Sample Category Title

UK Retail Sales Beats Expectations

Notes/Observations

- UK Apr Retail sales data handily beats expectations with higher back-month revisions

- Focus on Italy’s potential govt selection for the Finance Ministry position

Asia:

- North Korea Foreign Ministry Official suggested to North Korea leadership to reconsider US/North Korea summit; future of the summit is entirely up to the US

- China Foreign Min: US should stick to one China policy

- China State Council Member Wang Yi: The US decision to disinvite China from RimPac military exercise not constructive; hoped US would reconsider. Deployments have nothing to do with militarization

- China Premier Li saw 'huge' potential for China-Germany cooperation; stronger and more stable Euro benefits China. Hoped for a strong euro currency and to continue to buy euro denominated debt. CNY currency (yuan) internationalization was a long-term process – joint press conference with German Chancellor Merkel

Europe:

- Italy President Mattarella gave PM mandate to Giuseppe Conte to try and form a govt (as expected)

- Spain parliament approved 2018 budget (Vote was 177 to 168) - UK PM May said to ask EU for new Brexit transition to run until 2023 in avoid a hard border with Ireland. This new transition was proposed to cover trade and customs and the govt would follow the period already agreed and scheduled to run until 2020

- PM May reportedly targets to schedule controversial Brexit vote back in Parliament in June (Note: will mean a showdown between the different factions of her Conservative Party)

- German Chancellor Merkel supported the conclusion of the EU-China investment protection agreement. Chinese investment in Germany was appropriate.

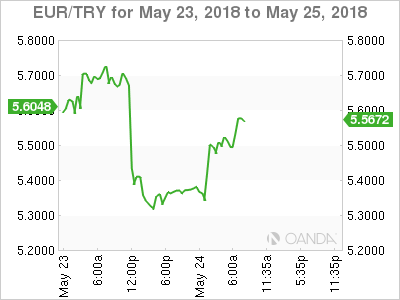

- Turkey Central Bank (CBRT) raised Late Liquidity Window (LLW) by 300bps to 16.50% (intra-meeting move). maintains Benchmark Repurchase Rate at 8.00%. Reiterated view that tight stance would be maintained decisively until inflation outlook displays significant improvement

Americas:

- US President Trump confirmed he gave Commerce Dept the order to consider probe on auto imports under Section 232 review (as speculated)

- FOMC Minutes (May 2nd) noted that the Fed Funds Rate could reach the neutral level before too long if rate hikes continued. Officials saw trade and fiscal policies as sources of uncertainty

- Pentagon: US has disinvited China from 2018 rim of the Pacific military exercises as country continues to militarize disputed island

Energy:

- Iran Supreme Leader announced 7 conditions for European nations if they wanted Iran to remain in the nuclear accord. Called on Europe to protect Iran's oil market against US sanctions by continuing to buy Iranian oil; called for European banks to protect trade with Iran

Economic Data:

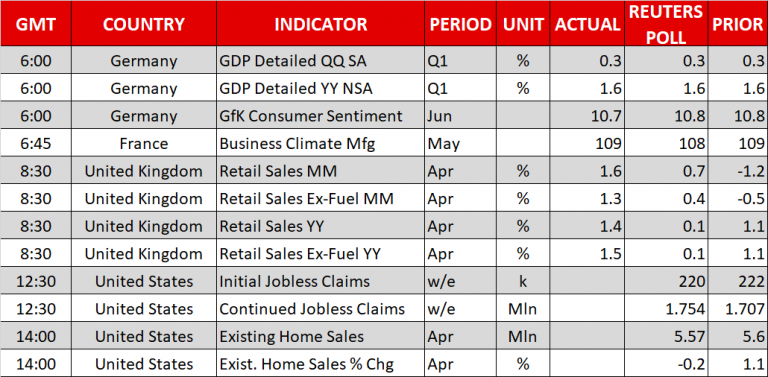

- (DE) Germany Q1 Final GDP Q/Q: 0.3% v 0.3%e; Y/Y: 2.3% v 2.3%e; GDP NSA Y/Y: 1.6% v 1.6%e

- (DE) Germany Q1 Private Consumption Q/Q: 0.4% v 0.2%e; Government Spending Q/Q: -0.5% v -0.2%e; Capital Investment Q/Q: 1.7% v 1.1%e; Construction Investment Q/Q: 2.1% v 1.0%e; Domestic Demand Q/Q: 0.4% v 0.4%e; Exports Q/Q: -1.0% v -0.5%e; Imports Q/Q: -1.1% v -0.5%e

- (DE) Germany Jun GfK Consumer Confidence: 10.7 v 10.8e

- (DK) Denmark Apr Retail Sales M/M: 0.2% v 0.1%e; Y/Y: 0.7% v 2.0% prior

- (FI) Finland Apr PPI M/M: 0.4% v 0.7% prior; Y/Y: 3.3% v 3.1% prior

- (FI) Finland Apr Preliminary Retail Sales Volume Y/Y: 0.1% v 2.7% prior

- (FR) France May Business Confidence: 106 v 108e; Manufacturing Confidence: 109 v 108e; Production Outlook Indicator: 15 v 22e; Own-company Production Outlook: 17 v 15 prior

- (CZ) Czech May Business Confidence: 15.6 v 17.2 prior; Consumer Confidence: 11.3 v 10.0 prior, Composite (Consumer & Business) Confidence: 14.7 v 15.8 prior

- (SE) Sweden Apr PPI M/M: 0.6% v 1.2% prior; Y/Y: 4.9% v 4.0% prior

- (SE) Sweden Q1 Total number of Employees Y/Y: 2.4% v 2.4% prior

- (UK) Apr Retail Sales (Ex Auto Fuel) M/M: 1.3% v 0.5%e; Y/Y: 1.5% v 0.1%e

- (UK) Apr Retail Sales (Includes Auto Fuel) M/M: 1.6% v 0.9%e; Y/Y: 1.4% v 0.2%e

Fixed Income Issuance:

- (SE) Sweden sold SEK500M vs. SEK500M indicated in 0.125% I/L 2026 bond; Avg Yield: -1.5372% v -1.277% prior; Bid-to-cover: x v 1.95x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx50 +0.4% at 3,557, FTSE -0.1% at 7,784, DAX +0.2% at 12,996, CAC-40 +0.5% at 5,591; IBEX-35 +0.6% at 10,082, FTSE MIB +0.9% at 23.14, SMI +.4% at 8,833 , S&P 500 Futures +0.1%]

- Market Focal Points/Key Themes: European stocks opened slightly higher and continued the trend; exception to upward move in indices was the FTSE 100; automotive stocks again in focus, this time negative following Trump considering tariffs; appointment of PM in Italy leads to support in stocks; energy stocks supported by oil price; commodities support materials; upcoming earnings expected in the US session inlcude Hormel Foods, Medtronic and Best Buy

Equities

- Consumer discretionary: Aryzta ARYN.CH -26.7%(results)

- Consumer staples: Tate & Lyle TATE.UK +5.9% (results)

- Financials: Euronext ENX.FR +3.2% (analyst action), Vontobel VONN.CH +0.2% (acquisition)

- Materials: Petra Diamonds PDL.UK -11.8% (rights offer)

- Telecom: TalkTalk TALK.UK +3.9% (results)

Speakers

- ECB Financial Stability Review: Increased risk taking in markets needs attention. Warned of risks of loose fiscal stance in high-debt countries

- ECB’s Praet (Belgium, chief economist): reiterated view that economic conditions are good despite recent softness

- ECB's Vasiliauskas (Lithuania): Does not disagree with forecasts of ECB rate hike in six months (**Note: view on the aggressive side)

- Spain PM Rajoy stated that Catalonia direct rule to remain until normal govt was in place

- Italy Five Star said to be considering Luigi Zingales for Finance Minister post (**Note: Seen more in the traditional style (not Euro skeptic). Paolo Savona (euro skeptic) said to remain the Five Star-League choice for that position

- UK govt official refuted speculation of an extended transition period (**Note: referred to reports that PM May said to ask EU for new Brexit transition to run until 2023 in avoid a hard border with Ireland)

- Russia Central Bank (CBR) Gov Nabiullina: Staff forecasts do not see a rate hike. Rates could move higher if domestic borrowings increased. Saw scope to increase sovereign borrowings

- Russia Fin Min Siluanov: Payment in Euros was possible for sanctioned goods

- Russia Energy Min Novak: To discuss gradual oil production recovery at the Jun OPEC/Non-Opec meeting; decision to depend on market situation

- China govt official: EU probe on China steel products huts trade. Hoped EU was cautious in trade restriction measures

