Sample Category Title

Dangerous Brinkmanship

Dangerous Brinkmanship

Another in the expanding history list of topsy-turvy Thursdays' when it comes to risk as the President Gave, and the President Hath Taken Away only to leave the door open again when it comes to North Korea discussions.

The increasing headline chatter around the North Korea summit finally culminated with President Trump cancelling his upcoming summit meeting with North Korea leader Kim Jong Un. But of course, as we've seen countless times before, the President tends to walk back some of his more boisterous rhetoric time and time again. So, it's hand out to North Korea in this risky ping-pong match of political brinkmanship.

After the initial knee-jerk reaction of risk off, the fixed income bid has tapered, USDJPY has also rejected a test of the 109 handles while US equity markets have pruned losses. The overall sell-off was a low keyed affair, but should not be interpreted as diminishing the fragility of the current state of geopolitical risk. But the market has travelled a path well-worn on Korean peninsula risk, and while the US and their allies have offered a way to prosperity for North Korea, it was never going to come without some significant concession on the nuclear non-proliferation front.

But given that Asian markets, particularly the Nikkei, have a higher sensitivity to this issue, the market is treading gingerly ahead of APAC open as we could have another case of risk aversion creep into the picture at that time.

Heading for the Friday finish line with a long weekend looming in both US and UK, we should expect some position consolidation. And while the markets look to favour, a risk-off strategy given geopolitical risk is up front and centre again, however, the slightly dovish lean from the FOMC minutes has provided a spark to US equities after the statement triggered of an unwind on bearish US interest rates short -end positioning. To make a long story short, it's complicated.

To be honest, after spending the better part of yesterday looking for the ideal set up on a currency trade, I've concluded the market will remain fickle until more coherence is offered on trade wars and the North Korea situation. Not the ideal market to be picking bottom or tops for that matter as a lot of currency opinions are gravitating to the ” do not trade zone “ahead of the US long weekend.

Oil Market

Yesterday's inventory shocker continues to reverberate in the markets as oil prices have gravitated lower. But of course, the potential increase in OPEC output to offset supply concerns continues to in broad strokes paint a bearish narrative. In the absence of another negative supply surprise, the top side moves will likely be capped by short-term trader's propensity to fade these moves on the assumption OPEC opens the spigot.

But, this supply unwind needs to be viewed cautiously as its very unlikely the OPEC / Non-OPREC compliance will buckle but instead, there will be a gradual supply accommodation commensurate with global demand rather than a decisive policy shift thereby most likely keeping the 3-6 month +$ 80 Brent /bbl views intact.

Gold Markets

The more dovish interpretation of the FOMC minutes coupled with the increase in geopolitical risk has Gold glittering above the critical $ 1300. But the overnight session was all about headline risk as North Korea and Trade risk continue to dominate. So, with the anticipation of more headline risk coming down the pipe, gold should hold a bid as its glittering appeal is hard to ignore when geopolitical risk rises.

Currencies

The dollar rally has cooled it jets after the latest FOMC minutes suggested a willingness to let inflation run hotter than their inflation target. Comparing the relative policy stances from the ECB and BOJ who are fighting neck and neck with the RBA to be the most boring central bank on the planet. Even the Feds three rate hike scenario in 2018s suggests that until either the ECB or BoJ stops sitting on their hands, the dollar should remain attractive over the near term.

JPY: Best instinct suggest staying away, but of course risk aversion trade is sometimes too hard to ignore even more so with the dovish market interpretation of the FOMC minutes. Look for the possible retest of 109 on geopolitical headline escalation.

EUR: The weaker PMI suggest more downside to come as the ECB should lean dovish on the data.

