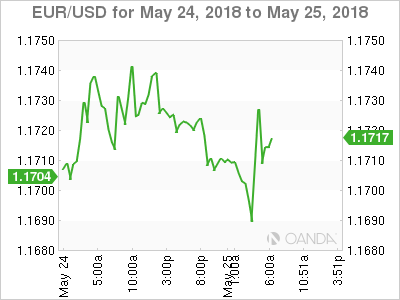

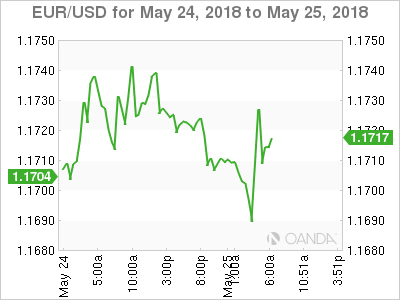

EURO Still Bearish Below 1.1715 Level

The euro currency has suffered another volatile European trading session against the US dollar, as Italian bond yields continue to rise across the board. The EURUSD pair currently trades around the 1.1713 level, after earlier hitting 1.1682, before recovering back above the 1.1700 level. Euro traders continue to look towards the Italian bond market and the US dollar index for direction.

The EURUSD pair remains strongly bearish while trading below the 1.1715 level. Key support is found at the 1.1682 and 1.1640 levels.

If the EURUSD pair trades above the 1.1715 level, near-term technical resistance is located at the 1.1728 and 1.1750 levels.