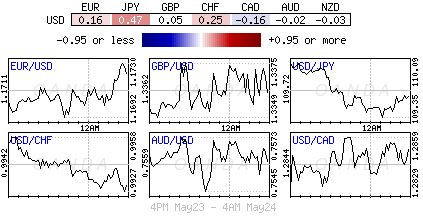

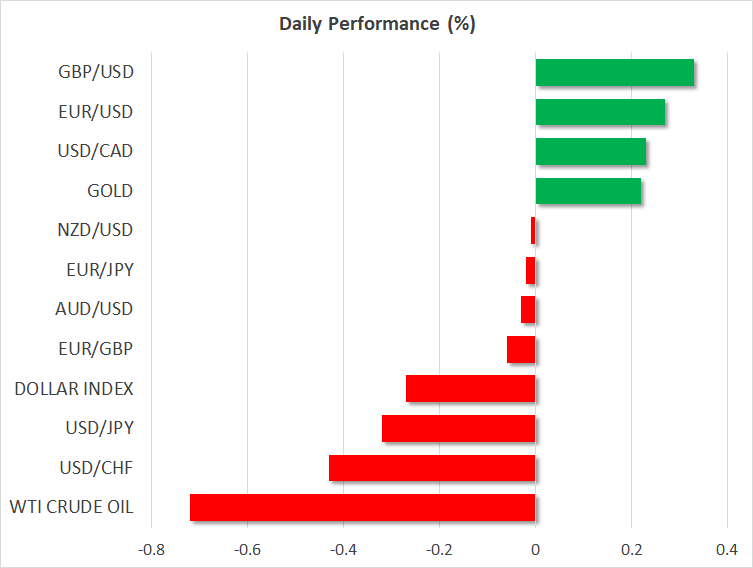

Currencies

- The USD consolidated some of its recent strength as bond yields moved lower after the perception of a slightly dovish set of Fed minutes.. Some analysts noted that the greenback might be losing momentum and putting its recent rally on the rocks. Fed minutes indicated that a further rate hike should be expected in June but that the Committee is not in a rush to clearly signal a more hawkish trajectory at this juncture

- EUR/USD was back above the 1.17 handle as markets awaited for more details on the proposed Conte govt in Italy. Focus will be on the selection of a Finance Minister (current speculation is between Luigi Zingales and Paolo Savona). Markets would favor Zingales as being less Euro skeptic.

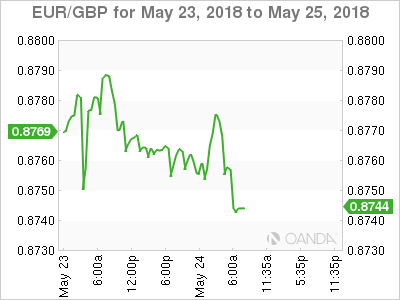

- The GBP currency (Cable) was firmer in the aftermath of better UK retail sales data. The GBP/USD moved above the 1.34 handle as market shorts were scrambling to cover.

- The TRY current was weaker in the session as participant believed that action taken by the Turkey Central Bank on Wed was viewed as a temporary fix in the overall scheme of things. CBRT only raised the Late Liquidity Window (a toll it has used frequently over the past year) rather than its key Benchmark Rate. USD/TRY tested 4.74 after the central bank action pushed the Lira to 4.55 area (from record lows of 4.93)

Fixed Income

- Bund Futures trade 10 ticks lower at 159.57 as the 10-year yield holds above 0.50%. Upside targets 159.75 followed by 160.50, while a return lower targets the 158.25 level.

- Gilt futures trade at 122.07 lower by 18 ticks following better than expected retail sales data. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Thursday’s liquidity report showed Wednesday's excess liquidity stayed rose from €1.837T to €1.838T. Use of the marginal lending facility increased from €128M to €295M.

- Corporate issuance saw 7 deals priced for $19.2B

Looking Ahead

- (UK) Last Day of Commons Session before Whitsun recess

- (AR) Argentina May Consumer Confidence: No est v 40.09 prior

- 05:30 (HU) Hungary Debt Agency (AKK) to sell bonds (3 tranches)

- 05:30 (PL) Poland to sell Bonds - 05:30 (IS) Iceland to sell 6-month Bills

- 05:30 (UK) DMO to sell £1.0B in 0.125%I/L Nov 2036 Gilts

- 06:00 (IL) Israel Mar Manufacturing Production M/M: No est v -3.3% prior

- 06:00 (RO) Romania to sell Bonds - 06:45 (US) Daily Libor Fixing

- 07:00 (UR) Ukraine Central Bank Interest Rate Decision: Expected to leave Key Rate unchanged at 17.00%

- 08:00 (PL) Poland Apr M3 Money Supply M/M: 0.5%e v 0.8% prior; Y/Y: 6.0%e v 5.8% prior

- 08:05 (UK) Baltic Dry Bulk Index

- 08:30 (US) Initial Jobless Claims: 220Ke v 222K prior; Continuing Claims: 1.75Me v 1.707M prior

- 08:30 (US) Weekly USDA Net Export Sales

- 09:00 (US) Mar FHFA House Price Index M/M: 0.6%e v 0.6% prior; Q/Q: 0.7%e v 1.6% prior

- 09:00 (BE) Belgium May Business Confidence: No est v 1.0 prior

- 09:00 (CL) Chile Apr PPI M/M: No est v -0.6% prior

- 09:00 (RU) Russia Gold and Forex Reserve w/e May 18th: No est v $457.7B prior

- 09:00 (ZA) South Africa Central Bank (SARB) Interest Rate Decision: Expected to leave Interest Rates unchanged at 6.50%

- 09:30 (BR) Brazil Apr Current Account: $1.2Be v $0.8B prior; Foreign Direct Investment (FDI): $3.0Be v $6.5B prior

- 10:00 (US) Apr Existing Home Sales: 5.55Me v 5.60M prior

- 10:30 (US) Weekly EIA Natural Gas Inventories

- 11:00 (US) May Kansas City Fed Manufacturing Activity: 20e v 26 prior

- 13:00 (US) Treasury to sell 7-Year Notes

ECB accounts offer nothing more than a bit of cautiousness

ECB's monetary meeting accounts offer nothing new to the markets, just a bit more cautiousness. Thus, Euro's reaction is rather muted.

Some quote from the monetary stance and policy considerations sections of the ECB monetary policy meeting accounts:

- The recent incoming information pointed to some moderation in activity but so far remained consistent with a solid and broad-based expansion of the euro area economy.

- The underlying strength of the euro area economy continued to support the Governing Council's confidence that inflation would gradually converge to its inflation aim of below, but close to, 2% over the medium term

- Measures of underlying inflation remained subdued and had yet to show convincing signs of a sustained upward trend.

- For underlying inflation pressures to continue to build up and support the path of headline inflation over the medium term, patience, persistence and prudence with regard to monetary policy remained warranted.

- Despite the observed moderation in activity, confidence in the underlying strength of the euro area economy and the eventual convergence of inflation to the Governing Council's inflation aim remained unchanged.

- While measures of underlying inflation continued to be subdued, some comfort was drawn from encouraging signs of a strengthening in nominal wage growth and the continued anchoring of long-term inflation expectations at levels consistent with the Governing Council's aim.

- While risks surrounding the euro area growth outlook remained broadly balanced, it was acknowledged that risks related to global factors, including the threat of increased protectionism, had become more prominent and warranted monitoring with regard to their implications for the medium-term outlook for growth and prices.