AUD: The dovish read on the FOMC minutes has seen US equities trade well and supporting risk currencies like the Aussie. However, Oil continues to trade heavy as do some of the other hard commodities suggesting the topside remains limited

MYR: The political noise is bordering on deafening and with fiscal uncertainty continuing to linger it's unlikely we will see much in the way of foreign participation or any meaningful flows over the short term for that matter. However, given the market tends to fade political risk, if the fire sale becomes big enough it will attract some interest but with the USD still sitting favourably vs the EURO and North Korea tensions coming to the fore, it's certainly not time to dip ones toe into the turbulent Malaysia waters just yet.

British Pound Edges Higher As Retail Sales Sparkle

The British pound has posted slight losses in the Thursday session. In North American trade, GBP/USD is trading at 1.3377, up 0.21% on the day. On the release front, British Retail Sales posted a strong gain of 1.6%, crushing the estimate of 0.8%. Over in the US, unemployment claims jumped to 234 thousand, its highest level in seven weeks. As well, Existing Home Sales dropped to 5.42 million, well off the estimate of 5.56 million. Friday will be busy, with key releases on both sides of the pond. The UK releases Second Estimate GDP and Preliminary Business Investment. In the US, we’ll get a look at durable goods orders and consumer confidence.

The Federal Reserve released the minutes from its May meeting. In the minutes, some Fed policymakers said they favored removing the phrase that “the stance of monetary policy remains accommodative”. Not surprisingly, the minutes didn’t shed light on the Fed’s plans, saying that another rate hike would occur “soon”, on the assumption that the US economy continues to perform as expected. Still, a quarter-point rate hike in August is virtually a given, with the CME Group setting the odds of a hike at 95 percent. This would mark a second hike in 2018. After that? The Fed projection remains at three rates hikes in 2018, but some analysts are predicting four increases this year.

Just a few weeks ago, there was a strong likelihood that the Bank of England would raise interest rates at the May policy meeting. However, a spate of weak economic releases and falling inflation resulted in policymakers standing pat, leaving rates at 0.50%. Are we in for a repeat performance in August? Inflation levels continue to drop, with April CPI falling to 2.4%, down from 2.5% a month earlier. If Friday’s GDP report misses expectations, an August rate hike will be in serious doubt. Earlier in the week, the markets priced in an August hike at 50%, but this dropped to just 33% after Wednesday’s weak inflation data. The pound is also under pressure, and the downward spiral is likely to continue if this week’s indicators do not perform well.

Eco Data 5/25/18

[php_everywhere instance="1"]

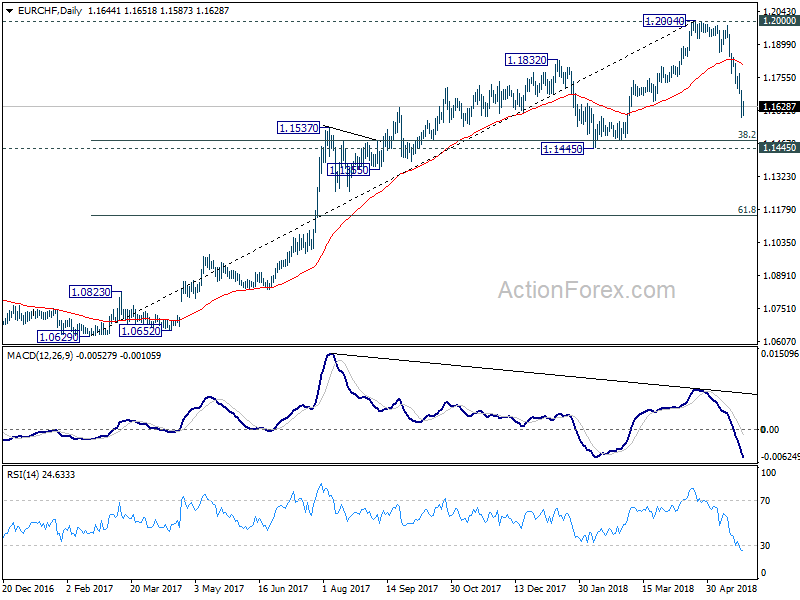

Swiss Franc unconvincingly the second strongest today, a look at EURCHF again

Yen is trading as the strongest one for today as boosted by risk aversion and falling treasury yields. Trump's pull out from the meeting with Kim triggered some selloff in stocks. But loss is relatively limited. On the other hand, it's the steep decline in 10 year yield, which hit as low as 2.955 so far, that looks more serious.