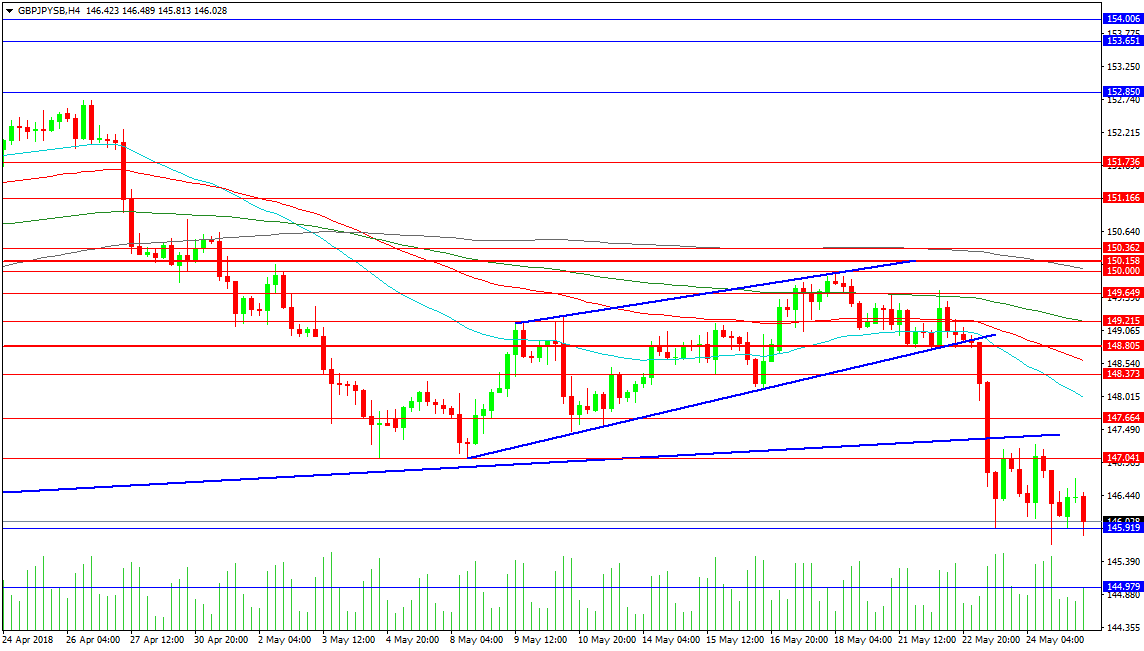

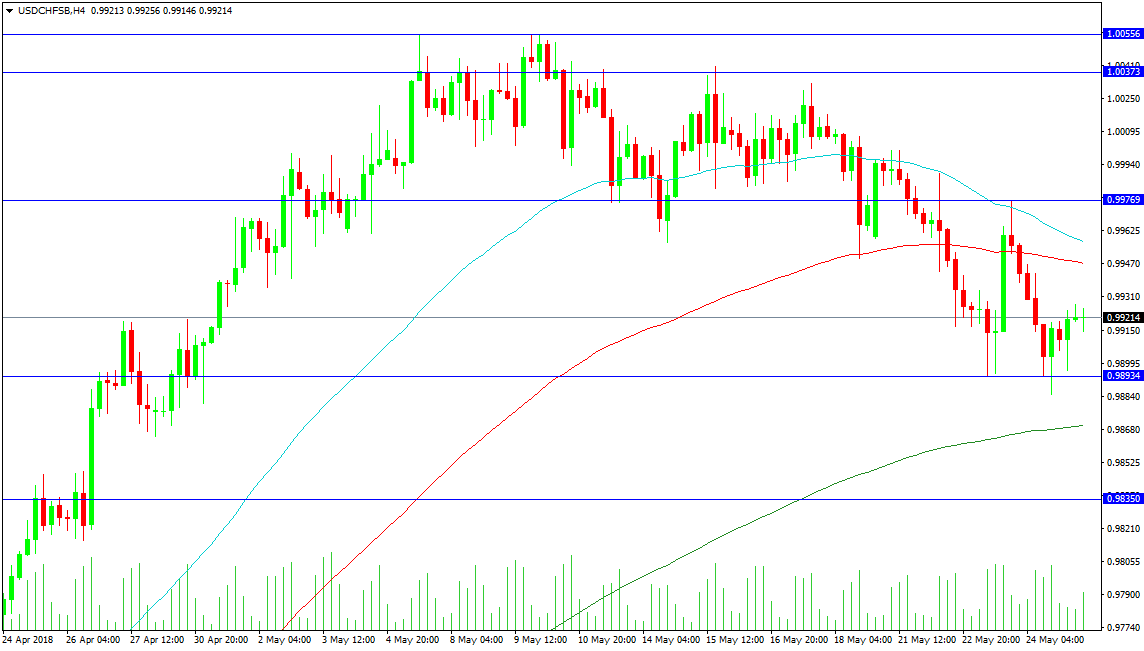

Forex Analysis: GBPJPY And USDCHF

The GBPJPY pair has fallen under support this week, first at the 148.800 area and then the rising support trend line at 147.300. The market spent the last couple of weeks consolidating between 150.000 and 147.000 with these levels now becoming resistive. The low reached yesterday was 145.679 and a break under this level would target 145.000 as support with the previous swing low at 144.979. Continued downward pressure would likely look to supports at 144.440 and 144.000 followed by 143.750 and 143.000.

Resistance at the rising trend line can be found at 147.358 today should the price get above 147.000. A retest on this area could find sellers but a move higher can target the 148.000 level. Resistance levels can also be seen at 149.215 and 149.650. A move above 150.000 would seek to visit 151.000 followed by the 152.000 area and 152.700.

USDCHF

This pair has turned lower from a double top pattern at 1.00556 and having broken under the 1.00000 level is now using the 50 period MA as resistance at 0.99735. This has pushed price under the 100 period MA at 0.99522. The 0.99769 area is also providing resistance and this may block any move back higher for the near term. Failure to push higher above parity may develop into a deeper retracement. However should price action be driven higher there is a chance that a bullish breakout looks to test the recent highs and targets at 1.01000 and 1.01250 become available.