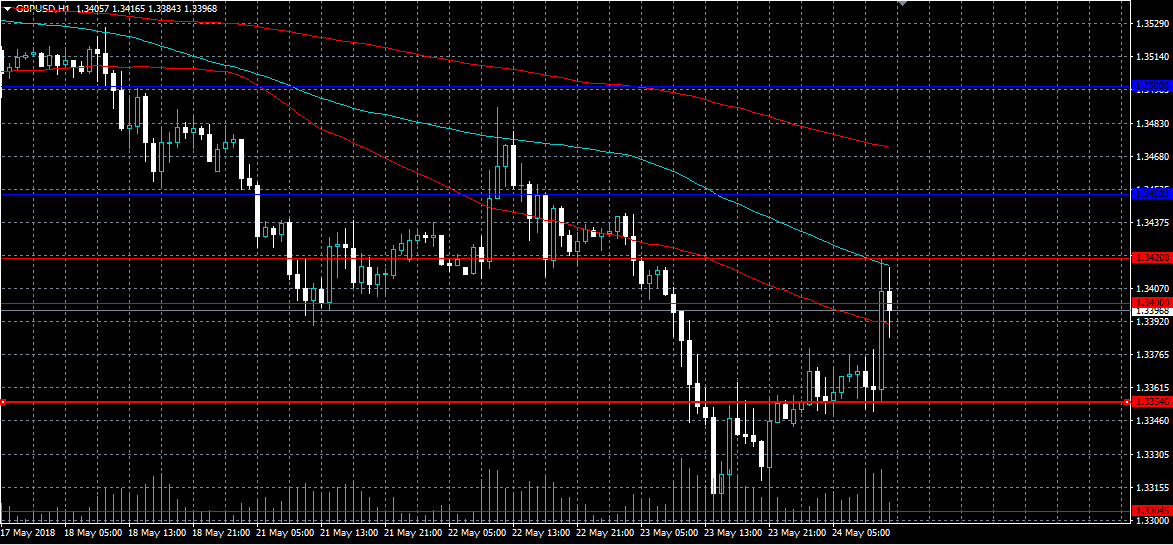

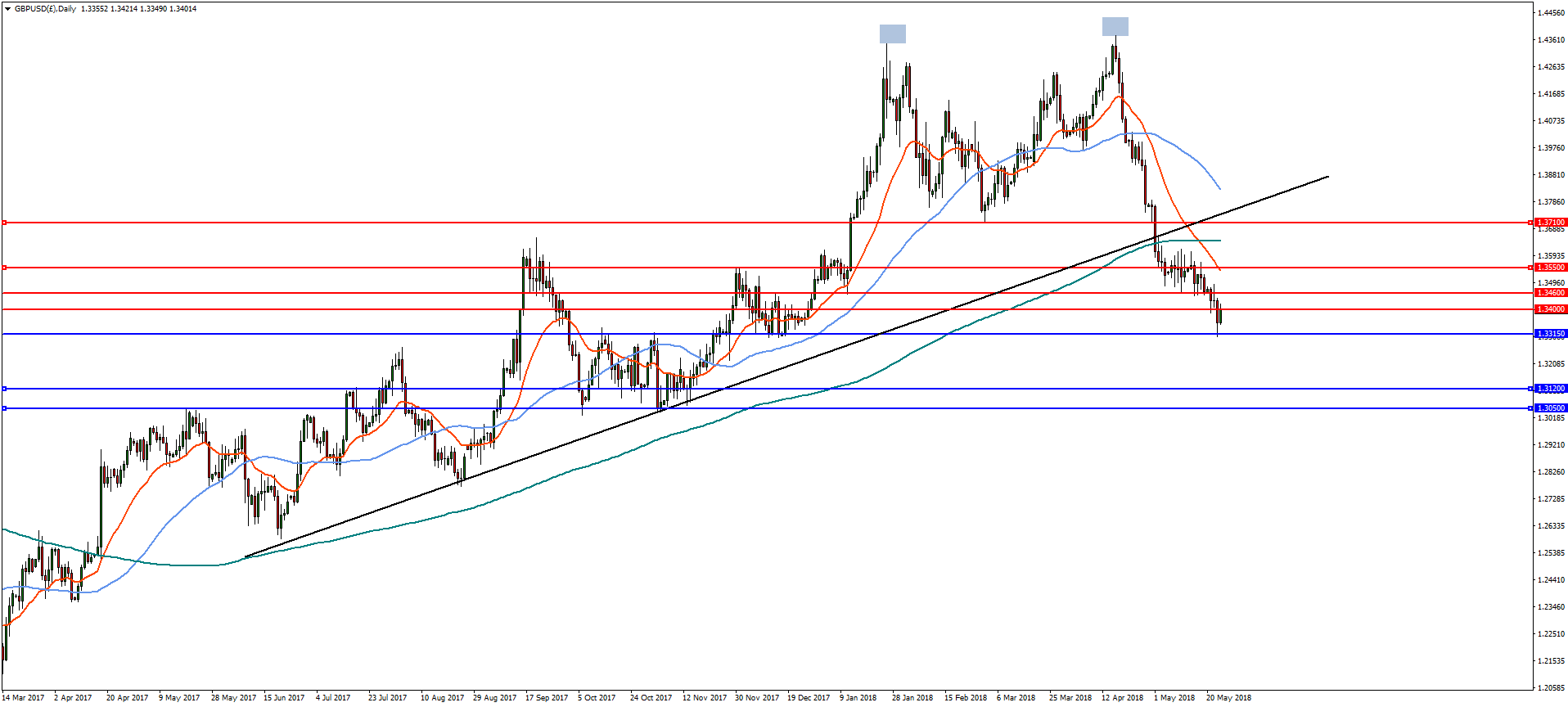

GBPUSD Attempting To Hold 1.3400 Level

The British pound has moved back towards the 1.3400 level against the US dollar, after the United Kingdom economy posted much better than expected monthly Retail Sales numbers. The GBPUSD pair currently trades around the 1.3390 level, after earlier moving to its highest trading level since May 22nd, hitting 1.3420. Sterling traders will look for further upside above the 1.3400 level, with the 1.3354 to 1.3450 trading-range now the key.

The GBPUSD pair is only bullish while trading above the 1.3450 level, key technical resistance is located at the 1.3450 and 1.3500 levels.

If the GBPUSD pair fails to move above the 1.3400 level, we may see a technical correction back towards the 1.3354 and 1.3304 support levels.

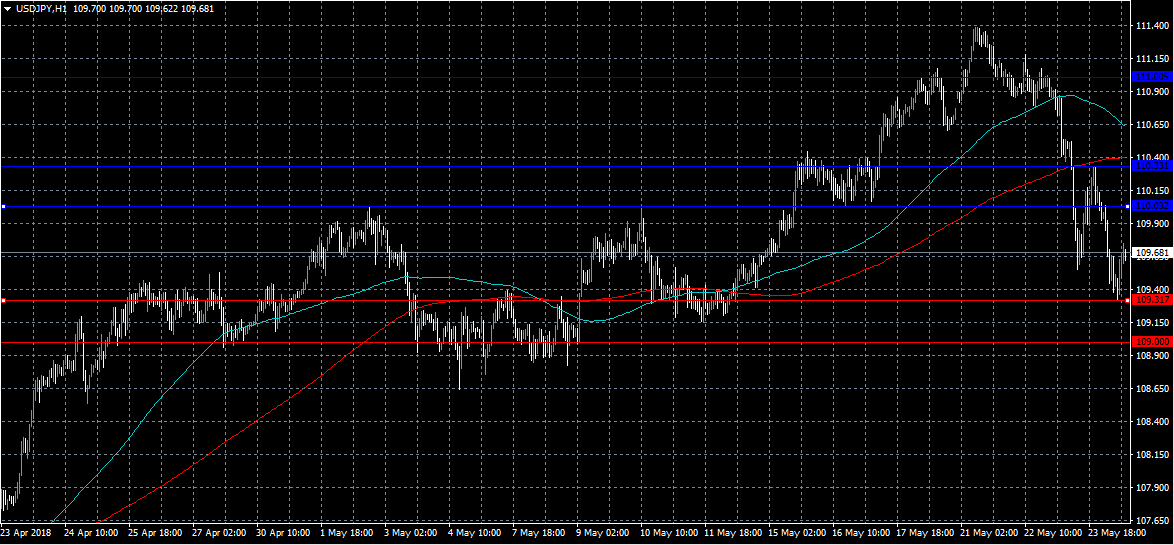

USDJPY Still Bearish Below Key 110.03 Level

The US dollar remains under selling pressure against the Japanese yen on Thursday, with traders using a short-lived move above the 110.00 level as an opportunity to sell the USDJPY pair. The US dollar index has also started to decline, adding further downside pressure to the pair, which earlier moved to a fresh weekly trading-low, hitting 109.31. Selling pressure is likely to remain on the USDJPY pair while price trades below the key 110.03 level.

The USDJPY pair is strongly bearish while trading below the 110.03 level, key support is currently located at the 109.31 and 109.00 levels.

If the USDJPY pair trades back above the 110.03 level, key resistance is now found at the 110.33 and 111.00 levels.

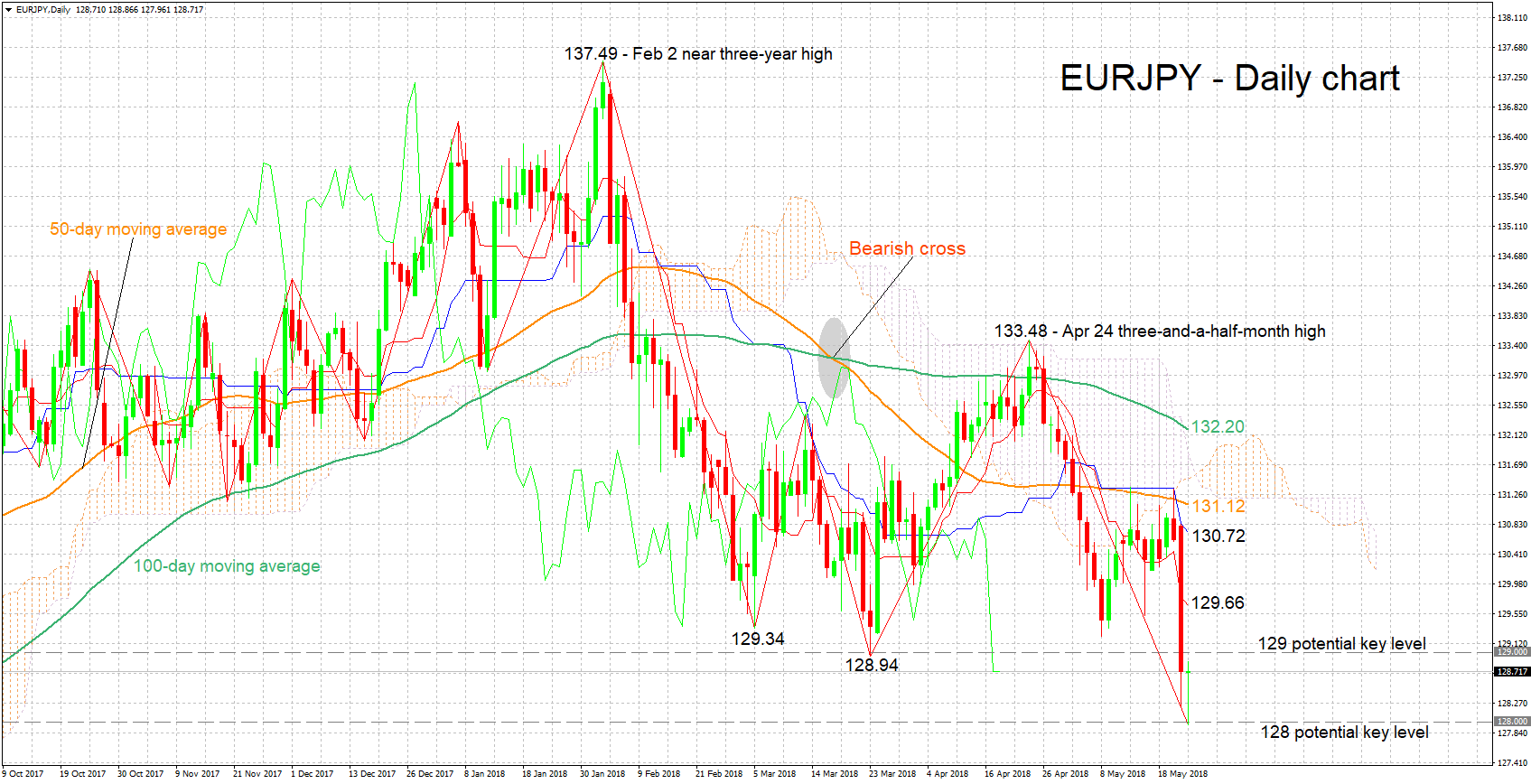

EURJPY Hits Fresh 9-Month Low, Possibly Oversold

EURJPY has declined considerably after posting a three-and-a-half-month high of 133.48 on April 24; it is currently trading 3.6% below that peak. Earlier on Thursday, it touched a fresh nine-month low of 127.96, after losing roughly 190 pips on Wednesday.