Swiss Franc follow as the second strongest one for today. However, even so, it's held below yesterday's high against all major currencies. Momentum is rather unconvincing. Having a look at EURCHF action bias table, while D action bias stays consistently downside red, 6H Action Bias is showing some hesitation.

A further look at the 6H Action Bias chart, it seems that EUR/CHF started to lose downside momentum after hitting 1.1580. Though, there is no convincing evidence that the cross is reversing yet.

Following up on our short strategy here. In the current situation, there are two choices, get out, or stay short. Considering that EUR/CHF is in deep over sold region as seen in daily RSI, we'd prefer to close short right now, with around 80 pt profit first. For those we'd like to hold on for 1.1445 target, we'd suggest to lower the stop to break even at 1.1705.

Italian Election Monitor: Rising Market Pressure Set to Challenge Spending Plans

- It will be difficult for the Five Star-League coalition government to fully implement its policy proposals, especially under rising market pressure and the moderating influence of the President.

- We expect a slow convergence between Italian government bonds relative to the core EU in the coming months, but still have a number risk factors ahead.

- Until more clarity regarding the actual policy implementation is obtained, an Italy risk premium will likely continue to weigh on the euro.

The personnel carousel keeps turning

Another hurdle was cleared in the Italian government formation process yesterday when President Mattarella affirmed law Professor Giuseppe Conte as Prime Minister and tasked him with forming a government. In his acceptance speech, Conte struck a relatively conciliatory tone, confirming Italy's European and international ties, but he also pledged that the blueprint presented by Five Star and League last week will guide the government agenda. Conte will consult with party leaders today and over the next few days will propose the list of cabinet ministers to the president for approval. Only then can the new government move ahead in securing a vote of confidence in both houses of parliament (potentially sometime next week) and start moving ahead with some of its policy proposals as outlined in Italian Election monitor: Stand-off between EU and new Italian government looming. For now, the new cabinet looks likely to become a mix of technocrats and politicians. The choice of finance minister will be of particular market interest given that he sets the budget policy. An appointment of the euro-sceptic front runner Paolo Savona could trigger another deterioration in market sentiment and sound alarm bells in Brussels – but we would not rule out President Mattarella making use of his veto in this case, given his concerns about the economy and financial stability. According to Italian media, an alternative choice could be Luigi Zingales, a professor of finance at the University of Chicago, whose appointment would likely trigger a positive market reaction given his strong professional background. The two leaders of Five Star and League, Luigi Di Maio and Matteo Salvini, are expected to head the Economic Development and Interior ministries, respectively.

Policy implementation faces hurdles

Given that the government composition is yet unknown, it is difficult to say which policies would be prioritised, but we would expect that one of the first tasks of the government will be to work on the 2019 budget, which needs to be approved in the autumn. Although Italy has some fiscal leeway of around 0.7% of GDP (roughly EUR12bn), we think it will be difficult for the Five Star-League coalition government to fully implement its programme in its current from (pointing to a fiscal deficit of 6-7% of GDP). Firstly, bills regarding budgetary measures require approval by both chambers of parliament and the government would have to rely on a fairly slim majority of 6 seats in the Senate (31 seats in the lower house). This could prove a hurdle, for example when approving contentious measures, due to possible defections in the face of rising market pressure on Italian yields.