Support comes from the recent low at 0.98934 followed by the rising 200 period MA at 0.98675. A move under this MA would see the consolidation area at 0.98350 used to prop up price. A bounce from the 200 period MA would be comfortable for buyers but a loss could create a run on stops leading to a break under 0.98000 and target lower levels at 0.97091 and 0.96485.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1705

The overall bias remains bearish, for a break through 1.1680, en route to 1.1570 zone. Crucial on the upside is 1.1830 peak and minor intraday resistance lies at 1.1750.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1750 | 1.2000 | 1.1680 | 1.1680 |

| 1.1830 | 1.2160 | 1.1570 | 1.1480 |

USD/JPY

USD/JPY

Current level - 109.41

The sell-off since 111.40 peak is over and a corrective pattern is underway, towards 110.30 zone. Initial intraday support lies at 109.30.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.80 | 111.40 | 109.30 | 108.30 |

| 110.40 | 114.40 | 108.90 | 107.00 |

GBP/USD

Current level - 1.3353

The rebound after 1.3300 test is pretty weak and the downtrend remains intact, so my outlook is bearish, for a renewal of the slide towards 1.3040 zone. Crucial on the upside is 1.3490 peak.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3460 | 1.3990 | 1.3300 | 1.3300 |

| 1.3570 | 1.4100 | 1.3210 | 1.3040 |

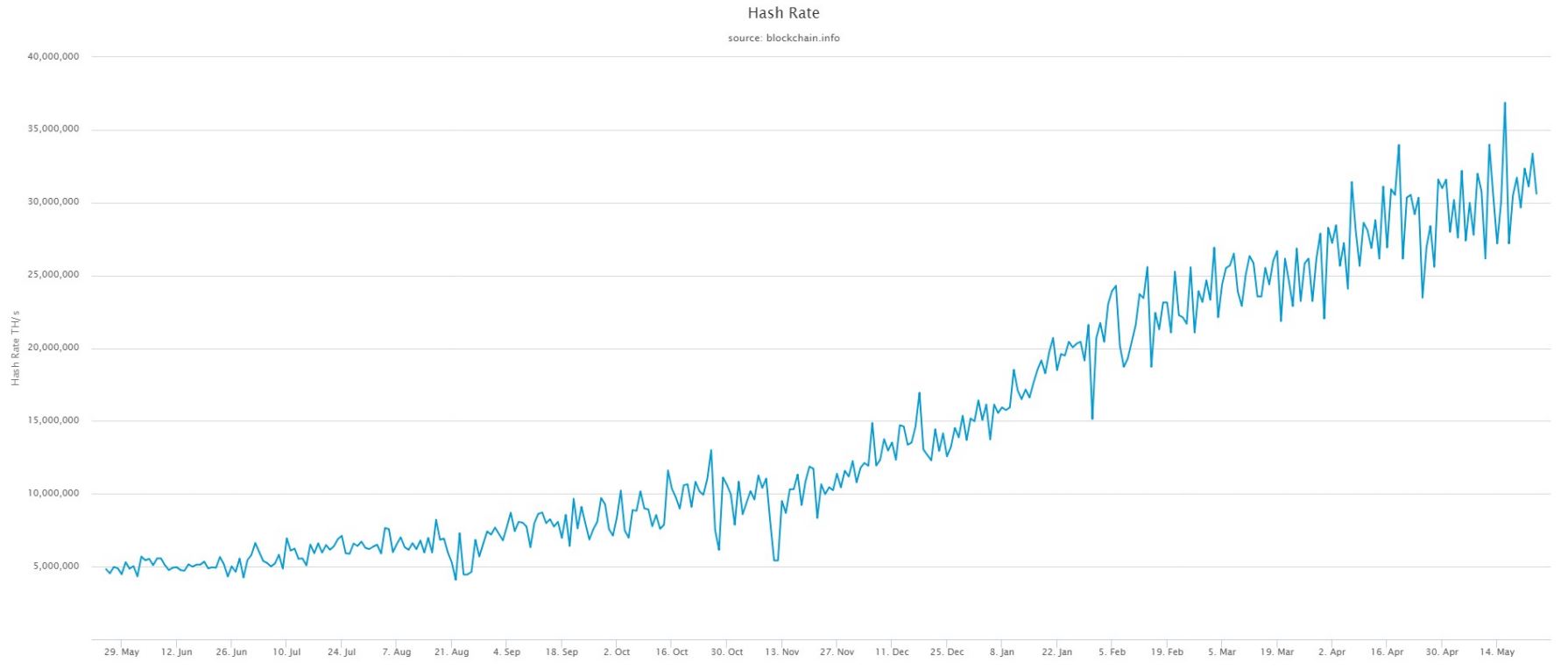

Bitcoin: Hash Rate Telling A Bullish Story

- Hash rate is increasing while prices are still in a continuing decline

- Bitcoin prices are falling at a steady pace, miners are still very much interested

As the cryptocurrency bear market presses on many investors worry that Bitcoin was just another passing fad. Bitcoin recently broke down past $8000 and is struggling to find support around $7800, the same level where Bitcoin broke out in early April in an attempt to break above $10000. The overall market capitalization is also in a steady decline breaking $400bn from its all-time highs of over $830 billion.

The market capitalization has been nearly cut in half resulting in major price declines in Bitcoin and nearly every Altcoin on the market. Aside from the declines in price action and market capitalization, there is one area where we are seeing growth and that is in hash rate. This may lead us to believe that miners know something we don’t.

Looking at the chart on Blockchain.info, we see a very steady increase in hash rate during the months leading up to and after the market sell-off. Looking at a chart of the total cryptocurrency market capitalization and hash rate side by side will show a clear divergence. Why is it that hash rate is increasing while prices are still in a continuing decline?

It is a fact that as more miners join the network, the higher the network hash rate is. This tells us that even though Bitcoin prices are falling at a steady pace, miners are still very much interested in mining Bitcoin.