The Tenkan-sen line remains below the Kijun-sen in support of a negative short-term picture for the pair. The Chikou Span, though, may be pointing to an oversold market; a near-term reversal should not be ruled out.

Support to further declines could come around the 128 and 127 round figures that may hold psychological significance; the 128 handle was momentarily violated earlier on Thursday before the price bouncing back above it.

On the upside, resistance may be met around the 129 handle. Notice that a couple of bottoms from the recent past at 129.34 and 128.94 also lie close to this level. Further above, the region around the current level of the Tenkan-sen at 129.66 could also act as a barrier to price gains.

The medium-term picture is looking predominantly bearish at the moment: price action is taking place below the 50- and 100-day moving average lines, as well as below the Ichimoku cloud. Moreover, a bearish cross was recorded around mid-March when the 50-day MA moved below the 100-day one.

Overall, both the short- and medium-term outlooks are looking negative, though there are some signs hinting to a potentially oversold market in the near-term.

Pound Jumps On Retail Sales, Euro Gains Ahead Of ECB Meeting Minutes

Here are the latest developments in global markets:

FOREX: The US dollar lost more momentum after the minutes of the Federal Reserve’s last policy meeting were seen as dovish and the US President Donald Trump raised the prospect of new tariffs on imported cars similar to those introduced on steel and aluminum in March. Dollar/yen traded lower by 0.31% on Thursday, posting a 10-day low of 109.32. The US dollar index stepped back to 93.72 from its five-month high (-0.29%). Euro/dollar edged higher by 0.26%, following the pullback on the 6-month low as China signaled its confidence in the euro, ahead of the European Central bank (ECB) minutes later in the day. Pound/dollar advanced by 0.38% to 1.3400 after the bigger-than-expected increase in retail sales by 1.6% m/m in April from 1.1% in March, jumping its most in 1½-years. The Turkish lira plummeted by 2.48% against the greenback today, reversing the strong bullish rally which came after the central bank raised interest rates by 300 basis points on Wednesday. The Antipodeans were again losing some ground versus the greenback. Aussie/dollar was down by 0.05%, while kiwi/dollar moved lower by 0.01%. Moreover, dollar/loonie rose by 0.25% to 1.2858 and continued to move sideways.

STOCKS: In Europe, the majority of the indices had a green day with the British FTSE 100 and the German DAX 30 being the only exceptions. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were both higher by 0.29% at 1100 GMT. In Germany, the DAX eased by 0.05%, while the French CAC 40 rose by 0.39%. In Italy, the FTSE MIB 100 was up by 0.34%, while the British FTSE 100 was weaker by 0.06%. The Spanish IBEX 35 traded higher by 0.48%. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in positive territory, pointing to a higher open today, continuing the upward movement from last week.

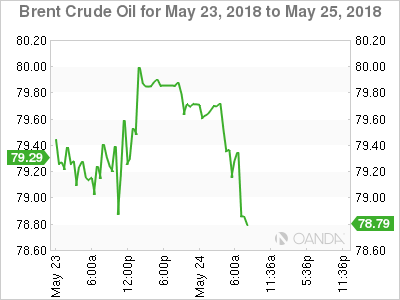

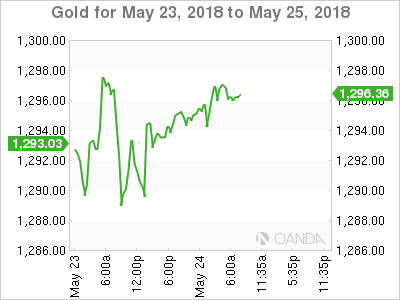

COMMODITIES: Both WTI and Brent crude oil were down by 0.70% and 0.91% respectively on expectations that OPEC members will step up production on supply worries from Venezuela and Iran. West Texas Intermediate crude dived to $71.34, while Brent dropped to $79.07. In precious metals, dollar-denominated gold rose nearly 0.26%, last trading near $1,296.3 per ounce, with the move likely being driven by the tumble in the greenback.

Day ahead: ECB meeting accounts next in focus

After the FOMC meeting minutes emphasized on Wednesday that inflation above 2.0% will not necessarily imply faster rate hikes, ECB meeting accounts will come next under the spotlight on Thursday at 1130 GMT. Recalling that ECB policymakers decided to leave monetary policy unchanged at their last policy meeting on April, acknowledging the slowdown in the EU’s economic performance, investors will be closely watching for clues on how the central bank plans to react to this weakness. Any remarks stating that the softness in data is temporary – as the ECB Chief Mario Draghi recently characterized – and/or the quantitative easing program is set to be phased out by the end of this year, could push the euro higher. However, if the accounts express concerns about the Eurozone’s economic outlook, pointing that the weakness could have stretched into the second quarter, the common currency could face a further sell-off. This could also increase speculation the QE program might extend beyond 2018.

Meanwhile, political developments in Italy are expected to continue to limit gains in the euro. Yesterday, the Italian President, Sergio Mattarella, approved the law professor Giuseppe Conte as the next Prime Minister of the new coalition government as the two Eurosceptic populist parties had proposed. Risks, though, remain on the political agenda and whether the new government will push forward potential fiscal reforms that could breach the EU’s spending rules program.

In the US, the economic calendar features initial jobless claims (1230 GMT) and figures on existing home sales (1400 GMT). Updates on the trade front, though, are likely to attract a greater attention as latest headlines have tempered hopes of progress in US-China trade relations as well as the optimism of a smooth US-North Korea summit on June 12. Particularly, risk-off sentiment strengthened even further after the US President, Donald Trump, admitted yesterday that talks with China need a different structure, twitting “Our trade deal with China is moving along nicely, but in the end we will probably have to use a different structure in that this will be too hard to get done and to verify results after completion”. Moreover, US trade relations with the EU remain in limbo as well, with Washington warning Brussels that exemption from the steel and aluminum import tariffs granted to the EU would not be extended. Trump’s order to probe the US automobile industry yesterday raised fears of new import tariffs. Note that the US is one of the biggest destinations for EU car exports.

In terms of public appearances, at 1235 GMT, comments by Atlanta Fed President Raphael Bostic and Dallas Fed President Robert Kaplan will be in focus. A few minutes later, at 1245 GMT, the Canadian Prime Minister, Justin Trudeau will be speaking on the role of the G7 and the future of the North American Free Trade Agreement, while at 1910 GMT the BoE Governor, Mark Carney will be appearing before the London’s Society of Professional Economists.

In other news, China, the UK, France, Germany, Russia, and Iran are set to meet on Friday to discuss the Iranian nuclear deal.

Forex Analysis: GBPUSD And GBPAUD

Retail sales finally provided some encouraging news for the British economy. The Office for National Statistics (ONS) reported that retail sales grew 1.4% on an annualised basis in April, beating market expectations for a reading of 0.1%. The monthly growth read at 1.6%, more than double the expectation of 0.8%. This follows CPI reported yesterday which was below expectations at 2.4%. Strong retail sales tend to correlate with robust economic activity so this may be seen as an early indication that the U.K. economy is about to leave behind a recent soft patch. The ONS will release GDP data tomorrow which will help set expectations for a possible August rate hike by the Bank of England.

GBPUSD

On the daily chart, GBPUSD is attempting to regain the 1.34 level and a break could see the pair make further gains with resistance at 1.3460 and then the 23.6% retracement level at 1.3550. A sustained recovery will run into a confluence of trend line, Fibonacci and horizontal resistance at 1.3710. However, a drop though support at 1.3315 will see the pair resume the decline towards the double top target at 1.3050 with support at 1.3120.