Furthermore, we expect President Mattarella to exert some moderating influence on exaggerated spending proposals. President Mattarella already indicated that he will play an active role in ensuring fiscal and political sustainability and accordance with international treaties of any bills presented to him for approval. The Italian President has the right to veto government bills which are deemed unconstitutional and may hence reject any legislation that threatens the stability of public finances and the balanced budget requirement according to Art. 81 (see box below). Although the two houses of parliament can override the president's veto, Mattarella could still postpone the implementation of controversial measures. Especially costly proposals such as the universal basic income and the introduction of a flat tax rate with an estimated cost of EUR67bn alone look like plans that could meet with opposition from the President and might end up being watered down in our view. Other factors could also hamper the implementation process, such as the inherent mistrust between the two parties and a preference for delaying difficult measures, especially in the face of rising market pressure.

Standoff with EU looming – snap elections still possible

In our view the new Italian government will think carefully before picking its fights both domestically and abroad and not pursue a pure confrontational course with the EU from the beginning, despite its call for an overhaul of European fiscal and monetary rules. We could get a first glimpse of the future Italy-EU relationship at the European Council meeting at the end of June. Despite some member states such a France and rating agencies already voicing concerns of the new Italian government's spending plans, we expect the EU to adopt a wait-and-see approach for now until more clarity is gained about the actual Italian 2019 budget proposal, to be submitted to Brussels by 15 October. We do not think the EU/European Commission will accept unfunded fiscal easing from Italy and in case of a clear violation of the Maastricht criteria, could for example launch an Excessive Deficit Procedure (EDP) against Italy

The new Italian government will be an inherently weak and fractious one and the risk of a government crisis and snap elections remains non-negligible in our view, especially in the face of rising market pressure on Italian debt servicing costs. We still see the risk of a pro-longed stand-off between the Italian government and the EU, but our base case remains that the Italian government will eventually conform with EU rules due to the reasons outlined above and agree to more moderate spending measures.

FI market: slow convergence to core EU with 'bumps' ahead

Italian bonds recovered slightly today, but the 10Y yield has reached 2.30%. The first comments from the new PM together with the possible choice of a finance minister that are "pro-business" such as Zingales will be supportive for the Italian government bonds. However, we still have a number risk factors in the coming months such as what fiscal policy will actually be implemented and how the fiscal expansion will be funded.

We expect that we will see a slow convergence between Italian government bonds relative to core-EU in the coming months, but there will be short-term "bumps" during the course of convergence. We have come too far to let the new Italian government derail the reform process that has been ongoing since the EU debt crisis began in 2011. We think the ECB will not be supporting Italy if the market sell offs on the back of a significant fiscal easing, that is deemed irresponsible. Here, we expect that EU and ECB will let the market pressure Italy towards a more responsible fiscal policy.

FX market: EUR debt risk revisited

Following complacency in the immediate aftermath of the election, EUR crosses have over the past week been markedly hit by the soaring Italian debt worries. As previously stressed, we think the Italy issue remains far from evolving into a new euro debt crisis, see e.g. Strategy - Italy under pressure - we keep our long position , but until more clarity regarding the actual policy implementation is obtained, an Italy risk premium will likely continue to weigh on the single currency. Notably, our Short-Term Financial Model for EUR/USD illustrates that the surge in Italian yields relative to Germany and the sustained uptick in US yields largely justifies the move towards 1.17. Lower levels in the cross could be tested but we have a hard time seeing November lows (watch out for 7-Nov low of 1.1554) being broken.

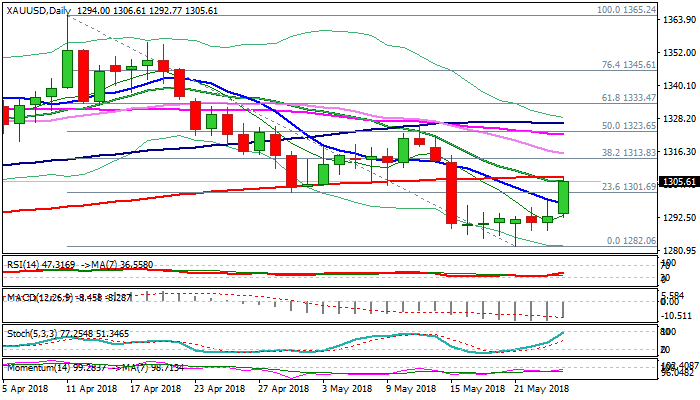

Spot Gold Rallies above $1300 on Renewed Uncertainty after US – North Korea Talks Were Cancelled

Spot Gold price surged above $1.1300 barrier on Wednesday, signaling an end of six-day congestion, marked by multiple long-legged Dojis.