From the data presented we can draw the conclusion that the overall outlook on Bitcoin is bullish, at least in the eyes of the miners. After all miners would not want to allocate their resources mining a digital asset they believe to be worthless. Miners are in the business to make money and perhaps the downturn in this market will allow them to accumulate more bitcoin at lower prices in preparation for the next Bull Run.

Many traders focus only on the technical outlook and can overlook solid fundamentals and clues such as an increasing hash rate. If the hash rate were to be falling in congruence with price, then there would be cause for concern. That would tell us that miners are less interested in mining Bitcoin and could be turning their focus to mining other cryptocurrencies or not mining at all. It seems to me that miners are taking a longer-term view on Bitcoin and cryptocurrencies, ignoring short-term downtrends in the market. This fact alone should give investors confidence that there is still a lot of interest in Bitcoin and in mining specifically. Network support is very strong and should continue to grow.

Miners are arguably the most important asset to the Bitcoin ecosystem because they work to create new blocks as well as verify all transactions to ensure the network is secure. A strong group of miners who are willing to support the network creates the image that Bitcoin is very strong and well positioned going forward. As we move closer to the end of Q2 and into Q3 fundamentals will continue to improve and my bet is that price action will surely catch up to the strong fundamentals. Without a strong group of miners to support the network, Bitcoin would surely be headed for a grim future. That is not the case judging by the data. Miners are still bullish long term as are we.

Geopolitics Downs Dollar And Stocks

Friday May 25: Five things the markets are talking about

President Trump's decision to cancel his summit with N. Korea's Kim Jong-Un yesterday, mentioning Pyongyang's anger, is expected to keep geopolitics the primary concern for investors and dealers throughout the long weekend in the U.S.

It's not a surprise that yesterday's White House move has provoked a knee-jerk reaction from the various asset classes, including in haven assets such as gold, JPY and CHF.

Stocks are mixed, while U.S Treasuries and other sovereign bonds have edged higher along with the U.S dollar as investors navigate a number of political developments from Asia, Middle East and Europe. Crude oil has extended its losses.

In Europe, Spain's biggest opposition party is pushing for a no-confidence motion against PM Mariano Rajoy, while in Italy, the markets are concerned that the incoming government could sully Italy's relations with E.U.