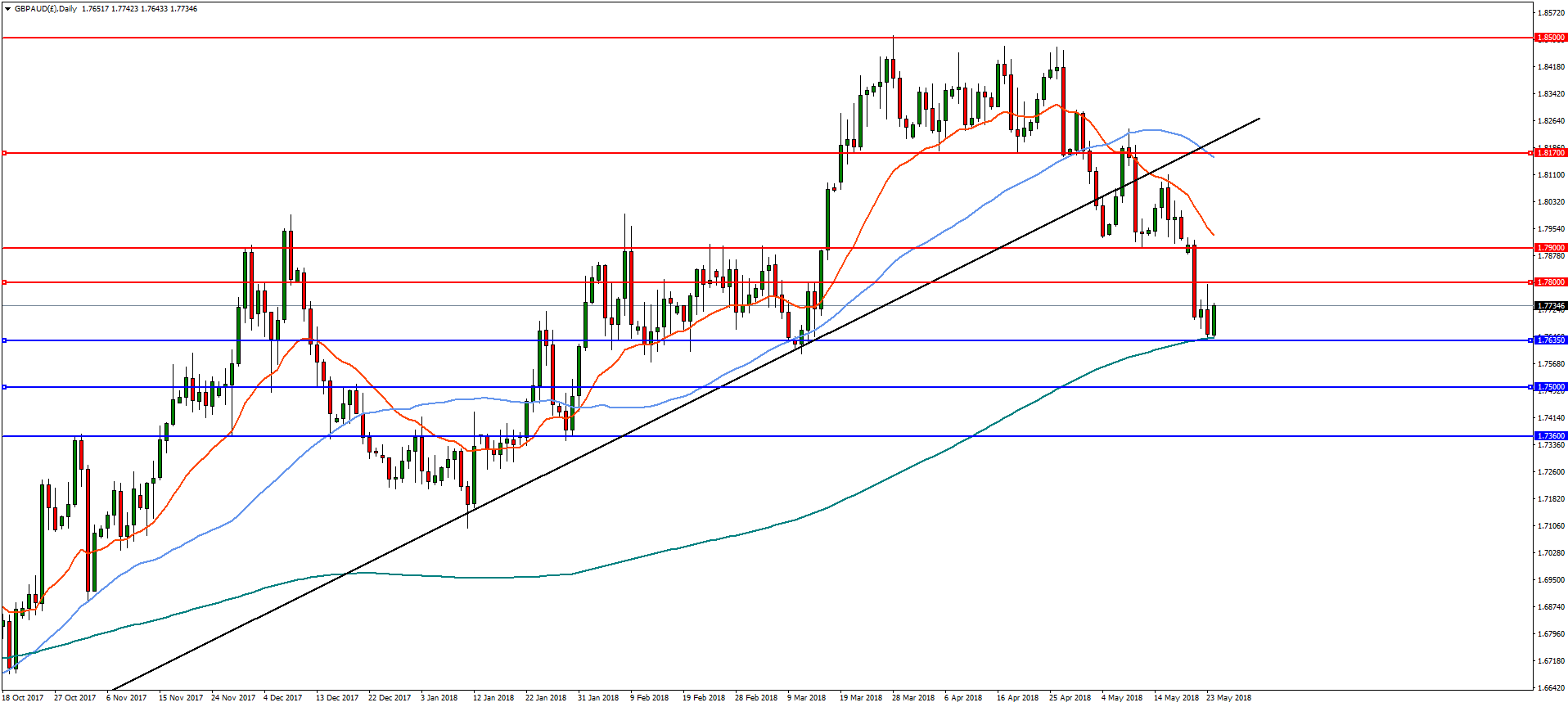

GBPAUD

On the daily chart, GBPAUD is finding support on the 200MA and 38.2% retracement of the lows from August at 1.7635. If this level breaks, the pair will resume the downside with supports at 1.7500 and then the 50% retracement at 1.7360. On the flip-side, a reversal above 1.7800 will open the way for gains towards resistance at 1.7900.

Euro Edges Higher After Fed Minutes

EUR/USD has rebounded in the Thursday session and has posted gains. Currently, the pair is trading at 1.1719, up 0.19% on the day. On the release front, Germany Final GDP dropped to 0.3%, matching the estimate. GfK Consumer Climate ticked lower to 10.7, just shy of the forecast of 10.8 points. Next up is the ECB will publish the minutes of its April policy meeting. In the US, unemployment claims is expected to tick lower to 220 thousand, while Existing Home Sales is forecast to drop to 5.56 million. On Friday, Germany releases Ifo Business Climate. The US will publish durable goods orders as well as consumer confidence.

The Federal Reserve minutes from the May meeting were somewhat hawkish in tone, but the dollar has responded with losses on Thursday. In the rate statement, some Fed policymakers said they favored removing the phrase that “the stance of monetary policy remains accommodative”. Not surprisingly, the minutes didn't shed light on the Fed's plans, saying that another rate hike would occur “soon”, on the assumption that the US economy continues to perform as expected. Still, a quarter-point rate hike in August is virtually a given, with the CME Group setting the odds of a hike at 95 percent. This would mark a second hike in 2018. After that? The Fed projection remains at three rates hikes in 2018, but some analysts are predicting four increases this year.

Earlier this week, there seemed to be some positive momentum regarding the US-China trade talks. However, President Trump voiced skepticism over progress in the negotiations, saying he was 'not really' satisfied with the results. Trump's comments have confused the markets, as Treasury Secretary Steven Mnuchin declared on the weekend that the trade spat was 'on hold'. The remarks spooked Asian and European stock markets on Wednesday. Investor risk appetite has also waned as there is uncertainty whether North Korean leader Kim Jong-un will meet with President Trump next month. On Tuesday, Trump acknowledged that there was a 'substantial' chance that the summit planned with Kim in Singapore on June 12 would not take place.

PMI reports disappointed on Wednesday and the euro responded with losses, as the currency dipped below the 1.17 line for the first time since mid-November. Investors are particularly concerned that both German and eurozone manufacturing PMIs dropped for a fifth straight month. German Manufacturing PMI posted its weakest gain in 16 months, while the eurozone indicator posted its worst reading in 18 months. These numbers, while certainly disappointing, should not cause any alarm, as the PMIs continue to indicate expansion in the services and manufacturing sectors. Still, the fact that growth was softer than expected could give ECB policymakers reason to re-evaluate the planned wind-up of its stimulus program in September.

(ECB) Account of the Monetary Policy Meeting 25-26 April

1. Review of financial, economic and monetary developments and policy options

Financial market developments

Mr Cœuré reviewed the latest financial market developments since the Governing Council's monetary policy meeting on 7-8 March 2018.

With regard to recent bond market developments, a gradual decline in the ten-year German government bond yield, which started in mid-February, had pushed yields back to levels not far from those observed for most of 2017. In the week leading up to the current meeting there had been a partial reversal of this downward trend. However, yields still remained well below the levels that had been observed earlier in 2018. By contrast, the ten-year US Treasury bond yield had resisted broad downward pressure and was approaching levels around 3% for the first time in more than four years. As a result, the yield spread between ten-year German Bunds and US Treasuries was at its widest since the late 1980s.

Changes in both components of long-term yields, the term premium and average expected short-term rates, contributed to these developments. A model-based breakdown suggested that the decline in long-term rates up until the week before the current meeting could be attributed to a drop in the term premium on both sides of the Atlantic. However, while the expectations component of German yields had remained fairly stable, there had been a continued rise in the expected path of future short-term rates in the United States. This helped to offset the initial drop in the term premium in the United States and suggested that investors maintained a favourable view about the prospects for the US economy.

As regards the causes for the decline in the term premium both in the United States and in the euro area, which had only recently come to a halt, two broad factors could be distinguished. The first related to incoming data that had been weaker than expected, in particular in the euro area. The second likely reflected global concerns about the current geopolitical environment.

The increase in global uncertainty, as well as the recent weaker than expected economic data, had also contributed to expectations of a later first rate hike in the euro area. According to the EONIA forward curve, a 10-basis point increase was currently priced in for around June 2019. This was consistent with the evidence from market surveys on euro area monetary policy expectations, which suggested a growing conviction among market participants that a rate rise would take place in the second quarter of 2019.

Turning to developments in stock markets, equities had, on the whole, benefited from the shifts in monetary policy expectations and the fall in long-term yields. The EURO STOXX 50 index had gone up by around 3% since the Governing Council's March monetary policy meeting. The picture differed somewhat in the United States, where the Standard & Poor's 500 index had lost around 2% over the same period, and in emerging markets, where stock markets had also declined.

In foreign exchange markets, volatility remained close to record low levels. Some market participants saw technical factors as having contributed to the broad stabilisation of the US dollar, in particular the cost of hedging. Mr Cœuré noted that the stability of exchange rates also suggested that investors did not appear to have materially changed their views on the euro area or US economic outlook.

The global environment and economic and monetary developments in the euro area

Mr Praet reviewed the global environment and recent economic and monetary developments in the euro area.

Regarding the external environment, global economic activity remained sustained, although recent indicators had pointed to some softening in momentum in the last couple of months. In March, the global composite output Purchasing Managers' Index had decreased, but it remained close to its long-term average. By contrast, consumer and business confidence indicators had held up well in February. Global financial conditions had remained supportive, sustained by accommodative monetary policies. Global trade indicators had been mixed, overall signalling some deceleration in the first quarter of this year.

Inflation dynamics had continued to be modest and underlying price pressures remained subdued. Annual consumer price inflation in the OECD countries had remained stable in February, while inflation excluding food and energy had edged up marginally. Since the Governing Council's March monetary policy meeting, Brent oil prices had risen sharply and stood at USD 73.5 on 24 April 2018, their highest level since the end of November 2014. Over the same period, the euro had remained broadly stable against the US dollar and also in nominal effective terms.