Decision of US President Trump to cancel planned historical summit with North Korea, causing uncertainty in the markets which sparked fresh safe-haven demand.

Gold price rose to new over one week high at $1306, where 200SMA limited rally for now.

Initial bullish signals were generated on lift above 10&20SMA’s with strengthening momentum underpinning the advance.

However, bulls need firm break above 200SMA to signal further recovery, with lift above $1313 (Fibo 38.2% of $1365/$1282 descend) to confirm and generate stronger reversal signal.

Corrective dips should remain above broken 10SMA ($1297) to keep fresh bulls in play.

Res: 1307; 1309; 1313; 1315

Sup: 1300; 1297; 1292; 1287

Commentary following Trump’s Announcement about the North Korea Summit

The pace in demand for the Japanese Yen has picked up significantly following the breaking announcement moments ago from President Trump that the North Korea summit will not be going ahead. Gold is also roaring higher, providing confidence to the view that investors are suddenly moving towards safe haven assets.

What we are noticing in the market is a sudden change in investor sentiment, where traders are becoming less inclined to look at riskier assets and are encouraged to safe havens instead.

If investors use this news to price political risk premium back into their portfolios, then we could have a very busy conclusion to what has already been an eventful week for the financial markets, with the Turkish Lira crisis and the ongoing trade negotiations between Washington and Beijing already attracting attention across the globe.

US 100 Index Eyes 7,000 Handle; Bullish in Long-Term

The US 100 index is moving marginally below the previous week’s high of 7,000. During yesterday’s session, the price rebounded on the middle Bollinger line (this being a 20-day simple moving average one) and is still developing well above the 50- and 200-day SMAs, suggesting an extension of the bullish tendency.

However, the RSI indicator seems to be somewhat halting its advance, hinting to a possible change in short-term dynamics from bullish to bearish. Turning to the MACD oscillator, in the short-term chart, it is giving neutral signals as it is flattening in the positive territory.

Should the index extend its gains, the next level to have in mind is the 7,000 psychological resistance level. A jump above this area would endorse the bullish bias and start to increasingly challenge the 7,185.15 record high, achieved on March 13.

On the downside, the price could touch the 50-day SMA near 6,733 before being able to slip towards the lower Bollinger Band around 6,600. The 6,420 barrier which was violated in the past may offer support on the way down as well.

Overall, there are bearish signals in the short-term, while the medium-term picture is still bullish, with price action taking place above both the 50- and 200-SMAs.

Sunset Market Commentary

Markets

Today, the intraday moves in (core) bonds were more modest compared to the previous days. The topics that caused investor nervousness of late aren’t solved. The Trump administration investigating the need of import tariffs on automobile imports might even become an additional source of uncertainty. However, at least today, there was little in the way of additional negative news e.g. from Italy. European equities and US equity futures tried a cautious rebound this morning, but the move could not be sustained. Bunds and Treasuries lost temporarily a few ticks but the downside was well protected. In the Minutes of the April policy meeting, the ECB admitted that uncertainty on the outlook had increased. However, the bank basically maintained a positive assessment on the economy. US yields decline between 1 bp and 2 bps. So, the 10-year yields is drifting a bit further below the 3.0% mark. German yields also decline marginally with long end outperforming (-2.2 bps for 30-y). So, there is clearly no upside reversal (in yields) after recent substantial decline. The bund contract and the 10-y yield stay near key resistance/support levels. EMU peripheral bond markets entered calmer waters. The 10-y Italian spread versus Germany ‘narrowed’ 1 bp. Spain (-5 bps), Portugal (-5 bps) and Greece (-14 bps) outperformed.