In the U.K, PM Theresa May continues to feel the heat as the E.U has dismissed many of the U.K.'s plans for their post-Brexit relationship.

On tap: This morning, E.U finance ministers will discuss the latest on Brexit talks, in Brussels, while stateside, core-durable goods orders are released at 08:30 am EDT.

1. Equity markets trade mixed

Markets have recovered some risk appetite after N. Korea offered a “measured response” to the U.S decision.

In Japan, the Nikkei edged up overnight, supported by large cap stocks, but gains were limited after President Trump cancelled the June 12 summit. Defence-related stocks attracted buying on speculation that geopolitical tensions would rise. The Nikkei share average closed up +0.1%. For the week, the index lost -2.1%, its first weekly decline in nearly three-months. The broader Topix dropped -0.2%.

Down-under, Aussie shares edged lower overnight, as declines in materials and energy stocks on lower commodities and oil prices outweighed gains in consumer staples. The S&P/ASX 200 index slipped -0.1% at the close of trade. The benchmark fell -0.9% for the week, its biggest decline since March. In S. Korea, the Kospi pared much of its earlier loss of -0.9% to trade down -0.2%.

In China and Hong Kong stocks edged lower, as sentiment soured after President Trump called off next months planned Singapore summit. The CSI300 index rose +0.1%, while the Shanghai Composite Index slipped -0.1%.

In Hong Kong, the Hang Seng index dropped -0.3%, while the Hong Kong China Enterprises Index lost -0.5%.

In Europe, regional indices have opened broadly higher and continued to move further into positive territory. Nevertheless, geopolitical concerns are keeping risk sentiment low.

U.S stocks are set to open deep in the ‘black' (+2.0%).

Indices: Stoxx50 +0.6% at 3,544, FTSE +0.3% at 7,741, DAX +0.9% at 12,976, CAC-40 +0.6% at 5,581; IBEX-35 +0.4% at 10,034, FTSE MIB +0.1% at 22,756, SMI +0.6% at 8,821, S&P 500 Futures +2.0%

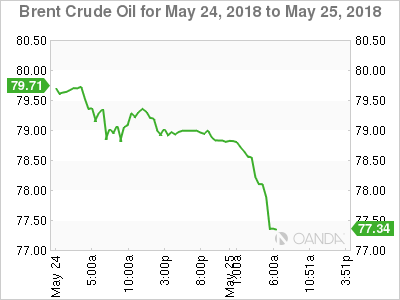

2. Oil slips on talk OPEC may lift output, gold prices lower

Oil prices remain soft as OPEC and Russia consider easing supply curbs to offset disruptions in Venezuela and an expected drop in Iranian exports.

Brent crude futures are down -44c at +$78.35 a barrel, having hit their highest since late 2014 at +$80.50 this month. U.S West Texas Intermediate (WTI) crude futures are at +$70.38 a barrel, down -33c.

Market chatter is suggesting that the energy ministers of Saudi Arabia, Russia and the U.A.E are discussing an output increase of about +1m bpd.

Global crude supplies have tightened sharply over the past year because of the OPEC-led cuts, which were boosted by a dramatic drop in Venezuelan production.

Note: Russia and OPEC's voluntary output cuts have opened the door to other producers to ramp up production and gain market share.

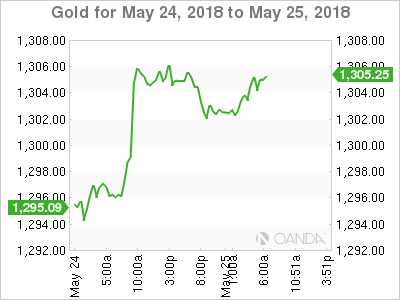

Ahead of the U.S open, gold prices have eased a tad on profit taking, after breaking above +$1,300 in yesterday's session on geopolitical worries. Spot gold is down -0.2% at +$1,301.65 per ounce, after climbing nearly +1% Thursday in its biggest one-day rally since early April.