Turning to the euro area economy, euro area GDP growth had remained robust in the fourth quarter of 2017. Eurostat's third estimate for the quarter put quarterly growth at 0.7%, implying that the euro area had grown for almost five consecutive years. However, recent incoming information had generally surprised to the downside and pointed to some moderation, following several quarters of higher than expected growth. Surveys had shown a broad-based decline in sentiment in the first quarter of 2018 across most sectors and countries. At the same time, sentiment indicators were still at high levels and well above their historical averages.

Overall, although incoming survey data suggested slower growth in the short term, the data remained consistent with a solid and broad-based expansion across sectors and countries. The moderation in part reflected a pull-back from the high pace of growth observed at the end of 2017, while temporary factors and supply constraints in certain sectors in some countries might also have played a role. Concerns about trade protectionism could also have dampened business sentiment and expectations. The underlying strength in growth continued to be supported by favourable financing conditions, a robust labour market and steady income and profit growth.

Forecasts by public and private institutions for euro area real GDP growth since the early March monetary policy meeting were broadly in line with the March 2018 ECB staff macroeconomic projections.

Euro area annual HICP inflation had stood at 1.3% in March 2018, up from 1.1% in February. This increase reflected mainly higher food inflation, which had continued to be driven by base effects. HICP inflation excluding food and energy had stood at 1.0% in March, unchanged from February and January but slightly up from the 0.9% recorded in December 2017. Measures of underlying inflation remained subdued and had yet to show convincing signs of a sustained upward trend. Meanwhile, price pressures along the pricing chain had continued to be subdued, with no clear evidence as yet of the euro's appreciation having had an impact on later stages of the chain. Recent developments in wage growth were signalling a moderate upward trend.

The results of the ECB Survey of Professional Forecasters (SPF) for the second quarter of 2018 had shown slight downward revisions for HICP inflation expectations in 2019 and 2020. At the same time, average longer-term inflation expectations had remained broadly unchanged, at 1.9%. Expectations for inflation excluding food and energy were unchanged over the whole horizon. Similarly, market-based inflation expectations stood broadly unchanged.

Compared with forecasts by other public and private institutions, which had become available since the Governing Council's early March meeting, the inflation projection in the March ECB staff projections was on the low side for both 2018 and 2019, but well within the range for 2020.

Financial conditions continued to be accommodative despite geopolitical uncertainties. Since the Governing Council's March monetary policy meeting, the EONIA forward curve had flattened. Long-term rates were somewhat lower than in March, notwithstanding a very recent increase, while inflation expectations were broadly unchanged. Equities were still supported by solid earnings expectations. The overall cost of financing for euro area firms had declined marginally since the March monetary policy meeting.

The annual growth rate of the broad monetary aggregate M3 had moderated in February 2018, to 4.2%, but remained close to the narrow range of 4.5-5.5% observed since mid-2015. The annual growth rate of loans to the private sector had overall remained on a path of moderate expansion. Credit developments continued to be supported by low bank lending rates for non-financial corporations (NFCs) and households and a favourable economic outlook. According to the euro area bank lending survey for the first quarter of 2018, credit standards had eased considerably for loans to enterprises and loans for house purchase. At the same time, loan demand had continued to increase across all categories.

Monetary policy considerations and policy options

Summing up, Mr Praet recalled that financial conditions had remained broadly stable at accommodative levels amid increased uncertainties about the prospects for international trade relations, and that borrowing conditions remained very favourable.

Incoming information since the Governing Council's March monetary policy meeting had pointed to some moderation in the pace of economic growth, which, in part, reflected a pull-back from the high growth rates observed at the end of 2017. Temporary factors might also have been at work. It was thus important to monitor to what extent these developments also reflected a more prolonged softening in demand.

Overall, growth could still be considered to remain solid and broad-based. Risks to growth continued to be broadly balanced, but those related to global factors, including the threat of increased protectionism, had become more prominent.

Measures of underlying inflation had moved sideways since the March meeting and had yet to show convincing signs of a sustained upward trend. At the same time, wages continued to edge higher and were expected to lend support to price pressures.

All in all, the underlying strength of the euro area economy continued to support confidence that inflation would converge to the Governing Council's inflation aim over the medium term. However, inflation convergence would likely proceed only gradually, remaining contingent on a highly accommodative monetary policy stance.

On the basis of this assessment, Mr Praet proposed, at this stage, to keep monetary policy unchanged and to reconfirm all elements of the ECB's forward guidance, including the sequencing.

Regarding communication, it was deemed important to highlight that, despite some moderation in the pace of growth, economic indicators had remained consistent with a solid and broad-based expansion in the euro area. Moreover, it needed to be emphasised that the risks surrounding the euro area growth outlook remained broadly balanced, but those related to global factors, including the threat of increased protectionism, had become more prominent. Furthermore, the Governing Council could stress that the underlying strength of the euro area economy continued to support confidence that inflation would converge to its aim over the medium term, while reiterating the importance of prudence, patience and persistence in its monetary policy for inflation pressures to build up.

2. Governing Council's discussion and monetary policy decisions

Economic and monetary analyses

With regard to the economic analysis, members agreed with the assessment of the outlook and risks for economic activity in the euro area provided by Mr Praet in his introduction. Recent data and survey results pointed to some moderation in the pace of growth since the start of the year, but were so far considered to remain consistent with a solid and broad-based expansion, supported by very favourable financing conditions. It was underlined that this moderation in growth had come after a period of very strong growth and when incoming data had surprised on the upside. This moderation might therefore reflect in part an expected normalisation from last year's exceptionally high growth rates, while unexpected temporary factors were also seen to have played a role. Hence, the underlying growth momentum was on the whole assessed to remain intact. At the same time, it was widely felt that uncertainty surrounding the outlook had increased and caution was seen as warranted in interpreting recent developments, also because the moderation in growth appeared to be broad-based across countries and sectors. A more pronounced weakening of demand, notably related to external factors, could therefore not be ruled out. Overall, the risks surrounding the outlook for economic growth were assessed to have remained broadly balanced, with downside risks related to the threat of trade protectionism having become more prominent.

Regarding the outlook for the external environment, global economic activity was seen as remaining robust, although recent indicators suggested that momentum had weakened somewhat in the last few months. The picture of a sustained global economic expansion was supported by the latest IMF projections for world real GDP growth. In this context, it was remarked that the impact of the fiscal stimulus in the United States remained a major factor in the outlook for global activity. Overall, the balance of risks to the outlook for global activity, including a more prominent risk of increasing trade tensions and the uncertain implications of the United Kingdom's withdrawal from the European Union, was considered to remain tilted to the downside.

Members agreed on the importance of external risks to the economic outlook for the euro area. In particular, concern was expressed that trade conflicts might not only have an adverse impact on activity for the countries involved via reduced trade, but could exert broader effects as a consequence of increased uncertainty and diminished confidence. Some of this uncertainty was related to upcoming decisions on trade policies. It was also remarked that turbulent trade relations had the potential to give rise to disorderly movements in exchange rates and to heightened volatility in financial markets.

The impact of trade protectionism and of possible retaliatory measures on global and euro area economic growth was considered as ranging from limited to having more substantial effects, depending on the scale of the imposed tariffs and on the diversion of trade flows and relocation of production in response to such measures. Reference was also made to evidence suggesting quantitatively large effects from the uncertainty associated with protracted tensions in trade relations. Some euro area economies might have been seeing such effects in recent months, for example in weaker export orders.

Turning to euro area activity, members discussed in more detail the moderation in economic growth at the start of the year, which was suggested by the latest hard data and survey-based indicators. It was noted that euro area real GDP had previously increased at a strong pace – by 0.7% quarter on quarter in both the third and fourth quarters of 2017, well above current estimates of potential output growth.

Members concurred that the underlying growth momentum in the euro area and its largest economies remained broadly intact, and expressed confidence in the continuation of the expansion at a solid pace. The observation was made that, while there had been a decline in hard data and survey-based indicators since the Governing Council's March monetary policy meeting, which had been rather broad-based both across euro area countries and across economic sectors, the indicators remained at elevated levels and were still clearly above their long-run historical averages.

In exchanging views about the interpretation of incoming information, members shared information on recent developments in the respective national economies and sought to provide an assessment of the factors behind the signs of weaker activity. A number of reasons of a temporary nature could in part explain a stronger than anticipated moderation. For many economies, reference was made to the possible impact of weather conditions earlier in the year, which implied a loss in value added in some sectors of the economy, such as construction or retail, but could equally imply gains in other sectors, such as those related to energy. Other temporary factors related to strikes affecting certain sectors of the economy and the unusually severe wave of seasonal influenza in some countries.

For the euro area as a whole, it was underlined that the signs of a moderation in economic growth at the start of the year did not change the picture regarding the underlying pace of expansion. In some parts of the euro area and in some sectors, the moderation in growth could be attributed to capacity constraints becoming increasingly binding. This was seen as consistent with the survey evidence on increasing labour supply shortages, suppliers' delivery times and order backlogs provided by Mr Praet in his introduction. It was argued that, in the absence of supply constraints, there would be an elastic response of output to changes in demand but, as capacity constraints were reached, growth in activity could be expected to slow down, with price pressures picking up instead. However, it was also argued that there were signs of softening demand, which warranted monitoring.