The dollar traded with a slightly negative bias today. USD/JPY stayed under pressure this morning (Japanese markets reacted in a negative way to the threat of US import tariffs on autos). USD/JPY finally settled in the mid 109 area. EUR/USD tried a cautious intraday rebound after an extensive test of the 1.1700 support area. However, the move has no strong legs. EUR/USD currently trades in the 1.1735 area. So, the recent lows are still within reach and the sources of recent euro softness are still pending.

After a series of disappointing data, the April UK retail sales finally brought a positive surprise. Sales excluding auto fuel rose 1.3% M/M (after a 0.5% decline in March). The consensus expected a more modest rise of 0.5% M/M. The reaction on the UK interest market and of sterling was modest. EUR/GBP drifted north going into the publication of the report, but this move was mainly due an overall intraday rebound of the euro, rather than sterling weakness. After the retail sales EUR/GBP reversed the earlier rebound. The pair dropped to the 0.8740/50 area. In a broader perspective, this retail sales report obviously isn’t a strong enough trigger for markets already to raise the probability of an August rate hike. This is a fortiori the case after yesterday’s soft April CPI data. More good news, both on economic activity and on prices, is needed for sterling to receive any meaningful interest rate support. For now EUR/GBP remains blocked in the 0.87 area. Cable regained the 1.34 barrier, but this move at least partially mirrors a less strong USD momentum.

News Headlines

At the IIF conference, the ECB’s chief economist Peter Praet reiterated economic conditions are good, but some “clouds” are on the horizon. He referred to political uncertainty in places like Italy that could fundamentally undermine business confidence.

The Turkish lira resumed its slide after it rallied back dramatically due to an emergency rate hike of 300 bps. Markets are questioning whether the move is sufficient to stabilize the currency, which already lost 15% since April.

In an interview, Fed’s Kaplan said “we should be raising rates until we get to neutral”, adding he’s not yet prepared to say he want to go above neutral. In Kaplan’s view, interest rates need to be raised four more times before reaching the equilibrium level.

Canadian Dollar Dips as Trump Threatens Tariffs

The Canadian dollar continues to head lower and has posted considerable losses in the Thursday session. Currently, USD/CAD is trading at 1.2895, up 0.47% on the day. On the release front, Canadian Corporate Profits rebounded in the first quarter with a strong gain of 2.7%. In the US, unemployment claims jumped to 234 thousand, its highest level in seven weeks. Later in the day, the US releases Existing Home Sales, which is expected to drop to 5.56 million. On Friday, the US will publish durable goods orders as well as consumer confidence.

The Federal Reserve released the minutes from its May meeting. In the minutes, some Fed policymakers said they favored removing the phrase that “the stance of monetary policy remains accommodative”. Not surprisingly, the minutes didn’t shed light on the Fed’s plans, saying that another rate hike would occur “soon”, on the assumption that the US economy continues to perform as expected. Still, a quarter-point rate hike in August is virtually a given, with the CME Group setting the odds of a hike at 95 percent. This would mark a second hike in 2018. After that? The Fed projection remains at three rates hikes in 2018, but some analysts are predicting four increases this year.

Earlier this week, there seemed to be some positive momentum regarding the US-China trade talks. However, President Trump has since voiced skepticism over progress in the negotiations, saying he was ‘not really’ satisfied with the results. This has been followed by reports on Wednesday that the US is investigating auto imports on national security concerns, which has raised concerns that US tariffs could shake-up the global auto sector. Trump’s comments have confused the markets, as Treasury Secretary Steven Mnuchin declared on the weekend that the trade spat was ‘on hold’. Investor risk appetite has also waned as there is uncertainty whether North Korean leader Kim Jong-un will meet with President Trump next month. On Tuesday, Trump acknowledged that there was a ‘substantial’ chance that the summit planned with Kim in Singapore on June 12 would not take place.