3. Sovereign yields fall on geopolitical worries

Sovereign bond yields have dropped to new monthly lows this week after the U.S/N. Korea summit was cancelled.

The White House announcement yesterday sparked a rush into safe haven assets including eurozone government bonds and the Japanese yen.

Note: German debt was already in demand after Wednesday's weak Euro PMI's and both the Italian and Spanish political risk scenario.

The yield on 10-year Bunds, one of the safest and most liquid have dropped -4 bps to +0.46% – it's lowest since mid-January. At +2.40%, the yield on Italy's 10-year BTP bond is not far from this week's 14-month high of +2.45%.

In the U.S, 10-year yields again have fallen below the psychological +3% (+2.965%) after this week's Fed minutes showed the central bank plans to stay on a “gradual” path of rate increases even if inflation meets its target. The minutes also showed U.S officials are still unsure over the degree to which low unemployment will fuel faster wage increases or firmer price pressures.

4. The dollar recovers slightly

G7 currency ranges remain relatively contained ahead of the bell on Wall Street and the long weekend stateside and in the U.K.

EUR/USD has fallen -0.1% to €1.1706 as the dollar recovers some small gains after yesterday's safe haven knee jerk. The safe-haven Japanese yen is retracing gains against the dollar as well, with USD/JPY up by +0.2% at ¥109.41.

GBP (£1.3361) continues to remain vulnerable to Brexit negotiations. This week saw the pound trade atop of its five-year low at £1.3304.

Turkey's lira is heading for its biggest five-day decline since the global financial crisis despite this week's emergency rate hike. TRY has given up a large chunk of the gains it made after the CBoT raised interest rates by +300 bps on Wednesday, falling -1.1% to $4.7202. The lira has fallen almost -15% so far this month.

5. U.K business investment slips in Q1,2018

Data this morning showed that U.K business investment posted its weakest quarterly growth in almost three-years in Q1 and more proof of slow economic growth and uncertainty surrounding Brexit.

ONS reported that capital expenditure by British businesses fell by -0.2% in Q1 and marked the sharpest slowdown since Q3, 2015.

Digging deeper, the ONS said that weakening investment in non-residential buildings and structures such as schools, bridges, and commercial buildings was among the key drivers of thaQ1 slip.

Other data reported by the ONS showed that its GDP second estimate for Q1 remained unchanged at +0.1%, with an annualized figure of +0.4% – the weakest quarterly growth for the U.K economy in more than five-years.

DAX Rebounds On Strong German Confidence Report

The DAX is sharply higher in the Friday session, erasing the losses from the Thursday session. Currently, the DAX is at 12,996, up 1.10% on the day. On the release front, German Ifo Business Climate ticked higher to 102.2, above the estimate of 102.0 points. Later in the day, Fed Chair Jerome Powell and German Bundesbank President Jens Weidmann will address a forum in Stockholm.

The much-anticipated summit between President Trump and Kim Jong-un has been abruptly canceled. Trump sent a letter to Kim on Wednesday, saying that he could not go ahead with the meeting, scheduled for June 12 in Singapore, after particularly harsh comments by the North Korean leader. For his part, Pyongyang was restrained in its response, saying that it still looked forward to resolving outstanding issues with the US. The muted reaction was good news for the stock markets, as tensions between the US and North Korea have rattled investors in recent months. If Trump and Kim decide to re-escalate tensions, the markets will likely respond with losses.

Drama in Italian politics is nothing new, but the latest saga is causing concern in Brussels and on the part of investors. After weeks of wrangling, President Sergio Mattarella handed a mandate to Giuseppe Conte to form a coalition. Conte is from the Five Star Movement, which plans to govern with the Lega Nord. Both parties are anti-establishment and euro-sceptic. Their platform includes increased deficit spending and a crackdown on immigration, two issues which could put Italy, the third largest economy in Europe, on a collision course with Brussels. Earlier in the week, ECB governing council member Ewald Nowotny admitted that the political situation in Italy had “created a lot of nervousness”, but that the new government would be judged on its actions.