In this context, it was recalled that, while the direction of change in the measures of slack was clear, the measurement of the level of the output gap was surrounded by considerable uncertainty, as had been discussed by the Governing Council at its March monetary policy meeting.

Looking ahead, members agreed that the underlying strength of the economic expansion remained broadly intact. At the same time, uncertainty surrounding the outlook had clearly increased and data releases ahead of the June monetary policy meeting would need to be carefully scrutinised to better understand the sources of the recent moderation in growth. In this regard, it was also deemed important to gain a deeper understanding of the reasons behind the high degree of synchronicity in the downturn in indicators, which might point to a broader weakening of demand. The need to closely monitor and assess the incoming data was emphasised. More generally, it was necessary to distinguish between temporary and potentially more lasting influences and to determine the extent to which they reflected a softening in demand as opposed to the emergence of supply constraints. This latter distinction was seen as especially relevant, as supply constraints had opposite implications for price pressures.

Overall, the risks to the euro area growth outlook were assessed to have remained broadly balanced. At the same time, the downside risks related to global factors had become more prominent. It was also emphasised that there was a risk of a more expansionary and pro-cyclical fiscal policy.

With regard to price developments, there was broad agreement with the assessment presented by Mr Praet in his introduction. Euro area annual HICP inflation had increased to 1.3% in March 2018, from 1.1% in January. This increase mainly reflected higher food price inflation. On the basis of current futures prices for oil, annual rates of headline inflation were likely to hover around 1.5% for the remainder of the year. It was noted that higher energy prices were currently supporting the outlook for headline inflation, while the latest data for non-energy industrial goods price inflation had surprised on the downside, which was argued to possibly also reflect a delayed pass-through from past appreciation of the euro. On balance, the picture for headline inflation had not changed materially. At the same time, measures of underlying inflation in the euro area remained subdued and had moved mostly sideways since the March monetary policy meeting.

Members observed signs in a number of euro area countries that wage dynamics continued to pick up gradually and thus would, over time, contribute to the expected rise in underlying inflation. It was noted that, in some cases, this might not only reflect a reduction in labour market slack and higher productivity, but also a stronger role of the inflation expectations component in wage settlements. At the same time, evidence for some euro area economies suggested that there was stronger dynamism in the labour costs of the self-employed, as reflected in the prices that they charged for their services. Reference was also made to emerging signs of labour shortages and capacity constraints in a number of euro area countries and sectors of the economy, which could be expected to lead to increased wage and price dynamism over time. At the same time, it was cautioned that the degree of pass-through of wage pressures to prices remained uncertain and the ability of firms to absorb higher costs via lower mark-ups, as well as the behaviour of margins more generally, deserved further analysis.

As regards recent developments in longer-term inflation expectations, members noted that both market-based and survey-based measures had remained broadly stable. Expectations of inflation five years ahead in the SPF for the second quarter of 2018 were unchanged at 1.9%. Market-based inflation expectations, as measured by the five-year forward inflation-linked swap rate five years ahead, stood at 1.70%, the same level as that observed at the time of the March monetary policy meeting.

With regard to the monetary analysis, members concurred with the assessment provided by Mr Praet in his introduction. Broad money (M3) had continued to expand at a robust pace, although it had fallen slightly below the range observed since mid-2015. The slight moderation in the growth rate of M3 was seen to reflect mainly a decline in the contribution of credit to general government amid the reduction in monthly purchase volumes by the Eurosystem under the asset purchase programme (APP).

The gradual recovery in the growth of MFI loans to the private sector, underway since the start of 2014, was proceeding. Growth in loans to NFCs, in particular, continued to be supported by the targeted longer-term refinancing operations, with the reference period for the second series having ended in January. Reference was also made to the bank lending survey for the first quarter of 2018, which indicated increasing loan demand across all loan categories and a further easing of credit standards for loans to enterprises and loans for house purchase. Against this background, it was remarked that the risk-taking channel had so far supported the effectiveness of monetary policy by encouraging bank lending to the economy and it was reiterated that, from a prudential perspective, the impact of very easy credit conditions and low bank lending rates needed to be monitored closely. It was noted that potential financial stability risks should be addressed by macroprudential measures, as had already been proposed or implemented in some jurisdictions.

Monetary policy stance and policy considerations

With regard to the monetary policy stance, members widely shared the assessment provided by Mr Praet in his introduction. The recent incoming information pointed to some moderation in activity but so far remained consistent with a solid and broad-based expansion of the euro area economy. The underlying strength of the euro area economy continued to support the Governing Council's confidence that inflation would gradually converge to its inflation aim of below, but close to, 2% over the medium term. At the same time, measures of underlying inflation remained subdued and had yet to show convincing signs of a sustained upward trend. For underlying inflation pressures to continue to build up and support the path of headline inflation over the medium term, patience, persistence and prudence with regard to monetary policy remained warranted.

Members broadly agreed that financial conditions continued to be very accommodative overall, in spite of increased uncertainty and volatility in some markets. A remark was made that survey and analysts' expectations regarding APP net purchases were unchanged, with market participants continuing to anticipate net purchases concluding towards the end of 2018. Overall, the pass-through of the ECB's monetary policy measures was continuing to provide significant support to borrowing conditions for firms and households.

With regard to the progress towards a sustained adjustment in the path of inflation, the incoming information had on the whole changed little compared with the assessment made at the previous meeting. Headline inflation was up slightly from its recent trough but remained some distance from the Governing Council's inflation aim. Price pressures were still weak and measures of underlying inflation had moved sideways.

Despite the observed moderation in activity, confidence in the underlying strength of the euro area economy and the eventual convergence of inflation to the Governing Council's inflation aim remained unchanged. While measures of underlying inflation continued to be subdued, some comfort was drawn from encouraging signs of a strengthening in nominal wage growth and the continued anchoring of long-term inflation expectations at levels consistent with the Governing Council's aim. In this context, a remark was made that the Phillips curve relationship may be non-linear, and this could support a swifter rebound in inflation when capacity constraints became binding. At the same time, it was widely cautioned that the uncertainty around the outlook had increased since the March monetary policy meeting. In particular, risks related to global factors, including the threat of increased protectionism, had become more prominent and warranted monitoring with regard to their implications for the medium-term outlook for growth and prices. The June 2018 Eurosystem staff projections would provide the next occasion for a more comprehensive assessment of progress with inflation.

Members broadly agreed that an ample degree of monetary policy accommodation remained necessary to accompany the economic expansion and secure the gradual convergence of inflation to levels below, but close to, 2%. The remaining uncertainties and the still muted underlying inflation pressures continued to justify caution and underlined the need to maintain patience, persistence and prudence with regard to monetary policy.

Overall, while a view was expressed that the Governing Council's criteria for a sustained adjustment in the path of inflation could be considered as close to being satisfied over a medium-term horizon, there was broad agreement that the evidence remained insufficient at the current stage.

Against this background, members widely agreed that a steady hand with regard to monetary policy was warranted at the current stage, in line with the elements proposed by Mr Praet in his introduction. This called for maintaining the current monetary policy stance in relation to the full set of policy instruments, which involved reconfirming the October 2017 monetary policy decisions on net asset purchases and reinvestments, the ECB key interest rates and the Governing Council's forward guidance on those measures, including the sequencing of policy instruments.

Looking ahead, there was consensus that the net asset purchases would continue to be guided by the Governing Council's assessment of the progress made towards a sustained adjustment in the path of inflation according to the three criteria of convergence, confidence and resilience.

With regard to communication, steadiness was seen as important and members widely agreed with the elements for communication put forward by Mr Praet in his introduction. This entailed highlighting the need for prudence, patience and persistence in monetary policy for inflation pressures to build up and to deliver on the Governing Council's commitment to secure a sustained return of inflation rates towards levels below, but close to, 2%. Despite some moderation in the pace of growth, economic indicators so far remained consistent with a solid and broad-based expansion in the euro area. The underlying strength of the euro area economy continued to support the Governing Council's confidence that inflation would converge to its aim over the medium term. At the same time, while risks surrounding the euro area growth outlook remained broadly balanced, it was acknowledged that risks related to global factors, including the threat of increased protectionism, had become more prominent and warranted monitoring with regard to their implications for the medium-term outlook for growth and prices.

It was reiterated that, beyond the horizon of the net asset purchases, the monetary policy support still necessary for inflation to converge to the inflation aim would be provided by the stock of acquired assets, by reinvestments continuing for an extended period of time, and by policy rates remaining at their present levels well past the end of the net asset purchases. Finally, as on previous occasions, the continuing case for substantial reform efforts by euro area governments was made with a view to reinforcing the longer-term growth potential of the euro area economy, increasing its resilience and reducing vulnerabilities. It was argued that structural reforms in euro area countries needed to be substantially stepped up, including with regard to reforms of education and training with a view to reducing skill mismatches in labour markets and enhancing productivity. There was broad agreement among members that it was warranted to reinforce calls for existing fiscal rules to be respected and for fiscal buffers to be rebuilt, in particular with regard to those Member States with high government debt. In addition, calls for a swift and substantive completion of the banking union and of the capital markets union were reiterated.

Monetary policy decisions and communication

Taking into account the foregoing discussion among the members, on a proposal from the President, the Governing Council decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility would remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expected the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

Regarding non-standard monetary policy measures, the Governing Council confirmed that the net asset purchases, at the current monthly pace of €30 billion, were intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council saw a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem would reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This would contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

The members of the Governing Council subsequently finalised the draft introductory statement, which the President and the Vice-President would, as usual, deliver at the press conference following the end of the current Governing Council meeting.

Introductory statement

http://www.ecb.europa.eu/press/pressconf/2018/html/ecb.is180426.en.html

Press release

http://www.ecb.europa.eu/press/pr/date/2018/html/ecb.mp180426.en.html

Meeting of the ECB's Governing Council, 25-26 April 2018

Members

Mr Draghi, President

Mr Constâncio, Vice-President

Mr Cœuré

Mr Costa

Mr Knot

Mr Lane

Ms Lautenschläger

Mr Liikanen*

Mr Linde

Mr Makúch*

Mr Mersch

Mr Nowotny

Mr Praet

Mr Reinesch

Mr Smets*

Mr Stournaras

Mr Vasiliauskas

Mr Vella

Mr Villeroy de Galhau

Mr Visco

Mr Weidmann*

* Members not holding a voting right in April 2018 under Article 10.2 of the ESCB Statute.

Other attendees

Mr Teixeira, Secretary, Director General Secretariat

Mr Smets, Secretary for monetary policy, Director General Economics

Mr Winkler, Deputy Secretary for monetary policy, Senior Adviser, DG Economics

Accompanying persons

Mr Alves

Mr Bradeško

Ms Buch

Mr Demarco

Mr Dolenc, Alternate to Mr Jazbec

Ms Donnery

Mr Gaiotti

Ms Goulard

Mr Hernández de Cos

Mr Kaasik, Alternate to Mr Hansson

Mr Kuodis

Mr Ódor

Mr Pattipeilohy

Mr Randveer

Ms Razmusa

Ms Ritzberger-Grünwald

Mr Rutkaste

Mr Schoder

Mr Stavrou, Alternate to Ms Georghadji

Mr Tavlas

Mr Välimäki

Mr Wunsch

Other ECB staff

Ms Graeff, Director General Communications

Mr Straub, Counsellor to the President

Mr Bindseil, Director General Market Operations

Mr Sousa, Deputy Director General Economic Developments, DG Economics

Mr Rostagno, Director General Monetary Policy, DG Economics

Release of the next monetary policy account foreseen on Thursday, 12 July 2018.

Trade War Talks Are Back And The Dollar Is Falling

Thursday May 24: Five things the markets are talking about

Global stock markets remain under pressure as investors shun risk assets for relative safe havens.

Rising Italian bond yields, fading prospects for the North Korea summit, disintegrating EM currencies, and deteriorating E.U economic data continue to wreak havoc amongst the various asset classes.

Note: Italian President Mattarella has given PM mandate to Giuseppe Conte to try and form a government.

The yield on U.S 10-year Treasuries have stabilized around +3%, while the euro’s ‘single unit’ has found some traction after yesterday’s release of the FOMC minutes, which indicated some policymakers saw that the Fed funds rate could reach its neutral level before too long. However, U.S officials also saw trade and fiscal policies as ‘sources of uncertainty.’

Turkey’s lira ($4.6671) has resumed its slump as the market continues to weigh yesterday’s intra-meeting rate hike was not enough to stem losses, while elsewhere, safe-haven assets including gold and Japan’s yen continue to climb, as crude oil prices slips.

1. Stocks mixed results

In Japan, the Nikkei fell to more than two-week lows overnight as automakers slumped after the Trump administration launched a national security investigation into car and truck imports that could lead to new U.S tariffs. The Nikkei ended -1.1% lower, while the broader Topix fell -1.2%.

Note: The Nikkei volatility index soared to 18.29, the highest level since mid-April.

Down-under, Aussie stocks snapped a five-day losing streak on Thursday, aided by gains for gambling equipment maker Aristocrat Leisure that helped outweigh a continued fall for financial stocks. The S&P/ASX 200 was up +0.1%. In S. Korea, the Kospi slid -0.24% on automakers.

In Hong Kong, stocks ended higher, helped by services and energy companies, though gains were capped amid renewed concerns over Sino-U.S trade tensions. At close of trade, the Hang Seng index rose +0.3%, while the China Enterprises Index gained +0.5%.

In China, stocks extended losses, as caution prevailed amid renewed concerns over China-U.S trade tensions. The blue-chip CSI300 index closed down -0.7%, while the Shanghai Composite Index ended -0.5% lower.

In Europe, regional bourses have opened a tad higher, with one exception thus far, the FTSE 100. It’s no surprise that automotive stocks again are in focus, this time negative following President Trump considering tariffs. An appointment of PM in Italy is lending some support in stocks.

U.S stocks are set to open in the ‘black’ (+0.1%).

Indices: Stoxx50 +0.4% at 3,557, FTSE -0.1% at 7,784, DAX +0.2% at 12,996, CAC-40 +0.5% at 5,591; IBEX-35 +0.6% at 10,082, FTSE MIB +0.9% at 23.14, SMI +0.4% at 8,833, S&P 500 Futures +0.1%

2. Oil under pressure as chances rise of OPEC raising output, gold higher

Oil trades under pressure, driven lower by the prospect of the first increase in OPEC output in two-years in the face of concern over supply from both Venezuela and Iran, while a surprise rise in U.S crude inventories raised doubt over seasonal demand.

Brent futures are down -59c at +$79.21 a barrel, while U.S crude futures have eased -41c to +$71.43 a barrel.

Currently, the market chatter about a possible OPEC supply increases after the June meeting has put a brake on oil prices for the time being. The +$80 handle remains a massive psychological hurdle to overcome.

Note: OPEC may decide next month to increase oil output to make up for reduced supply from Iran and Venezuela and in response to concerns from Washington over a rally in oil prices.

Yesterday’s Energy Information Administration reported U.S commercial crude oil inventories (ex-those in the SPR) increased by +5.8m barrels from the previous week. At +438.1m barrels, U.S crude oil inventories are in the lower half of the average range for this time of year.

Ahead of the U.S open, gold prices are holding gains, buoyed as the dollar extended losses after yesterday’s Fed minutes hinted at a ‘dovish’ approach to interest rate hikes. Spot gold has edged up +0.1% to +$1,293.93 per ounce, after gaining nearly +0.2% in the previous session. U.S gold futures for June delivery are up +0.3% at +$1,293.30 per ounce.

3. Sovereign yields under pressure

Italy continues to take center stage in the sovereign bond market as dealers focus shifts to the implementation of the coalition’s ambitious agenda and its potential ministers. Will the incoming government sully Italy’s relations with E.U?

Note: Italy’s government debt remains heavily dependent on support from the ECB’s bond purchases, and the country’s wider financial system is more closely linked to government debt markets than in much of Europe.

For German Bunds, the safety bid continues to gather pace as the Italian BTP sell-off spills over into the core market. Germany’s 10-year Bund yield has decreased -3 bps to +0.53%. The gap between Italy and Germany’s government bond yields has climbed to +192 bps, the highest in nearly a year – the spread has increased more quickly than at any time in the last five years.

Elsewhere, the yield on U.S 10-year notes has gained +1 bps to +3.00%, the biggest gain in a week. In Germany, the 10-year Bund yield has advanced +1 bps to +0.51%, while in the U.K, the 10-year Gilt yield has increased less than +1 bps to +1.44%.

4. Dollar remains dodgy on trade talks

Trade war talks are back and the dollar is under pressure. Reports that the U.S. commerce department has opened up “a section 232 investigation into the imports of cars to determine their effects on America’s national security” is ringing some alarm bells given what happened when the U.S. imposed steel and aluminum tariffs in March. Many view this proactive move as a pretty big escalation in the trade war narrative. EUR/USD is up +0.2% at €1.1732, USD/JPY is down by -0.5% at ¥109.60, while USD/CHF is down -0.2% at $0.9935.

With U.K retail sales rising by much more than expected last month (see below) has sent sterling higher. GBP/USD has rallied +0.6% to £1.3420, from £1.3384 before the data, while EUR/GBP falls to €0.8754, from €0.8769 beforehand.

Yesterday’s sizable emergency interest rate hike by Turkey’s central bank temporarily took some pressure off the lira in the near term and goes some way’s to improve confidence in the central bank’s ability to act. However, the pressure on the TRY is expected to remain high until the elections on 24 June. The lira has resumed its falls today after gaining sharply late Wednesday, with USD/TRY last up +2.6% at $4.6926.

Note: Fixed income dealers are pricing in another rate hike at the monetary policy meeting on 7 June, if not earlier, should the lira continue to remain under pressure.

5. U.K retail sales rebounds in April

Data this morning showed that U.K retail sales rebounded in April, recovering from a spell of bad weather in the previous month.

According to the Office for National Statistics, U.K retail sales climbed +1.6% in April, with all sectors apart from department stores picking up from subdued March levels. Gas sales also picked up after the poor March weather affected travel.

Note: The headline print beat market expectations of an on-the-month rise of +0.8%.

Today’s headline print marks a bright spot among Q2 data that has so far been mixed. CPI data released yesterday revealed the slowest growth in more than 12-months.

Note: The U.K economy is expected to lag behind its peers this year as uncertainty over the terms of its future relationship with the E.U weighs on activity and investment.